Abstract

International tourist flow positively affects human capital development and innovation at country and regional levels. This study examines how a country’s international tourist flow affects startup financing based on the “investment scope” and “market potential” perspectives. Analyzing the firm-country-year sample from 1995 to 2014 and the country-year tourism datasets, we find that startups engage in larger venture capital investment deals in countries attracting more international tourists and earning higher tourism revenue. The effect is more substantial for either venture capital-funded or high-technology startups, supporting that international tourist flow can increase the investment scope available to potential investors, specifically in the markets connected to tourism expenditures. Our findings contribute to the literature on the relationship between tourism and economic growth and practitioners and policymakers in the tourism and innovation sectors.

Keywords

Introduction

Global tourism has been proliferating, both in the number of tourists and in added value (Belloumi, 2010). This sector generates diverse direct and indirect economic impacts at national, provincial, and community levels. For example, tourism growth aids industry development (Pablo-Romero & Molina, 2013). According to a recent United Nations report, developing countries account for 40% of world tourism arrivals and 30% of tourism receipts (UNWTO, 2019). Given that tourism is one of the five top export earners in over 150 countries (Scott & Gössling, 2015), this money has fueled industrial upgrades in many emerging markets, attracting new private investment in a virtuous cycle.

Previous literature found an important relationship between international tourist flow and economic growth in the destinations. Recently, a strand of pioneering literature has examined the positive effects of international tourist flow on human capital development and innovation at country and regional levels (Croes et al., 2021; Liu & Nijkamp, 2019). However, the question of how international travel influences investment in local startups remains unexplored. This linkage is important for two reasons. First, encouraging startups and venture capital constitutes a novel and real effect of tourism. Second, the inclusive and sustainable tourism feature has crucial implications for policymakers attempting to motivate the innovation and investment areas. Therefore, in the study, we investigate the potential effect of tourist flow on financing activities from a firm-level perspective. Specifically, we propose the two potential underlying mechanisms, whether the “investment scope” or “market potential” channel drives the main result.

For examining the research question and mechanisms, we constructed the firm-country-year sample spans from 1995 to 2014. It combines two datasets: a firm-year dataset constructed from Crunchbase, which is the leading destination for company funding insights from early-stage startups to the Fortune 1,000 worldwide, and a country-year dataset sourced from World Tourism Organization (UNWTO), which systematically gathers the most comprehensive statistical information available on the tourism sector across the globe. To mitigate endogeneity concerns, we employ a two-stage least square (2SLS) estimation as our main empirical model, with football matches and heritage sites instrumenting our tourism measure (Henderson et al., 2010; Su & Lin, 2014). The main findings show that startups registered in countries with more flourishing tourism will obtain higher capital injection. On the one hand, tourism can indeed increase the scope of investment available to potential investors in a company’s early development stage. On the other hand, we also observe a more prominent impact of tourism on startup investment in sectors connected to tourism expenditures, such as the high technology consumer goods sector. The finding stays robust with alternative constructs of tourist and funding proxies and different cross-section and time-series subsamples.

Our study contributes to the extant literature on the relationship between tourism and economic growth. On the one hand, this paper is among the first studies examining the impact of international tourism flow and expenditures on startup financing. On the other hand, we propose a novel mechanism through which travelers’ information flow can promote idea spillover for potential entrepreneurs. Our findings also contribute to practitioners and policymakers in the tourism and innovation sectors by providing practical and policy implications on the socio-economic effects of international tourism.

Related Work

The important connection between tourism and economic growth is well developed in the literature, indicating that the expansion of tourism activities can influence the economic and socio-cultural development of society (Cárdenas-García et al., 2015). Early literature on the topic has investigated the relationship between tourism and growth from the perspective of the tourism-led growth hypothesis (Balaguer & Cantavella-Jordá, 2002). From this perspective, the core question is whether tourism growth creates equivalent economic growth and, if so, to what extent, or, conversely, whether economic expansion strongly contributes to tourism growth (Brida et al., 2016). For example, a meta-regression analysis based on 113 studies supports the statistically positive effects of tourism activities on economic growth in a country or a region, while the effects are sensitive to different factors that are relevant to country characteristics and tourism specialization (Nunkoo et al., 2020). The positive effect of tourism specialization on growth is dependent on the recipient economy’s level of economic development and finance system absorptive capacity (De Vita & Kyaw, 2017). These findings highlight the need for more consistent tourism development plans and strategies to be executed by governmental bodies at the national and regional levels (Surugiu & Surugiu, 2013).

A strand of literature focuses on the positive effects of inbound tourism flows on human capital development and innovation in the tourism destination areas (Croes et al., 2021; Liu & Nijkamp, 2019). The literature suggests that inbound tourism could be a new and significant driver of national and regional innovation, both in technological and social aspects (Rehman et al., 2020). Inbound tourism may improve the regional innovation network by attracting more institutions and resources, thus expanding the regional innovation network and bringing in more resources for innovation (Liu & Nijkamp, 2019). As inbound tourism grows, it creates a more dynamic and diverse demand system, which encourages greater entrepreneurial and commercial innovation. For example, entrepreneurial activity and the creation of new firms in the tourism and hospitality sectors may propel economies forward (Tleuberdinova et al., 2021). Relatedly, previous studies also show that tourism can alter individual thoughts regarding having new business plans (Richards, 2011; Richards & Wilson, 2006) and making consumption decisions (Walters et al., 2012; Woodside & Dubelaar, 2002).

Our study aims to extend this body of literature on the effects of inbound tourism flows on the human capital development and innovation in the tourism destination areas by examining how international inbound tourism influences investment in a broader scope of local startups.

Theoretical Framework

Startup financing and tourism are two central concepts in separate parts of the literature. For startup financing, our focus is angel investment and venture capital. They care more about the prospects of a target company and, more importantly, how the capital is allocated will determine incentives for innovation in both technology advancement (Groh & Wallmeroth, 2016; Jeng & Wells, 2000) and organizational development (Jin et al., 2020). Regarding tourism, its development also matters in the business domain as it can broaden a pioneer’s mindset by promoting knowledge spillovers (Hjalager, 2010; Richards, 2011). Small and medium-sized businesses, in particular, benefit greatly from inbound tourism development when it comes to generating business prospects (Saha et al., 2017). The destination will develop as an attractive pole that gathers a variety of services and information, in addition to the diversity driven by inbound tourism development (Ottaviano & Peri, 2006). More entrepreneurship and innovation are attracted to these areas on a regular basis (Salamzadeh & Kawamorita Kesim, 2017). As a result, in an area that benefits more from international tourism development, creative and innovative activities can obtain more recognition, encouraging more entrepreneurship. Taken together, entrepreneurs and their potential investors need to understand tourism’s role in the startup ecosystem. The tourism sector contributes to economic activities, market potential, and creative spirit. We posit that a country’s tourism growth can better help domestic firms accomplish their early-stage financing goals. Tourist flow could enhance startup financing through the following two possible channels.

First, tourists learn novel technology and hatch fresh ideas during their journey. Hence, entrepreneurs are more motivated to start a new business. This tendency may enlarge the investable universe for angel investors and venture capitalists. Williams (2011) suggests that more than 78% of surveyed startups across 10 famous cities consider networking, including connections acquired during trips, to play a vital part in their entrepreneurial success. Investors’ preferences of having more options for building up their portfolio of companies can be satisfied with an increased variety and number of startups. We name it the “investment scope” channel. The tourism sector’s growth facilitates potential entrepreneurs to discover new business opportunities and form new business ideas through traveling. For example, a trip around the world or a discussion with foreign travelers will broaden people’s views and bring out insights, increasing the likelihood of starting their business (Johns & Mattsson, 2005; Mshenga et al., 2010). It further expands the universe of startups from which venture capitalists can choose. Venture capital funds hold a much broader portfolio of target companies than angel investors (Fairchild, 2011). We expect to see a more substantial impact of tourism on venture-stage funding.

Second, a large body of research has documented that the tourism domain exerts a demand-pull effect in various industries, such as infrastructure, transportation, technology, and retail (e.g., Duan et al., 2020; Fainstein et al., 2003; Hjalager, 2010). The effect eventually increases the market potential of companies operating in the relevant markets. Because more favorable forecasting of the target market can improve startup evaluation, it would help entrepreneurs persuade potential investors and obtain a better investment deal. A more substantial profit projection can induce investors to invest more funds in the startup. We label this as the “market potential” channel. The effect of tourism on investment decisions varies with investors’ forecasts of the market potential of a startup. If the tourists’ propensity to consume drives our results, then the effect is expected to be stronger when investors consider investing in startups that are more closely related to tourism businesses. In other words, investors are more likely to invest in those firms that either sell final products and services to tourists or sell intermediates to companies operating in the tourism sector. This is because these investment target companies have greater growth prospects.

If the “investment scope” mechanism holds, then the effect of tourism growth on startup investment would be more substantial either in the sample of pure venture-funded firms or when tourism activities are much less important than entrepreneurial activities in a given country. The reasons are that venture capitalists value portfolio diversification more than angel investors and that the marginal increase of scope is sizable in countries with relatively underdeveloped tourism. On the other hand, if the “market potential” mechanism holds, we should observe a more prominent impact of tourism on startup investment in highly influenced tourism expenditures.

Empirical Setting

For tracking startups’ financing activities, we use a Crunchbase dataset collecting funding received by 22,982 startups in 108 countries over the period 1995 to 2014. After merging these data with data on tourist proxies and additional controls, we obtain a base sample of 20,475 startups (they are spread over 53 countries, though most of them are located in the US) based on the criterion that each firm in this base sample closes its series of investment deals within 1 year. The original Crunchbase data consist of firms with funding years spanning from 1921 to 2014. In this original database, there are 49,438 startups sourced from 110 countries or regions. As our tourism dataset starts from 1995, we restrict our sample period to 1995 to 2014. After removing observations with missing funding amount and home country, we have 37,062 startup companies left, out of which 14,080 have a period of funding lasting more than 1 year. If we continue to remove them and merge them with a list of controls, a final collection of 22,982 startups is obtained (when dropping missing values, we have 20,475 firms). The sample in which startups receive a series of funding over more than a year will be studied in the robustness section. The reason we make such a distinction is that the information on the annual amount of funds received by those firms is not disclosed. So, they cannot be treated in a way consistent with other firms that had finished all pre-IPO funding rounds within a single year. To understand the criteria, think of a sample startup that receives two venture capital investments. The first investment occurs in year 1, whereas the second may either follow up closely within a year or come later in year 3. Hence, uneven intervals between different rounds of investments bring in difficulties when we match annual tourism data to the 14,080 firms with intervals greater than 1 year (up to a maximum of 19 years). Nevertheless, we include them in a separate sample to study their case as a robustness check.

As for the dependent variable, our primary measure LN_funding is the natural logarithm of the total amount invested in a startup during its funding year. This amount can be further decomposed into two parts: LN_angel_funding and LN_venture_funding. Besides capital investment made by angel investors, we also include money raised via equity and product crowdfunding campaigns in angel-stage funding. The venture funding here consists of funds injected by both early-stage seed investors and late-stage venture capitalists. To get a sense of the magnitude of financing, a typical startup in our base sample will receive approximately 1 million US dollars from early-stage investors on average across countries. In addition to the level proxies, we construct three ratio proxies by dividing these funding levels over their respective averages. They are obtained by averaging across all firms receiving the same type of investment with the startup in consideration in the same year. We obtain the following three alternatives: Rate_funding, Rate_angel_funding, and Rate_venture_funding. What is more, for each sample year, we utilize a country-level proxy LN_firm_number to represent the total number of funded startups originating from a given country.

Regarding our main variable of interest, we construct LN_tourist, which equals the annual number of tourist departures and arrivals for a country in our sample data. There are as many as 20 million visitors per year averaged over time and across countries. Again, as this proxy is in natural logarithmic form, we calculate its corresponding ratio proxy Rate_tourist by expressing this tourist number as a percentage of the average number worldwide. Our alternative variable of interest is the natural logarithm of the country’s outbound travelers’ annual money plus the annual income earned in the country’s tourism sector. The sample mean of these expenditures exceeds 20 billion US dollars. At the firm-level sample, where country-level tourist numbers and expenditure may be counted multiple times, these two averages can go up as high as 80 million persons and 170 billion dollars. The primary and secondary measures for our variable of interest are taken directly from the World Bank’s World Development Indicators (WBWDI) computed from UNWTO statistics.

Figure 1 illustrates a crude co-movement between the above two dependent and independent variables. Since tourist numbers are already country-level variables, we take the average across all sample countries each year and plot it as a line. The funding variables are obtained by aggregating firm-level funds to the country-level and then by averaging across each country’s aggregated funding. They are plotted as bar charts for the tourism sector, high technology sector, and other sectors.

Tourist flow and sectoral startup funding.

For constructing control variables, following Islam et al. (2018) and Sakai et al. (2010), who studied the determinants of venture funding, we first incorporate two important firm characteristics: the Age of a startup firm, which is defined as the funding year minus the founding year; and a dummy variable, Survivorship, which equates to 1 if a startup firm has either been active or been acquired at the time of inspection; the value is 0 if it no longer operates. It merits a note that our way of defining firm age may have occasionally negative one if a firm receives funding prior to its formal legal establishment. Then, we continue to incorporate several macroeconomic indicators at a country level (Groh & Wallmeroth, 2016; Jeng & Wells, 2000), such as the GDP growth rate, GDPGR; the stock market capitalization of all public listed domestic companies, MarketCap; the total tax revenue collected, Tax; the value of exported goods and services, Export; and the composite index, EF, on institutional quality reported by the Economic Freedom of the World. Among these, GDPGR, MarketCap, and Tax are all normalized by dividing by GDP. Whereas the GDP growth rate should positively impact funding, a larger size of the public equity financing market may suppress pre-IPO funding due to substitution effects. Tax revenue can either increase a young firm’s cost or encourage the government to raise subsidies; hence, its effect is ambiguous. Firm age and operating status are obtained from the Crunchbase database, and the macroeconomic variables are sourced from the WBWDI database.

Table 1 lists the definitions, data source, and descriptive statistics for a complete range of variables used in this article at the firm-year observation level. Table 2 presents a pairwise correlation matrix table, providing a preliminary but significant confirmation of our concerned relationship between tourist flow and venture capital investment.

Firm-level Sample Summary Statistics.

Correlation Matrix.

Note. *** and ** denote significance at the 1% and 5% level, respectively.

Model Specification

Following the literature on the factors influencing venture investment decisions (e.g., Islam et al., 2018; Jeng & Wells, 2000), and focusing on the treatment of potential endogeneity due to reverse causality, we run equations (1) and (2) sequentially under a 2SLS framework. The aim is to identify the causal effect of international tourism development on the amount of capital raised by domestic startups.

Fundingit is a measure of capital received by startup i in its home country during its funding year t, equaling to either LN_fundingit or Rate_fundingit; Touristit is a measure of tourist outcome (LN_touristit, Rate_touristit, or LN_expenseit) in the same year t for that same country in which startup i is registered to; Est_Touristit is the forecasted value of Touristit after estimating the first-stage regression;

As for the instrument variables (IV), we employ the number of Football matches and the number of Heritage sites in the startup home country to instrument the part of tourism arrival and revenue remote from firm financing. Particularly, hosting international sports events frequently and having more places included in the World Heritage List have been proven to attract foreign tourists to visit a country (Henderson et al., 2010; Su & Lin, 2014), let alone the fact that citizens living in such a country will be cultivated with the traveling spirit. Moreover, these two IVs are more likely to be determined by non-financial cultural factors, which are less directly related to risky investment activities. Information on football matches is taken from the International Federation of Association Football’s official website, and the heritage site data are distributed by the United Nations Educational, Scientific, and Cultural Organization.

Because our base sample resembles an event database consisting of firm-country-year observations, instead of regressing equation (2) in the second stage of twoSLS, we implement the below equation (3) with additional time-invariant determinants

To further examine cross-border tourism’s mechanism affecting startup funding, we add two interaction terms in equation (2) to construct equation (3). In these two interactions, Hi-Techit is a dummy indicating whether the startup firm i with a funding year t belongs to the high technology industry (Appendix 1); whereas Tourismit is a dummy indicating whether this startup can be classified as falling into a tourism-related category (Appendix 2). In our base sample, 70.3% of startups are high-tech firms, 10.1% are in the tourism sector, and 8.0% operate in both sectors.

In addition to the above techniques, we also employ panel data estimators by deriving a country sample where firm-level funding variables are aggregated to the country level. We run both pooled-OLS and fixed-effect estimation for comparison and validation purposes.

Empirical Findings

Main Results

Table 3 includes results of regressing a benchmark OLS with various measures for startup financing and tourist flow, based on a pool of firms headquartered in all sample countries and funded in various sample years. In the absence of controls, Columns (1) to (3) report that more tourists or higher expenditures and a larger tourist ratio are significantly associated with a larger funding amount and a higher standardized ratio of funding, respectively. Columns (4) to (6) repeat these exercises by including firm-level determinants of funding. As expected, older and operating firms obtain more funding than their counterparts. Columns (7) to (9) include additional macroeconomic indicators. We find that, except for exports, GDP growth rate (a positive coefficient), tax revenue (a positive coefficient unless ratio measures are used), economic freedom index (a positive coefficient), and market capitalization (a negative coefficient) all turn out to be important funding determinants. Overall, the F-test statistics suggest a valid modeling choice. Focusing on coefficients of tourism proxies, given that the estimate in column (6) is an exception, their size is noticeably large, and they always stay significantly positive, at least at the 5% level, thus supporting our arguments.

Results of Benchmark OLS Estimation in the Firm-year Base Sample.

Note. All regressions include an intercept. Standard errors with White’s correction of heteroscedasticity are included in parentheses.

and ** denote significance at the 1% and 5% level respectively.

From this point on, we mainly work under the 2SLS framework since a major concern is that endogeneity could arise due to reverse causality. The IVs adopted are the number of international football matches held in a sample country and the number of certified heritage sites owned by a sample country. Both IVs are highly correlated with international tourism, and they display much less direct connections with investment flowing into startups in general. In line with the IV selection criteria proposed by Acemoglu et al. (2001) and Miguel et al. (2004), the investment-facilitating effect of tourism functions via a short-run economic process, we should choose IVs that belong to non-economic shocks. They will impose long-run impacts on outbound and inbound travel plans.

Moreover, our chosen IVs also pass tests for screening out weak and over-identified IVs. In columns (1) to (3) of Table 4, we present the second-stage results when cross-border tourists are instrumented in the first stage using our proposed IVs. In the presence of all controls, our coefficients of interest remain positive at the 1% significance level. Their magnitude is more significant than that of OLS estimates, suggesting that we may have successfully corrected the underestimation bias caused by measurement error. The two-way causality might not be a severe problem here.

Results of Main 2SLS Estimation in the Firm-year Base Sample.

Note. All regressions include an intercept. Standard errors with White’s correction of heteroscedasticity are included in parentheses.

and ** denote significance at the 1% and 5% level, respectively.

In columns (4) to (6) of Table 4, while sticking to the above 2SLS method, we also control for an array of time-fixed country-level geographical characteristics (e.g., land area, landlocked country or not, latitude, longitude, official language English or not, continent located) in the second stage to deal with another type of endogeneity caused by variable omission.

From the baseline regression results, we can see that the estimated coefficients of regressing startup funding on the number of tourists range from 0.234 to 0.410. This indicates that a 1% increase in the number of inbound and outbound tourists in the country where the startup is located will increase the venture investment received by the startup by 0.234% to 0.410% on average. In the table of descriptive statistics, the standard deviation of inbound and outbound traveler counts equals 0.802, and its mean value is 18.278. In terms of exactly how many international tourists before we take the logarithm, the country-level sample mean is about 20 million annually. As a result, an increase of 1 standard deviation of the growth rate in tourist flow can be translated to 877,558 (=0.802/18.278 × 20,000,000) more tourists. This further leads to an increase of 0.188% to 0.329% in the growth rate of funding for startups, or equivalently an extra capital amount of $1,880 (=0.188% × 1,000,000) to $3,290 (=0.329% × 1,000,000) on average (the average amount of venture capital is about 1 million across country and year in our sample). Similarly, a 1-standard-deviation rise in the growth rate of inbound and outbound travel spending (i.e., an average increase of 800 million) would indicate an 0.182% to 0.330% increase in the growth rate of entrepreneurial capital disbursed. As for the proportional measurement perspective, a 1% increase in the rate (which is defined as the number of inbound and outbound tourists of the concerned startups’ home country as a percentage of the average number of people traveling in and out of all countries in the same sample year) would increase the proportion of funds received by these startups as a percentage of the average amount of funds disbursed during that year by about 2.6% to 3.4%.

Two Underlying Mechanisms

This subsection attempts to explain our main results through theoretical lenses built on the two mechanisms. To capture the “investment scope difference,” we regress the twoSLS equations (1) and (2) in two subsamples with marginal overlaps: startups funded by angel investors and those funded by venture capital funds. In Table 5, the estimation shows that the effect of tourist flow on startup funding is always significant but is more pronounced with startups receiving venture capital investment. Specifically, based on the estimation in column (1) versus (4) and that in column (2) versus (5), the coefficients on both tourist numbers and expenditure are much larger for venture capital-funded startups than for angel-funded ones. When this scope effect is removed by normalizing tourism and funding proxies, as can be seen in columns (3) and (6), we observe no difference concerning magnitude between the coefficient estimates in the angel- and venture-stage subsample. One distinction is that the coefficient before survivorship is always negative in the angel-stage funding subsample. The reason might be that too much angel round investment could cause an imbalance in the capital structure of firms and harm their future operation. In all cases, the test statistics suggest that the IV approach delivers superior performance for the venture subsample. We provide substantial evidence that tourism can increase the scope of investment available to potential investors in a company’s early development stage. The results support the “investment scope” argument.

Results of 2SLS Estimation in Angel- versus Venture-stage Funding Subsample.

Note. All regressions include an intercept. Standard errors with White’s correction of heteroscedasticity are included in parentheses.

and ** denote significance at the 1% and 5% level, respectively.

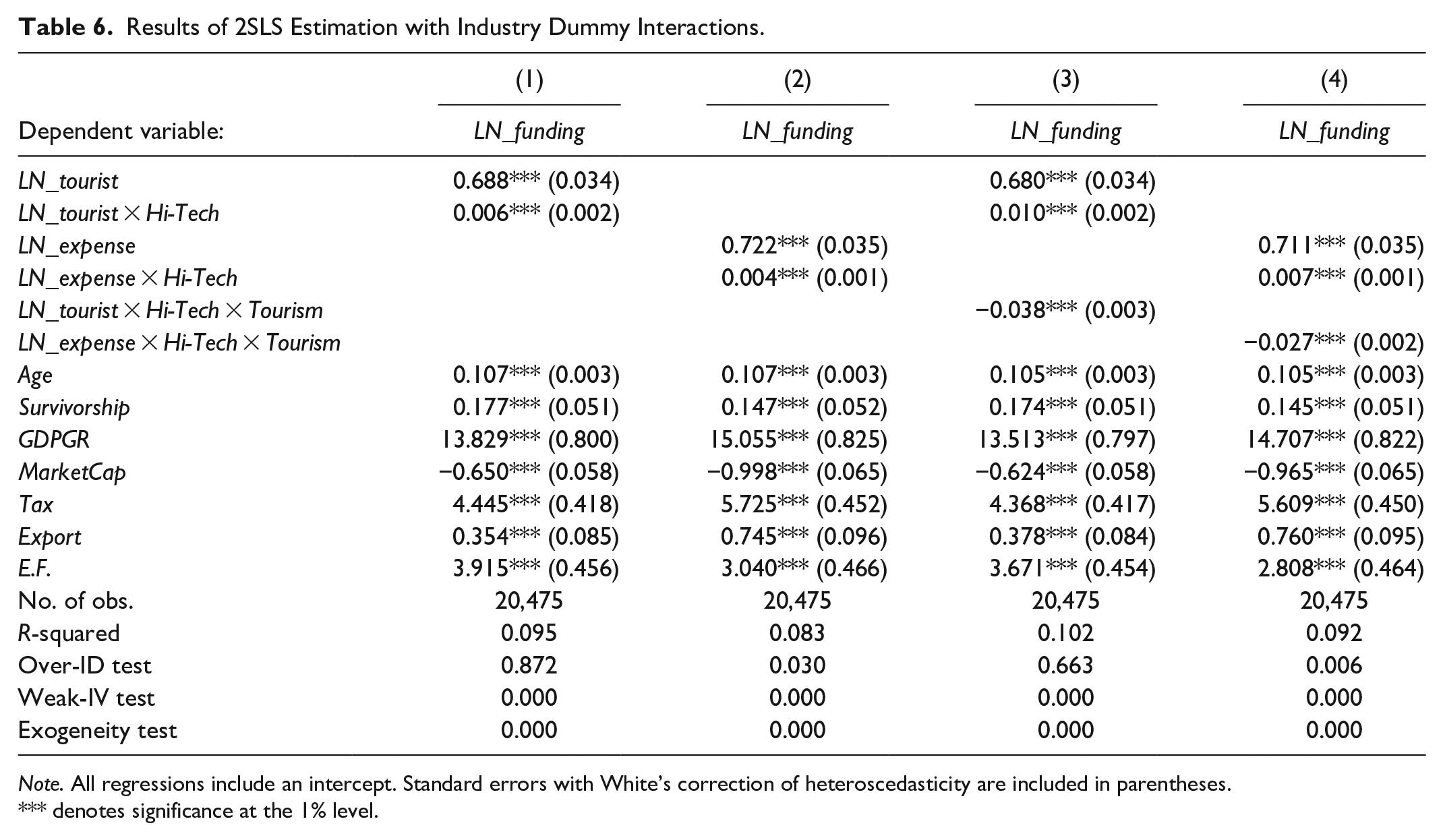

The “market potential” effect can also function through a realized channel. Tourism development will cause GDP growth in both host and destination countries, which further enhances the product markets’ actual size. As long as this tourism-GDP nexus drives our results, the effect of tourism on funding should be larger in tourism-related sectors when 3-year lagged rather than contemporaneous tourism outcome variables are used. We estimate equation (4) by including interactions between industry dummies and tourist proxies in the second stage regression. Tables 6 (contemporaneous tourism outcome variables) and 7 (3-year lagged tourism outcome variables) report the results. Although we find a larger effect of tourism promoting funding in high-technology sectors, this effect becomes smaller in tourism-related industries. In other words, we would observe a negative estimated coefficient of the interaction between three variables: the number of tourists, the hi-tech sector dummy, and a tourism sector dummy. We find that startups from the tourism sector receive fewer funds than those in other sectors. It is the high technology sector that benefits the most from tourism growth. Though this fact challenges the validity of the “market potential” channel, we believe it is still valid but that its power has been dampened by increased costs, diversion effects, and diminishing investment returns in the tourism sector accompanied by tourism development. This finding seems to be in contrast with our prediction based on the “market potential” argument. Nevertheless, there could be several reasons for this contradiction.

Results of 2SLS Estimation with Industry Dummy Interactions.

Note. All regressions include an intercept. Standard errors with White’s correction of heteroscedasticity are included in parentheses.

denotes significance at the 1% level.

Results of 2SLS Estimation with Industry Dummy Interactions and 3-year Lagged Explanatory Variables.

Note. All regressions include an intercept. The notation Lag3 means that this proxy is 3-year lagged behind the original value. Standard errors with White’s correction of heteroscedasticity are included in parentheses.

and **, denote significance at the 1% and 5% level, respectively.

One explanation is that despite enlarging the market size, tourism growth could also raise the cost of inputs in tourism countries, especially labor costs, and increase the tax burden of local startup firms, especially the property tax. For business entities operating in the tourism sector, the salary for unskilled labor and the tax imposed on tourism constitute a relatively larger proportion of their cost structure. Hence, the negative effect incurred by tourism development dominates the positive effect in the tourism industry. Another explanation relates to the diversion effect. The total amount of venture capital funds is relatively stable during our sample periods, except for the downward shift in investor confidence during the 2007 global crisis. If entrepreneurial opportunities in non-tourism sectors grow faster than those in the tourism sector, then funds injected into tourism-related startups will be diverted away. This explains why we observe that inbound and outbound tourism can enhance startup financing, but money invested in tourism-related startups increases at a slower pace than that invested in other startups. The final potential explanation for this negative interaction is that the diminishing marginal return on investment may come into play. In those countries where tourism markets are already matured, new tourism business ideas and related startups would lose their attraction to angel investors and venture capitalists.

Robustness Checks

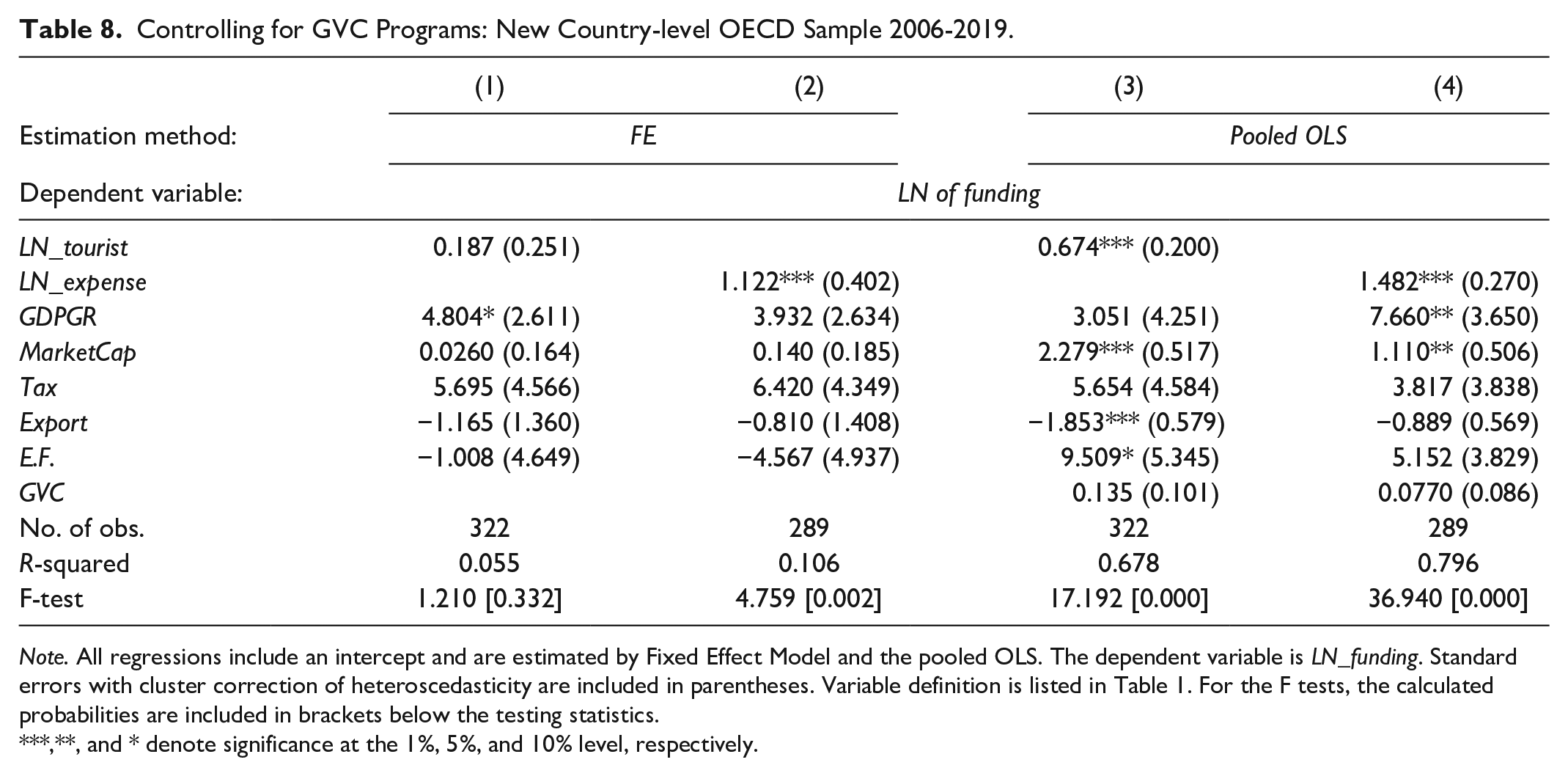

In addition to the main models, we further added country-level determinants of venture capital investment for examining the robustness of our findings. First, to control for the effect of government venture capital (GVC), we resort to Bai et al. (2021) who use hand-collected data on 755 government programs worldwide and find that public allocations to such funding programs are as important as global private venture capital disbursements. In specific, we use their measurement of how many times a country has been a focus among 140 official reports and academic papers published from 1998 to 2019 on the topic of entrepreneurial finance government policy and actions. Thus, higher counts would imply that the focused country has made greater efforts in facilitating venture investment.

The sample we use here to investigate the effect of GVC includes all OECD countries from 2006 to 2019. Since our new GVC proxy is a cumulative count number at the 2019 years-end, it is time-invariant and can only be estimated in a pooled OLS setup. As can be seen from columns (3) to (4) of Table 8 in this letter, both the tourist flow and the tourism expenditure remain significantly and positively correlated with venture capital funds. The estimator before the GVC proxy is positive as expected but not significant. This is probably due to the small sample size.

Controlling for GVC Programs: New Country-level OECD Sample 2006-2019.

Note. All regressions include an intercept and are estimated by Fixed Effect Model and the pooled OLS. The dependent variable is LN_funding. Standard errors with cluster correction of heteroscedasticity are included in parentheses. Variable definition is listed in Table 1. For the F tests, the calculated probabilities are included in brackets below the testing statistics.

,**, and * denote significance at the 1%, 5%, and 10% level, respectively.

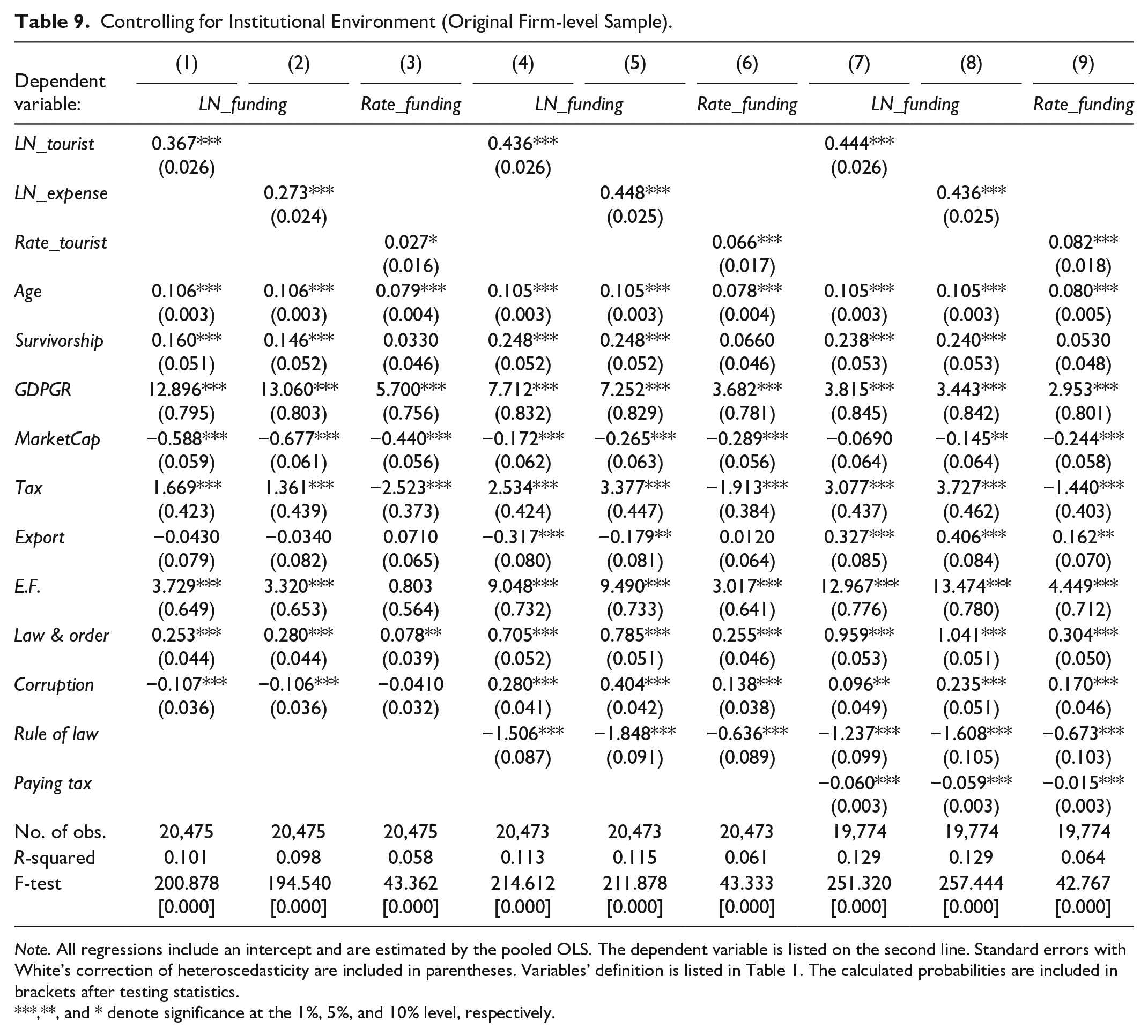

In columns (1) to (2) of Table 8, we list the fixed-effect estimators without the time-invariant GVC measure and based on the same OECD sample as a benchmark. Secondly, in line with Armour and Cumming (2006), who utilize variables from EVCA to measure the role played by tax and legal initiatives in supporting entrepreneurs, we control for the tax and legal driver of venture capital funds. In specific, we employ the score of “paying tax” issued by the doing business database (2006–2014) and the “rule of law” rating (1996–2014) published by World Governance Indicators. In addition, like in La Porta et al. (1998), we also control for the “law and order” and “corruption” statistics provided by the International Country Risk Guide database. After merging, the home countries of more than 90% of firms in our Crunchbase database are covered by the above legal environment and institutional quality proxies. Table 9 presents the estimation after considering the effect of all four institutional quality measures, the concerning effect of tourism on entrepreneurial financing remains positive and statistically significant.

Controlling for Institutional Environment (Original Firm-level Sample).

Note. All regressions include an intercept and are estimated by the pooled OLS. The dependent variable is listed on the second line. Standard errors with White’s correction of heteroscedasticity are included in parentheses. Variables’ definition is listed in Table 1. The calculated probabilities are included in brackets after testing statistics.

,**, and * denote significance at the 1%, 5%, and 10% level, respectively.

We also perform industry heterogeneity analysis. In total, there are six major categories of industries in our sample: tourism (i.e., the broader tourism sector), hi-tech (i.e., the emerging sector with adopting new technologies in developing their products and services), environ. (i.e., the environmental industry), daily (i.e., companies producing daily necessities for life), medicine (i.e., the pharmaceutical industry), and infra. (i.e., the infrastructure sector). After repeating the baseline regressions in the above industry subsamples, we find significant results in the first four columns of Table 10 and slightly lower significance in the estimated coefficients for the pharmaceutical and infrastructure industry. This indicates that the impact of inbound and outbound tourism on entrepreneurship in the host country indeed differs a lot across different and such linkages turn out to be weaker in ventures in the field of medicine and infrastructure.

Industry Heterogeneity Analysis.

Note. All regressions include an intercept and are estimated by the pooled OLS. The dependent variable is listed on the second line. Standard errors with White’s correction of heteroscedasticity are included in parentheses. Variable definition is listed in Table 1. For the F tests, the calculated probabilities are included in brackets below the testing statistics.

,**, and * denote significance at the 1%, 5%, and 10% level, respectively.

In terms of coefficient significance, funds received by startups involving new technologies are most significantly affected by inbound and outbound tourism. The reason is twofold. On the one hand, more than half of the startups in our sample are related to technology. On the other hand, our proposed mechanism of tourism opening entrepreneurs’ eyes to a wider range of novel products and business models should better function in the emerging sector. Turning to coefficient magnitude, cross-border traveling exerts the greatest impact on financing firms providing daily necessities to society. This is probably because different countries have distinct cultures and life modes, which can directly enlighten entrepreneurs’ inspiration and help them formulate their unique characteristics. Consistent with the recent study by Bianchini and Croce (2021), we also observe a statistically significant impact in the environmental sector due to the fact that sustainable economic growth development has guided many investment principles in most countries. However, our tourism-funding nexus becomes minimal in the pharmaceutical and infrastructure industries. The finding is intuitive since the former sector has fewer connections with tourism, and the latter sector takes years to develop, whereas the tourism impact tends to be immediate.

Discussion and Conclusion

Our findings show that international tourism development can promote the funding received by startups, as international tourists in a country are accompanied by new business opportunities and active capital flows.

Our study makes important contributions to the literature. First, it adds to the literature on the impact of tourism by documenting the real effect of tourist numbers and expenditures on startup financing. The previous literature on the relationship between tourism and economic growth mainly focuses on the relationship between the tourism market and economic factors such as employment and infrastructure (Belloumi, 2010; Fainstein et al., 2003; Spasojević & Božić, 2016). Only limited studies examine how international tourists are associated with addressing existing environmental, social, and cultural issues (e.g., Huang et al., 2019). Moreover, few studies have documented how international tourism influences firms’ financing choices and investors’ decisions. We intend to fill this gap. To the best of our knowledge, our article is among the first to examine the real impact of international tourism, operationalized by various indicators, on startup investment outcomes. Second, we provide an additional mechanism through which information flow can promote entrepreneurial ideas’ spillover. Our results suggest that a flourishing tourism sector facilitates venture deals in all industries. It is by enlarging the investable universe available to investors and incentivizing angel investors and venture capitalists to predict a higher market share for startups ex ante. However, this positive effect might be compromised by higher labor costs and a larger tax burden caused by more tourists.

As for this paper’s practical implication, startups should take full advantage of the positive externality brought in by global tourism growth. For policymakers, our study suggests that actions and projects aimed at developing international tourism can be more beneficial than is the tourism industry itself, which greatly enlarges the range of policy impact evaluation and functionary channel identification. We found startups in the high-technology sector to incur more entrepreneurship opportunities due to tourism growth because they capture the attention of angel investors and venture capitalists. However, startups closely related to tourist consumption are found to have disadvantages in obtaining investment associated with developing the cross-border traveling market. This seemingly counterintuitive finding could come from three possible outcomes caused by more tourists and larger tourism receipts: (i) an increase in labor costs and property tax, (ii) the functioning of the investment diversion effect, and (iii) the diminishing marginal return on startup funding.

Footnotes

Appendix 1

Appendix 2

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work is supported by Shanghai Municipal Education Commission and Shanghai Education Development Foundation “Chen Guang” project [ID: 17CG65] and Shanghai Young College Teachers Training Subsidy Program.