Abstract

This study aims to test the impact of digital technology and business regulations on financial inclusion and socioeconomic development in low-income countries. Digital technology and business regulations are perceived to be powerful factors to spur financial inclusive economies and ease several social and economic ills and thus enhance the welfare of low-income nations which represent most world regions. Secondary data were collected for 77 low-income countries from different sources including World Bank, IMF, and UNDP while Smart PLS 3. software was employed for data analysis. This study is distinguished by casting a new angle of linking digital technology and business regulations as drivers of financial inclusion and socioeconomic development. It also presents financial inclusion as a means to an end. Furthermore, it contributes to the literature by providing an empirical evidence on the significant positive impact of digital technology and business regulations on both financial inclusion and socioeconomic development using PLS-SEM method. Thus, stakeholders, governments, and supporters ought to sustainably endorse adoption of digital finance and business environment to assist the poor low-income citizens get pulled into a better-quality life and more improved living standards.

Keywords

Introduction

Digital technology and business regulations are recently attracting considerable interest due to their recognized impact on economic growth and development, especially for low-income countries by enabling them to have adequate access to financial services and resources besides improving the business environment that can optimally help them reduce poverty levels, enjoy better living conditions, and relish improved socioeconomic life (Adaba et al., 2019; Cohen et al., 2018; Djankov et al., 2019). In recent years, low-income countries have seen a huge increase in the adoption of digital technologies. For instance, in most low-income nations, the number of mobile subscriptions, internet users, and fixed board subscriptions has increased at rates much exceeding 50% (International Telecommunication Union, 2019; World Bank IBRD, 2016).

In fact, there are some obvious benefits to digital technology adoption recognized in both developed and developing countries. To cite an instance, evidence shows that digital technology could stimulate economic growth in Australia by contributing to the GDP per capita of about 5.8% on average(Qu et al., 2017). In Thailand, another conclusion, attained by Chakpitak et al. (2018), has shown that digital technologies could significantly enrich business practices and positively influence people’s life, together with the Thai economy. The importance of digital technology in connecting communities and inspiring individuals and building up modernization has further been emphasized by Solomon and Klyton (2020) who tested the impact of digital technology on economic development in 39 African countries and displayed various beneficial outcomes associated to digital technology adoption, such as boosting communication, empowering people, creating jobs, and fostering innovation. Additionally, Chiemeke and Imafidor (2021) realized the effectiveness of digital technology in raising labor productivity and growth. However, they specified the necessity of strengthening digital technology literacy to fully reap the benefits of the growing digital technologies in Nigeria. At the same time, Irtyshcheva et al. (2021) manifested the positive influences of digital technology on economic growth in Ukraine and confirmed the significance of digital technology advancements to boost digitalization in society and enhance GDP.

On the other hand, certain studies talked about the importance of business regulations and affirmed that business regulations and the ease of doing business could have a significant impact on the growth of businesses and firm productivity as well as on people’s livelihoods and income. To mention a few, Canare (2018) studied 120 nations and discovered that ease of doing business allowed favorably rigorous firm development and lead to better entrepreneurship. Similarly, Djankov et al. (2019) analyzed data for 189 economies and found a strong correlation between business regulations and the reduction of poverty head count ratio at the country level. Additionally, regulatory reforms boosted sectoral competitiveness and sustained market competition in Portugal, according to World Bank (2020), resulting in a 6% to 11% increase in income.

Recently, large number of international players, local governments, donors, and development organizations increasingly speak about the resulted gains of digital technology adoption besides the benefits of good business regulations (Bennett, 2019; Evans, 2018). They accordingly assign sizeable budgets, design various programs, and provide limitless supports for low-income countries to take on digital technology and enact regulatory framework reforms that can contribute to low-income economies’ betterment. At the same time, in the last few years, numerous emerging economies have shown vigorous concerns to catch up with digital technology and be digitally involved (Patwardhan et al., 2018). Additionally, many low-income countries have followed initiatives at different levels to build some technical infrastructures and design regulatory policy reforms to benefit from digital technology and regulations in the era of digital globalization. The Indian government, for instance, has lately made some steps to heighten digital financial inclusion and digitalization by improving essential digital infrastructure and internet speed and connection and outreach especially for rural areas (Ciuriak & Ptashkina, 2019; Srikanth et al., 2021).

What’s more, the growing adoption rates of digital technology is conceivably supposed to boost financial inclusion in low-income countries. Yin et al. (2019) hence assert the importance of financial inclusion to support financial stability, mitigate social and economic ills and inequalities, and reduce poverty. Van et al. (2019) also confirmed the value of financial inclusion for promoting economic growth and development especially in low-income countries.

Low-income countries are principally confronted with multi-facet economic and social problems such as insufficient access to essential financial services in addition to gender inequality, corruptions, and adversity. Many citizens of low-income or developing countries cannot approach formal banking channels to get the required services and products. Furthermore, most of them, particularly women, still suffer from acute levels of disparities and lack basic human development opportunities. Consequently, various organizations have realized the importance of modern technology and business regulations to support populations in developing countries to get adequate access to financial services and improve the business regulations environment. And all this can presumably reduce poverty in low-income countries and enable their population to rightfully enjoy suitable living conditions via being exposed to better human and socioeconomic prospects.

The enormous growth and expansion of digital technology call forth a thorough and systematic inquiry on its potentials for improving human lives, particularly through financial inclusion and socio-economic developments. Evans (2018) argues that there is a deficiency in current literature that highlight the effect of internet and digital mobile usage on financial inclusion. Similarly, business regulations are considered important motivators for a favorable structural change and socioeconomic growth (Dima & Dima, 2018). Therefore, their impact on the social and economic development of low-income nations necessitates scrutinizing as well.

The inherent benefits of digital technology in enhancing accessibility through digital financial inclusion in addition to business regulations that shape financial services and elevate investment constitute a very important phenomenon which perhaps requires further investigation. Business regulations seem to move unitedly together with digital technology to contribute to the compelling and central goal of socio-economic development especially in low-income countries (Djankov et al., 2019; Irtyshcheva et al., 2021). Examining the relationship between digital technology or business regulations and financial inclusion and socioeconomic growth has remained low in the literature. So, this study pursues to tackle this gap.

In fact, there are numerous empirical and theoretical studies that have tested the impact of digital technology on financial inclusion and the influence of business regulations on economic growth: Chen and Divanbeigi (2019), Divanbeigi and Ramalho (2015), Shen et al. (2020), and Vyas and Jain (2021) are few to name. However, as far as we know, no previous research has investigated the effect of the twins of digital technology and business regulations as drivers for either financial inclusion or socioeconomic development. Digital technology and business regulations seem to share the quality of being growth and development stimulators.

Furthermore, several theoretical and empirical studies such as Cicchiello et al. (2021), Demirguc-Kunt et al. (2017), and Musembi and Chun (2020) that separately revealed the significant relationships between financial inclusion and economic growth and development. Nevertheless, rare research appeared to study financial inclusion as a means that is influenced by digital technology or business regulations to provoke socioeconomic development so far. For this reason, this study seeks to fill this gap too. In addition to that, financial inclusion is here fully represented by its all three components that consist of Access, Usage, and Quality.

The field of examining the impact of modern digital technology on socioeconomic development is now maturing. O’Connell and Ghani (2016) argue that studying the role of technology and exploring its impact on growth and development is still a new issue and at its initial stage, though increasing quickly. Studying the impact of digital technology and ICT on economic growth is also a current topic which is still open to investigation, as assertedly confirmed by Bahrini and Qaffas (2019). Moreover, financial inclusion has now become a fertile area of study and research that still attracts many researchers and academics.

To that end, this study seeks to examine factors that influence financial inclusion and socio-economic development because of digital technology and business regulations adoptions. As aim indicates, the research tries to show the effects of taking on digital technology and business regulations for reaching inclusive financial systems and improved socioeconomic communities.

The specific objectives of this study are as follows: (1) To estimate and test the effect of Digital Technology on Access, Usage, and Socioeconomic Development as well as the effect of Business Regulations on Quality, Usage, and Socioeconomic Development. (2) To estimate and test the effect of Access, Usage, and Quality on Socioeconomic Development. (3) To estimate and test the effect of Usage on Access and Access on Quality.

This paper is divided into seven sections and is organized as follows: Following the Introduction. Section II briefly examines the literature review while Section III gives an overview of the conceptual framework and hypotheses development and measurements. Research methodology that includes data collection and analysis is outlined in Section IV. Section V presents the empirical findings of the measurement and structural model assessments which are accordingly discussed in Section VI. Section VII concludes and identifies possible areas for future research.

Literature Review

Digital Technology and Socioeconomic Development/Growth

There have been numerous studies that have examined the impact of digital technology on economic growth and welfare of poor nations. However, most of these studies focused either on certain regions or were at a country level. For instance, Cohen et al. (2018) conducted a study to test the relationship between access to internet and digital technology and quality of life in South Africa. They observed that individuals who had access to digital technology recorded higher scores of life quality than those who were not digitally connected.

Another seminal work in this area included Qu et al. (2017) who tested the impact of technology on economic growth in Australia and found a significant association between digital technology and economic growth that tended to bring about 5.8% on average to the GDP per capita. Therefore, they urged policy makers to prioritize their future interferences based on the expected expansion of digital technologies and their growing influence on economic growth and development. In the same way, Chakpitak et al. (2018) studied the impact of digital technology on economic growth in Thailand and provided empirical evidence showing that digital technologies could positively enhance business activities and improve people’s life and the Thai economy. More recently, Irtyshcheva et al. (2021) investigated the effect of digital technology on economic growth in Ukraine and came up with important affirmations demonstrating that digital technology advancements could raise the digitalization process in the Ukrainian society and increase the GDP as well. In the same manner, Solomon and Klyton (2020) examined the impact of digital technology on economic development in selected 39 African countries and found several positive consequences associated with digital technology adoption that included promoting communication, empowering individuals, creating employment, and stimulating innovation. Nevertheless, Chiemeke and Imafidor (2021) recently assessed the impact of digital technology adoption on economic growth and labor productivity in Nigeria and emphasized the importance of digital technology literacy in order to take advantage of the growing use of digital technologies in the country.

The contribution of digital technology to social and economic improvements was further examined by Adaba et al. (2019) who studied the impact of mobile money on the well-being and development. They discovered that digital finance through mobile money brought several benefits for mobile money users in Ghana. Interestingly, Forenbacher et al. (2019) examined the social and economic factors associated with mobile ownership and came upon with results showing a positive linkage between mobile phone ownership and the factors of education level, social engagement and employment. A more compelling research done by Bahrini and Qaffas (2019) tested the impact of information and communication technology (ICT) on economic growth and found out that digital technology factors represented by mobile phone, Internet usage, and broadband adoption were the key drivers of economic growth.

Additionally, there have been studies that examined the impact of technology adoption on different aspects related to organizations efficiencies, gender, and financial literacy. Mabula and Ping (2018), for example, scrutinized a dual impact of use of technology and SME financial literacy on the processes of record keeping and risk management at firms and discovered a positive relationship between the use of technology and record keeping and firm performance. Additionally, Orser et al. (2019) interviewed 21 Canadian individuals to study digital technology adoption and gender-related factors. Their results revealed three main themes related to gender barriers: they were expectancy factors, facilitating conditions, and performance expectations.

Business Regulations and Socioeconomic Development/Growth

On the other hand, many existing studies in the broader literature have separately examined the impact of business regulations on economic growth too. One example is the seminal work entitled “Business regulations and economic growth: What can be explained?”, carried out by Messaoud and Teheni (2014). They investigated the impact of business regulations on economic growth and discovered a strong correlation between business regulations and economic growth. Then in 2015, Divanbeigi and Ramalho (2015) examined the relationship between the regulatory changes and economic significant values and found out a link between business regulations and business creation and growth.

Reynolds et al. (2018) furthermore evaluated the effect of regulations of digital financial services, particularly that was related to cash-in, cash-out (CICO) networks, on markets and financial inclusion, and noticed a confined impact. They have ascribed the low impact to the low financial infrastructure that still exist largely in low-income countries as marked by the low numbers of bank branches. At the same time, Dima and Dima (2018) assessed the impact of business regulatory frameworks within the growth context and found a positive relationship.

In fact, a growing body of literature has analyzed business regulations and evaluated their impact on business creation and firms enhancement in addition to people’s livelihood and income. Canare (2018), for example, examined the effect of ease of doing business on firm formation in 120 countries and found out that the ease of doing business could positively affect business environment and thrive entrepreneurships and firm productivity in both developed and developing countries. He furthermore added that building a good business regulations environment and a sustained private sector would favorably drive the process of rapid economic growth and development. Moreover, according to the World Bank (2020), Fernandes et al. (2018) found that regulatory reforms improved sectoral competition in Portugal and the fostered market competition created an increase of about 6% to 11% in income. Another influential paper was produced by Djankov et al. (2019) who conducted an empirical study utilizing data from World Bank’s Doing Business and found out a significant correlation between business regulations and poverty at the country level. The significant impact of business regulations on poverty as revealed by this study validates the results of previous studies that used a cluster of business regulations measures and showed positive correlations too. The impact of business regulations on financial inclusion was further assessed by Chen and Divanbeigi (2019) in their study entitled “Can Regulation Promote Financial Inclusion.” They have detected a positive correlation between regulations and financial inclusion since people who live in countries that maintain good-quality regulations are mostly found to have accounts and access to financial institutions compared to those who live in poor or less regulatory environment.

As identified above, it was important to notice in the previous studies that when they evaluated the impact of business regulations on socioeconomic growth and poverty, the impact of digital technology remained somehow absent. Thus, this study intensifies the influencing factors of both digital technology and business regulations when evaluating their impact on socioeconomic development in low-income countries.

Digital Technology, Financial Inclusion, and Socioeconomic Development/Growth

It has been observed that the influence of digital technology on financial inclusion is likewise investigated in a vast amount of literature however, similar to the previous studies, the focus has mostly been on limited regions or at a country level. An influential work was conducted by Evans (2018) to test whether the use of internet and digital financial services could stimulate financial inclusion in Africa and found a significant positive relationship between using internet and mobile phones and financial inclusion process. A similar empirical study done by Durai and Stella (2019) examined the impact of digital finance on financial inclusion in India and proved that digital technology transformed the banking system and facilitated offering digital financial services via mobile phones and other devices linked to digital payment systems. In the same way, Vyas and Jain (2021) surveyed 433 educated adults from Rajasthan, India to empirically examine the importance of digital technology adoption for promoting financial inclusion and found that “a reflective impact (R2 = .28) of the extended technology acceptance model on digital economy and financial inclusion relationship.” Concurrently, Cicchiello et al. (2021) investigated the relationship between financial inclusion and development in 44 low-income countries selected from Asia and Africa and declared a significant correlation between financial inclusion and economic growth.

The link between financial inclusion and growth was also discussed by Demirguc-Kunt et al. (2017) in their paper entitled “Financial Inclusion and Inclusive Growth” where they presented empirical evidence on the efficiency of financial inclusion to contribute to economic growth and development. In a similar tone, Patwardhan et al. (2018) stressed the importance of financial inclusion for achieving inclusive economic growth and emphasized the power of digital technology, particularly Fintech firms to boost financial inclusion. They further indicated the interest of over 100 million people in Asia alone to benefits from digital financial services.

In addition to that, Musembi and Chun (2020) conducted an empirical study to test the impact of financial development and financial inclusion on economic growth in Kenya and found a positive significant relationship between financial inclusion and economic growth on the long-term. Another empirical work was run by Shen et al. (2020) who studied the role of technology for advancing financial inclusion in China and detected a significant relationship between the degree of financial literacy and the use of digital financial services. Therefore, they suggested increasing financial literacy of the customers as well as encouraging them to use digital financial products and services.

The issue of evaluating digital technology adoption and its associated factors for more financial inclusive economies was emphasized in several studies as well. Gbongli et al. (2019) studied the behavioral factors that affected the acceptance of mobile money application in Togo. They identified that the number of mobile subscribers and internet users increased, though the number of customers with bank accounts was less than 15% and the rate of mobile money acceptance was low among Togolese. On the other side, Hu et al.(2019) studied the attitude of digital technology adoption of 387 customers at Hefei Science and Technology Rural Commercial Bank in China and ascertained a strong influence on users intention toward using Fintech services with trust. The role of Fintech and the influencing factors of financial inclusion received attention from many researchers. Yin et al. (2019) used data from World Bank to study prominent factors that influenced financial inclusion in China. Monetary policy turned out to have a short-term positive impact on financial inclusion determinants.

In fact, evaluating financial inclusion in low-income countries is important and discussed in a number of studies. Several attempts were made to measure financial inclusion by developing a financial inclusion index (FII) similar to Human Development Index (HDI). FII is actually based on the involvement of a group of financial inclusion indicators and Wang and Guan (2017) here confirm that financial inclusion indicators can produce correct information and right outcomes “if and only if they are used together” because a single indicator cannot represent any meaning by itself and might also sometimes be misleading. They further add that financial inclusion becomes essential for countries to sustain inclusive financial systems in order to reach Millennium Development Goals.

This study favors to include the full three components of financial inclusion (access, usage, and quality), as outlined by Global Partnership for Financial Inclusion (GPFI, 2016), rather than using any indices when testing financial inclusion in low income countries. Moreover, the selected measures of each financial inclusion construct are meaningful and straightforward. Additionally, this study employs more representative indicators in order to catch their ideal contributions in the attempted financial inclusion constructs.

A closer look to the literature on the impact of digital technology and business regulations on economic growth or development, however, reveals a number of gaps and shortcomings that are addressed in this study.

First, despite the fact that both digital technology and business regulations have appeared in a considerable body of literature as the explanatory factors of the socioeconomic growth, the interrelatedness between digital technology and business regulations as drivers of socioeconomic growth or development has not been discussed before. As far as we know, no previous research has combined these two interconnected factors to investigate their eventual impact on socioeconomic development. Therefore, this study tries to fill this gap and contribute to the literature by uniting both digital technology and business regulations as the probable motivators of the big socioeconomic occurrence in low-income countries.

Then, it was further noticed that a significant review of literature that examined digital technology and financial inclusion concentrated mainly on analyzing the associated consequences of either digital technology such as attitudes toward technology adoption or financial inclusion such as monetary policy rather than handling a broad analysis of the financial inclusion elements. This study addresses the issue by inspecting financial inclusion from its comprehensive perspectives using several underlying measures to give a panoramic view of the current situation in low-income countries.

Lastly, there appears a need to examine the phenomena of financial inclusion and socioeconomic development at a global level since both entail broader concepts and higher manifestations of the development adventure. This study geographically covers all World Bank regions (except North America) and tests reciprocally connected vital concepts.

Conceptual Framework, Hypotheses Development, and Measurement Items

Conceptual Framework

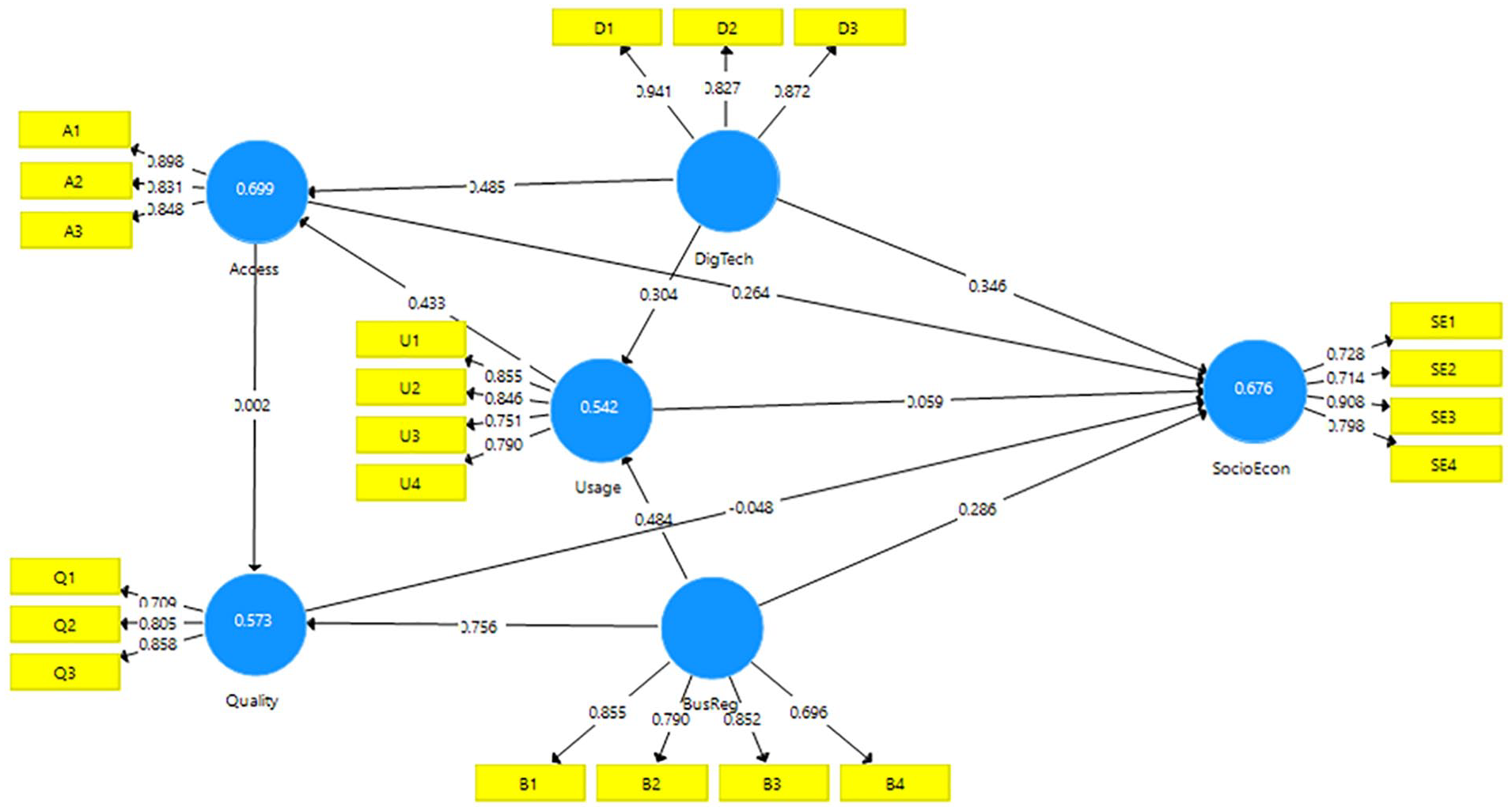

As projected in this Figure 1, the overall principal theoretical model of this study posits that digital technology factors directly influence both financial inclusion (particularly Access and Usage) and socioeconomic development. The study also postulates that business regulations factors have direct influences on both financial inclusion (especially Quality and Usage) and socioeconomic development. Furthermore, the study assumes that financial inclusion elements positively affect socioeconomic development. Finally, the study proposes that Usage influences Access and Access influences Quality within the financial inclusion components These concepts are presented and elaborated in the following subsection of hypotheses development.

The conceptual model of this study.

Hypotheses Development

Digital technology and financial inclusion and socioeconomic development

The relationship between digital technology and financial inclusion and economic growth and development has been highlighted in several recent studies. Bahrini and Qaffas (2019) tested the impact of information and communication technology (ICT) on economic growth and found out that digital technology represented by mobile phone, Internet usage, and broadband adoption were the key drivers of economic growth. Similarly, Gbongli et al. (2019) confirm that digital technologies, especially mobile phones, are seen as a crucial means to spark digital financial services. Digital financial services are now considered as an innovative and effective means to achieve financial inclusion and provide several financial services to the millions unbanked adults who seek for socioeconomic improvements in low-income economies. In this way, Evans (2018) adds that the impact of internet and mobile technology on financial inclusion is remarkably discussed throughout several current studies. Therefore, considering the previous studies, the following hypotheses are developed:

Hypothesis (1): Digital Technology has a significant impact on Access to financial services

Hypothesis (2): Digital Technology has a significant impact on Usage of financial services

Hypothesis (3): Digital Technology has a significant impact on Socio-Economic Development

Business regulations and financial inclusion and socioeconomic development

The link between business regulations and economic growth and development has also been noticed in plentiful studies. Messaoud and Teheni (2014) previously examined the impact of business regulations on economic growth and observed a strong correlation between them. Their findings were in accordance with many previous studies. Moreover, Divanbeigi and Ramalho (2015) studied the relationship between the regulatory changes and significant economic gains and found out a connection between business regulations and business creation and growth. Additionally, the concepts of financial inclusion, Quality and Usage in particular, seem thematically associated with the business regulations construct. Accordingly, the following hypotheses are introduced.

Hypothesis (4): Business Regulations have a significant impact on Quality of financial services

Hypothesis (5): Business Regulations have a significant impact on Usage of financial services

Hypothesis (6): Business Regulations have a significant impact on Socio-Economic Development

Financial inclusion and socioeconomic development

It is argued that understanding the relationship between financial inclusion and its surrounding conditions can help in identifying factors that contribute to the sustainable development of financial inclusion. Yin et al.(2019) assert that inclusive finance has become crucial to improve “income growth and industrial upgrading” especially for low-income people who lack sufficient financial resources. Financial inclusion is said to be closely associated with parts of Sustainable Development Goals declared by the UN and the main aim of sustainable financial inclusion is multifaceted. Financial inclusion seeks to ensure delivering appropriate financial services to the needy and marginalized groups on the basis of equal opportunities so that they can be financially and socially included and hence reduce poverty and social inequality and eventually achieve economic growth and development.

Finally, regarding the components of financial inclusion, literature and GPFI (2016) in particular reveal that financial inclusion is comprehensively measured through three main aspects: namely, Access to financial services, Usage of financial services, and Quality of products and services delivery. This study employs all these dimensions to assess their impact on socioeconomic development. Therefore, based on the three constituents and their interacted relationships, these hypotheses are established:

Hypothesis (7): Access to financial services has a significant impact on Socio-Economic Development

Hypothesis (8): Usage of financial services has a significant impact on Socio-Economic Development

Hypothesis (9): Quality of financial services has a significant impact on Socio-Economic Development

Hypothesis (10): Usage of financial services has a significant impact on Access to financial services

Hypothesis (11): Access to financial services has a significant impact on Quality of financial services.

Measurement items

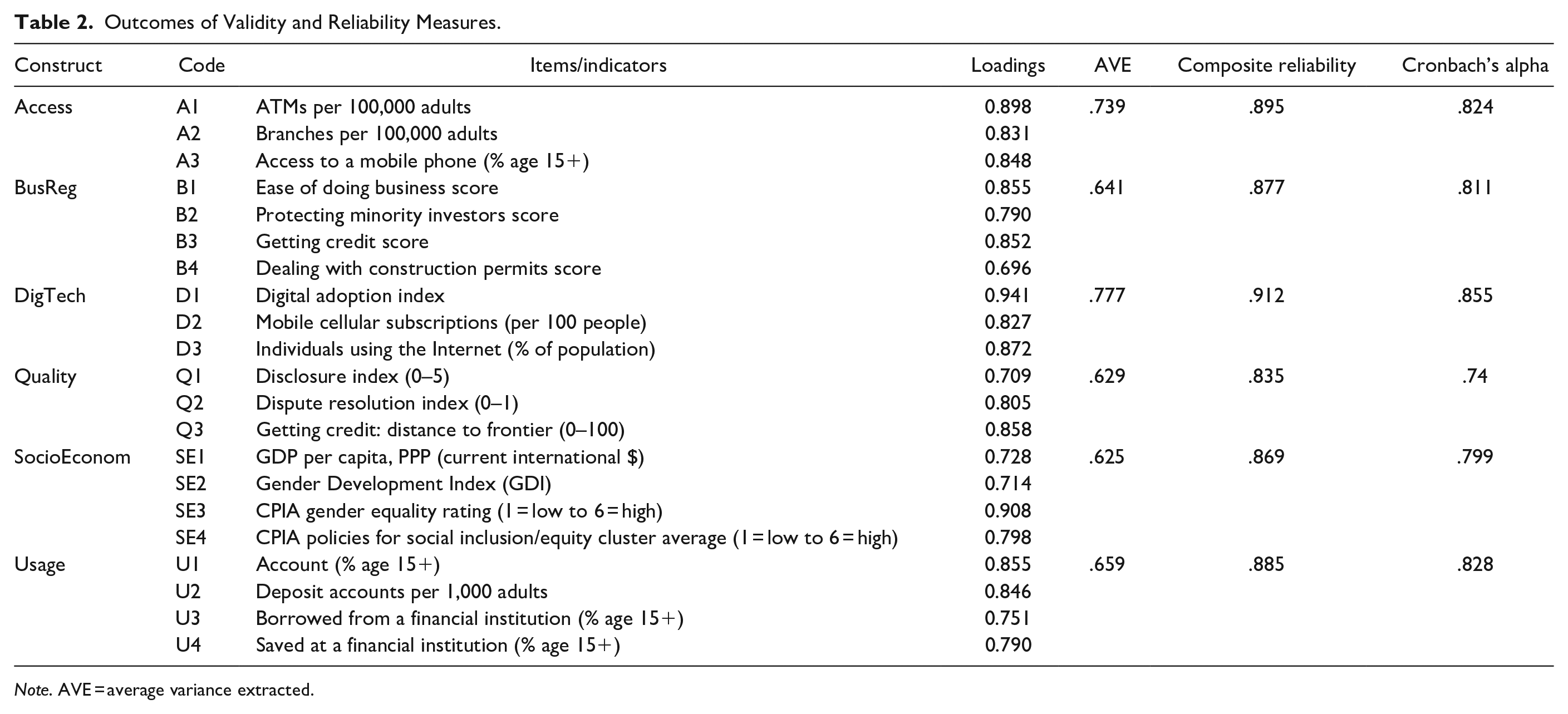

As stated before, there are six latent variables or constructs in this study to be measured by the underlying 21 indicators as illustrated in Table 1. The latent variables embrace both exogenous and endogenous variables. The exogenous latent variables are denoted by ksi (ξ) such as (ξ1) Digital Technology and (ξ2) Business Regulations. They are here the independent variables that influence and explain the dependent variables. Whereas the endogenous latent variables are denoted by eta (η) such as (η1) Access, (η2) Usage, (η3) Quality, and (η4) Socioeconomic Development. They are the dependent variables that are influenced by the independent variables. The following Table 1 shows the 6 latent variables/constructs with their 21 observed indicators labeled below:

Latent Variables With Their Indicators.

Methodology

Method

This study utilizes a “causal research approach” and employs structural equation modeling (SEM). Oppewal (2010) and Sreejesh et al. (2014) explain that causal research always embraces the hypothesized causes and their relationships with the resulted effects. SEM is nevertheless described by Hair et al. (2014) as a “multivariate technique combining aspects of factor analysis and multiple regression.” McQuitty and Wolf (2013) uphold that SEM is particularly well suited for evaluating the relationships among any number of observed and latent variables. Thus, this study adopts predominantly a quantitative method which seems advantageous for its high level of measurements and relies on data quantification which is usually analyzed and interpreted statistically (Faryadi, 2019).

Population and sampling

The population of this study consists of 77 countries. Thygesen and Ersbøll (2014) maintain that this kind of population could be regarded as an “all population sampling” technique since all the 77 low-income (and lower middle) countries are included in the research. Selecting all population sampling is a powerful procedure that allows all units to participate in investigation (Rahi, 2017). On the other hand, Etikan et al. (2016) present “Total Population Sampling” as a type of purposive sampling method which uses the entire population that meet the criteria incorporated in the research.

Data collection

This study used cross-sectional data based on chiefly secondary data and were collected from several resources including World Bank, IMF, and UNDP. Secondary data are described by Martins et al. (2018) as datasets that are formerly collected by someone else other than the researcher and appear convenient to address the research questions of this study. Moreover, Ellram and Tate (2016) consider secondary data as a useful source to be used in several fields. Secondary data are much preferred for the well-established measures they frequently provide which could help researchers to study real phenomena with a great deal of clarity (Hair et al., 2019). Johnston (2014) adds that secondary data provide researchers with flexible and viable sources that can be easily collected, compiled, and stored conveniently.

Data analysis

After examining the empirical data, the analysis of reliability and validity measurements was established. Smart PLS 3. Software Package was precisely employed for data analysis in this study, and it turned to be optimal to run the measurement and structural analysis. The study examined the hypothesized relationships between variables by following Partial Least Squares (PLS-SEM) path modeling. PLS-SEM is a variance -based technique renowned as a causal-predictive method of data analysis (Fatoki, 2019). Hair et al. (2019) clarify that PLS-SEM is causal-predictive technique that attracts many researchers by its efficiency for estimating complex models with many constructs and numerous structural paths besides being more flexible toward data distributional assumptions. PLS-SEM is additionally found advantageous for conducting secondary data analysis “from a measurement theory perspective.” The analysis involves the two consecutive stages of SEM Model assessments: measurement and structural.

Results

Measurement Model Assessment

The initial stage of measurement model assessment requires an overall evaluation of the reliability of indicators and validity of constructs. As explained by Hair et al. (2019), reliability typically involves indicator loadings to be more than 0.70 in addition to the internal consistency reliability that is usually represented by composite reliability and Cronbach’s alpha to be more than .70% too.

In fact, the evaluation of measurement model in this study included consistency reliability, convergent validity, and discriminant validity. Table 2 demonstrates the levels of reliability and validity of the constructs and their indicators. Composite reliability (CR) and Cronbach’s alpha were specifically used to examine the internal consistency of the data and their values were found greater than the recommended standard value of .70 denoting that the measurement model in this paper has a good internal consistency. More specifically, CR indicated that all constructs recorded higher values than .70%, for example, Access (.895) and BusReg (.877) implying adequate reliability for the study. Additionally, the values of Cronbach’s alpha exceeded the cutoff rate of .70% for all constructs, for example, DigTech (.855) and Usage (.828) suggesting levels of acceptable reliability too.

Outcomes of Validity and Reliability Measures.

Note. AVE = average variance extracted.

Factor loadings of all measures surpassed the 0.70%, for example, A1 (0.898) and A2 (0.834), except B4 (0.696), which reached the minimum level yet found significant and reliably contributed to its construct validity.

The next step was to estimate convergent validity of measures and discriminant validity of constructs. Convergent validity refers to the degree “to which the construct converges to explain the variance of its items” and it is evaluated by the average variance extracted (AVE) to be more than .50%. All values of AVE were also beyond .50, for example, Access (.739) and BusReg (.641).

Thus, results of convergent validity and consistency reliability of all constructs as measured by AVE, CR, Cronbach’s alpha, and factor loadings, as shown on Table 1, are supported in this study.

On the other hand, discriminant validity was assessed by applying Fornell and Larcker Criterion (Table 3) and the HTMT (heterotrait-monotrait) ratio of the correlations, Table 4. Discriminant validity refers to the degree “to which a construct is empirically distinct from other constructs in the structural model” (Hair et al., 2019).

Fornell-Larcker Criterion.

Note. Values on the diagonal (bolded) are square root of the AVE while the off-diagonals are correlations.

HTMT Ratio of Correlations Criterion.

Table 3 shows that the square root of AVE for every construct (bold value) is clearly above the correlations of any other construct, for example, the value of Access (.860) is larger than the values of other five constructs in this study. Moreover, Table 4 displays that HTMT values for all constructs are below 0.90% implying absence of discriminant validity problems as maintained by Hair et al. (2019).

To conclude, the findings shown in the above Tables 2 to 4 confirm adequate levels of reliability as well as convergent and discriminant validity of the measurement model of this study. Accordingly, structural model assessment was attempted.

Structural Model Assessment

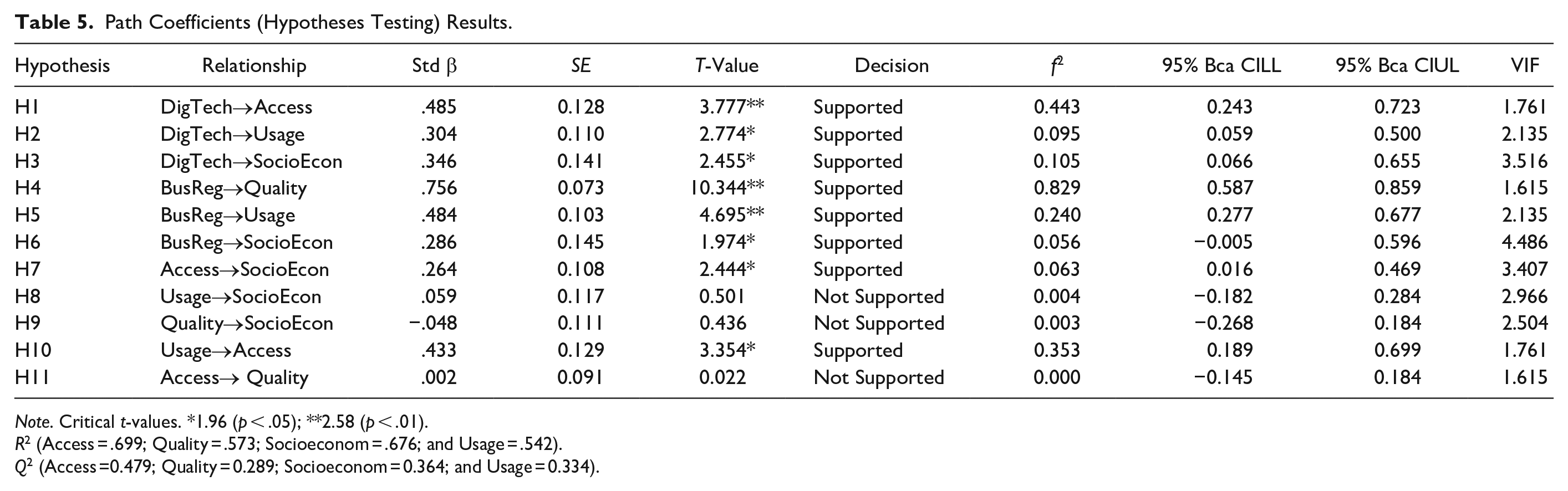

As recommended, Bias Corrected and Accelerated (BCa) bootstraps were selected at .05 significance level and two-tailed testing was followed. Figure 2 presents the bootstrapping outcome while the key results of the structural model assessment are provided in Table 5 which shows the hypothesized causal relationship between the constructs of the model of this study.

Results after bootstrapping.

Path Coefficients (Hypotheses Testing) Results.

Note. Critical t-values. *1.96 (p < .05); **2.58 (p < .01).

R2 (Access = .699; Quality = .573; Socioeconom = .676; and Usage = .542).

Q2 (Access =0.479; Quality = 0.289; Socioeconom = 0.364; and Usage = 0.334).

For evaluating structural model in PLS-SEM, Hair et al. (2017) recommend checking for collinearity and estimating the significance of the path coefficients, the level of the R2 values, the f2 effect size, and the predictive relevance Q2. As Hair et al. (2019) maintain, the first step is to confirm that the critical collinearity does not exist by making sure that VIF (Variance Inflation Factor) values are not higher than 5.

Therefore, the inner and outer collinearity was first checked before conducting structural model assessment. As a result, all indicators and constructs contained a VIF value less than 5 suggesting that they were devoid of critical collinearity (see Table 5).

The following step was to evaluate R2 values of the endogenous constructs. Hair et al. (2019) point out that R2 determines the explained variance in each endogenous construct and shows the “model’s explanatory power” in addition to the “in-sample predictive power.” The rule of thumb for R2 values of .75, .50, and .25 are viewed as substantial, moderate, and weak, respectively. Consequently, the estimated R2 values in this study for the four endogenous constructs are considered ranging from .57 for Quality to .70 for Access while the key endogenous construct of Socioeconomic reached an R2 value above .67. This may reveal the acceptable level of the “in-sample predictive power” of the whole endogenous constructs in this study.

After that and based on the threshold of the t-value for hypothesis testing, it is worth noting that most coefficients are found statistically significant at the significance level of p* < .05 and p** < .001, indicating that the majority of the study hypotheses are supported (see Table 5).

In fact, results of the first and second sets of hypotheses relevant to the impact of digital technology and business regulations on financial inclusion and socioeconomic development are all found significant. Yet, the impact of business regulations on financial inclusion and socioeconomic development is relatively higher than that of digital technology. That is to say, H1, H2, and H3 support significant positive relationships between DigTech and Access (β = .485, p < .01); DigTech and Usage (β = .304, p < .05); and DigTech and Socioecon (β = .346, p < .05) meaning that Digital Technology positively influence both financial inclusion and socioeconomic development in low income countries. Similarly, H4, H5, and H6 support significant positive relationships between BusReg and Quality (β = .756, p < .01); BusReg and Usage (β = .484, p < .01); and BusReg and Socioecon (β = .286, p < .05) revealing that Business Regulations have also a positive impact on both financial inclusion and socioeconomic development in low-income countries.

However, regarding the impact of financial inclusion on socioeconomic development, only Access is found significant, H7(β = .264, p < .05) while both Usage, H8 and Quality, H9 do not significantly affect socioeconomic development in low-income countries. And finally, with regard to the relationship among the three financial inclusion components, it was found that Usage, H10 has a positive impact on Access (β = .433, p < .05) whereas Access, H11 does not influence Quality.

Therefore, it can be concluded that digital technology and business regulations coincidently have a significant impact on both financial inclusion and socioeconomic development in low-income countries. However, financial inclusion influences socioeconomic development only through access to financial services.

Then again, the structural relations among constructs were additionally assessed using f2 effect size and found effective ranging from small, for example, H6 (0.05) to large effect size, for example, H4 (0.82). In fact, f2 values were above the minimum threshold of 0.02 for all supported hypotheses.

Finally, the predictive relevance of the structural model was also estimated in this study using the cross-validated redundancy measure of Q2 as recommended by Hair et al. (2017).They argue that Q2 values that are greater than 0 indicate a predictive relevance for any endogenous construct. Thus, it can be assumed that the model of this study has a good predictive relevance since the Q2 values of Access (0.479), Quality (0.289), Socioecon (0.364), and Usage (0.334) are all above 0.

To sum up, after conducting the validity and reliability analysis, structural assessment was pursued to test the study hypotheses and answer research questions. It was found out that digital technology and business regulations influenced both financial inclusion and socioeconomic development significantly in low-income countries. Though the influence of the business regulations was a bit higher. It was also found out that access to financial services had a positive impact on socioeconomic development.

Discussion

The most remarkable result to merge from the data is the significant relationship established between the dual forces of digital technology and business regulations for enhancing financial inclusion and socioeconomic development in low-income countries. The study generally hypothesizes that there is a significant positive relationship between digital technology and financial inclusion and socioeconomic development on one side, and a significant positive relationship between business regulations and financial inclusion and socioeconomic development on the other.

As seen above, findings demonstrate a significant positive relationship among these hypothesized relationships. In fact, the most striking observation was pertinent to the first set of the structural measurement analyses, that included hypotheses 1 to 6 and examined the impact of both digital technology and business regulations on financial inclusion and on socioeconomic development in low-income countries, which was entirely and interestingly supported in this study. These results further widen our knowledge of the crucial role of business regulations which was in parallel with digital technology and highly contributed to the flourishing of financial inclusion as well as socioeconomic development in low-income countries.

Another outstanding revelation contains hypotheses 7 to 9 and have relevance to the aftereffect of financial inclusion factors on socioeconomic development. Unexpectedly, among the three components of financial inclusion, only access to finance had a direct impact on socioeconomic development in this study. No significant correlations were detected between either usage or quality on the socioeconomic development construct.

It might be mentioned that the attained positive impact of digital technology on financial inclusion and socioeconomic development is found in accordance with a few former studies. One of them is Evans (2018) who concludes that access to internet and use of digital technology can reduce the cost of financial transactions and enhance facilities that could trigger financial inclusion. The findings of Cohen et al. (2018) further revealed a strong correlation between digital technology and individuals’ quality of life. A similar findings of a study by Adaba et al. (2019) illustrates the power of digital technology to enhance financial inclusion in developing countries. Moreover, results of this study seem in line with the findings of a recent research of Bahrini and Qaffas (2019) which indicates that digital technologies especially mobile phones act as key drivers of economic growth.

In a similar fashion, the impact of business regulations on usage and quality as well as socioeconomic development was also observed and was in conformity with the conclusions of Messaoud and Teheni (2014) and Dima and Dima (2018) who found a significant association between business regulations and economic development.

However, unlike the findings of some empirical studies that showed a full effect of financial inclusion on socioeconomic development, such as (Yin et al., 2019).This study produces evidence that only access to financial services has a significant impact on socioeconomic development in low-income countries. In this regard, the outcomes of this study became in line with the results of Demirgüç-Kunt et al. (2008) who previously emphasized the importance of access to finance to poor countries to invest and improve life.

Finally, yet importantly, the results of this study suggest that the use of mobile technology and internet besides the adoption of sound business regulations can lead to better levels of financial inclusion and improved living standards and gender equality in low-income countries. Simultaneously, adequate access to financial services and products could also be effective to raise social and economic status and strengthen gender equality among low-income nations as well.

Conclusion

This study examined the factors that influenced the growth of financial inclusion and socioeconomic development in low-income countries by developing an empirical model to emphatically test the significance of digital technology and business regulations adoption and spotlight their main effects. The exploratory model evinced that the likely combination of aspects of technology adoption with business regulatory frameworks could drive a higher financial inclusion status and result in better socioeconomic welfare for low-income economies.

Policy makers may advocate increasing the diffusion of internet and digital tools such as mobile phones besides endorsing splendid business regulations in order to improve people’s lives and address some gender gaps that still largely exist in low-income countries. Financial institutions are also encouraged to promote appropriate and sufficient access to digital financial services and products to meet low-income citizens’ needs and reach those unbanked groups.

Future studies may investigate the influence of COVID-19 factors on digital technology and business regulations as well as their relationships with financial inclusion and socioeconomic development. The emerged attributes of these relationships could possibly include patterns of business practices, users’ experiences, e-commerce regulations, and digital finance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.