Abstract

Although some empirical studies have examined the direct impact of outward foreign direct investment (outward FDI) on economic growth, but the indirect role play by home country institutions in outward FDI-induced economic growth remain unexplored. To cover this research gap, this study examines the impact of outward FDI on economic growth mediated by home country institutions in global panel of 161 economies, divided into World Bank income clusters such as high, upper-middle, lower-middle, and low-income economies for the period 1998 to 2019. For empirical analysis, this study utilized the Cross-Sectionally Augmented ARDL (CS-ARDL) and the Common Correlated Effect Mean Group (CCEMG) techniques robust to numerous econometric problems. In low-income countries, results indicate that outward FDI internationalization activities have adverse effect on economic growth, and the impact of home country institutions in stimulating outward FDI-induced growth appears weak both in the short term and long-term. In the case of high income, upper-middle income and lower-middle income countries, finding highlights that the joint impact of outward FDI and home country institutions stimulate higher economic growth and accelerate economic integration into the global economy. These impacts were found to diminish moving from high to low-income countries, which suggests that home country institutional development and income economy level matters for outward FDI-induced growth effects. The study also discusses key implications for policy.

Keywords

Introduction

In the past few decades, the global outward foreign direct investment flows (hereafter referred to as outward FDI) has played a significant impact in facilitating technology transfer, stimulating economic growth, and expanding the domestic economy into the global market (Knoerich, 2017; Saad et al., 2014). These productivity “spillover effects” to domestic economy allows firm to mitigate risks by diversifying their investments portfolio, penetrate new markets, upgrade production processes, receives low-cost importation of goods from affiliates abroad, secure technology transfer, as well as acquire managerial knowledge and skills. This increases the competitiveness of investing firms, raising investment productivity, and boosting domestic growth. However, this perspective portrays outward FDI as a pursuit of assets and advantages rather than the assets-exploitation. Nevertheless, seminal papers from international economic (IE) and business (IB) scholars show that, besides crowding-out investments (Ali et al., 2018; Ameer & Mansour, 2017; Kurtović et al., 2022), global outward FDI spillover effects can give rise to “hollowing-out” phenomenon (de-industrialization), transfer capital, create unemployment, and decrease home country economic growth (Huijie, 2018; Liu et al., 2015; Simeon & Ikeda, 2003; Weng et al., 2010).

As a crucial growth and development factor in modern economy, outward FDI flows are not only driven by global specific-business differences (Barney, 1991); or specific industry conditions (Porter, 1990), but are also motivated by home country institutions which act as background check that controls firm’s strategies and interactions with the institutional framework (Cuervo-Cazurra & Ramamurti, 2017; Dunning & Lundan, 2008; Hitt, 2016; Peng et al., 2008). This implies that institutions could be a channel through which FDI promote growth and productivity for home country. Therefore, it is possible that global outward FDI spillover effects on economic growth may not occur or produce adverse effects if there are institutional deficiencies which can constrain the absorptive capacity of domestic enterprises. These views are further reinforced by Soh et al. (2021), Cantwell et al. (2010) studies that strong institutional framework facilitates both local and foreign firms to compete for output rationalization and decrease negative impacts of FDI. Thus, there is a growing consensus among economic scholars that institutions “rules of the game” plays a prominent role in influencing the activities of multinational corporations (MNCs) as well as the impact of the spillover effects they produce (Cantwell et al., 2010; Peng et al., 2008).

Recently, studies on FDI and economic growth relationship have received great attention, but the burgeoning literature mainly focused on FDI inflow for host developing economies (Aziz, 2020; Bouchoucha & Yahyaoui, 2019). However, the results for most of these studies show that FDI inflow improves the domestic economy of host countries. Even so, several empirical findings indicate that crucial economic growth determinants such as—financial markets development (Azman-Saini et al., 2010); human capital (Mohamed Sghaier, 2022); political stability (Hoque et al., 2018), level of economic development (Blomstrom et al., 1994); and lately, institutional quality (Alguacil et al., 2011; Baiashvili & Gattini, 2020; Hayat, 2019; Jude & Levieuge, 2017), may influence FDI inflow-led growth relationship for host country. Thus, host country institutions mediate the impacts of FDI inflow on economic growth, but the effect varies significantly due to different institutional environment (Baiashvili & Gattini, 2020). This finding is particularly relevant in developing economies where the institutional framework is significantly different from the developed economies which stringently regulate the way MNCs react and interact with the local firms (Borensztein et al., 1998; Cantwell et al., 2010). This sub-strand of literature on the impact of institutions in FDI inflow-led growth relationship continues to grow steadily. For instance, Aziz (2020), Hayat (2019), Baiashvili and Gattini (2020), Holmes et al. (2013) etc., examines the role of institutions in the mediation of FDI inflow-led growth for host countries using global panel of different income groups. Specifically, Hayat (2019) study argues that institutional quality enhances FDI inflow-led growth in host country, especially in low and middle-income countries.

On the contrary, studies examining the spillover effects of outward FDI on home country economy are scanty, this include Kakoti et al. (2019)—India; Ali et al. (2018)—China; Ciesielska and Kołtuniak (2017)—Poland; Wong (2013)—Malaysia; etc. These few available studies are in single country analysis, but the role of home country institutions in the impact of outward FDI-growth across global income economies cluster remain unexamined. For the most part, extant literatures examining MNC’s expansion abroad mainly focus on the impact of capital investment, export, and domestic employment in developing economies. To this end, this study examines the impact of outward FDI on economic growth via home country institutions in global panel of 161 countries clustered according to the world bank income groups such as low-income, lower-middle, upper-middle, and high-income. This study considers the heterogeneous panel cointegration techniques such as the cross-sectional autoregressive distributed lags (CS-ARDL) and the common correlated effect mean group (CCEMG) techniques proposed by Chudik and Pesaran (2015) and Pesaran (2006) respectively to examine this relationship. These techniques are robust to cross-sectional dependence, heterogeneity, and endogeneity. The World Bank categorized the global economy into four income groups (low, lower-middle, upper-middle, and high income) contingent on the relationship between the measures of well-being and GNI per capita, based on the purchasing power parity (PPP) in US. Dollars.

This study contributes significantly to literatures on outward FDI-growth relationship in several ways. First, most existing studies employ empirical techniques that assume cross-sectional homogeneity across panel, believing that the results could be applied to some group of countries. But given the nature of FDI across countries with potential heterogeneous effect, the assumption for cross-sectional independence is likely to be violated. Therefore, this study employs the CS-ARDL and the CCEMG techniques which accounts for cross-sectional dependence, endogeneity, as well as heterogeneity to investigate the short-term and long-term effects of outward FDI-induced economic growth mediated by home country institutions. Second, this study explores the role of home country institutions in the impact of outward FDI-growth across different income economies, as existing studies only explore inflow FDI-led growth for host country. Third, our findings suggest the impact of outward FDI-growth via home country institutions appear to contribute positively to high-income, upper-middle income and lower-middle income countries, but the effect varies across income groups and decreases from high to low-income economies. However, overseas direct investments in low-income countries have negative impact on growth, which suggests a decrease in economic growth when outward FDI flow increases in home country. Furthermore, the institutional components of government effectiveness (GE) and political stability (PS) appears to contribute most to stimulating outward FDI-induced growth across income economies.

We have organized the rest of the paper as follows: In section 2, the study presents the review of theoretical background and empirical literatures. Then, in section 3, it describes the data collected and explains the methodology employed. Section 4 discusses the results of the estimated coefficients. Section 5 is the summary and policy implications of the study.

A Review of Theoretical Background and Empirical Literature

The conventional theories regarding the advent of MNCs are based on the views that firm-specific advantages and the oligopolistic markets dominated by MNCs are key prerequisite for FDI to occur (Dunning, 2001). These traditional theories and literatures which perceive MNCs investments as an activity that exploit competitive assets (Dunning, 2001; Knoerich, 2017) in host country is well documented. Recently, literatures on MNCs from developing countries have suggested otherwise and exposed the shortcoming in the traditional theories to fully explain the cross-border investment activities of MNCs. These development in FDI theory shows that, besides asset exploitation, firms conduct overseas direct investment in order to seek or enhance existing assets (Oetzel & Doh, 2009; UNCTAD, 2006). Thus, the major aims of MNCs in these countries (host) is to pursue economic activities that are related and supportive of the investments hitherto developed by the parent company in home country. This suggests that through outward FDI, firms’ production could increase, and their competitive position enhanced, and in-turn stimulate the domestic growth. Overseas direct investments spillover also improves home country technological know-how and management techniques which positively affects the overall production and economic growth of home country (Kokko, 2006; Osabuohien-Irabor & Drapkin, 2022b). These positive impact affects both the MNCs and the local manufacturing firms, thus benefiting the whole economy. Furthermore, firms may manufacture intermediate products via investments abroad and become domestically accessible at a very low price. However, empirical literatures concerning MNCs overseas direct investment are discussed in the sub-sections.

Institutional Quality and Outward FDI Nexus

Several empirical studies have shed light on the role of institutions in facilitating outward FDI flow. Globerman and Shapiro (1999) paper argued that good institutions have positive impact on FDI outflows and create favorable conditions for firms to emerge and invest in foreign country. However, empirical results revealed that the strength of informal institutions related to intellectual property (IP) enforcement positively moderates the effect of formal legal aspects of IP law on FDI flows (Papageorgiadis et al., 2020). A study conducted by Zheng et al. (2022) examined the impact of cultural distance (CD) and institutional distance (ID) on the efficiency of China’s outward FDI for a panel of 43 countries for the period 2003 to 2016, found a U-shaped relationship between cultural distance and the efficiency of China’s outward FDI. More so, study found that the Chinese outward FDI is invested in countries with abundant of natural resources and poor institutional quality, but the exchange rate variability has dampening effect on outward FDI (Y. Li & Rengifo, 2018). Mishra and Daly (2007) study explores the quality of institutions in OECD and Asian countries on overseas investment stocks for source countries using International Country Risk Guide governance indicators. Results showed that quality of institutions in the host countries have an overall positive and significant effect on source countries outward FDI.

Institutional Quality and Economic Growth Nexus

Growing numbers of studies have examined how institutional quality affect per capita GDP in different economy. Some of these studies includes, Ugur (2014), Arezki and van der Ploeg (2011), Baliamoune-Lutz and Ndikumana (2007), Dollar and Kraay (2003), etc. Examining 29 primary studies with extracted 327 estimates of corruption effect, per-capital GDP growth due to corruption effects have more adverse effects when the estimates from the primary study are linked with the long-run growth for low-income country (Ugur, 2014). Dependance on natural resource has negative and significant effect on per capita income in countries with bad policies and bad rule of law, after controlling for geography, and de-facto trade openness (Arezki & van der Ploeg, 2011). Using a derived fuzzy-set transformation based on freedom indices, Baliamoune-Lutz and Ndikumana (2007) study showed that weak institutional quality may reduce income per capita to a stage of “partial improvement,” with trade and financial reforms connected to unintended negative effects. In a cross-country analysis, Dollar and Kraay (2002) argues that the effects of per capita GDP on trade and institutional quality are uninformative about the relative importance of institutions and trade in the long run. Study conducted by Xu et al. (2021) showed that political stability, sound regulatory control, and global integration are positively linked to economic growth, and help achieve sustainable development. However, Kaneva and Untura (2019) study indicates that knowledge spillover efficiently disseminated to regions improve economic growth.

Outward FDI and Economic Growth Nexus

Empirical studies on outward FDI-growth nexus have continued to increase, but most documented literatures are on single country specific analysis. For instance, Ciesielska and Kołtuniak (2017) study investigate economic growth and outward FDI within the Polish national economy, and results indicate that the unidirectional growth-led internationalization is consistent with the Investment Development Path (IDP) paradigm concept. Positive long-run and bi-directional Granger-causality was detected in the relationship between outward FDI and economic growth of Malaysia, but results revealed nonexistence of causality in the short-run for the period 1980 to 2010 (Chena & Zulkifli, 2012). Amin et al. (2020) investigates the long-run and short-run asymmetric impacts of outward FDI-led growth in Romania covering the period 1990 to 2019. They found that increase or decrease in outward FDI have positive and significant impact on economic growth. The effects of the Chinese outward FDI on home country economic growth both in the long-run and short-run showed that growth responds positively but differently to increase and decrease in outward FDI (Ali et al., 2018). Herzer (2010) study showed that outward FDI is positively linked with economic growth in a cross-country regression of 50 countries, and the causality test for USA indicates that increase in outward FDI is both a cause and a consequence of increased domestic output.

Outward FDI, Economic Growth, and Institutional Quality Nexus

Recently, strand of literature on the relationship between FDI flow, institutional quality, and economic growth have gained attention, see; Soh et al. (2021), Baiashvili and Gattini (2020), Aziz (2020), Hayat (2019), Bouchoucha and Yahyaoui (2019), Jude and Levieuge (2017), Alguacil et al. (2011). These papers focus on inward FDI internationalization of host country and employ different empirical techniques. For instance, Hayat (2019) study showed that FDI inflow slow down economic growth in high-income countries due to the indirect impact of institutional quality, but in low-and-middle income countries, FDI-led growth was experienced. Baiashvili and Gattini (2020) paper found that the nexus between income level and the magnitude of FDI-growth is inverted U-shaped, which get larger moving from low to middle-income countries. However, the results from Soh et al. (2021) paper found a threshold effect for logistic performance and FDI relationship mediated by institutional quality for Asia countries. Similarly, study revealed that FDI impact on economic growth is significant only when institutional quality is above a certain threshold (Jude & Levieuge, 2017). Nevertheless, empirical studies that examines the role of institutional quality in outward FDI-induced growth remain unexplored, particularly at different income groups, as existing literature focuses on examining “FDI inflow” in host countries. Oversea direct investment may complement or substitutes domestic production when firms move parts of the production to foreign country. Their competitive positions are improved, and the spillover effect enhances home country economic growth, but role of home country institutions remain very crucial in facilitating these effects.

Methodology and Data

Data Description

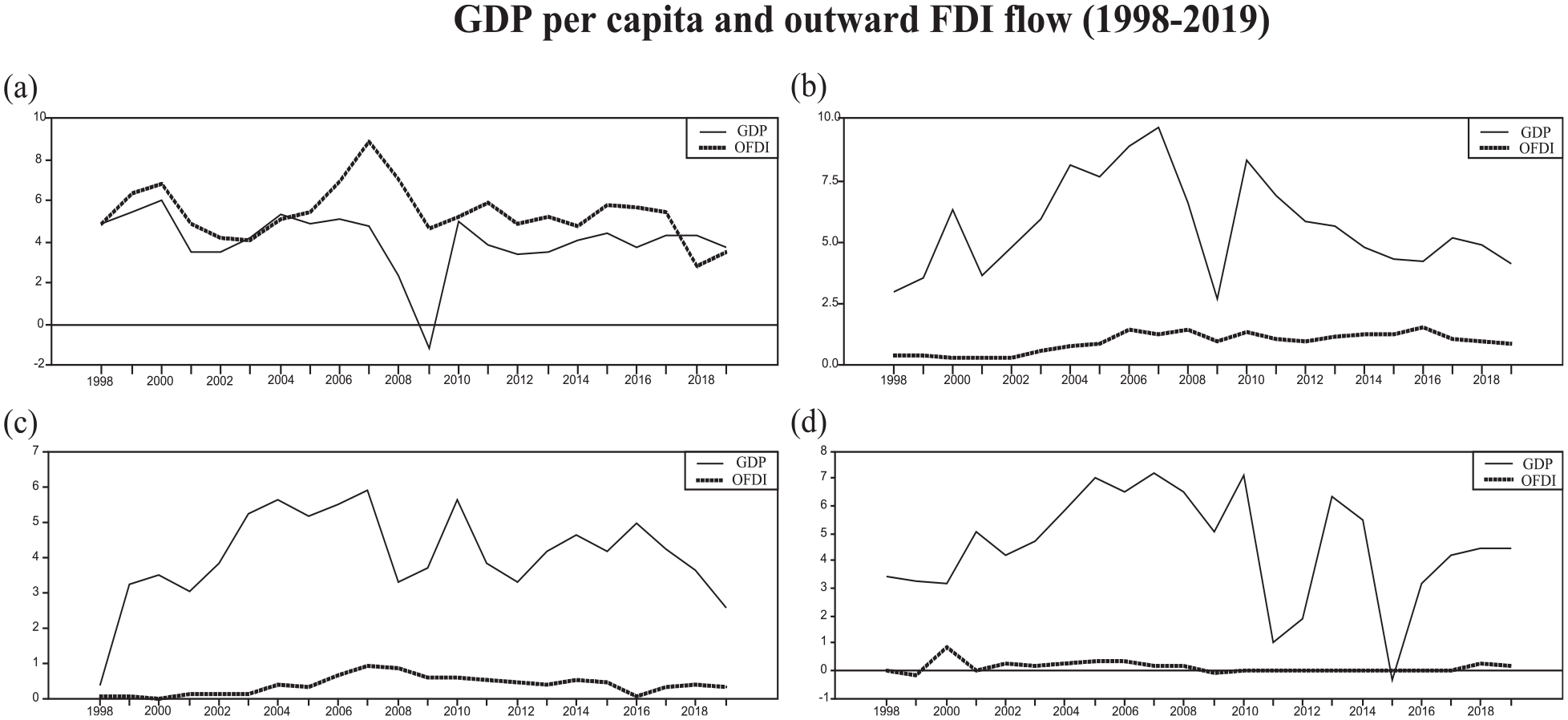

This study examines the impact of outward FDI-growth mediated by home country institutions whilst controlling for economic factors such as gross fixed capital formation (X), and trade openness (Z) for the period 1998 to 2019. The effects of the six institutional indicators (Kaufmann et al., 2009) in outward FDI-induced economic growth is examined. These indicators include voice and accountability (VA), political stability and absence of violence (PS), government effectiveness (GE), regulatory quality (RQ), rule of law (RL), and control of corruption (CC). We applied log (3+institutional value) to deal with the negative signs associated with institutional quality. Data is collected from 161 countries and split based on the world bank income economies classification such as high-income (51 countries), upper-middle income (47 countries), lower-middle income (41 countries) and low-income (22 countries) economies (see Table A1). These countries and data are selected based on the availability of dataset for the period under study. While Table 1 presents the variables and data sources, Figure 1 illustrates graphically, the past two decades linkage between outward FDI and economic growth. Precisely, the graphs show outward FDI-economic growth relationships at different income groups for the period 1998 to 2019.

Definitions of Variables and Data Sources.

Plots showing per capita GDP and outward FDI relationships in different income classifications such as high-income, upper-middle, lower-middle, and low-income economies: (a) high income, (b) upper-middle income, (c) lower middle income, and (d) low income.

Estimation Strategy

Following the construction of economic models by X. Li and Liu (2005), P. M. Romer (1990), Levine and Renelt (1992) which suggests that GDP is a function of other independent variables, this study examines the impact of outward FDI (Y) on economic growth (S) given the quality of home country institutions across different income clusters. We begin with the growth model shown in equation (1), then examine the existence of cross-sectional dependence heterogeneity, and endogeneity in the model.

Where

S = growth, X = gross capita formation, Y = outward FDI, Z = Trade openness, ISQ = Institutions.

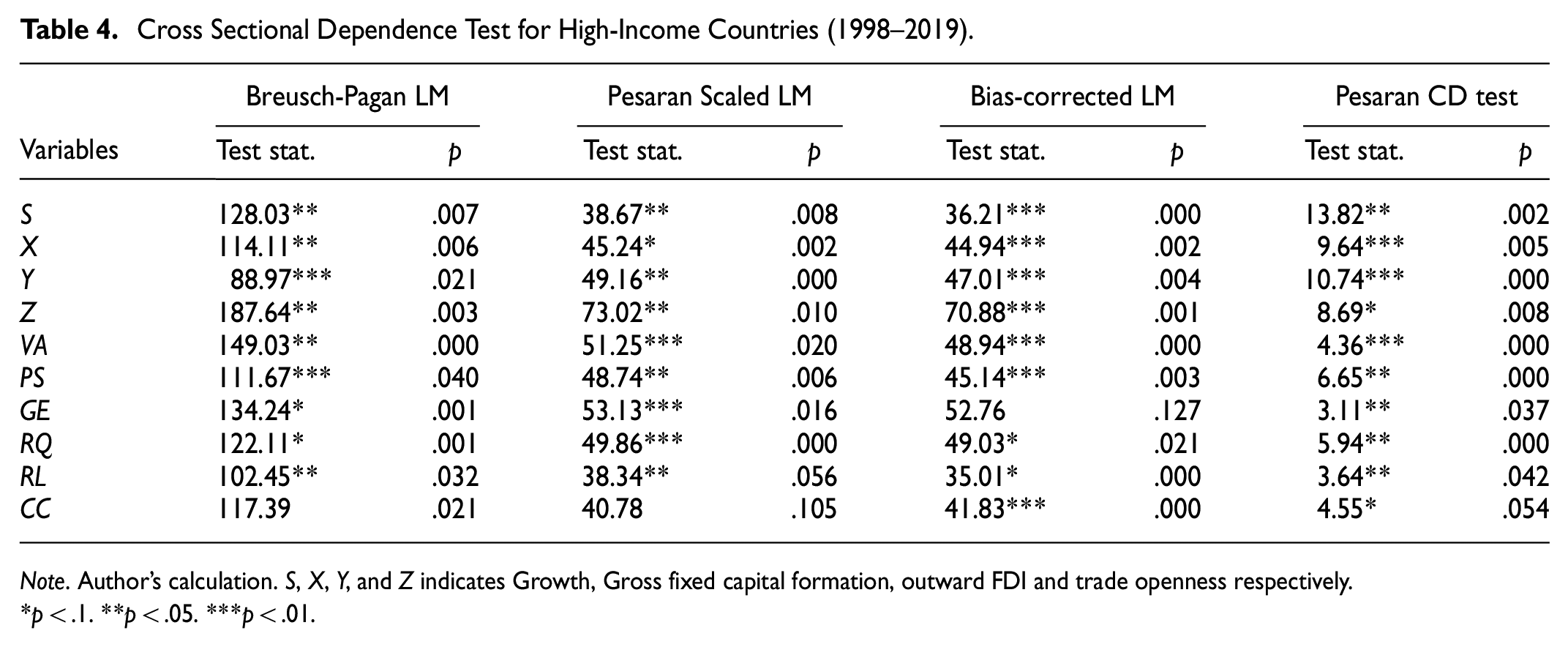

Cross-Sectional Dependence (CSD) Test

Cross-sectional dependence (CSD) in panel analysis may bring about bias estimate and inconsistent results due to unobserved shocks (Phillips & Sul, 2003), hence it is considered as the most critical test in panel data analysis. Thus, CSD assumption in panel analysis is not appropriate for empirical investigation. Similarly, the traditional panel unit root methods assume non-occurrence of spill-over effect in cross countries analysis, but in-reality, cross-sectional dependency may arise due to numerous factors (Hsiao, 2003; Pesaran & Tosetti, 2011). To address this issue, this study employs the CSD test introduced by Pesaran (2004) under the null hypothesis of cross-sectional independence, and for result consistency, four CDS tests are utilized. These include the Breusch-Pagan Lagrange Multiplier (LM), the Pesaran Scaled Lagrange Multiplier (LM), Bias-corrected (LM) and the Pesaran Cross-sectional Dependence (CD). The Pesaran (2004) CSD test equation is given as follows:

Where T represents the time (period), N indicates panel cross-section, and

Slope Homogeneity Test

If homogeneity of the slope is assumed, the estimated model will be bias and inconsistent if the assumption about the slope parameters of the equation is false (Hernández, 2015; Osabuohien-Irabor & Drapkin, 2022b). Therefore, this study examines whether the slope coefficients of the cointegration equation in cross-section are homogenous. The slope homogenous tests developed by Swamy (1970) and improved by M. Pesaran and Yamagata (2008) investigates the null hypothesis (

Where N is the numbers of cross-sectional unit; S indicates the Swamy test statistic; k is the independent variables. If the null hypothesis is accepted, then the cointegrating coefficients is considered homogenous.

Panel Unit-Root Test

The standard panel unit root techniques, such as the Breitung (2000), Levin et al. (2002), Im et al. (2003), Maddala and Wu (1999) tests, may yield misleading results in the presence of cross-sectional dependence (Bhattarai, 2021; Osabuohien-Irabor & Drapkin, 2022a; Tugcu, 2018). To get more efficient technique to address this issue, Pesaran (2007) combined both the Augmented Dickey-Fuller and IPS tests to examine panel stationarity under cross-sectional dependence. To this end, this study employs Pesaran (2007) cross-sectional Augmented Dickey-Fuller (CADF) and cross-sectional Im-Pesaran-Shin (CIPS) tests to examine unit root in panel data. The CADF test is given as:

Where

The null and the alternative hypotheses is

Panel Cointegration Test

This study applies the Westerlund (2007) dynamic panel cointegration test to determine whether long-run cointegrating relationship exist among the variables listed in Table 1 due to cross-sectional dependency and heterogeneity. The test is based on structural form rather than the residual dynamics cointegration test using the error correction model (ECM). Its can be applied on the condition that the dependent variable is I(1) and the independent variables are at different integration levels. The test is robust, and the results are reliable with the null hypothesis of no cointegration in the error-correction term (ECT). For instance, equation (7) illustrates the cointegrating relationship between the dependent variable (

Where

The Westerlund (2007) test statistics are partitioned in two—the panel statistics

where

Where,

The Null and alternative hypotheses to be investigated are

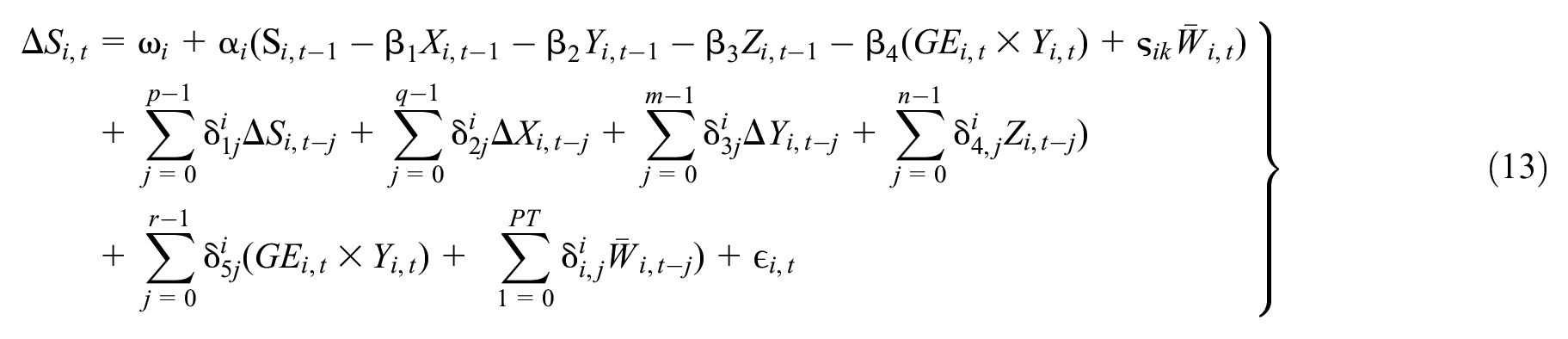

Cross-Sectionally Augmented Autoregressive Distributed Lags (CS-ARDL)

Empirical studies have showed that using the first generation cointegration techniques such as the Fully Modified Ordinary Least Squares (FMOLS) and the Dynamic Ordinary Least Squares (DOLS) may give rise to bias and inconsistent estimates in the presence of cross-sectional dependence and heterogeneity in panel (Ahmad et al., 2022; Azam & Haseeb, 2021). The unobserved factors may be correlated with the errors term and distort the true parameters if these estimators are used (Azam & Haseeb, 2021). The autoregressive distributed lags (ARDL) model is considered as one of the most desired second-generation heterogeneous panel data estimators that have been applied to many cointegration analysis. For instance, Pradhan and Bagchi (2012) examined expenditure-GDP nexus in seven SAARC countries, Vinayagathasan and Ramesh (2022) investigates Corruption-Poverty nexus also of SAARC countries, Ismail (2017) analyzed military expenditure and economic growth relation in South Asian countries, etc. In line with M. H. Pesaran et al.’s (1999) paper, the panel ARDL technique is given as,

Where

Nevertheless, empirical studies have showed that the traditional ARDL model adequately accounts for slope heterogeneity regardless of whether the regressors are exogenous (Zhenxiong & Hilary, 2020), but the model’s inability to address potential cross-sectional dependence error in panel, remains it major drawback (Phillips & Sul, 2003; Wooldridge, 2002). To overcome this problem, Chudik and Pesaran (2015) proposed the cross-sectional autoregressive distributed lags (CS-ARDL) model to capture the cross-sectional correlation in the error term associated with the traditional ARDL model. This was done by adding the linear combinations of cross-sectional averages of the dependent and explanatory variables. Zhenxiong and Hilary (2020) study specified the CS-ARDL model as,

Where

Model Specifications

The specified models shown in equations (10) to (17) examines the short-run and long-runs effects of outward FDI-induced growth mediated by home country institutions using the CS-ARDL techniques proposed by Chudik and Pesaran (2015). Noticeably, the equation distinguishes the short-term and long-term behaviors of the cross-sectional correlations, given as follows:

Model-I

Model I examine the impact of the short and long-runs effects of outward FDI (Y), gross capital formation (X), trade openness (Z), on home country economic growth without the effect of institutional quality. The

Model-II

In examining the short and long-run effects, model II also investigates the interaction of voice and accountability (VA) with outward FDI (Y) on home country economic growth. Thus, the VA induced outward FDI on economic growth is evaluated.

Model-III

Model III, equation (12) shows the impact of the joint effect of political stability and outward FDI for home country. The effects are evaluated both in the short-run and long-run.

Model-IV

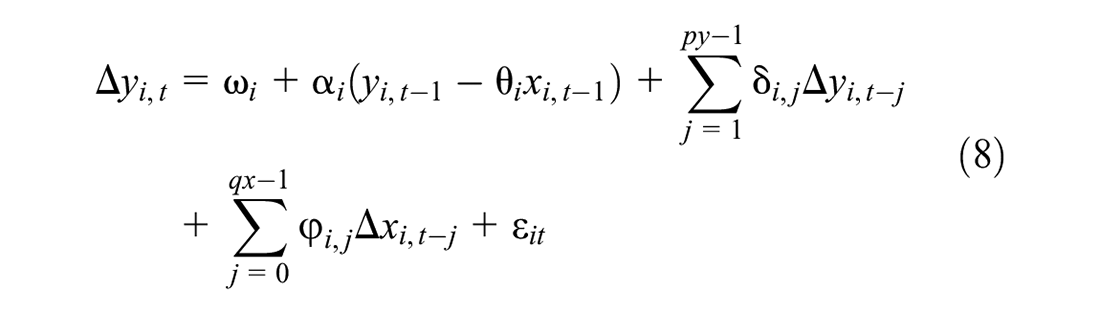

To examine the mediating effects of governance effectiveness (GE) in the impact of outward FDI (Y) on economic growth (S), model IV shown in equation (13) is utilized. The control variables such as X and Z are also evaluated in the short-run and long-run.

Model-V

The effect of outward FDI-led economic growth based on home country regulatory quality (RQ) is examined in model V. This reveals the effect of the combination of

Model-VI

Model VI is constructed to specifically examine how home country rules and regulation (RL) impact outward FDI-led economic growth both in the short-run and long-run. It also captures the direct and indirect impact of the variables.

Model-VII

We construct the effect of the joint impact of control of corruption (CC) and outward FDI (Y) on growth. The effect is shown in model VII as

Model-VIII

Model VIII shows the impact of the interaction of outward FDI and the combined six institutional components

Results and Discussion

Descriptive Statistics Analysis

Table 2 describes the summary statistics for different income economies groups. The average values of Y decreases from high-income countries to low-income countries which indicates that outward FDI-internationalization activities from home country is highest in high-income countries (1.917) and lowest in low-income (1.007). The standard deviation of outward FDI is highest (0.986) in countries with low-income and suggests large amount of variability in the data points. However, the mean value of X for high-income is (3.039), upper-middle (3.099), lower-middle (3.096), and low-income (2.981) countries. Interestingly, the average S for the period under study shows to follow similar pattern of Y. S is lowest in low-income countries with an average value of 1.009 and highest in high-income countries with an average value of 1.498. The S and Y variables show to be monotonically increasing from high-income to low-income economy clusters for the period 1998 to 2019. The growth rate volatilities show to be most stable in high-income group with a standard deviation of 0.059 compared to other income economy groups. For Z, high-income countries show to have more trade openness policies compared to other income groups. Except low-income group, the average values of institutional indicators are positive in all income economies.

Summary Statistics for World Bank Income Economies Cluster 1998 to 2019.

Source. World Bank database: https://data.worldbank.org/.

Note. Author’s calculations. S, X, Y, and Z indicates Growth, Gross fixed capital formation, outward FDI and trade openness respectively.

Cross-Sectional Dependence and Slope Homogeneity

This section investigates the existence of heterogeneity and cross-sectional dependence among variables across income groups using the slope homogeneity test by M. Pesaran and Yamagata (2008). Results show that in all income groups, the delta (

Pesaran-Yamagata Homogeneity Test for High-income (1998 to 2019).

Note. Author’s calculation.

p < .1. **p < .05. ***p < .01 3. H0: slope coefficients are homogenous.

Cross Sectional Dependence Test for High-Income Countries (1998–2019).

Note. Author’s calculation. S, X, Y, and Z indicates Growth, Gross fixed capital formation, outward FDI and trade openness respectively.

p < .1. **p < .05. ***p < .01.

Panel Unit Root Tests

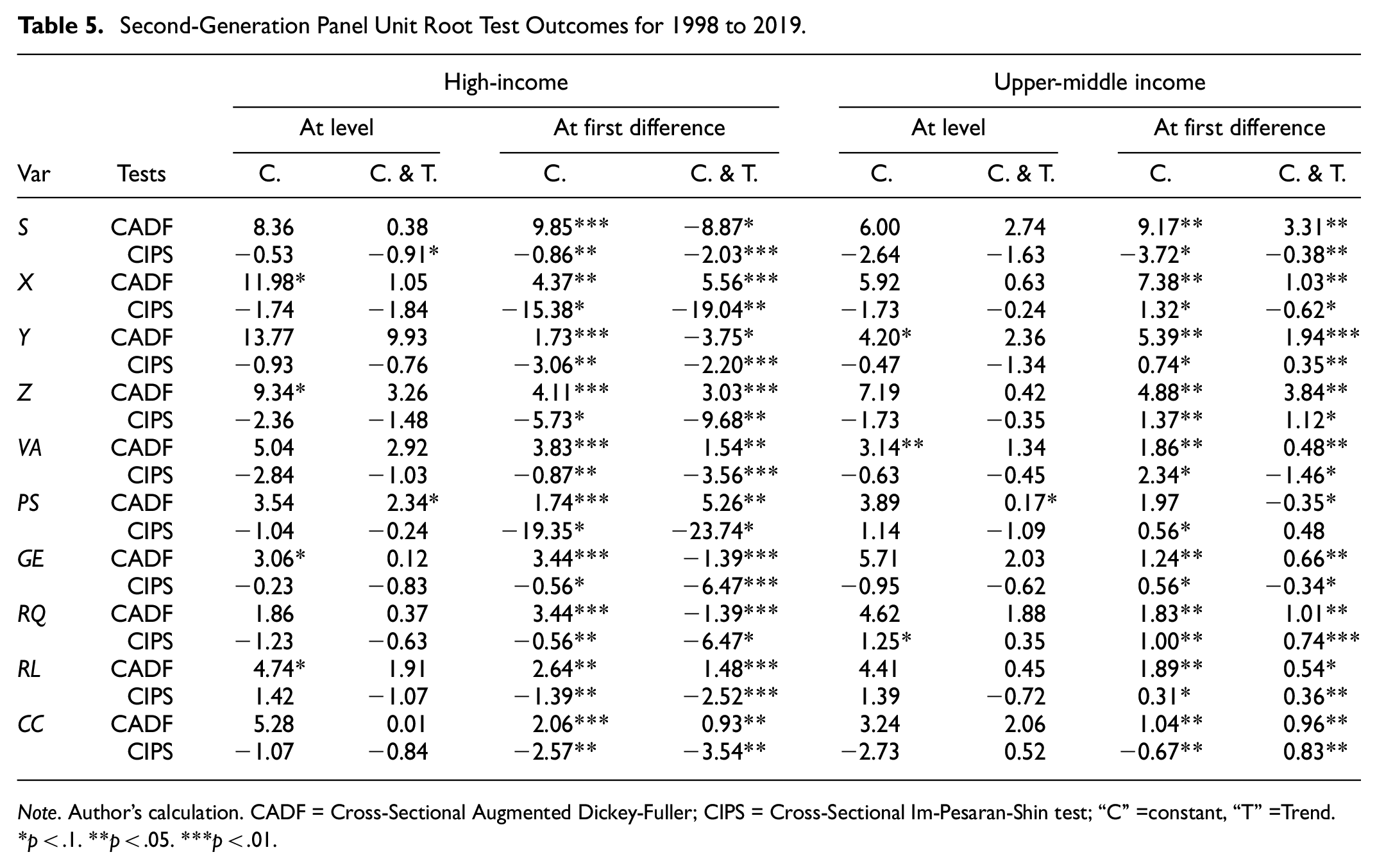

The stationary property among the variables is examined using the CIPS and CADF tests proposed by Pesaran (2007). These tests specifically investigate the constant (C), and constant (C) plus trend (T) both at the level and at first differenced. Results from High, upper-middle, lower-middle and low-income groups indicate that the variables appear non-stationary I(0) at level using the constant, and constant & trend, but after the first difference the variables became stationary I(1) and significant. This shows that the variables in this study have a unique order of integration I(1) which suggests the use of an advanced econometric technique such as ARDL to examine the long-run association between the variables. ARDL model is applicable where variables are in I(I) or I(0) or a mixture of both I(0) and I(1) but certainly not I(2) (Pesaran et al., 2001). Table 5 presents the panel unit root results of CIPS and CADF tests for high and upper-middle income countries. Results for lower-middle and low-income are available on request.

Second-Generation Panel Unit Root Test Outcomes for 1998 to 2019.

Note. Author’s calculation. CADF = Cross-Sectional Augmented Dickey-Fuller; CIPS = Cross-Sectional Im-Pesaran-Shin test; “C” =constant, “T” =Trend.

p < .1. **p < .05. ***p < .01.

Cointegration Test

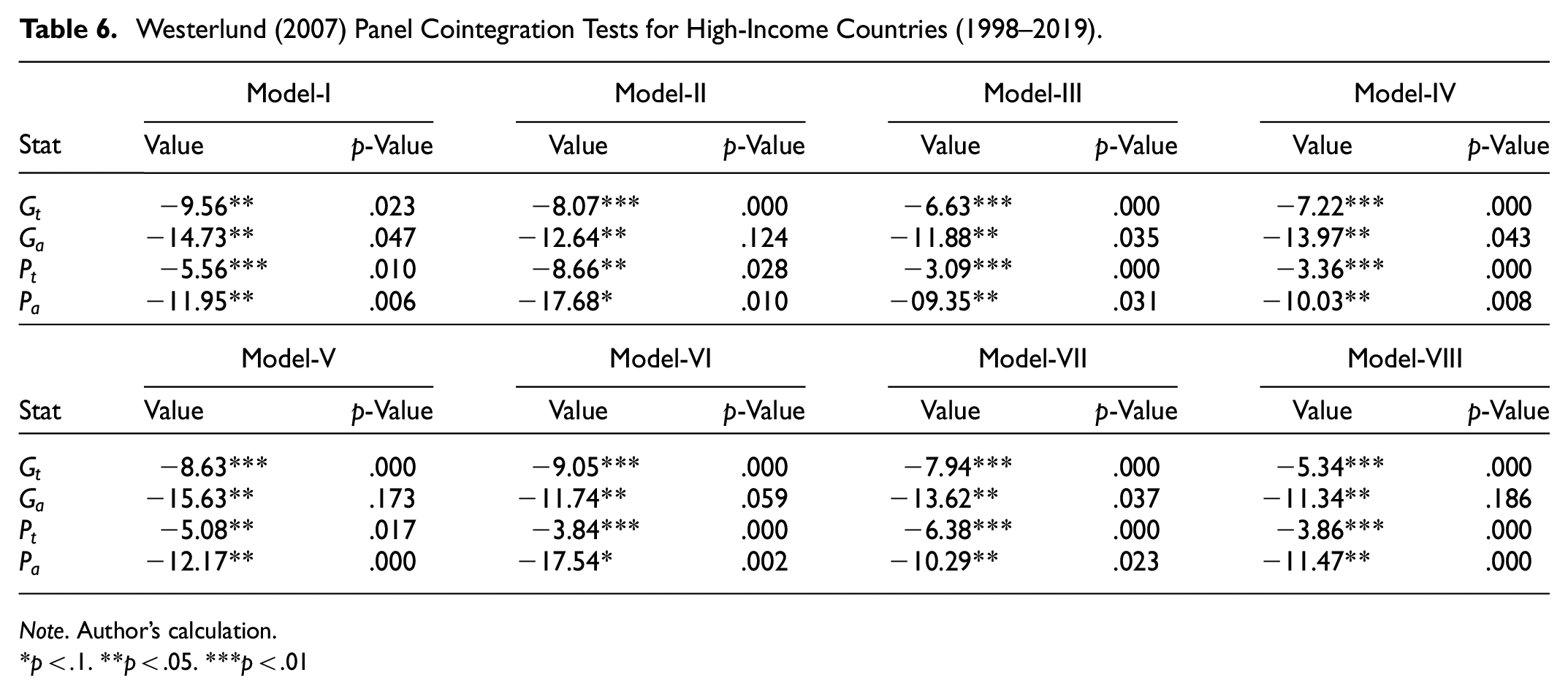

The Westerlund (2007) cointegration test can be used to examine cointegration in the presence of heterogeneity and cross-sectional dependence among variables. The test provides p-values that are quite consistent and robust to dependent and independent variables. In high-income, upper-middle, lower-middle, and low-income group, results indicate that the p-values of at least one cross-sectional (Gt or Ga) and the two panel statistics (Pt and Pa) give evidence that the null hypothesis of “no cointegration” is rejected at 1%, 5%, and 10% significance level, see Table 6 for high-income group. This suggests the existence of long run cointegration relationship between growth and explanatory variables. Thus, the need to employ an econometric technique to estimate the long-run and short-run dynamic. But with the presence of CSD and heterogeneity in panel, this study adopts the CS-ARDL technique by Chudik and Pesaran (2015) robust to heterogeneity and cross-sectional dependent to examine the long-run relationship between S, X, Y, and Z in all income groups.

Westerlund (2007) Panel Cointegration Tests for High-Income Countries (1998–2019).

Note. Author’s calculation.

p < .1. **p < .05. ***p < .01

Impact of Outward FDI on Economic Growth via the Mediation of Country Institutions

Economic Growth, Outward FDI, and Institutions in High Income Countries

According to the results show in Table 7, the coefficient of the ECM term which measures the speed of adjustment toward equilibrium is significantly negative and confirms the existence of a stable cointegration among the variables in long-run. This suggests that the system reverts quickly to long-term equilibrium in case of a shock, at an average speed of 68.36%. However, the impact of outward FDI-growth is positive and significant both in the short-run and long-run, but with a stronger effect in the long-run. Positive impact implies increase in production and economic growth in home country which further stimulate firms to conduct cross border investments. This shows that a 1% increase in outward FDI leads to an increase in economic growth by an average of 0.310% and 0.351% in the short-run and long-term respectively. These findings coincide with some previous studies on countries with high-income using single analysis. For instance, Barba Navaretti and Castellani (2004) study found that outward FDI improve the growth of total factor productivity and output of Italy; outward FDI was found to strengthens the economic activities of Japanese firms (Hijzen et al., 2007); the effect of Outward FDI in German economy shows growth-enhancing (Herzer, 2012).

CS-ARDL Estimations Outcome for High Income Countries (1998–2019).

Note. Author’s calculation; Δ indicates difference, WOI indicates model “without institutions.”

S, X, Y, and Z indicates Growth, Gross fixed capital formation, outward FDI and trade openness respectively.

p < .1. **p < .05. ***p < .01, values in the parentheses are robust standard errors.

The coefficient of outward FDI interactions with home country institutions is positive and larger than the direct impact of outward FDI-growth both in the long and the short-term. This suggests that institutional component in high-income countries indirectly enhances economic growth by facilitating and stimulating outward FDI. This finding is consistent with numerous studies such as Globerman et al. (2004)—developed countries; Globerman and Shapiro (2002)—developing and developed countries; etc., which argues that high quality institutions strongly determine the internationalization of innovative activity in home country. Furthermore, result indicates that government effectiveness (GE) in high-income countries contribute most to outward FDI-growth improvement in the short-run and long-run. This shows that efforts by home country to improve on governance effectiveness, strengthens the impact of outward FDI on economic growth by 0.542% and 0.585% in the short-term and long-term respectively. This is followed by maintaining political stability (PS) which improves outward FDI-induced economic growth by 0.518% and 0.576% in the short-run and long-run respectively. The post estimation CSD test results confirm the absence of cross-sectional dependence among variables which in-turn validates the estimated coefficients.

Economic Growth, Outward FDI, and Institutions in Upper-Middle Income Countries

Table 8 results show that the impact of outward FDI-growth is positive in all models in the short-run and long-run. In the short run, it is evident that a 1% increase in outward FDI leads to an increase in economic growth within 0.096% to 0.313%. Regarding the long-run elasticity, results show that a 1% increase in outward FDI leads to economic growth within the range of 0.117% to 0.387%. This finding implies that outward FDI may increase home country economic growth via technology spillover effects (Clark et al., 2011; S. Zhu & Ye, 2018), repatriation of return on investment to home country for reinvestment purpose or to upgrade production processes (Brooks & Jongwanich, 2011). However, the long-run estimated coefficients appear larger compared to the short-run indicating that outward FDI has stronger impact on economic growth at the long-run. The coefficients of ECM(−1) term are negative and statistically significant, which implies that the system may return to steady state at an average speed of 53.03% if there is a shock that causes disequilibrium.

CS-ARDL Estimations Outcome for Upper-Middle Income Countries (1998–2019).

Note. Author’s calculation; Δ indicates difference, WOI indicates model “without institutions.”

S, X, Y, and Z indicates Growth, Gross fixed capital formation, outward FDI and trade openness respectively.

p < .1. **p < .05. ***p < .01, values in the parentheses are robust standard errors.

More so, the coefficients of the impact of outward FDI-growth via home country institution are positive, significant, and larger than the coefficients of the direct impact of outward FDI on growth both in the short and long-run analysis. This suggests that home country institutional components enhance outward FDI-induced economic growth in upper-middle income countries in the short-and long-term. Specifically, political stability (PS) in upper-middle income countries appear to be the most contributing factor in outward FDI-induced growth. This implies that given the level of home country political stability (PS), a 1% increase in outward FDI leads to 0.533% and 0.572% increase in economic growth in the short-run and long-run respectively. The p-values of the CSD tests indicate no cross-sectional dependence among the variables which further validates the robustness of estimated coefficients.

Economic Growth, Outward FDI, and Institutions in Lower-Middle Income Countries

Table 9 presents the estimated results on the role of home country institutions in outward FDI-induced economic growth in low-middle income country using the CS-ARDL technique. The impact of outward FDI-growth in home country indicates mixed results in the short-run, but the effect among the various models in the long-run is positive and unanimous. The mixed results may be due to home country specificity and factors affecting outward FDI in different countries. Negative impact suggests that overseas direct investments in some low-middle income countries may decrease growth by crowding out domestic investments, substitute exports (Osabuohien-Irabor & Drapkin, 2021), give rise to hollow-out effects which may lead to unemployment and recession in home country (Huijie, 2018; Liu et al., 2015). However, more positive signs in the model results (two against eight) shows that many lower-middle income countries benefit from the impact of outward FDI which promotes home country economic growth. The coefficients of all the ECTs term are negative and significant which indicates that the systems revert to equilibrium at an average speed of 48.71% in case of a shock that causes a disequilibrium. This further implies that mean half-life disequilibrium (50% of the deviation) will occur in about 1.038 years (approximately 1 year).

CS-ARDL Estimations Outcome for Lower-Middle Income Countries (1998 to 2019).

Note. Author’s calculation; Δ indicates difference, WOI indicates model without institutions.

S, X, Y, and Z indicates Growth, Gross fixed capital formation, outward FDI and trade openness respectively.

p < .1. **p < .05. ***p < .01, values in the parentheses are robust standard errors.

The result of the interaction of outward FDI with home country institutional quality is positive and significant in all models. This implies that home country institutions strengthen outward FDI-induced economic growth in lower-middle income countries both in the short and long-run. Interestingly, control of corruption (CC) component shows to be the least contributing factor to outward FDI-growth both in the short term and long-term. This implies that steps by governments to curb corruptions in lower-middle income countries only boost outward FDI-growth by 0.003% and 0.027% respectively in the short and long term. Contrarily, government effectiveness (GE) has the greatest impact in outward FDI-growth, which implies that efforts by government in lower-middle income countries to better service delivery to it citizenry improves the effect of outward FDI-induced economic growth by 0.121% and 0.147% in short and long-run respectively. The p-values of post estimation test of Pesaran (2004) CD show that the estimated coefficients are cross-sectionally independent, thus the estimated coefficients are reliable.

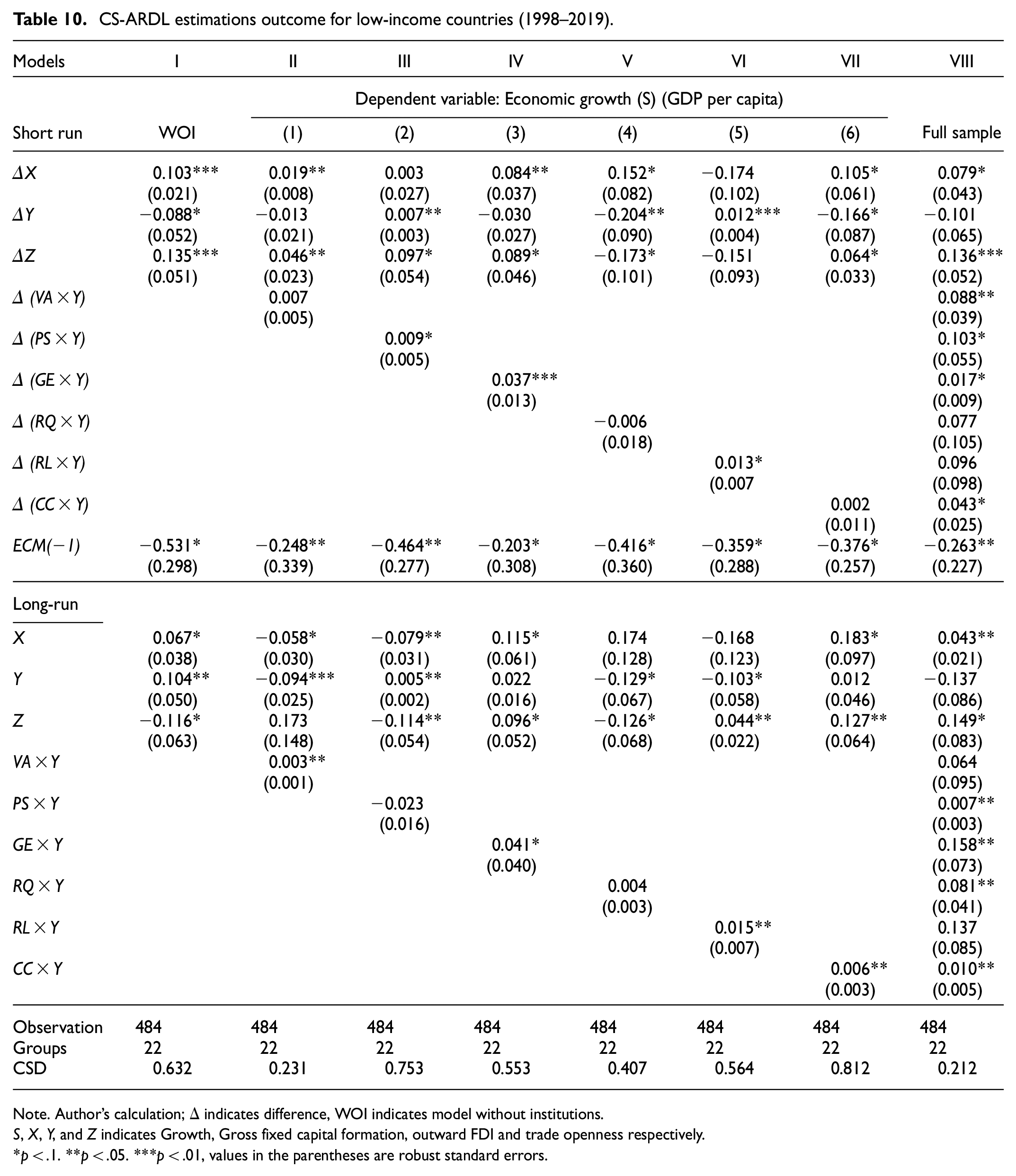

Economic Growth, Outward FDI, and Institutions in Low-Income Countries

The results reported in Table 10 clearly indicate that the ECM term is negatively significant, suggesting an average recovery speedy of 35.75% from any short-run disequilibrium in the long-run, which suggests that the mean half-life disequilibrium will be about 1.566 years (almost 1-year 6 months). For the impact of outward FDI on growth in the short-run, six out of eight experimenting models show negative results, but in the long-run, four out of eight models indicate negative effects. This suggests that outward FDI in low-income countries have adverse effects on economic growth both in the short-and long-term, but the negative impact seems severe in the short-term. The implication for the negative effect implies that increase in outward FDI leads to a decrease in economic growth in low-income countries. More so, negative effects of outward FDI on growth also suggests FDI escapism (Osabuohien-Irabor & Drapkin, 2022a), as MNCs may initiate an escape strategy due to institutional void (Doh et al., 2017; Stoian & Mohr, 2016); political instability (Osabuohien-Irabor & Drapkin, 2022a) as well as misalignment between MNCs and domestic firms, which affects economic growth negatively (Barnard & Luiz, 2018).

CS-ARDL estimations outcome for low-income countries (1998–2019).

Note. Author’s calculation; Δ indicates difference, WOI indicates model without institutions.

S, X, Y, and Z indicates Growth, Gross fixed capital formation, outward FDI and trade openness respectively.

p < .1. **p < .05. ***p < .01, values in the parentheses are robust standard errors.

Although the joint impact of outward FDI and institutions on home country economic growth is positive, but the coefficient of the combined impact is small compared to lower-middle, upper-middle and high-income countries. This indicates that the impact of home country institutions in outward FDI-growth appears weak both in the short term and long term. Nevertheless, the impact of the interaction of VA × Y, RQ × Y, and CC × Y are insignificant in the short-term, while PS × Y and RQ × Y are insignificant in the long run. However, GE, RL, and CC appear to positively affect growth in the long run. Overall, finding suggests that countries with low wage appears not to benefit from MNCs outward-internationalization activities, and the role play by home country institutions in stimulating outward FDI-induced growth appears weak. This may be due to the small number of MNCs investments and financially constrained domestic firm, leading to an economy with lack of investment capital and weak institutional framework.

Robustness Checks and Further Analysis

This section examines the consistency of the estimated results by CS-ARDL techniques proposed by Chudik and Pesaran (2015), by re-examining outward FDI and economic growth relationship mediated by home country institutions using the the Common Correlated Effect Mean Group (CCEMG) proposed by Pesaran (2006). Both the CS-ARDL and CCEMG estimators are equally efficient to produce reliable estimates in the presence of endogeneity, heterogeneity, and cross-sectional dependence. The representation of the CCEMG model according to Azam and Haseeb (2021), Josifidis et al. (2018) is:

Where

Evaluating equation (18), leads to equation (19)

The relationship is specified in the growth model I–VIII, and the estimated results are presented in Tables A2 to A5. The results for high and upper-middle income countries reported in Tables A2 and A3 shows that the coefficients of the impact of outward FDI-growth is positive and statistically significant except in model I and VIII for high and upper-middle income countries and indicates improvement of home country economies growth. The interactions of outward FDI and institutions are also positive and significant for high and upper-middle income countries suggesting that home country institution improves economic growth. Government effectiveness (GE) and political stability (PS) in high and upper-middle income countries respectively appears to promote outward FDI-induced economic growth more than any other institutional indicator. These findings confirm the long-run results showed in Tables 7 and 8 using CS-ARDL techniques.

Regarding the impact of outward FDI-growth in lower-middle countries, five of the estimating models show positive and significant effect, whilst the other three models also show positive results but insignificant effects (Table A4). Nevertheless, almost all the estimating models reports negative and significant effects in the impact of outward FDI on growth in low-income countries using CCEMG estimator—see Table A5. These results also coincide with the estimated long-run coefficient of CS-ARDL technique reported in Tables 9 and 10. However, the indirect impact of outward FDI on economic growth via home country institution appears positive in lower and low-income countries, but the magnitude of the coefficients compared to high and upper-middle income countries is small. This indicates that institutional quality as well as income levels play a significant role in the spillover of outward FDI on home country economic growth. These results are robust and correspond to the long-run results of Tables 9 and 10 using CS-ARDL technique.

Conclusions

This study examined the role of institutions in outward FDI-growth nexus in global panel of 161 countries split into different income groups based on the world bank income classifications viz. high, upper-middle, lower-middle, and low-income countries for the period 1998 to 2019. Several second-generation tests (slope homogeneity test, CSD test, CADF test, and CIPS test) and heterogeneous panel cointegration techniques (CS-ARDL and CCEMG techniques) were employed to tackle econometric problems such as cross-sectional dependence, endogeneity, as well as heterogeneity in panel. The study revealed several interesting results both for the direct impacts of outward FDI-growth and its indirect impact via home country institutions in different income economies. The findings are highly significant, sensitive to different income clusters, consistent with modern global economy, and specifically contributes to the growing literature on outward FDI-growth relationship.

The study finds that the impact of outward FDI on economic growth in high, upper-middle, and lower-middle income countries positively affect economic growth both in the short-term and long-term. This supports the new outward FDI-induced growth theories consistent with the notion that overseas direct investment increases domestic production, facilitates transfer of technology, and stimulates economic growth which help integrates domestic economy into the global economy. On the contrary, the impact of outward FDI on economic growth in low-income countries is significantly negative, implying that overseas direct investments activities in low-income countries may have adverse effects on home country economic growth. This suggests MNCs activities crowding-out investments. FDI may also be escaping the economy or MNCs relocating investments in low-income countries to avoid competitive disadvantages. In the same vein, the impact of institutions in stimulating outward FDI-growth appears weak both in the short-term and long-term, suggesting that the indirect channel outward FDI impact economic growth in low-income countries is weak and may not promote growth.

Furthermore, finding reveals that the combine effect of outward FDI and institutions in high-income, upper-middle income, and lower-income countries enhance economic growth both in the short-run and long-run. This suggests mutual reinforcement which stimulates economic growth and increases competition among investing firms. Thus, the impact of outward FDI-growth become more effective when it is linked with strong national institutions. However, the magnitude of the impact of outward FDI-led growth mediated by institutions vary across income economies and appears larger in high and upper-middle income economies compared to lower-middle and low-income countries. These impacts were found to diminish moving from high to low-income countries.

Regarding individual institutional components, the effect of outward FDI-induced economic growth is non-uniform across country income groups. However, government effectiveness (GE) in delivering quality services contribute most to outward FDI-induced economic growth in almost all income groups, followed by government efforts in maintaining political stability (PS). Control of corruption (CC) appears to contribute least to the improvement of outward FDI-induced growth in upper-middle and lower-middle income countries both in the short-run and long-run. In low-income countries, results show that government effectiveness (GE) and political stability (PS) are the most and least impacting institutional components to outward FDI-led growth respectively. Overall, findings indicate that outward FDI spillover is more likely to stimulate higher economic growth in the presence of effective government with better quality of public service and policy formulation in a politically stable economy.

The empirical findings in this study highlights that policy implications are more relevant in low-middle and low-income countries where the impact of outward FDI-growth via home country institutions appears weak. Therefore, policymakers should consider holistic strategy that includes upgrading national institutions, improving the absorptive capabilities of local firm, and enacting sound economic policies that integrates FDI policies with national institutions in order to strengthen the overseas investment impact on economic growth. However, the variations in institutional quality across income groups is certainly not the only factor that vary the impact of outward FDI spillover on economic growth. Many other determinants such as resource endowments, political stability, level of economic development etc., may potentially impede overseas direct investment in some countries. Thus, examining the mediating impact of these factors to explain outward FDI differences across group of countries, especially developing countries may be a potential area for future research. Nevertheless, the findings of this study are limited to the variables selected, the econometric techniques applied, the sample of countries used, as well as the period analyzed.

Footnotes

Appendix 1

CCEMG Estimations for Low-Income Countries (1998–2019).

| Models | I | II | III | IV | V | VI | VII | VIII |

|---|---|---|---|---|---|---|---|---|

| WOI | Dependent variable: S (GDP per capita) | Full sample | ||||||

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | ||

| X | 0.092* (0.048) | 0.331 (0.175) | −0.284** (0.163) | 0.132 (0.184) | 0.147*** (0.033) | 0.106* (0.057) | −0.318 (0.199) | 0.105* (0.054) |

| Y | 0.206** (0.095) | −0.313** (0.128) | −0.121 (0.087) | −0.118** (0.053) | −0.078** (0.034) | −0.211* (0.114) | −0.091* (0.047) | 0.152* (0.087) |

| Z | −0.046*** (0.011) | 0.117 (0.083) | −0.186** (0.111) | 0.362 (0.228) | −0.127** (0.062) | 0.105 (0.125) | 0.318** (0.157) | −0.077 (0.055) |

| VA × Y | 0.098* (0.051) | 0.135* (0.071) | ||||||

| PS × Y | 0.107** (0.053) | 0.109*** (0.003) | ||||||

| GE × Y | 0.130** (0.065) | 0.087 (0.062) | ||||||

| RQ × Y | 0.115 (0.084) | 0.103** (0.047) | ||||||

| RL × Y | 0.103 (0.073) | 0.248** (0.112) | ||||||

| CC × Y | 0.093* (0.048) | 0.111 (0.074) | ||||||

Note. Author’s calculation.

Δ indicates difference; WOI indicates model Without institutions.

p < .1. **p < .05. ***p < .01, values in the parentheses are robust standard errors.

Acknowledgements

Our sincere thanks go to the editor and the anonymous referees for their painstaking effort in reading our manuscript as well as their many insightful comments and suggestions which greatly improved this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: the Ministry of Science and Higher Education of the Russian Federation (Ural Federal University Program of Developing within the Priority-2030 Program).

Data Availability Statement

Publicly available datasets were analyzed in this study. This data can be found here: (https://databank.worldbank.org/source/world-development-indicators, and ![]() )

)

However, the datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.