Abstract

The study aims to determine the effect of legal systems and property rights enforcement on developing financial markets, institutions, and overall financial development in Sub-Saharan Africa. Data for this study were extracted from the Financial Development Index of the World Bank Global financial database, the Economic Freedom database of the Fraiser Institute, and the World Bank Development Indicators database covering 41 Sub-Saharan African countries from 2000 to 2020. The models were estimated using the System GMM and the SURE model as robustness checks to address cross-equation correlations and linkages between financial markets and institutions. Results showed that legal systems and property rights enforcement have an effect on the growth of financial markets, institutions, and overall financial development, regardless of the measure of financial development used. Moreover, trade and GDP positively affect financial development and financial markets, while stringent regulatory trade barriers have a negative effect. The need for governments to prioritize strengthening legal systems and ensuring the enforcement of property rights protection to create a predictable and stable environment for businesses and investors is key. Reducing trade barriers and eliminating restrictions that may discourage foreign investment to increase trade volumes and capital inflows into SSA is also important.

Introduction

The Sub-Saharan African region has witnessed significant growth in financial systems in recent years (Asongu, 2014; Odhiambo, 2018). However, there are still considerable differences in financial development across the region (Asongu, 2014; Beck et al., 2000). One key factor identified as potentially influencing financial development is the legal system and the strength of property rights. Property rights and the legal system both have various effects on financial development. According to Nawaz (2015) and Asongu (2014), a strong legal system and well-defined property rights can boost investor confidence, lower transaction costs, and expand credit availability.

According to Beck et al. (2003), Economic growth depends on financial development since it offers the resources for investment, innovation, and expansion. For the financial sector to develop, a strong legal structure and well-defined property rights are necessary. They also foster an environment where financial institutions may function successfully and efficiently.

For financial institutions to operate, a strong legal system must provide the basis for contract enforcement, dispute resolution, and regulatory oversight. More investors will be drawn to the financial system as a result, increasing the flow of capital. Property rights that are clearly defined ensure that people and companies can own and utilize their assets without worrying about expropriation or unlawful use by others, which encourages investment and capital development (Acemoglu & Johnson, 2005; Ekpeno, 2015).

La Porta et al. (1998) and Miletkov and Wintoki (2012) also observed that, property rights and legal systems differ significantly from country to country, with some having strong systems that support economic development while others have poor or dysfunctional systems that impede it. For instance, the legal framework is highly developed and transparent in nations like the United States and the United Kingdom, and strong property rights protection results in robust financial sectors. In contrast, many developing nations have weak legal frameworks and inadequate protection for property rights, which results in underdeveloped financial sectors.

Financial development is transmitted through several ways from sound legal systems and property rights. The first benefit is that they lower transaction costs and risk, making it simpler and less expensive for both individuals and corporations to conduct financial transactions. Second, they encourage competition and innovation in the financial sector by creating a level playing field and defending intellectual property rights. According to Demirgüç-Kunt et al. (2008), they also increase investor security and confidence, which increases capital inflows into the economy.

Every market economy needs property rights and a legal system in place. While legal systems provide the rules and laws that govern economic activity, property rights protect individuals’ and organizations’ rights to own and manage property. These two elements are crucial for creating an environment that is conducive to economic growth and development, according to Deininger and Feder (2009). According to Barzel (1997) and Alchian and Demsetz (1972), property rights, also called “use rights,” describe a person’s ability to use a resource for personal use or to generate income. A further aspect of property rights is the capacity to “transfer” ownership to another individual through purchases, gifts, or bequests. Property rights often also include the capacity to enter into agreements with third parties through the rental, pledging, or mortgage of the asset or the granting of permission for others to use it, as in employment contracts.

Aristotle was one of the earliest proponents of private property rights. He argued that individuals were more likely to take charge of goods they owned or were paid to maintain than communal ones (Robbins, 2000). Private property rights are often understood by economists to be those that legally forbid others from making use of an item or asset. According to Robbins (2000), property rights have an impact on resource allocation through altering people’s incentives to utilize the asset productively, investing in ways to maintain or expand its worth, and transferring or leasing it for other purposes.

According to the 2022 Economic Freedom Report, several SSA countries under scrutiny have been cataloged as either “highly unfree” or “repressed” economies” and this would result in low financial development. For instance, Demirgüç-Kunt et al. (2013) argued that property rights enforcement and effective legal institutions could stimulate innovation and entrepreneurship in the financial sector because they would make it possible to develop new financial products and services that address a variety of customer needs. The enforcement of property rights and strong legal systems, according to Beck et al. (2008), could lower the costs and risks involved in financial intermediation and market transactions by facilitating the enforcement of contracts, the resolution of disputes, the disclosure of information, and the protection of creditors.

Enforcing property rights and having strong legal systems could promote efficiency and competition in the financial sector. They would stop monopoly power, rent seeking, and corruption that impede financial development and distort resource distribution. Moreover, property rights enforcement and effective legal institutions could increase the confidence and willingness of savers and investors to finance firms and markets, as they would be assured of their rights to own, control, and recover their assets, as indicated by World Bank (2008) and Beck and Levine (2008).

Against this background, this study examines the effect of legal systems and property rights on financial markets and institutions and the overall financial development in SSA. In assessing the law-finance link where financial markets and institutions are considered, the intrinsic link between financial markets and institutions must be accounted for. Financial institutions such as banks, insurance corporations, and pension funds are often listed on stock markets, where their worth is determined. Similarly, the participation of financial institutions in financial markets determines market activity, capitalization, stability, and efficiency. Thus, any analysis of the law-finance nexus must account for these interlinkages to produce reliable results, which has been missing in most methodologies. One estimation technique that addresses interlinkages is the seemingly unrelated regressions (SURE) proposed by Zellner (1962). The SURE model accommodates the interactions between financial markets and institutions and addresses endogeneity. Since the equations are seemingly related, the SURE model is used as a robustness check to address cross-equation correlations and linkages between financial markets and institutions. The analysis presented in this paper assumes that financial markets and institutions bear no relationship and are independent.

Theoretical Underpinnings and Hypothesis Development

There are several theories that could explain the relationship between institutions and financial development. These include the Settler Mortality Hypothesis, Theory of Law and Finance, Financial Liberalization Theory and the Growth-Led Hypothesis.

The Settler Mortality Hypothesis, also known as the Endowment Theory, emphasizes the critical role of institutions, resource endowments, and geography in shaping the development of financial sectors. Acemoglu et al. (2001) proposed that during the colonial era, institutions were established to safeguard private property, prevent government expropriation, and facilitate the transfer of resources from colonies to colonizers with minimal investment. Supporting this idea, Beck et al. (2003) suggest that initial endowments are more influential in explaining cross-country variations in financial sector development than legal origins and that countries with unfavorable geographical endowments are likely to have less advanced financial sectors.

The theory of Law and Finance, introduced by La Porta et al. (1998), posits that a country’s legal framework, particularly its financial sector laws, is a significant determinant of financial sector development. The theory has two main components. Firstly, it suggests that countries with robust legal systems tend to experience higher levels of financial sector development. Secondly, it identifies legal traditions as the underlying factor for differences in financial sector development across countries. The theory further assumes that legal systems reduce transaction costs, enforce contracts, and secure property rights, which are crucial for the operation of financial markets (Beck and Levine, 2008; La Porta et al., 1998). The theory also distinguishes between legal origins, such as common law, civil law, and Scandinavian law, and their implications for financial regulation and innovation (Boughanmi & Nigam, 2022). Consistent with this theory, Djankov et al. (2007) argue that civil law countries have less bureaucracy and corruption, greater government credibility, and more advanced financial sectors. However, a more recent study by Fowowe (2014) fails to find support for this theory in the context of certain African countries.

The Financial Liberalization Theory is based on the ideas presented by McKinnon (2010) and Shaw (1973), which suggest that a country’s financial sector develops when the government reduces control. The theory proposes that domestic savings and access to investment funds increase when the interest rate is moderately high and positive. According to this theory, financial repression results in market disequilibrium, limiting allocative efficiency due to credit controls and restricted access to external finance. Baltagi et al. (2009) also argue that a country’s financial sector grows even faster if financial liberalization is accompanied by greater trade and financial openness.

The Growth-Led Hypothesis is based on Robinson’s (1952) argument that economic expansion drives demand for financial services. The theory proposes that increasing living standards are essential for achieving greater financial inclusion and development. Empirical studies, such as Liang and Jian-Zhou (2006), have greatly enhanced this theory by providing supporting evidence. In developing or emerging economies, sustained economic growth can promote financial sector activity, profitability, and development. Aluko and Ibrahim (2020) found that financial development spurs economic growth. However, the growth-enhancing effect is disproportionate, given the level of institutional quality. More specifically, financial development does not significantly promote economic growth when the International Country Risk Guide (ICRG)-based measure of institutions is used as the threshold variable below the optimal level of institutional quality.

Literature Review

Legal systems and the protection of property rights are underdeveloped in Sub-Saharan Africa, which has hampered the region’s development. Additionally, the poor legal frameworks have bred an atmosphere of unpredictability and ambiguity, making it challenging for businesses to make long-term investment decisions. According to Asongu and Nwachukwu (2017), this uncertainty has also increased transaction costs and decreased the effectiveness of the financial system.

Similar, insecure property rights have resulted from inadequate property rights protection, making it challenging for people and businesses to use property as collateral for loans. For people and businesses, especially those operating in the informal sector, this has lowered access to financing. Foreign investment has also been deterred by insecure property rights since investors are hesitant to make investments in countries where their property rights are not safeguarded (Doss et al., 2018).

Strong institutions are essential in fostering economic growth through financial development, according to Law et al. (2018). Effective institutional frameworks and regulations enhance financial systems’ efficacy in mobilizing savings, allocating resources, and promoting investment. This, in turn, leads to increased productivity, employment, and economic growth. The authors argue that a well-functioning financial sector requires a stable and predictable legal system, robust property rights, and efficient contract enforcement mechanisms, which strong institutions provide. Institutions help to reduce information asymmetry, monitor and control moral hazard, and mitigate adverse selection, which are inherent risks in the financial sector. The results suggest that countries with weaker institutional frameworks may face significant barriers to financial sector development, which, in turn, hinder their economic growth prospects.

Aluko and Ibrahim (2020) and Salifu et al. (2024) found that financial development spurs economic growth. However, the growth-enhancing effect is disproportionate, given the level of institutional quality. More specifically, when the threshold variable is set below the optimum level of institutional quality, financial development does not significantly contribute to economic growth (Aluko and Ajayi, 2018). This is based on the International Country Risk Guide (ICRG)-based measure of institutions.

According to Khan et al. (2020) the effectiveness of legal institutions affects how well financial systems reallocate capital among various businesses in a country. This is due to the crucial role that legal institutions play in creating a stable and predictable regulatory framework, which is necessary for the effective operation of financial markets. When legal institutions are functioning well, they aid in the growth of financial markets, encourage openness, and guarantee the upholding of the law. As a result, investors are better able to allocate capital across the numerous businesses that make up an economy since they have access to fast and accurate information.

Strong institutional frameworks, according to Aluko and Azeez (2019) and Aluko and Ajay (2018), are essential for fostering financial development in African nations. They argued that strong legal and regulatory frameworks, paired with efficient supervision and oversight, may improve trust and confidence in the financial sector, draw investment, and promote financial innovation. The authors also emphasized the role of political stability and the rule of law in promoting financial development. They argued that a stable political environment and an independent judiciary can help to ensure that contracts are enforced, property rights are protected, and disputes are resolved fairly and efficiently. This, in turn, can help to reduce transaction costs and increase the availability of credit and other financial services.

According to Khan et al. (2020) and Batuo et al. (2018), improved institutions are critical for financial development. Specifically, political stability, the fight against corruption, and high-quality regulations all have a favorable impact on financial development. Financial development is negatively impacted by the rule of law, indicating how weak the rule of law is in the majority of the world’s nations. The financial development of developing and global panels is positively impacted by the control of corruption index, indicating that most countries have successfully eliminated corruption to a low degree. The same study also discovered a decrease in corruption in rising nations, however other institutional markers were deemed negligible. Overall, the findings point to the importance of high-quality institutions as the primary forces behind and promoters of financial development.

In a study of East Asian nations, Feng and Yu (2021) discover that institutional elements related to law and politics have a greater influence on financial development than institutional aspects related to economics in East Asia. Financial development can be aided by improvements in institutional quality, including corporate freedom, fiscal independence, government efficacy, corruption control, rule of law, and regulatory quality. Enhancements to these establishments can help businesses better distribute resources and fortify their operations, which can lower expenses and provide a more equitable and productive financial operating environment.

Khan et al. (2020) investigates the impact of institutional quality on the financial development of 15 emerging and growth-leading economies. Their findings demonstrate that ethnic fragmentation may be effectively managed by an institutional framework, which can also serve as a catalyst for improved financial development.

Andrieş et al. (2023) use a dataset that spans 34 Organisation for Economic Co-operation and Development (OECD) member nations from 1995 to 2019 to evaluate the impact of institutional investors on financial development. Their findings imply that the financial system as a whole benefit from the growing number of institutional investors, particularly investment funds. They expand on their study by looking at the key elements of financial development and find that, while the influence on financial markets is determined to be statistically insignificant, it manifests primarily for financial institutions. As a result, institutional investors can facilitate better access to financial services and long-term investments.

Using a trivariate panel cointegration methodology, Singh et al. (2023) examine how financial deepening affects economic volatility for Sub-Saharan African (SSA) nations between 1982 and 2019. According to the study, there is a long-term correlation between financial deepening indices and economic instability. When financial deepening is reflected by wide money, panel parameter estimations by Fully Modified OLS, Pooled Mean Group, and Dynamic OLS (ordinary least square) imply that broad money positively effects economic volatility. However, there is a detrimental effect when domestic credit is used as a stand-in for financial deepening. Therefore, broad money promotes economic instability whereas local credit helps to reduce it. In addition, the estimators show that, for SSA countries, broad money has a larger correlation with economic volatility than domestic credit.

The dynamics of financial deepening and the business cycle volatility in the United Arab Emirates (UAE) are examined by Abosedra et al. (2023). Their results point to the existence of asymmetry between growth volatility and financial deepening, as well as regime shifts in the cointegrating connection. Additionally, the study shows that there are notable variations in how the business cycle reacts to either positive or negative shifts in the financial deepening, with the latter being more noticeable in the short term. As a result, the found imbalance implies that changes in the UAE’s financial system are greeted with swift and unfavorable responses from the business cycle.

Sanga and Aziakpono (2022) examine the influence of institutional factors on financial deepening and its consequences for bank credit in Africa. The findings demonstrate that political stability, voice and accountability, government efficacy, rule of law, and the ability to combat corruption all have a substantial impact on Africa’s financial development. On the other hand, other variables have a greater impact on low-income countries, but government effectiveness has a greater impact on middle- and high-income countries. In comparison to countries with lower degrees of financial depth, all institutional variables had larger effects—nearly twice as strong—at higher levels. Financial deepening is more affected by government efficacy and regulatory quality in nation-states with robust institutions than in those with weaker ones (Ibrahim and Alagidede, 2018; Khan, 2022; Law and Azman-Saini, 2012).

The study therefore tests the following hypotheses.

H1: Legal systems and Property rights enforcement positively affect financial development

H2: Legal systems and Property rights enforcement positively affect financial market development

H3: Legal systems and Property rights enforcement positively affect financial institutions development

Research Gap Analysis

This study contributes to the law-finance nexus methodology by accounting for the cross-equation correlations and linkages between financial markets and institutions, which has been missing in most methodologies by assuming that financial markets and institutions bear no relationship and, for that matter, are independent.

Methodology and Data

Data

This study relies on a panel dataset of 41 sub-Saharan African countries from 2000 to 2020. Out of a total of 49 SSA countries, we chose 41 countries. The choice of these countries was due to the availability of data. Data on the Financial Development Index is sourced from the World Bank Global financial database. Legal systems and property rights, final government consumption, sound money, and regulatory barriers are sourced from the economic freedom database of the Fraiser Institute. Data on the gross domestic product, inflation, trade, and foreign direct investment, are sourced from the World Bank Development Indicators database. The study aims to add new dimensions to the literature on the effect of legal systems and property rights on financial markets, financial institutions, and financial development.

Empirical Model

Following the works of Chinode and Kwenda (2019) who showed that financial inclusion is dependent on institutions and economic factors and assuming financial development, financial markets, and financial institutions are a function of legal systems and property rights enforcement, and other variables; we could specify the function as

Where

In Equation 1, we specify that financial development, financial markets, and financial institutions are dependent variables denoted by

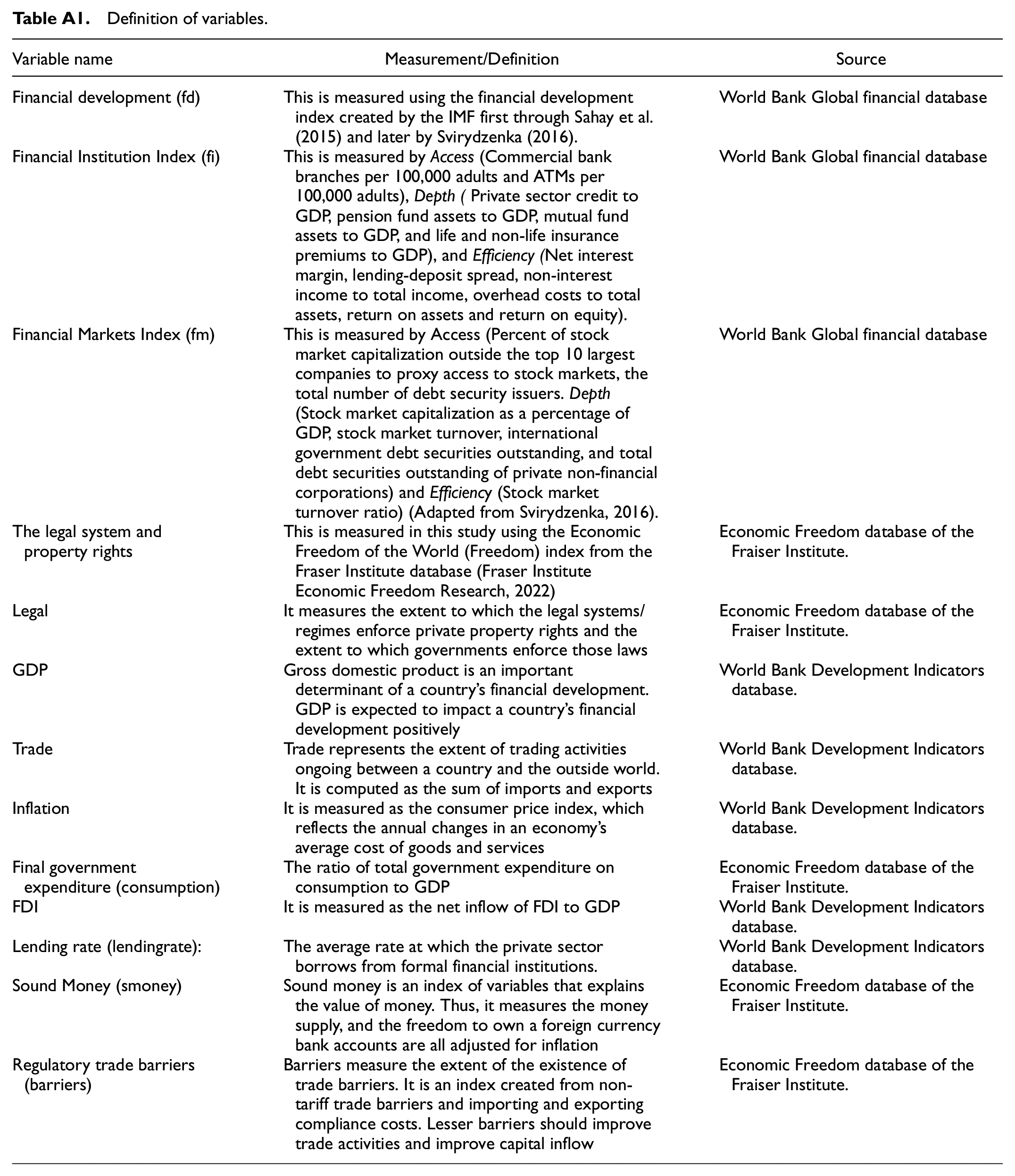

The definitions, measurement and sources of data is contained in Table A1 in Appendix A.

Diagnostics

There are two recommended tests for instrument validity when implementing the GMM model: Hansen’s (1982) J test and Sargan’s (1983) test of over-identification restrictions. Most of the time, the Hansen test is used for the test of instrument validity—the second diagnostic check tests for autocorrelation or serial correlation of the error term. Failure to reject the null hypothesis of no second-order serial correlation means that the original error term is serially uncorrelated, and the moment conditions are correctly specified. Thus, the values of

Results and Discussions

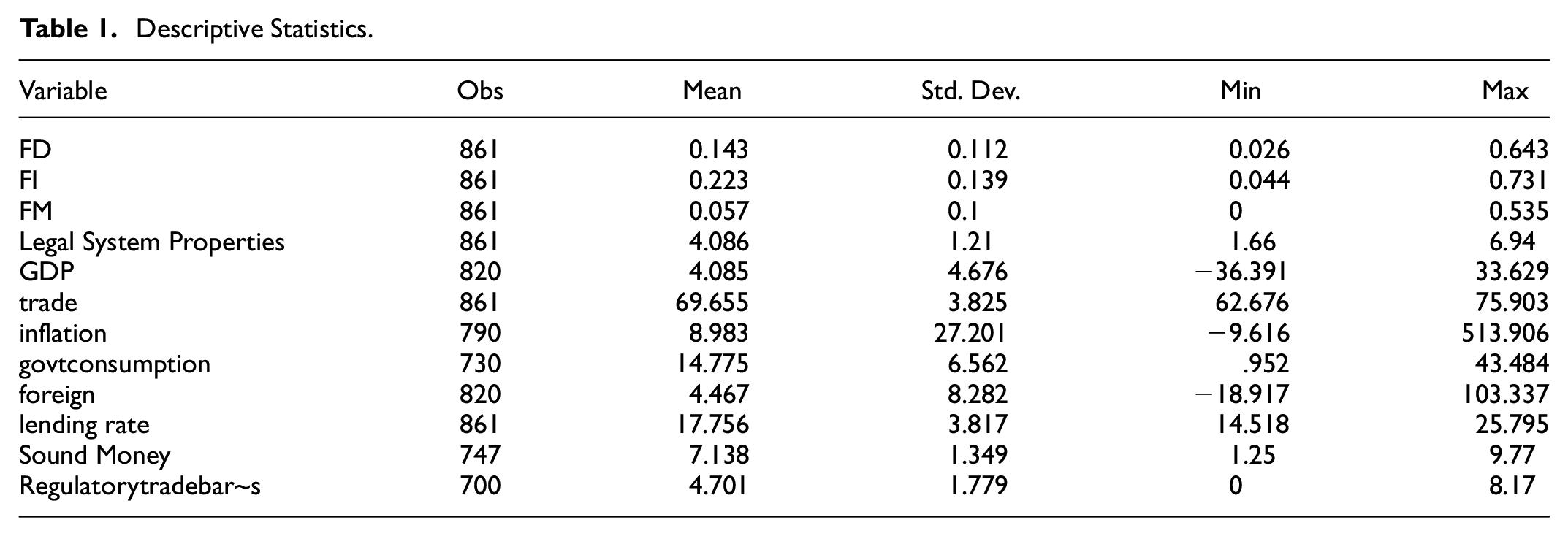

Descriptive Statistics of Variables

Table 1 gives an overview of the summary of the variables used in the study. Financial development has a mean value of 0.143. Given the range of computed values for the level of financial development, it implies that the level of financial development in Sub-Saharan African countries is relatively low. While some countries have a maximum level of financial development at 0.643, others have a level of financial development as low as 0.026. The level of development of financial institutions also has a mean value of 0.223. While some have a maximum level of financial institutions development of about 0.731, others have a minimum of about 0.044.

Descriptive Statistics.

Financial market development has a mean value of 0.057, a maximum value of 0.535, and a minimum value of 0. The data reveals similarities between the development of financial institutions and the financial sector.

Legal systems and property rights have a mean value of about 4.086. Overall, in sub-Saharan Africa, Legal systems and property rights enforcement are relatively low. While some countries in sub-Saharan Africa have a development score of about 6.94, others have a score as low as 1.66. The level of trade activity is considerably high in the SSA region, with a mean value of about 69.655. While some countries have a maximum percentage of about 76, others have a minimum of about 63%. Regulatory barriers measure the level of regulations and restrictions of trade capital movements. The mean score of regulatory barriers in sub-Saharan Africa is 4.7. While some countries have a high regulatory score of about 8.17, others have a very low regulatory score of zero.

The Correlation Coefficient of Variables

The result of the pairwise correlation indicates a moderate and positive correlation between legal systems and property rights enforcement on the level of financial development, financial markets development, and development of financial institutions, respectively. As indicated in Table 2, the correlation coefficients between legal systems and property rights enforcement and level of financial development, financial markets development, and development of financial institutions are 0.659, 0.678, and 0.509, respectively, and statistically significant.

Correlations Analysis.

p < .01. **p < .05. *p < .1.

Legal Systems, Property Rights, and Financial Development

Table 3 shows the results of the GMM estimates of the effect of legal systems and property rights on financial development as a whole, as well as the development of financial markets and institutions, as indicated in models 1, 2, and 3 of Table 3. The unobservable heterogeneities among the study’s participating countries are not taken into account by OLS results. The dependent and complex nature of property rights and legal institutions across economies requires our analysis to account for such heterogeneities and unobservable factors. In all models, the research takes other macroeconomic factors into account that could influence financial institutions, financial market development, and overall financial development. These include the log of GDP, trade, inflation, government consumption, foreign investment, lending rate, Sound money, and Regulatory barriers. The study uses the first lags of the independent variables as instruments (Arellano and Bover, 1995). Hansen J test reported for all models indicates that the instruments used in the models are valid, and a significant AR statistic reported indicated the absence of serial correlation in the models, respectively (Hansen, 1982).

Two-Step System GMM Estimates of Legal System and Property Rights on FD, FM, and FI.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .010.

Financial Development

The lag of financial development has a significant positive effect on the current level of financial development. As indicated by Chinn and Ito (2006), previous levels of financial development should significantly affect the current level of financial development. Positive lagged coefficients imply that financially developed countries are projected to show higher growth in financial development. The results indicate that a percentage increase in past values of financial development will increase the current level of financial development by about 0.689%.

The results indicate that legal systems and property rights have a significant positive relationship with financial development. The results suggest that increasing the score of legal systems and property rights enforcement by one basis point will increase financial development by about 0.04. Effective legal systems, coupled with effective enforcement of property rights, could improve asset allocations, affecting growth in sectorial values and improving access to finance. The finance and law theory argues that in economies where the legal system enforces property rights, supports private contract arrangements, and protects the legal right of investors, holders of funds are willing to save their funds, and finance firms, and therefore financial markets would flourish. This result is consistent with Levine (2002), Wurgler (2000), and Duba (2022), who explain how legal institutions could affect how effectively financial systems redistributed capital among the various sectors in a country.

Similarly, legal systems and property rights enforcement have a significant positive relationship with the development of financial markets. The results indicate that lagged values of financial market development positively affect the current values. A percentage increase in the previous value could lead to a 0.805% increase in the current level of financial market development. As indicated in column 2 of Table 3, the result implies that an increase in legal systems and property rights enforcement by one basis point will increase financial development by about 0.01. Developing legal systems and property rights can propel the development of financial markets in sub-Saharan Africa. The legal system should make sure that contracts and property rights are sufficiently clear and predictable so that the independence of the court, its perception, the effectiveness of its judgment, and the enforcement of the court’s decision are essential features whose deformation has a direct impact on the operation of the financial system.

Khan et al. (2020) argues that financial markets tend to flourish when the legal systems effectively enforce property rights and there is the existence of the rule of law, which the government effectively enforces. Effective legal systems are essential ingredients for competitive markets. This could explain why the US financial markets tend to be competitive and attractive over other financial markets across the globe. Their financial markets are characterized by greater standardization of legal systems and norms. Without a proper legal system, it becomes harder to trade in almost any financial instrument. In other words, an inefficient legal system may lead businesses to move elsewhere.

As indicated in column 3 of Table 3, legal systems and the enforcement of property rights have a positive and significant effect on the development of financial institutions. Like the financial markets model in column 2, a basis increase in the level of legal systems and the enforcement of property rights is expected to increase the development of financial institutions by about 0.02. the results confirm an a priori expectation of a positive relationship between legal systems and property rights enforcement and the development of financial institutions. The lagged values of the development of financial institutions also have a significant positive relationship with the current level of development of financial institutions. A percentage increase in past values will result in a 0.881% increase in financial institutions’ development level.

The estimates in Table 3 indicate that the log of the gross domestic product has a significant positive effect on both financial development and financial markets development but has no significant impact on the development of financial institutions in sub-Saharan Africa. A percent increase in the gross domestic product will increase financial development and the development of financial markets by 0.00970 and 0.0139, respectively. This result is consistent with the finance growth theory. Countries with higher GDP levels will allow for greater economies of scale in financial services provision, promoting supply-side financial development.

The log of inflation significantly negatively affects the development of financial institutions and markets and the overall financial sector development in SSA. A percentage increase in the inflation rate will induce a negative rate of change in financial development and the development of financial institutions, respectively, as indicated in Table 3. Inflationary periods tend to lead to uncertainty in the investment environment since they erode the value of money. It is, therefore, the case that inflation represses investment in financial instruments and noninvolvement in financial markets. As Mahyar (2017) and Salifu et al. (2024) indicated, inflation raises the risk of investment because of market uncertainty and erodes the value of investments, repressing financial development.

The level of trade regulatory barriers significantly negatively affects financial markets and overall financial development. Still, it has no significant effect on the development of financial institutions in SSA, as indicated in Table 3 (columns 1 and 2). This is consistent with apriori expectations of a negative relationship between financial development and regulatory trade barriers. In addition, stringent regulatory trade barriers reduce the ongoing trade activity between a country and the outside world. This leads to a decrease in capital inflows into an economy which could affect the growth of financial development and markets. The insignificant effect on financial institutions’ development could result from cross-border banking restrictions in sub-Saharan Africa because of a lack of infrastructure, regulatory obstacles, and other issues. As a result, financial institutions may be less significantly impacted by trade regulatory restrictions than in other regions with more advanced cross-border banking. Also, focusing on domestic markets rather than diversifying into global markets, many financial institutions in sub-Saharan Africa strongly emphasize serving their home markets. Because financial institutions may be less dependent on international trade in financial services, the impact of trade regulatory barriers on them may be minimal.

The average lending rate is also a significant determinant of financial development and the development of financial markets. A percentage increase in the average lending rate could lead to a 0.00154% and 0.0004% increase in the level of financial development and development of financial markets, respectively. As Lachman and Shaw (1974) argued, higher lending rates stimulate total and financial savings and thus lead to quality investment in the financial sector since higher interest rates rule out investments with low productivity. Therefore, resources are moved to more efficient accumulation of saving from less efficient forms of accumulation.

The level of government consumption has a significant negative effect on the level of financial market development (0.0007) and a significant positive effect on the development of financial institutions (0.001). The results also indicate that sound money significantly negatively affects the development of financial institutions (0.004) and the overall financial sector development (0.007). The plausible reason for such a result could be that an increase in money supply could lead to an increase in inflation, which could repress the level of financial development.

Results Diagnostics

As indicated in Table 4, the post-estimation diagnostic tests are consistent with the assumptions necessary for implementing a system Generalized Methods of Moments.

Diagnostics Test of SYS-GMM.

Robustness Checks

An alternative measure of financial development is used to ascertain the robustness of the empirical results above, which could be sensitive to different proxies, as seen with Demetriades and James (2011). An alternative measure of financial development is a credit to the private sector from the World Bank database, which equals financial intermediary credits to the private sector divided by the gross domestic product. The variable measures the claims on the private sector by financial intermediaries. Rajan and Zingales (1998), Levine et al. (2000), Beck (2002), Claessens and Laeven (2003), Beck et al. (2003), and Bekaert et al. (2005), among others, also use this measure as a proxy for financial development. The results of the dynamic panel SYS-GMM regressions are reported in Table 5. The results are invariant with the earlier results. Legal systems and property rights have a significant positive relationship with the financial development indicator (i.e., credit to the private sector). Thus, there is no significant variation as earlier results are robust irrespective of the proxy measures for financial development. Therefore, the results are generally robust.

Two-Step System GMM Regression of the Legal System and Property Rights with Credit to Private Sector.

The results, as indicated in Table 5, show that legal systems and property rights enforcement significantly and positively affect the level of financial development in sub-Saharan Africa. The results suggest that a percentage increase in the score of legal systems and the enforcement of property rights could result in a 0.0901% increase in financial development. The results in Table 5 are consistent with the results in Table 3 both in sign, and the magnitude of the effect is not wide off. The implication is that the measure of financial development does not matter for financial development. Well-enforced property rights and effective legal systems should positively affect financial development. It increases investor confidence in an economy, which could result in an inflow of capital from overseas, resulting in the larger capitalization of businesses. The effect of other control variables on financial development is also consistent with the results in Table 3.

Seemingly Unrelated Regression (SUR) was used to estimate the same models in order to confirm the consistency of the study’s findings. SUR can explain cross-equational connections and correlations between financial markets and financial institutions (Avery, 1977). These variables are simultaneously estimated and given the endogenous variable treatment. Equations 3 to 5 were therefore estimated simultaneously. Table 6 shows the findings in relation to the effect of legal systems and property rights on financial development. In fact, the data demonstrated that property rights and legal systems had positive effects on financial institutions, markets, and overall financial development. This correlates with the main GMM model’s findings. The analysis presented in this paper assumes that financial markets and institutions bear no relationship and are independent. However, financial markets and institutions are interlinked.

Legal Systems and Property Rights on Financial Development: SUR Model.

Note. Standard errors are in parentheses

p < .01, **p < .05, and *p < .1 refer to significant levels at 1%, 5%, and 10% respectively.

The estimation so far assumes no relationship between financial development, financial markets, and financial institutions. However, the reality is that these variables are linked and highly correlated (see correlation matrix Table 2). Financial development comprises both financial institutions and financial markets. On the other hand, financial institutions rely on financial markets for capital mobilization while contributing to the development of the financial market through listing on the stock market. Hence, there is a need to employ a model capable of accounting for the interdependence among these variables. Therefore, for further robustness check, the study uses the SUR model to account for the interdependence among these variables.

According to a study by Akinlo and Egbetunde (2016), financial institutions such as banks and microfinance institutions play a crucial role in promoting economic growth and development in sub-Saharan Africa by mobilizing savings and allocating credit to various economic sectors. These institutions often rely on financial markets to raise funds and manage their liquidity.

Similarly, Agyei-Boapeah and Ansah-Adu (2018) argue that the development of financial markets in sub-Saharan Africa can significantly impact financial institutions’ performance. For example, a well-developed bond market can provide banks with an alternative funding source, reducing their reliance on deposits and improving their liquidity and stability.

However, the degree of interlinkage between financial institutions and financial markets varies across countries and regions in sub-Saharan Africa. According to Beck et al. (2000), a country’s financial market development level can affect the degree to which financial institutions rely on financial markets for funding and liquidity.

Overall, sub-Saharan African financial institutions and financial markets are interlinked, and their development is mutually reinforcing. The extent of this interlinkage depends on the level of financial market development and the regulatory environment.

Conclusions

The study examined the effect of legal systems and property rights enforcement on the level of financial markets and institutions and the overall financial development in SSA using data from 2000 to 2020 for 41 countries. The motivation for this research stemmed from the inconclusive results in the empirical literature regarding the impact of legal systems and property rights on financial development, as found across a diverse array of developed and developing nations. Also, the SUR model for robustness checks and to account for cross-equational linkages and correlations between financial markets and financial institutions, which had been overlooked in most previous studies. They contended that an analysis customized to a specific region, comprising countries with comparable economic fundamentals, cultural backgrounds, and historical contexts, was essential for deriving pertinent policy implications. Additionally, we emphasized the importance of linking Sub-Saharan Africa reforms with economic performance, focusing on enhancing both the financial sector and institutional capacity. In addition, the fact that the study is inspired by the available literature on the institution-finance nexus is still growing and very scanty in SSA.

The results show that legal systems and property rights enforcement positively affect financial markets, financial institutions, and overall financial sector development. Also, using credit to the private sector as a substitute indicator of financial development, a positive relationship was still found between legal systems and property rights enforcement on financial development. The study concludes that the effect of legal systems and property rights enforcement on financial development does not depend on the measure of financial development. Moreover, trade openness and GDP significantly positively affect the financial market dimension and overall financial development. We also observe that the lending rate positively influences the financial market dimension of financial development and the overall financial development index. Regulatory trade barriers significantly negatively affect financial markets and overall financial development.

Recommendations/Policy Implications

Following the empirical results, the study recommends that governments of SSA countries strengthen legal systems and ensure proper enforcement of property rights is a crucial step in promoting financial development in SSA. This includes establishing and enforcing clear laws and regulations that protect property rights and providing effective dispute resolution mechanisms to resolve conflicts. This will create a more predictable and stable environment for businesses and investors, encouraging them to invest in firms and financial markets. This could result in increased confidence in institutions and thus result in capital inflow and free flow of information into the sub-region, which could result in growth. Further, trade barriers should be less restrictive such that they could increase trade volumes and capital inflight into the region.

Governments of SSA countries should foster trade and support economic growth initiatives to drive financial markets development and the overall financial sector development. They should reduce trade barriers and eliminate any restrictions that may discourage foreign investment. In addition, governments need to work with international organizations and financial institutions to develop a comprehensive set of measures that accurately reflect the state of financial development and regularly adjust these measures to reflect changes in the financial sector and ensure they remain relevant.

Central Banks in SSA countries should use monetary policy to regulate lending rates, keeping them at a level that supports financial development and adjusting interest rates as necessary to maintain stability. Governments of SSA countries can also work with their commercial banks to encourage the provision of credit to small businesses, which are often seen as high-risk borrowers.

Finally, the government’s policy of SSA countries should focus on the financial sector and institutional development. Specifically, initiatives should prioritize enhancing institutions pertinent to the financial system to facilitate unrestricted information flow, enforce contract agreements, and protect property rights.

Limitation

Finally, the authors recommend a sub-sample analysis on the effect, institutions have on financial development which could be considered in future studies to understand the dynamics of the relationships. Further works could also consider the problem of “too much finance” using threshold models.

Footnotes

Appendix A

Definition of variables.

| Variable name | Measurement/Definition | Source |

|---|---|---|

| Financial development (fd) | This is measured using the financial development index created by the IMF first through Sahay et al. (2015) and later by Svirydzenka (2016). | World Bank Global financial database |

| Financial Institution Index (fi) | This is measured by Access (Commercial bank branches per 100,000 adults and ATMs per 100,000 adults), Depth ( Private sector credit to GDP, pension fund assets to GDP, mutual fund assets to GDP, and life and non-life insurance premiums to GDP), and Efficiency (Net interest margin, lending-deposit spread, non-interest income to total income, overhead costs to total assets, return on assets and return on equity). | World Bank Global financial database |

| Financial Markets Index (fm) | This is measured by Access (Percent of stock market capitalization outside the top 10 largest companies to proxy access to stock markets, the total number of debt security issuers. Depth (Stock market capitalization as a percentage of GDP, stock market turnover, international government debt securities outstanding, and total debt securities outstanding of private non-financial corporations) and Efficiency (Stock market turnover ratio) (Adapted from Svirydzenka, 2016). | World Bank Global financial database |

| The legal system and property rights | This is measured in this study using the Economic Freedom of the World (Freedom) index from the Fraser Institute database (Fraser Institute Economic Freedom Research, 2022) | Economic Freedom database of the Fraiser Institute. |

| Legal | It measures the extent to which the legal systems/regimes enforce private property rights and the extent to which governments enforce those laws | Economic Freedom database of the Fraiser Institute. |

| GDP | Gross domestic product is an important determinant of a country’s financial development. GDP is expected to impact a country’s financial development positively | World Bank Development Indicators database. |

| Trade | Trade represents the extent of trading activities ongoing between a country and the outside world. It is computed as the sum of imports and exports | World Bank Development Indicators database. |

| Inflation | It is measured as the consumer price index, which reflects the annual changes in an economy’s average cost of goods and services | World Bank Development Indicators database. |

| Final government expenditure (consumption) | The ratio of total government expenditure on consumption to GDP | Economic Freedom database of the Fraiser Institute. |

| FDI | It is measured as the net inflow of FDI to GDP | World Bank Development Indicators database. |

| Lending rate (lendingrate): | The average rate at which the private sector borrows from formal financial institutions. | World Bank Development Indicators database. |

| Sound Money (smoney) | Sound money is an index of variables that explains the value of money. Thus, it measures the money supply, and the freedom to own a foreign currency bank accounts are all adjusted for inflation | Economic Freedom database of the Fraiser Institute. |

| Regulatory trade barriers (barriers) | Barriers measure the extent of the existence of trade barriers. It is an index created from non-tariff trade barriers and importing and exporting compliance costs. Lesser barriers should improve trade activities and improve capital inflow | Economic Freedom database of the Fraiser Institute. |

Acknowledgements

The paper was presented at the 5th International Research Conference of the College of Humanities, University of Ghana on 13 – 15 October 2022 at Cedi Conference Center, University of Ghana, Accra, Ghana. The authors appreciate the organizers and the comments of participants which we utilized in revising the paper. Any other errors remain the author’s responsibility.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

This is not applicable.

Data Availability

The data is available upon request from the corresponding author.