Abstract

Market segmentation severely restricts corporate investment efficiency, while the role of standardisation as a basic system for reshaping market rules has not been fully studied. Using data from A-share listed companies in Shanghai and Shenzhen from 2013 to 2024, this paper employs the multi-period DID method to examine the impact of the national standardisation comprehensive reform pilot policy on enterprise investment efficiency. It is found that the policy significantly enhances enterprise investment efficiency and reduces the deviation of actual investment from optimal investment, with the effect improving over time. Mechanism analysis reveals that the policy operates through two key paths: strengthening market competition and reducing transaction costs. Heterogeneity analysis reveals that the policy effect is more significant in regions with lower marketisation, larger government size, and lower social trust. This study provides new evidence for understanding the microeconomic consequences of standardisation regimes.

Keywords

Introduction

The efficiency of capital allocation lies at the heart of corporate strategic decision-making and financial management (Dong et al., 2020), with managers’ strategic investment choices directly determining a firm’s value creation, financial health, and capacity for sustainable growth (Y. Liu et al., 2015). The persistent flow of capital towards inefficient sectors erodes short-term profits and undermines long-term competitiveness (Grazzi et al., 2016), exacerbating operational risks and potentially triggering bankruptcy. If widespread, this phenomenon further hampers macroeconomic growth and intensifies employment pressures (Nguyen Trong & Nguyen, 2021). Consequently, investment efficiency serves as a pivotal metric for gauging a firm’s resource allocation capabilities (Fazzari et al., 1987). Within the context of global competition, enhancing investment efficiency has become both a core imperative and an intrinsic requirement for maintaining competitive advantage and achieving resilient, sustainable growth (Delios et al., 2021; Y. Liu et al., 2021). Existing literature identifies systematic enhancement pathways centred on intensified market competition and reduced transaction costs. At the market competition level, competitive pressures compel enterprises to divest inefficient projects and concentrate on core, high-return investments (Hay & Liu, 1997); while antitrust policies dismantle monopolies and local protectionism, channelling capital towards innovation and technological upgrading (Kong et al., 2022). Concurrently, competition strengthens corporate governance and disclosure quality, mitigating agency conflicts and curbing irrational investment (F. Chen et al., 2011), with tax incentives synergistically empowering innovation investment within competitive environments (Shiyuan et al., 2020). Regarding transaction costs, tax incentives alleviate financing constraints and fund efficient projects (Zhai et al., 2022); local government support through information provision, innovation subsidies, and loan facilitation reduces institutional interaction friction costs (Cull et al., 2017); while high-quality financial disclosure diminishes information asymmetry, providing reliable foundations for investment decisions (F. Chen et al., 2011).

Market segmentation, as a core barrier to optimal resource allocation, originates from natural geographical conditions, high transaction costs, and institutional barriers (Beane & Ennis, 1987), and produces systematic distortions in firms’ investment behaviour. On the one hand, regional barriers induce obstacles to cross-regional information flow, leading to overestimation of local market demand (B. Hou et al., 2023) and overinvestment and overcapacity (Bekaert & De Santis, 2021); on the other hand, rising cross-regional transaction costs inhibit firms’ willingness to invest, exacerbate underinvestment (Devos & Li, 2021), and discourage R&D and long-term capacity building (Cannon et al., 2020). The World Bank (2020) points out that market segmentation on a global scale is a key contributor to inefficient business investment. Moreover, inconsistencies in standards and regulations elevate firms’ compliance adaptation costs, heighten uncertainty in investment decisions, and dampen long-term investment propensity (Toh & Pyun, 2024). Local protectionism distorts factor allocation through tax incentives and subsidies, triggering redundant construction and homogeneous competition while impeding efficient factor mobility (C. Zhao et al., 2021); while local government debt mismatches and political interference in state-owned enterprise investments further exacerbate resource misallocation (S. Chen et al., 2011; Zhu et al., 2022). Administrative monopolies and sectoral monopolies erect market barriers and stifle competition; administrative monopolies influence debt financing costs, indirectly hindering effective investment (Cai & Ni, 2025; Zhai et al., 2022). Industry monopolies, lacking competition, are prone to investment inertia and capacity mismatches while raising barriers to entry for newcomers (Cali & Presidente, 2025; Pohlmann et al., 2016). Moreover, policy uncertainty reduces investment scale and deviates from optimal levels (Pastor & Veronesi, 2012), while financial mismatches in government subsidies lead to inefficient capital utilisation, thereby undermining investment efficiency (Tingli et al., 2020).

However, improving the efficiency of business investment is not an easy task. The phenomenon of market segmentation is deeply rooted in China’s economic system and constitutes a key institutional barrier, and this fragmentation not only stems from local protectionism but is also closely related to the inadequacy of the standardisation system. To address this challenge at its root, China launched a pilot comprehensive national standardisation reform in 2015 to reduce transaction costs through institutional restructuring. The national comprehensive standardisation reform pilot policy, by establishing a unified system of technical specifications and rules, focuses on resolving market fragmentation and standardisation fragmentation issues, thereby providing a more systematic institutional safeguard for enhancing investment efficiency. The reform focuses on a three-fold mechanism: first, integrating mandatory national standards to eliminate regional barriers triggered by local standards, consolidating mandatory national standards, and optimising recommended standards; fragmented regulations arising from local protectionism are dismantled (Han & Wu, 2024). This relieves enterprises from bearing additional compliance and adaptation costs associated with aligning to differing technical specifications and certification processes across regions (Toh & Pyun, 2024). Consequently, information search and transaction costs for cross-regional investment are reduced, redirecting capital away from regulatory compliance towards high-return core production and R&D projects. Secondly, by implementing a system for the self-declaration and public disclosure of enterprise standards alongside oversight mechanisms, standardisation reforms encourage market-driven competitive standards to break regional barriers (Yu et al., 2025), lowering market entry barriers for SMEs and facilitating the free flow of production factors (L. Chen et al., 2025). This intensifies competitive pressures, compelling enterprises to abandon inefficient investment practices reliant on policy protectionism. Instead, they optimise capital allocation and accelerate technological innovation to enhance core competitiveness (Hay & Liu, 1997); Thirdly, a unified standards system provides enterprises with clear and stable institutional expectations, preventing investment decision distortions caused by ambiguous policy interpretations and frequent standard adjustments (Pastor & Veronesi, 2012). Simultaneously, the industry knowledge base built upon group standards and the autonomous space for enterprise standards assist enterprises in accurately grasping market demands and technological trends, reducing overinvestment or underinvestment issues stemming from information asymmetry (Biddle et al., 2009); Fourthly, standardisation unification reduces negotiation and oversight costs between creditors and enterprises by clarifying supply chain cooperation rights and obligations and harmonising implicit rules in debt covenants (Cai & Ni, 2025). This effectively alleviates financing constraints (Zhai et al., 2022), ensuring efficient investment projects receive adequate funding support and generating multifaceted synergistic empowerment effects.

Academic research on the unified national market has developed a multidimensional, cross-level framework. Centred on four core themes—standardisation reform, unified market construction, market segmentation, and local protectionism—it explores these issues from both micro-enterprise and macroeconomic perspectives. Regarding standardisation reform, micro-level research focuses on corporate behaviour, confirming its influence on labour hiring decisions (Yu et al., 2025) and its interaction with product innovation and patent applications (Blind et al., 2022). Macro-level analysis emphasises its role as an institutional foundation for reducing transaction costs and facilitating factor mobility, necessitating the promotion of domestic and international standard interoperability (Blind et al., 2023). Concerning the construction of a unified national market, micro-level research centres on rule refinement, examining how fair competition reviews improve cross-regional capital flows (S. Li & Xu, 2024), administrative monopoly regulation impacts corporate resource allocation (Y. Zhao et al., 2024), and market segmentation affects entrepreneurial dynamism and competitiveness (L. Chen et al., 2025; S. Li et al., 2024; Luo, 2025). At the macro level, attention is directed towards market integration effects, such as how optimised transport infrastructure enhances the synergistic efficiency of economic environments (Y. Wang, 2022) and tax incentives mitigate market segmentation (J. Liu et al., 2024), thereby driving industrial transformation. Regarding market segmentation, the focus is on its negative impacts: at the micro level, it suppresses R&D investment by private enterprises and reduces their survival probability (B. Hou et al., 2023; Lyu et al., 2022); at the macro level, it hinders cross-regional factor mobility, exacerbates industrial homogeneity, and impedes carbon reduction and environmental efficiency (Kou & Xu, 2022; Qin et al., 2020). Regarding local protectionism as a core driver of market segmentation, its essence lies in administrative measures obstructing market integration (Qin et al., 2020); Micro-level distortions pervert corporate behaviour and stifle technological upgrading (Ji et al., 2024); macro-level disruptions undermine the foundations of market integration (D. Zhao et al., 2022), triggering international trade barriers and damaging supply chains and export trade (Handley et al., 2025; Pandey, 2025).

This paper takes A-share listed companies in Shanghai and Shenzhen from 2013 to 2024 as samples, focuses on the institutional change of the national comprehensive standardisation reform pilot, and systematically explores the impact of the standardisation reform on corporate investment efficiency and its mechanism. Firstly, the empirical model is constructed by multi-temporal double-difference method (DID) to analyse the impact of the pilot standardisation reform policy on enterprise investment efficiency; secondly, the reliability of the conclusion is ensured by dynamic effect test and seven robustness methods; then the mechanism is revealed from the dual paths of market competition and transaction cost, and finally, the heterogeneity analysis focuses on the moderating effects of the level of marketisation, the size of the government, and the trust of the society.

The contributions of the research in this paper are as follows. First, the study in this paper extends the research on the economic consequences of market integration. Previous studies have focused on the effects of market integration on entrepreneurial dynamism (L. Chen et al., 2025), firm competitiveness and innovation capacity (Luo, 2025), and firm leverage and vertical risk (S. Li et al., 2024), but have paid insufficient attention to the mechanisms of firm behaviour at the micro level, especially the efficiency of investment decision-making. Moreover, the unique value of unified institutional rules in market integration remains unexplored. This paper reveals for the first time that standardisation reform, as a core institutional arrangement for building a unified national market, enhances investment efficiency by harmonising technical specifications and certification systems while eliminating fragmented regulations. This fundamentally differs from traditional market integration approaches reliant on infrastructure improvements or policy liberalisation. The core distinction lies in the fact that the standardisation-driven unified market employs “rule unification” as its central lever. By consolidating mandatory national standards, optimising recommended standards, and fostering market-driven voluntary standards, it fundamentally resolves the fragmentation of standards caused by local protectionism (Han & Wu, 2024), thereby reducing compliance costs and information asymmetry for enterprises operating across regions (Toh & Pyun, 2024). Traditional market integration, however, relies more heavily on upgrading physical infrastructure such as transport and logistics (Y. Wang, 2022) or policy incentives like tax breaks (J. Liu et al., 2024), failing to address deep-seated institutional barriers at the level of regulatory frameworks. This study offers a novel perspective on how institutional integration drives the high-quality allocation of resources. Second, this paper incorporates standardisation into the framework of factors affecting enterprise investment efficiency. Not only does this supplement existing findings on the impact of formal institutional environments on micro-level firm decision-making, but it also clarifies the boundaries between standardisation and other influencing factors. Existing literature has examined the effects on corporate investment efficiency from both external environments and firm-level perspectives. Within external environments, the dual effects of market competition intensity (Boubaker et al., 2022; Tinaikar & Xu, 2023), the differential impacts of environmental and climate policies (M. Chen & Yan, 2025; Z. Zhang et al., 2025), and the enabling role of environmental innovation and green policies (X. Liu et al., 2024; Rehman et al., 2024) all exert significant effects on corporate investment efficiency. At the internal characteristics level, the technological empowerment pathways of smart manufacturing and digital transformation (Y. Liu & Zheng, 2025; B. Zhou & Ge, 2024), the governance optimisation effects of ESG performance and official website disclosure (F. J. Liu, 2025; Y. Wang et al., 2025), and the leverage mitigation function of marketing policies (B. Wang et al., 2025) are core drivers of corporate investment efficiency optimisation. These factors pay limited attention to the role of standardisation as a fundamental institutional rule. The standardisation reform examined in this study, however, influences investment efficiency through dual pathways: reshaping the institutional rules governing market operations by intensifying market competition and reducing transaction costs. Unlike prior literature, the uniqueness of standardisation reform lies in its institutional nature. It simultaneously lowers market entry barriers by implementing a self-declaration and disclosure system for corporate standards, thereby amplifying the competitive pressure effect (Yu et al., 2025). Concurrently, it directly reduces transaction costs and financing constraints by unifying implicit rules in debt contracts and clarifying rights and obligations within supply chains (Cai & Ni, 2025; Zhai et al., 2022), thereby creating a dual-empowerment mechanism that simultaneously intensifies competition and reduces transaction costs. Thirdly, the findings of this study hold significant international reference value. The findings regarding how standardisation reforms dismantle institutional barriers and enhance resource allocation efficiency offer practical guidance for nations and regions globally grappling with market fragmentation and inconsistent regulatory frameworks. These economies may prioritise institutional rule harmonisation as a core strategy, drawing upon experiences in unified technical standards and certification systems to resolve deep-seated market distortions. This approach reduces compliance costs for enterprises operating across regions, ultimately driving high-quality economic development through more efficient resource allocation.

Institutional Context and Theoretical Assumptions

Institutional Context

China’s long period of rapid economic growth has been accompanied by significant market segmentation. Institutional factors such as local protectionism and industry barriers have stymied the free flow of factors across regions, leading to challenges in the construction of a unified national market and weakening the decisive role of the market in the allocation of resources. This state of segmentation is not a single dimension of market fragmentation, but rather manifests itself in multi-level and multi-domain institutional differences, with local governments protecting local firms through differentiated access standards and inspection procedures, administrative measures exacerbating resource mismatches and leading to economic downturns (C. Cao & Su, 2024), and monopolistic industries setting exclusionary technological standards to restrict market competition, this highly heterogeneous regional market environment The information asymmetry caused by this highly heterogeneous regional market environment tends to hinder firms’ cross-regional business decisions (Ren et al., 2025), significantly increasing firms’ uncertainty and transaction costs associated with cross-regional operations and investments. Overall, market segmentation in China is characterised by a combination of local protection and industry barriers, which not only hinders efficient factor mobility and results in the loss of capital-space mismatch efficiency, but also inhibits firms’ investment efficiency through systemic transaction costs.

In recent years, China’s standardisation work has achieved remarkable results, but there are still contradictions of cross-standard duplication, insufficient supply lagging, the vitality of market players has not been fully released, the implementation of supervision needs to be strengthened and other issues, which restrict the formation of a unified large market. In 2015, the State Council initiated a pilot comprehensive reform of the national standardisation, taking a three-phase incremental path, and in 2017, Zhejiang became the first national-level pilot; in 2018 Expanded to Guangdong, Shanxi, Shandong, Jiangsu to achieve the classification of exploration; 2023 Heilongjiang, Anhui, Shanghai to join the formation of the East, Central, and West full coverage, efforts to build the government and the market co-governance, synergistic development of high-quality standards system, the core measures and the construction of a unified market in the country in the breaking down of barriers, unifying the rules, stimulate vitality, improve the quality of the strengthening of supervision, docking the international and other key dimensions of the formation of the close links and deep synergy, and have also provided a systematic framework and implementation guideline for the comprehensive local standardisation reform.

The pilot system takes the leap in governance effectiveness as the core orientation, and reconstructs rules around the triple dimension. In terms of the market competition mechanism, it abolishes the enterprise standard approval system, implements self-declaration and public supervision, and encourages competitive standards to break local protection; in terms of transaction cost control, it integrates mandatory national standards and eliminates the systematic or non-systematic transaction costs caused by differences in regional rules; and in terms of collaborative governance, it establishes a layered structure for government-led basic public welfare standards and market-led group standards, forming a multi-dimensional collaborative supply mode. In terms of collaborative governance, a layered structure of government-led basic public welfare standards and market-led group standards has been established to form a multifaceted and collaborative supply model, aiming to form a government-led, market-driven, socially participatory, and collaboratively-promoted standardisation work pattern, and to effectively support the construction of a unified market system.

Theoretical Hypothesis

Firms’ investment efficiency is synergistically shaped by the external environment and internal characteristics. At the external environment level, the intensity of market competition optimises resource allocation by eliminating inefficient investments (Boubaker et al., 2022), but excessive competition may induce short-sightedness in firms (Tinaikar & Xu, 2023); reduced environmental uncertainty improves efficiency by stabilising expectations (M. Chen & Yan, 2025); Climate policy uncertainty and climate change risks, however, diminish corporate investment efficiency by exacerbating agency conflicts, financing constraints and operational risks (Z. Zhang et al., 2025). environmental innovations that reduce information asymmetry can also improve firm investment efficiency (Rehman et al., 2024), while green policy mix improves investment by highly polluting firms through technology inducement and financing constraint mitigation (X. Liu et al., 2024); innovation policy reduces redundant investment (G. Hou & Feng, 2024), but industrial policy stimulated cross-regional expansion may reduce the efficiency of subsidiaries (Dai et al., 2021); among institutional differences, deleveraging policies optimise the capital structure (Lin et al., 2024), and credit ratings regulate investment decisions through information transparency (Xiao & Yu, 2025), Supply chain finance and shadow banking regulation influence corporate investment behaviour through channels of capital availability, exerting a significant effect on the efficiency of small and medium-sized enterprises and outward direct investment (Y. Ma & Hu, 2024; Zheng & Chen, 2024). At the level of internal characteristics, smart manufacturing technology increases efficiency by enhancing information processing capabilities (Y. Liu & Zheng, 2025), while digitalisation reduces agency costs to optimise investment (B. Zhou & Ge, 2024); ESG performance reduces investment bias by improving governance efficacy (F. J. Liu, 2025) and official websites enhance the efficiency of resource allocation through information disclosure (Y. Wang et al., 2025); and marketing policies enhance efficiency by alleviating financial leverage pressure (B. Wang et al., 2025). Moreover, institutional investors’ on-site research and digital transformation can also optimise corporate labour investment or overall investment efficiency by reducing information asymmetry and lowering agency costs (Z. Cao et al., 2025; S. Wang et al., 2024). This suggests that investment efficiency is the result of the multi-dimensional interaction of policy environment, market rules, technical capabilities, and governance mechanisms.

Based on market competition theory, the core logic for enhancing investment efficiency lies in establishing a fully competitive market environment, where competitive pressures compel enterprises to optimise resource allocation. This theory posits that effective competition requires three conditions: first, dismantling market segmentation and regional protectionism to ensure the free flow of factors; second, lowering market entry barriers to stimulate the vitality of all market entities; and third, reducing information asymmetry to establish fair and transparent competitive rules (Hay & Liu, 1997). Only when these conditions are met will enterprises abandon inefficient investment habits reliant on policy protectionism, redirecting capital towards core operations and high-return projects (Cai & Ni, 2025). Concurrently, they will strengthen core competitiveness through technological innovation and process upgrades, ultimately achieving a systemic improvement in investment efficiency (Blind et al., 2022). Where monopolies or regional barriers exist within the market, enterprises are prone to engage in low-level repetitive construction and homogeneous competition. Investment decisions become detached from efficiency-oriented principles, leading to misallocation of resources (Han & Wu, 2024).

The national comprehensive standardisation reform pilot programme precisely aligns with the three conditions proposed by market competition theory through the establishment of a unified large market: Firstly, by consolidating mandatory national standards and optimising recommended standards, it dismantles fragmented rules arising from local protectionism (Han & Wu, 2024), eliminating technical barriers and certification obstacles to cross-regional competition while ensuring the free flow of capital, technology and other factors of production; Secondly, it implements a system of self-declaration and public oversight for enterprise standards, lowering market entry barriers for small and medium-sized enterprises (SMEs). This enables SMEs to rapidly enter markets through standardised technologies, disrupting the monopoly structures of incumbent firms (Yu et al., 2025) and invigorating market competition. Thirdly, a unified standards system provides clear, quantifiable technical specifications and quality requirements for the market, reducing information asymmetry between trading parties. This prevents enterprises from gaining excessive profits through information monopolies, thereby shifting market competition from low-level price rivalry towards technological efficiency competition (Blind et al., 2022). By fulfilling the core conditions of market competition theory, standardisation reform constructs a fully competitive market environment, subsequently driving enterprises to enhance investment efficiency.

Based on transaction cost theory, enhancing investment efficiency relies on simultaneously reducing both institutional and non-institutional transaction costs. Optimising organisational ownership governance models can replace inefficient market transactions, thereby reducing additional expenditures in areas such as information search, contract negotiation, and enforcement. This, in turn, strengthens the effectiveness of internal resource allocation in controlling transaction costs (Foss et al., 2023). Uncertainty in transactional processes and the characteristics of asset specificity directly inflate corporate compliance adaptation and oversight costs. This not only constricts investment space for core operations but also dampens cross-regional cooperation willingness, ultimately leading to distorted investment decisions and inefficient resource allocation (Tennakoon et al., 2025). Consequently, enhancing investment efficiency hinges on refining governance structures through institutional design. This dual-pronged approach—optimising internal organisational mechanisms while strengthening external institutional constraints—reduces diverse transaction costs, thereby guiding enterprises to allocate greater resources towards productive investments and technological innovation.

The national comprehensive standardisation reform pilot scheme systematically reduces various transaction costs through institutional restructuring, fully aligning with the core tenets of transaction cost theory. Firstly, by unifying technical specifications and certification systems, it diminishes compliance adaptation costs for enterprises operating across regions, avoiding redundant investments arising from regional standard discrepancies (Toh & Pyun, 2024). Concurrently, it lowers information search costs, enabling businesses to swiftly and accurately grasp market demands and technological trends (D. L. Jiang et al., 2025). Secondly, by establishing industry knowledge repositories through group standards, it clarifies the boundaries of rights and obligations in supply chain collaborations. This reduces contractual negotiation and oversight costs, thereby enhancing supply chain coordination efficiency (Cai & Ni, 2025); Thirdly, through self-declaration mechanisms for corporate standards, internal technical capabilities are transformed into market-recognised quality signals, mitigating adverse selection and moral hazard stemming from information asymmetry, thereby reducing financing negotiation costs and commercial credit transaction frictions (Zhai et al., 2022); Fourthly, standardising implicit rules within debt covenants reduces negotiation costs between creditors and enterprises, effectively alleviating financing constraints and ensuring efficient investment projects receive adequate capital support (Dyreng et al., 2025). By fulfilling the core conditions of transaction cost theory, standardisation reforms clear institutional obstacles to enhancing corporate investment efficiency.

In summary, existing research shows corporate investment efficiency is jointly shaped by external environments and internal characteristics, with market competition theory and transaction cost theory providing core theoretical guidance. Establishing a fully competitive market forces enterprises to abandon inefficient investments, while systematically reducing institutional and non-institutional transaction costs safeguards productive investment. The national comprehensive standardisation reform pilot aligns with these requirements: it unifies market rules to break regional segmentation and access barriers, and leverages standardised technical specifications to cut transaction costs in compliance, contract execution, and information transmission. This dual pathway drives resources to high-return sectors, ultimately enhancing investment efficiency. The positive correlation between standardisation reform and corporate investment efficiency is no coincidental statistical result but an inevitable trend supported by solid theories and clear transmission mechanisms. Accordingly, this paper proposes the core research hypothesis:

Research Design

Data and Sample

This paper selects listed companies on the Shanghai and Shenzhen A-share markets from 2013 to 2024 as the initial research sample and performs the following processing: first, financial companies are excluded; second, ST and delisted samples are excluded; third, to reduce the impact of outliers, this paper performs 1% and 99% trimmed tail processing on all continuous variables at the micro level. Additionally, the observation period for the explanatory variables is from 2013 to 2023. The data of listed companies are matched with provincial panel data based on the provinces where the companies are located. The original data are sourced from the Guotai An Database (CSMAR), the China Urban Statistical Yearbook, and the China Research Data Service Platform (CNRDS).

Model Specification

This study aims to explore the potential impact of the National Standardisation Comprehensive Reform Policy on corporate investment efficiency. The National Standardisation Comprehensive Reform Pilot Work Plan, officially implemented by provincial governments starting in 2017, is used as the policy under study, and a multi-period difference-in-differences method is employed for empirical analysis. The specific model specification is as follows:

In this model, p represents the province, t represents the year, and a i represents the firm.

The specific measurements of the core variables are as follows: First, regarding the measurement of the explanatory variable standardisation construction (SC). This paper adopts a multi-time point difference-in-differences model, so SC should be set as a dummy variable. Instrumental variable specification aligns with the classical design of multi-period difference-in-differences in policy evaluation studies (L. Sun & Abraham, 2021). It effectively distinguishes between treatment and control groups while isolating the net policy effect by controlling for firm and year fixed effects. This measurement approach has been widely adopted in comparable policy evaluation research (X. Li et al., 2022; Yu et al., 2025; Q. Zhou et al., 2022). SC indicates whether an enterprise was affected by the national standardised comprehensive reform pilot policy in a specific year. When the sample enterprise’s office location is in a national standardisation comprehensive reform pilot province, SC is set to 1; otherwise, it is set to 0. The policy pilot information referenced herein is sourced exclusively from the following official public documents. All details have undergone cross-verification through the official channels of the State Administration for Market Regulation, provincial-level people’s governments, and relevant competent authorities to ensure the accuracy of pilot province coverage, policy commencement dates and policy validity. Specifically, companies with offices located in Zhejiang Province and time periods from 2017 onwards are assigned a value of 1, those located in Shanxi Province, Jiangsu Province, Shandong Province, and Guangdong Province and time periods from 2018 onwards are also assigned a value of 1, those located in Shanghai Municipality, Heilongjiang Province, and Anhui Province and time periods from 2023 onwards are also assigned a value of 1, and all others are assigned a value of 0.

Second, regarding the measurement of the explained variable, corporate investment efficiency (IE). This study adopts Richardson’s (2006) expected investment model to measure corporate investment efficiency. The construction method is detailed in the Appendix. Data sources: CSMAR Cash Flow Statement Database and Balance Sheet Database. A higher IE indicates a greater deviation between actual and expected investment, resulting in lower investment efficiency.

Third, regarding the measurement of control variables. To more accurately assess the impact of standardisation on corporate investment efficiency, it is necessary to control for other factors that may influence investment efficiency. At the firm level, the following control variables are included: firm size (Size), measured using the natural logarithm of total assets; debt-to-asset ratio (Lev), measured using the ratio of total liabilities to total assets; return on assets (ROA), measured using the ratio of net profit to total assets; fixed asset ratio (PPE), measured using the ratio of net fixed assets to total assets; Cash holdings (Cash) are measured as the ratio of cash and cash equivalents to total assets; Corporate growth (Growth) is measured as the revenue growth rate; The proportion of independent directors (Indep) is measured as the ratio of independent directors to the total number of directors; Institutional investor ownership ratio (Inst), measured as the ratio of total shares held by institutional investors to the total number of circulating shares; Provincial-level per capita GDP (PGDP), measured as the ratio of regional total GDP to the regional year-end total population; Secondary industry share (Second), measured as the ratio of secondary industry value added to regional total GDP; Government intervention (Gov), measured as the ratio of government fiscal expenditure to GDP.

Empirical Results

Descriptive Statistics

Table 1 presents the descriptive statistical results for the main variables in this paper. The mean value of IE is 0.0282, indicating that the deviation between actual investment and expected investment in the sample firms is small, with most firms’ investment behaviour being relatively close to reasonable levels; the standard deviation is 0.0334, indicating that the dispersion in investment efficiency among the sample firms is relatively pronounced; From the perspective of quantiles, the 25th percentile (P25) is 0.0081, the median is 0.0181, and the 75th percentile (P75) is 0.0343, indicating that the deviation in investment for most firms is concentrated in the higher range, but there are still some firms with significant issues of investment inefficiency. The mean of SC is 0.6052, indicating that approximately 60.52% of the observations in the sample are in the standardisation reform pilot phase, suggesting that the pilot policy has a broad coverage among the sample enterprises; the standard deviation is 0.4888, which is close to the theoretical maximum standard deviation of 0.5 for dummy variables, reflecting a relatively balanced distribution between pilot and non-pilot samples. Additionally, the descriptive statistics results for the remaining variables are consistent with existing research and fall within reasonable ranges.

Descriptive Statistics.

Benchmark Regression

Table 2 presents the regression results between national standardisation reform pilot programmes and enterprise investment efficiency. Column (1) reports the regression results with only the core explanatory variable (SC) and fixed effects included. The coefficient for the national standardisation reform pilot programme (SC) is −0.0040 and is statistically significant at the 1% level. Since higher values of the IE indicator indicate lower corporate investment efficiency, this result suggests that after implementing the standardisation reform pilot programme, the deviation between actual and expected investment has significantly decreased, indicating a significant improvement in corporate investment efficiency. Theoretically, this aligns closely with institutional economics and market integration theories: standardisation eliminates institutional barriers arising from fragmented regional standards by reconstructing unified market rules (North, 1990), thereby reducing transaction costs and investment uncertainty for enterprises (Toh & Pyun, 2024). Simultaneously, it facilitates the free flow of factors across regions (Han & Wu, 2024), enabling enterprises to allocate resources based on project efficiency rather than regional constraints, thereby curbing inefficient investment behaviour.

Benchmark Regression.

Note. Robust standard errors clustered at the industry level are in parentheses.

p < .1, **p < .05, ***p < .01.

Column (2) adds a series of control variables and fixed effects to Column (1). At this point, the coefficient for the national standardisation reform pilot programme (SC) is −0.0032 and remains statistically significant at the 1% level. This indicates that, after controlling for other factors, the standardisation reform pilot programme still significantly reduces the deviation between actual and expected investment, thereby promoting corporate investment efficiency. This result preliminarily supports the positive impact of the national standardisation reform pilot programme on corporate investment efficiency, This outcome can be explained through market competition theory and transaction cost theory: the reform lowered market entry barriers through a self-declaration system for enterprise standards, intensifying market competition and compelling enterprises to abandon inefficient investments reliant on policy protection (Hay & Liu, 1997); simultaneously, unified standards reduced supply chain negotiation costs, financing frictions (Cai & Ni, 2025) and information search costs (Williamson, 1985), alleviating corporate financing constraints and enhancing the precision of investment decisions.

Dynamic Effect Testing

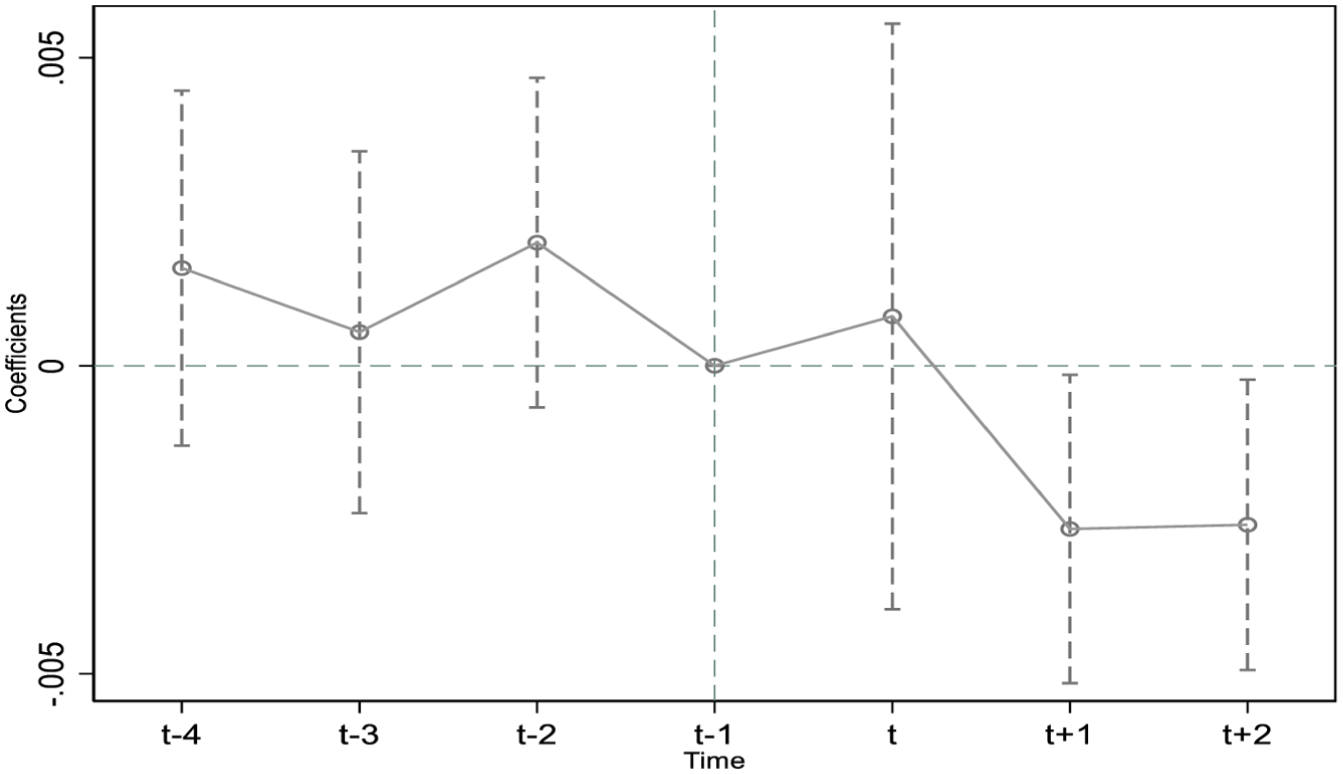

In order to test the dynamic effect of the national standardisation comprehensive reform pilot policy on the investment efficiency of enterprises, as shown in Figure 1, the parallel trend hypothesis is satisfied before the implementation of the policy. The coefficient in the period of policy implementation is positive but not significant. In the first period after the implementation of the policy, the coefficient began to be significantly negative and continued to maintain a significant negative direction. This indicates that the policy effect of the standardisation reform pilot is gradually released after the implementation, and its role in improving the investment efficiency of enterprises is increasingly visible over time.

Dynamic effect testing.

Robustness Testing

Placebo Test

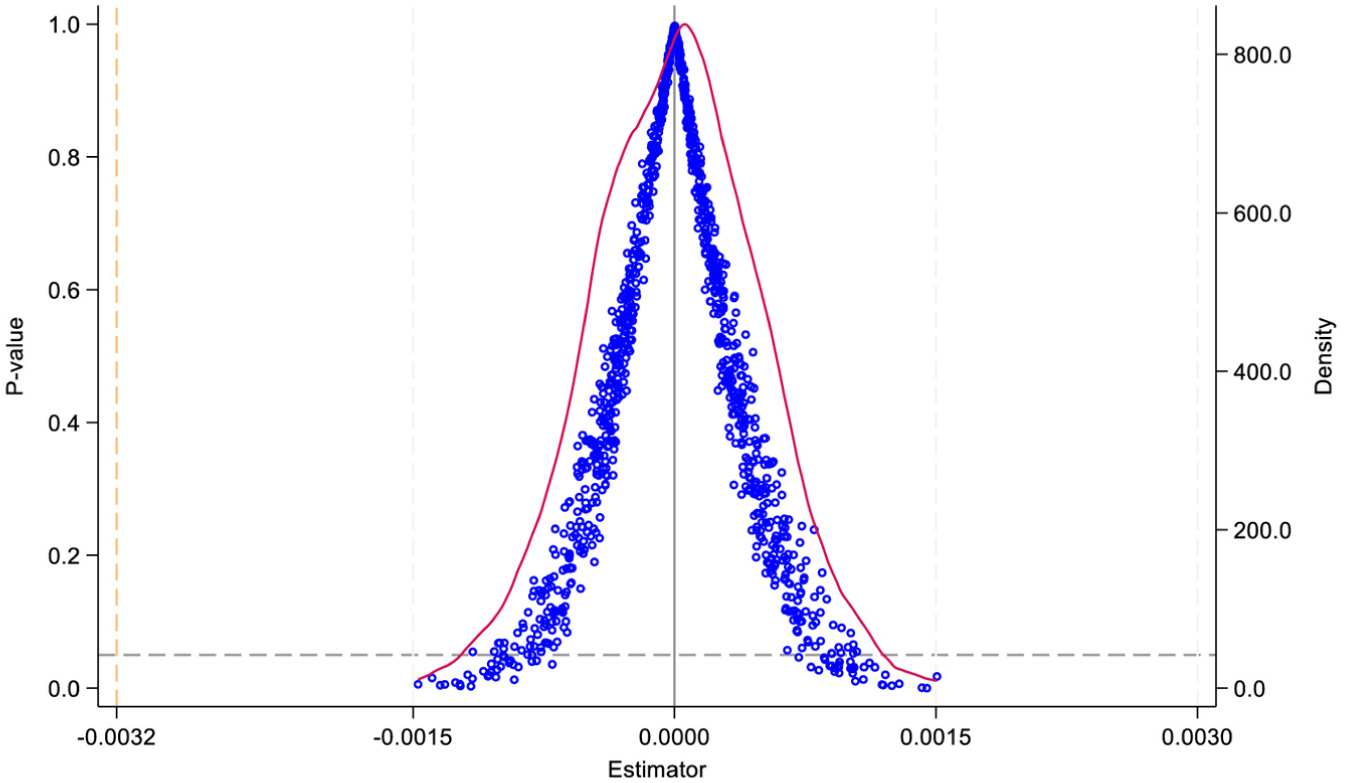

In order to verify the reliability of the benchmark regression results, this paper adopts the method of a random fictitious treatment group for a placebo test, based on the benchmark model setting randomly selected 1,000 times. The results, as shown in Figure 2, show that the estimated coefficients of the fictitious treatments are centrally distributed around the zero point; the estimated effects of the placebo samples are significantly weaker than those of the benchmark regression results, which supports the robustness of the conclusions.

Placebo tests.

Interpolation Estimation

This paper carries out robustness tests using interpolated estimation (L. Liu et al., 2024), and the results are shown in Figure 3, where the average treatment effect estimate is insignificant and tends to be zero before the policy intervention. After the policy intervention, the estimate turns significantly negative. This indicates that the policy implementation significantly improves the investment efficiency of enterprises, and the effect persists after the policy implementation.

Interpolation estimator.

Group-Period Average Treatment Effect

This paper uses group-period average treatment effects for robustness testing (L. Sun & Abraham, 2021), and the results are shown in Figure 4, where no significant trend differences are observed before the policy intervention. After the policy intervention, the results are insignificant in the current period, and the estimates are significantly negative in the subsequent periods, suggesting that the policy has a progressive role in promoting firms’ investment efficiency.

Group-period average treatment effects.

Mitigating Model-Setting Bias

To overcome the sample selection bias and model setting problems, this study adopts three methods for robustness testing: (1) PSM-DID, which balances the samples of the treatment and control groups through propensity score matching; (2) Entropy balancing method, which accurately matches the distributional characteristics of the covariates; (3) Double machine learning, which deals with high-dimensional control variables and potential non-linear relationships (Bodory et al., 2022). The results show (see Columns (1)–(3) of Table 3) that the coefficients of SC are significantly negative under all three methods, suggesting that the core conclusion that the policy enhances the efficiency of corporate investment still holds robustly after mitigating the potential endogeneity problem.

Robustness Check.

Note. Robust standard errors clustered at the industry level are in parentheses.

p < .1, **p < .05, ***p < .01.

Binary Variable Measure

In order to ensure that the findings do not depend on a particular modelling set-up, two key tests are conducted in this study. Firstly, the measure of the explanatory variables is replaced, and investment efficiency is re-measured using Biddle et al.’s (2009) methodology, and secondly, the sample is differentiated by subdividing the overall investment efficiency sample into “over-investment” and “under-investment” groups according to the direction of the investment bias, and examining the policy effects separately. The results show (see Columns (4), (8), and (9) of Table 3) that the coefficients of SC are significantly negative regardless of the investment efficiency measure used, or in the overinvestment and underinvestment groups. This suggests that the core findings are highly robust to specific model settings or types of investment bias.

Adding Fixed Effects

Traditional firm-year fixed effects may overlook industry-year-level interaction heterogeneity. Therefore, this paper further incorporates the “Industry × year” interaction fixed effect to account for factors such as policy shocks and technological changes that vary over time within industries. The results in Table 3, Column (5), show that after controlling for code and “Industry × Year” fixed effects, the SC coefficient is significantly negative. This indicates that even when considering the dynamic heterogeneity of industry-year interactions, the negative effects of standardised pilot programmes remain robust, ruling out biases caused by omitting key fixed effects.

Adjusting Cluster Standard Errors

The choice of clustering level directly affects the reliability of statistical inference. Traditional studies often use industry as the clustering level, but corporate investment behaviour may exhibit stronger correlations at the individual firm or city level. This study re-estimates the results using both firms and cities as clustering units. The results for firm-level clustering are shown in Column (6) of Table 3, where the SC coefficient is significantly negative; the results for city-level clustering are shown in Column (7) of Table 3, where the SC coefficient is significantly negative. The negative significance of SC remains consistent across both clustering levels, validating the robustness of statistical inference to the choice of clustering standard errors and indicating that the core effect is not driven by specific sampling error structures.

Mechanism Testing

To elucidate the mechanism through which national standardisation reform policies influence corporate investment efficiency, this paper adopts a stepwise regression framework for mediating effect testing. In Formula (2), the superscript

Market Competition

National standardisation reforms have significantly intensified market competition by unifying technical specifications and dismantling regional and sectoral barriers (Hay & Liu, 1997; Yu et al., 2025). This approach lowers entry thresholds for small and medium-sized enterprises while stimulating entrepreneurial dynamism (L. Chen et al., 2025), simultaneously driving competition towards technological efficiency (Blind et al., 2022). Amid intensified competition, enterprises must focus on core and high-return investments, abandoning inefficient practices fostered by policy protection. Concurrently, enhancing the quality of information disclosure mitigates agency conflicts (F. Chen et al., 2011), thereby directing capital flows towards efficient domains such as technological innovation. This paper empirically examines this transmission mechanism through three dimensions: entrepreneurial dynamism, market concentration, and corporate gross profit margins.

Entrepreneurial dynamism (New) serves as a core indicator for gauging market entry barriers and competitive vigour, reflecting the emergence rate of new market entities within a region. The influx of new enterprises disrupts existing market structures, intensifies competition over products, technologies, and resources, and compels incumbent firms to enhance investment efficiency (Y. Sun & You, 2023). This study employs the proxy variable “number of newly established enterprises in the region/total population of the region.” Specifically, calculations are conducted at the city level: the number of newly registered enterprises recorded annually by market regulatory authorities is divided by the city’s year-end total population to yield the per capita figure for newly established enterprises (W. Jiang et al., 2025). To mitigate measurement errors, random noise is used to fine-tune the data, simulating the random fluctuations in enterprise entry observed in reality. The regression results are shown in Table 4, Column (1). The SC coefficient is significantly positive, indicating that the national standardisation comprehensive reform pilot programme can promote an increase in entrepreneurial vitality, confirming the positive impact of the national standardisation comprehensive reform pilot programme on enhancing market competition. From a theoretical perspective, standardisation reform draws upon information asymmetry theory and market access barrier theory. Through multiple institutional designs, it lowers entry thresholds, underpins entrepreneurial activities, and establishes a competitive foundation for optimising corporate investment efficiency. Drawing upon market access barrier theory, harmonising mandatory national standards and refining recommended standards dismantles regional technical barriers arising from local protectionism, thereby reducing compliance costs for new enterprises establishing operations across regions (Han & Wu, 2024). Drawing upon information asymmetry theory, implementing a self-declaration and public disclosure system for enterprise standards converts corporate technical capabilities into market-recognised quality signals, alleviating the trust deficit faced by small and medium-sized enterprises (Yu et al., 2025). Concurrently, this reduces information asymmetry between government and enterprises, compressing the information rent space for incumbent firms (Kao & Xie, 2025) and optimising labour market structure alongside human capital matching efficiency (Yu et al., 2025).

Mechanisms to Test Market Competition.

Note. Robust standard errors clustered at the industry level are in parentheses.

p < .05, ***p < .01.

Market concentration measures the degree of uneven distribution of enterprise scale within an industry, serving as a classic indicator of competitive intensity. Higher concentration indicates that a small number of large enterprises command a greater share of the market, signifying stronger monopolistic tendencies and weaker competition; conversely, lower concentration reflects more vigorous competition. Regarding market concentration, this paper uses the Herfindahl-Hirschman Index (HHI) to measure market concentration (Benson et al., 2024). A smaller HHI indicates smaller differences in revenue among firms within an industry and higher levels of market competition. The regression results are shown in Table 4 (Column (2)). The SC coefficient is significantly negative, indicating that the national standardisation reform pilot policy reduces the HHI index, thereby confirming the promotional effect of national standardisation policies on market competition. From a theoretical perspective, first, standardisation unifies technical specifications to break regional monopolies, conforming to competition-enhancing and innovation-driven theories. Removing institutional barriers allows SMEs to use standardised technologies to narrow technical compatibility gaps with incumbents, reducing market entry sunk costs and diluting incumbents’ market share (Aghion et al., 2021), which aligns with this study’s finding that standardisation eliminates regional standard barriers for SMEs. Second, transaction cost theory explains standardisation’s dampening effect on market concentration: unified technical specifications and certification systems increase new entrants by eliminating inefficiencies from fragmented regional standards, sparing SMEs repeated adaptation investments and enabling them to compete with incumbents (Blind et al., 2023), providing empirical support for this paper’s argument.

The gross profit margin (Margin) of an enterprise reflects the profitability of its products, exhibiting an inverse relationship with market competition intensity. In highly competitive markets, enterprises struggle to sustain high margins through monopolistic positions, whereas in monopolistic markets, firms can leverage barriers to capture excess profits. The weighted average of gross profit margins across a company’s principal business lines serves as a proxy variable. Specifically, this is calculated by weighting the gross profit margin of each principal business line ((Principal business revenue − Principal business costs)/Principal business revenue) using its respective operating revenue as the weighting factor, thereby deriving the company’s comprehensive gross profit margin (Du et al., 2020). The regression results are shown in Column (3) of Table 4, and the coefficient of the interaction term “SC × Magin” is significantly negative, which indicates that the national standardisation has a stronger competitive promotion effect on firms with high gross profit margins. From a theoretical perspective, based on monopoly advantage and information rent theory, high gross profit margins typically indicate significant market monopolisation or information asymmetry (Toh & Pyun, 2024). Enterprises may sustain excess profits through technological barriers and regional protectionism, lacking incentives to optimise investment efficiency. Standardisation reforms, by unifying technical specifications and enhancing information transparency, directly erode such firms’ information rents and monopoly advantages. According to market competition theory, this compels them to abandon inefficient investment habits and redirect resources towards high-efficiency areas like technological innovation and process upgrades (Hay & Liu, 1997), thereby compressing inefficient profit margins. By contrast, industries with inherently low gross profit margins exhibit intense competition, where standardisation reforms yield weaker marginal effects in intensifying competition. This aligns with the logic of diminishing marginal utility theory.

Transaction Costs

National standardisation reforms systematically reduce both institutional and non-institutional transaction costs by unifying technical specifications and regulatory frameworks (Toh & Pyun, 2024). This approach integrates national standards, dismantles local protectionism, and diminishes friction costs associated with corporate compliance and cross-regional operations. Concurrently, it lowers negotiation and oversight costs by clarifying supply chain rights and obligations while standardising debt contract rules (Cai & Ni, 2025). Cost reductions optimise the investment environment: increased corporate cash flow alleviates financing constraints (Zhai et al., 2022), while diminished information asymmetry lowers decision-making risks (F. Chen et al., 2011). This redirects capital away from non-productive expenditures towards core operations and innovation investments. This paper empirically examines this transmission mechanism by analysing both institutional and non-institutional cost categories.

Non-Institutional Transaction Costs

The cost of debt financing (Debt) constitutes the core transaction cost for enterprises in obtaining debt capital, reflecting the degree of contractual friction between the enterprise and its creditors. The greater the information asymmetry and the more ambiguous the contractual rules, the higher the risk premium demanded by creditors, and consequently the higher the enterprise’s financing costs. This paper uses interest expenses/total liabilities as the metric, reflecting the proportion of debt financing costs to total liabilities. When calculating, interest expense is taken from the amount under “finance costs” in the income statement, while total liabilities are taken from the year-end total liabilities figure in the balance sheet (Hu et al., 2024). The higher the debt financing costs, the greater the transaction friction on the debt side of enterprises. The regression results are shown in Table 5, Column (1). The SC coefficient is significantly negative, indicating that standardisation significantly reduces corporate debt financing costs. This resonates with the core argument that optimising the quotation system cuts transaction costs and underpins efficient investment. Theoretically, first, reducing information asymmetry mitigates adverse selection and moral hazard: standardisation unifies implicit debt contract rules, turning ambiguous risk assessment criteria into quantifiable technical indicators to narrow information gaps between creditors and enterprises (Toh & Pyun, 2024), which aligns with credit rationing theory—enhanced transparency reduces creditors’ risk premium demands and lowers corporate financing costs (Stiglitz & Weiss, 1981). Second, standardisation lowers debt financing costs by unifying institutional rules to cut debt covenant negotiation and monitoring costs, thus reducing average corporate borrowing rates (Z. Wang et al., 2023), consistent with this paper’s empirical findings. Moreover, unified rules reducing contractual and financing costs align with the introduction’s framework that institutional cost control safeguards investment efficiency improvement.

Mechanisms to Test Transaction Costs.

Note. Robust standard errors clustered at the industry level in parentheses.

p < .1. **p < .05.

Regarding commercial credit financing, commercial credit financing (Credit) measures the transaction cost of the supply chain side of the enterprise, Reflecting the degree of friction in collaboration between enterprises and their upstream and downstream partners—the clearer the rights and obligations within supply chain cooperation and the higher the level of trust, the lower the difficulty for enterprises to obtain commercial credit and the lower the transaction costs within the supply chain. measured by the ratio of payables to total assets. Accounts payable shall be taken as the amount of accounts payable at the balance sheet year-end, and total liabilities shall be taken as the amount of total liabilities at the year-end (Yang et al., 2025). The regression results are shown in Column (2) of Table 5. The SC coefficient is significantly positive, indicating that standardisation significantly increases the proportion of commercial credit financing. Standardisation reduces moral hazard within supply chains by clarifying the boundaries of rights and obligations in collaborative arrangements (Cai & Ni, 2025). This aligns with transaction cost economics theory, which posits that improved contractual environments mitigate opportunistic behaviour in cooperation, thereby enhancing upstream enterprises’ willingness to extend commercial credit to downstream counterparts (Williamson, 1985).

Institutional Transaction Costs

Rent-seeking costs (Rent) represent non-productive expenditures incurred by enterprises to circumvent administrative barriers, secure policy preferences, or obtain resource advantages. At their core, these constitute misallocation costs stemming from institutional distortions. This paper employs “administrative expenses/operating revenue” as a proxy variable, calculated as follows: the total annual administrative expenses of an enterprise (including implicit expenditures such as entertainment expenses, intermediary fees, and administrative coordination fees) divided by its total operating revenue for the same year (J. Zhang & Luan, 2025). The regression results are shown in Table 5, Column (3). The SC coefficient is significantly negative, indicating that standardisation significantly reduces firms’ rent-seeking costs. From the perspective of transaction cost theory, standardisation reforms transform implicit relational interactions between government and enterprises into explicit rule-based interactions by unifying technical specifications and certification systems. On the one hand, standardisation eliminates local governments’ scope for rent-seeking through differentiated regulations, enabling enterprises to gain equitable market access without resorting to such practices. On the other hand, standardisation reforms clarify the boundaries of government oversight, curtailing administrative discretion and diminishing enterprises’ incentives to secure resources through bribery or lobbying (Tang et al., 2024). This demonstrates how standardisation reforms, by restructuring the institutional environment, reduce the rent-seeking component within institutional transaction costs.

Local protectionism refers to the practice of local governments erecting market barriers through administrative means to safeguard local enterprises’ interests, thereby restricting the cross-regional flow of factors. This constitutes a core driver of market segmentation (Qin et al., 2020). Given the difficulty in directly quantifying the motivations behind local protectionism, this study employs fiscal decentralisation (FD) as a proxy variable, calculated as: (per capita local fiscal expenditure in that province + per capita central fiscal expenditure nationwide) (Han & Wu, 2024). The theoretical rationale is that higher fiscal decentralisation enhances local governments’ fiscal autonomy and economic regulatory power, thereby strengthening their motivation and capacity to protect local enterprises through tax incentives and administrative barriers. This, in turn, elevates the institutional friction costs of cross-regional transactions. The regression results are shown in Column (4) of Table 5. The interaction term “SC × FD” is significantly negative, indicating that national standardisation reverses the negative impact of local protectionism on investment efficiency and promotes the flow of capital to efficient investment. Local governments protect local enterprises by setting up market barriers, while enterprises rely on policy shelters to weaken the incentive to improve investment efficiency. This kind of government-enterprise alliance distorts the principal-agent relationship of market competition, with local governments defaulting to the inefficient survival of enterprises in the pursuit of short-term economic growth, and enterprises exchanging employment and tax revenue contributions for protection, creating a two-way bundle of interests (Han & Wu, 2024). The direct consequence is that capital flows to protected inefficient businesses; meanwhile, policy frictions prevent the entry of high-productivity firms and exacerbate capital mismatch (Han & Wu, 2024). Ultimately, protected firms do not need to invest efficiently in order to survive and are even induced to overinvest in inefficient businesses, leading to a decline in overall investment efficiency.

Heterogeneity Analysis

Level of Marketisation

Marketisation indices serve to illustrate the sophistication of regional market mechanisms and the degree to which resource allocation operates through market forces. In this paper, we refer to the 2012 provincial-level marketisation index report and use the marketisation index (Market) to conduct the heterogeneity analysis of the marketisation level. For the specific calculation method, see the Appendix. The marketisation index comprises five sub-indices: the relationship between government and the market, the development of the non-state-owned economy, the maturity of product markets, the maturity of factor markets, and the development of market intermediary organisations and the rule of law environment. These sub-indices are combined with equal weighting to form the overall marketisation index (Z. C. Wang et al., 2025) which is calculated based on the average growth of the marketisation index over the years using the historical average method, with higher values representing stronger marketisation. The regression results are shown in Column (1) of Table 6, and the coefficient of the interaction term “SC × Market” is significantly positive, indicating that the higher the level of marketisation, the weaker the marginal enhancement effect of standardisation on investment efficiency. Regions with higher marketisation levels have developed more sophisticated mechanisms for price signalling, competitive elimination, and contract enforcement, aligning with the core tenets of institutional complementarity theory. This theory posits that mature market institutions form an interconnected system: price signals accurately reflect resource scarcity, competitive mechanisms naturally weed out inefficient capacity, while robust contract enforcement systems reduce transactional uncertainty. Within this context, standardisation reforms serve merely as supplementary institutional arrangements, with their marginal scope for reducing information asymmetry and optimising resource allocation inherently constrained. Empirical research within China’s markets further corroborates this: in regions with higher marketisation levels, the information disclosure and resource allocation effects of standardisation reforms significantly overlap with mature market mechanisms, resulting in limited marginal policy benefits (Z. C. Wang et al., 2025).

Heterogeneity Analysis.

Note. Robust standard errors clustered at the industry level are in parentheses.

p < .1, **p < .05, ***p < .01.

Government Size

Government size (GSize) serves as a core indicator for characterising the abundance of administrative resources and market intervention capacity within regional governments. Larger governments typically possess more ample administrative resources and more sophisticated implementation systems, conferring inherent advantages in policy execution, institutional implementation, and cross-departmental coordination. Conversely, smaller governments are often constrained by resource limitations, resulting in comparatively weaker policy implementation efficiency and coordination capabilities. This paper measures the size of government (GSize) as the ratio of the number of civil servants to the total population (Yao & Ma, 2025). Civil servant data: sourced from provincial Statistical Bulletins on Human Resources and Social Security Development and Annual Reports on Civil Servant Recruitment and Registration, with the core statistical scope being the total number of staff within the established staffing quotas of Party and government organs and public institutions at all levels. Regional total population data is sourced from the China Urban Statistical Yearbook, employing year-end resident population totals to align with the actual population served by administrative resources, thereby ensuring the indicator’s validity, reflecting the government’s ability to intervene in the market. The regression results are shown in Column (2) of Table 6, and the negative and significant coefficient of the interaction term “SC × GSize” indicates that the larger the government size, the stronger the promotion effect of standardisation on investment efficiency. Standardisation reform, as a public policy aimed at optimising market rules, requires sufficient administrative resources for the government to advance standard implementation and oversight. Its core objectives of unifying technical specifications and dismantling local protectionism hinge on this capacity. The abundance of governmental administrative resources directly determines the resource allocation effects of public policy. Governments with strong administrative capacity ensure that institutional reforms genuinely dismantle market barriers and reduce transaction costs for enterprises. Conversely, smaller governments with insufficient administrative resources often struggle to implement policies effectively due to enforcement gaps, failing to correct market distortions (Andrews & Cingano, 2014). Standardisation reform involves multiple departments, including market regulation, quality supervision, and industry oversight. Larger governments possess more robust coordination mechanisms, effectively preventing inconsistent standard implementation caused by departmental barriers. This ensures the rigid enforcement of unified technical specifications across entire regions, thereby reducing compliance costs and uncertainties for enterprises operating across borders (Toh & Pyun, 2024).

Social Trust

Social trust, as an informal institution (North, 1990), safeguards market transactions and corporate investment by reducing information asymmetry, lowering contract enforcement costs, and curbing opportunistic behaviour. This study employs the classic CGSS 2012 questionnaire item measuring generalised social trust: “In general, do you think most people can be trusted? Or is it better to be cautious when dealing with others?” This question directly reflects individuals’ propensity to trust others and serves as a core proxy indicator for social trust. The questionnaire options comprise four categories: Trust them very much, Trust them somewhat, Do not trust them very much, Do not trust them at all. This study uses the ratio of the number of respondents who answered “somewhat trust” and “very trust” to the total number of respondents in the region as the measurement method for social trust (Trust) (Ding et al., 2023). The regression results are shown in Column (3) of Table 6, and the positive and significant coefficient of the interaction term “SC × Trust” indicates that the lower the social trust, the stronger the promotion effect of standardisation on investment efficiency. In environments of low trust, transactional frictions within enterprises constrain the efficiency of resource allocation. Here, standardisation reforms form an institutional complementarity with low-trust environments through formal institutional design, filling gaps in informal systems. Unified technical specifications and certification frameworks guarantee product quality and collaborative standards, substituting for absent trust mechanisms while reducing adverse selection and moral hazard among enterprises (Toh & Pyun, 2024). Formal institutions thus address governance deficiencies in low-trust regions (Ziller & Andreß, 2022). High-trust environments suppress corporate financing irregularities and reduce oversight costs in contract enforcement, facilitating smoother market transactions. Here, standardisation reform as a formal institutional arrangement exhibits significant functional overlap with informal trust mechanisms in high-trust regions through its core functions of “unifying rules, clarifying rights and obligations, and reducing trust risks.” The marginal improvement potential of standardisation reform’s mandatory technical certification for investment decisions is thus limited (Qiu et al., 2021).

Conclusions and Recommendations

This paper, based on data from A-share listed companies on the Shanghai and Shenzhen stock exchanges from 2013 to 2024, uses the national standardisation comprehensive reform pilot programme as a natural experiment to systematically investigate the impact of standardisation reform on corporate investment efficiency. The main conclusions are as follows First, the pilot policy of comprehensive national standardisation reform significantly improves the investment efficiency of enterprises, and the multi-period DID dynamic effect test confirms that the effect continues to increase over time; second, the mechanism of action is reflected in the synergy of two paths: the path of strengthening market competition and the path of reducing transaction costs; third, the heterogeneity analysis reveals that the policy effect is more significant in regions with a lower degree of marketisation, a larger government, and a lower degree of social trust, suggesting that the Standardised reforms have complementary value for regions with weak institutions.The aforementioned research findings make three key contributions to the existing literature. First, within the unified large market research domain, existing studies predominantly focus on the unified large market’s significant impact on corporate behaviour and developmental dynamism (Blind et al., 2022; Yu et al., 2025), factor allocation and market efficiency (Blind et al., 2023; Y. Zhao et al., 2024), industrial structure and green transition (Qin et al., 2020), supply chains and trade stability (Handley et al., 2025; Pandey, 2025). This paper complements the macro-micro transmission mechanism of market integration by revealing how standardisation reforms enhance investment efficiency through unified technical specifications and the elimination of regional standard fragmentation. This institutional integration perspective enriches the research dimensions within this field. Secondly, regarding factors influencing corporate investment efficiency, existing literature predominantly emphasises the roles of internal governance and external market environments. Internal governance aspects include smart technologies and digitalisation (Y. Liu & Zheng, 2025; B. Zhou & Ge, 2024), ESG performance (F. J. Liu, 2025), and financial motivation (Z. Wang et al., 2023). External market environments include market competition intensity (Boubaker et al., 2022; Tinaikar & Xu, 2023), environmental uncertainty (M. Chen & Yan, 2025), and policy frameworks (G. Hou & Feng, 2024; Lin et al., 2024; X. Liu et al., 2024). However, there remains insufficient attention to standardisation as a foundational institutional rule (W. Li et al., 2025; F. J. Liu, 2025). This study incorporates standardisation into its analytical framework, confirming its dual function of intensifying competition while reducing costs. This provides new empirical evidence for research examining how formal institutional environments influence micro-level corporate decision-making. Finally, the study’s conclusions hold significant international reference value. Its findings on how standardisation reforms can dismantle institutional barriers and enhance resource allocation efficiency offer practical guidance for countries and regions globally facing market fragmentation and inconsistent regulatory frameworks.

Based on the research findings, this paper proposes the following policy recommendations. Regions with low marketisation, constrained by imperfect market mechanisms, severe local protectionism, and high transaction costs, represent key areas where standardisation reforms can yield significant effects. The first step involves prioritising the integration of foundational general standards across critical sectors such as manufacturing, energy, and logistics to establish a unified national standardisation framework, thereby eliminating institutional barriers caused by fragmented regional standards. Secondly, accelerate the development of standardised information disclosure platforms, requiring enterprises to publicly declare product technical parameters, quality indicators, and compliance certification status according to unified standards, thereby reducing market information asymmetry. Thirdly, link standardisation with industrial policy, prioritising support for enterprises complying with national unified standards in project approvals, fiscal subsidies, and tax incentives. This will guide capital towards efficient investment projects and break the inertia of inefficient investment driven by local protectionism. Regions with larger government scales possess ample administrative resources and robust policy enforcement capabilities, enabling effective implementation of standardisation reforms. However, they also face risks of excessive administrative intervention. This can be mitigated by establishing a cross-departmental coordination mechanism led by market regulators and involving industry authorities, judicial bodies, and trade associations. This mechanism should develop a standard implementation roadmap that clarifies responsibilities, timelines, and oversight methods for each department. A negative list for government standard intervention should be introduced, specifying that government participation is limited to standards in public welfare areas such as public safety and environmental protection, while fully delegating the authority to set competitive product standards to market entities. Regions with low social trust suffer from persistently high transaction costs and heightened investment risks due to the absence of informal institutional safeguards such as mutual trust. Standardisation reform can serve as a formal institutional supplement to address this deficiency. It is necessary to promote the deep integration of standardisation with enforcement mechanisms, incorporating key standard compliance indicators into the scope of administrative enforcement and judicial review, while clarifying the legal liabilities for non-compliance. Efforts should also be strengthened to promote standard awareness and dissemination, conducting training on the application of enterprise standards to enhance businesses’ awareness and capability in utilising standards to mitigate transaction risks.

Despite the aforementioned research findings presented herein, certain limitations remain, which point to directions for future studies. Firstly, in terms of scope, this paper focuses on A-share listed companies and fails to adequately reflect the impact of standardisation reforms on small and medium-sized enterprises (SMEs) and unlisted firms. Future research could expand the sample to include micro-enterprises, conducting comparative analyses to examine the heterogeneous effects of the policy across enterprises of different scales. Second, in measuring standardisation reform, this study employs regional pilot dummy variables, which fail to fully capture the depth and intensity of enterprise participation in standardisation. Future research could develop more refined indicators based on enterprise-level standard participation data to more accurately gauge policy effects. Third, in mechanism analysis, this study focuses on two pathways—market competition and transaction costs—yet specific transmission mechanisms may vary across industries. For instance, standardisation’s impact on investment efficiency in technology-intensive industries may primarily operate through technological innovation channels. In contrast, in labour-intensive sectors, it may predominantly function via cost reduction channels. Future research could explore industry-specific heterogeneity to deepen the understanding of these mechanisms. Fourthly, as digital transformation advances, the convergence of digital technologies with standardisation reforms may generate novel effects on corporate investment efficiency. Future studies could investigate synergies between digitalisation and standardisation, offering fresh perspectives for advancing high-quality enterprise development.

Footnotes

Appendix

This method estimates the optimal investment level of a company through OLS regression and uses the absolute value of the residual deviation between actual investment and expected investment as a proxy variable for inefficient investment. The specific model is set as follows: