Abstract

Greater access to finance by SMEs in developing countries is one of the most import powerful strategies to reduce poverty and unemployment issues and promote economic growth. The main objective of this study is to construct financial inclusion index for SMEs and identify the determinants of SMEs’ financial inclusion. The data are collected from the primary survey conducted in Sabaragamuwa province using the Stratified Random sampling method to achieve the abovementioned aims. A sample of 139 SMEs is used to analyze the data from a well-structured questionnaire. Principal Component Analysis (PCA) and Multiple Regression Analysis are applied to construct an index and identifying factors. The study’s findings reveal that the financial inclusion index for SMEs is weighted equally by access and quality of the financial services as the pillars. Further, the financial inclusion of SMEs is mainly determined by demand-side factors (ability to manage economic changes, proffer record keeping, and willingness to expand the business), supply-side factors (collateral requirements and application procedure), institutional factors (ownership type and sector of the firm), and some demographic characteristics of owner-manager of SMEs. The study recommends that the state bankers, commercial bankers, and policymakers should put in place policies that encourage financial service providers to set up their operations close and incorporate innovative approaches to ensure that they adopt technologies and financial services that are more accessible.

Introduction

Financial Inclusion (FI) is a universal problem for all countries. It is a general issue for countries with developing economies. Financial inclusion enhances the opportunity to obtain the economy’s capabilities and uplift the nation’s living standards. It is an emerging concept throughout the world. It has been identified by researchers Ratnawati (2020) and Omar and Inaba (2020) the improvement of Small and Medium Enterprises (SMEs) comprehensively as one of the solutions.

SMEs contribute significantly to economic development, job creation, poverty reduction, economic growth and social cohesion (Bayraktar & Algan, 2019; Gherghina et al., 2020). According to the World Bank (2020) report, SMEs represent approximately 90% of businesses and over 50% of employment opportunities worldwide. Formal and informal SMEs in emerging economies have supplied 40% of the country’s earnings, a significantly higher percentage of the Gross Domestic Product (GDP). The next important aspect is the contribution to value creation, generating between 50% and 60% of value added on average (Asgary et al., 2020; World Bank, 2020). Further, formal employment opportunities are provided by SMEs, which create 70% of jobs. Especially in emerging markets, it has been estimated that 600 million jobs will be required by 2030 to be absorbed into the global workforce. Ninety percent of new employment opportunities are provided by SMEs globally (World Bank, 2022). Thus, the development of SMEs is crucial in almost all countries, whether developed or developing economies, to economic diversification and resilience, the development status of the developing economies depends on the success of the SMEs. Thus, most developing economies look forward to encouraging financial inclusion, including broad access to financial services for low-income families and firms (Morgan & Pontines, 2018).

Generally, SMEs are crucial to enhancing social development, economic progression, and job creation to reduce poverty (Ahamed & Mallick, 2019). Considering any nation, SMEs provide intensely to reaching their primary objectives working as the backbone of social-economic progress (Rewilak, 2017). SMEs play an important role in economies and have been defined as a significant strategic sector in the policy objectives of most economies. Developing the SME sector in developing nations is essential for improving the country’s development. Considering the importance of the SME sector worldwide, it is well recognized due to several critical effects on socioeconomic aims such as higher employment progression, production, export, income, and fostering entrepreneurship and innovation.

Greater SME financial inclusion would have potential macro-finance benefits, including economic growth, employment increment, poverty reduction, enhancement of macroeconomic policy, and macro-financial stability. Generally, it is well known that SMEs are a leading part of job creation, social capital development, and ultimately providing fuel to the national economic engines. Enhancing the performance of SMEs is an effective tool for poverty alleviation in developing countries. SMEs are providing significant importance not only for developing countries but for developed countries as well.

Sri Lanka has been identified as one of the significant areas to accomplish sustainable economic growth through financial inclusion, and the country has made considerable progress. World Bank Enterprise Survey (2011) with 610 firms in Sri Lanka surveyed and results highlighted that 30% of the firms have that business environment. According to the IFC (2010) micro study, 40% of firms inspected and answered that access to finance is the main issue in opening and expanding the business. In addition, the IPS-NCCSL Survey revealed that 50% of respondents considered access to finance as their most significant constraint. Considering the Sri Lankan situation of SMEs, on the demand side, lack of financial literacy, market knowledge and transparency with the shortcoming of market infrastructure will be the issues of access to the formal financial system. Due to the limitation of risk-averse banking culture, heavy security expectations and insufficient mechanisms to smooth flow to improve the system, errors would be the supply-side issues (Wijesinha & Perera, 2015).

In developing countries, development measurements are discussed in different aspects without paying attention to the development of the financial market. Further, when constrained to access the Formal Financial (FF) sector, SMEs use informal financing as an alternative solution, including money from family sources, friends, or even from money lenders. Therefore, providing support to access finance SMEs would be a prerequisite for reducing poverty and inclusiveness of growth. Access to finance limits several constraints in the developing countries context, including Sri Lanka.

Scholars, policymakers, and economists have studied the variables that affect SME performance and growth and, consequently, their contribution to the economy. The majority of research on SMEs has shown that the most significant barrier to their expansion is their lack of access to funding (Duygan-Bump et al., 2015; Gozzi & Schmukler, 2016; International Monetary Fund, 2014; Shinozaki, 2012; Wellalage & Locke, 2017). Other issues include a lack of managerial abilities, inadequate tools and technology, a rigid regulatory framework, and restricted access to foreign markets (Yoshino & Taghizadeh-Hesary, 2016).

Limitations of finance access have slowed firms’ growth down (Fowowe, 2017; Yoshino & Taghizadeh-Hesary, 2018). Considering South Asian countries, SMEs face difficulties when access to credits either fully or partially. Fully constrained usually fall into two categories: those who applied for a loan but were turned down or those who were deterred from applying due to harsh terms and circumstances. Partially limited (include firms that have an external source of financing and firms that applied for a loan that was then partially approved or rejected). The finance gap survey (MSME Finance Gap, 2017) highlighted that around 65% of SMEs face difficulties accessing credits from the formal financial sector in Sri Lanka. It is comparatively high compared to other countries in South Asia.

The SME finance gap can be defined as the difference between credit demand by the SMEs and credit supply by the service provided, either formal or informal. Reducing or closing the supply–demand gap in SME finance would help increase annual economic growth and yield long–term growth benefits in most developing countries since SMEs are producing significant contributions to the national economies in developing nations. Fiscal policy activities are more smoothly functioning due to SME financial inclusion. More remarkable financial inclusion changes in SMEs would influence the effectiveness of monetary policy within the country (Mehrotra & Yetman, 2014). Further, greater SME financial inclusion leads to higher macroeconomic policy effectiveness. Transmission of monetary policy and price stability are also expected to be increased due to higher SME financial inclusion. The interest rate may increase due to the increment of formal financial lending by SMEs, thus increasing monetary transactions and letting authorities working related to monetary policies guarantee price stability. Financial stability and inclusion are commonly associated, and greater FI can support financial stability. Proper risk management, organization of assets, and financial supervision are in good standing with the support of financial stability through financial inclusion.

The general objective of the current study is to identify determinants of SMEs’ financial inclusion for SMEs. The significance of the study is considered under several vital areas. Firstly, the findings of this research will enhance the awareness of both the financial sector and firms together with the demand-side and supply-side indicators. Next, literacy-based development helps to develop policies aimed at reducing poverty. The financial inclusion of SMEs is one of the critical aspects of development that many nations do not currently neglect. However, attention regarding financial inclusion has increased more recently in developing countries, including Sri Lanka, with the introduction of the National Financial Inclusion Strategy (NFIS). Economic inequalities across enterprises will also be discussed, including size, firm duration, establishment, and close contact with political supporters. Thus social experts from several subjects, such as economists, sociologists, and political scientists, are commencing to rethink “whom” and “what” in economic development through financial inclusion.

This study can assist the government in developing physical policies by identifying the current state of SME financial inclusion. So the responsible authorities in the government and the Central Bank of Sri Lanka will design appropriate policies to overcome underlying issues and bridge the gaps that hinder efforts toward improving SME financial inclusion. Lastly, help this research’s findings will assist in observing leading elements for financial exclusion among the SMEs and, lastly, it might assist in reconstructing their related policies.

As the state banking sector dominates the financial system in the country, the financial industry would be the determining part of enhancement in regulatory and policy direction, allowing improved responsible SME access to finance. Micro-credits for SME development related to only the FF process would be another aspect the country could consider attentively. Hence, a public bank can assist and promote young, energetic people living in remote areas and low-income families to access finance via large, expanding, and subsidized bank branches to promote the regional development of industry and reduce poverty in all parts of the country. An effective policy within the banking sector could ensure that banks increase social returns to maximize their profits.

Literature Review

Theories on Capital Structure and Peaking Order

The theories underlying capital structure decisions have advanced significantly as the trade-off theory (Kraus & Litzenberger, 1973), the pecking order theory (Myers, 1984), and the agency theory (Jensen & Meckling, 1976). The capital structure describes the equity and outside funding that the company uses to finance its investments. Investigating the effects of variables on indebtedness, which is used as a stand-in for capital structure, has been the main focus of the research on capital structure decisions. The theory holds that internal resources, debt, and equity are the three primary sources of financing for businesses. This concept is important because it acknowledges that when it comes to financing their operations, business owners prefer to look internally rather than externally (Doku et al., 2016). Since the cost of capital is a function of capital structure and this method presupposes an ideal capital structure, capital structure theory approaches the demand of finance. The idea behind an optimal capital structure is that at a specific debt-to-equity ratio, the cost of capital is at its lowest and the firm’s value is at its highest. Once the SMEs have significant assets, good financial management will increase access to financing.

Pecking order theory appears to have greater relevance for SME studies empirically. The pecking order theory assumes that businesses have a hierarchy of sources for financing, either internal or external. Asymmetric information and transaction costs are critical components of this theory. Further, businesses adhere to the original pecking order concept, which states that when choosing their capital structure, businesses choose debt over equity. Furthermore, decisions about financing are based on knowledge asymmetry (Rathnasingha et al., 2019). According to Botta et al. (2016), internal finances precede external funds. Businesses only look for outside capital when their internal resources are insufficient. So, external financing for the business must be required, safe, and free of control constraints. Because it discusses collateral, this theory is relevant to Sri Lankan SMEs. In addition, business owners in Sri Lanka do not typically have a property or other asset to give as collateral for loans. According to this idea, firms follow a hierarchy of financing options, prefer internal financing while it’s available, and choose debt over equity when they need external financing. The hierarchy is dependent on the size and stage of development of the firm because each stage of growth has a unique level of information asymmetry and financial requirements .

Definition and Behavior of SMEs in Sri Lanka

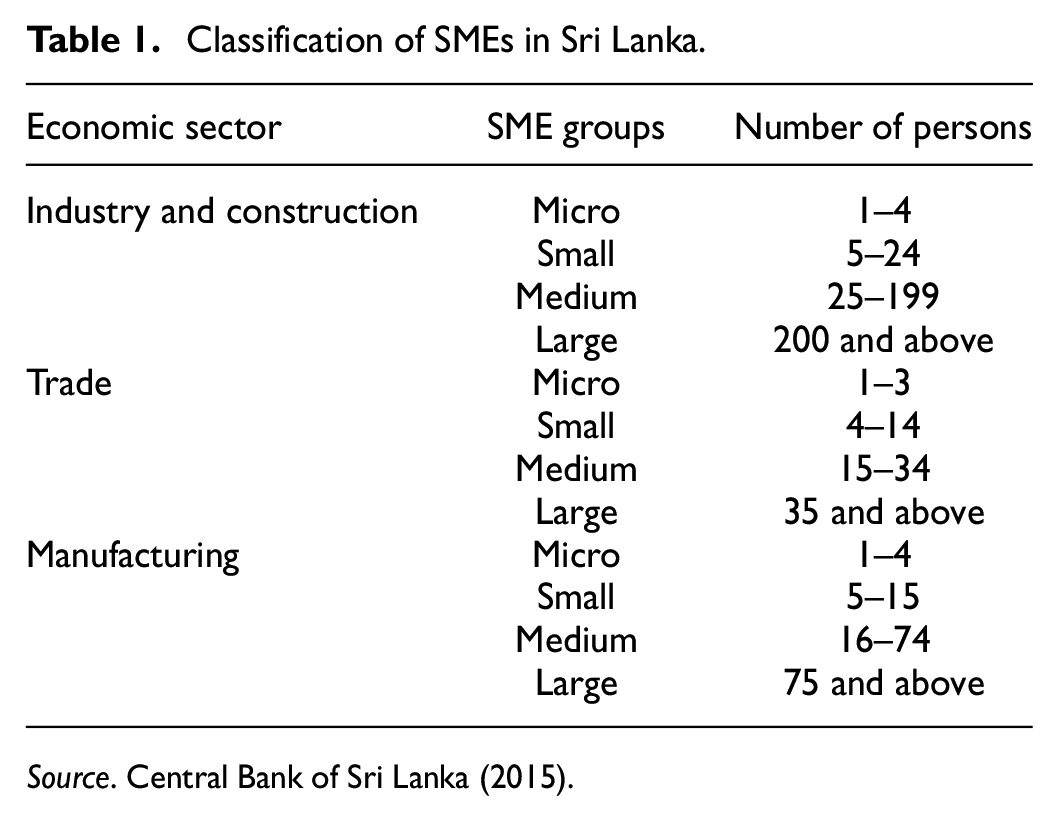

Standard definition regarding SMEs is essential for the provision of concessionary financial facilities and specific business development services toward the implication of the policies in the country. For that, a precise classification has been conveyed with the discussion of experts selected by the cabinet subcommittee for Economic Affairs. In Sri Lanka, out of several definitions regarding SMEs, common and widely considered description is presented in the following Table 1.

Classification of SMEs in Sri Lanka.

Source. Central Bank of Sri Lanka (2015).

SMEs play a central role in economies and have been defined as a significant strategic sector in most economies’ policy objectives. Developing the SME sector in developing countries is essential for development. The importance of the SME sector worldwide is well recognized due to the several key critical effects on socioeconomic objectives such as higher employment growth, production, export, income, and fostering entrepreneurship and innovation.

Financial Inclusion and Its Determinants

Mainly three key pillars of FI introduced by the Financial Inclusion Data Working Group (FIDWG) include access, usage, and quality regarding the services and products of finance for SMEs (AFI, 2015). Usually, access to finance by SMEs would be a fundamental limitation on development faced by individuals and firms (Yoshino & Taghizadeh-Hesary, 2016). Thus, FI supports building a solid beginning of a country’s financial infrastructure and the ultimate goal is to directly or indirectly facilitate economic and rural area development. Most of the economies and policymakers’ priorities, particularly in developing economies, have considered FI as the best solution for the constraint of finance. Further developing nations are depending on large number of SMEs and SMEs have contributed significantly to the GDP in a country.

Researchers in financial studies have mentioned various dimensions for FI with numerous proxy variables. Former studies have discussed different measurements for FI with several proxy variables. The financial inclusion index is calculated using three components: access, availability, and usage as a multidimensional approach (Sarma, 2008). Access to finance is necessary for SME growth and development, and the accessibility of finance provided by external sources is positively associated with productivity and growth (Mbuva & Wachira, 2019; Myint, 2020).

Accessibility has encountered supply-side factors associated with physical closeness and affordability concepts. According to what Adebisi et al. (2015) have highlighted, access to the services of the financial sector has a significant constructive result on the performances of business organizations. Considering further the relationship between accessibility and operations of the business sector, it was revealed that the ability to enter the financial services assists in the development of businesses, handling of activities, addressing risk, attaining success, and ability to adapt to financial shocks of entrepreneurs (Ageme et al., 2018).

Nkwede (2015) showed a significant relationship between financial availability and African business performance, using Nigeria as a case study. The availability of various financial services assists performance, sales growth, and productivity (Harrison et al., 2014). Spreading of bank financial services and SMEs’ financial performance are positively correlated (Ina Ibor et al., 2017; Turkmen & Yigit, 2012). Moreover, they pointed out that huge distances to access centers to gain financial services can adversely affect the operations and growth of SMEs. Further, some studies have identified that accessibility of ATMs, availability of machines for deposits and spreading of branches, especially in rural and remote areas, will expand the financial services to the community and, finally, it would support the growth, development, and competitiveness of SMEs (Simiyu & Oloko, 2015).

The next category is usage, defined as the depth of financial service and product use (Ombi et al., 2018), financial services affordability positively impacts the performance of SMEs. Correspondingly, not only affordability but also the improving availability of financial services in a nation under the dimension of FI has a relationship with the performance expansion of firms (Williams et al., 2017). Companies with fewer credit restrictions expand faster than those with more credit restrictions. Funding is crucial for business success and supports the numerous policies and programs implemented to increase the amount of credit available to African businesses (Fowowe, 2017). The borrowing capacity of SMEs increased due to low-interest rates and, thus, would benefit their performances (Okoye & Adetiloye, 2017).

Financial inclusion is the ability to access the FF system; several factors could determine it. Studies showed that factors including demand, supply, and infrastructural were associated significantly with the FI of SMEs (Oshora et al., 2021). Further, the study’s findings reveal that less confidence toward the banking sector, high bank charges, poor credit history records, fewer earnings, poor infrastructure, absence of consumer protection regulation, and inability to access information were the major determinants of financial inclusion (Bekele, 2022). Availability of funds, plans for expanding the business, and the necessity of working capital, machinery, equipment, and technology under the demand side factor are positively associated with the financial inclusion of SMEs (Desalegn, 2021).

Easy access to market information, alertness about productions, adaptability toward changing business environments, and skill of handling new technology were measured under market opportunity. Those positively affected the firm’s access to finance (Desalegn, 2021). Rachapaettayakom et al. (2020) conducted a study to observe the consequences of financial knowledge affecting knowledge acquisition tools and technology. The study’s results discovered that mainly six financial knowledge, including financing, record keeping and accounting, cash management, cost calculation, business planning, and a feasibility study (Rachapaettayakom et al., 2020) are necessary to manage financial difficulties. Additionally, it is more important to be aware of raising money and calculating the cost correctly for small business entrepreneurs. Additionally, a study was conducted to see the associated factors for financial inclusion for SMEs (Oshora et al., 2021). Study findings show that factors including collateral requirements determine access to finance by firms, market opportunity, cost of borrowing, institutional framework, demand-side factors, and supply-side factors (Oshora et al., 2021).

The firm’s size is also a critical factor determining a bank while accessing finance. Generally, large firms are well-established and more diversified than SMEs, thus making the likelihood of approving a loan considerably high (Wernli & Dietrich, 2022). Financial records are also more valid when considering access to formal financial sectors. Maintaining a proper bookkeeping record and if they are more transparent, access to finance will be more convenient (Adekunle et al., 2014; Mintah et al., 2022).

Following the above literature discussions, the present study is focused on constructing composite indexes for mainly financial inclusion, which would use as the dependent variables and for other three factors, including supply, demand, and institutional factors for SMEs.

Demand-side elements have to do with using the formal financial system, while supply-side factors are primarily related to the access side or the financial institutions’ side (Kumar et al., 2019). Demand-side factors are the elements that directly affect owner-manager decisions regarding purchasing goods and services from the financial sector. These elements facilitate intelligent decision-making by owner-manager. Demand-side factors are considered when all the means of providing financial services to the public have been made available or when there is access to those services, but no one is using them. The supply-side factors outlined how the monetary system works, what it does, how it is designed, and how it helps an economy by directly reducing the number of firms financially excluded. Financial inclusion, however, cannot occur from a supply-side perspective if national financial institutions do not offer those unbanked individuals a platform or services. The summary and the latest research support are summarized in Table 2.

Summary of Previous Research Findings.

Source. Own Work (2022).

Then formulates the following hypotheses for testing:

Methods

Data Collection Method

The present study followed a quantitative methodology with a field survey plan and a cross-sectional study. The desired population was all SMEs in Sri Lanka and the target respondents were owner-managers of the firm. They were selected mainly considering their awareness of the firms’ financial strategies and overall business situations. In SMEs studies, the target respondents were usually the owner-managers, given they have more knowledge regarding their enterprises’ strategies and overall business situations. The first stage, stratified sampling method, is used as a sampling procedure for data collection. The total population of SME was divided into different segments based on the type of SMEs as small and large. Then random sampling is applied to select SMEs since each stratum is homogeneous. Initially, 150 firms were projected to cover the data. However, only 139 firms could be finalized with the telephone and online survey. For the selected email list, questionnaires were sent. Since the response rate is very low, a reminder was sent again and we finally contacted over the telephone.

The basic structure of the questionnaire utilized in the study contained three sections. Section 1 covered basic details, section 2 was on a key characteristic of the financial inclusion determinants, and the final section was on the influential factor of financial inclusion. This study included the population of all types of SMEs in Sri Lanka. The sample has been selected from the population of firms in Sabaragamuwa province.

Variables and Model Specification

The financial inclusion index has mainly covered access, usage, and quality. Further demand-side and supply-side measurements used in factor identification are also measured with several pillars. All dimensions are measured by several proxies using a five-point Likert scale, varying from 1 to 5 (strongly agree to strongly disagree), because respondents could answer it more conveniently. The estimated equation of financial inclusion is presented below

Equations (1) and (2) were presented mathematically derived FI index for SMEs.FI component was the dependent variable of this study and it has measured by using three pillars Access to Finance (AC), Availability to Finance (AV), and Quality (QU) of financial services. The financial inclusion of the SMEs was determined by several factors derived as independent components; demand-side, supply-side, and institutional factors were measured using indexes. Other independent variables are institutional factors and demographic features of the owner-manager of the firm (Table 3).

Variable Description.

Source. Researcher Design (2022).

Data analyzing method

Collected data using the questionnaire were examined before utilizing for the final analysis. The distribution of the sample profile was as follows (see Table 4).

Sample Profile.

Source. Own Calculation (2022).

The highest proportion of 76% from the manufacturing sector, whereas 17% and 7% among the firms recorded the service and trade sectors, respectively. According to the sample data more than 50% of employees of SMEs were less than 20 workers and a few of the employees (3.46%) were over eighty workers. Almost 69% of firms were established in rural area, and females owned a few percentages (11.5%). Additionally, 49% of firms had less than three years of operations, while 36% were 4 to 10.

Lately, Principal Component Analysis (PCA) for constructing indexes and Multiple regression analysis techniques for finding the possible factors were applied. PCA reduces the dimensionality of a data set and increases interpretability (Jollife & Cadima, 2016). FI was measured through a composite index method including three main directions: access, usage, and quality of financial system services. However, FI could not derive straightly since those were quantitatively measured unobservable concepts (Cámara et al., 2017). As a first step, raw variables were standardized to remove the scale consequence by applying normalized transportation techniques (Le et al., 2019).

Next, obtain the covariance matrix for the raw data

Identify the eigenvalue and the eigenvector of the covariance matrix

Eigenvalues are set in descending order and the eigenvector is consistent with its eigenvalue.

Observed data were converted into k number of dimensional subspaces to a selection of high k eigenvectors of the covariance matrix. Components were selected with an uncorrelated measurement and each component had the largest possible variances in PCS as much as possible.

Multiple regression assesses the relationship between one dependent variable and some predictor variables (Petchko, 2018). The mathematical relationship was derived in equation (8) where FI demonstrated as a function of the several independent variables to study the influential factor on financial inclusion of SMEs as the dependent variable.

whereas;

Results

Results of PCA

The first step of principal component analysis has been performed separately for the variables under each type of dimension presented in three pillars. This is simply as the PCA sheds light on individual indicators’ relative contribution within each dimension. The individual index for each type was calculated from the weights obtained from the first step of PCA. Following the procedure and criteria described above, one component solution has been selected as the component in each dimension, including dependent and independent variables. Because components were selected based on eigenvalue and criteria for the selection was higher than 1. This suggested that over 70% of the variance in each variable was presented in the above Table 5.

PCA for Access, Usage, Quality, Demand Side, and Supply Side Demotions.

Source. Authors’ Calculation (2022).

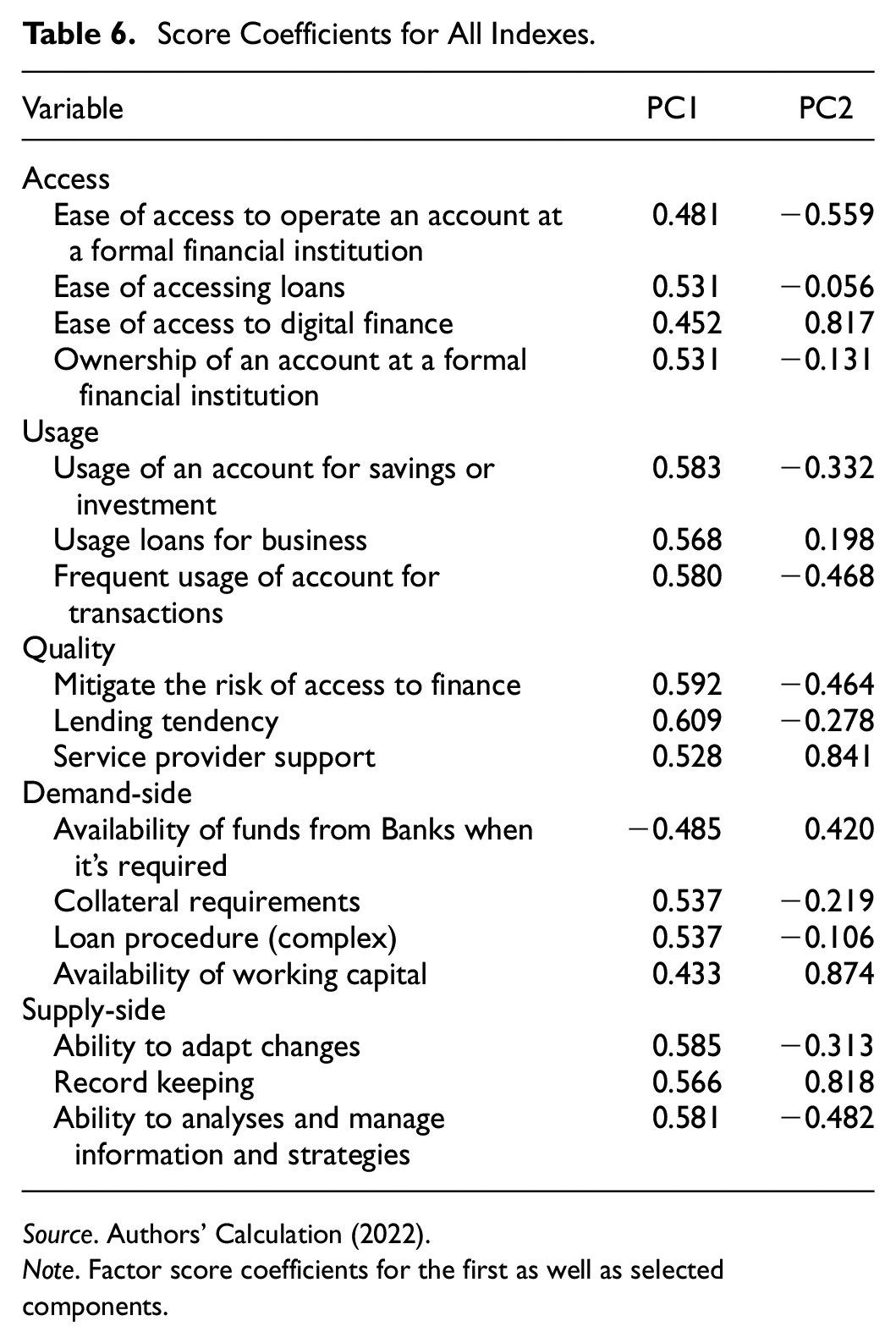

This is suggested evidence on the principal component analysis techniques for the financial inclusion index. The loadings of each variable on components are presented in the Table 6. In this analysis, the first principal component of the financial inclusion for three response variables was the linear compound;

Score Coefficients for All Indexes.

Source. Authors’ Calculation (2022).

Note. Factor score coefficients for the first as well as selected components.

Multiple regression was prepared to identify the linear combination of the constructs.

R 2 showed how much the variation of financial inclusion of SMEs as the dependent variable had been explained by selected predictor variables (demand side, supply side, institutional, and demographic) in the population. Adjusted R2 accounted for the number of predictors, which makes into consideration the dropped in degrees of freedom following the results of adding extra variables. According to the analysis results in Table 7, R2 and adjusted R2 had a value of 65.53% and 62.27%, respectively, which indicated that the model fits the data well.

Summary Result for the Final Model.

Source. Authors’ Own Calculation (2022).

Significant at 5%. *Significant at 10%.

Model equation is

The p-value of the F-statistic presented the overall significance level of the model used in the study. According to Table 7, the F-statistic of 30.14 of .0000 probability value indicated that the model is significant at 1%. There was enough evidence to claim that selected independent variables used for the study jointly influence SME finance inclusion.

To conclude the goodness of fit of the selected model, the normality test for errors was checked. The corresponding probability plot has shown the normality of errors. In addition to that following hypotheses were tested using a normality test as the Anderson-Darling test. H1: Standardize errors are not following the distribution of normal with the parameter of (0, 1).

The Anderson-Darling test results 0.471 on the p-value indicated that corresponding ∝ levels (.05) were less than that. Evidence showed that the errors followed a normal distribution (Appendix), demonstrating that the selected model fits well for the observed data.

Discussion

According to the present study findings, all three dimensions of financial inclusion were weighted positively. Essay access to loans, credit facilities, access through digital financing, and ownership of accounts have increased the SMEs financial inclusion. Lack of financial usage limited the financial inclusion of SMEs. The financial inclusion level was highly dependent upon the quality of the financial services used by the individual firms. The support offered in this study by Gabor and Brooks (2017) and Eton et al. (2021) regarding digital financing accelerated financial inclusion and easy access to service providers, especially for ATM services and the ability to move from one bank to another.

Further, PCA analysis presented the highest weights on access to financial services (0.663) followed by quality (0.659) and usage of financial services (0.354) in the present study. Similar findings could be observed in the study conducted by Cáamara and Tuesta (2014) and Cámara et al. (2017) the highest weight of PCA values allocated for access indicators was 0.42, next for usage indicator was 0.3 barrier indicator as 0.28. Accordingly, this evidence demonstrated that the access pillar was the most significant aspect of financial inclusion among the countries.

According to regression findings, age under the demographic factor had a negative relationship with financial inclusion and was statically significant. Nakano and Nguyen (2011) showed that the age of the firm’s leader affected the finance access as older adults are higher risk-averse and less enthusiastic while working at work. However, this finding contradicted the finding of Yaldiz et al. (2011) that suggested firm’s financing obstacles are reduced with the owner’s age and working experience.

Demand-side factors had a negative relationship with financial inclusion and the coefficients were statistically significant at a 1% significance level. This factor has been measured with the availability of funds from banks, Collateral requirements loan procedure (complexity) and availability of working capital. An increase in such demand-related factors had some effect on reducing financial inclusion. The results were inconsistent with other studies (Oshora et al., 2021). However, the findings regarding the supply-side factor had a positive association with FI. The coefficient on the variable showed that; the increase of supply-side factors by one unit caused to increase in financial inclusion by 1.49 units and was statistically significant at a 1% significance level. This finding was as same as the studies of Oshora et al. (2021) and Nega and Hussein (2016). There were a negative association between manufacturing (−0.238) and trading (−0.250) type businesses compared to the services type SMEs with financial inclusion. Meantime SMEs situated in urban (+0.182) or rural (+0.276) areas had a more positive influence on FI than firms situated in the estate sector. However, there was a negative impact on the financial inclusion of firms owned by the family (−0.512) and group (−1.217) compared to the individually owned firms.

Conclusion

The present study sought to construct the composite index for financial inclusion and determine the influencing factors on the financial inclusion of SMEs in Sabaragamuwa province in Sri Lanka. Results of PCA summarized that access, usage, and quality of financial services positively contributed to the financial inclusion index, respectively. Multiple regression analysis indicated that age as a demographic factor, demand-side factors, manufacturing, and trading compared to services business type, family owned, and group owned compared to single owned positively affected SMEs financial inclusion. However, supply-side factors the situation of SMEs in rural areas (compared to the estate sector) had a negative effect on SMEs financial inclusion.

Financial inclusion is prominent since it would reduce poverty and boost shared prosperity. So policymakers in the country should pay attention to enhancing the financial system systematically to provide affordable and sustainable financial services to SMEs. Developing a formal financial system and microfinance firms with the sophisticated digital financial system would be a better solution to promote financial inclusion. Further, policy ramifications for bankers were highlighted, and the least conventional methods through which bankers could reach out to SMEs were explored. It is well known that SMEs are one of the economically least integrated groups in many developing and growing nations, despite the fact that they are also seen as the engine of economic progress. Thus, more services and follow-up should be provided to SMEs by financial and non-financial institutions and organizations to strengthen their position as the engine of economic growth, employment creation, and job creation.

Footnotes

Appendix

Acknowledgements

We thank our colleagues from the School of Economics, Wuhan University of Technology for comments and assistance to improve the manuscript. Furthers Proffers in the same School who encourage us a lot.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.