Abstract

The study investigates how corporate social responsibility (CSR) impacts customer engagement and the mediating role of customer-brand identification and customer satisfaction. Survey data collected from 293 life insurance customers were analyzed using structural equation modeling. The findings reveal that CSR, customer-brand identification, and customer satisfaction are essential drivers of customer engagement. Furthermore, the findings show that CSR significantly influences customer-brand identification and customer satisfaction. The results also show that customer-brand identification and customer satisfaction play a key mediating effect in the relationship between CSR and customer engagement. The findings underscore the need for life insurance firms to consider CSR as a strategic instrument to stimulate and elicit favorable customer responses.

Introduction

Customer engagement (CE) has emerged as a construct of increasing importance in current marketing literature and as a new technique in nurturing consumer value and understanding modern marketing (Kumar et al., 2019; Leckie et al., 2016; Rather, 2020). Furthermore, scholars have acknowledged that CE gives firms a real competitive advantage and increases their performance (Hollebeek, 2012; Islam et al., 2019; Rather & Camilleri, 2019; Sirvi et al., 2021). Therefore, practitioners are striving in their actions to foster relationships and to develop bonds with customers (Rather & Camilleri, 2019).

Previous studies have explored some of the factors that drive customers to remain actively engaged with an organization’s services and products or brands with considerable service or online focus, including tourism brands (Harrigan et al., 2018; Rather et al., 2018, 2021; Rather & Hollebeek, 2021), virtual and social media brand communities (Hinson et al., 2019; Hollebeek et al., 2014; Islam et al., 2018; Kaur et al., 2020), online and retail banking (Islam et al., 2020; Kosiba et al., 2018), integrated resort brands (Ahn & Back, 2018), and mobile phone service providers (Leckie et al., 2016), to mention a few.

However, in the insurance context, which represents a particular service sub-sector, much less is understood about the drivers of CE. While this study identifies a few recent studies (e.g., Agyei et al., 2020; Solem, 2016; van Tonder & Petzer, 2018) that address CE’s drivers and outcomes in the insurance context, much more research is still needed to comprehensively understand the role of CE and its particular conceptual connections in this context. According to Kosiba et al. (2018), “insurance marketing is one of the areas that are under-researched” (p. 11). In addition, research by KBM Group & 1to1 Media (2013) shows that the engagement of customers varies widely in the life insurance sector. Their study reveals that only 38% of customers are strongly engaged, with a nearly equal amount (36%) moderately engaged and 27% being weakly engaged. The researchers put forward that strongly engaged customers are most likely to be brand enthusiasts, thus warranting the need for firms in the sector to focus on strengthening CE.

The existing literature has identified some constructs as precursors of CE, including customer brand experience (Carvalho & Fernandes, 2018; Rather, 2020), customer involvement (Harrigan et al., 2018; Hollebeek et al., 2014; Leckie et al., 2016; Vivek et al., 2012), service quality (Islam et al., 2019; Rather & Camilleri, 2019; Verhoef et al., 2010), commitment (Bowden, 2009; van Doorn et al., 2010), customer trust (Agyei et al., 2020; Kosiba et al., 2018), customer satisfaction (Rather, 2019), and reward (Kaur et al., 2020), to name a few. However, despite the existing insight, little is known about the role of CSR in shaping CE. Although some recent studies (e.g., Abbas et al., 2018; Badenes-Rocha et al., 2019; Chomvilailuk & Butcher, 2018; Jarvis et al., 2017) have attempted to link CSR to CE, the findings from these studies have been mixed and inconclusive. For instance, whereas Jarvis et al. (2017), Abbas et al. (2018), and Chomvilailuk and Butcher (2018) found CSR as a significant predictor of CE, the work of Badenes-Rocha et al. (2019) did not find any significant link between CSR and CE, thus warranting further research to fully appreciate CSR and customer behavior consequences (Raza et al., 2020; Uhlig et al., 2020). Furthermore, the existing insight on the link between CSR and CE, to the authors’ best knowledge, is dominated by studies from developed economies (e.g., Australia; Jarvis et al., 2017), and emerging economies (e.g., Thailand and Pakistan; Abbas et al., 2018; Chomvilailuk & Butcher, 2018) with no insight from the African continent. In response to these gaps, this study explores the link between CSR and CE in the African context, specifically in an underexplored area (i.e., insurance sector) where past studies (e.g., Akotey et al., 2013; Alhassan & Fiador, 2014) have mainly focused on constructs like service quality and performance, thus contributing to the insight of the constructs’ role in shaping life insurance firms’ performance.

Customer-brand identification (CBI) reflects a strong psychological or emotional attachment, which is suggestive of future behavior and long-term association (Rather et al., 2018; So et al., 2013). Customer satisfaction, on the other hand, refers to a positive affective state ensuing from consumers’ overall evaluation of their experience with a firm’s services or products (Johnson & Fornell, 1991; Rather, 2019). However, little is known about their roles in the relationship between CSR and CE. Prior studies linking CSR to CE mainly focused on direct relationships (e.g., Abbas et al., 2018; Jarvis et al., 2017), thereby neglecting the possibility of any mediating mechanisms. In addition, theoretical models have posited positive associations between CBI and CE and customer satisfaction and CE (van Doorn et al., 2010). Yet, empirical evidence on these connections remains scarce (Rather, 2019; Rather et al., 2018). That is, studies addressing the role of CBI and customer satisfaction in the link between CSR and CE is limited, and to the best of the authors’ knowledge, this research provides a pioneering examination of the mediating effect of CBI and customer satisfaction in the link between CSR and CE in the life insurance context and an African context.

This study, by addressing these gaps, makes some significant contributions to the literature. First, we propose a conceptual model that examines the unique role CSR plays in shaping CE. Enhanced insight into this area is particularly imperative given CSR’s emergence in recent times as a good marketing instrument for firms, including life insurance companies to inspire good customer response (Chomvilailuk & Butcher, 2018; Lee, 2019) and to create value (Raza et al., 2020). Second, the research empirically validates the mediating effects of CBI and customer satisfaction on the connection between CSR and CE. By mediating these two constructs, this research expands the existing insight and guides future studies away from focusing mainly on the direct relationship between CSR and CE as the relationship between the two constructs may not be straightforward (Badenes-Rocha et al., 2019). Previous studies highlight CBI’s mediating role in the relationship between constructs like CSR and customer loyalty (e.g., Martínez & Rodríguez del Bosque, 2013), and consumer brand-value congruity and CE (e.g., Rather & Camilleri, 2019). However, to the best of the authors’ knowledge, no study has examined CBI and customer satisfaction as mediators in the relationship between CSR and CE. Therefore, this current study is the first effort in CE literature, particularly in the insurance marketing literature to explore the link between CSR and CE via CBI and customer satisfaction which represents a valuable addition to the literature. Finally, the research adds to the literature by investigating CE in the life insurance context, thus responding to calls for the concept’s context-specific exploration (Hollebeek, 2018; Islam et al., 2019; Kumar et al., 2019). Furthermore, this research complements the literature by linking CSR to CE, thereby replying to calls for the examination of CE in the CSR context (Abbas et al., 2018). In addition, this study supplements both CSR and CE literature by carrying out empirical research in a developing economy context (Ghana) and an African context. To date, in the African context, no study has explored the nexus between CSR and CE, and the mediating role of CBI and customer satisfaction. Thus, given that there is much distinction between developed and less developed economies cultures (Farooq et al., 2014; Raza et al., 2020), providing insight from the African perspective, as undertaken in this article, is valuable.

The next section details the literature and conceptual development. This is followed by the methodology. The fourth section presents the data analysis and results. The final part covers the discussion and implications, limitations, and future study direction.

Literature and Conceptual Development

The social exchange theory (SET) has underpinned prior studies that have explored firm–customer relationships in both offline settings (Nunkoo et al., 2010; Rather, 2019; Teye et al., 2002) and online settings (Harrigan et al., 2018). SET supports the idea of investments, which holds that individuals or persons evaluate the benefits and costs of engaging in relationships (Guo et al., 2017; Thibaut & Kelley, 1959). Therefore, for CE to continue, customers must at least achieve equilibrium in these intangible and tangible benefits and costs over time (Hollebeek, 2011; Rather, 2020). Customers may, for example, exhibit enthusiasm and attention in engaging with a brand or a provider to obtain benefits such as news and product/service offers via a sense of belonging (Harrigan et al., 2018; Rather, 2019).

Modern marketing thought considers service-dominant and relationship marketing perspectives, which together suggest that customers are nowadays partners with marketers, creating exchanges via a co-creation process (Harrigan et al., 2018; Vargo & Lusch, 2008). Thus, customers exchange cognitive, emotional, economic, social, and physical resources with marketers (Harrigan et al., 2018; Rather, 2020). So, for CE to persist, the customer, as well as the marketer, must perceive that it is equitable (Brodie et al., 2011; Harrigan et al., 2018; Rather, 2020), thus defining CE as a social exchange.

Customer Engagement

In recent years, the notion of “engagement” has progressively been a topic of investigation in the marketing literature. This is because it is primarily regarded as a dynamic strategy for building and sustaining a competitive edge. Likewise, it is gradually being viewed as a capable driver of future firm performance (Harrigan et al., 2018; Hollebeek, 2012; Loureiro & Lopes, 2019; Rather, 2020). Several studies have confirmed the promising benefits of engaged customers, demonstrating these can show improved customer loyalty, trust, emotional ties, commitment, customer identification, customer experience, customer participation, and so on (Agyei et al., 2020; Brodie et al., 2013; Carvalho & Fernandes, 2018; Kaur et al., 2020; Prentice et al., 2019; Rather, 2020; Rather et al., 2019a; Solem, 2016). These can be critical to the realization of higher firm performance results such as growth in sales, brand referrals, enriched co-creative experiences, and superior profitability (Hollebeek et al., 2014; Loureiro & Lopes, 2019).

There is no consensus regarding CE’s conceptualization and constituents. Researchers have often conceptualized engagement in diverse ways, comprising consumer and customer engagement (e.g., Bolton, 2011; Verhoef et al., 2010), community engagement (e.g., Algesheimer et al., 2005; Brodie et al., 2013), and customer-medium engagement (e.g., Kim et al., 2013). Other conceptualizations include engagement for co-creation (e.g., Jaakkola & Alexander, 2014) and so on, all of which reveal the “evolving state of the construct” (Kosiba et al., 2018; Thakur, 2016). Moreover, it denotes the growing attention among researchers from a diverse perspective.

Together with the diverse conceptualizations, there are different definitions of CE that have been offered by researchers (Islam et al., 2019; Martínek, 2021; Thakur, 2016). For instance, viewing it as a unidimensional concept, van Doorn et al. (2010, p. 254) defined CE as “behaviors that go beyond transactions and may be specifically defined as a customer’s behavioral manifestations that have a brand or firm focus, beyond purchase, resulting from motivational drivers.” Hollebeek et al. (2014, p. 154) define it as “a consumer’s positively valenced brand-related cognitive, emotional, and behavioral activity during or related to focal consumer/brand interactions.” Despite these differences, however, past studies (e.g., Brodie et al., 2011, 2013; Harrigan et al., 2018; Hollebeek et al., 2014; Islam et al., 2019, 2020; Kosiba et al., 2018; Rather, 2020; Rather et al., 2019a) have viewed CE as a multidimensional construct which primarily comprises “cognitive, affective/emotional, and behavioral dimensions” of consumers’ relationship with a company or a brand. Indeed, a review of the related literature points to the dominance of the multidimensional perspective. Therefore, we consider CE as customers’ emotional, cognitive, and behavioral investments in life insurance brand interactions (Brodie et al., 2011; Kosiba et al., 2018).

Corporate Social Responsibility and Customer Engagement

CSR is one of the relationship fostering strategies that has attracted substantial research attention in the service sector (Raza et al., 2020). Given its context-specific nature, its conceptualization is hard (Raza et al., 2020; Uhlig et al., 2020; Wood, 2010). In this study, CSR includes the three dimensions of the “triple-bottom-line concept such as economic, environmental, and social responsibility” (e.g., Dahlsrud, 2008; Park et al., 2015). Recently, CSR has emerged as a specific marketing instrument for firms to build lasting relationships with customers, create value, and enhance competitive advantage (Farooq & Salam, 2020; Lee, 2019; Raza et al., 2020). Indeed, one of the foremost findings of CSR studies is that customers seek to reward socially responsible firms (Abbas et al., 2018; Sen et al., 2006). This assertion appears to be consistent with the stakeholder theory. According to the stakeholder theory (Freeman, 1984), the strength of the stakeholder-firm relationship directly impacts stakeholders’ (i.e., customers) “attitudes and behaviors” (Bhattacharya et al., 2009). Therefore, customers being one of the corporation’s most significant stakeholders among the different stakeholder groups (Park, 2019), reward corporations that engage in CSR activities and programs via favorable evaluations, and higher intent to buy their services and products (Karaosmanoglu et al., 2016; Sen et al., 2006).

Furthermore, researchers argue that when companies work for the well-being of the community through their CSR initiatives, customers are more likely to become emotionally involved with such corporations (Abbas et al., 2018; Lichtenstein et al., 2004). Similarly, scholars claim that CSR generates a sense of belief that companies want the welfare of stakeholders, and that companies do not seek to exploit others (Martínez & Rodríguez del Bosque, 2013). Consequently, customers tend to trust and have confidence in socially responsible companies and feel safe in building relationships with them, including becoming more and more open to such companies (Badenes-Rocha et al., 2019; Lichtenstein et al., 2004; Raza et al., 2020; Sen et al., 2006). Moreover, theoretically, van Doorn et al. (2010) argue that when consumers see a firm as more reliable, they are more in the cards to show engagement behaviors. Considering that CE is a psychological/emotional process in which trust is a critical element (Bowden, 2009), CSR is expected to shape CE.

In the service context, empirical studies have identified that CSR enhances customer satisfaction, brand identification, customers’ trust, customers’ attitude, and brand loyalty (Badenes-Rocha et al., 2019; Martínez & Rodríguez del Bosque, 2013; Park, 2019; Raza et al., 2020). For example, Park (2019) found that CSR activities significantly influence customer satisfaction and customer attitude in the airline service industry. Despite these advances, however, not much is known about how a firm’s CSR activities evoke positive customer responses in the insurance marketing literature. Specifically, the few existing studies on the nexus between CSR and CE have reported mixed results. That is, while Badenes-Rocha et al. (2019) did not find any substantial relationship between CSR and CE, studies by Jarvis et al. (2017), Chomvilailuk and Butcher (2018), and Abbas et al. (2018) found CSR to significantly shape CE. Based on the above discussion, we propose that a life insurance company’s engagement in CSR will create an environment that is fitting for reinforcing customers’ interactions and engagement with their brands. Thus, we propose the following hypothesis:

Corporate Social Responsibility and Customer-Brand Identification

CBI reflects a cognitive self-categorization in which consumers connect to an organization. Researchers have acknowledged that social identity theory or SIT is an important theoretical base for marketing-based CBI (e.g., Lam et al., 2013; Rather & Hollebeek, 2019; Raza et al., 2020). According to SIT, individuals will spend considerable effort to build their own social identity, along with their further private identity (Bhattacharya & Sen, 2003; Rather & Hollebeek, 2019; Tajfel & Turner, 1986). CBI arises via a cognitive classification development where people place themselves as affiliates or members of a firm. In this sense, members underline their similarities to other members and their dissimilarities from non-members (Hollebeek, 2018; Martínez & Rodríguez del Bosque, 2013; Prentice et al., 2019; Rather, 2017). So, through the consciousness of belonging and perceived link to a firm or an object (e.g., a brand), people can attain a positive social identity (Kreiner & Ashforth, 2004; Rather & Camilleri, 2019; Rather & Hollebeek, 2019). Besides, Scott and Lane (2000) emphasize that individual-firm identification can also happen even when the people are not formal members of the firm. In this regard, consumers want to describe themselves by articulating socially identifying connections (Hur et al., 2018; Martínez & Rodríguez del Bosque, 2013; Rather et al., 2019b).

CSR is suitable for enriching general trust toward a firm (Aaker, 1996) and is particularly precise in shaping customers’ affective responses, including identification (Pérez et al., 2012). For this reason, several prior studies (e.g., Badenes-Rocha et al., 2019; Lichtenstein et al., 2004; Marin & Ruiz, 2007; Raza et al., 2020) claim that one of the best ways in stimulating a brand or CBI is CSR communication. Furthermore, the literature suggests that CSR tends to exert a considerable positive effect on consumers’ attitudes and behavior toward the focal brand, such as brand identification. Likewise, past studies reveal that CSR is the most significant antecedent of CBI (Huang et al., 2017; Hur et al., 2018). In this regard, a firm’s engagement in CSR activities shows its identity and values, permitting customers to relate the firm with their own identity (Lichtenstein et al., 2004). Besides, identification with a firm that is intensely engaged in CSR activities may provide consumers with high self-esteem as regards their social and ethical image (Bhattacharya & Sen, 2003; He & Li, 2011; Hur et al., 2018; Raza et al., 2020). In addition, the direct nexus between CSR and CBI has been confirmed by studies in a different context, including the banking sector (Hur et al., 2018; Pérez et al., 2012; Raza et al., 2020), the hotel industry (Badenes-Rocha et al., 2019; Martínez & Rodríguez del Bosque, 2013), and mobile telecommunications (He & Li, 2011). While these studies have shown the existence of a strong link between CSR and CBI, there is a lack of empirical proof about the dynamics depicting this relationship in the life insurance sector. Hence, consistent with existing studies, we posit that life insurance firms’ CSR activities will shape customers’ affective responses like CBI. Thus, we propose the following hypothesis:

Corporate Social Responsibility and Customer Satisfaction

Customer satisfaction is regarded as an important construct that plays a significant role in marketing practice (Rather, 2019; Yang et al., 2017). Customer satisfaction signifies an emotional state arising from customers’ evaluation of a service supplied by a firm and their response to it (Park et al., 2017; Rather, 2019). Similarly, it is viewed as a measure of how services/products provided by a firm meet or exceed customers’ expectations (Saeidi et al., 2015). For this reason, satisfaction is argued to be determined generally by the quality of customers’ experience and communication with the service provider (Crosby et al., 1990). The related literature shows that customer satisfaction has the potential to influence consumer relationship consequences, including customers’ readiness to purchase, corporate reputation, and customer loyalty (Park, 2019; Saeidi et al., 2015; Su et al., 2016; Yang et al., 2017).

CSR, according to Brown and Dacin (1997), creates a favorable environment around the firm, thereby stimulating the production of more effective judgments regarding the service experience. Past studies have reported a positive association between CSR activities and customer satisfaction (e.g., He & Li, 2011; Martínez & Rodríguez del Bosque, 2013; Park, 2019; Park et al., 2017; Pérez et al., 2012; Saeidi et al., 2015). The possible reasons for this positive relationship between CSR and customer satisfaction are the following: First, a firm’s consumers could be potential or actual stakeholders who are not only concerned about the economic value of consumption, but also care about the overall standing, including the social performance of the firm (Luo & Bhattacharya, 2006). Second, Consumers are largely more likely to be satisfied when the products or services are provided by a more socially responsible firm (He & Li, 2011; Lee, 2019). Third, it is argued that a firm’s robust CSR record generates a favorable image that positively enriches customers’ assessment of the firm and their attitudes toward the firm (Martínez & Rodríguez del Bosque, 2013; Sen & Bhattacharya, 2001).

Furthermore, CSR is a core part of corporate identity that can influence consumers to identify or classify themselves with the firm. As such, these consumers are more probable to be satisfied with what the firm offers or provides (Bhattacharya & Sen, 2003). Also, perceived value is regarded as an essential driver that stimulates customer satisfaction (Mithas et al., 2005). All things being the same, customers are more likely to derive perceived value and greater satisfaction from products or services offered by a socially responsible company (i.e., the added value gained via good social causes; Luo & Bhattacharya, 2006). CSR has been found to have a positive effect on customer satisfaction in prior studies (e.g., He & Li, 2011; Lee, 2019; Park, 2019; Saeidi et al., 2015). Based on the above, we hypothesize the following:

Customer-Brand Identification and Customer Engagement

CBI refers to a resilient psychological or emotional connection, which is suggestive of future behavior and long-term relationship (Rather et al., 2018; So et al., 2013). Brands or firms (e.g., hospitality and tourism brands) have extensively employed branding strategies to differentiate their products/services from those of their competitors. This is indicative of the particular relevance of CBI in exploring customer-brand interactions (Rather et al., 2018; So et al., 2013). Consistent with SET, customers feel the need to assist a firm if they perceive it to be doing well in terms of economic, social, and environmental responsibility (Badenes-Rocha et al., 2019). Furthermore, the theoretical work of van Doorn et al. (2010) suggests that CBI can have a positive influence on CE. However, empirical evidence of this suggested relationship is inadequate (Rather et al., 2018; Tuskej & Podnar, 2018), particularly in the insurance marketing literature. Prior empirical research has confirmed that customers who identify with brands enhance their engagement with those particular brands (Badenes-Rocha et al., 2019; Dessart et al., 2015; Rather & Camilleri, 2019; Rather et al., 2018; Romero, 2017). Based on these, we expect that customers’ identification with a particular life insurance brand can impact their engagement with such a brand. Thus, we propose the following hypothesis:

Customer Satisfaction and Customer Engagement

Customer satisfaction, as described earlier, is a positive affective state ensuing from consumers’ overall evaluation of their experience with a firm’s services or products. One of the salient drivers of CE that has been highlighted in the existing literature comprises attitudinal precursors like customer satisfaction (Palmatier et al., 2006). Similarly, Higgins and Scholer (2009) examined customer satisfaction as a crucial determinant of engagement and considered it indispensable if a high level of satisfaction is to be maintained over time. Again, van Doorn et al.’s (2010) theoretical work lends credence to this assertion as these researchers suggested that CE is motivated and driven by customer satisfaction. Thus, a higher degree of customer satisfaction with a brand, product, or service will more likely trigger a higher level of CE toward the brand or firm. Indeed, empirical studies show that customer satisfaction significantly influences CE (Cambra-Fierro et al., 2016; Dessart et al., 2015). So, it is expected that customers’ satisfaction with life insurance firms’ services and products or brands may influence their engagement with these brands. Hence, we propose the following hypothesis:

Mediating Effects

Customer satisfaction and CBI have been identified in the existing literature as critical variables that add to company success and performance by facilitating the connection between predictor constructs and outcome variables, including service brand loyalty (Martínez & Rodríguez del Bosque, 2013). Whereas customer satisfaction mainly represents a customer’s emotional state or condition resulting from his or her subjective assessment of experience from consumption associated activities (Oliver, 1997; Park et al., 2017), CBI reflects a mental state of self-categorization, association, and closeness of a customer to a brand or company (Bhattacharya & Sen, 2003; Hinson et al., 2019; Prentice et al., 2019; Rather, 2020).

Similarly, Lichtenstein et al. (2004) have established that CBI mediates the pathway from CSR to consumers’ purchase behavior. Furthermore, Hur et al. (2018) have indicated that CBI mediates the link between CSR and customer citizen behavior. In addition, Cambra-Fierro et al. (2016) found that complaint-handling satisfaction plays a mediating role in the relationship between perceived effort and CE. In addition, both CBI and customer satisfaction have been established as mediators in the link between CSR and loyalty (Martínez & Rodríguez del Bosque, 2013; Raza et al., 2020). More recent research also indicates that CBI and customer trust mediates the link between CSR and CE (Badenes-Rocha et al., 2019). Given that there is scant empirical proof on the mediating role of CBI and customer satisfaction in the nexus between CSR and CE, we suggest the following hypotheses:

Figure 1 illustrates the study’s proposed research framework.

Research framework.

Method

Measures

The study adopted existing well-validated multiple indicators (see the appendix) and used a 5-point Likert-type scale to gauge the degree of agreement for each item, starting from 1 = strongly disagree to 5 = strongly agree. The five items measuring CSR were adopted from the works of Martínez and Rodríguez del Bosque (2013) and Park et al. (2015). Three items measuring CBI were sourced from Stokburger-Sauer et al. (2012) and Rather (2017). Furthermore, we measured customer satisfaction following three items provided by Pérez et al. (2012) and Yang et al. (2017). CE was gauged by five items taken from the studies of Rich et al. (2010) and Kosiba et al. (2018).

A pre-test was initially done with two university lecturers and one PhD student to establish the face and content validity of the survey questionnaire. After that, we carried out a pilot test with 40 life insurance customers to assess the questionnaire regarding clarity, wording, relevancy, and time expended. Most of the participants assured the researchers that the questionnaire was clear and understandable. Furthermore, we tested for Cronbach’s alpha for all the items used in the questionnaire, and the values were higher than 0.70 (Nunnally, 1978).

Sampling and Data Collection

Data were collected through a survey administered to customers of life insurance companies in Ghana. The participants of this study were customers from branches of 10 life insurance companies in three regional capitals such as Accra, Takoradi, and Kumasi selected based on size and popularity. We chose these cities because most of the life insurance companies in Ghana have their offices situated in these cities. The study focused on the life insurance sector because it is crucial to financial development in any economy (Ghosh, 2013), including Ghana. In recent years, the sector has become competitive, and it is a flourishing one with massive growth potential in Ghana. In addition, insurance firms [life] also engage in various CSR initiatives (e.g., awareness campaigns toward climate change, donations to sporting activities, and contributions to communities) that cover their corporate obligations to different stakeholders (e.g., customers, government, and the society) that are interested in CSR issues.

Consistent with past studies (Narteh et al., 2013; Rather, 2019; van Tonder & Petzer, 2018), a convenience non-probability sampling approach was used to select participants for the study. To screen our participants, three opening questions were used to ensure that (a) the respondent has had a policy with a particular life insurance company for at least a year, (b) the respondent was aware of the CSR initiatives of his or her insurer, and (c) the respondent was above 18 years. Customers who answered “yes” to all three questions participated in the survey. The questionnaire was written in English. To enhance the participation of customers, the study’s aim was explained to the customers we approached. Also, they were assured of confidentiality. The survey was carried out during the period from November 13, 2018, to December 13, 2018. We did not offer participants any incentives. Out of the total 320 distributed questionnaires, 293 valid responses were collected for the final analysis. The sample (see Table 1) indicates an equal distribution across the cities (Accra, 34.5%, Takoradi, 33.1%, and Kumasi, 32.4%). The sample comprised 170 (58%) males and 123 (42%) females. Table 1 gives the full details of the participant’s profile.

Demographic Profile of Participants.

Data Analysis and Results

The investigations involve a two-step technique of structural equation modeling (SEM) to examine the data and then test the proposed research hypotheses (Anderson & Gerbing, 1988). The data analysis was done using SPSS AMOS, version 24.0 (maximum likelihood estimation).

Measurement Model

A confirmatory factor analysis (CFA) and reliability tests were done on the items to assess the psychometric properties of the constructs used in this study. Accordingly, two items (CSR4 from the “corporate social responsibility” construct and CE6 from the “customer engagement” construct) were deleted due to low factor loadings (George & Mallery, 2006) (see the appendix). Subsequently, the model showed an acceptable fit to the data. The χ2/df was 2.534, and the values for root mean square residual (RMR) and root mean square error of approximation (RMSEA) were 0.023 and 0.072 correspondingly. Also, the goodness of fit index (GFI), normed fit index (NFI), relative fit index (RFI), incremental fit index (IFI), and comparative fit index (CFI) values were all higher than 0.90. Besides, the adjusted goodness of fit index (AGFI) value was above 0.80. So, following the assessment criteria proposed by Bagozzi and Yi (1988), these fit indices show a satisfactory model fit.

Reliability and Validity

The results demonstrate that all the constructs in the study attained adequate reliability levels based on composite reliability (CR) values surpassing 0.70, as suggested by Fornell and Larcker (1981). In addition, the latent constructs’ Cronbach’s alpha coefficients ranged from 0.801 to 0.909 (Table 2). Next, a convergent validity check was performed, and as displayed in Table 2, the AVE ranged from 0.605 to 0.714. All the standardized factor loadings were above 0.50, starting from 0.702 to 0.896, suggesting convergent validity is achieved (Anderson & Gerbing, 1988). Moreover, the squared root of the average variance extracted for every construct was above the inter-correlation coefficients with other corresponding constructs, supporting the discriminant validity of the constructs in our proposed model (Fornell & Larcker, 1981; Hair et al., 2014) (Table 2).

Results of the Confirmatory Factor Analysis.

Common Method Bias (CMB)

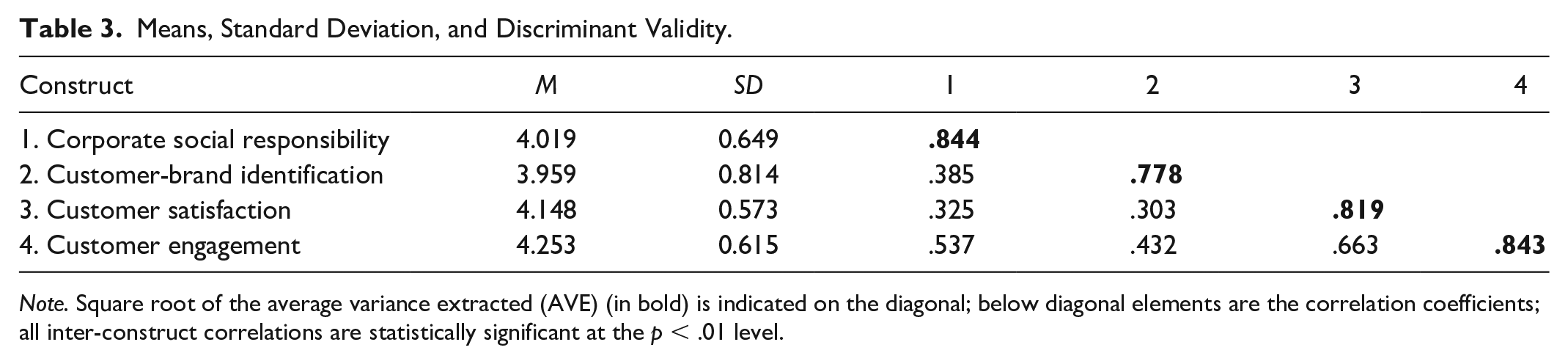

In checking for the presence of CMB, Harman’s one-factor technique was first utilized. An exploratory examination of the data revealed the nonexistence of a single factor explaining the majority of variance among the measures. So, in this study, CMB was not a challenge or concern (Podsakoff & Organ, 1986). Second, CMB is not likely if correlations are not very high (i.e., below 0.90; Hair et al., 2010). The correlation matrix (see Table 3) shows that CMB is not a concern in this study since there are no very high correlations.

Means, Standard Deviation, and Discriminant Validity.

Note. Square root of the average variance extracted (AVE) (in bold) is indicated on the diagonal; below diagonal elements are the correlation coefficients; all inter-construct correlations are statistically significant at the p < .01 level.

Structural Model

The study’s hypotheses (Table 4) were tested using AMOS, version 24.0 (maximum likelihood estimation). The fit indices of the structural model were found to be within their suggested values as follows: χ2/df = 2.776, RMR = 0.029, RMSEA = 0.078, GFI = 0.930, AGFI = 0.883, CFI = 0.956, NFI = 0.934, RFI = 0.907, IFI = 0.956, and Tucker–Lewis index (TLI) = 0.938, showing a good model fit. The study’s model explains 57.2% of the observed variance R2 (Figure 2).

Standardized Path Coefficients.

Note. C.R. = critical ratio; CSR = corporate social responsibility; CE = customer engagement; CBI = customer-brand identification.

p < .05. **p < .01. ***p < .001.

Results of the framework.

Hypothesis Testing

Figure 2 and Table 4 give an overview of the results of the hypothesis testing. The results illustrate that all the paths are significant. Specifically, CSR has significant impacts on CE (β = 0.282, CR = 4.284, p = .000), CBI (β = .396, CR = 5.129, p = .000), and customer satisfaction (β = .356, CR = 4.649, p = .000), so H1, H2, and H3 are supported. In the same way, CBI showed a significant effect on CE (β = .176, CR = 3.066, p = .000). Also, customer satisfaction proved to have a salient effect on CE (β = .537, CR = 8.229, p = .000). As a result, H4 and H5 were both accepted.

Mediating Effects Testing

In testing the mediating effects, we examined the covariance structural model by following the bootstrap approach (Zhao et al., 2010). Brown’s (1997) approach to determining direct, indirect, and total effects was followed as well. In this sense, mediation exists if an independent variable influences a dependent variable at the same time that it impacts the mediator, which likewise affects the dependent variable (Hair et al., 2010; Rather & Hollebeek, 2019). As Table 5 reveals, both CBI and customer satisfaction exhibited a mediating effect in the link between CSR and CE, with customer satisfaction showing a stronger mediating influence. Also, we applied the bootstrap mediation test to produce an empirical sampling distribution of the mediated impact, calculating parameters and generating a 95% confidence interval from the bootstrap samples (Preacher & Hayes, 2008), a method that has been used by Cambra-Fierro et al. (2016) and Yang et al. (2017). “When an interval for a mediating effect does not contain zero, the indirect effect is significantly different from zero with 95% confidence level.” As Table 6 indicates, in the confidence intervals found, the value zero is not contained in the relationships CSR→CBI→CE and CSR→Customer satisfaction→CE, hence we can conclude that the indirect effects are significant.

Direct and Indirect Effect.

Note. CSR = corporate social responsibility; CBI = customer-brand identification; CE = customer engagement; CS = customer satisfaction.

p < .001.

Mediation Analysis (Bootstrap Test).

Note. IV = independent variable; M = mediator; DV = dependent variable; CI = confidence interval; CSR = corporate social responsibility; CBI = customer-brand identification; CE = customer engagement; CS = customer satisfaction.

Discussion and Implications

CE is ever more becoming a significant topic in marketing discussions and even more in service brands context (Leckie et al., 2016; Rather, 2019). At the same time, the literature highlights the growing significance of CE as a strategy essential for nurturing customer relationships (Rather, 2019; Rather & Sharma, 2017). Accordingly, our study explored the link between CSR and CE and the mediating role of CBI and customer satisfaction. The main results of our study are threefold. First, in the context of life insurance, CSR impacts CE. This result is consistent with previous studies that show that CSR is an important driver of CE (Abbas et al., 2018; Jarvis et al., 2017). This indicates that CSR generates an emotional connection with the firm and consumers feel like part of it. Thus, they see the firm as a dependable partner and build positive feelings for it and their devotion toward the firm rises and they subsequently become more engaged (Abbas et al., 2018; Lichtenstein et al., 2004; Pérez & Del Bosque, 2015). By validating CSR as a precursor of CE, our study empirically confirms prior conceptual results (van Doorn et al., 2010).

Second, we found that CSR influences CBI. This result is consistent with prior studies that suggest that CSR is an important antecedent of CBI (e.g., Badenes-Rocha et al., 2019; Hur et al., 2018; Martínez & Rodríguez del Bosque, 2013; Raza et al., 2020). Similarly, we found that CSR significantly impacts customer satisfaction. Again, this finding is consistent with past studies (Lee, 2019; Park et al., 2017; Saeidi et al., 2015). Furthermore, we established that CBI enriches CE. Thus, our study’s finding is in line with prior research that shows that CBI is a fundamental emotional process that helps to enhance customers’ engagement with a firm or brand (Hinson et al., 2019; Rather & Camilleri, 2019; Rather et al., 2018). In addition, our study found customer satisfaction to be a predictor of CE which agrees with past studies (Cambra-Fierro et al., 2016; Palmatier et al., 2006). This indicates that customers’ satisfaction with a firm’s product and services motivates them and increases their engagement with the firm.

Finally, our findings revealed that CBI and customer satisfaction mediate the link between CSR to CE. By empirically validating the mediation role of both CBI and customer satisfaction in the link between CSR and CE in the life insurance context, our study contributes to the marketing and insurance literature.

Theoretical Implication

Theoretically, this study contributes significantly to the CSR and CE literature in several ways. First, this study linked CSR to CE. Despite the growing importance of CE, it has received little attention in the CSR literature (Abbas et al., 2018). Although past studies have investigated the effect of CSR on customer outcomes, their focus was mainly on service quality, trust, and customer loyalty (e.g., He & Li, 2011; Martínez & Rodríguez del Bosque, 2013; Raza et al., 2020). This current study offers empirical evidence on the link between CSR and CE, thereby replying to a recent call for attention from Abbas et al. (2018). The empirical linkage between CSR and CE is consistent with previous research (Jarvis et al., 2017).

Second, this study also contributes to the insurance marketing literature by studying the link between CSR and CE and exploring CBI and customer satisfaction as mediators in a unique specific service context (life insurance). To the best of our knowledge, no past study has examined the interrelationship among these constructs from an insurance marketing perspective. Previous studies connecting CSR to CE via other intervening constructs such as trust, CBI, and e-service quality, to mention a few, originated from contexts such as banking (Abbas et al., 2018), hotel (Badenes-Rocha et al., 2019), football club (Jarvis et al., 2017), and mobile telephone service providers (Chomvilailuk & Butcher, 2018). Therefore, our study answers call from researchers (Abbas et al., 2018; Badenes-Rocha et al., 2019; He & Li, 2011; Hur et al., 2018; Jarvis et al., 2017) for more investigations into customer responses to CSR from different contexts around the globe. Specifically, in the context of life insurance, our study provides strong empirical evidence of the significance of CBI and customer satisfaction as mediators of the connections between CSR and CE. Thus, given CE’s key contribution to firm performance (Brodie et al., 2011; Rather et al., 2019a), CSR, CBI, and customer satisfaction should be fostered to help CE’s development, thereby adding valuable information to the understanding of customers of this market.

Third, although customers also engage with product or services brands offline (Islam & Rahman, 2016; Rather, 2019), past studies on CE have largely focused on online context (e.g., Brodie et al., 2013; Islam et al., 2018; Solem, 2016), thereby making the CE construct underresearched in an offline setting. Therefore, exploring CE with service settings (life insurance) in an offline setting is an additional contribution of this study. Thus, the study responds to a call from Kosiba et al. (2018) for the investigation of CE in the insurance marketing context as it is one of the most underresearched areas. In addition, our study also answers calls from several researchers (e.g., Hollebeek, 2018; Islam et al., 2019; Kumar et al., 2019; Rather & Sharma, 2019) for further study of CE in different contexts.

Finally, this study was carried out in a specific geographic location on the African continent (Ghana), thereby providing a significant addition to the CSR and CE literature, which is dominated by insight from advanced economy context to date (Abbas et al., 2018; Kosiba et al., 2018; Rather et al., 2019a; Raza et al., 2020). To some extent, the customer consumption and engagement of insurance services have been affected due to the high customer uncertainty about insurance products/services, particularly in emerging markets where the settlement of claims is at times challenging (Agyei et al., 2020; Kosiba et al., 2018). Therefore, this study will assist life insurance marketers to craft marketing strategies that will drive customers to engage with their brands. Furthermore, CSR awareness is on the rise (Karaosmanoglu et al., 2016), and customers, including life insurance customers in emerging markets, are welcoming it. Our findings empirically confirmed that CSR engenders emotional attachment with a brand. Therefore, this will help insurance marketers to devise effective means to communicate their CSR activities to their customers.

Managerial Implication

In addition to the above theoretical contributions, this study as well provides some managerial implications. First, our findings show that life insurance firms benefit from being socially responsible as CSR was found to significantly impact CE. Thus, customers’ perceived CSR of life insurance firms influences them to engage with their brands. In this sense, managers and marketers of life insurance firms should bring into line their CSR and engagement strategies to become more effective in building strong relationships with customers which will increase customers’ engagement with their service or brands (Abbas et al., 2018). Furthermore, life insurance firms’ managers should consider CSR not only as means to enhance their corporate reputation or brand image but also as a strategic marketing tool that is part of their customer interaction management (Hur et al., 2018) to motivate and elicit favorable customer responses toward their firms or brands.

Second, life insurance marketers should take a critical look at their CSR communications as they play an important role in getting their CSR activities and programs to their customers and the public at large. Considering that CSR awareness is still somewhat low (Chomvilailuk & Butcher, 2018), life insurance managers and marketers should structure their CSR communications effectively to get their CSR activities across to their most important stakeholders (i.e., customers). This can be achieved through effective communication of their CSR activities via more full channels, including CSR reports, TV, websites, and newspapers (Raza et al., 2020). Customers’ increased awareness of their actual involvement in CSR activities will most likely trigger a more favorable response such as enhanced CE with their brands or service. In addition, life insurance firms need to activate their CSR activities and programs by offering their customers the chance to participate in such activities through volunteering and donations, thereby allowing them to express their support for the program and its benefits (Park et al., 2017; Raza et al., 2020).

The findings of the study also highlight the important role of CBI and customer satisfaction in shaping CE. This indicates that life insurance managers should pay special attention to their CSR activities and focus on aspects that customers can identify with, which in turn, will make them see the brand as part of themselves (Rather & Hollebeek, 2019; Sprott et al., 2009). Again, CSR communication is key here. So, life insurance managers should formulate their CSR communication strategy in ways that can drive customers to identify themselves with their firm or brands (Abbas et al., 2018) Thus, they can employ mediums such as social media platforms (e.g., Facebook, Twitter, and Instagram) and mobile apps to build and promote CBI and emotional connections with their brands (Badenes-Rocha et al., 2019; Rather & Camilleri, 2019; Raza et al., 2020).

Finally, the findings of our study show that customer satisfaction improves CE. This suggests that life insurance firms should focus on meeting and surpassing customers’ expectations. Meeting and surpassing customers’ expectations will give rise to customer satisfaction with the service encounter which will result in overall customer satisfaction and consequently increase their engagement with life insurance brands (van Tonder & Petzer, 2018). In addition, life insurance managers should pay special attention to the quality of every customer’s experience of their services or products (Pérez et al., 2012; Yang et al., 2017). For example, they should invest in training their workers and studying customers’ needs. This way, life insurance managers can monitor their employee’s aptitude to satisfy their customers’ needs and provide them with sufficient guidelines to help and support customers to maximize their service experiences.

Limitation and Future Study Direction

The study has some limitations which provide an avenue for future research. First, the study focused on only participants recruited from life insurance firms in Ghana, which diminishes external validity. Future research needs to test our model in other contexts, and preferably in other countries (developed vs. developing) to validate the external validity of our study’s findings. Next, this study treated CSR as a single construct, thereby ignoring its multidimensional nature, which is acknowledged in the CSR literature (Dahlsrud, 2008; Park, 2019). So, future scholars can improve on the conclusion reached in this article by investigating how the different dimensions of CSR (i.e., economic, social, and environmental responsibility) influence CE and the mediators included in this study. Finally, our proposed model employed only CSR, CBI, customer satisfaction, and CE-based insights in the life insurance context. Future research can include other different and emerging constructs, including value co-creation, service innovation, service failure, service quality, customer experience, commitment, trust, and loyalty to examine the predictive power of the model (Hollebeek & Rather, 2019; Rather et al., 2020; Shams et al., 2020).

Footnotes

Appendix

Scale Items and Source.

| Construct and items | Source |

|---|---|

CSR4 ABC life insurance makes effort to create new jobs |

Martínez and Rodríguez del Bosque (2013), Park et al. (2015) |

| Stokburger-Sauer et al., (2012), Rather (2017) | |

| Pérez et al. (2012)

, Yang et al. (2017) |

|

CE6 I find it difficult to detach myself when I am interacting with ABC life insurance company. |

Rich et al. (2010), Kosiba et al. (2018) |

Note. CSR4 and CE6 were removed due to low factor loadings.

Acknowledgements

We thank the anonymous reviewers for their invaluable comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.