Abstract

After Brazil, Russia, India, and China (BRIC) started meeting in the BRIC countries format, and since 2011 with South Africa in the BRICS format, these countries’ leaders made several pledges for strengthening intra-BRICS economic cooperation. This article examines the degree this is reflected in the increase of Chinese Outward Foreign Direct Investment (COFDI) in the other four BRICS countries, the value of Chinese construction contracts, and bilateral trade between China and Brazil, India, Russia South Africa in 2009 to 2019. Focusing on these aspects contributes to the ongoing debate about the institutionalization of the BRICS political grouping. This article demonstrates that, thus far, despite the various pledges, the intensification of intra-BRICS economic cooperation is very limited. With some exemptions due to mega investment deals, COFDI in the other BRICS partners is still reasonably modest and shows no clear trend of increase over time in both absolute and relative figures. There is no significant increase in total trade, and various imbalances and asymmetries remain. Thus, the reality does not mirror the BRICS rhetoric on the intensification of economic cooperation.

Keywords

Introduction

Over the past decades, the BRICS countries (Brazil, Russia, India, China, and South Africa) have gained more weight in global affairs (see Hooijmaaijers & Keukeleire, 2016; Käkönen, 2019a; Kirton & Larionova, 2018; Lukin, 2019a; Roberts et al., 2017; Stuenkel, 2015). They have steadily developed a dialog and cooperation process on various levels since 2006, and annual summits take place since 2009, and what started as the BRIC (Brazil, Russia, India, and China) grouping became BRICS from 2011 onward (Hooijmaaijers & Keukeleire, 2016). The widening range of covered topics and the growing size of the BRICS Declarations and Joint Statements reflected this increase. In these statements, the BRICS sides called for economic cooperation and intensification of trade and investment flows between their countries (see BRICS, 2011a, 2011b, 2012a, 2013, 2014).

Since its inception, the BRIC political grouping has been part of an academic debate. Scholars disagree about the meaning and future of the BRICS countries (see Helleiner & Wang, 2018; Käkönen, 2019a; Li, 2019; Lukin, 2019a). Notwithstanding the club’s limitations, in a decade, the BRICS club has proven itself among the global governance institutions due to it having shaped new institutions “and demonstrated its capability to provide global public goods” (Käkönen, 2019b, p. 418). Cooperation in the BRICS framework is an example of South-South cooperation (see Duggan et al., accepted). Per the United Nations (UN, 2019), South-South cooperation is executed via a wide collaboration framework between the global South countries in “the political, economic, social, cultural, environmental, and technical domains.” This means that South-South cooperation involves “two or more developing countries” and can appear on a bilateral, regional, intraregional, or interregional basis (UN, 2019).

This article tests the bilateral economic relations between the BRICS countries by examining the extent to which the pledges for intensification of BRICS economic cooperation are reflected in the increase of Chinese Outward Foreign Direct Investment (COFDI) in the other BRICS partners, the value of Chinese construction contracts with these countries, and Chinese bilateral trade with the other BRICS partners. It focuses on the economic reality behind the official BRICS rhetoric of their statements. Because of its political-economic weight, China outweighs the other BRICS countries. China’s economy is more significant than the four other BRICS parties combined. Therefore, the focus is on COFDI and Chinese construction contracts in these four countries and Chinese bilateral trade with the other BRICS partners. Our analysis’s starting point is 2009; the year of the first BRIC Summit (see BRIC, 2009). The study therefore involves the phase in which the BRICS countries intensified their cooperation. This allows for an examination of whether their bilateral economic ties were strengthened during this period. Based on the China Global Investment Tracker (CGIT) and trade statistics from UN Comtrade, we will obtain more in-depth insight. The collected data contributes to the enduring debate on the interaction between and institutionalization of the BRICS countries that began around 2001 when O’Neill (2001) coined the term BRIC.

This article’s main empirical contribution is that it demonstrates that, despite the various pledges, the intensification of the intra-BRICS economic relations measured in COFDI and value of Chinese construction contracts in Brazil, India, Russia, and South Africa and Chinese trade relations with these four BRICS partners is very limited. Various imbalances and asymmetries remain. The findings highlight the differences between policy statements and outcomes, which are understood in the public choice literature. It also links with the neorealism IR literature, where (economic) state interests are an essential determinant. On a related note, these statements are not legally binding.

This article proceeds as follows. First, we will explain and justify the methods used to collect the investment and trade data and measure China’s evolving economic relations with the other four BRICS countries. Second, we will briefly discuss the BRICS debate in which we will situate our findings. Third, we will assess the intensification of BRICS interaction and the various BRICS statements on economic cooperation. The collected data provides the foundation for analyzing COFDI and Chinese construction contracts and the bilateral trade relations with China and Brazil, Russia, India, and South Africa. The subsequent sections focus on COFDI in Brazil, Russia, India, and South Africa, Chinese construction contracts with the BRICS partners, and the bilateral trade of China with the other BRICS, followed by a discussion of the findings in the penultimate section. The conclusion summarizes this article’s main findings and expounds on their relevance.

Literature Review: The BRICS Debate

The BRIC debate started around 2001 when Goldman Sachs’ Jim O’Neill launched the term as he focused on the Gross Domestic Product (GDP) growth of Brazil, Russia, India, and in particular, China and the weight of the BRICs countries in world GDP (O’Neill, 2001). Analysts disagree about the importance and future of the BRICS political grouping (see Cooper, 2016; Donno & Rudra, 2014; Helleiner & Wang, 2018; Käkönen, 2019a; Li, 2019; Lukin, 2019a; Roberts et al., 2017). Some observers consider the BRICS a new collective force, challenging the world order founded under the United States (US) governance after World War II (see Mielniczuk, 2013). Using a social constructivist approach, Mielniczuk (2013) shows that the BRICS’ changing identities are the “main cause of the convergence of their interests in the international arena” (p. 1075). Since 2006, the BRICS have gradually developed a dialog and cooperation process on several levels, starting as BRIC and since 2011 as BRICS (Hooijmaaijers & Keukeleire, 2016). Strengthening the BRICS dialog and cooperation paralleled South Africa joining the BRICS political grouping in 2011.

The loose coalition has developed into a formal economic and political partnership (de Oliveira & Jing, 2020). On a more theoretical note, global change and the emergence of the BRICS countries can be understood as continuing the decolonization process (Käkönen, 2019b). The cooperation of the BRICS countries can be seen as South-South Cooperation (see Bergamaschi et al., 2017; Cooper, 2021; Mthembu, 2018; Muhr, 2016). As outlined by Käkönen (2019b, p. 415), Global South cooperation “changes continuously” and serves the developing world’s interests in the international system’s decolonization. The BRICS and other China-centric multilateral cooperation frameworks “might challenge the current liberal international order” (see Beeson & Zeng, 2018), however, they are not against free trade or globalization (Käkönen, 2019b, p. 417).

In this light, it is relevant to mention the extensive literature on international cooperation and trade. International cooperation refers to policy coordination processes by which states and other entities alter their behavior to the real or expected preferences (Krieger, 2004). For decades, international trade has been critical to economic growth and improved living standards for countries and regions worldwide (Looney, 2019). Trade is an “Engine” of integration, growth, or inequality (Deese, 2016). China’s role in the global economy is ever increasing in prominence (Zeng, 2019). This is reflected in various China-sponsored and co-sponsored initiatives, including the Belt and Road Initiative (BRI), New Development Bank (NDB), and Asian Infrastructure Investment Bank (AIIB) (see Hooijmaaijers, 2021a, 2021b, 2021c; Hooijmaaijers & Keukeleire, 2020).

One (potential) advantage of the BRICS format is that due to these developments, parties are meeting that before were not meeting, which is a sign of the institutionalization of the BRICS cooperation (see Hooijmaaijers, 2021c; Hooijmaaijers & Keukeleire, 2020). The broadening range of issues that were covered, the increasing BRICS declarations, and the institutionalization of the BRICS cooperation with the foundation of the NDB and the Contingent Reserves Arrangement (CRA) reflect this rise (see Duggan, 2015; Helleiner & Wang, 2018; Vazquez et al., 2017; Wang, 2017). These institutions are signs of internal BRICS institutionalization, including strengthening the cooperation among the BRICS countries and expanding the grouping’s agenda (see Duggan et al., accepted). The founding of the NDB is a major milestone in the BRICS cooperation. It “put to rest much of the concern around the future of the grouping” because it institutionalized the engagement between the five parties (Viswanathan & Soni, 2017, p. 17; see also Cooper & Farooq, 2016). It is the first multilateral development bank (MDB) created by emerging markets and developing countries (EMDCs) (Hooijmaaijers, 2021c).

Against the backdrop of the economic and financial crisis of 2007 to 2009, the BRICS initiatives such as the NDB and CRA challenged the current multilateral order with a key role for the IMF, the World Bank, and the WTO, in which these countries are underrepresented (see Boughton et al., 2017; Stuenkel, 2013, 2015). The BRICS have in common that they all consider the post-World War II world order, with, for instance, a dominant role for the US and Europe in the Bretton Woods institutions, as unjust (see also Lukin, 2019b; Thakur, 2014). Much of the BRICS debate has focused on whether the BRICS club is an innovative force in global governance and whether the parties are rule changers or makers (Hooijmaaijers, 2021c). Several features make that the NDB embodies something new (Hooijmaaijers, 2021a). This includes the key role of infrastructure and sustainable development tasks, country systems, equal voting rights, local currency funding, and execution speed (Cooper, 2017; Hooijmaaijers, 2021a; Suchodolski & Demeulemeester, 2018). The COVID-19 pandemic also strengthened intra-BRICS cooperation, as the NDB focused on assisting the member countries in dealing with the crisis and following economic recovery, reflected by its Board of Governors approving an emergency line of up to $10 billion to assist the NDB’s states (Hooijmaaijers, 2021c).

As Lukin (2019b, p. 453) mentioned, BRICS has turned from a “hobby club” into “a full-fledged mechanism of versatile strategic partnership.” BRICS leaders meet twice a year. This includes the main BRICS summit and a meeting in the margins of the G-20 meeting, along with around 100 official events, with 20 taking place at the ministerial level. There is “a broad network of industry-specific contacts and cooperation between the BRICS countries,” including the party’s business communities, academics, and other civil society representatives (Lukin, 2019b, p. 453). Although it is debatable to what degree the increasing number of meetings has led to concrete results, it is important to put these developments into perspective. According to Henry Kissinger, the Chinese game 围棋 (weiqi) and not Western chess guides Chinese strategy (accessed in Mahbubani, 2020). The essential difference between these two games is that Western chess seeks the fastest way to capture the king. In contrast, weiqi aims to slowly and patiently build up assets to tip the balance of one’s game in one’s favor. The emphasis is not on short-term goals but long-term strategy. This difference is not only of critical relevance for a better understanding of China’s foreign policy; it also illuminates the development of the BRICS grouping.

Other analysts remain skeptical of the BRICS’ potential due to the various limitations of the BRICS political grouping. In the early days of the then still BRICs, observers pointed out that the four countries had little in common apart from being large, rapidly growing economies with huge domestic markets (Wang, 2010). Others wonder whether the BRICS are merely a fable (Hopewell, 2017). The BRICS is an unbalanced group of countries, the relations between the BRICS sides are variable, and at times they have conflicting interests. Due to the nature of the group, the BRICS “failed to leverage their growing economic might into effective diplomatic clout” (Pant, 2013).

Similarly, “in the absence of clear common objectives, the BRICS abandon all but the rhetoric of coalitional behaviour” and “unless the five emerging powers agree on a coherent strategy to harness their relative strengths, the BRICS’ geopolitical play will be defeated by their own tactical ploys” (Brütsch & Papa, 2013, p. 299). Indeed, the BRICS dynamics limit the club’s potential to restructure global economic governance (Hooijmaaijers, 2021a). There are limited people-to-people exchanges among the BRICS countries, and all BRICS countries have domestic issues. These issues were already present in the pre-COVID-19 pandemic era.

Thus far, on the bilateral level, China and India have not resolved any issues (see also Bajpai et al., 2017). The Sino-Indian relationship is arguably at its lowest point in decades, as in May 2020, the stand-off between India and China erupted in the Galwan River valley on the border between Ladakh in Chinese-administered Aksai Chin and Indian-administered Kashmir. The Sino-Russian relationship is imbalanced, and the Chinese moving to Siberia is a thorny issue (see Krickovic, 2017). The current state of this relationship is a quasi-alliance (Lukin, 2021). As mentioned by Trinkunas (2020), since President Jair Bolsonaro assumed office in January 2019, he and his foreign policy team had adopted “a strongly pro-U.S.” (particularly pro-President Donald Trump) agenda internationally, including frequent critiques of China. Domestically, the relationship with the PRC has been “controversial” in some sectors (Trinkunas, 2020). Notably, the Brazilian manufacturing sector has criticized the partnership because it faces fierce “competition from Chinese products and lacks reciprocal access” to the Chinese market, and by nationalist-populist voters supporting President Bolsonaro (Trinkunas, 2020). By contrast, agricultural export interests “favor a strong relationship with Beijing” due to China being a significant export market for them (Trinkunas, 2020).

Brazil, Russia, India, China, and South Africa differ substantially on various power indicators, including demographic, economic, military, political weight, and regional and global ambitions (see Beeson & Zeng, 2018; Liu, 2016). The reality that China’s economy is more significant than the other BRICS countries’ combined economies manifests these differences. Also, an assessment of the voting cohesion among the five BRICS countries at the United Nations General Assembly (UNGA) found that, overall, since the start of the BRIC consultations in 2006, there is no substantial surge in the degree of voting cohesion (Hooijmaaijers & Keukeleire, 2016; see also Dijkhuizen & Onderco, 2019; Ferdinand, 2014).

Given these issues with the BRICS political grouping, Vazquez (2020) argues that the “bilateralization” of the BRICS club “expands the options for the grouping to act and might be the only way to survive another decade.” Alternatively, the countries aim to improve economic connectivity via the BRICS Plus format (Arapova, 2019). This article contributes to the ongoing BRICS debate by examining the extent to which the pledges for intensification of BRICS economic cooperation are reflected in the strengthening of their trade and investment relations. We now turn to an analysis of the various BRICS statements on strengthening economic cooperation to get a clearer idea of what the BRICS parties pledged and how.

Methods

Several data sources contribute to answering the leading question of this article and the debate on the institutionalization of the BRICS cooperation in which we will situate our findings. Due to the use of policy documents and statistical data, the approach of this article is mixed. Internal BRICS institutionalization encompasses strengthening the BRICS cooperation and expanding the BRICS agenda (see Hooijmaaijers, 2021c). Over the past decade, the BRICS countries made various references to BRICS economic cooperation. These BRICS Declarations and Joint Statements issued after the various BRICS Summits and meetings of Trade Ministers are critical data sources for this research. For all data used in this article, the starting point is 2009, the year of the first BRIC Summit (see BRIC, 2009). Therefore, it is essential to clarify what is tested in the paper: the bilateral economic relations between the BRICS countries.

The CGIT is the primary source for analyzing the evolution of COFDI and Chinese construction contracts with Brazil, India, Russia, and South Africa. We will use data from the CGIT from 2009 until December 2019. CGIT’s dataset allows for an overview of investment flows and per sector in the four selected countries. An advantage of the CGIT is that it is a transparent source. It is a bottom-up database that lists China’s construction activities and global investments worth $100 million or more.

It is essential to consider that the CGIT includes deals valued at least $100 million; it does not include foreign direct investment (FDI) deals below this threshold. Moreover, and more generally, mega deals may have a substantial effect on the data. For example, deals concluded in December will end up in statistics for year x, but deals concluded in January are included in the statistics for year y. Therefore, it is essential to look at the broader trends in COFDI relations.

We will use the UN Comtrade database and their statistics for goods for the 2009 to 2019 period for trade statistics. At the time of writing, 2019 was the latest year with annual data available. Substantial different figures are expected for 2020 and the years onwards. As an illustration of the dire economic situation, China-Africa trade took a big hit from coronavirus in the first half of 2020, with South Africa’s exports to China being down almost a third (South China Morning Post, 2020d). China’s trade surplus for November 2020 was at a record of $75 billion. UN Comtrade is the biggest depository of international trade data (UN Comtrade Database, 2020). The United Nations Statistics Division (UNSD) transforms the data of reporter countries into their standard format, allowing for cross-country comparison. We focus on import, export, trade balance, and trade volume. This article will use China’s data on imports and exports to Brazil, India, Russia, and China. A country’s trade balance is positive if the value of exports exceeds the value of imports. However, a trade surplus for one country naturally means a trade deficit for the partner country. It is essential to emphasize the possibility of differences in trade figures reported by the countries on their bilateral trade relations. Similar to the COFDI data, one way to deal with this limitation is to focus on broader trends.

The Intensification of BRICS Interaction and BRICS Statements on Economic Cooperation

This section focuses on the intensification of BRICS interaction and BRICS statements on economic cooperation. Over the past decade, the BRICS countries made various references to BRICS economic cooperation. This becomes visible from the analysis of the BRICS Declarations and Joint Statements issued after the various BRICS Summits and meetings of Trade Ministers. The BRIC leaders made no references to intra-BRICS trade or investment in their Joint Statement issued after the first BRIC Summit in Yekaterinburg. However, the parties did mention the recognition of “the important role played by international trade and foreign direct investments in the world economic recovery” against the backdrop of the Global Financial Crisis (GFC) (BRIC, 2009). The BRIC (2009) parties also stated they stand for “strengthening coordination and cooperation among states in the energy field, including amongst energy producers and consumers and transit states, in an effort to decrease uncertainty and ensure stability and sustainability.” One year later, the parties stated: “In order to facilitate trade and investment, we will study feasibilities of monetary cooperation, including local currency trade settlement arrangement between our countries” (BRIC, 2010). In April 2011, the now BRICS issued a Declaration after the Sanya Summit in which they stated they “agreed to continue further expanding and deepening economic, trade and investment cooperation among our countries” (BRICS, 2011a).

After the first meeting of BRICS Trade Ministers held in Sanya on 13 April 2011, the BRICS ministers met again before the 8th World Trade Organization (WTO) Ministerial Conference in December of the same year. The parties mentioned they were “pleased” with the recent creation of “a contact group” assigned with the task of proposing an institutional framework and concrete measures to increase “economic cooperation” both among the BRICS countries and between the “BRICS countries and all developing countries, within a South-South perspective” (BRICS, 2011b). This contact group met for the first time in December 2011.

In the subsequent year, in the Declaration issued after the 2012 Delhi Summit, the parties stated they agreed to build upon their synergies and cooperate “to intensify trade and investment flows” among their countries to advance their industrial development and employment goals (BRICS, 2012a). Around the same time, the BRICS Trade Ministers held their second meeting in New Delhi. The BRICS Trade Ministers directed their officials to explore ways and means for developing and furthering “intra-BRICS cooperation” in various areas (BRICS, 2012b).

In 2013, the parties established a “BRICS trade and investment cooperation framework” (BRICS, 2013). The Contact Group on Economic and Trade Issues (CGETI) founded this framework (see BRICS, 2013). It is developed and initiated with various aims, including promoting trade, investment, and economic cooperation among the BRICS countries and encouraging trade and investment links between BRICS countries to support industrial complementarities, sustainable development, and inclusive growth (BRICS, 2013). In the 2014 Fortaleza Declaration, the BRICS countries expressed their commitment to “raise” their “economic cooperation” qualitatively (BRICS, 2014). To achieve this, they vowed to establish “a road map for intra-BRICS economic cooperation (BRICS, 2014).” In this light, they welcomed the proposals for a “BRICS Economic Cooperation Strategy” and a “Framework of BRICS Closer Economic Partnership,” which designate steps to “promote intra-BRICS economic, trade, and investment cooperation” (BRICS, 2014). More recently, in November 2019, the BRICS parties signed a “Memorandum of Understanding among BRICS Trade and Investment Promotion Agencies (TIPAs)” (BRICS, 2019).

In sum, an examination of the BRICS Joint Statements and Declarations shows various references and pledges to promote trade, investment, and economic cooperation among these countries. However, one of the issues with BRICS research is that, except for the declarations adopted after the annual summit meetings and some ministerial meetings, they provide “little or no information about the actual outcomes” of the interactions between the parties (Hooijmaaijers & Keukeleire, 2016, p. 393). This is also noticeable in the various BRICS action plans issued after each BRICS Summit, starting from 2011. These plans “often do not provide much detail” but only generally refer to meetings and consultations among the BRICS parties (Hooijmaaijers & Keukeleire, 2016, p. 393). The analysis above fits this observation. Many statements include vague and general commitments to expand and deepen economic, trade, and investment cooperation among the BRICS countries. The commitments made in these statements are by no means legally binding. These are among the reasons why it is valuable to examine whether these BRICS’ pledges for intensification of BRICS economic cooperation are reflected in the COFDI in the other BRICS countries, the value of Chinese construction contracts, and bilateral trade of China with the four other BRICS, questions that are at the center of this article.

The evolution of COFDI in Brazil, Russia, India, and South Africa

This section focuses on COFDI flows in other BRICS countries. Figure 1 below provides an overview of the COFDI flows in Brazil, Russia, India, and South Africa in 2009 to 2019. Infrastructure development is a priority of Beijing’s FDI in various parts of the (developing) world (Wang, 2017; see also Brautigam & Gallagher, 2014).

COFDI in Brazil, India, Russia, and South Africa, 2009 to 2019 (in $ billion).

Most striking is the data on Chinese investment in Brazil. Scholars have pointed out that COFDI in Brazil has increased considerably since 2010 (see Blanchard, 2019). However, the figure above reveals that it mainly concerns two peaks in investment in 2010 and 2016. A handful of mega deals profoundly affect COFDI numbers in the Latin American country, and in part, explain these peaks in investment. Expectations of greater COFDI in the Latin American country “were exaggerated” because the general investments in the country’s domestic infrastructure, urban mobility, and manufacturing generally “have undergone huge losses since 2014” (Guilhon Albuquerque & Fernandes Lima, 2016, p. 598).

COFDI in India seems to have slightly increased with two steps over the last decade. However, overall it is still reasonably modest. Sino-Indian bilateral investment has not experienced the same growth as the parties’ total trade (see also below). While China and India both have arisen as “top investment destinations for the rest of the world,” mutual investment flows between both sides are yet to catch up (Embassy of India, 2020). Krishnan (2020, p. 4) states that the increase of COFDI into India since 2014 “has changed the nature” of what has been a predominantly “transactional trade relationship.” Chinese firms were “emerging as prominent players and investors” in various fields, including infrastructure, energy, technology startups, and real estate (Krishnan, 2020, p. 4).

However, Chinese investment in India recently declined, as the troubled relations between both sides led to “a fall in investor confidence” (Business Today, 2020). In April 2020, the Indian government “had tightened its FDI policy” to curb Chinese companies from acquiring a stake in Indian companies (Business Today, 2020). In a April 17 press note, the Department for Promotion of Industry and Internal Trade (DPIIT) stated “the revision of the FDI policy” intends to restrict “opportunistic takeovers/acquisitions of Indian companies due to the current COVID-19 pandemic” (Business Today, 2020). The Indian newspaper Business Today highlighted that the revision intended to control FDI from entities or citizens “of any country that shares land borders with India makes China its prime target” (Business Today, 2020). Chinese state media outlet Global Times also mentioned that “more Chinese investors abandon hopes for [the] Indian market as restrictions rise” (Global Times, 2020). These are all signs of a worsening investment relationship.

Russia is not attracting much Chinese investment. COFDI in Russia saw a modest increase in the first years of the 2010s. However, later during the decade, it decreased. Medeiros and Chase point out that a significant turning point in their bilateral energy relationship occurred following the Ukraine-related sanctions when Moscow started negotiating much lower prices with Beijing for investment in Russian oil and gas fields. As a result, COFDI in key Russian liquefied natural gas (LNG) projects embody a new and thorny dimension to the relationship (Medeiros & Chase, 2017). Alexander Gabuev points out that while being a devoted consumer of Russian resources, the PRC “has never been keen to invest in its trade partner (accessed in Nikkei Asian Review, 2019)” He challenges that Chinese investors are “turned off by Russia’s risky business environment” that has experienced various renowned business tycoons’ arrests (Nikkei Asian Review, 2019). China’s antagonistic history with Russia also matters. Furthermore, Chinese firms prioritize big, “growing” markets like the US and Asia’s rising economies (accessed in Nikkei Asian Review, 2019). Be that as it may, the reality that COFDI in Russia is hardly increasing in spite of importing vast amounts of resources “has its partner on edge” (Nikkei Asian Review, 2019).

China has developed into a significant investor in South Africa’s main industries, including financial services and mining (Bradley, 2016). On many indicators, South Africa is the smallest member of the BRICS club. In line with this reality, it receives the least COFDI of the individual BRICS members. Moreover, the data shows no increasing trend of COFDI vis-à-vis the African BRICS member.

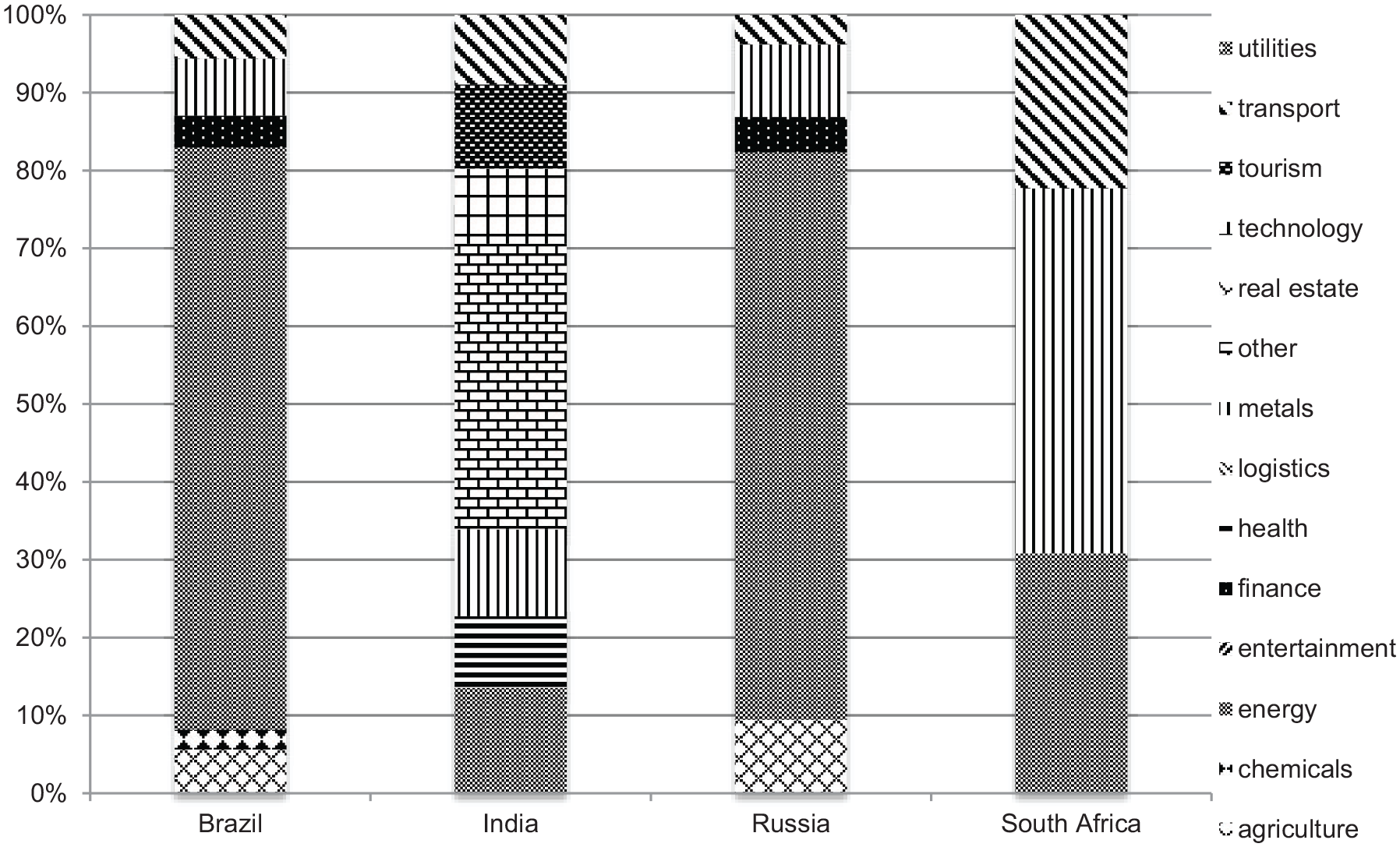

Figure 2 below presents an overview of the cumulative value of COFDI per BRICS country per sector in 2009 to 2019. It shows China’s preference for investment in metals (natural resources) and energy.

Cumulative value of COFDI in Brazil, India, Russia, and South Africa, per sector, 2009 to 2019 (percentage).

Some remarks should be made regarding COFDI in the BRICS countries. First, mega deals may significantly influence 1-year data, as Brazil’s data showed. Therefore, it is worthwhile looking at more significant trends. Also, since 2000, Beijing has “gradually implemented more liberal rules” for COFDI (Hanemann & Huotari, 2015). These changes allowed Chinese firms to follow “their increasing commercial incentives to expand globally” (Hanemann & Huotari, 2015). This triggered “fast growth” in COFDI flows since the mid-2000s, as in just a decade, annual flows developed from practically nothing to over $100 billion per year (Hanemann & Huotari, 2015). One should understand COFDI in Brazil, India, Russia, and South Africa in the broader context of the global COFDI trends. COFDI’s trajectory has changed severely over the past 5 years. After a period of double-digit growth, COFDI peaked in 2016 and is decreasing since then (Kratz et al., 2020). Moreover, the composition of COFDI has shifted in the sector and target country. It evolved from mainly pursuing natural resources to a more varied mix, such as technology, consumer capabilities, and brands, and from EMDCs to advanced economies (Hanemann & Huotari, 2015).

In order to put the global trends of COFDI in the target countries in perspective, we now turn to analyze COFDI in Brazil, India, Russia, and South Africa as a percentage of total COFDI per year in the 2009 to 2019 period.

Table 1 above reveals that the numbers broadly fluctuate. Mostly, there are no significant increases over the long term. There are peaks, primarily due to and in line with the mega-deals discussed above.

COFDI in Brazil, India, Russia, and South Africa as a Percentage of Total COFDI (2009–2019).

Source. CGIT.

A “—” means no investment deals in the CGIT were recorded for that year.

Chinese Construction Contracts with Its BRICS Partners

This section focuses on Chinese construction contracts with Brazil, India, Russia, and South Africa in order to assess whether the vows for more economic cooperation among the BRICS are reflected in these contracts.

Russia is the BRICS country receiving the most Chinese construction contracts in both numbers and values, with a peak in 2017. Brazil experienced a peak in 2015, India in 2013. There were minimal Chinese construction deals in South Africa. There are some variations over time. However, the data in Figure 3 does not reveal a stable increase in Chinese construction deals over time. All Chinese construction contracts in Russia since 2014 were part of the BRI, as was the 2017 South Africa deal. This also shows the linkages between the initiatives (see Hooijmaaijers, 2021a, 2021b; Hooijmaaijers & Keukeleire, 2020; Thussu, 2018). None of the Chinese construction contracts in India and Brazil were BRI projects. When New Delhi was invited to participate in the 2017 BRI Forum India declined the invitation, and stated: “We are of firm belief that connectivity initiatives must be based on universally recognized international norms, good governance, rule of law, openness, transparency and equality” (Ministry of External Affairs Government of India, 2017). Notwithstanding the ongoing diplomatic tensions between New Delhi and Beijing (see also above), India is the largest beneficiary of the Asian Infrastructure Investment Bank (AIIB), as it receives around a quarter of the Bank’s investment commitments (Financial Times, 2018). From India’s perspective, there is an essential difference between the AIIB and other BRI-related initiatives. The most significant one is that concerning the AIIB, China contacted India in “a consultative process” first (Panda, 2018).

Chinese construction contracts in Brazil, India, Russia, and South Africa, 2009 to 2019 (in $ billion).

Bilateral Trade Relations of China and the Other BRICS Countries

This section focuses on China’s bilateral trade relations with Brazil, India, Russia, and South Africa. We will discuss the imports, exports, trade balance, and total trade, country by country for analytical purposes. The data contributes to answering the question of to what degree the BRICS leaders’ pledges for intensification of BRICS economic cooperation are reflected in their bilateral trade.

The Sino-Brazilian Trade Relationship

Trade is the primary driver of the Sino-Brazilian relationship. Trade between both sides was insignificant in the 1990s but massively increased with China’s shift into the world’s factory and increasing per capita consumption that generated “a voracious Chinese appetite” for Brazilian iron ore, oil, meat, soybeans, and other goods (Blanchard, 2019, p. 588). However, despite the rapid growth of bilateral trade, the pattern has led to concern. Jenkins (2012) highlights that Brazil’s exports predominantly relate to a few primary products. By contrast, imports from the PRC are “nearly entirely manufactured goods that are becoming more technologically sophisticated over time” (Jenkins, 2012, p. 21). Pereira and de Castro Neves (2011) point out that, despite beneficial trade relations, there is “a pattern of growing imbalances and asymmetries in trade flows” that are more advantageous to China than Brazil.

The data reveals a sharp increase from 2009 to 2011. However, this is primarily due to the trade situation because of the GFC. In 2008, Brazil’s exports to its traditional markets diminished substantially. A substantial rise in Chinese commodity purchases saved the country (Guilhon Albuquerque & Fernandes Lima, 2016). China has a considerable trade deficit with Brazil. There is no significant increase in total trade between Brazil and China in the subsequent years after the various BRICS pledges to promote trade among the BRICS countries. Table 2 shows that Brazil and China’s total trade in 2017 was around the same level as 2011. The years 2018 and 2019 showed a hike in trade volume. It is too early to tell whether this was an exemption or the start of a new trend with sustainable growth. The COVID-19 pandemic only strengthens this uncertainty.

Bilateral Trade Between Brazil and China 2009 to 2019 as Reported by China (in $ Billion).

Source. UN Comtrade Database.

The Sino-Indian Trade Relationship

The Sino-Indian relationship is a relationship that, at times, is troubled, for instance, with the continuing border dispute and with the string of pearls and Chinese intentions in the Indian Ocean Region (see Brewster, 2018; Cooper, 2021; Scott, 2008, Table 3).

Bilateral Trade Between India and China 2009 to 2019 as Reported by China (in $ Billion).

Source. General Administration of Customs, China. Accessed via the embassy of India in Beijing; UN Comtrade Database.

The swift increase of bilateral trade between India and China since the early 2000s boosted China to arise as India’s leading goods trading partner by 2008. Today it still holds this position. Since the start of the 2010s, bilateral trade between both sides experienced exponential growth. However, there was a dip in 2012. Moreover, both countries set a goal of $100 billion of total trade for 2015. However, this was not reached by that year and has not been reached yet. As a result, the total trade between India and China in 2016 was slightly smaller than in 2011.

China has a massive trade surplus with India. The trade imbalance has continuously been widening year after year (Embassy of India, 2020). India’s trade deficit with China is the most significant single trade deficit it has with any country. Against the backdrop of the Indian concerns that New Delhi perceives as not economically sustainable and sensitive to its domestic industry, during the second India-China informal summit between Indian Prime Minister Narendra Modi and China’s President Xi Jinping in October 2019, both sides agreed to set up a “high-level economic and trade dialogue mechanism” to touch upon trade, investment, and services (The Hindu, 2019). The “mechanism” would involve India’s Finance Minister Nirmala Sitharaman and China’s Vice-Premier Hu Chunhua (The Hindu, 2019). For the moment, it is too early to tell if there will be any concrete output related to this move. Notably, as in the aftermath of the deadly Sino-Indian border clash in the Himalayas that reportedly “left 20 Indian soldiers dead and 76 injured,” Indians have called for “a boycott on Chinese goods,” and New Delhi has pledged to block COFDI and increase tariffs for China (The Guardian, 2020). According to India’s foreign minister Subrahmanyam Jaishankar, the Sino-Indian relationship is at its “lowest point in 30 to 40 years” (South China Morning Post, 2020c).

The Sino-Russian Trade Relationship

The 2008 to 2009 global economic crisis has revealed the magnitude of asymmetry between Russia and China (Kaczmarski, 2015). As pointed out by Silvius (2019, p. 631), one can reasonably show the strengthening of Russia’s economic engagement with the PRC in the aftermath of the Ukrainian crisis and following Western sanctions that solidified “normal” economic conduct with Western parties more challenging for Russian officials and businesses. However, it would be improper to presume the rationale of rising Chinese-Russian economic relations from each party’s stated “world order preference” in just the context of geopolitical crisis (Silvius, 2019, p. 631).

Table 4 shows that the two-way trade increased from 2009 to 2011, mainly related to the GFC. The data reveals no significant increase in Sino-Russian total trade after the various BRICS pledges promote trade among the BRICS countries. The trade volume of 2017 is slightly smaller than the volume 5 years earlier. In September 2019, Russian and Chinese news agencies stated that both sides wanted to double their bilateral trade over the next half a decade to approximately $200 billion by implementing joint projects in energy, industry, and agriculture (see Xinhua, 2019). Despite these pledges to increase bilateral trade, the economic relationship between the Sino-Russian economic relationship and China is not equal. For Beijing, Moscow is a source of energy and advanced technology and is pleased to sell its manufactured goods to Russia. As a result of the Western sanctions on Russia following its annexation of Crimea and the invasion of Ukraine, the asymmetry in the Sino-Russian economic relationship deepened further. However, Russia could not do much about this situation (Medeiros & Chase, 2017). Still, since the 2014 Ukraine crisis, the Russian Federation saw the exports and imports with all top 10 trade partners decline, except China (Lukin, 2021).

Bilateral Trade Between Russia and China 2009 to 2019 as Reported by China (in $ Billion).

Source. UN Comtrade Database.

The data above reveals that in 2018, the Sino-Russian total trade value for the first time exceeded $100 billion. Oil and other minerals were responsible for 76% of Russian exports to China, and wood and paper products accounted for 8% (Nikkei Asian Review, 2019). Russia’s resource exports to the PRC rose after a new oil pipeline from East Siberia to the Asia-Pacific region became operational in 2009 (Nikkei Asian Review, 2019). In 2018, higher oil prices boosted export value. China is now the biggest foreign market for Russian oil, as it is responsible for a quarter of Russia’s oil exports (Nikkei Asian Review, 2019). The part of mineral resources in Russian exports is expected to grow further after finalizing a new natural gas pipeline (Nikkei Asian Review, 2019).

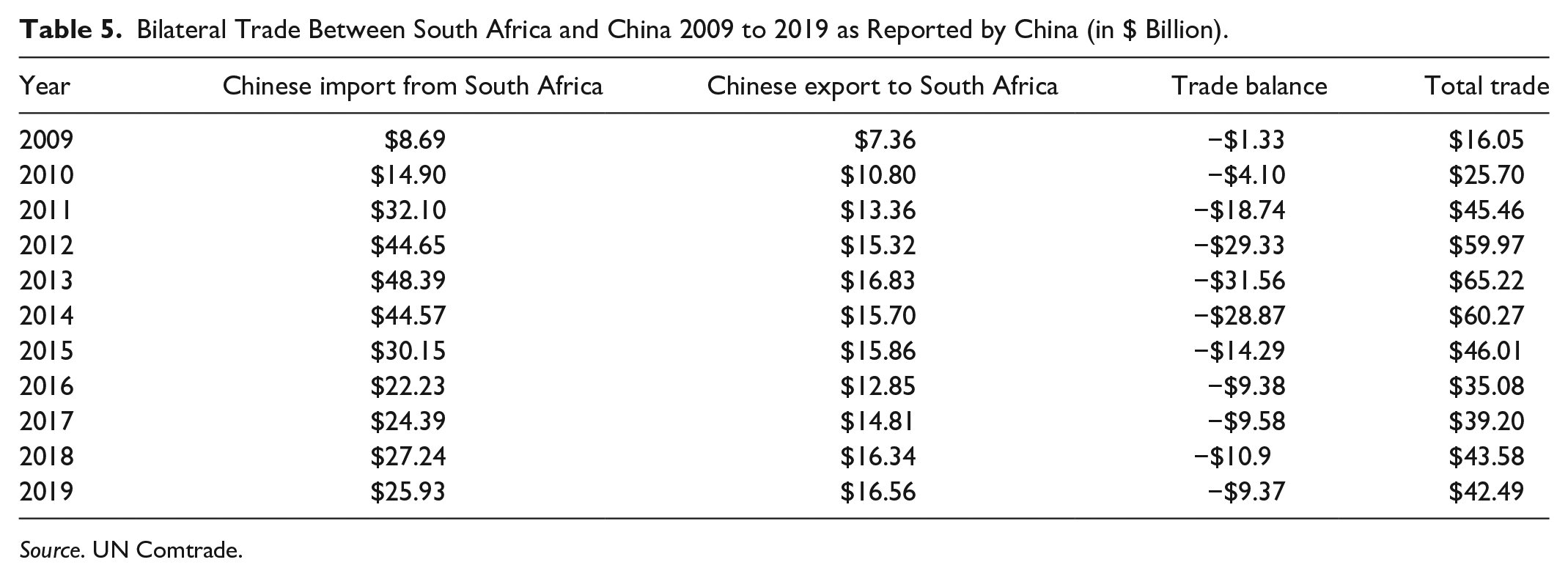

The Sino-South African Trade Relationship

Diplomatic relations between South Africa and China were only established in 1998 (Lu & Shu, 2019). The relationship between the two countries has developed from minimal contact to substantial economic arrangements, troubled with ideological and political uncertainty (Bradley, 2016). South Africa is China’s largest African trading partner. Table 5 below provides an overview of the bilateral trade relations between South Africa and China.

Bilateral Trade Between South Africa and China 2009 to 2019 as Reported by China (in $ Billion).

Source. UN Comtrade.

Table 5 shows that the two-way trade flourished from 2009 to 2013. This is partially due to global trade contraction following the 2008 financial crisis (Alden & Wu, 2016). China has an enormous trade surplus with South Africa, with the gap climaxing in 2012 to 2014. The imbalanced trade relationship is an issue of concern the relationship (Bradley, 2016). In 2018, against the backdrop of the US-China trade war, South Africa experienced a substantial surge in the balance of trade deficit (Ngwakwe & Sebola, 2020).

The pledges for an increase in economic cooperation are not reflected in the total trade volume. Interestingly, both parties’ trade volume in the two most recent years was slightly below 2011 levels. The data reveal no increase in total trade after the various BRICS pledges to promote trade among the BRICS countries.

Discussion of the Findings

This section is dedicated to discussing the findings on China’s economic relations with its BRICS partners. To what degree have the BRICS countries strengthened their intra-BRICS cooperation since the start of the BRIC summits in 2009? The data above reveals that, thus far, despite the various pledges, the intensification of the intra-BRICS economic cooperation as measured by growth in China’s trade relations with the four other BRIC countries, COFDI, and Chinese construction contracts in these four states is minimal. The sections above also revealed various continuing unequal relationships and significant trade deficits of several BRICS countries, with China.

Are these findings surprising? Given what we typically know about politics and foreign policy, rhetoric differing from reality is to be expected. This is well understood in the public choice literature and plausibly by the realist IR literature (The author would like to thank one of the anonymous reviewers for pointing this out. The findings can be related to the “rational choice” literature, which focuses on policy statements over policy outcomes. It is essential to highlight the difference between policy statements and policy outcomes. The former identifies the guiding principles or what is to be done. The latter is the outcome of what is implemented. Policy outcomes are the immediate consequences of a policy decision (Schmitt, 2012). Gaps between statements and outcomes are far from uncommon. In this light, it is also relevant to connect this with neorealism IR literature. Neorealism emphasizes that state interests dominate. The model considers states as autonomous actors that rationally pursue their interests in an international system where a central authority is absent (see Hooijmaaijers, 2021d; Waltz, 1979, p. 94). The security, economic and other interests of, in this case, the BRICS countries are essential. It serves as an explanatory model of why things occur or not. In addition, it is noteworthy that the commitments made in the BRICS statements are by no means legally binding. This may widen the gap between statements and outcomes. This should also be understood in the context of earlier BRICS research that showed that the BRICS countries prefer “a purely intergovernmental approach,” with decision-making by consensus, respect for national sovereignty, voluntary commitments, and no treaty obligations (Keukeleire & Hooijmaaijers, 2014, p. 591).

Similar issues have arisen elsewhere. For instance, Europe’s 17 + 1 countries, a group of Central and Eastern European Countries (CEECs), are increasingly dissatisfied with their China relations, as, for instance, their trade deficit with Beijing has increased since the launch of the framework in 2012 (South China Morning Post, 2020a). The 17 European countries include Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Czech Republic, Estonia, Greece, Hungary, Latvia, Lithuania, North Macedonia, Montenegro, Poland, Romania, Serbia, Slovakia, and Slovenia. Of note, in May 2021, Lithuania quit 17 + 1 because market access in China did not improve. Illustrating the issue, COFDI in these countries had slowly grown since the framework’s initiation, though 75% of it was concentrated in region’s biggest countries Hungary, the Czech Republic, Poland, and Slovakia, which left most other CEECS frustrated (South China Morning Post, 2020a). Moreover, in January 2020, due to a lack of COFDI Czech President Milos Zeman snubbed an invitation to attend the 17 + 1 Summit that then was still scheduled to take place in April in Beijing (South China Morning Post, 2020b).

The lack of reciprocity is one of the main issues in the European Union’s (EU) relationship with China (Hanemann & Huotari, 2018). The European side seeks market access to deal with the substantial trade deficit. Also, Chinese firms can make investments in European firms that, for instance, European businesses are not allowed to make in China, causing friction in the Sino-European relationship (see Meunier, 2019). Krishnan points out that the influx of COFDI in India presents particular challenges for India’s FDI regulation. This highlights the need for a “transparent, credible, and predictable regulatory framework” that better balances creating a “friendly, open and predictable investment environment and safeguarding longer-term security and privacy” (Krishnan, 2020). Other parties, including Europe, face similar challenges regarding COFDI, and the EU investment screening mechanism started operating in October 2020 (see Meunier, 2019).

Moreover, whether the trade and investment occur due to these vows for increasing intra-BRICS economic cooperation, or whether these deals would have happened in any event because businesses go where business opportunities are remains to be seen. As an illustration, previous research revealed, rising Sino-African trade figures are not that surprising because the Chinese economy has experienced spectacular growth over the past decades (Liu, 2011). The GFC, too, is relevant, as it led to a decrease and a rebound in economic relations. Also, for the moment, it is unclear to what degree precisely the COVID-19 pandemic affected intra-BRICS trade and investment relations, given the absence of full data on the year 2020. However, it will be of substantial importance, given the plunge in South Africa’s exports to China (see South China Morning Post, 2020d). Moreover, the souring relations between India and China also affect the bilateral economic relationship.

In sum, we see various similarities in the economic relationships between China and its BRICS partners, as we have seen in the relations of the PRC with other countries, including concerns regarding various, continuing imbalances.

Conclusion

Since Jim O’Neill coined the term BRIC, the countries have been part of an ongoing academic debate about the grouping’s relevance. This article contributes to the debate on the institutionalization of the cooperation between the BRICS countries by examining the degree to which the pledges in the various BRICS Declarations and Joint Statements for intensification of intra-BRICS economic cooperation are reflected in COFDI in the four other BRICS countries, the value of Chinese construction contracts in these countries, and bilateral trade between China and the other four BRICS. It focused on the economic reality behind the official BRICS rhetoric outlined in their statements by testing the bilateral economic relations between the BRICS countries. Despite the various pledges, the intensification of the BRICS economic cooperation is limited. A handful of mega deals profoundly affect COFDI numbers in Brazil, and in part, explain peaks in annual investment. China and India have become main investment destinations for foreign investors, but mutual investment between the two sides does not reflect this. Worsening Sino-Indian relations led to a fall in investor confidence, as New Delhi had tightened its FDI policy to curb Chinese firms from obtaining shares in Indian firms (Business Today, 2020). Russia is not attracting much investment from the Chinese side. On many indicators of power, South Africa is the smallest member of the BRICS grouping, and it also receives the least COFDI.

The data reveal no substantial increase in total trade after the various BRICS pledges promote trade among the BRICS countries. It shows an increase in the 2009 to 2011 period. This was primarily before the vows for increasing intra-BRICS economic cooperation were made, and mostly due to the GFC situation. The various imbalances in the trade relations largely remain, or for instance, in the case of India’s trade deficit with China, even increased. The $100 billion Sino-Indian total trade goal set for 2015 has not been reached yet. The Sino-Russian relation is asymmetric, and the unequal trade relationship is an issue in the Sino-South African relationship. Brazil has a significant trade surplus with China. Often, trade levels in, for instance, 2017 were around the same level as in 2011 or 2012.

For the moment, the reality does not reflect the BRICS rhetoric on the strengthening of economic cooperation. Although this article’s data sets are limited to 31 December 2019, it is critical to mention that the COVID-19 pandemic has severely affected intra-BRICS trade and investment. Various similarities in China’s bilateral economic relationships with its BRICS partners also occur in China’s relations with other countries, including various imbalances.

There are various limitations to this study. First, the paper is primarily an empirical contribution. Despite this paper mainly being an empirical contribution, it does contribute to the literature on international cooperation and trade. The findings are also well understood in the public choice literature, highlighting the difference between policy statements and outcomes. In this light, it is also relevant to link this with the neorealism IR literature, where state interests prevail. The findings should probably also be seen in the broader context of earlier BRICS research that demonstrated that the BRICS countries prefer an intergovernmental approach, with decision-making by consensus, respect for national sovereignty, voluntary commitments, and no treaty obligations (Keukeleire & Hooijmaaijers, 2014, p. 591). Second, concerning the used methods, data from a Chinese perspective was preferred, given that the PRC is the BRICS’ political-economic heavyweight. Due to different countries using different methods to calculate their trade statistics, this may affect trade data. Third, the research period comprises 2009—the year of the first BRIC summit—until December 2019 because this was the final year with full trade and investment data available at the time of writing. This means that the effects of the COVID-19 pandemic are not encapsulated in the data. There are, however, significant influences, as China’s trade surplus for November 2020 was at a record of $75 billion. Fourth, the BRICS countries are cooperating via various NDB projects (see Cooper, 2017; Hooijmaaijers, 2021a, 2021c; Suchodolski & Demeulemeester, 2018; Viswanathan & Soni, 2017). In addition, the China-led AIIB and the BRI focus on economic cooperation and development financing and have a significant role for China (see Hooijmaaijers, 2021a, 2021b). The BRICS phenomenon should be understood in the broader context of the global power shift toward the global South. In this development, a growing number of (Southern) countries are progressively meeting in several configurations (see Hooijmaaijers & Keukeleire, 2020). However, this goes beyond this article’s scope. The various limitations also serve as venues for further research.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.