Abstract

Organizations should constantly improve their business processes to increase performance while keeping employees satisfied. Therefore, human actors are considered a success factor in business process management (BPM) projects. This fact amplifies the impact of employees’ satisfaction on business process performance. Although several reward approaches exist, it remains unclear how they affect job satisfaction specifically in combination with certain process characteristics. To address this gap, we conducted a statistical analysis of survey data based on a representative European working conditions dataset. We applied two-way analysis of variance (ANOVA) and analysis of covariance (ANCOVA, i.e., controlled for organization size and sector) to explore the interaction effects. By looking at all possible combinations, we uncover how the presence or absence of specific pay modes and process-related aspects influence job satisfaction. Additionally, we reveal and discuss the joint effect of process characteristics and pay-for-performance types on job satisfaction. The results argue for a differentiated approach in pay-for-performance to obtain optimal reward solutions. Moreover, we advise for better strategic planning and facilitating successful BPM implementation.

Keywords

Introduction

When entering Industry 4.0, organizations try to keep up with disruptive transformations by focusing on their strengths, unique assets, and innovative opportunities (vom Brocke & Schmiedel, 2015). As a result, business process management (BPM) remains crucial and preeminent for digital work transformations (Denner et al., 2018). BPM deals with cross-functional process analysis and optimization and helps to focus on value for customers (Hernaus et al., 2016), leading to a sustainable implementation of the corporate strategy.

Employees (as the main actors of business processes) not only execute activities but also contribute to the entire value chain and its deliverables in terms of business value (Kirchmer, 2017). The success of BPM and digital transformation mostly depends on the presence of capabilities related to both technological and people management, and their alignment with each other (Van Looy & Devos, 2019; vom Brocke & Rosemann, 2015). Therefore, the process literature starts recognizing the human side of business processes (Van Looy, 2015). In this regard, organizations should keep their employees satisfied to work in a changing business environment (Aktepe & Ersoz, 2012; Binci et al., 2019; Dumas et al., 2018; vom Brocke & Rosemann, 2015), while constantly improving and reinventing business processes to obtain better business performance and customer satisfaction (Reijers et al., 2008).

In order to motivate employees toward better performance and desired behavior, organizations use various reward strategies (e.g., financial/non-financial, individual/team-based; Alhmoud & Rjoub, 2019; Boyd & Salamin, 2001; Gerhart & Milkovich, 1992). Business processes mostly require team-based work (i.e., within or across departments as process participants, process executing teams, or process improvement teams). Therefore, the BPM literature has acknowledged the importance of team-based rewards, which is specifically essential when organizations are shifting the focus from individual employees toward the bigger picture of process goals and improving end customer satisfaction (Kohlbacher & Gruenwald, 2011). Furthermore, the holistic view of BPM gives equal importance to hard BPM aspects (i.e., IT and methods throughout a BPM lifecycle view) and soft BPM aspects (i.e., people and culture with BPM-supportive values; Van Looy, 2015; vom Brocke & Rosemann, 2015; Schmiedel et al., 2013; Willaert et al., 2009). Nonetheless, these studies mostly cover an organizational and managerial perspective by focusing on a top-down approach, while the bottom-up reactions to process changes and the employee perspective also play an important role in successful BPM implementations (Beverungen, 2014; Harmon, 2007). Given that many undesired process outcomes might be caused by employees’ dissatisfaction, such a bottom-up perspective helps explain the issues that managers face during BPM implementation (Al-Mashari & Zairi, 1999; Hammer & Stanton, 1999). This perspective is important to scrutinize since employees actually improve, manage, and execute processes in daily work. Unsatisfied or unmotivated employees can become serious bottlenecks in process execution (Hammer, 2007; Harmon, 2007). For instance, if employees are not satisfied with new process changes and not motivated to commit to process outcomes, even a perfectly designed process equipped with the best IT will be doomed to fail (Hammer, 2007; Harmon, 2007), and a sustainable adoption of BPM will be questionable.

Despite the demonstrated link between rewards and job satisfaction in the HRM (human resource management) literature, it remains unclear how employees’ job satisfaction is maintained within the context of business processes and affected by rewards. While the HRM literature primarily examines team-based rewards in general (Gomez-mejia & Franco-Santos, 2015), little is known about how different reward types together with certain business process characteristics affect the job satisfaction of process participants (i.e., individual employees and teams; Van Looy et al., 2014). An employee perspective (and specifically, satisfaction with business processes and the linked rewards) still remains under-researched and thus a crucial gap to be investigated. For instance, few studies have tried to achieve BPM-HRM alignment through practices from an organizational and managerial perspective (Scekic et al., 2012; Shafagatova & Van Looy, 2021; Zhang, 2018), but not the impact of different reward types or their interaction with different process-related characteristics on job satisfaction.

We argue that it is essential to gain more insight into what the best selection of reward types for different process circumstances is in order to enhance employees’ job satisfaction. Therefore, we will identify possible interaction effects between the process-related aspects of one’s job and existing pay-for-performance practices on the resulting job satisfaction. Accordingly, we define the following research question:

RQ. How do business process-related job characteristics and performance-based rewards jointly contribute to the average employees’ job satisfaction?

To address the research question, we have developed the following objectives:

(a) To study the impact of process-related characteristics on the average employees’ job satisfaction

(b) To study the impact of different types of pay-for-performance on the average employees’ job satisfaction

(c) To study if any interaction effect exists between the level of involvement of process characteristics and the type of pay-for-performance on the average job satisfaction

(d) To provide a refined model based on the interaction among the above-mentioned independent and dependent factors of our study

We address these objectives by applying a quantitative research design on a large and representative open-access European dataset containing five-yearly responses gathered from 35 European countries. While conceptualizing the reward approaches that work best for organizations, we report on a series of factorial analysis of variance (ANOVA with interaction effects) and analysis of covariance (ANCOVA, i.e., interaction effects controlled for organization size and sector as covariates). These statistical tests allow us to thoroughly explore how job satisfaction is influenced by the presence or absence of specific pay modes and process-related aspects, namely both as separate effects and as interaction effects on job satisfaction. This study is innovative in the sense of combining theories in the HRM-BPM literature (Section 2.5), and providing a novel approach to connect process-related factors with pay-for-performance types, while analyzing their interactive effect on job satisfaction. Additionally, we derive practical contributions. For instance, our findings will assist organizations in planning their HRM and BPM strategies in the context of a digital age. Thus, the intended findings can have an important impact on the success of BPM implementation practices, especially within digital transformations.

We proceed as follows. Section 2 presents relevant literature and derives the hypotheses for this study. Section 3 details our research method. Section 4 presents the findings, whereas Section 5 adds interpretations, contributions, and limitations while also presenting recommendations for future works. We conclude by presenting a synthesis in Section 6.

Theoretical Background and Hypothesis Development

We start by positioning the relevant concepts, definitions, and their interrelationships to identify our theoretical underpinnings. Furthermore, we position the gaps and derive the hypotheses to be tackled in this work.

Business Processes and BPM

BPM is a management discipline that encompasses a body of methods and tools to explore, analyze, redesign, implement and monitor business processes throughout their lifecycle (Dumas et al., 2018). For this study, we focus on three BPM pillars that are subsequently described, namely (1) business processes, (2) process-related outcomes, and (3) BPM-supporting values.

Business Processes

Business processes (as the core pillar of BPM) represent the functioning of an organization to deliver products or services (Skrinjar & Indihar Štemberger, 2009). A business process is defined as “a collection of inter-related events, activities, and decision points that involve a number of actors and objects, and which collectively lead to an outcome that is of value to at least one customer” (Dumas et al., 2018, p. 6). Similarly, people as process participants are defined as a core BPM element, and need to continually enhance and apply their process skills and knowledge to improve business performance (vom Brocke & Rosemann, 2015). Hence, we are focusing on human actors in business processes in this research, and examine the employee-oriented process characteristics related to their roles and activities.

Process-Related Outcomes

The main objective of BPM implementation is to improve the process-related performance outcomes of organizations (e.g., effectiveness, efficiency, and quality; Schmiedel et al., 2013; Van Looy & Shafagatova, 2016). Such direct positive impact has been agreed upon in other BPM-related studies (Hernaus, 2012; Skrinjar et al., 2007; Weitlaner & Kohlbacher, 2015). Hence, by fostering alignment between BPM and the corporate strategy, the strategic view of BPM enables the implementation of an organizational strategy by means of process goals (de Bruin & Rosemann, 2006), and supports system thinking for integrating complexities and different management areas (Fowler, 2003). The concept of value chains highlights the added value of core processes and how to get the best out of a process chain by linking it with the organization’s strategy execution (Porter, 1985; vom Brocke & Rosemann, 2015). Consequently, we consider the process-related outcomes as the second core pillar of BPM in this study.

BPM-Supporting Values

In addition to the strategic approach of BPM, recent studies have emphasized the importance of BPM-supportive values in organizations for successfully achieving process goals (Benraad et al., 2022; Hermkens et al., 2022). Examples of process-oriented values are customer focus, excellence, responsibility, and teamwork (i.e., also known as CERT values), which have a proven positive impact on BPM success (Schmiedel et al., 2013). These strategic and cultural elements are part of a holistic approach to BPM, that encourages a comprehensive look at BPM by including people-related success factors next to methods and IT (vom Brocke & Rosemann, 2015). Therefore, we consider BPM-supportive values as the third pillar of BPM in this study.

While studies have been done on different people aspects of BPM (Benraad et al., 2022; Danilova, 2018; Harmon, 2007; Hermkens et al., 2022; Kratzer et al., 2019; Müller et al., 2016; Skrinjar & Trkman, 2013), most of them deal with management, organizational, and cultural perspectives. Few studies have been conducted to explore employee-related topics, such as the resistance to change among employees during BPM implementation, empowerment aspects of BPM, and employees’ perception of BPM (Mertens et al., 2011; Meyer & Schiffner, 2014; Pereira et al., 2019). Prior studies have proven that BPM has both a direct and indirect positive effect on organizational performance (Hernaus, 2012; Klun & Trkman, 2018; Skrinjar et al., 2007). However, the employee perspective of BPM in terms of how BPM affects job satisfaction is not studied so far.

The main objectives of organizational BPM are improving efficiency, effectiveness, flexibility, and quality of processes. The employee perspective is implicitly mentioned in the “internal quality” subdimension of process performance measurement, which is related to the process participants’ viewpoint. Typical internal quality concerns are the level that a process participant feels in control of the work performed, the level of variation experienced, and whether working within the context of the business process is felt as challenging. Thus, they is limited to the perception of control, variation, and challenges that employees feel within a business process. However, the job satisfaction of those process participants and what effect process characteristics and rewards have on it is still unknown.

Considering the employee perspective in terms of job satisfaction and incentivization will ensure the smooth implementation and adoption of BPM changes. In this perspective, our study supplements the BPM body of knowledge by targeting the process participants involved in the business processes in terms of their job satisfaction. For the purpose of this study, we will focus on the following BPM components: (1) business processes in the form of their task-related characteristics, (2) their process-related or management-related outcomes (e.g., quality, targets, improvements), and (3) the BPM-supportive values. Hence, we propose that the presence of these BPM components has a direct effect on employees’ job satisfaction (as a specification of the earlier business performance studies).

Rewards and Pay-for-Performance

Besides BPM, we focus on HRM rewards. Rewards drive organizational goals by reinforcing desirable behavior and enhancing the motivation and satisfaction of individual employees (Bernardin & Russel, 2013; DeMatteo et al., 1998; Lawler, 2011). The latter refers to employees’ behavior contributing to the corporate strategy and meeting the organizational objectives in an effective way (Lorincová et al., 2020). The strategic importance of rewards has been thoroughly researched in the HRM literature (Armstrong & Brown, 2006; Boyd & Salamin, 2001; Zhang, 2018). Rewards include all forms of financial returns (e.g., base pay, variable pay, and benefits) and non-financial returns (e.g., for recognition or development) that employees receive as part of their employment relationship (Armstrong & Stephens, 2005; Noe et al., 2015). More specifically, pay-for-performance is a variable pay that is awarded based on output measures or performance contributions and can be both on the individual or group level (Agarwal, 1995).

The theoretical foundations underlying pay-for-performance are explained by expectancy theory and goal-setting theory, which jointly provide strong predictive power for improving pay-for-performance systems (Bernardin & Russel, 2013). Goal-setting theory assumes that motivation and performance will improve if people have difficult but agreed goals and receive feedback (Locke & Latham, 2002), while expectancy theory states that employees will direct their work efforts toward behaviors that they believe will lead to desired outcomes (i.e., rewards; Collings & Wood, 2009). If implemented correctly, reward systems have been demonstrated to motivate employee performance (Gerhart & Milkovich, 1992; Lawler, 2003) because money tends to influence employees’ behavior by shaping their attitudes (Parker & Whright, 2001).

In recent years, working in teams has increased in practice and necessitates the introduction of team-based and performance-based rewards, which are topics with much attention in the HRM literature (Aguinis et al., 2013; DeMatteo et al., 1998). Bringing rewards to team levels can increase the line of sight among team members and give the motivation to keep an eye on the business outcomes (Aguinis et al., 2013; Boswell et al., 2006; DeMatteo et al., 1998). This reasoning also applies to BPM since managing business processes should occur on both individual levels (i.e., by process workers, process analysts, and process managers) and team levels (i.e., cross-functional teams for process improvement and process execution; Dumas et al., 2018). While individual and team-based rewards have been studied in generic HRM literature, their business process context and joint impact on satisfaction are under-researched. Consequently, this study will focus both on the individual- and team-based pay-for-performance practices in organizations. We specifically assume that the presence of an individual or team-based pay-for-performance will have a direct effect on employees’ job satisfaction (in line with expectancy theory and goal-setting theory).

Job Satisfaction

Since our focus of interest lies on the employee perspective, we take a closer look at the concept of job satisfaction. Locke (1976) originally defined job satisfaction as “a pleasurable or positive emotional state resulting from the appraisal of one’s job or job experiences” (p. 1304). This definition focuses on the employee perspective by means of employee perceptions and experiences, as proved by following researches as well (Aktepe & Ersoz, 2012; Petty et al., 1984; Saari & Judge, 2004). Job satisfaction is typically measured by several dimensions such as satisfaction with perceptions of pay, relationships, recognition, work environment, enthusiasm, promotion, and overall satisfaction (Bala & Venkatesh, 2017; Davis, 2004; Siengthai & Pila-Ngarm, 2016). Interestingly, this bottom-up perspective can help explain the issues that managers face during BPM implementation, since employees’ dissatisfaction might be the root cause of undesired process outcomes (Al-Mashari & Zairi, 1999; Hammer & Stanton, 1999). Such an important link is still less studied in the BPM literature. Hence, it is required yet preeminent to focus more on how certain process-related elements influence employees’ job satisfaction.

The Combined Impact of Processes and Rewards on Job Satisfaction

Prior studies have demonstrated that effectively organized HRM practices (and especially appropriate rewards) have a positive impact on job satisfaction (Lawler, 2003; Najam et al., 2020; Terera & Ngirande, 2014), namely as being one of the most significant concepts determining employees’ job satisfaction (Armstrong & Stephens, 2005). Moreover, especially financial incentives are believed to affect job satisfaction (Heimerl et al., 2020; Kosteas, 2011). In addition, the BPM literature mentions the importance of rewards for successful implementations and calls for better aligning rewards to the needs of business processes (Van Looy et al., 2014; Willaert et al., 2009). While few studies have examined how to achieve this BPM-HRM alignment through practices from a managerial and organizational perspective (Scekic et al., 2012; Shafagatova & Van Looy, 2021; Zhang, 2018), research is lacking about the impact of dedicated reward types with a direct link to process-related characteristics on employees’ job satisfaction.

We expect that the dynamics between BPM, rewarding types, and job satisfaction are critical for an organization’s BPM implementation. The reason is that, independent of how well process designs and BPM-related tools can work in theory, the risk of becoming indifferent to the success of processes and the organization increases when employees are dissatisfied with the processes they are involved in or when they are not incentivized with appropriate rewards (Hammer & Stanton, 1999; vom Brocke & Rosemann, 2015). Moreover, unsatisfied or unmotivated employees can become serious bottlenecks in process executions (Hammer, 2007; Harmon, 2007).

Therefore, it is essential to acquire more insight into what the best selection of reward types is for different business process circumstances in order to enhance employees’ job satisfaction. This study addresses the crucial research gap on the combined impact of business process characteristics and reward types on employees’ job satisfaction, which is essential when designing business processes and jobs.

Hypothesis Formulation

Our theoretical starting point is “expectancy theory,” suggesting that individuals are motivated to perform if they know their extra performance is recognized and rewarded (Vroom, 1964). As a result, employees’ actions will lead to a specific result, for which they will receive attractive rewards (Adamopoulos, 2022; Collings & Wood, 2009) and consequently organizations using performance-based pay can expect improvements. Similarly, “goal-setting theory” assumes that motivation and performance will improve if people have difficult but agreed goals and receive feedback (Locke & Latham, 2002). A third conceptual motivation for our hypotheses is the “model of motivation” by Lawler and Porter (1967), which was built based on the “expectancy theory” of Vroom (1964). The basic idea of this model is that the concepts of motivation, satisfaction, and performance are three independent but interrelated factors, which can complicate the concept of employee motivation (Adamopoulos, 2022). Our fourth theoretical lens is the “theory of job characteristics,” which is based on the idea that work itself is the key to motivating employees (Hackman & Oldham, 1976). Such specific work characteristics affect employee behavior and attitudes in different ways (Adamopoulos, 2022). While the expectancy theory and job characteristics theory focus on objectivity and subjectivity respectively, the model of motivation has a broader view of the links among factors.

Based on the above-mentioned theoretical concepts and the crucial gaps in the literature that were mentioned earlier, we hypothesize that the combination of process-based characteristics and different types of pay-for-performance rewards has an interaction effect on job satisfaction, meaning that a change in one factor will change the effect of the other factors on job satisfaction. In order to explore the interrelated links between process-oriented factors and HRM rewards and their impact on job satisfaction, we have developed a research model with three hypotheses (H1, H2, and H3), as illustrated in Figure 1. This model contains three main elements: process-related characteristics and pay-for-performance as the independent variables, and job satisfaction as the dependent outcome.

The initial research model for combining BPM with specific HRM reward types.

First, based on the theory of job characteristics (Hackman & Oldham, 1976) and the previously-discussed literature, we expect that a difference in job satisfaction depends on the involvement of dedicated process characteristics in an employee’s job (Wood et al., 2012). In this sense, the presence or absence of those characteristics will trigger higher or lower job satisfaction, respectively. Hence, H1 scrutinizes this difference in average job satisfaction for the process-related categories. Accordingly, we develop our null and alternative hypotheses for the first main effect as follows:

H10: There is no difference in the average job satisfaction level among the process-related factors.

H1a: There is a difference in the average job satisfaction for the process-related factors.

Secondly, inspired by the expectancy theory (Vroom, 1964), the goal-setting theory (Locke & Latham, 2002), and the previously-discussed literature in HRM, we anticipate that job satisfaction will differ for certain types of pay-for-performance. Therefore, we expect an increased satisfaction rate as a result of individuals and specifically team-based pay-for-performance rewards (Kosteas, 2011; Terera & Ngirande, 2014). Thus, for the second main effect, we hypothesize:

H20: There is no difference in the average job satisfaction level for any type of pay-for-performance.

H2a: There is a difference in the average job satisfaction by the type of pay-for-performance.

Finally, inspired by the model of motivation (Lawler & Porter, 1967) and by combining H1 and H2, we expect an interaction effect of process characteristics and pay-for-performance reward types on job satisfaction (Terera & Ngirande, 2014). Therefore, the presence or absence of certain process characteristics will affect job satisfaction differently for each pay-for-performance type. Hence, H3 investigates this interaction effect as follows.

H30: The effect of one independent factor (i.e., HRM-related) on the average job satisfaction does not depend on the effect of the other independent factor (i.e., process-related).

H3a: The effect of one independent factor (i.e., HRM-related) on the average job satisfaction depends on the effect of the other independent factor (i.e., process-related).

Research Method

In order to study the hypotheses presented in our model (Figure 1), we applied empirical evidence based on a quantitative research design. We subsequently present the related data preparation and operationalization (Section 3.1), after which the statistical tests are motivated (Section 3.2). Section 3.3 continues with the evaluation criteria of validity and reliability.

Data Preparation and Operationalization

Due to the high amount of data that was required to examine the hypotheses, we used an open-access European dataset, namely the European Working Conditions dataset (Eurofound, n.d.). This dataset contained five-yearly responses from employees in 35 European countries, considering that there was only one respondent per organization. The countries included the EU Member States, Norway, Switzerland, Albania, North Macedonia, Montenegro, Serbia, and Turkey.

The questions were categorized and the majority of them were defined as binary (i.e., yes/no options). The most recent dataset went back to the year 2015, which was the version that we applied in our study. We selected this dataset for our research because it was the only dataset including variables on pay for individual performance. Nevertheless, we did not collect the data for this study ourselves and decided to use the mentioned open-access dataset without any manipulation but only filtering based on the required domains and variables. Hence, we reduced the initial sample of 43,850 respondents to 35,843 respondents, and limited our scope to pay-for-performance, business processes, and job satisfaction variables (Table 1). Given this secondary data collection approach, no extra ethical considerations were required unless those stipulated by (Eurofound, n.d.). Due to the size of the dataset, it was not possible to add it to the Supplemental Appendices of this paper but the entire dataset is available upon request (Eurofound, n.d.).

List of the Selected Variables From the European Working Conditions Dataset (2015).

Table 1 demonstrates all variables selected for our analysis which were mapped to the relevant theoretical concepts in Section 2. For the process-related variables, we selected 17 variables that helped us operationalize the BPM components in Section 2. Our selection included process design (i.e., process tasks and activities), process outcomes (i.e., targets and standards), and CERT values (i.e., customer focus, excellence, responsibility, and teamwork).

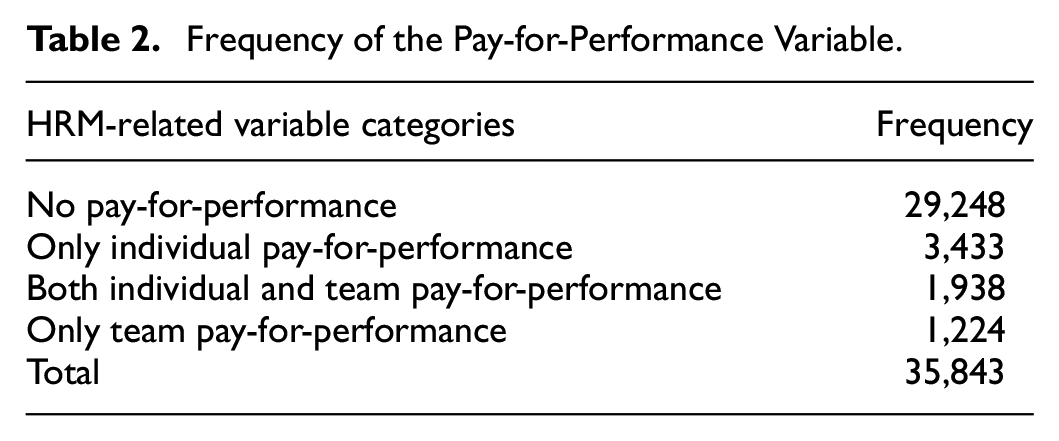

Regarding the pay-for-performance rewards variable, we computed a new variable by combining the two pay-for-performance sub-variables (Q101f and Q101g). Due to their binary character, we obtained a 2x2 matrix containing four categories for this new HRM variable as shown in Table 2 (i.e., NoxNo, YesxNo, NoxYes, and YesxYes).

Frequency of the Pay-for-Performance Variable.

Surprisingly, we observed that the majority of respondents received no pay-for-performance reward (i.e., the first group in Table 2). It indicates that the pay-for-performance practice is not yet ingrained in European organizations. This observation demonstrates our study’s relevance by uncovering the under-used opportunities and exploring their effect on employees’ satisfaction for future usage (i.e., for convincing managers).

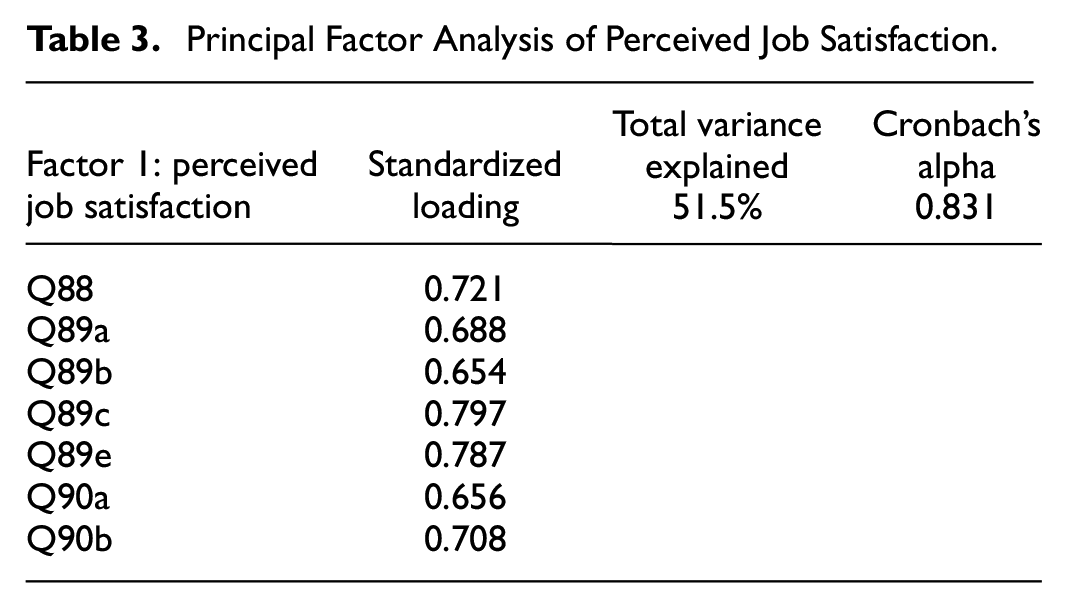

Regarding the job satisfaction variable, we conducted different rounds of factor analyses with satisfaction-related items from the dataset to demonstrate scale validity and reliability. The factor loadings of the seven satisfaction-related variables in Table 3 were satisfactory (i.e., with values higher than 0.6) to determine our latent construct of “perceived job satisfaction.” The principal factor analysis extracted one factor that explained 51.5% of the total variance of the satisfaction variables. Reliability was shown by a high Cronbach’s alpha of .831.

Principal Factor Analysis of Perceived Job Satisfaction.

Data Analysis

In order to analyze the data, we applied a series of two-way analysis of variance (ANOVA) and analysis of covariance (ANCOVA) tests, implemented in SPSS (version 26). ANOVA is one of the most common statistical analyses, frequently used in many research areas, and allowing researchers to determine if and how variables are related. More specifically, it allows to determine if the mean scores of different groups or conditions differ (Rutherford, 2011). Two-way ANOVA is used when there are two independent variables and the outcome or dependent variable is an interval or ratio (Adams & McGuire, 2022). Furthermore, ANCOVA is a combination of regression and ANOVA, that allows researchers to determine if the group or condition mean scores differ after the influence of another variable on the analysis of data (Rutherford, 2011).

In this study, we used two-way ANOVA to explore the interaction effect between our two independent, categorical variables (i.e., reward-related and process-related) on the dependent interval variable (i.e., job satisfaction). We also applied ANCOVA for controlling the environmental factors (i.e., size and sector) during the interaction effect. The first two hypotheses of Section 2.5 separately linked the independent variables related to BPM and HRM to average job satisfaction. Next, based on the third statistical hypothesis in Section 2.5, we examined the joint interaction effect of each process-related variable with each pay-for-performance type on the average job satisfaction. Thus, we started the analysis phase by investigating the effects of each independent variable separately, and consequently, we examined the respective interaction effect.

We started by checking the ANOVA assumptions of: (1) independence of observations, (2) a normally-distributed dependent variable, and (3) homogeneity of variance (i.e., homoscedasticity). First, since all observations were different employees and there was no repeated measurement, the first assumption was met. Secondly, because of the large sample size (i.e., of more than thirty-thousand respondents), the central limit theorem holds (Rouaud, 2013; Waymire, 2008), thus the sampling distribution of the mean for a variable will approximate a normal distribution. Finally, the variance was examined with box-plots (see Figure 2 for an example), which showed that the variances were similar so that we could proceed with two-way ANOVA (Field, 2016b; Recker, 2013; Stockemer, 2019).

Sample box-plot showing variance (more plots in Supplemental Appendix A).

All process-related variables from Table 1 were included in SPSS to explore whether any of them had an interaction effect with pay-for-performance on job satisfaction. Consequently, we conducted 17 separate two-way ANOVA tests, each time with one process-related characteristic and pay-for-performance as independent variables, and “perceived job satisfaction” as the outcome variable.

When a statistically significant difference in interactions was present, the procedure for a simple main effect was carried out to examine which groups differ pairwise. In this case, one cannot interpret the main effects without considering the interaction effect. Since SPSS does not yet offer an explicit procedure for examining such simple main effects, we made use of the syntax in Table 4 (Field, 2016b; Finney, 1948).

Sample Syntax for Simple Main Effects Analysis in SPSS.

Finally, we also added size and sector (i.e., of organizations where respondents work) as control variables to get more accurate results when examining the significant interactions by means of two-way ANCOVA tests. Thus, we recoded and regrouped the given size and sector categories in the original dataset into higher-level groups (i.e., size: small, medium, and large; sector: production, service, and social profit), and created dummy variables for each option to be added as a covariate in our two-way ANCOVA. We added this step in order to remove the possible effect of these covariates and reduce standard error for the means (Field, 2016a).

Validity and Reliability

Reliability was assured by checking internal consistency with a Cronbach’s alpha for the outcome latent variable, which had a highly acceptable value of .8. We also described all steps and syntax used in our research for repeatability. Likewise, the dataset was gathered from almost all European countries and included 35,843 respondents as being a large variety of observations (Eurofound, n.d.). We selected our variables based on the theoretical background in Section 2, which ensured that variables measure what we intended to study for content validity. At the end, we ensured the construct validity for our latent variable by principal factor analysis (Recker, 2013).

Results

In this section, we describe the results of the two-way analyses of variance (two-way ANOVA) to statistically demonstrate the main effects (H1 and H2) and possible interaction effects (H3) of the two independent variables (i.e., one process-related and one pay-for-performance type) on the perceived job satisfaction of employees.

We started by examining the main effects of the process-related variables on the average job satisfaction, which was the first objective of this study (a) based on H1. Table 5 shows that almost all main effects of the process-related variables were significant in our two-way ANOVA analysis (i.e., conducted separately for the 17 process variables). This finding indicated that the average perceived job satisfaction differs based on the presence or absence of process-related variables. Therefore, we could argue that H1a is accepted and our first objective (a) is met.

The Main Effects of Process-Related Variables on Job Satisfaction.

p < .050.

In a similar way, we found that the main effects of all pay-for-performance types were significant, which means that job satisfaction differences were present in the pay-for-performance categories (i.e., supporting H2a). Analyzing the post-hoc Bonferroni results, we observed that all pairwise comparisons were significant except for the difference between the “only individual pay-for-performance” group and the “only team pay-for-performance” group. This result proves H2a and addresses our second objective (b).

Furthermore, we found that five out of 17 process-related variables (i.e., Q50a, Q50c, Q53a, Q53b, and Q53f) turned out to have significant interaction effects with pay-for-performance on job satisfaction. This finding addresses H3a and our third objective (c).

Consequently, for these five variables, we conducted a two-way ANCOVA test to analyze the effect of environmental variables (i.e., with organization size and sector being controlled as covariates). Subsequently, we describe the results for these five process-related variables, namely by relooking at the main effects of H1 and H2, and the interaction effects of H3 where size and sector were controlled for more accurate results. For each of the subsequent subsections, we report on the research steps as follows:

Step 1: we report on the two-way ANCOVA with one process-related variable and pay-for-performance as independent variables to reject the null hypotheses of Section 2.5.

Step 2: we report on the simple main effect procedure to uncover pairwise group differences, and we do this for all options per process-related variable.

Work Interdependency (Q50a)

We first looked at the interaction of HRM rewards and work dependency on colleagues (Q50a) with organizational size and sector as controlled variables. We noticed that there was a significant main effect of pay-for-performance (F(3, 34,925) = 138,303, p = .000) and work interdependency (F(1, 34,925) = 15,741, p = .000) on job satisfaction. These findings rejected both main effect null hypotheses of H1 and H2 (Supplemental Appendix B1 and B2). Additionally, a significant interaction was present between the combined effect of work interdependency and pay-for-performance type on perceived job satisfaction (F(3, 34925) = 3,198, p = .022). Consequently, we rejected the interaction effect null hypothesis of H3 as well.

Next, we conducted the simple main effect test to examine the group-level differences (Supplemental Appendix B3 and B4). For most pay-for-performance levels, employees had lower satisfaction scores when they are dependent on colleagues. Only in case they received both reward types, the satisfaction rate was the same (i.e., adjusted mean = 0.388) for both categories (i.e., dependent and non-dependent on colleagues; Figure 3).

Interaction plot of pay-for-performance and dependency on colleagues on job satisfaction.

The simple main effects analysis showed that when employees’ work pace was dependent on colleagues, employees without any pay-for-performance had a significant lower job satisfaction compared to other employees (i.e., with “only individual” pay-for-performance, “both” types of pay-for-performance and “only team” pay-for-performance). Furthermore, employees who received both pay-for-performance types turned out to have significantly higher job satisfaction scores as compared to the others (i.e., ones without pay-for-performance, only individual pay-for-performance, or only team pay-for-performance; Figure 3). The satisfaction difference was bigger when “both types” of pay-for-performance and “only team” pay-for-performance were compared. Interestingly, employees were significantly less satisfied when they only received team rewards and were dependent on colleagues.

The trends were similar for employees whose work pace was not dependent on colleagues, but with a slightly higher job satisfaction. There were no significant differences between “only individual” and “only team” pay-for-performance employees in both categories (Supplemental Appendix B3 and B4).

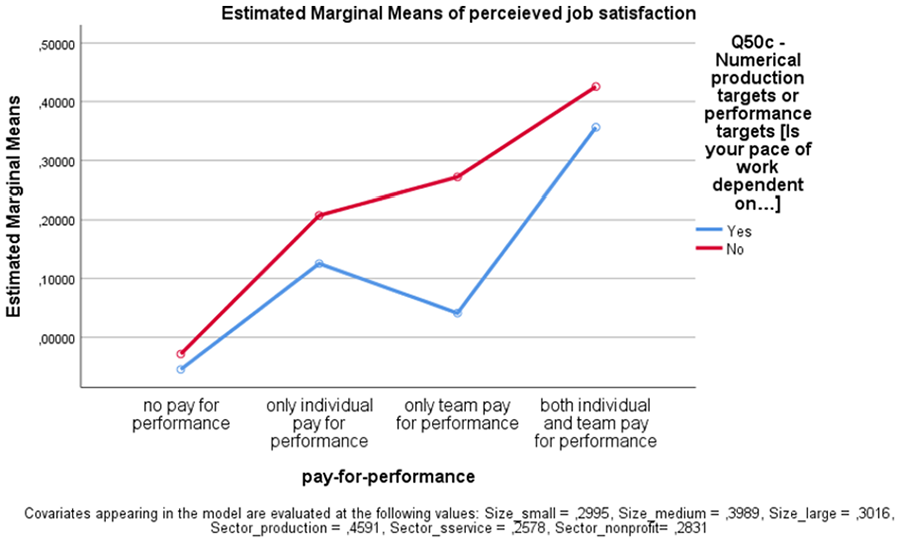

Performance Targets (Q50c)

In a similar way, we analyzed the interaction of HRM rewards and the variable of performance targets (Q50c). There was a significant main effect on job satisfaction, leading to the rejection of both main effect null hypotheses of H1 and H2 (Supplemental Appendix C1 and C2). Moreover, for H3, there was a significant interaction effect: F(3, 34,724) = 4.513, p = .004. For all pay-for-performance levels, employees had a significantly lower job satisfaction when they were dependent on targets, except for “both types” of rewards (i.e., no significant difference; Supplemental Appendix C1 and C2). The conducted simple main effect tests for examining the group level differences are shown in Supplemental Appendix C3 and C4.

The simple main effects analysis showed that when employees’ work pace was dependent on performance targets, employees without pay-for-performance had a significant lower job satisfaction compared to other employees. Employees who received “both types” of pay-for-performance had a significant higher job satisfaction compared to the rest of the employees. Employees who received “only individual” pay-for-performance showed no significant difference in job satisfaction compared to the ones who received “only team” pay-for-performance. The satisfaction difference was bigger when “both types” of pay-for-performance were compared with “only team” pay-for-performance, whereas employees were are much less satisfied when they received “only team” rewards (Figure 4).

Interaction plot of pay-for-performance and performance targets on job satisfaction.

The trends were similar for employees whose work pace was not dependent on performance targets, albeit now with higher satisfaction rates. No significant differences were found between employees in the “only individual” and “only team” pay-for-performance groups for this category (Supplemental Appendix C3 and C4). When comparing the two categories (i.e., dependent and non-dependent on performance targets), it is remarkable that employees who do not depend on performance targets and have no pay-for-performance have a slightly higher job satisfaction than employees who depend on performance targets and have “only team” rewards.

Quality Standards (Q53a)

A similar line of thought applied to the interaction of HRM rewards and quality standards. Given a significant main effect of the independent variables on job satisfaction, we rejected both main effect null hypotheses (Supplemental Appendix D1 and D2). Additionally, there was a significant interaction effect on perceived job satisfaction: F(3, 34,925) = 3.198, p = .022. Consequently, we conducted the simple main effect test to examine the group-level differences (Supplemental Appendix D3 and D4).

The simple main effects analysis showed that when an employee’s job involved meeting quality standards, employees without pay-for-performance had a significant lower job satisfaction compared to other employees. Furthermore, we observed that employees who received both types of pay-for-performance had significantly higher job satisfaction compared to other employees. Employees’ satisfaction was almost the same for “only individual” and “only team” reward groups (i.e., with adjusted means of 0.189 and 0.181, respectively).

The trends were similar for employees whose job did not involve meeting quality standards. There were no significant differences between employees with “only individual” and “only team” pay-for-performance (Supplemental Appendix D3 and D4). They both had a significant higher job satisfaction than the “no pay-for-performance” groups and a lower job satisfaction than employees with “both reward” types. When comparing the two categories of quality standards for rewards, there is only a significant difference for the no pay-for-performance groups, meaning that employees with quality standards have a higher job satisfaction than those who do not have quality standards when both categories had no pay-for-performance (Figure 5).

Interaction plot of pay-for-performance and quality standards on job satisfaction.

Quality Self-Assessment (Q53b)

A fourth interaction dealt with HRM rewards and quality self-assessment (Q53b). We observed a significant main effect of the independent variables on job satisfaction, thus rejecting both main effect null hypotheses (Supplemental Appendix E1 and E2). Similarly, there was a significant interaction effect: F(3, 35,359) = 4.069, p = .007. Employees had a significantly higher job satisfaction when they could assess quality themselves, except for the “only team” pay-for-performance group (i.e., no significant difference). Supplemental Appendix E3 and E4 show the simple main effect test to examine the group-level differences.

The simple main effects analysis showed that when an employee’s job involved assessing one’s own work quality, this employee without pay-for-performance had significantly lower job satisfaction compared to other groups of employees. Furthermore, employees who received both types of pay-for-performance had significantly higher job satisfaction compared to the other groups. No significant differences were found between employees with “only individual” and “only team” pay-for-performance (Figure 6).

Interaction plot of pay-for-performance and self-assessment on job satisfaction.

The trends were similar for employees whose job did not involve assessing their own work quality, albeit with much lower satisfaction rates. No significant differences were found between employees with “only individual” and “only team” pay-for-performance groups, nor between “both types” of pay-for-performance and “only team” pay-for-performance groups (Supplemental Appendix E3 and E4). This means that if employees did not self-assess quality, “both types” of pay-for-performance and “only team” reward had similar effects on job satisfaction. On the other hand, when employees did quality self-assessments, they were more satisfied if they received “both types” of rewards. Furthermore, self-assessed employees reporting on “only team-based” rewards and “only individual” rewards had a higher satisfaction rate as the non-self-assessed employees receiving both reward types (Figure 6).

Learning New Things (Q53f)

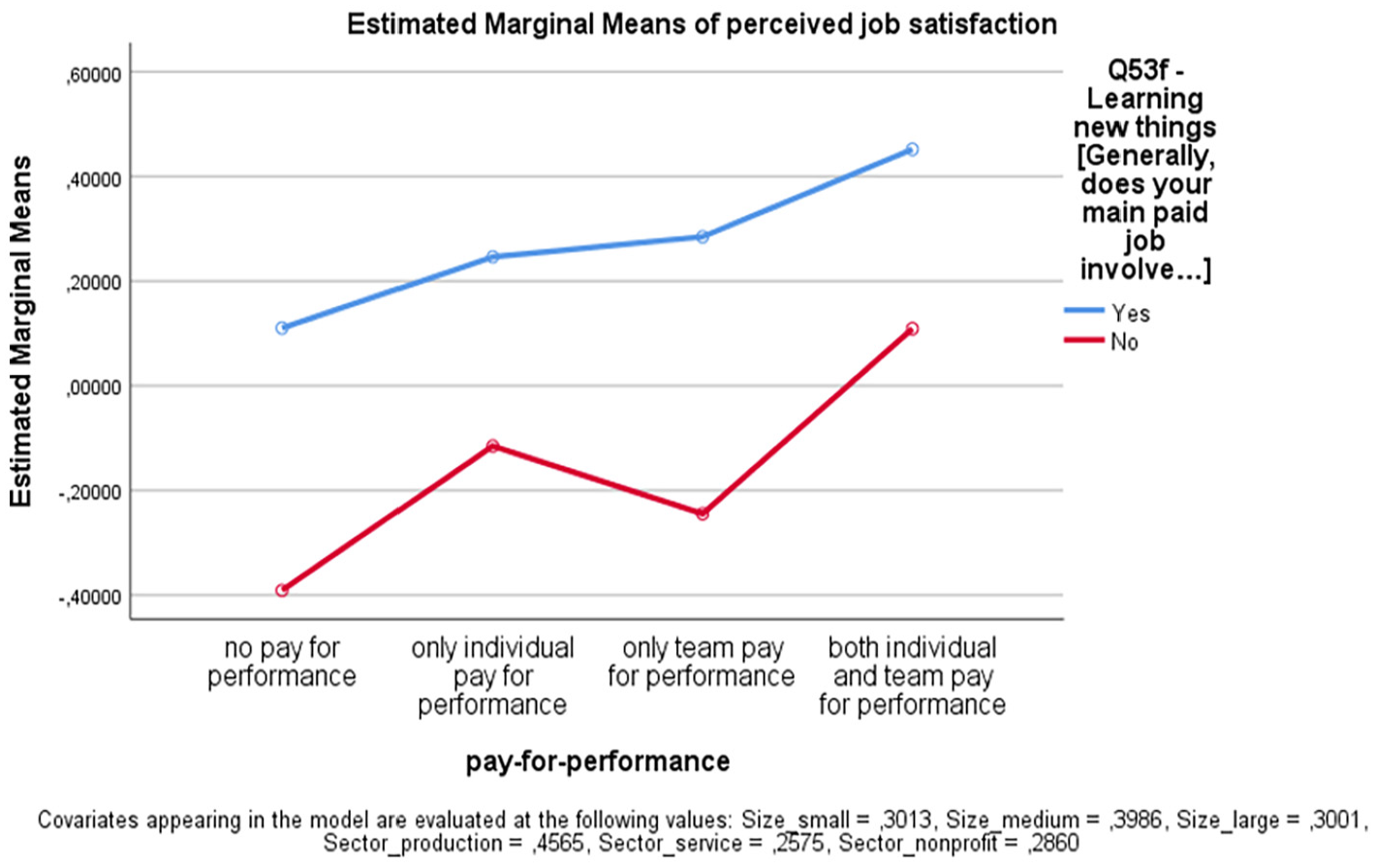

A final significant interaction was observed between HRM rewards and the process-related variable for learning new things (Q53f). Given the significant main effect of the independent variables on job satisfaction, we rejected both main effect null hypotheses (Supplemental Appendix F1 and F2). Data also showed a significant interaction effect on perceived job satisfaction: F(3, 35,479) = 5.044, p = .002. For all pay-for-performance levels, employees had a remarkable higher job satisfaction when learning new things. Supplemental Appendix F3 and F4 presents the simple main effect test to examine the group level differences.

The simple main effects analysis showed that when employees’ job involved learning new things, employees without pay-for-performance had a significant lower job satisfaction compared to other employees (i.e., with “only individual” pay-for-performance, “both” types of pay-for-performance, and “only team” pay-for-performance). Employees with “both types” of pay-for-performance had a significant higher job satisfaction compared to the other groups. There were no significant differences between employees with “only individual” and “only team” pay-for-performance (Figure 7).

Interaction plot of pay-for-performance and learning new things on job satisfaction.

Among employees whose job did not involve learning new things, the job satisfaction difference was bigger when “both types” and “only team” pay-for-performance were compared. In other words, employees who do not learn new things had a lower job satisfaction when they received “only team” rewards. There were no significant satisfaction differences between “only individual” and “only team” pay-for-performance employees, not between the “no” pay-for-performance and “only team” pay-for-performance groups (Supplemental Appendix F3 and F4). When comparing both categories (i.e., learning new things and not learning new things), we observed that employees whose job did not involve learning new things but still received both rewards types, were similarly satisfied with their job as employees whose job involves learning new things but without getting any reward for performance.

General Observations

The results demonstrated that any kind of pay-for-performance is better than no pay-for-performance. If organizations plan for giving pay-for-performance rewards, considering both reward types (i.e., individual and team-based) is the best approach or they can also start with individual types (i.e., with “only individual” being better than “only team” pay-for-performance). In sum, Table 6 compares the adjusted mean values of all job satisfaction across the independent variables.

Perceived Job Satisfaction Compared Across Process Variables (Adjusted Mean Values Controlled by Organizational Size and Sector).

Table 6 shows (in bold) that the lowest satisfaction rate belonged to the group of employees who do not learn new things and do not receive any kind of rewards. Interestingly, the highest satisfaction rates were observed for the groups whose job involve either learning new things or self-assessing their work quality in combination with receiving both reward types (as indicated in bold). We should mention that those results were adjusted by controlling the covariance variables of size and sector. However, those mean values were comparable to the values without control that can be consulted for each process variable in Supplemental Appendices B2-3, C2-3, D2-3, E2-3, and F2-3.

Discussion

This research has followed an innovative approach based on theories, and by identifying research opportunities and crucial gaps at the intersection of HRM-BPM literature. We have provided a novel avenue to connect process-related factors with pay-for-performance types and have analyzed their interaction effect on job satisfaction by means of an empirical survey analysis using factorial ANOVA and ANCOVA tests. Novelty resides in being purposefully selective with variables, and by focusing on linking process-related factors and pay-for-performance with job satisfaction outcomes.

The findings have provided an answer to our research question in the form that certain process factors (i.e., work interdependency, performance targets, quality standards, self-assessments, and learning new things) together with reward types can lead to positive differences in employees’ job satisfaction. In other words, our study has resulted in conceptualizing optimal solutions that work well for all organizations in strategic planning and for facilitating BPM implementation while considering this multidisciplinary perspective.

The central contributions are as follows. First, our findings contribute to the people aspects of BPM, which are still underrepresented as compared to the literature linked to the BPM lifecycle view (Van der Aalst et al., 2016; Van Looy et al., 2014; vom Brocke & Rosemann, 2015). Secondly, we provide a deeper understanding of which reward types are better linked to which process-related characteristics in order to enhance job satisfaction. Thirdly, we contribute to BPM-supporting values and their realization through employee reinforcement and satisfaction. Subsequently, we elaborate on these related contributions to HRM and BPM practices.

Refined Research Model

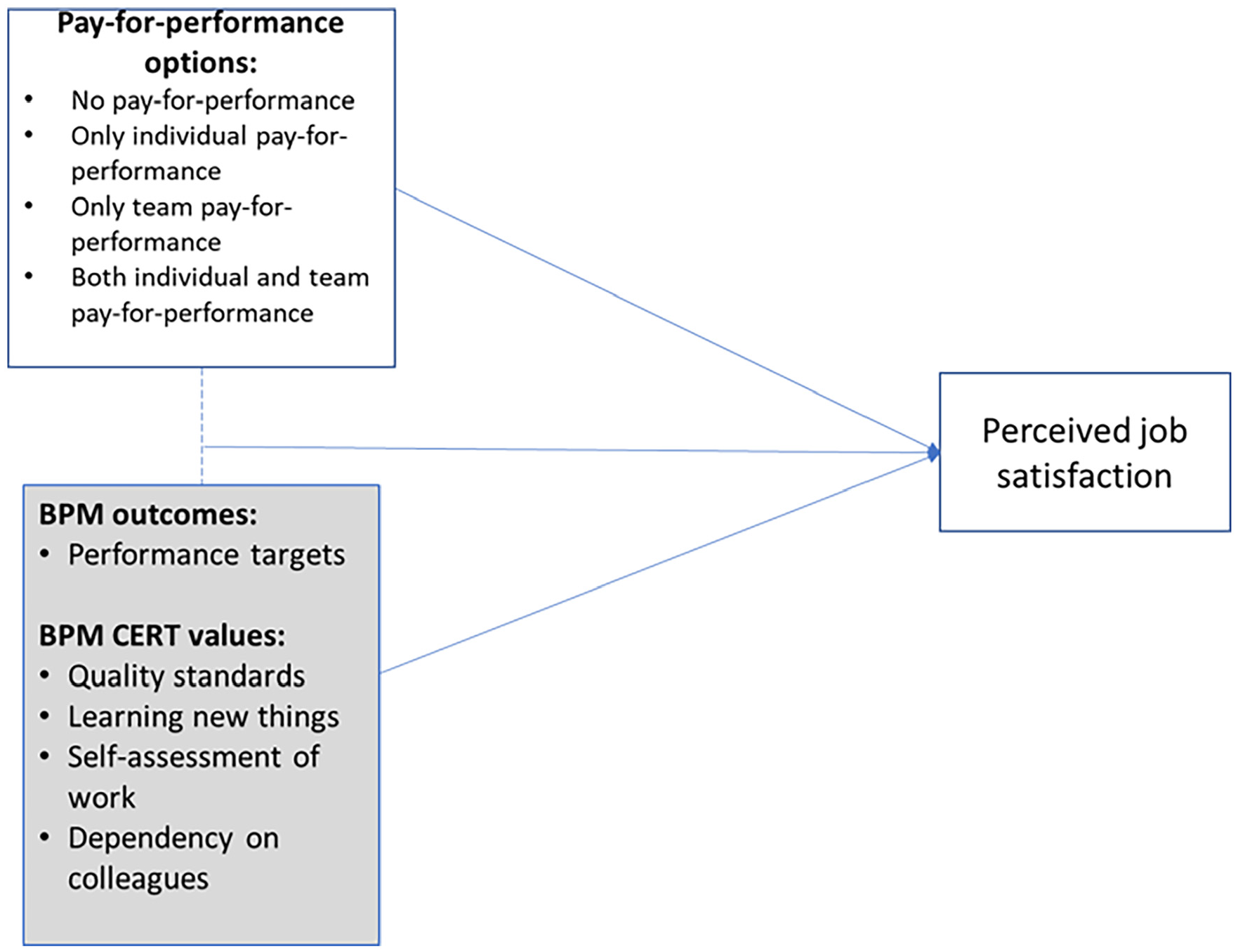

Since BPM outcomes are typically expressed as process goals in terms of efficiency, effectiveness, and quality (Dumas et al., 2018; vom Brocke & Rosemann, 2015), our findings related to performance, numerical targets, and quality standards adhere to the current strategic line of thoughts within the BPM literature (de Bruin & Rosemann, 2006; Hernaus, 2012; vom Brocke & Rosemann, 2015). Furthermore, the BPM discipline refers to the cultural values supporting BPM, and more specifically the CERT values (i.e., customer focus, excellence, responsibility/accountability, and teamwork; Schmiedel et al., 2014). From this CERT perspective, our results on quality standards can be linked to the value of a customer focus, whereas our notion of learning new things can be linked to the excellence value, our self-assessment finding to the responsibility/accountability value, and our colleague interdependence findings to the teamwork value. Since our findings can be clearly positioned in two recognized BPM streams (i.e., the BPM outcomes and the BPM-supporting values), Figure 8 refines our initial research model to better emphasize these theoretical streams along with the significant combinations of BPM aspects and HRM reward types. Moreover, we have considered organizational size and sector as control factors that are widely used in the BPM literature (Van Looy & Van den Bergh, 2018).

Refined research model for combining BPM characteristics with specific HRM reward types based on our interaction analysis results.

Figure 8 presents that our findings have demonstrated a more differentiated approach in pay-for-performance to obtain job satisfaction, controlled by size and sector, resulting in new aspects of process outcomes and values. This finding addresses our fourth objective (d).

We have uncovered five significant combinations of process-related aspects and rewards affecting job satisfaction, resulting in a differentiated approach to find optimal rewards so that employees feel more satisfied. Those process-related job characteristics are jobs involving performance targets, quality standards, learning new things, self-assessment of work, and dependency on colleagues. They all significantly interact with pay-for-performance types of “no pay-for-performance,” “only individual pay-for-performance,” “only team pay-for-performance,” and “both types of pay-for-performance,” and have a differentiated impact on job satisfaction. The results have demonstrated that for all five process-related variables, a combination of both rewards types (i.e., individual and team) turned out to be the best in order to achieve higher job satisfaction and any kind of pay-for-performance is better than no pay-for-performance. If organizations want to give pay-for-performance rewards, then it is better to give both reward types (i.e., individual and team-based) or to start with individual types (i.e., with “only individual” being better than “only team” pay-for-performance). This finding can be explained because employees give more value to a balanced rewarding, while only giving team-based rewards can undermine their satisfaction due to unmet individual needs (Aguinis et al., 2013; Mcclurg, 2001).

Consequently, we discuss the five significant process-related aspects separately, starting with work interdependency. While the direct effect of colleague dependency is likely to result in lower job satisfaction, the interactions with HRM reward types bring some interesting refinements. More specifically, employees tend to perceive the same degree of job satisfaction in both colleague-dependent and non-colleague-dependent groups when they receive both reward types. However, differences in job satisfaction increase for colleague-dependent employees when they get only team rewards (i.e., resulting in much lower job satisfaction) than for both reward types, whereas this difference is smaller in the no-colleague-dependent group. On the other hand, employees who receive both reward types and are dependent on colleagues are generally more satisfied with their job as compared to the employees who receive only individual or team rewards and who are not dependent on colleagues. The negative effect of colleague dependency on job satisfaction can be explained by its limiting effect on employees’ autonomy. Based on our study, one of its intrinsic drivers (Ryan et al., 2000) is that pay-for-performance rewards can change this effect since rewarding employees’ team efforts together with individual efforts can incentivize them to compromise their autonomy.

Secondly, we look at performance targets. While employees with performance targets generally have a lower job satisfaction than employees without performance targets (i.e., as a direct effect), more differences appear when we also consider their HRM rewards. Employees with performance targets who get both reward types tend to have a higher job satisfaction than employees without performance targets who get only team or individual rewards. Employees with targets who do not receive rewards have a similar low satisfaction level as employees without targets who get only team rewards.

Third, regarding quality standards, it appears that employees with quality standards have higher job satisfaction as a direct effect, but some exceptions exists for interactions with HRM rewards. Employees without quality standards and with both reward types are typically more satisfied with their job than employees with quality standards who get only individual or only team rewards. Having quality standards alone without any pay-for-performance also gives more job satisfaction compared to employees without quality standards and without rewards.

Fourth, the possibility of self-assessing work quality appears to have a direct positive effect on job satisfaction, which can also be explained by self-determination theory that emphasizes the individual’s need for autonomy (Deci & Ryan, 2000). Self-assessed employees without rewards are slightly more satisfied than non-self-assessed employees with individual rewards, and they are almost similarly satisfied as non-self-assessed employees with team rewards. Furthermore, self-assessed employees with only team rewards are equally satisfied as non-self-assessed employees getting both reward types. The inclusion of this process-related aspect alone can already drive employees’ job satisfaction higher, even if employees do not get any pay-for-performance rewards.

Finally, learning new things turned out to have a positive direct effect on job satisfaction, which can be explained by the intrinsic need of employees to get better in their competences (Ryan et al., 2000). Employees who do not learn new things at their job and get both reward types are equally satisfied as employees learning new things but without getting any reward for performance. They are also much more satisfied with their job than employees without learning new things but having only individual or only team rewards. The lowest satisfaction rate belongs to the group of employees who do not learn new things and do not get any kind of rewards. Interestingly, the highest satisfaction rates were observed for the groups whose job involve either learning new things or self-assessing their work quality in combination with receiving both rewards types.

The significant main effect of pay-for-performance on job satisfaction confirms prior research about the role of financial rewards on job satisfaction (Kosteas, 2011; Lawler, 2003; Terera & Ngirande, 2014), and can be explained by motivational theories (Armstrong, 2010; Gerhart et al., 2009). Additionally, the significant main effects of the 16 process-related variables (Table 5) add new dimensions into job satisfaction research to address the related gap within the BPM and job satisfaction literature. More specifically, we found ample evidence that business process characteristics such as process design, process outcomes, and values are essential to consider if managers want to ensure job satisfaction as well.

Practical Implications

Based on the interpretations of Section 5.1, we have derived five practical recommendations (Table 7) for HRM managers to decide on applying particular rewards considering different process-related aspects, and this with the ultimate goal of increasing employees’ job satisfaction.

Summary of the Main Takeaways for HRM Strategies.

It seems that providing opportunities to learn new things will have better effects on job satisfaction than rewards. Also self-assessing the quality of own work gives better job satisfaction without rewards compared to a situation in which those quality assessments are absent but replaced by rewards (e.g., only individual or only team rewards). In general, the need of autonomy, and competence from self-determination theory (Meske & Junglas, 2020; Ryan et al., 2000) provides important perspectives that help understand our results on differing satisfaction levels toward certain process characteristics. Nonetheless, combining intrinsic motivational elements with financial rewards still gives the best results in terms of job satisfaction.

Almost all situations in which individual and team rewards are combined will lead to higher job satisfaction. This combination of rewards can even neutralize the perceived negative effect of some working conditions on job satisfaction, such as a dependency on colleagues or having performance targets (i.e., which would normally result in lower job satisfaction).

This study added knowledge about the fact that certain process-related job characteristics and reward types jointly affect job satisfaction differently. We aspire that by providing more insights into the importance of the combined impact of process-related job characteristics and rewards selection on job satisfaction, our study will encourage researchers to better motivate why certain combinations are implemented and to further research those relationships by including other process-related job characteristics and reward types.

Limitations and Future Work

Despite the novelty of our findings and the related practical recommendations, we acknowledge the following research limitations. First, since we benefited from secondary data by relying on the 2015 European Working Conditions dataset (Section 3), we were limited to the variables included and their measurement levels (i.e., mainly binary). Although the selected variables were all related and linked to the concepts identified from BPM (i.e., process, design, process outcome, and process-supportive values) and HRM literature (i.e., pay-or-performance schemes), they were not encompassing all aspects of those concepts and therefore could not give a comprehensive view. As a result, the process-related variables were not always reflecting the entire process orientation character of organization. Therefore, we call for quantitative follow-up studies with more dedicated BPM and BPO variables. Furthermore, since our process related variables were binary in nature and limited to Europe, we also call for quantitative follow-up studies with more dedicated BPM variables containing different data types and expanded to other continents which will be valuable and practical.

On the other hand, quantitative studies typically have trouble in reaching out to a large set of respondents, which is an issue that we did not face. Instead, our analysis profited from a highly representative set of 35,843 respondents across 35 European countries for the sake of generalization. Thus, we attempted to get some thought-provoking insights from this large dataset by exploring the unique combination of certain variables that were not addressed before by other researchers who also employed this dataset.

Furthermore, our latent job satisfaction variable explained only 51% of variability in the involved seven satisfaction statements (Table 3), indicating that the results should be carefully interpreted and with moderate confidence. It means that the interaction model was limited to explaining 51% of variability in job satisfaction. Although the variability in our data was large, the size of our dataset still allowed us to make an accurate estimation of the population mean with a relatively small confidence interval. Meanwhile, we limited this influence by using organizational size and sector as control variables.

Finally, the explorative character of our study paves ways for new avenues. For instance, a qualitative study can be conducted to elaborate on the underlying reasons of the results obtained in this study. Since the employee perspective in terms of well-being and job satisfaction is not covered in organizational BPM objectives (i.e., effectiveness, efficiency, and quality), it would be valuable to further explore the possibilities of explicitly recognizing employee well-being as a fourth objective. This aspect can be introduced as a powerful tool to make employees aware that BPM implementation and change are not only about automating processes or having higher efficiency, but also about taking care of employees and giving their well-being equal importance.

Conclusion

While BPM has become an integrative part for digital transformation in organizations (Denner et al., 2018), the success of its implementation depends on broader factors (Dumas et al., 2018; Recker & Mendling, 2016; van der Aalst et al., 2016), and it has to go beyond a mere application of IT and methods. Nevertheless, the top-down deterministic machine character of business processes should be accompanied by bottom-up people behavior and performance. In this regard, keeping employees satisfied has a critical role in their motivation toward process success and performance. Such employee perspective remains under-researched and yet preeminent.

In this study, we have followed a novel approach in exploring the joint effect of process-related job characteristics and pay-for-performance rewards on job satisfaction by focusing on linking process-related factors and pay-for-performance. Such joint effect of these two groups was not studied before, yet crucial regarding the theories and the gaps in the BPM-HRM literature. Our study sheds light on how different reward types together with certain business process characteristics affect the job satisfaction of employees (i.e., as process participants), specifically on how they perceive job satisfaction when different kinds of process aspects are combined with different HRM reward types. By performing an empirical survey analysis on a large and representative European dataset, we found that certain process variables together with reward types can lead to significant differences in employees’ job satisfaction. We uncovered five significant combinations of process-related aspects and rewards resulting in a differentiated approach to find optimal rewards so that employees feel more satisfied. This study contributes to the people perspective of BPM, as well as to behavioral management studies and addresses the crucial gap within the BPM and job satisfaction literature and added knowledge about the fact that certain process-related job characteristics and reward types jointly impact job satisfaction differently. We strongly encourage organizations to use these five combinations (Table 7) in order to focus more on the well-being of their human capital in the context of BPM implementation.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440231160125 – Supplemental material for Uncovering the Combined Impact of Process Characteristics and Reward Types on Employees’ Job Satisfaction: A European Quantitative Study

Supplemental material, sj-docx-1-sgo-10.1177_21582440231160125 for Uncovering the Combined Impact of Process Characteristics and Reward Types on Employees’ Job Satisfaction: A European Quantitative Study by Aygun Shafagatova, Amy Van Looy and Simin Maleki Shamasbi in SAGE Open

Footnotes

Acknowledgements

We acknowledge the support of the European Foundation for the Improvement of Living and Working Conditions, and for granting us access to their 2015 European Working Conditions Survey.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.