Abstract

The sustainable economic role of the financial markets is essential for a trade-dependent economy such as China. Notably, the Chinese financial market has shown some unpleasant trends over the past two decades, coupled with the mounting national debt. Most of the earlier literature on the impact of the sovereign credit rating (SCR) on the financial market development (FMD) of China is confined to the event study approach, which provides policy input for short-term decision making. In this scenario, it is worthwhile investigating how the SCR asymmetrically affected the FMD of China and the threshold point (level) where the relationship of SCR-FMD turns non-linear. The Non-Linear Autoregressive Distributed Lag model’s empirical findings show that the reaction of FMD to SCR disclosure is asymmetric. In addition, the result of the threshold estimator finds a single threshold level of 3.628 above which the relationship of SCR-FMD turns non-linear. It is important to note that up to a threshold of 3.628 the coefficient is −.516 and −.627 which turns positive afterwards, no matter whether the variation explained is relatively less with the coefficient of .058 and .056 respectively. This implies that policymakers and regulators need to consider this benchmark of 3.628 to formulate future policy matters related to the equity market.

Keywords

Introduction

Credit rating appears to be an incredibly focused industry, while Standard & Poor’s (S&P), Moody’s, and Fitch are collectively known as the big three in the field of credit rating. The latest statistics show that the big three credit rating agencies (CRAs) control around 95% of the rating business. S&P and Moody’s market share is 40% each, while Fitch accounts for only 15% (CFI, 2020). CRAs play a vital role in the financial markets, by assessing the likelihood of an entity (an economy/company) to honor its debt obligations as agreed. These agencies have the most significant impact when assigning a credit rating to a country because it can be said that the country’s ability to borrow ultimately affects its overall economic policy. The aim of CRAs is to reduce the asymmetrical information between investors and issuers. Schmukler (1999) argues that changes in the SCR encourage both the stock market and the country risk—such a change provides borrowers and lenders with an indication of a corporation’s risk profile, enabling them to determine the risk premiums.

The SCR acts as a credit passport to disclose investors’ credit quality for succeeding in the broader capital markets. Williams et al. (2013) recommend that SCR agencies should manage access to financial markets for participants. McLean et al. (2012) advise investors to promote reliable information regarding share prices and reduce financial barriers through dynamic investment based on SCR information. Similarly, accounting information is useful to financial accounting, standard-setting bodies, and equity investors (Al-Baidhani, 2018; Al-Baidhani et al., 2017).

Owing to the critical role of CRAs in the financial sector, this study examines the influence of sovereign credit rating (SCR) changes on the Chinese financial market development. For this purpose, S&P and Moody’s credit outlooks are considered. Fitch is not included for estimation due to its similar outlook grades to S&P. This is a crucial question to be answered in the context of China because developed economies slowed down after being strategically sidelined by China’s low cost of labor. This eventually pulled manufacturing to China; thus, the Chinese government become indebted. According to a report released by the Institute of International Finance (IIF, 2020), the country’s total corporate, household and government debt has reached 335% of GDP in the second quarter of 2020 and accounts for around 15% of all global debt. Figure 1 shows the change in percentage points of debt to GDP ratio in the second quarter of 2020, where China is at the top with the cumulative points of households, non-financial firms, and the government.

Debt-to-GDP ratio (change in percentage points 2020Q1).

Drawing on the ongoing discussion, this research is an effort to answer the following questions: 1. Is the impact of SCR announcements on the Chinese FMD non-linear? 2. At what threshold does SCR start to have a negative effect on the Chinese FMD?

By empirically answering these questions, this work contributes to the financial market literature on non-linear and threshold horizons.

To empirically answer the first question, this study uses the asymmetric modelling (Non-linear Autoregressive Distributed Lag—NARDL) of Shin et al. (2014), which determines the non-linearity and collectively analyzes the short- and long-run asymmetry between impulses. This method enables us to model the co-integration and asymmetric dynamics collectively between variables. The advantage of the NARDL approach is that not all relevant variables need to be I(1). As long as they are not I(2), co-integration tests can be performed. The NARDL methodology validates hidden co-integration between drives that linear models usually escape. Based on these advantages, NARDL estimation makes it possible to identify the asymmetric relationship between the stock market and its underlying determinants. The current study extends the financial market literature, subject to an SCR’s asymmetric impact on China’s financial market and transmission of changes in related determinants to the stock market using the NARDL model. To obtain empirical support for the second question, we estimated the threshold model (Hansen, 1999, 2000), identifying the point where non-linearities exist.

Based on overall findings, we suggest that stakeholders consider the asymmetric and threshold dynamics in decision making. Overlooking the non-linear association of the FMD in response to the SCR may be misleading, because of drastic changes in financial and economic conditions, especially when studying dynamic relationships. In addition, bond market participants, investors, and regulators may consider these asymmetries a necessary input in decision making and policy matters.

The rest of the paper proceeds as follows: Section 2 reviews the classic literature on financial development, the linkage of financial market development with sovereign credit ratings, and other macro variables with financial market development. The methodology is covered in Section 3. Section 4 presents the empirical results, and these are discussed in Section 5. Section 6 concludes the article.

What Do We Know About Financial Development?

This section initially overviews the classic literature on financial development, and its economic dynamics, followed by specific empirical literature on sovereign credit rating and financial market development. The section is concluded in the form of the hypothesis statement.

Financial system development is widely studied in financial literature as an indicator of economic growth (Kapidani & Luci, 2019). Classic literature (Cole & Park, 1983; M. Fry, 1984; M. J. Fry, 1984; Fry, 1986; Goldsmith, 1969; John, 1993, 1988; McKinnon, 1986; McKinnon, 1989; Ronald, 1973; Rostow, 1971; Shaw, 1973) has unfolded the dynamics of financial development in economic structure and evolution. Financial development can be attributed to transferring property into an unidentified arrangement of an unregistered and unpaid financial claim (Ronald, 1973; Shaw, 1973).

Cole et al. (1983) described the evolution of the Korean financial system and post-WWII monetary policy perspectives, highlighting the government’s bureaucratic role in using the financial system to distribute funds. It also shows how unregulated financial markets have mitigated the effects of government intervention and redesigned financial resources with more dependent principles. M. Fry (1984) and Goldsmith (1969) are among pioneers in presenting an econometric linkage of financial development with overall economic development. Fry (1986) highlighted the structural differences between Asian financial systems and those in developed western countries, which he argued have had a significant impact on financial innovation in Asia and found financial markets to be more oligopolistic in developing countries in Asia than in developed countries. Rostow (1971) documents that the process of economic growth can usefully be focused on a relatively short interval of two or three decades when the economy and the society of which it is a part change in such a way that economic growth takes place automatically.

Levine (2005) argues that well-developed financial systems remove the barriers to external finance that firms face, thus highlighting a mechanism by which financial growth affects economic growth and that both financial intermediaries and markets are essential for growth. A comprehensive review of China’s financial system by Allen et al. (2012) reveals that the stock market’s role in allocating resources to the economy has been limited and inefficient.

In the global competitive environment, analyzing financial markets’ efficiency is valuable (Fakhry et al., 2018). Allen et al. (2004) examined different risk scoring models and suggested that these models allow lenders and regulators to develop portfolio accumulation techniques to measure exposure to retail credit risk. Allen et al. (2012) recommend policies that will help maintain steady economic growth in China and reduce the likelihood of a financial crisis, such as a banking crisis, a real estate crisis, or a stock market crash. John and John (1991) have shown that organizing the financing of a project, where the maximum amount of debt is allocated to the sponsoring company and the new project, reduces the agency’s cost and increases the value of tax shields. The maximum amount of loans to finance a project is allocated to the sponsoring company and the level of loans for the new project is equal to their individual maximum capital structure.

How Is Financial Market Development Linked With Credit Rating?

Stock prices are substantially correlated with SCR disclosure (Ng & Ariff, 2019). The literature on the effects of the SCR on the financial market is scant, focusing primarily on emerging markets like China. The stock market is considered one of the active indicators of a country’s real economic activities. It is observed that stock markets are more sensitive to SCR degradation in bordering countries, especially during a crisis. China suffered significant losses during the Asian financial crises (Li et al., 2008; Murcia et al., 2013). The authors examined the impact of the SCR on the equity prices of Brazilian public listed companies and proved that the rating announcement contains valuable informational content, leading to abnormal stock market returns, especially when “bad news” floats in the market. Reisen and Von Maltzan (1999) have reported that the boom-bust cycle in the stock markets is highly vulnerable to the rating news. This argument shares the view that the country’s ratings provide fresh information to the financial markets.

Improvements usually occur during periods of financial market unification, while downgrades arise during a market downturn. Specifically, Huang et al., (2018) investigate how the bond rating downgrades, in the context of China, influenced the stock prices during the period from January 2008 to May 2016. Poon and Chan (2008) use aggregated time- series cross-section rating data from 170 companies registered on the Shanghai and Shenzhen Stock Exchanges from January 2002 to July 2006 to investigate the certification results of the initial rating announcement and the signal impact of the rating downgrade in China. The empirical results support that SCR announcements by various CRAs contain substantial information value, and the market is sensitive to such announcements and responds accordingly. Charoenwong et al. (2004) examined the impact of variation in the Iranian Stock market rating by employing event study methodology and evidenced that only downgrades contain useful information about the stock market. Hammoudeh et al. (2013) researched the BRICS countries and indicated that Chinese stock markets are the ones sensitive to political risk.

SCR takes careful consideration when evaluating sustainable corporate performance (Cubas-Díaz & Martínez Sedano, 2018). Subaşı (2008) investigates the sovereign rating and examines the impact on stock returns, exchange rates, and volatility in Turkish markets. He found that sovereign rating downgrades have a little negative effect because they predict rating changes in post-announcement periods while the rating upgrades do not create a significant market impact.

Lee et al., (2016) analyze the impact of SCR changes on equity liquidity in 40 countries between 1990 and 2009 and find that effect is more robust with a downgrade than an upgrade, and the event is not linear in size. Using credit rating as a measure of credit risk, Nedumparambil and Bhandari (2020) examine the existence of a risk-return puzzle in India between July 2011 and March 2019. Contrary to the asset valuation theory, there is a negative relationship between risk and return.

Sensoy et al. (2016) find that the combined impact of both rating announcements does not have a significant influence. However, individual analysis reveals that Moody’s announcements are far more influential. Their results identify that any shock due to the variations in SCR is usually less likely to spread. Brooks et al. (2004) investigate the impact of SCR change on home country financial market return. They reported that SCR news impacts the home country and international bond markets and portfolios. An SCR improves emerging economies’ capability to capture the global market by attracting foreign investments (Andritzky et al. 2007; Bissoondoyal-Bheenick & Brooks, 2015; Kim & Wu, 2008). Kräussl (2005) consider the role of SCR agencies in global financial markets using an event study approach and reveal an enormous impact on the bond market’s size and volatility. Ismailescu and Kazemi (2010) affirm that upgrade announcements may spill over into emerging economies more than downgrade news. Afonso et al. (2012) demonstrate the evidence of notable impacts from SCR news for the bond, while Sori et al. (2019) show that the effect of the downgrade is more obvious than that of the upgrade.

Treepongkaruna and Wu (2012) examine the outcome of different SCR announcements and their spillover impact on stock and currency markets in the Asia-Pacific region during the Asia Financial Crises from 1997 to 2001. They argue that currency and stock markets react differently to rating announcements. Another group of researchers, for example, Kliger and Sarig (2000), Goh and Ederington (1993), Holthausen and Leftwich (1986), Hand et al. (1992), and Poon et al. (2008), interrogates whether changes in the SCR influence stock and bond prices. These studies use event study methods to analyze the instant effects of SCR pronouncements on security price variations.

The reviewed literature suggests that the impact of SCR upgrades and downgrades are not the same. As a result, the following hypotheses are proposed.

Hypothesis 1: Sovereign credit rating announcements have a non-linear relationship with the Chinese financial market development.

Hypothesis 2: What is the threshold point, where the relationship of sovereign credit rating announcements to Chinese financial market development turns non-linear?

What Are the Other Determinants of Financial Market Development?

Earlier literature reveals that financial development is explained by several factors. Among them, the most common regarding emerging and developing countries include economic development, trade openness, inflation, banking development and investment (Li et al., 2019). These are explained here concisely.

Economic development

This factor signifies the natural strength of a sovereign’s economy as this is essential for determining a country’s pliability or shock-absorption capability (Lennkh & Moshammer, 2018). The most important measure for this economic analysis is based on a country’s income level, measured by the GDP per capita. This initial outcome is adjusted by the economic growth factor and is captured by GDP per capita trend growth, which summarizes the credibility of a sovereign on a single industry or sector (van Damme & van Paridon, 2016). A highly developed financial system helps improve capital formation and resource distribution proficiency and encourages economic development (Hondroyiannis et al., 2005; Levine & Zervos, 1999). Widening economic activities give rise to an essential need for financial products and services, resulting in extending the banking sector and capital markets to match rising demand. Therefore, we include economic growth as an essential control for financial market development.

Trade openness

International trade drives employment and generates the formation of capital which gives rise to high living standards with a higher GDP and GDP per capita. Trade openness enhances the productivity of resource allocation, speeds up technological development, expands a country’s market size and thus may enable domestic firms to gain economies of scale (Alesina et al., 2000; Shahbaz & Rahman, 2010). The presence of the correlation between financial market development and trade openness may be linked by two different means, which can be defined as “supply-side” and “demand-side” roles. Rajan and Zingales (2003) point out the “supply-side” part of interest groups. They argue that trade openness has a beneficial influence on financial market development. It disables the rewards of financial intermediaries when blocking financial market development to diminish entry and competition. Therefore, trade openness expands investment and banks’ lending, thus improving financial market development. Therefore, we study trade openness as an essential control for financial development.

Inflation

According to Bittencourt (2006), inflation positively affects financial development because of the low macroeconomic operation. Almalki and Batayneh (2015) applied time-series data from 11 MENA region countries to investigate the influence of inflation rate on the financial sector performance using GMM methodology. Their results show that inflation had a negative and significant impact on financial sector development. They indicate that a minimal increase in inflation was powerless to stock market performance and banking sector development nevertheless of inflation. Wahid et al. (2011), Odhiambo (2012), and Ozturk and Karagoz (2012) examine the impact of inflation on financial development by using the ARDL bound testing approach and Error Correction Model. Their outcomes suggest that the relationship between inflation and financial development was negative in the short and long run, verifying that inflation diminished the efficiency of financial sector performance. Hence, inflation is a part of research because of its effect on the stock market.

Bank development

Claessens and Laeven (2005) point out that, in the banking sector, “the capacity of competition is an essential feature of financial sector functioning” and, in conclusion, “international financially dependent regions develop faster in the most-competitive banking system.” Benczúr et al. (2019) conclude that “bank credit and debt security have a considerably negative influence on growth, at the same time stock market financing have a substantially positive impact. By focusing on high-income countries from OECD, they conclude that the latter is more salutary for growth, at least in high-income economies.” Thus, banking development is a crucial section of research keeping in observe its impact on financial market development.

Investment

The financial sector’s importance is mostly described in economics research, through its promotion of investment through capital accumulation and technological innovation that then affects growth (Levine, 1999). According to Schumpeter (1912), the importance of the banking system in economic growth and development is universally accepted; financial institutions encourage innovation and creativity and strengthen future growth by determining and funding productive investment. Padilla and Mayer (2002) suggest that the countries whose economies expand more rapidly are forced to pledge more investment in enhancing their financial system to stabilize their economic conditions.

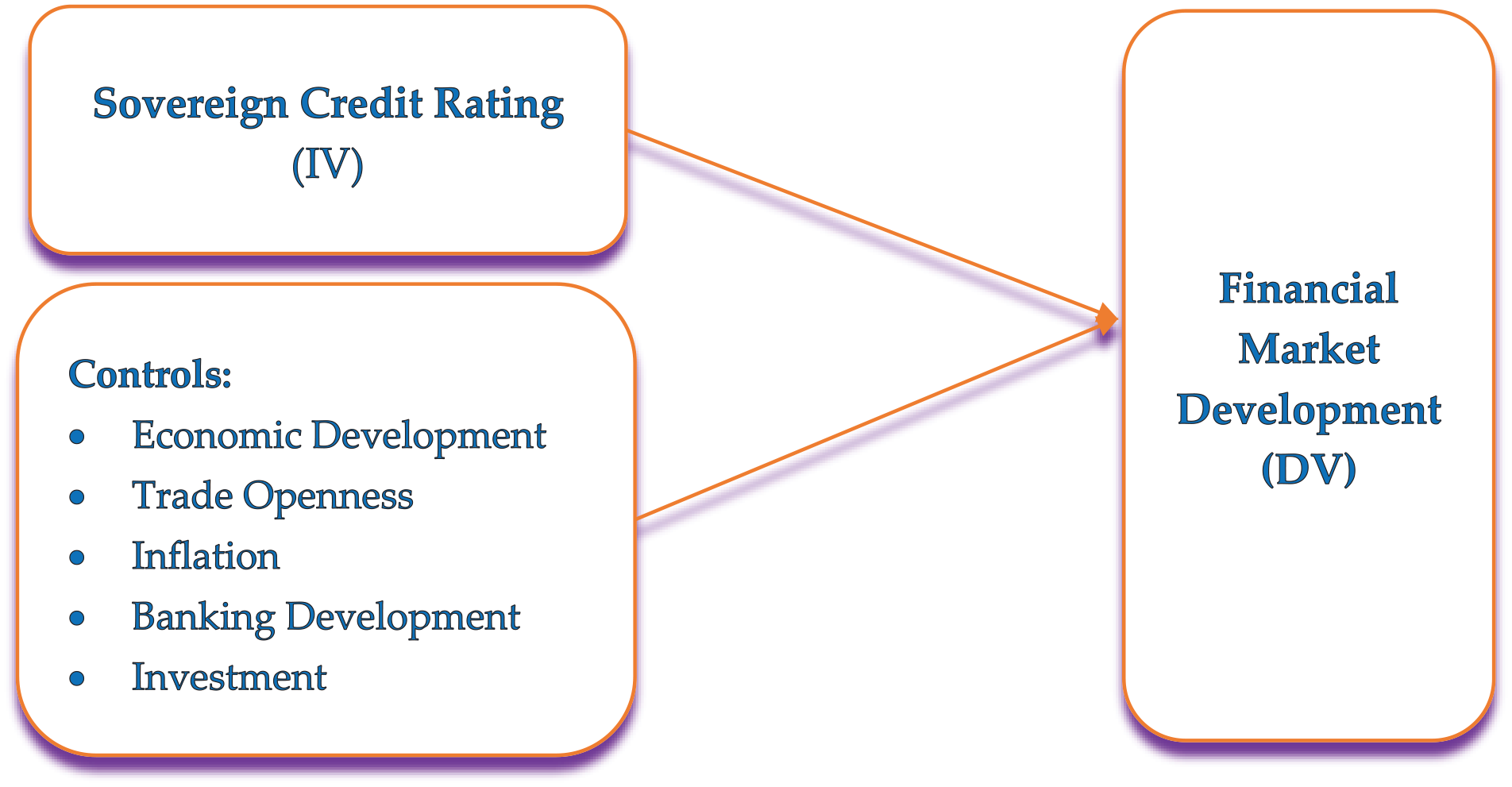

Figure 2 illustrates the theoretical framework for the present study. It draws on the famous risk-return theory (Markowitz, 1991) and its controls follow Li et al. (2019). Here sovereign credit rating is an independent variable, and financial market development is the dependent variable. Controls include economic development, trade openness, inflation, banking development, and investment. All the variables are defined and explained in detail in the methodology section.

Theoretical framework. IV: independent variable, DV: dependent variable.

The next section lays out the methodological foundations of the study.

Data Sources, Variables, and Methods

Data and Variables

The objective of the current study is to investigate the asymmetric impact of the SCR on the Chinese financial market, for which we use yearly time series data from 1980 to 2018, as per the data availability. Thus, there are overall 39 observations to be estimated, which differs across alternative measures. The study uses the asset pricing theory of risk and returns to model the impact of the SCR on FMD. The risk-return function holds that the associated risk determines return. Drawing on this function, we define SCR as the risk of failure to meet the obligations when they come due, and return is broadly defined as an improvement in the FMD. Our dependent variable FMD is a composite index of financial market depth, access, and efficiency. It ranges from 0% to 100%. We transformed to the natural logarithm. A high score shows more remarkable development of the financial market based on underpinned indicators, and a low score indicates a low level of such development. The data on FMD is assembled from the International Monetary Fund, which is publicly available at https://data.imf.org/?sk=F8032E80-B36C-43B1-AC26-493C5B1CD33B.

The explanatory variable, SCR grades, is sourced from the periodical outlooks of Standard & Poor’s and Moody’s and numeric weights based on the trading economic benchmark (https://tradingeconomics.com/china/rating). The weight ranges between 0–100, the highest score depicting a low level of default risk of a country, whereas the lowest score makes it vulnerable to default risk. The study uses ratings given by two agencies: Standard & Poors’ and Moody’s. Following Li et al. (2019) these grades are numerically transformed into a natural logarithm for convenient interpretation.

Lee et al. (2016) argue that the macroeconomic environment is vital in explaining how changes in an individual state’s credit rating affect financial market activities. To be consistent with the empirical literature in controlling the macroeconomic environment, we follow recent related literature (Li et al., 2019) and include economic development, openness, inflation, bank sector development, and investment as potential controls. Economic development substantially determines the volume of economic activities and the resulting standard of living of respective citizens. Both the supply-driven and demand-following hypotheses, state that development fosters financial activities. It is measured by the natural logarithm of GDP per capita. Openness provides the opportunity to the citizens/businesses of a country to be involved in international trade (import and export activities) which calls for financial channels to help settle the transactions. This implies that the ability to trade internationally enhances the level of FMD. Openness is measured as the natural logarithm of the sum of the exports and imports ratio to GDP.

Inflation is another macro indicator that influences the financial market activities through saving and investment channels. It is measured by the natural logarithm of the consumer price index. The development of the banking sector plays a supportive role in all types of financial market activities; therefore, we include it as a determinant of FMD and proxy it by the natural logarithm of the domestic credit ratio to the private sector to GDP. Finally, we include investment as the last control, which shows the conducive investment environment of an economy. Individuals and businesses with savings are free to convert them to various profitable investments activities. We measure this by the natural logarithm of the gross fixed capital formation ratio to GDP. The data on all these controls are sourced from the World Development Indicator of the World Bank. This database is also publicly available and broadly used in related research. The descriptive statistics of all variables are given in Table 1.

Description and Summary Statistics of Key Variables.

The NARDL technique has recently gained popularity and has been applied in various fields such as agricultural economics (Mitra, 2014), environmental economics (Ahmad et al., 2018, 2019) and energy economics (Atil et al., 2014). The methodology of the NARDL technique provides flexibility to the integration order of impulses, that is, it can be practiced whether variables are I(0)/I(1) or a combination of both (Shin et al., 2014). Prior to the evaluation of both NARDL techniques, some pre-tests are necessary. Unit root testing is a useful tool in deciding which estimator is suitable for performing a co-integration test. The first generation unit root tests, like Dickey and Fuller (1981) and Phillips and Perron (1988) have been extensively used, but these tests assume no structural break. The results of the ADF test may render biased results which makes the estimation less reliable. To overcome this problem, we use the structural break unit root test formulated by Zivot and Andrews (2002). The result for each variable is reported in Table 2.

Unit-Root Test Results.

Note. Significance is tested using p-values of .01, .05, and .10, ***, **, and * denote significance at respective p-values.

Method

The classic Markowitz model (Markowitz, 1991) revolutionized empirical finance by providing a theoretical framework for analyzing risk and return and the relationships between them. Statistical analysis is commonly used to measure risk and mathematical programming for the efficient selection of assets in a portfolio. The classic Markowitz risk-return model is at the core of building theoretical foundations for the present study. Markowitz models return as a function of risk, which is shown in Eq. 1.

Here return represents the yield on security (typically a financial asset—equity stock). Risk is denoted as the probability of losing the expected return which may result from fluctuations in economic conditions. We expand the definition of return into broader terms to capture improvement in all aspects of the financial market, denoted by FMD in Table 1. Similarly, the risk originating from fluctuations in the SCR fits into the broader perspective of Markowitz’s risk definition. Thus, equation (1) is rewritten as:

Where LnFMD is a function of LnSCR. To be aligned with the objective of the study, the risk-return function is further extended to add control variables aligned with Li et al. (2019), and written as under:

All the acronyms used in equation (2) are defined in the variables’ description (Table 1).

Linear ARDL framework

The autoregressive distributed lag (ARDL) method (Pesaran et al., 2001) has been widely employed to investigate the short-run and long-run nexuses between study variables. This approach is flexible if there is any co-integration existence among variables at various levels as modelled by Pesaran and Pesaran (2010). The ARDL method has greater flexibility, and it can be applied to series with a non-identical order of integration, that is, I(0) and I(I), and it is found efficient in case of small sample size as well (Banerjee et al., 1998; Ehigiamusoe et al., 2019; Khan et al., 2019; Khan & Khan, 2019; Pesaran et al., 2001).

The following specifications has been formulated to test the ARDL bounds testing approach:

We determine the optimal lag in an unrestricted error correction model by applying the Schwartz information criterion (SIC). All variables given in the above error-correction equation are supposed to have a linear effect on output (FMD).

Non-linear ARDL framework

Since there may be non-linearities present in time series, we conduct the current study in non-linear settings to focus on the long- and short-term asymmetries among variables. The linear ARDL is extended to asymmetric ARDL by Shin et al. (2014). It is also referred to as non-linear ARDL (NARDL). The current research aims to investigate the asymmetric (non-linear) long-run and short-run relationships among the SCR and FMD. Moreover, NARDL does not need the same order of integration among the studied variables. It can be exercised regardless of the regressor’s order of integration, whether it is I(0) or I(1). It is based on the current contemporary advances in the field of error-correction models and co-integration methodology. To investigate the symmetric and asymmetric impacts of SCR, we follow Shin et al. (2014) and distinguish between upgrades and degrades. First, we make changes in the real SCR as ∆LnSCR+ which includes positive upgrades denoted by ∆LnSCR and negative downgrades denoted by ∆LnSCR−. We then create two new series, one referred to as upgrades (denoted by POS) and other referred to as downgrades (denoted as NEG). These changes are described as the partial sum of positive and negative changes. respectively, and given as below:

The NARDL framework by Shin et al. (2014) then endorsed the asymmetric error correction model as follows:

Specification (5) represents an error correction model (ECM) which Shin et al. (2014) call an asymmetric (non-linear) NARDL specification, due to the mechanism of creating partial sum variables (Pesaran et al., 2001). Once equation (5) is estimated, and the long-run relationship is established, the various hypothesis regarding the asymmetric impact of SCR changes on the performance of FMD can be determined. We can assess three types of asymmetries. First, short-run asymmetry is determined if

Threshold Regression

Although NARDL specification uncovers the important dimensions of the connection of SCR and FMD, it does not give any insight into the minimum level of SCR as a threshold may be where non-linearities appear. For this purpose, we use robust threshold regression to provide a threshold level where the linear relationship turns into non-linear. In such a situation, a threshold model (Hansen, 1999, 2000) is suitable for tracing the turning points (coefficient change). Thus equation (5) specifies the single threshold regression setting used in this study.

In equation (6),

Results

Table 2 reports the unit root test results for the Dickey-Fuller and Zivot-Andrews tests, respectively. In the existence of a single structure break, all the variables have unit roots in their levels, as shown in Table 2. Zivot et al. (2002), using structural break unit root tests, show that SCR, ED, TO, INF and BD have unit roots in their levels in the presence of a single structure break except for FMD and INV. This provides evidence that all the variables are integrated of 1(1) except for FMD and INV, 1(0). Likewise, in 2007, the structural break happened because the Chinese financial market was primarily affected by government policy and the global financial crisis. Similarly, in 1989, the structural break was found to be due to the destruction of capital control and market crash effects of 1987. Both tests show a similar output except for INV. The unit root test results furnish a strong explanation for the use of the ARDL and NARDL model, as all variables are on the 1(1) and 1(0) level and none were found to be 1(2).

In the next phase, to examine the difference between upgrade and downgrading, we estimate the non-linear ARDL model (Shin et al., 2014) for both SCR outlooks. The long-run coefficient results in Table 3 indicate that SCR upgrades bring a positive change to FMD, and a downgrade is followed by an adverse change in the long run when S&P’s outlook is used to measure SCR. Using Moody’s perspective, both upgrades and downgrades negatively hamper the Chinese FMD in the long-run. The short-run dynamics are consistent in S&P, while Moody’s rating explains prosperity in the Chinese financial market. The findings gain support from related literature. For example, Bales and Malikane (2020) using panel data under volatility settings document an asymmetric effect of rating changes on the Asian region’s stock volatilities. The authors find that CR downgrades significantly influence the volatility, while CR upgrades have no such volatile effect. The empirical results calculated by t-statistics

Non-Linear Impact of SCR on FMD.

Note. Significance is tested using p-values of 0.01, 0.05, and 0.10, ***, **, and * denote significance at respective p-values. Dt represents the structural break dummy in FMD.

The results of asymmetric dynamics in Table 4 show that asymmetric cointegration exists between study variables. Notably, both the SCR outlooks note that the effect of an upgrade and downgrade is not the same. These novel findings give valuable policy insight to investors, regulators, and other stakeholders. Furthermore, these results prove the significance of considering asymmetry while investigating the nexuses between SCR and FMD.

Asymmetric Dynamics and Diagnostics Test of NARDL.

Note. Significance is tested using p-values of .01, .05, and .10, ***, **, and * denote significance at respective p-values.

Importantly, in addition to the non-linear coefficients of SCR

Threshold Analysis

Table 5 incorporates the single threshold output and diagnostic statistics. Interestingly, under both SCR measures, we find a single threshold of 3.628 above which the relationship of the SCR and FMD turns non-linear. It is important to note that up to a threshold of 3.628 the coefficient is −.516, and −.627 which turns positive afterwards, no matter whether the variation explained is relatively less with the coefficient of .058 and .056, respectively. This implies that policymakers and regulators need to consider this benchmark of 3.628 to influence equity markets positively. For a convenient interpretation, locate the original SCR score of S&P grade BB+ and Ba2 assigned by Moody’s. These grades designate a stable outlook, below which there is a negative grade of BBB− (S&P) and Ba1 (Moody’s). This implies that in future if the Chinese economy receives S&P BBB− and Moody’s Ba1, regulators may have to monitor the debt servicing more carefully and possibly take immediate measures to reduce the debt level. Figure A3 graphically illustrates the threshold level using S&P data for the estimation period. The blue line represents the threshold value of 3.628, below which the creditworthiness of sampling entity leads towards the probability of default.

Threshold Regression Results.

Note. ***, **, and * denote significance level at 1%, 5%, and 10%, respectively.

Discussion

SCR is gaining importance in the worldwide capital markets as it portrays the credit risk of peculiar debt securities and provides credit information to the market participants. An SCR agency considers the creditworthiness of a defaulter, principally, a business corporation, or a government’s ability to pay interest on their borrowings and the contingency of omission. Investors are concerned with such announcements for learning vital information to make investment decisions beyond the borders (as the Chinese stock market offers B-shares to foreigners).

The negative reaction of FMD to SCR can probably be explained because a credit upgrade signifies the low level of a default risk of a country, which eventually decreases the risk premium that composes an integral part of the security prices. On the contrary, upgrading in SCR also influences fixed-income securities and turns them into a low-cost source of finance for firms in that country, which turns the focus from equity market securities to bond markets.

Therefore, in the long-run stock traded volume reduces. On the contrary, we see that both types of SCR announcements positively drive the FMD in China. This signifies that improvement in credit outlook enhances investors’ confidence to participate in trading activities, which eventually uplifts the stock market capitalization and volume of trading activities. Hence, the Chinese stock market thrives in the short run. There is one more reason for this short-run raise, which is that most of the Chinse stockholders are small investors (those who bought A-shares), who are sensitive to the new information. A positive view from Standard & Poor’s and Moody’s given them the confidence to trade actively, while an increase in trading volume enhances the stock market index.

These findings of a threshold effect of SCR can be valuable, as the investor will likely react to any fresh update regarding rate changes. In the context of the current study, it can be assumed that these factors are firmly fixed in the political, financial, and economic risk components. It is possible to predict a significant relationship between a SCR announcement and FMD using a non-linear framework.

Conclusions

In this article, we answer three essential questions identified in the previous literature. First, whether there exists a long-run relationship between SCR and FMD in the context of China. Secondly, whether the reaction to changing SCR is symmetric or asymmetric. Thirdly, what the threshold level (point) where the relationship of SCR and FMD turns non-linear. We extend the financial market modelling by using non-linear and threshold specifications. The NARDL results demonstrate an asymmetric impact of SCR variations on FMD in both the short run and long run. Under NARDL specification, the results vary across the SCR measurement. It signifies that stakeholders like analysts, investors and regulators may consider these asymmetries in the nexuses between SCR and FMD while interpreting the sovereign rating announcements, as these may not carry uniform implications. Moreover, the current study is subject to several limitations for example it does not consider the SCR scores given by domestic SCR Agencies. In the future, an endeavor to evaluate local SCR in asymmetric perspectives may provide useful policy implications, while the asymmetric setting may also be extended to the forex market.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the major project of Education Department of Hebei Province: ZD201904.