Abstract

This study examines the influence of organizational characteristics on the agility of tax-planning decision-making by the Korean business groups known as chaebols. Using South Korea’s transition from a worldwide to territorial tax system in 2023 as a quasi-exogenous shock, a triple-differences analysis shows that Korean multinational corporations (MNCs) engaged in tax-arbitrage transactions by significantly increasing tax-motivated income shifting and dividend payouts following the reform. In addition, chaebol MNCs were less responsive than non-chaebol MNCs. The results suggest that the complex and hierarchical organizational structures of chaebols hinder swift strategic adjustments in response to tax-policy changes, consistent with strategic agility theory. This study is the first to empirically examine the impact of South Korea’s transition from a worldwide to territorial tax system. In addition, it provides an interdisciplinary contribution to relevant literature by integrating the management theory of strategic agility and international taxation.

Plain Language Summary

This study investigates how large Korean business groups, known as chaebols, respond to changes in tax policy. In 2023, South Korea changed its tax system so that income earned by multinational companies (MNCs) abroad would no longer be taxed again when repatriated to Korea. This policy change created new opportunities for MNCs to reduce their tax burden by shifting profits to low-tax countries and bringing them back as dividends. The study finds that, after the reform, many MNCs took advantage of this tax saving opportunity instead of expanding domestic investment. In addition, chaebol MNCs were less responsive than non-chaebol MNCs. These results suggest that the complex and hierarchical organizational structures of chaebols limit their ability to act quickly in response to policy changes. This study is the first to empirically examine the impact of South Korea’s tax policy reform. It also contributes to interdisciplinary literature by linking management theory with international taxation.

Introduction

Large Korean business groups, known as chaebols, are distinct from ordinary “big” corporate groups. The ownership structures of chaebols are characterized by pyramidal hierarchies and complex cross-shareholding networks, making them significantly more intricate than typical conglomerates (Bae et al., 2002; Bae & Jeong, 2007; Baek et al., 2004; Jung et al., 2009). A substantial body of literature examines these organizational characteristics and their implications for firm behavior and decision-making (La Porta et al., 1998; Ahn et al., 2025; Claessens et al., 2000, 2002; Kim, 2025; Lee & Lee, 2025; Oh & Park, 2001). In the context of tax avoidance, prior studies consistently find that chaebols engage in more aggressive tax strategies than non-chaebols, often by making opportunistic decisions and leveraging group-level advantages (Jung et al., 2009; Kang & Kim, 2021; Park, 2018). However, the complex, hierarchical organizational structure of chaebols may significantly constrain their ability to make swift decisions (Doz & Kosonen, 2010; Gopalan et al., 2007; Khanna & Yafeh, 2007; Miller et al., 2011; Minichilli et al., 2016; Mueller-Saegebrecht & Walter, 2025). Since tax avoidance results from strategic corporate decision-making, it cannot be assumed that chaebols always pursue the maximization of after-tax profits swiftly and efficiently. Therefore, careful consideration is required before generalizing that chaebols engage in higher levels of tax avoidance than non-chaebols across all contexts.

In 2023, South Korea transitioned from a worldwide tax system to a territorial tax system for international corporate taxation. Under the previous worldwide tax regime, foreign income repatriated by a multinational corporation (MNC) from its foreign affiliates to the Korean parent company in the form of dividends was subject to additional taxation in South Korea at the time of repatriation. Consequently, if the foreign income was remitted from a low-tax jurisdiction, the MNC faced an additional tax burden on the repatriated income. By contrast, under the territorial tax system implemented in 2023, foreign income repatriated from foreign affiliates is exempt from Korean corporate tax. This reform substantially increased the incentives for Korean MNCs to repatriate more foreign income. Furthermore, the reform enabled MNCs to shift profits to low-tax jurisdictions and subsequently repatriate those profits as dividends without incurring additional taxation in South Korea. That is, the transition created new strategic opportunities for tax arbitrage. As a result, novel tax-motivated income-shifting and dividend-payout strategies became viable under the territorial tax regime.

The legislative amendment for this reform was discussed and passed within a relatively short timeframe in 2022, raising the possibility that not all MNCs were able to promptly design and execute tax strategies in response to the regime change. This context raises the critical research question of whether chaebol firms were able to swiftly adjust their tax planning in response to this policy shock. Thus, South Korea’s 2023 transition to a territorial tax system offers a unique empirical setting to assess how the distinct organizational structure of chaebols influences their responsiveness to policy changes that demand swift tax planning.

To answer this question, this study first investigates whether Korean MNCs engaged in greater tax-motivated income shifting and dividend payouts than non-MNCs following the transition to the territorial tax system in 2023. This initial analysis aims to establish whether the reform influenced the cross-border tax-planning strategies of MNCs. Building on this evidence of strategic tax responses, the study then turns to the core question of whether chaebol MNCs responded differently from non-chaebol MNCs in this high-stakes, time-sensitive policy environment.

A panel dataset of 239,484 Korean firm-year observations of both MNC and non-MNCs from 2014 to 2024 is analyzed. Because this study aims to examine how the tax-motivated behaviors of MNCs and chaebols differed from those of non-MNCs and non-chaebols, respectively, following the tax reform, a triple-differences approach is used. This method exploits the variation in tax incentives to isolate differential responses to the reform across firm types and time periods.

The empirical results yield two key insights. First, MNCs increased tax-motivated income shifting and dividend payouts after the 2023 tax reform, actively leveraging tax-arbitrage opportunities created by the new territorial system. Second, despite similar incentives, the responses of chaebols were significantly weaker than those of non-chaebols. Their slower adjustment suggests that organizational rigidity due to complex hierarchies and internal coordination costs hindered the ability of chaebols to swiftly realign tax strategies in a time-sensitive environment. A series of robustness and supplementary analyses confirms that these findings are not driven by sample imbalance, timing issues, or alternative interpretations. Collectively, the results highlight how chaebols’ unique governance structures may limit strategic agility, even when tax-saving opportunities are apparent.

This study provides several contributions to academics, practitioners, and policymakers. First, it contributes to the literature by moving beyond an assessment of the overall tax-avoidance level of chaebols. It offers a novel perspective by examining how the organizational features of chaebols affect their tax-planning responses in the context of a quasi-natural experiment. Chaebols implement tax-planning strategies by leveraging shared resources and internal capital. The prior literature has predominantly focused on their aggressive tax-avoidance behavior, but this study provides a more nuanced perspective on this behavior by demonstrating that chaebols may respond slowly in situations that demand agile and flexible decision-making.

Second, this study is the first to empirically examine the impact of South Korea’s transition from a worldwide to territorial tax system. Prior research documents how the transitions in countries such as the UK, Japan, and the US affected the tax-motivated income-shifting and repatriation behavior of MNCs. This study extends and strengthens this literature by providing evidence from South Korea. Moreover, by examining the interplay between tax-motivated income shifting and dividend payouts, the study further broadens the literature by capturing the full scope of tax-arbitrage behavior.

Last, this study suggests that the decision-making of chaebols can be complex and bureaucratic, highlighting that internal managers and practitioners need to enhance organizational agility and governance efficiency. In particular, flexible and responsive decision-making processes may be essential for chaebols to adapt effectively to environments that demand rapid strategic adjustments. These findings have important implications for policymakers, as they indicate that firms do not respond uniformly to policy changes. There may be notable heterogeneity not only between MNCs and non-MNCs but also between chaebol and non-chaebol MNCs, underscoring the need for targeted, differentiated policy approaches that reflect the diverse behavioral responses of different types of business groups.

The remainder of this study is organized as follows. Section 2 reviews the relevant background and develops the hypotheses. Section 3 describes the sample and explains the research design. Section 4 reports and discusses the results of the hypothesis testing and a series of robustness and additional tests. Section 5 provides the conclusions and limitations of the study.

Background and Hypotheses

Background of Worldwide and Territorial Tax Systems

There are two types of tax systems for taxing foreign-source income earned by foreign subsidiaries of MNCs: worldwide and territorial. Under a worldwide tax system, foreign-source income is taxed by the home country when it is repatriated to the parent company. If a foreign subsidiary located in a low-tax jurisdiction remits its income to the parent company headquartered in a high-tax jurisdiction in the form of dividends, the remitted dividends become subject to the higher tax rate of the home country. As a result, the MNC incurs additional taxes, commonly referred to as repatriation taxes. By contrast, a territorial tax system exempts foreign-source income from home-country taxation upon repatriation. That is, once the income is taxed in the foreign jurisdiction, no additional tax is imposed when the income is remitted to the parent company as dividends.

Under a worldwide tax system, MNCs have strong incentives to retain foreign-source income abroad as undistributed earnings in order to defer repatriation taxes. The reduction in repatriated dividends undermines domestic investment in capital and research and development (Egger et al., 2015; Hasegawa, 2023; Hasegawa & Kiyota, 2017). MNCs subject to a worldwide tax system face competitive disadvantages compared to MNCs in countries with territorial tax systems due to a higher tax burden and resource misallocation (Kohlhase & Pierk, 2020). Moreover, a worldwide tax system incurs substantial administrative and compliance burdens, as it typically requires a complex foreign tax-credit mechanism to eliminate double taxation on repatriated dividends. For these reasons, several countries have shifted from a worldwide to a territorial tax system, including the UK and Japan in 2009 and the US in 2018. To encourage dividend repatriation, South Korea transitioned from a worldwide to a territorial tax system in 2023 by introducing a 95% exemption on dividends repatriated from foreign subsidiaries. The transition in South Korea was implemented relatively quickly: the issue was first added to the public agenda and discussed by the Presidential Transition Committee of the Korean government in May 2022, and the reform was legislated in corporate tax law on December 31, 2022. Given the limited flexibility of MNCs in adjusting their income-shifting strategies (Hopland et al., 2018), it is likely that tax planning under the new regime required MNCs to rapidly analyze their tax burden and make swift strategic decisions. Therefore, this tax reform not only provides a quasi-natural experiment to examine the impact of tax-policy changes on MNCs but also serves as a quasi-exogenous shock enabling an investigation of how the organizational characteristics of chaebols affect time-sensitive decision-making.

Hypothesis Development

Effect of the Tax-System Transition on Tax-Motivated Income Shifting and Dividend Payouts

According to the principle of capital ownership neutrality, tax policies should not influence or distort the ownership of productive assets across different countries (Desai & Hines, 2003; Devereux, 1990; Dharmapala, 2018). However, in the real world and its significant level of explicit taxes, repatriation taxes affect the location of resources by altering the income-shifting and dividend-payout strategies of MNCs (Blaylock et al., 2022; K. Clausing & Shaviro, 2010; Desai et al., 2001; Dyreng et al., 2015; Fritz Foley et al., 2007; Harris & O’Brien, 2025; Hines, 1996; Nessa, 2017).

A substantial body of empirical research has reported a negative association between repatriation and repatriation taxes (Altshuler & Newlon, 1993; Desai et al., 2001; Nessa, 2017). That is, the burden of repatriation taxes hinder MNCs from repatriating foreign income to the home country. By eliminating repatriation taxes, a transition to a territorial tax system is expected to increase dividend payouts to the parent companies of MNCs. Consistent with this expectation, Egger et al. (2015) and Hasegawa & Kiyota (2017) find that foreign affiliates in the UK and Japan, respectively, increased dividend payments to their parent companies following these countries’ shifts from a worldwide to a territorial tax system. Douidar and Sutton (2024) also find that MNCs with high foreign sales substantially increased dividends per share after the US transition to a territorial system under the Tax Cuts and Jobs Act (TCJA).

However, the transition in the tax system is expected to promote more sophisticated changes in tax planning than simply an increase in dividends. Langenmayr and Liu (2023) and Hasegawa (2023) provide empirical evidence that following tax reforms, UK and Japanese MNCs shifted more income from parent companies in higher-tax jurisdictions to foreign subsidiaries in lower-tax jurisdictions in order to minimize their overall tax liabilities. K. A. Clausing (2020) also notes that the US transition to a territorial system is likely to increase profit shifting to foreign affiliates despite anti-abuse provisions in the TCJA such as the global intangible low-taxed income (GILTI) regime, which is designed to curb excessive shifting of income from the US to foreign tax havens. These findings imply that MNCs adopt proactive tax strategies to fully exploit the tax saving opportunities arising from a new tax system. Such incentives may even lead to tax arbitrage transactions of shifting income out to low-tax foreign affiliates and repatriating that income as dividends, thereby avoiding high domestic taxation in the home country (Yoo & Choi, 2018).

This study examines whether Korean MNCs with foreign affiliates engaged in greater tax-motivated income shifting and, consequently, tax-motivated dividend payouts than non-MNCs following the transition to a territorial tax system. This study differs from prior research in UK, Japan, and US settings in several ways (e.g., K. A. Clausing, 2020; Douidar & Sutton, 2024; Egger et al., 2015; Hasegawa, 2023; Hasegawa & Kiyota, 2017; Langenmayr & Liu, 2023). First, while other countries transitioned to a territorial system prior to 2020, South Korea’s transition occurred in 2023. This transition coincided with the recent wave of international tax reforms, including Base Erosion and Profit Shifting (BEPS) measures and the introduction of global minimum taxes, creating an opportunity to empirically examine how MNCs respond to tax reform within an evolving multilateral tax framework. Second, this study is the first to identify tax-arbitrage strategies by simultaneously examining both tax-motivated income shifting and tax-motivated dividend payouts in the context of a major tax reform. Accordingly, the first hypothesis is as follows:

Tax-Motivated Income-Shifting and Dividend-Payout Behaviors of Chaebols

After examining the effects of the change in tax regimes on the behavior of MNCs through the first hypothesis, this study now turns to the central research question: whether the organizational characteristics of chaebols led to differences in the degree to which tax-arbitrage strategies were employed compared to non-chaebols.

Chaebols are distinct in both ownership and governance structure. They are predominantly family-controlled. They also exhibit high concentrations of both ownership and control, often accompanied by a substantial divergence between cash flow rights and control rights (Ahn et al., 2025; Claessens et al., 2000; Faccio et al., 2001). Unlike US conglomerates or business groups in other countries, chaebols operate through pyramidal ownership structures and extensive cross-shareholding networks (Bae et al., 2002; Baek et al., 2006; Claessens et al., 2002). From the perspective of dynamic capability theory (Choo, 2025; Teece, 2007; Teece et al., 1997), chaebols’ tightly connected ownership structures and internal capital markets can be viewed as valuable organizational resources that enhance their ability to exploit opportunities. Specifically, their group-level advantages, such as shared resources, accumulated experience and technology (Khanna & Rivkin, 2001), economies of scale (Gaur et al., 2014), greater access to internal and foreign capital, and lower foreign operating costs, enable them to pursue unified strategies. Indeed, a number of previous studies consistently find that chaebols engage in more aggressive tax strategies than non-chaebol firms by utilizing their internal resources to serve the interests of controlling shareholders. Jung et al. (2009) show that chaebols are more actively involved in income shifting, while Kang & Kim (2021) find that the positive association between international diversification and tax avoidance is significantly stronger among chaebols than among non-chaebols. Similarly, Park (2018) reports that chaebol affiliates exhibit higher levels of tax avoidance through related-party transactions, although this behavior decreased following the implementation of the Unfair Related Party Transactions Tax Law. These studies demonstrate that the unique ownership structures of chaebols allow controlling shareholders to make opportunistic decisions that may expropriate minority shareholders (Bae et al., 2002; Johnson et al., 2000; La Porta et al., 1998).

However, according to strategic agility theory (Doz & Kosonen, 2010; Mueller-Saegebrecht & Walter, 2025), the same organizational characteristics that offer strength in execution can also inhibit adaptability in the face of sudden environmental changes. Compared with decentralized non-chaebol MNCs, the hierarchical, family-centered governance of chaebol MNCs may generate coordination frictions and slow the decision-making process (Gopalan et al., 2007; Khanna & Yafeh, 2007). Research on family firms also suggests greater tendencies toward risk aversion and conservatism in their strategic choices, which limit their ability to act decisively in time-sensitive contexts (Miller et al., 2011; Minichilli et al., 2016). Because tax planning demands timely adaptation to a given environment (Dyreng et al., 2015; Kohlhase & Pierk, 2020), these constraints are especially salient when facing unexpected policy changes that require rapid adjustment, such as Korea’s 2023 transition to a territorial tax system. In this regard, chaebols may be less agile than non-chaebol firms when responding to a shift in the international tax system that demands swift restructuring of global income-shifting and dividend strategies.

In summary, it remains an open empirical question whether, following the transition, chaebols engaged in greater tax-motivated income shifting and dividend payouts by making responsive decisions utilizing their internal capital—consistent with dynamic capability theory—or engaged less in such behavior due to coordination frictions and internal bureaucracy, supporting strategic agility theory. Consequently, the second hypothesis is non-directional:

Figure 1 illustrates the hypothesized relationships by which the 2023 tax reform is expected to influence the tax-motivated behavior of Korean firms.

Conceptual Framework of Research Hypotheses.

Research Method

Data

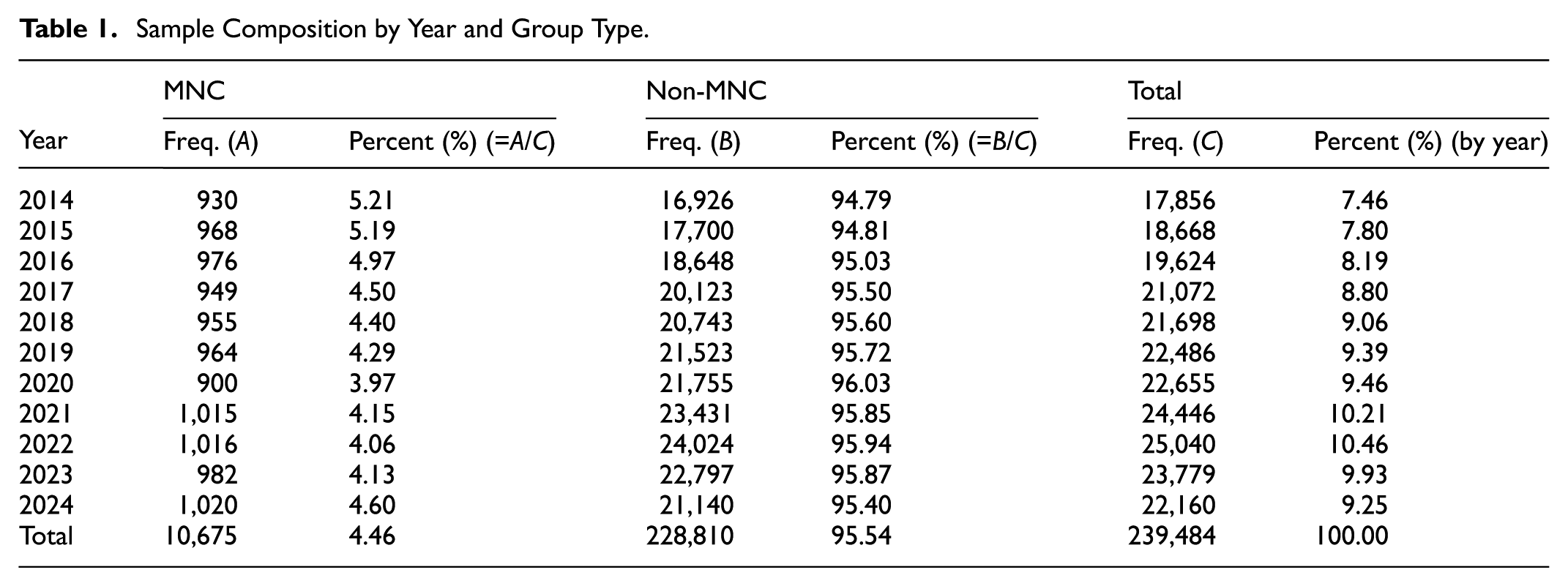

This study uses ownership and financial data on both MNCs and non-MNCs in Korea. First, ownership data are obtained from Moody’s Orbis database, which provides detailed information on the ownership structures of firms. Specifically, Korean parent companies and their domestic affiliates are identified. For MNCs, information on foreign affiliates is further obtained. Second, for MNCs, the geographic locations of the overseas affiliates are used to construct a tax-incentive variable, which is calculated as the average corporate tax-rate differential between the Korean parent company and its foreign affiliates. This tax-rate differential measures the incentives of MNCs to shift income from higher-tax jurisdictions to lower-tax jurisdictions for tax saving purposes. Last, financial data are collected from the Value Search database provided by NICE Information Service, which offers detailed firm-level financial statements of Korean firms. The final sample comprises an unbalanced panel of 239,484 firm-year observations from 33,646 Korean firms over the period 2014 to 2024. Table 1 presents the sample distribution by year and group type (i.e., MNC and non-MNC). With the exception of a temporary decrease in 2023, the number of firm-year observations gradually increases over time. MNC firm-year observations account for approximately 4.5% of the total observations.

Sample Composition by Year and Group Type.

Research Model

Tests of Hypothesis 1

The empirical model is based on the income-shifting framework developed by Hines & Rice (1994) and extended by Huizinga & Laeven (2008), which is widely applied in international tax research. The approach assumes that a firm’s reported pre-tax income measured as the logarithm of profit or loss before tax (PLBT) consists of both “true” income generated from capital and labor inputs and “shifted” income arising from tax-motivated income shifting. True income is typically proxied using the logarithm of tangible fixed assets (FA) and the logarithm of compensation expenses (COMP). Tax incentives for income shifting are captured through the variable TI, which is calculated as the average tax rate difference between the parent firm and its foreign affiliates. Specifically, TI is calculated as the statutory tax rate of the parent company minus that of the foreign affiliate. A positive (negative) TI indicates that the parent company is located in a higher (lower) tax jurisdiction than the foreign affiliate. Since tax-motivated income shifting refers to the shifting of profits from high-tax to low-tax jurisdictions, a negative coefficient on TI provides evidence consistent with tax-motivated income shifting. MNC is an indicator variable equaling 1 if a firm is a parent company of an MNC that owns more than one foreign affiliate with an ownership stake exceeding 50% and 0 otherwise. POST is an indicator variable equaling 1 if the year of the observation is 2023 or later and 0 otherwise. Since this study predicts that MNCs engaged in more tax-motivated income shifting following the transition to a territorial tax system in 2023, the triple-interaction term MNC × TI × POST is used to capture the combined effects of multinational status, tax incentives, and the post-reform period.

The dependent variable is the natural logarithm of dividend payouts (DIV). The model controls for factors known to influence the dividend-payout decisions of firms (e.g., Hasegawa & Kiyota, 2017; Kinney & Liu, 2018): total assets (TA), leverage ratio (LEV), profitability (ROA), research and development intensity (RD), and the ratio of ownership share held by foreign investors (FRN). Because

Tests of Hypothesis 2

Equations 3 and 4 are nearly identical to Equations 1 and 2, respectively, except that the variable MNC is replaced with CHAEBOL, an indicator variable equaling 1 if the MNC belongs to a chaebol, a business group designated as a “mutual investment restricted group” by Korea’s Fair Trade Commission, and 0 otherwise (Kang & Kim, 2021; Park, 2018). The primary variables of interest in both equations are the triple-interaction term CHAEBOL × TI × POST.

Results

Descriptive Statistics

The empirical analysis uses the sample of 239,484 firm-year observations for the period 2014 to 2024. Table 2 presents the summary statistics for the variables. The mean value of MNC is 0.045, indicating that approximately 4.5% of the total observations are MNCs that hold at least one foreign affiliate with an ownership stake exceeding 50%. The mean value of CHAEBOL is 0.039 in the full sample, and this figure increases to 0.06 when the sample is restricted to MNCs. This suggests that chaebol firms account for approximately 6% of the MNC subsample. The mean value of TI is −0.003, which indicates that, on average, the statutory corporate tax rate of South Korea is 0.3% higher than the statutory tax rates of foreign affiliates. All continuous variables are winsorized at the first and 99th percentiles to mitigate the effects of outliers.

Descriptive Statistics.

Note. All variables are defined in Appendix 1.

Hypothesis Testing

Tests of Hypothesis 1

Table 3 presents the results for

The Effects of Changes in Tax Regimes on Tax-motivated Income Shifting and Dividend Payouts of MNCs (

Note. Column (1) presents the estimation results for Equation 1, which evaluates the impact of Korea’s transition to a territorial system on tax-motivated income shifting among Korean MNCs. Column (2) reports the results for Equation 2, which assesses how the transition influenced tax-motivated dividend payouts by Korean MNCs. For both columns, the tax-motivated behavior of MNCs following the 2023 transition is captured by the coefficient on the triple-interaction term, MNC × TI × POST, which reflects differential changes in tax-motivated behavior in response to the reform across firm types and time periods.

Statistical significance at the 1% level. Standard errors are reported in parentheses below the estimate. All variables are defined in Appendix 1.

The coefficient on the triple-interaction term MNC × TI × POST is negative and statistically significant in Column (1; –0.257, p < .01), indicating that MNCs shifted more income to low-tax jurisdictions after the tax reform. This finding supports

In Column (2), the triple-interaction term MNC × TI × POST is positive and significant (9.994, p < .01), suggesting that MNCs also increased dividend payouts from low-tax affiliates post-reform. This is consistent with

Several prior studies have examined the consequences of transitioning to a territorial tax system, focusing either on income-shifting behavior (e.g., K. A. Clausing, 2020; Hasegawa, 2023; Langenmayr & Liu, 2023) or on profit repatriation (e.g., Douidar & Sutton, 2024; Egger et al., 2015; Hasegawa & Kiyota, 2017). By contrast, this study demonstrates that South Korea’s transition to a territorial tax regime altered MNCs’ tax-planning behavior in a more integrated manner. Specifically, MNCs not only shifted more income to low-tax jurisdictions but also increased the repatriation of foreign profits through dividends. By jointly analyzing income shifting and dividend payouts, this study provides novel empirical evidence of tax arbitrage strategies under a new tax regime. If the increased repatriation is partly driven by outward income shifting for tax arbitrage purposes, the repatriated resources may contribute less than expected to domestic investment. In addition, even if the increase in repatriation has positive effects in the short term, there is a possibility that these effects may not be sustained in the long term, consistent with the findings of Eulaiwi et al. (2024). Therefore, the effects of this tax regime change need to be investigated over the longer term in future research.

Tests of Hypothesis 2

Table 4 presents the regression results for

Chaebol Responses to Tax-Motivated Income-Shifting and Dividend-Payout Strategies (

Note. Column (1) presents the estimation results for Equation 3, which evaluates the impact of Korea’s transition to a territorial system on tax-motivated income shifting among chaebol MNCs. Column (2) reports the results for Equation 4, which assesses how the transition influenced tax-motivated dividend payouts by chaebol MNCs. For both columns, the tax-motivated behavior of chaebol MNCs following the 2023 transition is captured by the coefficient on the triple-interaction term, CHAEBOL × TI × POST, which reflects differential changes in tax-motivated behavior in response to the reform across business-group types and time periods.

, **, and ***Statistical significance at the 10%, 5%, and 1% levels, respectively. Standard errors are reported in parentheses below the estimate. All variables are defined in Appendix 1.

The results provide empirical support for strategic agility theory (Doz & Kosonen, 2010; Mueller-Saegebrecht & Walter, 2025). While chaebols possess numerous structural advantages, their organizational complexity and governance rigidity may impose meaningful constraints in environments requiring agile strategic responses. This interpretation aligns with prior theoretical insights of Khanna & Yafeh (2007) and Gopalan et al. (2007), who emphasize that the hierarchical control, cross-shareholding, and bureaucratic layers inherent to chaebol governance can impair timely coordination. Similarly, Doz & Kosonen (2010) argue that firms with rigid structures are less responsive to external shocks. From a practical perspective, chaebols may be less able to make swift income-shifting decisions in response to sudden tax reforms than non-chaebol MNCs. Chaebols maintain more complex transfer pricing policies, internal debts, royalty payments, and shared services with a larger number of foreign affiliates. Moreover, the presence of numerous stakeholders and shareholders may make it difficult to implement immediate increases in dividend payouts. Such organizational complexity and rigidity are likely to result in a “when big is slow” phenomenon. This pattern underscores the fact that policy changes aimed at influencing corporate behavior should account for the governance characteristics of business groups. Overall, the evidence supports

Robustness Tests

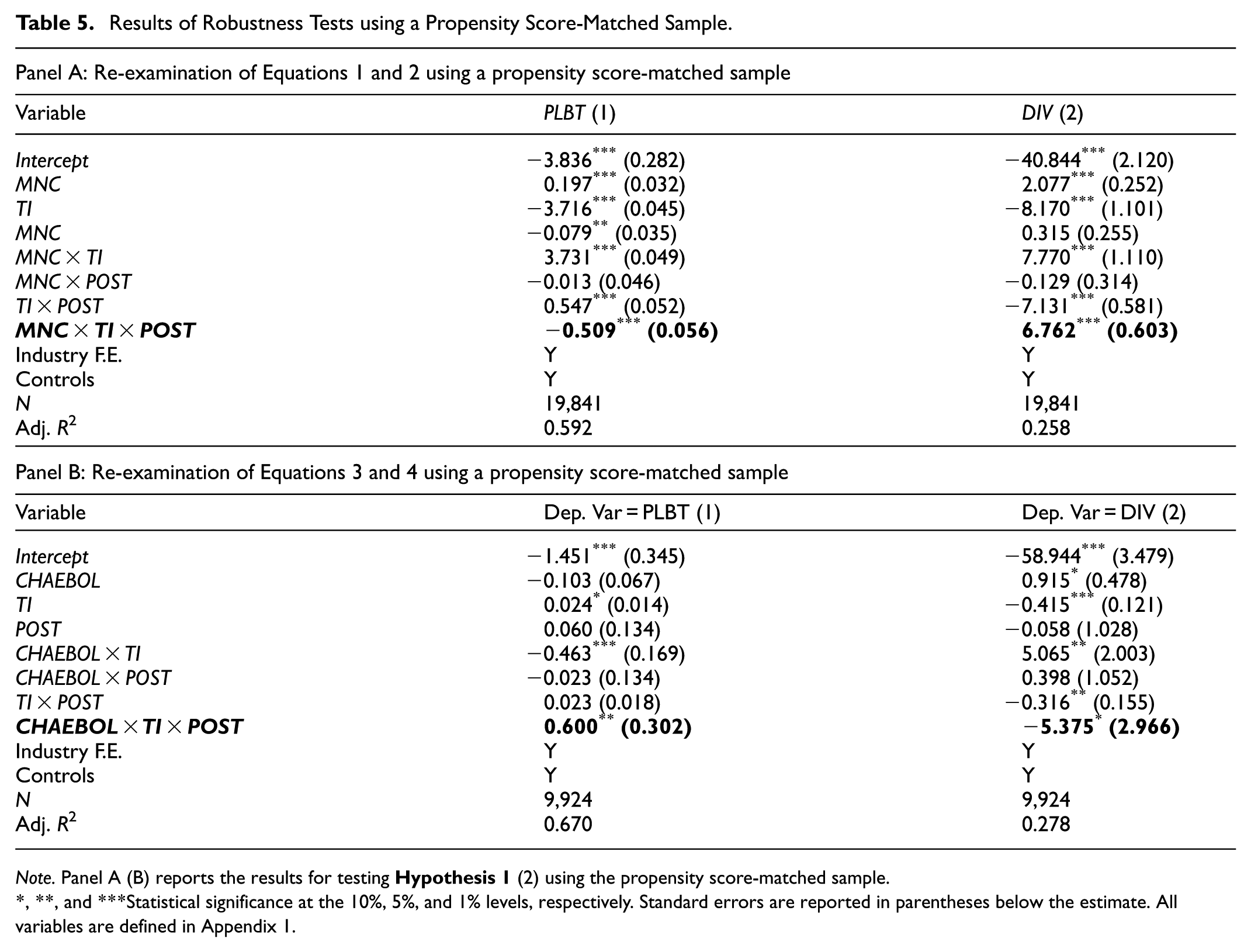

Use of a Propensity-Score-Matched Sample

Among the full sample of 239,484 firm-year observations, only 10,675 are classified as MNCs, highlighting a significant imbalance between MNCs and non-MNCs. This imbalance raises concerns that differences in firm characteristics could bias the estimation results. To mitigate this issue, a robustness check is conducted using propensity score matching (PSM) to create a more balanced and comparable sample. Using 1:1 nearest-neighbor matching without replacement and a caliper of 0.01, MNCs are matched with non-MNCs based on firm size, proxied by total assets (TA). This procedure yields a matched sample of 19,841 firm-year observations for testing

Panel A of Table 5 presents the results of re-estimating Equations 1 and 2 using the matched full sample, while Panel B reports the results of re-estimating Equations 3 and 4 based on the matched MNC subsample. Across all model specifications, the coefficients on the triple-interaction terms remain consistent with those in the main analysis, confirming the robustness of the primary findings to concerns regarding sample imbalance and firm-size heterogeneity.

Results of Robustness Tests using a Propensity Score-Matched Sample.

Note. Panel A (B) reports the results for testing

, **, and ***Statistical significance at the 10%, 5%, and 1% levels, respectively. Standard errors are reported in parentheses below the estimate. All variables are defined in Appendix 1.

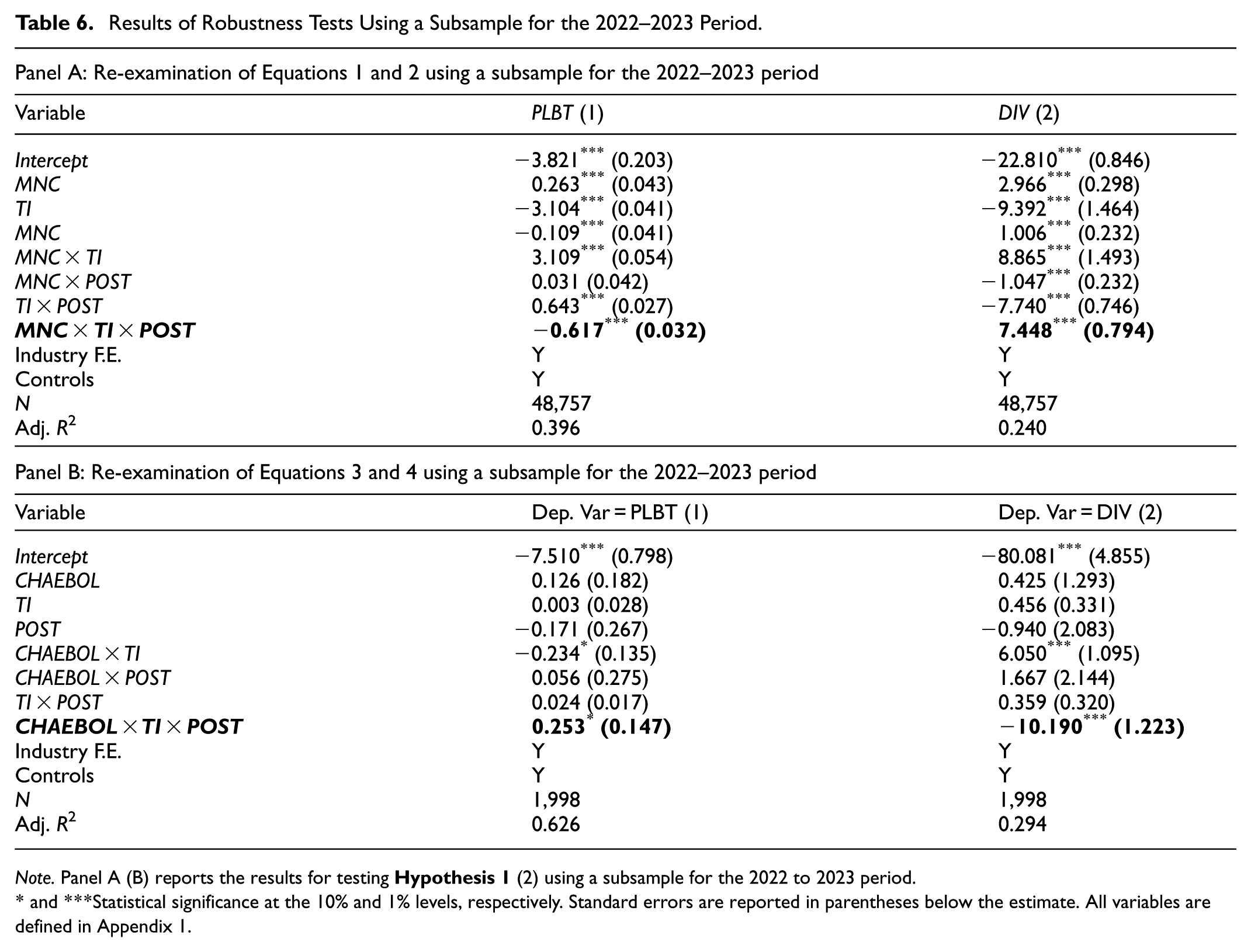

Use of a Narrow Window Around the Tax Reform

The main analysis spans the 2014 to 2024 period, and such a broad time window may dilute the observable impact of Korea’s transition to a territorial tax system. To more precisely isolate the immediate effects of the reform, a robustness check using a restricted sample covering only the years 2022 and 2023 is performed. This narrow window captures the critical period during which firms were most likely to adjust their tax strategies in direct response to the policy shift.

Panels A and B of Table 6 present the regression results for

Results of Robustness Tests Using a Subsample for the 2022–2023 Period.

Note. Panel A (B) reports the results for testing

and ***Statistical significance at the 10% and 1% levels, respectively. Standard errors are reported in parentheses below the estimate. All variables are defined in Appendix 1.

Distinguishing Chaebol Effects From Ownership Concentration

To examine whether the observed chaebol effects are simply driven by high ownership concentration, a robustness check is conducted by replacing CHAEBOL in Equations 3 and 4 with HOLDINGRATIO, defined as the cumulative ownership share of the firm’s top 5 shareholders. This approach allows for a direct comparison of the effects of ownership concentration with those of the broader organizational characteristics uniquely associated with chaebols, such as complex intra-group governance, centralized decision-making, and pyramidal control structures.

Table 7 reports the results. Compared to the results of the main analysis using the CHAEBOL variable, the triple-interaction term HOLDINGRATIO × TI × POST in Columns (1) and (2) exhibits opposite signs and significant magnitudes. That is, MNCs with highly concentrated ownership promptly increased tax-motivated income shifting and dividend payments following Korea’s transition in 2023, unlike chaebol MNCs. These findings suggest that high ownership concentration alone does not drive the tax-planning behavior observed among chaebols. In other words, the distinctive effects attributed to chaebols in the main analysis cannot be explained solely by concentrated ownership.

Results of Robustness Tests on the Distinction Between Chaebols and Ownership Concentration.

Note. Column (1) presents the estimation results for Equation 3, which evaluates the impact of Korea’s transition to a territorial system on tax-motivated income shifting among MNCs with highly concentrated ownership. Column (2) reports the results for Equation 4, which assesses how the transition influenced tax-motivated dividend payouts by MNCs with highly concentrated ownership.

, **, and ***Statistical significance at the 10%, 5%, and 1% levels, respectively. Standard errors are reported in parentheses below the estimate. All variables are defined in Appendix 1.

Visual Robustness Analysis for Chaebol and Non-chaebol MNCs

To provide more intuitive evidence on the behavioral differences between chaebol and non-chaebol MNCs, the following robustness test is performed. First, the baseline regressions in Equations 5 and 6 for tax-motivated income shifting and dividend payouts are estimated separately for each year from 2022 to 2024 and for the two subsamples of chaebol and non-chaebol MNCs.

The estimated coefficients on TI are then illustrated by group type (chaebol vs. non-chaebol) and by year (2022–2024) in plot graphs to offer visual evidence on the difference between chaebol and non-chaebol firms. Panels A and B in Figure 2 provide results for the tax-motivated income shifting and dividend payouts, respectively.

Comparison of Coefficients on TI of Chaebol and Non-chaebol MNCs by Year. Panel (A) Coefficients on TI for the tax-motivated income-shifting baseline model of Equation 5. Notes: A more negative coefficient on TI indicates greater tax-motivated income shifting. Panel (B) Coefficients on TI for the tax-motivated dividend payout baseline model of Equation 6. Notes: A more positive coefficient on TI indicates greater tax-motivated dividend payouts.

In Panel A in Figure 2, where a more negative coefficient on TI indicates greater tax-motivated income shifting, chaebol MNCs exhibit higher coefficients (smaller income shifting) than non-chaebols. The wider gap in 2023 suggests that chaebols became relatively less responsive to tax differentials during this period. In Panel B in Figure 2, where a more positive TI coefficient implies greater tax-motivated dividend payouts, chaebols show smaller coefficients than non-chaebols. The results indicate that chaebols are less likely to adjust their dividend policies in response to tax incentives. Taken together, these results reinforce the findings of the main analysis but with more direct visual evidence.

Year Fixed Effects

The main estimation models do not include year fixed effects, as the analysis focuses on identifying the effect of an exogenous event that occurred in 2023. However, to ensure that the results are not driven by unobserved time-specific factors, all analyses are re-estimated using a triple-differences approach that includes year fixed effects. Although untabulated, the results of the main analysis remain unchanged.

Additional Analysis

Overall Tax Avoidance of Chaebols

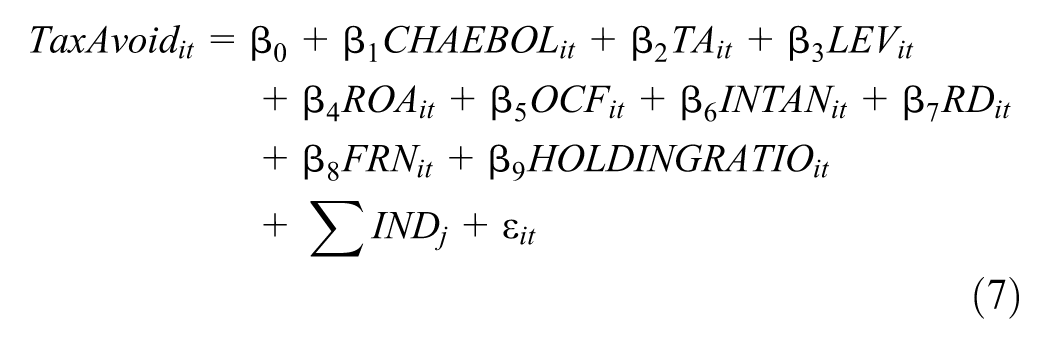

This study provides empirical evidence that chaebols are less effective in situations requiring swift strategic decision-making. However, most prior studies examining the tax avoidance of chaebols, such as Jung et al. (2009), Kang & Kim (2021), and Park (2018), find that they are generally more aggressive than non-chaebols in pursuing tax-avoidance strategies. To further explore this contrast, an additional analysis is conducted to examine the general level of tax avoidance by chaebols in situations that do not require urgent or time-sensitive decision-making. Specifically, the following standard regression model of tax avoidance is estimated using various firm characteristics.

Two alternative measures of tax avoidance are used as dependent variables: TaxAvoid_GETR and TaxAvoid_CETR. The former is based on the ratio of total tax expenses to pre-tax income, while the latter is based on the ratio of cash taxes paid to taxable income. Since a lower effective tax rate indicates more aggressive tax avoidance, both measures are multiplied by negative one to facilitate interpretation. The key explanatory variable is CHAEBOL, and the model includes controls for firm size (TA), leverage (LEV), profitability (ROA), liquidity (OCF), intangible assets (INTAN), R&D intensity (RD), foreign ownership (FRN), and ownership concentration (HOLDINGRATIO).

Table 8 presents the results of this analysis. In both specifications, the coefficient on CHAEBOL is positive and statistically significant, suggesting that chaebols engage in significantly greater tax avoidance than non-chaebols. These results are consistent with prior research highlighting the aggressive tax practices of chaebols under normal circumstances (e.g., Jung et al., 2009; Kang & Kim, 2021; Park, 2018).

Additional Analysis of the Overall Tax Avoidance of Chaebols.

Note. Columns (1) and (2) present the estimation results of the standard tax avoidance model, where the dependent variables are TaxAvoid_GETR and TaxAvoid_CETR, respectively. TaxAvoid_GETR is defined as the ratio of total tax expenses to pre-tax income. TaxAvoid_CETR is the ratio of cash taxes paid to taxable income. The coefficient on CHAEBOL captures the relative level of tax avoidance of chaebol MNCs compared with non-chaebol MNCs.

, **, and ***Statistical significance at the 10%, 5%, and 1% levels, respectively. Standard errors are reported in parentheses below the estimate. All variables are defined in Appendix 1.

Moreover, the results show that other governance-related variables, such as foreign ownership (FRN) and ownership concentration (HOLDINGRATIO), are associated with lower levels of tax avoidance. These findings reinforce the idea that chaebols’ aggressive tax behavior is not simply a byproduct of high ownership concentration but stems from their unique institutional and organizational structure. Taken together, this additional analysis strengthens the interpretation that the weaker performance of chaebols in the main analysis stems not from a lack of willingness to engage in tax avoidance but from constraints in strategic agility when rapid and coordinated decision-making is required.

Effects of the Tax Reform on Investment

To investigate whether the territorial tax system reform in South Korea led to increased domestic investment as observed in the UK following its transition (Liu, 2020), Equation 2 is modified by replacing the dependent variable with firm-level investment. Specifically, two alternative proxies of investment are used: INVEST_ASSET, which captures increases in tangible, intangible, and leased assets, and INVEST_CF, which reflects cash outflows related to investment activities. The control variables are adjusted accordingly to better account for firm characteristics relevant to investment behavior.

As show in the regression results presented in Table 9, the triple-interaction term is negative and statistically significant across Columns (1) and (2). These findings indicate that, contrary to expectations, MNCs did not increase investment following the transition to a territorial tax system. Rather, their investment intensity appears to have declined relative to non-MNCs during the post-reform period, even when accounting for tax incentives for income repatriation.

Additional Analysis of the Effects of Changes in Tax Regimes on Investment.

Note. Columns (1) and (2) present the results on the impact of Korea’s transition to a territorial tax system on domestic investment. In Column (1), the dependent variable is INVEST_ASSET, which measures increases in tangible, intangible, and leased assets. In Column (2), the dependent variable is INVEST_CF, which captures cash outflows associated with investment activities. The coefficient on MNC × TI × POST represents the differential changes in investment behavior in response to the reform across business-group types and over time.

, **, and ***Statistical significance at the 10%, 5%, and 1% levels, respectively. Standard errors are reported in parentheses below the estimate. All variables are defined in Appendix 1.

One possible interpretation is that although repatriated income increased after the reform, these funds were not immediately allocated toward capital investment. This delay may be attributed to the heightened economic uncertainty in South Korea during the observation window, which could have prompted firms to adopt a more cautious stance toward long-term investment decisions.

Conclusion

This study examines how the organizational characteristics of chaebols influence the agility of tax-planning strategies and decision-making. Specifically, South Korea’s 2023 transition from a worldwide to a territorial tax system is leveraged as a quasi-natural experiment. The study finds that MNCs significantly increased both tax-motivated income shifting and tax-motivated dividend payouts to exploit the tax-arbitrage opportunities made possible by the removal of repatriation taxes under the new territorial system. In addition, chaebols were less responsive to this tax-motivated behavior than non-chaebols due to organizational rigidities such as hierarchical decision-making structures, complex intra-group governance, and coordination frictions. These constraints limited their ability to adapt swiftly to the policy change, despite potential tax-saving incentives.

Beyond confirming the behavioral impact of Korea’s territorial tax reform, this study contributes to the literature and policy in several broader ways. First, the findings of this study support a gap between policy objectives and MNC behavior. Dharmapala et al. (2011) observe that the U.S. tax holiday for repatriation provided by the Homeland Investment Act in 2005 did not increase domestic investment, employment, or research and development; only shareholder payouts increased significantly. Consistent with this result, the findings of this study suggest that MNCs primarily used repatriations as a short-term arbitrage tool, even though the transition to a territorial system was intended to encourage domestic investment in capital and research and development. To ensure their policy objectives of investment promotion, policymakers should therefore design tax reforms with mechanisms that suppress short-term arbitrage. Measures such as introducing a reinvestment plan requirement, defining qualified uses of repatriated funds, or anti-abuse provisions that limit purely fiscal arbitrage could be considered. In addition, monitoring of MNCs’ tax-planning strategies by tax authorities should be strengthened.

Second, by linking organizational inertia to tax planning outcomes, the evidence on chaebol behavior extends strategic agility theory. This study is among the first to integrate management theory and international taxation. It demonstrates that the management theory of strategic agility can be applied to explain MNCs’ financial behavior in the context of international taxation. Conversely, the findings enrich international tax research by highlighting that the effectiveness of tax reforms is not solely determined by statutory incentives but is also conditioned by organizational and behavioral factors that drive MNCs’ responsiveness. Therefore, this study builds a conceptual bridge between management and taxation research, expanding the theoretical foundations of both disciplines.

Finally, the study lays the groundwork for future research by emphasizing the need to further integrate management and international taxation perspectives. In an era of global trade tensions and unpredictable tariff regimes, organizational adaptability has become a crucial strategy for sustainability. Future studies should therefore explore how strategic agility shapes MNCs’ responses to complex global tax and trade environments. This research serves as a meaningful starting point for such interdisciplinary extension.

In addition to its multiple contributions, this study has certain limitations. First, a highly precise analysis of income shifting would require detailed financial data for all MNC affiliates (e.g., Huizinga & Laeven, 2008). Due to limitations in data availability, however, this study constructs a tax-incentive variable based on the location information of foreign affiliates and the corresponding statutory tax rates of those jurisdictions. While this proxy approach makes the empirical analysis feasible, the absence of affiliate-level financial data may influence the accuracy of the estimates. Second, the analysis is based on a relatively short post-reform period, which may capture MNCs’ immediate tax responses but not longer-term adjustments in investment or organizational strategies. Third, given the unique institutional and governance features of Korean business groups, the generalizability of the findings to other countries or corporate systems may be limited. Therefore, the empirical results in this study should be interpreted with caution.

Footnotes

Appendix

Variable Definitions.

| Variable | Definition |

|---|---|

| PLBT | is the natural logarithm of profit or loss before tax. |

| DIV | is the natural logarithm of the dividends paid to the parent company. |

| MNC | is an indicator variable equaling 1 if a firm is a parent company of an MNC that owns more than one foreign affiliate with an ownership stake exceeding 50% and 0 otherwise. |

| CHAEBOL | is an indicator variable equaling 1 if the MNC belongs to a business group designated as a “mutual investment restricted group” by Korea’s Fair Trade Commission. |

| TI | is a variable for tax incentives calculated as the average tax rate difference between the parent firm and its foreign affiliates. Tax rate differences are calculated as the statutory tax rate of the parent company minus that of the foreign affiliate. |

| POST | is an indicator variable equaling 1 if the year of the observation is 2023 or later and 0 otherwise. |

| FA | is the natural logarithm of tangible fixed assets. |

| COMP | is the natural logarithm of compensation expenses. |

| TA | is the natural logarithm of total assets. |

| LEV | is the ratio of total liabilities to total assets. |

| ROA | is the ratio of profit or loss before tax to total assets. |

| RD | is the ratio of research and development expense to total assets. |

| FRN | is the ratio of ownership share held by foreign investors. |

| HOLDINGRATIO | is the cumulative ownership share of the firm’s top five shareholders. |

| OCF | is the ratio of operating cash flow to total assets. |

| INTAN | is the ratio of intangible assets to total assets. |

| INVEST_ASSET | is the ratio of the sum of property, plant, and equipment, intangible assets, and financial lease assets to total assets. |

| INVEST_CF | is the logarithm of cash outflow for investment. |

Ethical Considerations

There are no human participants in this study and informed consent is not required.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study will be available from the corresponding author upon reasonable request.