Abstract

This study aims to compose a portfolio consisting crypto hedge fund and ASEAN-5 stock market and to examine the hedging effect of crypto hedge fund against those stock markets. This study employs dynamic portfolio approach using data from the period of July 2013 to August 2021. This analysis finds that crypto hedge fund can provide hedging effect against ASEAN-5 stock portfolio resulting in hedging effectiveness with positive value. Crypto hedge fund is also proven to be able to increase the risk adjusted performance of all ASEAN-5 portfolio observed under this study, shown by an increase in Sharpe ratio and Sortino ratio.

Introduction

Since the launch of bitcoin by Satoshi Nakamoto on January 2009, there are plenty of new types of cryptocurrency which later emerge and are continuously being traded until today. As of now, there are around 6,978 types of cryptocurrency that are actively traded with various market capitalization value. According to the data from coinmarketcap.com, Bitcoin still has the largest market-cap value of all cryptocurrencies, namely approximately 1.1 trillion US Dollar. The continuously increasing price and capitalization of cryptocurrency as well as a better return potential relative to other conservative instruments have attracted investors’ interest to move their investment flow to this new investment category, namely the cryptocurrency funds (Bianchi & Babiak, 2020).

Cryptocurrency is known to have a high-risk characteristic due to its unpredictable rate of return. However, despite showing a high reactivity rate, cryptocurrency also exhibits a faster recovery rate post-crisis compared to other financial assets (Yarovaya et al., 2022). With such characteristics, cryptocurrency may be considered by investors as one of alternative investments that may serve as risk diversifier or safe haven during crisis or extreme conditions on the market (Chkili et al., 2021; Koutmos et al., 2021; Tzouvanas et al., 2020).

Several studies have investigated the role of various types of cryptocurrency as a hedging instrument for portfolios. Those researches resulted in different findings about types of cryptocurrencies that have the ability as a hedging tool. Several studies found the function of Bitcoin in reducing portfolio risk during crisis (Diniz-Maganini et al., 2021; Jiang et al., 2022; Koutmos et al., 2021; Paule-Vianez et al., 2020). Other studies used other instruments and found that Etherum had a better hedging ability relative to Bitcoin (Dwita et al., 2020; Melki & Nefzi, 2022). On the other hand, Jeribi et al. (2021) found that only Dash and Ripple have a consistent hedging protection. While Conlon et al. (2020) found that apparently, Tether is the only one with hedging ability on extreme conditions.

Bouri et al. (2020), in their studies further presented that there were different characteristics in each type of cryptocurrency being examined. Several other studies also found that each type of cryptocurrency had different roles in serving as hedge on each market observed (Omane-Adjepong & Alagidede, 2020; Shahzad et al., 2020). Each type of cryptocurrency has different hedging role and characteristics and that there is a hedging relationship and ability between types of cryptocurrency instrument during crisis period (Nasreen et al., 2021). Currently, there is an instrument called Crypto Hedge Fund which consists of combinations of several types of cryptocurrency, hence it can represent the cryptocurrency market more extensively in comparison to using individual instruments. Convenience for investors to access crypto hedge fund is also an interesting point to be observed as an inseparable part of hedging instrument in the portfolio. To date, Crypto Hedge Fund has witnessed an increase in market capitalization of nearly US$ 3.8 billion in 2020 (PwC and Elwood, 2021).

Therefore, this analysis will focus on formulating a portfolio using Crypto Hedge Fund and stock market. The stock market that will be examined is the stock market in ASEAN-5. The portfolio formulation method that is used is the dynamic method considering several analyses found that this dynamic method performed better compared to static method (Giamouridis & Vrontos, 2007). This study will also probe into the potential of hedging effectiveness of Crypto Hedge Fund against ASEAN-5 stock market.

This study is expected to contribute by filling the gap of existing literatures, which are (1) There are not many research which specifically discuss and introduce crypto hedge fund as one of alternative investment instruments. (2) To date, there is no study that examine the role of crypto hedge fund in providing hedging protection against the stock market. (3) There is no research which examine the hedging ability of crypto hedge fund with dynamic portfolio approach. (4) This study is able to examine the performance of crypto hedge fund in reducing portfolio risk and improving the portfolio’s performance of the stock market in ASEAN’s five largest countries. This is appealing due to the long-term integration in Southeast Asia’s stock market, where the highest integration level occurs during crisis period and continues until one year after the crisis (Robiyanto et al., 2021). This research is expected to become a research which contribute in enriching the literatures concerning crypto hedge fund, ASEAN-5, and the dynamic portfolio approach method.

Literature Review

Merton (1969) developed a concept concerning dynamic continuous time model portfolio that has a better performance relative to one period model portfolio. Dynamic portfolio model which keeps changing over time has proven to generate a lower portfolio risk and produces higher rate of return compared to static portfolio model (Giamouridis & Vrontos, 2007). This is consistent with the philosophy of modern portfolio concept presented by Markowitz (1959) that investor has to choose the most optimum portfolio combination that is able to produce the most optimum rate of return and the lowest rate of risk. Markowitz (2012) further perfected the concept of portfolio approach after considering higher moment events using the concept of mean variance approach.

In several earlier studies concerning portfolio diversification strategies, one of the alternative instruments that are widely examined for its role as a hedge against stock market is cryptocurrency. Several studies found that cryptocurrency can be used to reduce overall portfolio risk (Diniz-Maganini et al., 2021; Melki & Nefzi, 2022; Paule-Vianez et al., 2020). Crypto Hedge Fund, which is a combination of several types of cryptocurrency, is proven to not be significantly influenced by crisis such as COVID-19 (Ben Khelifa et al., 2021). In addition to that, using several types of equally-weighted cryptocurrencies apparently resulted in a more significant and consistent hedging effect compared to using only one type of cryptocurrency (Susilo et al., 2020).

The ability of an instrument to provide hedging effect and reduce portfolio risk can be measured using hedging effectiveness which was presented by Ederington (1979) for the first time. Such hedging effectiveness formula measurement was further developed by Howard and D’Antonio (1984) and Ku et al. (2007). If the resulting hedging effectiveness has positive value, it means that the instrument included in that portfolio has the ability to reduce overall portfolio risk. The studies performed by Tarchella and Dhaoui (2021), Chemkha et al. (2021), and Mensi et al. (2021) found that the portfolio which included a hedging instrument could generate a hedging effectiveness that could reduce the portfolio risk. From the explanation of those previous studies, the first hypothesis of this research can be concluded, that is the ASEAN-5 stocks portfolio which include crypto hedge fund instrument will have positive hedging effectiveness.

Risk-adjusted return of dynamic portfolio which include hedging instrument can be measured using Sharpe ratio and Sortino ratio (Damianov & Elsayed, 2020; Mirza et al., 2021). Stock portfolio which include cryptocurrency as hedging instrument could generate a better risk-adjusted return compared to stock-exclusive portfolio (Bouri et al., 2020; Damianov & Elsayed, 2020). From the explanation of those previous studies, a second hypothesis of this research can be formulated, which is that a stock portfolio that includes crypto hedge fund as hedging instrument will generate a better risk-adjusted return performance compared to stock-exclusive portfolio.

A study concerning hedge fund strategy had also been carried out by Racicot and Theoret (2019) which examine higher moments hedge fund strategy in certain macroeconomic and financial uncertainty conditions using GARCH multivariate technique. Racicot and Theoret (2016) previously also study hedge fund strategy pattern in dealing with systemic risk and macroeconomic uncertainty.

The approach used in this research is by composing a dynamic portfolio between stocks in ASEAN-5 and crypto hedge fund. By adding crypto hedge fund to the stock portfolio, it is expected to result in (1) Positive hedging effectiveness that could reduce overall portfolio risk. (2) A better risk-adjusted return in the portfolio performance. If those two conditions are met, crypto hedge fund can be used as an instrument that could provide hedging effect against the stocks in ASEAN-5.

Method

The data used in this analysis is secondary data that is observed during the period of July 2013 until August 2021. Crypto Hedge Fund is represented by Eurekahedge Crypto-Currency Hedge Fund Index which consisted of equally weighted index of 19 constituent funds and can be obtained from eurekahedge.com. Meanwhile, data relating to ASEAN-5 stock market such as Jakarta Composite Index (JCI) from Indonesia Stock Exchange (IDX), Straits Time Index (STI) from Singapore Stock Exchange (SGX), Kuala Lumpur Composite Index (KLCI) from Kuala Lumpur Stock Exchange (KLSE), Stock Exchange of Thailand Index (SETI) from Stock Exchange of Thailand (SET), and Philippines Stock Exchange Index (PSEI) from Philippines Stock Exchange (PSX) were extracted from Bloomberg.

In this research, the dynamic portfolio approach uses the DCC-GARCH model. Engle (2002) introduced the concept of dynamic conditional correlation as a multivariate model that has the flexibility in correlation estimation. The DCC-GARCH model can be used to formulate a dynamic portfolio that is able to generate hedging effectiveness (Belhassine & Karamti, 2020; Mensi et al., 2021; Robiyanto, 2018; Robiyanto et al., 2019; Zhang et al., 2020).

From the DCC-GARCH model used in this research, a conditional variance will be obtained from each tested variable and a conditional covariance between each stock market and crypto hedge fund. Kroner and Sultan (1993) introduced hedge ratio measurement method that can be calculated with the following formula:

Where

Further, Kroner and Ng (1998) developed a formula to measure optimum portfolio weight with the following formula:

Meanwhile, hedging effectiveness (HE) can be calculated using the formula developed by Ku et al. (2007) as follow:

The performance of dynamic portfolio which include crypto hedge fund in this study can be measured using indicators such as Sharpe ratio and Sortino ratio as follow:

Where ri is the portfolio return, rf is the risk-free rate,

Results

This research uses monthly data from the period of July 2013 until August 2021. Table 1 showed that among all the observed stock market in 5 ASEAN countries, JCI return has the highest standard deviation. Average stock market return in the ASEAN 5 market recorded positive value except for the average return in KLCI. The highest return throughout the observation period is recorded to occur in the SETI whereas the lowest return throughout the observation period happened in PSEI.

Descriptive Statistics.

Source. Secondary data, processed.

From the result of dynamic portfolio composition between return in ASEAN-5 and crypto hedge fund, it is obtained that the overall average return on portfolio of ASEAN-5 and crypto hedge fund have positive value, including the average return on KLCI portfolio which earned a negative value prior to including crypto hedge fund. The summary of the result from dynamic portfolio formulation using DCC-GARCH model can be viewed in Table 2. Dynamic portfolio of KLCI and crypto hedge fund have the highest average return compared to the average return of other portfolio combination. Meanwhile, the lowest average return is derived from dynamic portfolio combination of PSEI and crypto hedge fund. The graph of return of portfolio consisting JCI and crypto hedge fund is presented in Figure 1.

DCC-GARCH Between ASEAN-5 and Crypto Hedge Fund.

Source. Secondary data, processed.

Time varying dynamic conditional correlation between ASEAN-5 return and crypto hedge fund return.

Figure 1. showed the result of time-varying dynamic conditional correlation between ASEAN-5 return and crypto hedge fund return. The DCC score between return of JCI and crypto hedge fund ranges from −0.086 until 0.357. Whereas the DCC score between return of PSEI and crypto hedge fund return ranges between −0.351 and 0.391. DCC score of KLCI-CF return, SETI-CF return, and STI-CF return are always positive throughout the observation period. Return of KLCI-CF ranges between 0.228 and 0.360, return of SETI-CF ranges from 0.047 to 0.313, and return of STI-CF is between 0.179 and 0.215 throughout the observation period. The dynamic portfolio approach shows dynamic correlation between ASEAN-5 return and crypto hedge fund return which continuously change across the analysis time period.

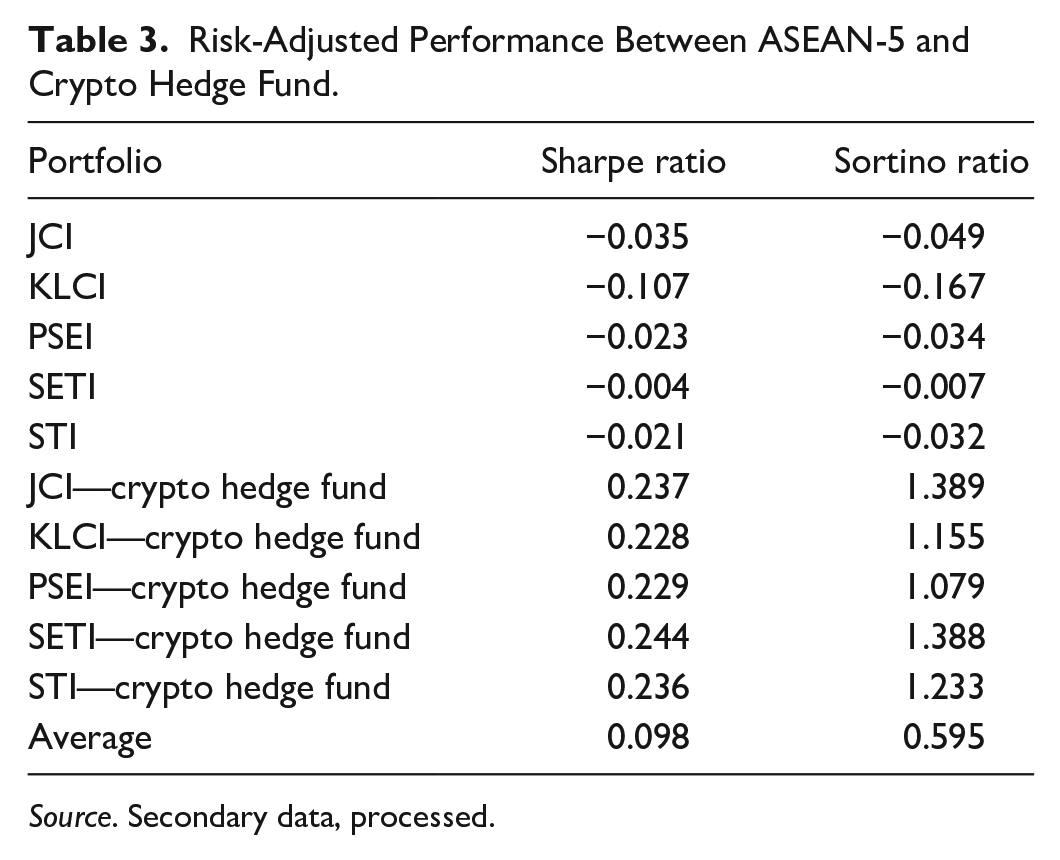

Based on the dynamic portfolio composed of ASEAN-5 and Crypto Hedge Fund, the portfolio performance can be calculated in the form of risk-adjusted return from the formulated portfolio. The risk-adjusted performance of that dynamic portfolio is calculated using Sharpe ratio and Sortino ratio which is presented in Table 3. All of the Sharpe ratio and Sortino ratio from unhedged portfolio in the stock of ASEAN-5 have negative value. The lowest Sharpe ratio and Sortino ratio was generated by KLCI, which was −0.035 and −0.049, whereas the highest Sharpe ratio and Sortino ratio was generated by SETI which was −0.004 and −0.007.

Risk-Adjusted Performance Between ASEAN-5 and Crypto Hedge Fund.

Source. Secondary data, processed.

Sharpe ratio and Sortino ratio of the JCI portfolio experienced an increase when adding Crypto Hedge Fund to the portfolio, from −0.035 and −0.049 to 0.237 and 1.389. Also, the value of Sharpe ratio and Sortino ratio of KLCI-CF portfolio was 0.228 and 1.155, which is higher than the value of Sharpe ratio and Sortino ratio of KLCI portfolio, that is, −0.107 and −0.167. The PSEI portfolio also witnessed an increase in performance, shown by an increment in the value of Sharpe ratio and Sortino ratio after being combined in a dynamic portfolio of PSEI-CF, that is from −0.023 and −0.034 to 0.229 and 1.709. The SETI portfolio, which have the highest Sharpe ratio and Sortino ratio among other ASEAN-5 stocks, also experienced an escalation in Sharpe ratio and Sortino ratio, which was previously −0.004 and −0.007 to be 0.244 and 1.388. The STI-CF portfolio results in Sharpe ratio and Sortino ratio of 0.236 and 1.233, which are higher than the ratios in the portfolio with only STI, that is, −0.021 and −0.032. The value of Sharpe ratio and Sortino ratio from the ASEAN-5 effect, which overall have negative value, turns to positive value after including Crypto Hedge Fund to each stock portfolio. Hence, Crypto Hedge Fund is found to be able to improve the Sharpe ratio and Sortino ratio in all stock in ASEAN-5.

Discussion

The ASEAN-5 stock portfolio which was hedged using Crypto Hedge Fund is found to have a better performance compared to unhedged portfolio. Overall, the value of Sharpe ratio and Sortino ratio of the unhedged portfolio in all ASEAN-5 stock, which initially have negative value, turn positive after including Crypto Hedge Fund as hedging instrument. This result is consistent with the previous studies conducted by Bouri et al. (2020) as well as Damianov and Elsayed (2020) which also found that the portfolio which included cryptocurrency as hedging instrument was able to generate a better risk-adjusted return compared to unhedged portfolio.

Further, to find out whether there is a significant difference between the value of Sharpe ratio and Sortino ratio of the unhedged portfolio and hedged portfolio, mean difference test was performed, in which its results are presented in Table 4.

Mean Difference Test Between Sharpe and Sortino Ratio from Hedged and Unhedged Portfolio by Crypto Hedge Fund.

Source. Secondary data, processed.

From the mean difference test performed, it is found that there is a significant difference in the Sharpe ratio between the portfolio of ASEAN-5 stock that is unhedged and the ASEAN-5 portfolio that is hedged using Crypto Hedge Fund. The same applies to the Sortino ratio between the portfolio of ASEAN-5 stock that is unhedged and the ASEAN-5 portfolio that is hedged using Crypto Hedge Fund, which also shows significant difference.

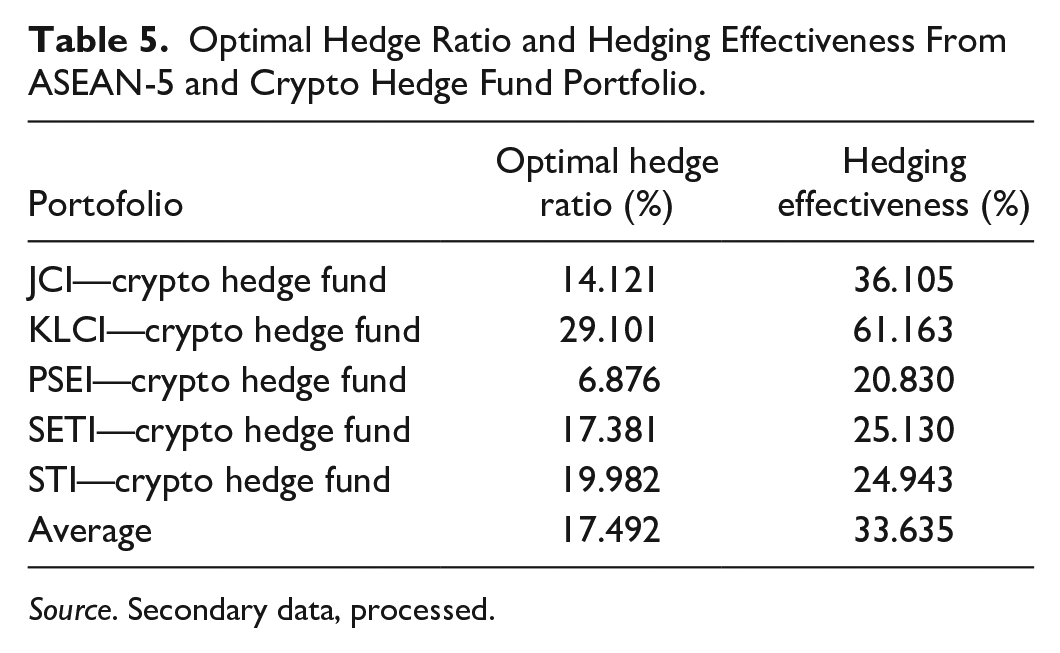

Table 5 showed that the dynamic portfolio composed of ASEAN-5 and Crypto Hedge Fund is found to be able to produce positive hedging effectiveness. KLCI-CF generates the highest hedging effectiveness relative to other portfolio combination between crypto hedge fund and ASEAN-5 stock. KLCI-CF generates the highest hedging effectiveness of 61.163% which means the inclusion of crypto hedge fund to the KLCI portfolio can reduce the portfolio risk by 61.163%. The lowest hedging effectiveness is generated by PSEI-CF portfolio, which is 20.830%. Meanwhile, hedging effectiveness produced by the portfolio combination of JCI-CF, SETI-CF, and STI-CF, is respectively 36.105%, 25.130%, and 24.943%. This finding reveals that crypto hedge fund is proven to be able to provide hedging effect that could reduce the risk of ASEAN-5 stock portfolio. The result of this research is consistent with the previous studies carried out by Tarchella and Dhaoui (2021), Chemkha et al. (2021), and Mensi et al. (2021) which also found that portfolio which included hedging instruments was able to generate a positive hedging effectiveness.

Optimal Hedge Ratio and Hedging Effectiveness From ASEAN-5 and Crypto Hedge Fund Portfolio.

Source. Secondary data, processed.

From optimal hedge ratio measurement using the calculation method developed by Kroner and Sultan (1993), it is found that the lowest optimum hedge ratio is generated by PSEI-CF portfolio, that is, 6.876%, whereas the highest optimum hedge ratio is produced by KLCI-CF portfolio, which is 29.101%. This means that when an investor made an investment by purchasing KLCI stock amounting 1 USD, that investor had to sell their Crypto Hedge Fund instrument amounting to 0.291 USD in order to protect their portfolio value. The same applies when an investor owned PSEI stock amounting to 1 USD, that investor should sell their Crypto Hedge Fund instrument amounting to 0.068 USD in order to hedge their portfolio. Overall, the average value of optimum hedge ratio between ASEAN-5 portfolio and crypto hedge fund is 17.492%.

The measurement of optimal weight ratio using the formula developed by Kroner and Ng (1998) is a dynamic composition that keeps changing over time. Optimal weight between ASEAN-5 and crypto hedge fund in the composed dynamic portfolio is shown in Figure 2. Optimal weight between ASEAN-5 and crypto hedge fund in the composed dynamic portfolio is shown in Figure 2. The weight composition of ASEAN-5 and crypto hedge fund keeps changing to obtain the most optimum portfolio performance. In the JCI-CF portfolio, the optimum ratio composition of JCI weighted between 0.389 to 0.581 and 0.419 to 0.611 for crypto hedge fund. On average, the weight composition of JCI is 0.499 and crypto hedge fund is 0.501.

Time varying portfolio weight of ASEAN-5 and crypto hedge fund.

Meanwhile, for the KLCI-CF portfolio, the weight ratio composition that is generated include KLCI in the range of weight between 0.428 to 0.554 and crypto hedge fund in the range of 0.446 to 0.572. On average, the weight composition of KLCI is 0.497 and crypto hedge fund is 0.503. While in the SETI-CF portfolio, SETI has a weight ratio ranging from 0.392 to 0.597 of the composed portfolio. On average, the weight composition of SETI is 0.508 and crypto hedge fund is 0.492.

PSEI has the most varying range of weight ratio against CF compared to other ASEAN-5 stocks, that is between 0.226 to 0.693 from the composed PSEI-CF portfolio. Meanwhile, STI tends to have the most balanced range of weight ratio, which is between 0.483 and 0.511 from the composed STI-CF portfolio. The range of the weight ratio from the composed portfolio of ASEAN-5 and crypto hedge fund also portrays hedging effect of crypto hedge fund to ASEAN-5 in reducing risk and improving the performance of the composed portfolio.

Conclusion

This study concluded that crypto hedge fund is able to serve as a hedge against stock in ASEAN-5. The conclusion is derived from the finding that of all five dynamic portfolios that was composed between ASEAN-5 and crypto hedge fund, all of which are able to produce a positive hedging effectiveness. This means that by including crypto hedge fund to the dynamic portfolio, we can reduce the portfolio risk.

The portfolio performance measured with risk-adjusted return of the ASEAN-5 stock portfolio which included crypto hedge fund is also found to be better. This can be seen from the value of Sharpe ratio and Sortino ratio of the unhedged portfolio ASEAN-5 which are all showing negative value and then turned into positive value when crypto hedge fund is added to each portfolio. The higher the Sharpe ratio and Sortino ratio produced means that the risk-adjusted return formed out of a portfolio is better. The result of mean difference test of Sharpe ratio and Sortino ratio of the ASEAN-5 unhedged portfolio and ASEAN-5 portfolio hedged by crypto hedge fund also shows significant difference, hence this signifies that crypto hedge fund can enhance the portfolio performance of ASEAN-5 significantly.

Each stock in ASEAN-5 has a specific characteristic when being hedged with crypto hedge fund. PSEI has the lowest hedging effectiveness and optimum hedge ratio relative to other ASEAN-5 stock, whereas KLCI has the highest hedging effectiveness and optimum hedge among others. Meanwhile, JCI has the best risk-adjusted performance of all ASEAN-5 stock when being hedged with crypto hedge fund. From the generated time-varying optimum weight, STI tends to have the most balanced various range of weight ratio to crypto hedge fund in the composed portfolio throughout the research period. Meanwhile, PSEI have the most varying weight ratio range to crypto hedge fund compared to other ASEAN-5 stocks.

The practical implication of this research is that crypto hedge fund can become an alternative investment instrument that can hedge ASEAN-5 stocks. By adding the crypto hedge fund instrument to the portfolio, it is proven to be able to improve the risk-adjusted performance of the ASEAN-5 stock portfolio and reduce overall portfolio risk. Although each stock in ASEAN-5 has a different characteristic when it is hedged using crypto hedge fund, all stocks in ASEAN-5 show a better performance when combined with crypto hedge fund in a dynamic portfolio.

This research still has limitation in its scope of study which allow room of a more specific and extensive development. The ability of crypto hedge fund to hedge other stock markets than ASEAN-5 can still be examined in future researches. Studying the ability of crypto hedge fund as hedge and specific safe haven against stock in certain industry sectors such as technology and finance industry will also be an appealing topic to be studied in the future.

Footnotes

Availability of Data and Materials

The datasets used and/or analyzed during the current study are available from the corresponding author on reasonable request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.