Abstract

Using data of the mergers among accounting firms from 2007 to 2018 in China, this paper examines how regional cultural differences between accounting firms in different places affect audit quality after a merger. We found that the greater the regional cultural differences (proxied by dialectal difference in spoken Chinese) between the accounting firms’ registered places before the merger, the greater the improvement in audit quality of the merged accounting firm after the merger. Our research indicates that in the process of accounting firms’ mergers, the utility of cultural capital brought about by regional cultural variations exceeds cultural conflicts. The results imply that cultural differences could be potentially beneficial to firms’ mergers and acquisitions. Therefore, managers should try to make full use of cultural differences to help a newly merged firm to achieve competitive advantage and sustainable development.

Introduction

Audit quality is the common probability that the auditor finds that the auditee violates the accounting system and publicly exposes such violations. Audit quality can represent the level of accounting firms’ corporate governance and the reputation and sustainable development of accounting firms heavily depend on their audit quality. Good audit quality can enhance an accounting firm’s reputation and help the firm to win more market share and achieve competitive advantage and sustainable development. Prior research finds that accounting firms often try to improve audit quality to achieve competitive advantage through mergers (DeFond & Zhang, 2014; Lai, 2019; Sullivan, 2002). Many firm-level factors (e.g., accounting firm’s size, reputation, and professionalism) are reported to be influential on the audit quality of merged firms (Lennox & Pittman, 2010). However, little attention has been paid to macro-level factors such as culture that could influence the audit quality of merged accounting firms. New institutional economics argues that cultural influences are more fundamental than formal institutions on organizations (North, 1990; Williamson, 2000). The successful establishment and operation of an organization is inseparable from the cultural environment. Therefore, it is of great importance to examine the role of culture in organizations. Prior studies have shown that culture deeply affects the behavioral choices of organizations and individuals (DeBacker et al., 2015; Ketprapakorn & Kantabutra, 2019). However, there is a lack of research specifically targeting the role of culture in organizational behavior. For example, despite Astami et al. (2017) arguing that informal systems, including culture, have a significant effect on audit quality, their research is limited to preliminary discussions on the theoretical level and lacks of empirical evidence. Therefore, whether audit quality, as an important type of behavioral outcome of accounting firms, is affected by cultural differences after accounting firm mergers remains untested in research.

To examine empirically the influence of regional cultural differences in accounting firms’ mergers, we use data of the mergers of accounting firms from 2007 to 2018 in China. Chinese accounting firms are selected as the sample for this research because of the frequency and wide distribution of mergers of these firms across China, and because China has vast and clear geographic and cultural differences between regions (J. Li et al., 2013). The Chinese audit market is far from highly concentrated (Desai et al., 2016; Zhan et al., 2020). Facing the reality of diversified market demand and the internationalization of accounting services, China issued a policy document in 2007 to promote the expansion and growth of accounting firms (Desai et al., 2016). The purpose of this document is to promote the moderate concentration of the Chinese audit market through mergers (Zhan et al., 2020). Therefore, accounting firm mergers in China occur quite frequently, thus providing sufficient samples to test our research question. In addition, China has a vast territory and its population is distributed throughout many different areas. Given the diversity throughout China in geographical environment, historical heritage, religious beliefs, dialects, and levels of economic development, there are great regional cultural differences (J. Li et al., 2013). Thus, China provides a good setting to test whether cultural differences influence the effects of accounting firm mergers.

This study uses dialectal difference to measure the regional cultural differences between the two parties in a merger. We use Cheng’s (1997) Dialect Interoperability Index to calculate the dialectal difference between the merged parties. Our results show that the greater the dialectal difference between the accounting firms participating in the merger, that is, the greater the regional cultural differences, the greater the improvement in audit quality after the merger. Our research provides evidence for the influence of regional culture on accounting firms’ governance. Particularly in the merger of accounting firms, cultural differences influence the integration of management styles and firms’ economic outcomes by enhancing merged firms’ audit quality.

Our research makes the following contributions to the literature. First, this study adds new evidence of the debatable role of cultural differences in an organization by showing that cultural differences may not necessarily lead to conflict and friction. Prior studies often indicate that cultural differences can be risky and detrimental to firms (e.g., Knein et al., 2020; Sivapalan & Anindita, 2016; Zolfaghari & Madjdi, 2022). However, our research extends such literature by showing that prior cultural differences between two accounting firms can be beneficial to the audit quality of the merged accounting firm. Second, our research extends the literature on the mergers of accounting firms because this study is among the earliest to use large samples of Chinese accounting firms’ mergers to investigate whether regional cultural differences affect the outcomes of accounting firms’ mergers. Third, it adds to the growing literature on the effects of informal institutions in emerging markets. Prior literature reveals that informal institutions are important for firms in emerging markets due to institutional voids (Z. Li et al., 2021). This study adds to this stream of literature by indicating that culture, a form of informal institution, has economic consequences for firms.

The remainder of this article is organized as follows. In Section 2, we present the hypotheses development. In Section 3, we introduce materials and methods. In Section 4, we discuss the empirical results. In Section 5, we conclude the study.

Hypothesis Development

Culture is a collection of group thinking (Hofstede, 1980). New institutional economics argues that the influence of culture is even more fundamental than that of formal institutions on organizations (North, 1990; Williamson, 2000). Culture influences not only individual behavior but also organizational behavior (Adler & Aycan, 2018; Gelfand et al., 2007; Tabellini, 2008). Of all the cultures that influence the behavior of organizations such as accounting firms, regional cultures are the most observable and representative. For example, prior studies show that regional culture restricts people’s communication behavior and life goals, which will affect the regional economy (Gupta & Hanges, 2004; Vinson et al., 2020). Regional culture has been found to influence a company’s cash holding and earnings management behavior (Chang & Noorbakhsh, 2009; El-Halaby et al., 2021; Han et al., 2010; Kutan et al., 2020), debt maturity choices (Orlova & Harper, 2021; Zheng et al., 2012), dividend policies (Bae et al., 2012), and innovative activities (Shane, 1993; Taylor & Wilson, 2012; Wei et al., 2019). The same is true for accounting firms (Astami et al., 2017). Regional culture, as a soft constraint, can internally influence the behavior of auditors and the development of audit services through the penetration and assimilation of consciousness and concepts, and it can then affect audit quality. Prior literature finds that cultural differences can be important resources for firms but may also bring conflicts to the merged firms (Backmann et al., 2020; Bernile et al., 2018; Pieterse et al., 2013; Sivapalan & Anindita, 2016). Therefore, regional cultural differences can influence the effectiveness of accounting firms’ mergers in two opposing ways.

First, regional cultural differences, which can be considered a source of diversity, can bring more cultural capital to accounting firms. The advantages of cultural differences for a team’s decision-making process can be divided into general advantages and special advantages (Maznevski, 1994). A general advantage refers to cultural differences that can bring different global perspectives to the team and provide different channels for collecting and receiving information (Backmann et al., 2020; Bernile et al., 2018; Pieterse et al., 2013). Directors from different cultural backgrounds tend to represent sources of information (Anderson et al., 2011). A special advantage of cultural differences refers to the fact that groups with different cultures can use cultural characteristics such as language and social networks to communicate and cooperate with customers with similar cultural backgrounds, thereby improving corporate performance. The higher the cultural differences within the organization, the larger the network scale and the greater the heterogeneity of resources, thereby effectively increasing the total network resources (Erickson, 1996; Yilmaz et al., 2021). For example, Masulis et al. (2012) found that companies listed in the United States that have foreign directors tend to perform better in cross-border liquidation and reorganization with companies from the same country. Pieterse et al. (2013) argue that culture can expand the scope of information exchange, and thus bring more information to the company. Wen et al. (2020) find that directors with foreign experience are negatively associated with corporate tax avoidance.

Second, regional cultural differences sometimes create communication barriers for team members. This can generate friction (leading to slower and more difficult communication and collaboration) and cause misunderstandings and prejudices of varying degrees (Sivapalan & Anindita, 2016). Cultural differences can even have a destructive effect on the team’s problem solving, which in turn negatively affects the team’s performance and lead to conflict in plan implementation (Anderson et al., 2011; Doney et al., 1998; Knein et al., 2020). Sivapalan and Anindita (2016) examine the effect of cross-cultural management teams on organizational performance for Malaysian small- and medium-sized technology companies and find that cultural diversity hinders both the communication among the team and with customers. This conflict created by cultural diversity is particularly prominent when the company’s management team is small and weak. Zolfaghari and Madjdi (2022) find that variations, not only across but also within individuals, can hinder or promote trusting relationships in the workplace.

Thus, cultural differences may have two distinct influences on the audit quality of merged accounting firms. That is, cultural diversity created by regional and cultural differences may enhance the integration of resources within the organization, improve operational efficiency, and drive improvement of audit quality. However, regional cultural differences may lead to inconsistent styles and concepts between management and auditors. This creates cultural barriers within the firm and causes loose teamwork. Work efficiency is reduced when the level of teamwork decreases, which leads to a decrease in audit quality.

Based on the above analysis, this article proposes the following competing hypotheses:

Material and Methods

Sample and Data

Our sample is listed Chinese companies that changed auditors as a result of merging accounting firms between 2007 and 2018. Because international accounting firms are less influenced by traditional regional cultures, the sample includes only mergers between accounting firms located in mainland China. The year 2007 was chosen as the starting year because China issued policy documents in 2007 that pushed accounting firms to become bigger and stronger, after which mergers became more frequent.

We compile the mergers of accounting firms from 2007 to 2018 by searching the audit institution changes of all A-share companies on the China Stock Market and Accounting Research (CSMAR) database and websites. We then use search engines to manually collect the locations of the parties before the merger of the accounting firm and determine the dialect used in each firm by consulting the Atlas of Chinese Dialects. After excluding samples with missing variables, we obtain 864 firm-year observations.

Empirical Model

To test the influence of regional culture on audit quality referring to the setting of Spolaore and Wacziarg (2009), this study constructs the following regression model:

The dependent variable is audit quality (AQ). With reference to the existing literature, the study uses discretionary accruals (DA) as a substitute variable for audit quality (Becker et al., 1998; Krishnan, 2003; Kothari et al., 2005). We take the opposite of the change in the absolute value of DA in the year before the merger and the year of the merger to measure the change in audit quality (ΔAQ = −Δabs(DA)). Prior literature uses traditional cultural indicators such as language, colonial relations, and religious beliefs to measure cultural similarity (Cultural Similarity) as a proxy variable for cultural differences (Fidrmuc & Fidrmuc, 2016; Melitz & Toubal, 2014). Consistent with prior literature, we use language similarity to measure cultural differences. The key variable

Following prior literature (e.g., F. Wang et al., 2020), the main control variables include company characteristic variables such as asset scale, financial leverage, return on net assets, degree of regional marketization, and level of corporate governance. Given that prior studies have shown that the size of accounting firms affects audit quality (DeAngelo, 1981), we also employ accounting firm’s size as a control variable. If the regional cultural barrier caused by the merger of firms leads to a decrease in audit quality, the expected β1 will be significantly negative; if the regional cultural diversification brought about by the merger of firms leads to an improvement in audit quality, then the expected β1 will be significantly positive.

Validation of the Independent Variable

Cheng’s (1997) Dialect Interoperability Index is the most influential and comprehensive quantitative analysis of the relationship between Chinese dialects. This index calculates the phonological correlation coefficient between two dialects based on the pronunciation of more than 2,700 Chinese characters in “Chinese dialect words” in different dialects. Then, according to the statements of more than 900 Mandarin words in different dialects in a “Chinese Dialect Vocabulary,” the vocabulary correlation coefficient between two dialects is calculated, and finally the “Dialect Interoperability Index” is synthesized. We validate our measurement by comparing with method of genetic distance (Desmet et al., 2011), we take the logarithm of the Dialect Interoperability Index and then take the opposite number to obtain the dialectal difference index. The correlation coefficient between this indicator and the Dialect Interoperability Index reaches −0.99 (R2 = .39).

It is worth noting that genetic distance can also be used as a proxy variable to measure cultural differences. Genetic distance is mainly used to measure the degree of genetic difference between two different populations, generally by measuring the allele frequency at the different sites of the two populations. Cavalli-Sforza et al. (1994) argue that genetic distance is closely related to population migration and that the increase of genetic distance will lead to language differentiation. These researchers proposed that genetic distance can be used to explain the emergence of some social phenomena such as language differences. Desmet et al. (2011) use data based on the World Value Survey to measure cultural distance and compared it with genetic distance, and they found that there is a high correlation. Therefore, this study uses the immunoglobulin Gm haplotype frequency to measure the genetic distance between different regions in China. This indicator is characterized by direct accuracy, availability, and wide coverage. We tested the relationship between genetic distance and dialectal difference we constructed and found a highly positive correlation (see Figure 1).

Correlation between dialectal difference and genetic differences.

Descriptive Statistics

Table 1 lists the definitions of the variables. Table 2 presents the descriptive statistics of the main variables used in the empirical tests. We winsorized the continuous variables at the 1% level to eliminate the influence of extreme values. During the sample period, the average audit quality of the sample company after the merger improved. More than half of the merged firms do not belong to the same dialect area. The Beijing office participated in the mergers associated with 72.3% of the sample companies. The descriptive statistics of other variables are within a reasonable range of values that are comparable to those found in previous studies.

Definitions of the Variables.

Descriptive Statistics.

Empirical Results

Regression Analysis

Table 3 reports the main regression results of model (1). In columns (1) to (5), the dependent variable is ΔAQ. In column (1), we do not include control variables, firm fixed effects, or year fixed effects. In column (2), we add the control variables of finance status. In column (3), we include the control variables of financial status, corporate governance and accounting firm size. In column (4), we further include the year fixed effects. In column (5), we include all control variables and the firm fixed effects and year fixed effects in the regression. The coefficients of the explanatory variables

Effect of Dialectal Difference on Audit Quality.

and ** denote significance at the 10% and 5% level, respectively, significance at the 10% and 5% level, respectively.

Additional Test

Competing Hypothesis

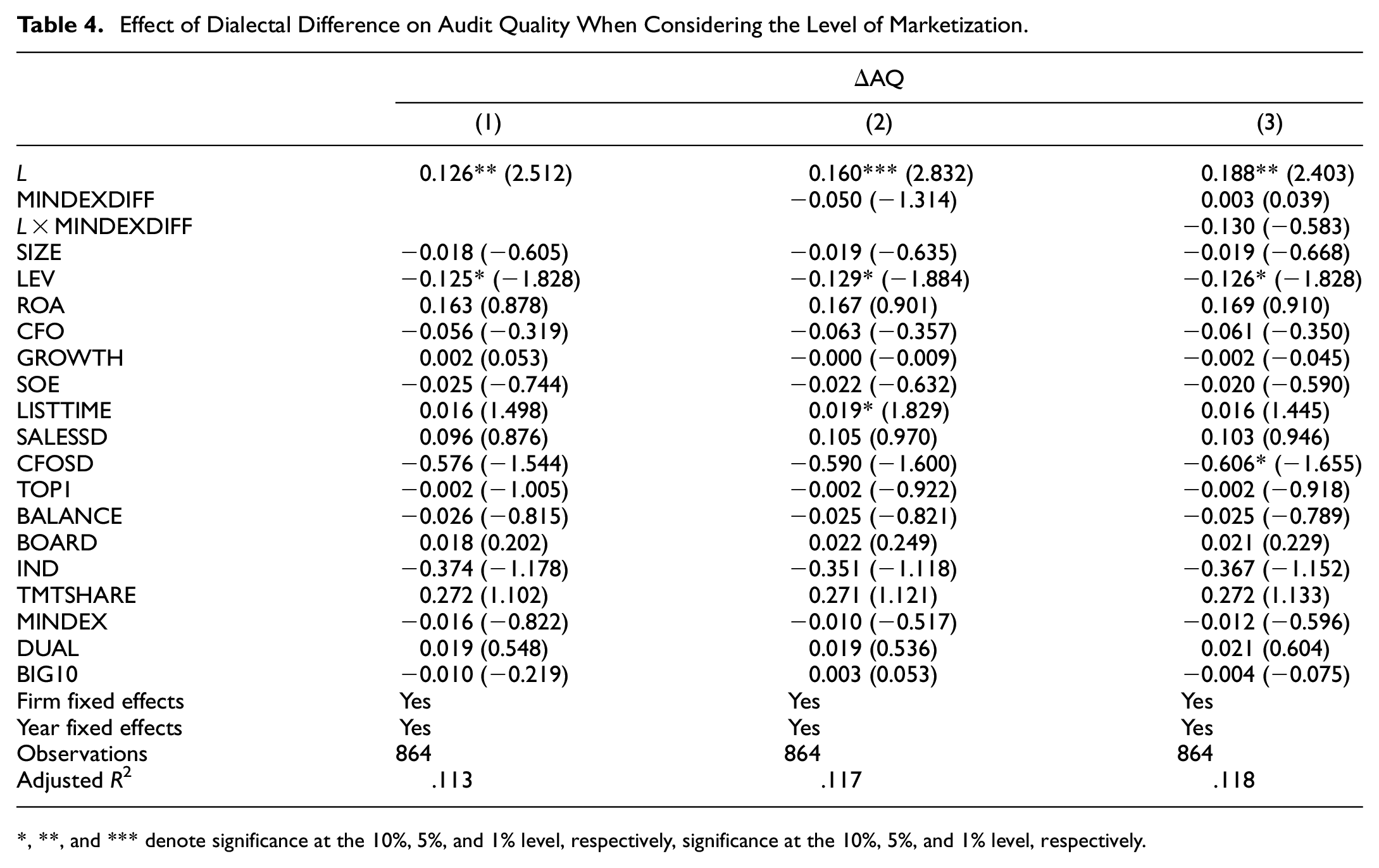

There may be some factors that affecting the accuracy of our conclusions. First, the improvement of audit quality may be caused by differences in the formal institutional environment of the merger firms. Given that some regions have more developed economies and more complete formal systems, after the merger of two firms, the audit quality in regions with poor formal system environments before the merger will improve significantly. Thus, we use the level of marketization to measure the institutional environment.

As shown in Table 4, the coefficient of L is significant, and the coefficients of MINDEXDIFF and the interaction term L × MINDEXDIFF are not significant. This demonstrates that even if the differences in the level of marketization (formal systems) are considered, the coefficient of dialectal difference remains significant as a result of cultural differences. Compared with the differences in the institutional environment of the two locations, cultural differences are found to play a greater role in affecting the merger process.

Effect of Dialectal Difference on Audit Quality When Considering the Level of Marketization.

, **, and *** denote significance at the 10%, 5%, and 1% level, respectively, significance at the 10%, 5%, and 1% level, respectively.

Second, in response to the Chinese government’s call for accounting firms bigger and stronger, many firm mergers have been conducted between Beijing firms and non-Beijing firms. Thus, a large part of this dialectal difference may be between the differences that exist between the Beijing area and other regions, rather than purely cultural differences. Therefore, we further consider whether the merger includes firms located in Beijing. As shown in Table 5, our test found that the coefficients of L and PEK are significantly positive, but the coefficient of the interaction term L × PEK is not significant. Thus, it is noted that audit quality does improve when the merger includes a Beijing firm compared with a merger between two non-Beijing firms, but that regional cultural differences still play an independent role in the audit quality of the merged firm. Even if the economic environment and institutional environment are considered, cultural differences in the areas where accounting firms are located are found to have a positive effect on audit quality of the merged firm.

Effect of Dialectal Difference on Audit Quality When Considering Beijing Firms.

, **, and *** denote significance at the 10%, 5%, and 1% level, respectively, significance at the 10%, 5%, and 1% level, respectively.

Sustainable Effect of Dialectal Difference on Audit Quality

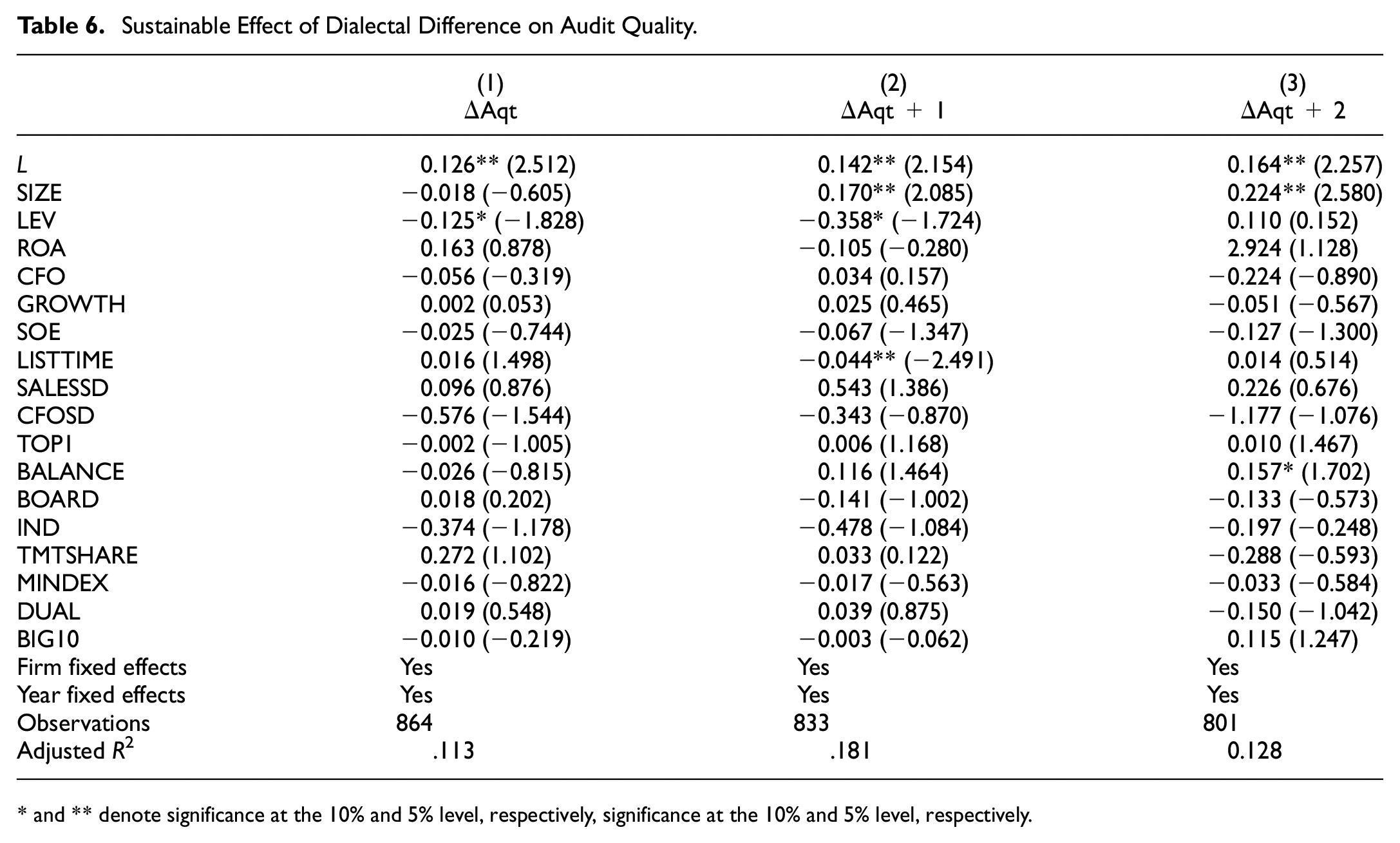

One of the goals of a merger of accounting firms is to obtain greater competitive advantage through the integration of talents and resources. Therefore, the improvement of audit quality after a merger should be continuous rather than temporary. Thus, we further examine the relationship between cultural differences and audit quality of merged firms 1 and 2 years after the merger.

Table 6 presents the results of this examination. The dependent variable in column (1) is the difference in audit quality between year t and the year before the merger. The dependent variable in column (2) is the difference in audit quality between year t + 1 and the year before the merger. The dependent variable in column (3) is the difference in audit quality between year t + 2 and the year before the merger. In columns (2) and (3), we remove samples of changes in accounting firms in subsequent years. The coefficient of L is significantly and continuously increasing from columns (1) to (3), indicating that the influence of cultural differences on audit quality gradually increases in the years after the merger.

Sustainable Effect of Dialectal Difference on Audit Quality.

and ** denote significance at the 10% and 5% level, respectively, significance at the 10% and 5% level, respectively.

Robustness Tests

Alternative Measurement for Dialectal Difference

We recalculate dialectal difference using the other dialect area coding method following the Atlas of Chinese Dialect. We make L’ equal to 3 if the merged firms belong to completely different dialect regions, 0 if they are fully consistent, and 2 or 1 if they are related to some extent. We replace the dialectal difference and regress model (1) and obtain another set of results, as shown in Table 7. The coefficient of L’ is significantly positive after controlling for the year fixed effect, indicating that our results are robust.

Alternative Measurement for the Dialectal Difference.

and ** denote significance at the 10% and 5% level, respectively, significance at the 10% and 5% level, respectively.

Alternative Measurement for Audit Quality

Outside stakeholders of an audited company can observe audit results but cannot observe the audit process. The direct manifestation of audit results is the type of audit opinion that is given after the audit. Based on this, many scholars use non-standard opinions as an agent variable for high audit quality (Francis & Krishnan, 1999; Lennox, 1999). When the accounting firm issues a standard unqualified opinion to the client, MAO is equal to 0, otherwise it is equal to 1. We use the logit model to test the relationship between cultural differences and audit opinions.

As shown in Table 8, the coefficient of L is positive and significant when controlling for year and firm fixed effects. The results show that after controlling for firm characteristics and macro-environmental factors, accounting firms with greater cultural differences before the merger are more likely to issue non-standard audit opinions. This is most likely due to the improvement in auditors’ capabilities.

Alternative Measurement for Audit Quality.

, **, and *** denote significance at the 10%, 5%, and 1% level, respectively, significance at the 10%, 5%, and 1% level, respectively.

Propensity Score Matching

The improvement in audit quality brought about by cultural differences may be attributed to differences in the characteristics of the clients served by firms that merge across dialects and those that merge with the same dialect. We use propensity score matching (PSM) to attempt to alleviate this concern. We divide the customers into two subsamples, namely, two groups with a dialectal difference of 0 and a dialectal difference of not 0.

Panel A of Table 9 reports the results of the first-stage logistic regression model. Compared with clients of firms that merged in the same dialect area, clients of firms that merged in different dialect areas went public earlier, with less income volatility, lower board size and executive shareholding, and lower levels of marketization in the region where the company is located.

Effect of Dialectal Difference on Audit Quality Propensity Score Matched Sample.

, **, and *** denote significance at the 10%, 5%, and 1% level, respectively, significance at the 10%, 5%, and 1% level, respectively.

Based on the results of the first-stage model, we match each firm year where L is greater than 0 with a firm year where L is equal to 0, without replacement, at a calliper distance of .05. Panel B shows insignificant difference in the mean of the variables for the matched subsamples after PSM. It is found that PSM mitigates the observable differences in client characteristics. We re-estimate model (1) using matching samples, and the results shown in panel C indicate that our main findings are reliable.

Discussion of Results

This article examines whether regional cultural differences between accounting firms before mergers affect the merged firms’ audit quality after the merger. The following valuable results are found.

First, the results show that the greater the regional cultural differences between the accounting firms prior the merger, the greater the improvement in audit quality after the merger. Prior literature on the economic consequences of cultural differences on firm outcomes is debatable and inconclusive. Some researchers argue that cultural differences can be a soft resource for firms and thus have good effects on firms (e.g., Backmann et al., 2020; Wen et al., 2020; Yilmaz et al., 2021), while others find that cultural differences can create conflicts for firms (Knein et al., 2020; Zolfaghari & Madjdi, 2022). Our study demonstrates that regional cultural differences can increase accounting firms’ audit quality after a merger, thus providing new evidence of the benefits of cultural differences for firm outcomes. In addition, our further test shows that even if the differences in formal institutions are controlled, the relationship between cultural differences and audit quality holds, which indicates that cultural differences, as a form of informal institution, do indeed influence the outcomes of accounting firms’ mergers independently.

Second, we find that the relationship between cultural differences and the audit quality of the merged firms remains significant even after 1 and 2 years of the merger. Moreover, the coefficient on L is continuously increasing from the year of the merger year to the next 2 years, indicating that the influence of cultural differences on audit quality gradually continues to increase in years after the merger. This finding is in line with Y. Wang et al.’s (2021) argument that the influence of culture on firm behavior is long lasting.

Third, the findings show that when comparing mergers that include accounting firms located in Beijing and mergers of two non-Beijing firms, the audit quality improves more when the merger includes a Beijing firm rather than two non-Beijing firms. However, the coefficient on the cultural differences remain positively significant in this comparison. This result demonstrates that even though accounting firms in Beijing have a more developed economic and institutional environment, which can in turn increase the audit quality of merged accounting firms, cultural differences continue to play an important role in influencing the outcomes of accounting firm mergers by enhancing the audit quality of the merged firms.

Taken together, the results of this research provide empirical evidence that cultural differences between merged accounting firms can increase audit quality of these firms. These findings add new evidence to the literature on the economic consequences of cultural differences.

Conclusions

We use data of mergers of accounting firms in China from 2007 to 2018 to examine how regional cultural differences between accounting firms affect the merged firms’ audit quality after the merger. We find that the greater the dialectal difference between the accounting firms participating in the merger, that is, the greater the regional cultural differences, the greater the improvement in audit quality after the merger. When we consider the differences in the market environment in the region where the merging firms are located and exclude accounting firms located in the Beijing office because they generally have better quality control, the influence of regional culture remains significant. The results show that in the process of the merger of firms, the utility of cultural capital brought about by regional cultural differences exceeds the damage caused by cultural conflicts.

Our research provides several theoretical implications. First, this study provides new evidence of the debatable role of cultural differences in an organization by examining whether cultural differences affect the success of mergers of accounting firms. Prior literature often indicates that cultural differences can be risky and detrimental to the merger of firms, and that they are often marked by conflict and friction between the merged firms. However, this research extends such literature by showing that cultural differences may not necessarily lead to conflict and friction. Our empirical results indicate that prior cultural differences between two accounting firms can be beneficial to the audit quality of the merged accounting firm. Second, we extend the literature on the mergers of accounting firms because this study is among the earliest to use large samples of accounting firms’ mergers in China to examine whether regional cultural differences affect the effects of accounting firms’ mergers. Third, the study adds to the growing literature on the effects of informal institutions in emerging markets. Prior studies reveal that informal institutions are important for firms in emerging markets due to institutional voids (Z. Li et al., 2021). Our results suggest that culture, a form of informal institution, has economic consequences for firms.

This research also has several practical implications. First, the study indicates that cultural differences in a newly merged accounting firm can improve its corporate governance level, which is vital for the sustainable development of a firm. Therefore, managers should try to make full use of cultural differences and prevent potential conflicts to help newly merged accounting firms achieve competitive advantage and sustainable development. Second, the results show that cultural differences have a significant effect on the success of the merger of accounting firms. Therefore, before the merging of accounting firms, stakeholders should fully consider the cultural differences between the two sides, so that they can choose the most appropriate merger target and effectively manage the process of the merger. Third, the study indicates that culture could be an important resource for an organization, thus managers should be aware of this factor and properly utilize it to enhance the governance of the organization.

Our research has several limitations. First, because of the limitation of data availability, we use dialectal differences as the proxy for regional cultural differences. We agree that this measurement may not fully represent cultural differences. Therefore, future research could use other proxies for regional cultural differences to deepen our understanding of this topic. Second, we use archival data in China only to generate our research results. Thus, we call on future research to use data from the Western context to provide further understanding of this topic. Third, our samples are limited to accounting firms, and it remains a question whether these findings are generalizable to other types of firms. Thus, future research could focus on the same question using other types of firms to obtain a fuller picture of the economic consequences of cultural differences.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article is supported by the National Natural Science Foundation of China (Grant No. 72132004).

Ethical Approval

Not applicable.