Abstract

This research examines the effect of diversification strategy on corporate tax aggressiveness activities with board effectiveness as the moderating variable. This study brings a context of the ASEAN Economic Community (AEC), which is argued inducing diversification strategies taken by companies in ASEAN countries. A sample from a developing country, that is, Indonesia, is collected due to this country’s specific characteristics related to tax regimes. Therefore, 246 observations from non-financial listed companies from 2014 to 2016 are used. The findings show that the firms with an international diversification strategy positively associate with corporate tax aggressiveness. On the other hand, companies conducting industrial diversification strategies were found to have ineffective tax management. The study also found an ineffective board of commissioners in the condition of corporate tax aggressiveness and ineffective tax management. This study brings some practical implications that the government needs to evaluate its tax policy while business practitioners must choose a business strategy congruent with tax management.

Keywords

Introduction

Corporate tax aggressiveness has existed throughout history and will likely be non-trivial and prevalent in many countries for as long as corporations are subject to tax. In fact, base erosion and profit shifting (BEPS) activities conducted by multinational enterprises have threatened all countries’ tax revenues. Countries lost revenue as much as 100 to 240 billion USD annually, equivalent to 4% to 10% of the global corporate income tax revenue (OECD, 2022). From a corporate’s point of view, however, tax obligation is a burden that needs to be reduced so that the companies can generate higher profits. Therefore, tax avoidance is perceived as one of the strategic policies of the company’s management to maximize the company’s value. This tax avoidance or tax aggressiveness activity may bring uncertainty to cashflows in the future since while the action causes tax savings, there is also a probability that the company will pay the higher tax due to tax penalties or other punishments due to non-tax-compliant activities. Moreover, additional risks related to asymmetric information risks may arise due to complex and less transparent tax avoidance strategies. Therefore, the degree of the tax aggressiveness can be up and down, depending upon the calculation of the management related to the costs and benefits of this tax aggressiveness strategy.

Diversification is argued to be one of the management strategies related to aggressive tax management (Aditama, 2016; Ettredge et al., 2006; Gyan et al., 2017; Zheng, 2017). This strategy is also related to earnings management activities harming the shareholders’ interests (Dalton et al., 2007; Jiraporn et al., 2008; Masud et al., 2017; Rodriguez-Perez & Hemmen, 2010). Committing tax aggressiveness activities, multinational companies not only conduct the diversification strategy expanding the business to particular markets, sectors, industries, or segments but also exploit gaps and mismatches between different countries’ tax systems. This risky activity may threaten the company in the future; hence, in this context, corporate governance, especially board supervision, has a vital role so that management runs the business on behalf of shareholders’ interests whilst meeting other stakeholders’ expectations, leading to value creation in the long term.

Based on the discussion above, the objective of this study is to examine the effect of diversification strategy on corporate tax aggressiveness activities. This study fills the research gap by analyzing further the moderating effect of board effectiveness on the relationship between diversification and tax aggressiveness. In addition, this study extends the previous study by taking a sample from more than one industry so that the results can provide more general evidence. Moreover, an integrated scorecard approach (Hermawan, 2009) which is used to measure the board’s effectiveness, rather than a simple proxy such as an individual measurement such as percentage of independence or experience, is argued to improve the robustness of the study. This study has become more important since the ASEAN Economic Community (AEC) formation in 2015, which is argued to induce diversification strategies taken by companies in ASEAN countries.

This study is conducted by taking Indonesia as a case study as one of the emerging countries in ASEAN. While it is a populous country, its tax ratio is relatively low compared to other ASEAN countries. Examining 246 observations of non-financial listed companies, this study found that the international diversification strategy of a company has a positive association with corporate tax aggressiveness. On the other hand, the industrial diversification strategy was ineffective in tax management. The study also found that the supervisory board is ineffective as it cannot moderate corporate tax aggressiveness and ineffective tax management.

The structure of the paper is as follows. The next section is a literature review and hypotheses development. It is followed by a section on the data collection method and analysis. Results of the study and discussions are then presented. The last section presents the conclusion and implications of the study.

Literature Review and Hypotheses Development

Based on agency theory, in modern firms, there is a relationship between principals (shareholders) and agents (corporate executive and manager) (Jensen & Meckling, 1976). Shareholders, as the owners/principals of the firm, employ agents to do a particular work. In the agency theory, shareholders expect that agents are likely to do activities or make a decision on behalf of the principals. However, in some situations, both principals and agents want to maximize their utility, and agents will not always take the best possible conditions to satisfy the principals’ interests (Godfrey et al., 2010). Such a conflict between principals and agents arises due to the information asymmetry by either party. In this case, the management, as the executive of the business activities in firms, has the power to obtain complete information about the firms.

On the other hand, the principals only have a limited amount of information the management provides.

Based on the agency problem framework, the management tends to maximize their interests by utilizing their managerial abilities, which one of the ways is by conducting aggressive tax avoidance (Desai & Dharmapala, 2006; Koester et al., 2017, Lanis & Richardson, 2011). Tax aggressiveness can be defined as an effort to reduce taxable income in the form of tax planning (Lanis & Richardson, 2011). Similarly, Frank et al. (2009) suggest that an aggressive tax report is a derivative of manipulating the taxable income as a tax plan that may be considered fraud in tax evasion. Meanwhile, Garbarino (2011) suggests that tax aggressiveness represents the tax manager’s behavior to reduce the firms’ tax obligation for their interests.

Diversification is one of the management strategies related to aggressive tax management (Aditama, 2016; Ettredge et al., 2006; Gyan et al., 2017; Park & Jang, 2013; Zheng, 2017). Multinational companies, for example, while implementing the diversification strategy as a tool to respond to the competition in the business environment and to improve the managerial skills of the management and brand reputation (Wang et al., 2013; Yang et al., 2017); it is predicted that they exploit gaps and mismatches all countries’ tax systems to commit aggressive tax avoidance.

Several studies have examined the relationship between diversification and tax aggressiveness in firms. Some studies found a negative association between corporate diversification and tax aggressiveness (Husnain et al., 2021; Vahdani et al., 2019). Other studies suggest that corporate diversification enables the firms to engage in earnings smoothing for their particular unit segments (Ettredge et al., 2006; Lewellen, 1971). In addition, diversified firms are more likely to engage in transfer prices among the business segments and areas, which will lead to tax avoidance. Wentland (2016) found that diversified firms in the USA tend to have nonvolatile earnings because diversified firms can successfully distribute the business risk to the business segments. Zheng (2017) also found that diversified firms persistently engage in fewer tax avoidance practices than stand-alone firms. Diversified firms are more likely to have higher complexity of organizational structure (Erickson & Wang, 2007). Therefore, it is expected that diversified firms will have a higher level of information asymmetry than the focused firms because diversified firms may have business segments with different tax treatment from the firms’ main industry. Such a condition enables the diversified firms to get benefits from the firms’ tax plans and arrangements. Wentland (2016) shows that the tax authority finds some tax audit difficulties in diversified firms. Such a condition implies that diversified firms have a lower level of tax obligation than the focused firms (Wentland, 2016). Therefore, it can be concluded that diversified firms have a higher level of information asymmetry than focused firms do, and accordingly, diversified firms tend to arrange aggressive tax planning. Therefore, the following hypothesis is developed:

H1: Diversification strategy has a positive association with tax aggressiveness

This study argues that the firms that engage in global diversification strategy have a higher tax reporting complexity than the locally operating firms. In other words, internationally diversified firms will have a higher level of information asymmetry because internationally diversified firms have dispersed resources in different geographical areas. Consequently, the firms need suitable organizational structures to supervise their operation. Accordingly, it will be difficult for the public or even the analyst to ensure that the firms’ income has been reported appropriately (Jiraporn et al., 2008). Therefore, the firms may engage in tax aggressiveness. Based on the discussion, the development of the hypothesis is as follows:

H1a: International diversification strategy has a positive association with tax aggressiveness

In line with the hypothesis above, industrially diversified firms will have a higher level of information asymmetry than the focused firms since the firms engaged in industrial diversification strategy have several operating segments that may be different from the firms’ core segments, which leads the firms to engage in the tax planning for their operating segments. Therefore, the research proposes the following hypothesis:

H1a: Industrial diversification strategy has a positive association with tax aggressiveness

As discussed earlier, tax aggressiveness is conducted by utilizing the gray areas in tax regulations and tax gaps among countries around the world; hence it is argued to be risky as while there is a possibility of obtaining tax savings in the future, it may also cause higher tax payments in the form of penalties, tax interests, and other punishment due to non-tax compliant activities (Cheng, 2014; Goh et al., 2016; Hanlon et al., 2012; Hutchens & Rego, 2015). Since this risky activity threatens the company in the future, corporate governance, especially board supervision, has a vital role in disciplining the managers so that they do not take risky strategies in managing the company. In the context of Indonesia, where corporate governance follows a two-tier board system, the existence of a board of commissioners as a monitoring board in firms is expected to minimize the agency problem between the principals and the agents. The board of commissioners and their committees in firms are to protect the rights of the owners of the firms. In addition, they prevent any act possibly endangering the owners of the firms. Several studies have found that the board of commissioners may minimize or prevent some kinds of opportunistic actions of the firms’ executives. The research conducted by Busirin et al. (2015) found that the board of commissioners was negatively associated with earnings management. Furthermore, Halioui et al. (2016) and Mulyadi and Anwar (2015) found that the board of commissioners has a negative effect on tax aggressiveness activities. Therefore, in line with the literature, this study argues that the board of commissioners minimizes the harmful management activities; hence, the hypothesis is:

H1a: Board of commissioners’ effectiveness weakens the positive association between diversification strategy firms and tax aggressiveness.

Sample and Data Collection

This research employs the independent variable of diversification strategy by dividing it into international and industrial diversification. This study also examines the effectiveness of the board of commissioners as a moderating variable. These variables associate with the dependent variable of firms’ tax aggressiveness (Current Effective Tax Rate—Current ETR- and Cash ETR). In addition, the research model also employs such control variables as firms’ size, performance (ROA), capital intensity, and leverage. The sample of this research comprises all non-financial public firms listed on the Indonesia Stock Exchange (IDX) from 2014 to 2016. Data were collected for 3 years to identify the movement of the diversification strategy of the public firms in Indonesia during the period before and after the establishment of the ASEAN Economic Community in 2015. The research adopted the purposive sampling technique. Some industries such as property, mining, shipping, and construction are excluded from the sample because those industries have different tax calculations from other sectors. In addition, the sample selection excludes the firms with the negative earning-before-tax, the firms with a negative ETR or a score of ETR higher than one, and the firms that failed to complete the required data. Based on the sampling criteria, the research obtained 82 firms for each year or the total number of 246 firms for the 3 years for further observation.

Model of Research

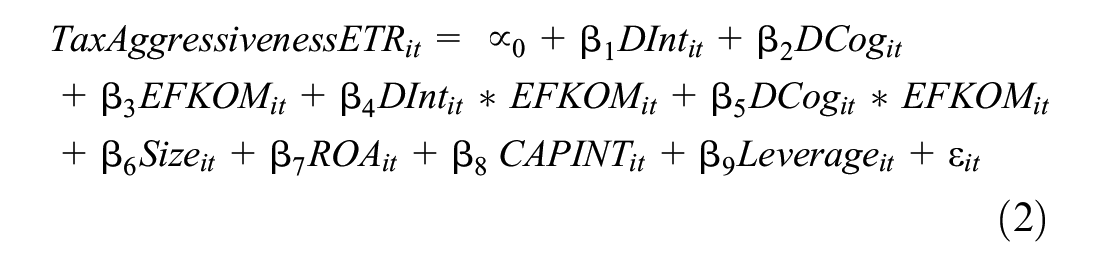

Hypotheses are tested with the model as follows. To measure tax aggressiveness, this study examines two dependent variables: Current ETR and Cash ETR. The Board of commissioners’ effectiveness is the moderating variable in Model 2.

where:

Tax aggressiveness = Measured by Current ETR and Cash ETR

DInt = International corporate diversification

DCog = Industrial corporate diversification

EFKOM = Score of board of commissioners’ effectiveness (Hermawan, 2009)

DInt × EFKOM, Dcog × EFKOM = Interaction between diversification and board of commissioners’ effectiveness

Size = Firms’ capacity (log total assets)

ROA = Firms’ performance (profitability)

CAPINT = Capital Intensity (net Property Plant and Equipment/total assets)

Leverage = Debt rate (long term debt/total assets)

ε = Error

The formula for measuring tax aggressiveness is as follows (Hanlon & Heitzman, 2010).

The proxy of international diversifications is shown below (Gyan et al., 2017):

DInt: 1 if the company’s international sales > 10%

0 if the company’s international sales ≤ 10%

DCog: 1 if the company’s industry segment > 1 segment

0 if the company’s industry segment ≤ 1 segment

Regarding assessing the effectiveness of the board of commissioners, this study follows the scoring of Hermawan (2009) by taking into account factors such as size, activity, independence, and competence of the board of commissioners.

Results and Discussion

Table 1 shows that the mean of Current ETR of non-financial public firms in Indonesia is 0.254627 (25.46%), while Cash ETR has the mean of 0.30193 (30.19%). The rate is higher than statutory corporate income tax in Indonesia (25%). This suggests that on average non-financial public firms in Indonesia did not engage in aggressive tax (compliant with the prevailing regulations). The score is different from the Current ETR because Cash ETR shows current cash taxes paid, considering the taxes paid in previous periods. Therefore, the taxes paid will be higher than the current tax. This indicates ineffective tax management, as the sample companies experience a cash flow management problem. The higher Cash ETR suggests that the companies experience high/significant tax overpaid since, during the year, the companies pay tax more through monthly tax installments and a withholding tax system. The difference between Cash ETR and Current ETR also shows the effect of cash basis and accrual basis in financial statements; tax obligation can be seen in the cash flows report and income statement, that is, cash flow statements reflect a cash basis transaction only while income statement is based on an accrual basis. The mean of the moderating variable of the board of commissioners’ effectiveness (EFKOM) is 38.60163. The score is quite good compared to the median score of EFKOM of 34, obtained from 17 questions of the scoring index multiplied by 2 (median of the Likert scale of the score), representing a fair score. The minimum score is 17, and the maximal score of EFKOM is 51.

Descriptive Statistics.

Note: Current ETR, Cash ETR = proxy of tax aggressiveness; DInt = international corporate diversification; DCog = industrial corporate diversification; EFKOM = score of board of commissioners’ effectiveness; SIZE = firms’ capacity (log natural total assets); ROA = firms’ performance (profitability); CAPINT = capital intensity (net PPE/total assets); LEV = leverage (long term debt/total assets).

Table 2 shows that in 2016, 24 out of 82 observed firms (29%) of non-financial public firms in Indonesia engaged in an international diversification strategy and 68 out of 82 firms (83%) engaged in an industrial diversification strategy. The rate indicates a slight increase from the rate in the year 2014 (before the establishment of AEC), in which 23 out of 82 (28%) non-financial public firms in Indonesia engaged in international diversification strategy, and 66 out of 82 (80%) committed in an industrial diversification strategy.

Corporate Diversification Strategy.

Testing of Model Determination and Classic Assumption

Based on the model determination testing of the Chow and Hausman Test, the appropriate model determination is the Fixed Effect. The classic assumption was also tested to identify the results meeting the assumption of BLUE (Best Linear Unbiased Estimator). The testing results indicate that some variables were found to have multicollinearity problems, and therefore centering treatment is conducted to overcome the problem. After the treatment, all models are free of multicollinearity and autocorrelation. The model testing was also indicated to suffer from the problem of heteroskedasticity. Accordingly, in the regression testing, treatment Robust is required.

Hypothesis Testing

Table 3 shows the regression analysis results in Model 1 using the proxies of Current ETR and Cash ETR. The results suggest that the international diversification strategy negatively affects Current ETR but is insignificant with Cash ETR. The results that the international diversification strategy decreases the value of Current ETR suggest that diversified international companies conduct tax aggressiveness. Table 3 also presents that industrial diversification strategy is positively associated with corporate tax aggressiveness proxied by Cash ETR but not significant with Current ETR. The results that industry diversification strategy increases the value of Cash ETR suggests that industry diversified companies experience ineffective tax management as industrial diversification strategy leads to an increase in Cash ETR.

Results of Model 1 (Current ETR and Cash ETR).

Note: Current ETR, Cash ETR = proxy of tax aggressiveness; DInt = international corporate diversification; DCog = industrial corporate diversification; EFKOM = Score of board of commissioners’ effectiveness; SIZE = Firms’ capacity (log natural total assets); ROA = Firms’ performance (profitability); CAPINT = Capital Intensity (net PPE/total assets); LEV = leverage (long term debt/total assets).

Significant level at 1%. **Significant level at 5%. *Significant level at 10%.

The findings on international diversification strategy confirm Wentland (2016) and Aditama (2016) which further suggests that companies conducting global diversification strategy have lower tax obligations and more aggressively engage in tax avoidance. Indonesian companies which operate international diversification conduct very effective tax management as indicated by one of the following possibilities: the total taxable income (worldwide income) was relatively much lower (indicating income shifting), deductible tax expenses are relatively higher, or pretax book income is relatively higher compared to taxable income; hence, ceteris paribus, this causes lower current income tax expense and high ETR. Furthermore, the results indicate that geographically diversified firms have a complex structure. Hence, it will be more difficult for the public or even the analysts to ensure the reliability of the firms’ reports. The findings also indicate the presence of asymmetric information between the managers and the readers of financial statements.

On the other hand, the industrial diversification strategy leads to increasing cash tax paid. This finding confirms previous studies such as Zheng (2017), which found that firms with industrial diversification strategies are less likely to engage in tax avoidance than stand-alone firms. The results also suggest two conditions. Firstly, industrial competition (market mechanisms) effectively suppresses information asymmetry. Therefore, the firms have no loophole to engage in tax aggressiveness. It also indicates ineffective tax management. As found by Lang and Stulz (1994) and Berger and Ofek (1995), the shares of diversified firms are usually traded at a diversification discount. It is assumed that industrially diversified firms have failed to transfer the business risks to other operating segments owned by the firms since the management of firms with diversification strategies requires knowledge about the limits allowed for the firms to engage in diversification. When the firms fail to appropriately determine the limit of diversification, it will affect their performance (Nayyar, 1993).

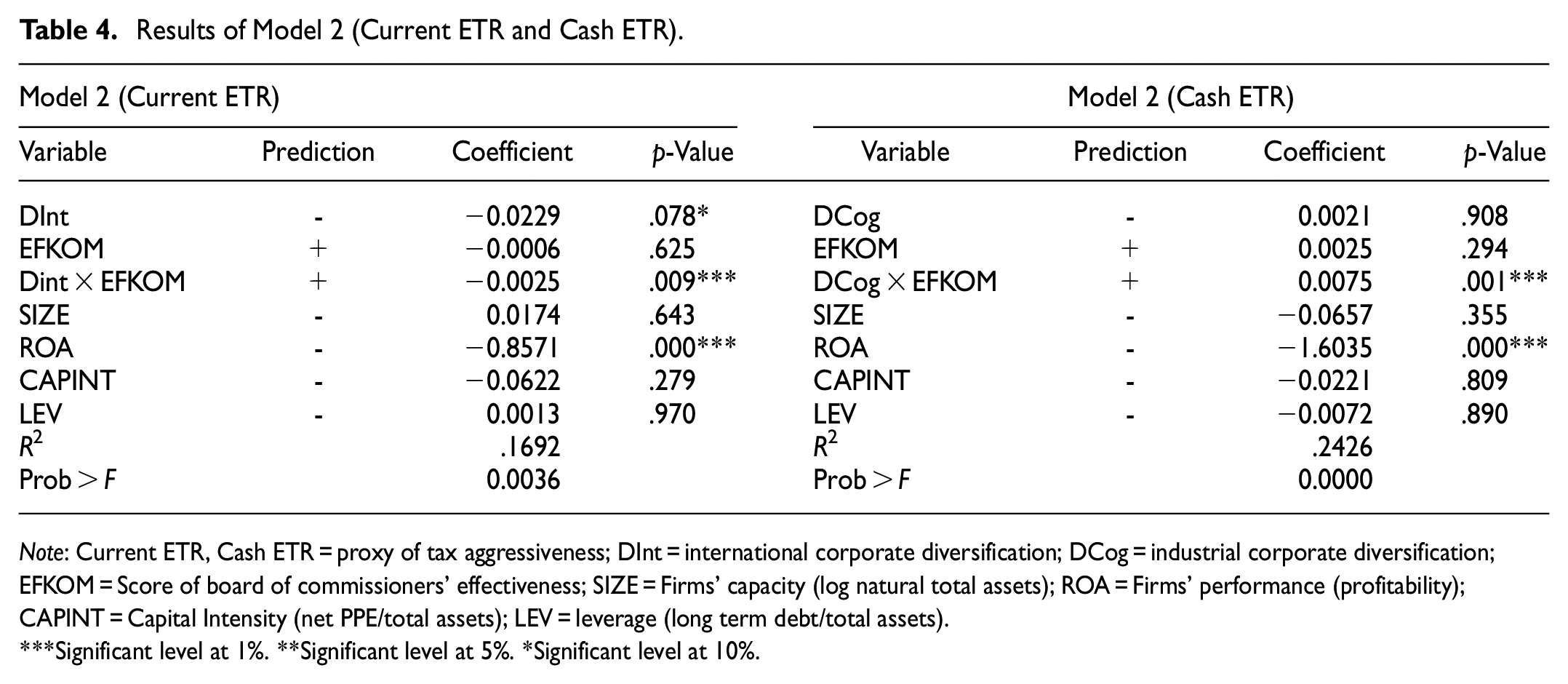

Table 4 shows that the effectiveness of the board of commissioners strengthens the association between diversification strategy and tax aggressiveness. In the context of an international diversification strategy, the board of commissioners strengthens the corporate tax aggressiveness. This finding contradicts the hypothesis that suggests the board controls (moderates) the tax aggressiveness. This can be explained due to the condition that firms in Indonesia are characterized by familial ownership (Claessens et al., 2000). In family firms, many family members or affiliated relatives may hold the positions in the structure of the board of commissioners or the executives of the firms.

Results of Model 2 (Current ETR and Cash ETR).

Note: Current ETR, Cash ETR = proxy of tax aggressiveness; DInt = international corporate diversification; DCog = industrial corporate diversification; EFKOM = Score of board of commissioners’ effectiveness; SIZE = Firms’ capacity (log natural total assets); ROA = Firms’ performance (profitability); CAPINT = Capital Intensity (net PPE/total assets); LEV = leverage (long term debt/total assets).

Significant level at 1%. **Significant level at 5%. *Significant level at 10%.

Consequently, the board of commissioners cannot serve as effective supervisors for the performance of the firms (managers). In addition, internationally diversified firms have more complicated reporting and taxation systems than locally operating firms (Jiraporn et al., 2008). Such conditions will result in a higher level of asymmetric information in the firms with an international diversification strategy. Therefore, it will be difficult for the public, analysts and the board of commissioners to supervise the tax aggressiveness activities in the firms.

In the context of an industrial diversification strategy, the board of commissioners strengthens the ineffective corporate tax management. This finding suggests the poor performance of the supervisory board as, ideally, the role of the monitoring board is to control corporate tax aggressiveness, as found in companies with international diversification strategies. Since tax aggressiveness may lead to risks in the future, such as a company’s bad reputation and tax penalty/sanction (Goh et al., 2016), the board should advise the management to conduct proper tax management so that the company’s tax management is not wasting the company’s resources. The finding on the board of commissioners’ effectiveness overall confirms the Asian Development Bank (2014), which found a minimal score of the board of commissioners in the assessment of Corporate Governance in Indonesia. The position of Indonesia is still below other countries of ASEAN, such as Singapore, Malaysia, and Thailand.

The result of controlling variables that shows ROA has a positive association with tax aggressiveness is consistent with Frank et al. (2009), suggesting that the firms with large profits will have more considerable resources. They can use tax deductions and credits to decrease the tax tariff. In addition, the firms with a high level of profitability will be more flexible in developing structured tax management to ensure the efficiency of tax payment by employing people with reliable expertise and skills (tax consultants).

Conclusion, Implications, Limitations, and Suggestions for Future Studies

This research has two main purposes. It identifies the effect of the diversification strategy of firms on tax aggressiveness activities. In addition, it examines whether the board of commissioners’ effectiveness affects the relationship between the diversification strategy of the firms and tax aggressiveness activities. The sample of this research comprises all non-financial public firms listed on the Indonesia Stock Exchange (IDX) from 2014 to 2016. With a purposive sampling technique, the study obtained 246 observations.

Based on the results, it is found that the firms with an international diversification strategy have a positive and significant effect on tax aggressiveness activities as measured by Current ETR. On the other hand, industrial diversification strategy is found to have a negative effect on tax aggressiveness activities as measured with Cash ETR. This negative effect indicates two conditions: the effective industrial competition (market mechanisms), which suppresses information asymmetry; hence, the firms do not have any loophole to engage in tax aggressiveness. Secondly, it may indicate ineffective tax management. The findings also suggest a poor performance of the board of commissioners as in the context of international diversification strategy where companies conducting tax aggressiveness, the board strengthens this practice. This may lead the company to face risks in the long term, such as a bad image and tax penalties/sanctions. In ineffective tax management, as found in companies with an industrial diversification strategy, the board does not attempt to control the management that wastes the company’s resources due to paying higher cash.

The results of this study suggest that while diversified international companies and industrial diversification face fierce market competition, the diversified international companies have more dispersed resources in different geographical areas. Hence, they will have a higher level of information asymmetry. The companies also need suitable organizational structures to supervise their international operation. Accordingly, it will be difficult for the public or even the analyst to ensure that the firms’ income has been reported appropriately (Jiraporn et al., 2008). There is also a possibility that the multinational companies exploit the tax gaps among countries, so that enable to avoid the tax. As the information asymmetry is high, the tax aggressiveness may not be detected by the owners. These characteristics, that is, dispersed resources in different geographical areas with different tax regulations, are found in the diversified international companies so that they are more able to conduct tax avoidance than the diversified industrial companies.

The findings of this study bring some practical implications; firstly, the government needs to evaluate its tax policy since international diversification strategy conducted by a company may lead to corporate tax aggressiveness. Results of the industrial diversification strategy suggest the tax authority assess tax policy in the industry, such as creating more tax benefits or incentives stimulating the business practice and attracting investors. The findings also contribute to business practitioners that business strategy chosen by executives should be congruent with tax management strategy and vice versa so that the companies can maximize company value and fulfill the stakeholders’ expectations. This study provides theoretical contributions by giving empirical evidence on the ineffectiveness of the supervisory board as one of the internal governance mechanisms that discipline the manager as explained by the agency theory in the context of family companies’ characteristics in a country such as Indonesia.

This study recognizes its limitations that need to be considered in future studies. This study cannot find the effectiveness of the supervisory board in reducing tax aggressiveness. Therefore, the future research can examine other variables related to the board effectiveness such as the effect of board incentives (i.e., as found by Desai & Dharampala, 2006) as one of the scores of the effectiveness of the board, especially in the family-owned enterprises in East Asia including Indonesia (Claessens et al., 2000). It is also recommended that this study be extended by examining the monitoring role of the board in related to aggressive tax planning as stated in OECD (2015) Principles of Corporate Governance. The tax aggressiveness study can also analyze the effect of the Common Reporting Standard (CRS) and other current initiatives related to financial sector reforms to minimize aggressive tax avoidance and BEPS activities which at the end to achieve macroeconomy stability and economic growth of all countries in the region. Finally, the future study can examine the regional case study by collecting data from other ASEAN countries so that the establishment of the ASEAN Economic Community (AEC) in 2015 brings economic benefits not only to companies but also to other stakeholders such as the relevant governments, the customers, and all community. Moreover, the vision of having an AEC by 2025 can be achieved if that AEC is highly integrated and cohesive, competitive, innovative and dynamic, with enhanced connectivity and sectoral cooperation; and a more resilient, inclusive, and people-oriented, people-centered community, integrated with the global economy.

Footnotes

Author Note

This article is a revised and expanded version of a paper entitled “The Effect of Board Effectiveness on The Relationship Between Diversification and Tax Aggressiveness” presented at “The thirteenth New Zealand Management Accounting Conference,” Wellington, New Zealand, 21–22 November 2019.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the research funding from the research grant: PUTI Q1 Universitas Indonesia (research funding: NKB-371/UN2.RST/HKP.05.00/2022).

Ethical Approval

An ethic statement is not applicable because the study is based in secondary data.