Abstract

COVID-19 has spread across the globe at a shocking level and significantly affects the world economy. The pandemic has significantly impacted rural households, the primary workforce for industrialized urban areas, in every sector of rural businesses, including agriculture. Furthermore, the dearth of employment in the primary industry has also adversely influenced rural inhabitants’ livelihood and financial decisions. COVID-19 changed the perception of people regarding their income and expenditure. This study is intended to analyse the transformation of savings and spending of rural households during COVID-19. A questionnaire was developed using a Likert scale to elicit study variables, and the collected data were analysed using structural equation modelling. The results showed that all types of savings had a positive and significant relationship with the savings motive of rural households during COVID-19. Further, customary and spontaneous spending had a positive and significant relationship spending pattern of rural households. Rural inhabitants were interested in compromising their spending and other forms of savings to have more emergency savings. Earlier studies have examined either the savings or the spending pattern of rural households, and studies on both savings and spending by rural households are very few. The present study thus adds to the existing literature in the field.

Introduction

The Corona Virus Disease 2019 (COVID-19) is an infectious disease caused by a novel virus affecting the human respiratory system. The first case was reported in Wuhan, China, in late 2019 (Chakraborty & Maity, 2020). The epidemic of COVID-19 gradually spread around different parts of the world and was declared a pandemic later. To slower the spread of COVID-19, the Government of India imposed a countrywide lockdown from March 25, 2020, in different phases. As an outcome of the lockdown, many people lost their jobs, and thereby their income went down. A statistic by the Centre for Monitoring Indian Economy (CMIE) stated that the Indian unemployment rate increased by 20% due to the pandemic. It is even more in the case of Tamil Nadu, where the rate was 49.8%. Due to job loss and salary cuts, people are forced to use their savings or borrow. For example, from April to July, employees withdrew around 30,000 crores from their provident fund. It clearly shows how badly the workforce has been financially affected. A report by McKinsey stated that almost one-fourth of households reduced their expenditure, and around 36% of people reduced their savings because of COVID-19 (Mckinsey, 2020). The spread of COVID-19 created a panic. In large numbers, people responded by stocking up essentials and purchasing medical goods like masks and hand sanitiser along with relevant household essential products.

The government-led lockdown has had a widespread impact on rural households in India, even though the pandemic affects all spheres of human life, both urban and rural. Businesses and other economic activities have been highly affected due to social distancing restrictions and fear of spreading the virus. Lockdown, travel restrictions, and suspension of commercial activities have interrupted rural inhabitants’ financial planning considerably (Haleem et al., 2020). The pandemic has had a significant effect on rural households in every sector of diverse rural businesses, including agriculture. Furthermore, the dearth of employment in the primary sector also influenced rural inhabitants’ livelihood and financial decision-making. Comparatively, rural households have miserable income-earning opportunities than their urban counterparts. Therefore, awareness on overcoming such economic fallacy due to such pandemic has been increased among rural households. During the pandemic time, they have more intention to save money than spend on different household necessities (Geetha & Vimala, 2014). Still, during this pandemic, people started to purchase & store essential items and withdraw savings from banks due to the disrupted supply chain. COVID-19 has opened its eyes to the importance of savings. Under such situations, savings will support overcoming unforeseen problems prevailing in the nation. Savings is the outcome of abstaining from current consumption for future needs (Athukorala & Sen, 2004). Rural households believe it is ideal for saving a portion of money by cutting unnecessary expenses associated with routine life (Amu & Amu, 2012).

COVID-19 spread across the globe at a shocking level. It was an unprecedented disaster and thus called for extraordinary measures. It significantly affected the world economy and hit both service and manufacturing sectors alike, heavily affecting employment. Its impact on susceptible persons and families already financially broken may broaden the disparity gaps and even lead to deficiency (Kumar et al., 2020). In India, roughly two-thirds of the population lived in rural areas and had limited earning opportunities during this period. The actual economic impact is yet to be fully revealed as search for income could lead to the spread of the virus and has been limited or nonexistent. As a result, the deceleration in the growth of GDP could be significant. Intense progress of the pandemic and a lack of earning opportunities directly force rural inhabitants to save money rather than spend (Lai & Tan, 2009). The rural population already has a savings plan for different purposes, but still, this pandemic signals a red alert to save money for emergency needs (Niculescu-Aron & Mihăescu, 2012). The savings habit among the rural residents has always been influenced by protective and wealth accumulation motives and not for emergencies (Hafeez et al., 2010), but COVID-19 has changed the attitude of rural households towards building up emergency savings.

The savings motive of rural people can be three ways: emergency savings, precautionary savings, and secured life savings (Canova et al., 2005). Emergency savings is for food and health requirements and personal well-being. Precautionary savings is for peaceful retirement life, kids future and insurance against unexpected events (Kennickell & Lusardi, 1998). Similarly, people use secured life savings for financial autonomy, luxury aspiration, and investments (Ramakrishna, 2007). The sudden lockdown due to COVID-19 brought routine life to a halt and distressed all economic activities. It restricted movement from one place to another, creating a labour shortage, which stopped factory functioning, disrupted logistics, and closed essential services.

Further, it triggered a panic buying among consumers in purchasing essential goods for food and shelter. At the same time, this was possible when one had enough money. But many rural inhabitants struggled a lot in purchasing essential goods because of lack of income during the lockdown. They were reluctant to withdraw and use money from the pool of savings set apart for protective and wealth creation purposes (Shahbaz & Mahmood, 2004). They were further limited by the closedown of banks and other financial organizations to withdraw money. This made them consider the importance of keeping ready cash or liquid resources to overcome such difficulties for everyday living in a short period. This made them think about the importance of keeping ready money to overcome such challenges for regular life in the short run rather than in the long run. Hence, they were willing to cut a portion of savings devoted for precautionary and secured life purposes and channel into emergency savings. During the pandemic, they transformed their savings preference to emergency needs such as food, health, and personal well-being (Prema-Chandra & Pang-Long, 2003). After the pandemic spread in India, the money required for spending is the only aspect chanted among the rural population.

The spending habit of the rural population can be classified into two ways: customary spending and spontaneous spending. Day-to-day spending can be associated with cooking, contingent household expenses and other shelter-oriented purposes. However, unplanned spending is medical requirements, auspicious events and repayment of the loan (Brown & Taylor, 2006). The real motivation of the study is to examine the impact of the pandemic on the savings and spending of rural households. The ambition and aspiration in terms of savings and spending may differ from person to person. During the pandemic period, income opportunities are limited. Under such circumstances, how they are allocating priority to save or spend money is a great question. Our study helps find a precise picture of how the rural population repurposed its savings patterns and how they cut their spending to protect their life by accumulating savings for COVID-19 situations. Earlier studies have examined rural households’ savings and spending habits at the normal condition, and studies on both savings and spending by rural households are very few. Further savings and spending by the rural households under uncertain times are very few. The present study thus adds to the existing literature in the field

Theoretical Development

Savings Motive

Emergency savings

Emergency savings can perform as a protection against unexpected income drops. It works as a financial cushion in terms of food security, housing stability, medical care, and utility needs of practical life (Gjertson, 2014). People can use the money saved today to meet emergency needs tomorrow. In this way, they mainly save money for education, marriage, business, and household expenses (Girija & Kalaivani, 2018). Savings also assist in reducing expenses involved in routine life and enable family well-being (Pathy, 2017).

Medical expenditure and income-earning capability significantly influence the savings behavior of households in rural areas (Gedela, 2012). During the pandemic, many rural families lost their jobs that affected their earning capability (Williams & Kayaoglu, 2020), and their savings patterns may vary. Further, financial attentiveness through savings is considered a pivotal contributor to overcoming a financial emergency (Babiarz & Robb, 2014). This indicates that food, health, and well-being are significant factors in rural households’ emergency savings. Emergency savings help rural families to manage financially in critical and emergencies. At the same time, income-earning capability also decides the savings pattern. This leads to the first issue in this study: emergency savings influence the savings motive, and the following hypotheses are proposed:

H1: Food, health and well-being are the basis for emergency savings among rural households.

H2: Emergency savings have a direct and significant impact on the savings motive of rural households.

Precautionary savings

Preparing for a possible short-term oscillation is the primary motive for rural households for precautionary savings. However, the prudent reason for saving has a significant share of total savings (Carroll & Samwick, 1997). Rural homes are more inclined towards financial asset saving than physical asset saving (Kesavan et al., 2012) and save in bank deposits, life insurance and post office scheme but not in other financial assets like shares, mutual funds and government securities. It ensures liquidity and a stable savings avenue for precaution purposes (Umesha & Nelakanta, 2019). Savings for long-term perspectives such as retirement and investment plans are challenging to meet by the low-income household during emergency times (Bernheim et al., 2001). Families with more education orientation spend more because they have to spend money on child education and basic needs (Abid & Afridi, 2010). It can be seen that precautionary savings are mainly induced by retirement planning, insurance and children’s future in terms of their education, marriage and career planning. People save money as a precaution, and during emergencies, they postpone their saving for preventive purposes and use it for emergency needs. Therefore, we can conclude that during such times, rural people postpone their precautionary savings. Hence the following hypotheses are framed:

H3: Retirement, kids’ future and insurance are the bases for precautionary savings among rural households.

H4: Precautionary savings have a direct and significant impact on the savings’ motive of rural households.

Secured life savings

Savings are needed for clothing, family functions and emergency requirements, followed by child education and a secured future (Ramaratnam & Jayaraman, 2016). Further, Savings directly provide several advantages for rural households and increase their wealth (Kibet et al., 2009). Savings behavior is influenced by household financial planning and financial literacy (Payne et al., 2014). Investment availability, incentives and information are the main factors influencing rural and low-income individuals (Chowa et al., 2012). Rural households use savings for the construction of the house, financial freedom and protection, wealth creation and safety against natural disasters (Selvakumar et al., 2012). Investors preferred to invest in real estate, gold and jewellery and bank deposits to ensure the safety of their investment. They make investments for life security and wealth creation (Lokhande, 2015). It is ascertained that financial autonomy, luxury aspiration and investments are the motives behind secured life savings. Studies found that people can minimize secured life savings to strengthen their food and health needs in emergency times. Thus, the following hypotheses are proposed.

H5: Financial autonomy, luxury aspiration, and investments are the basis for secured life savings among rural households.

H6: Secured life savings have a direct and significant impact on the savings motive of rural households.

H7: Savings motive has a direct and significant impact on the financial planning of rural households.

Spending Pattern

Customary spending

The COVID-19 pandemic created supply-side shock initially but owing to panic buying by consumers, it morphed into a demand-side shock later. High uncertainty and strict lockdown measures have people saving by cutting their spending in the short term. Moreover, the government’s direct contribution in the form of free ration as a short-term relief helped them cut their spending significantly (Vadivu & Annamuthu, 2020). Spending is always influenced by the priority of food and other household expenses (Hayhoe et al., 2000). People prioritize purchasing essential goods like food commodities, medicines and other necessary products (Furnham, 1999) during the emergency time. During the lockdown, consumer behavior was affected mainly by food requirements because of living habits (Durante & Laran, 2016). Consumers have decreased their expenditure involved purchasing food products in stores (Jung et al., 2016). Due to safety concerns and strict lockdown measures, people can only leave their homes for emergency needs. This pandemic has impacted the frequency of grocery purchases among consumers (Jribi et al., 2020). Therefore, it is understood that customary spending money is associated with regular cooking, household consumption and sheltering. Accordingly, we propose the following hypotheses:

H8: Cooking, household consumption and shelter are the bases for customary spending among rural households.

H9: Customary spending has a direct and significant impact on the spending pattern of rural households.

Spontaneous spending

The significant share of consumption is the non-food item in spontaneous spending. Expenditure on education is main among different expenses incurred by the households (Patrick, 2015). People find it difficult to spend on pleasure and self-gratification during periods of financial deficiency (Yeoman, 2011). Consumers shelve their luxury needs during such times. Instead, they purchase essential commodities for immediate consumption by changing their behavior and mindset related to spending requirements (Tsai, 2005). In emergencies, people focus on their health by avoiding harmful work, food and climatic conditions. They take medical advice or treatment in extreme circumstances (Eng & Bogaert, 2010). It can be seen from the discussion that medical requirements, auspicious events and lavish spending account for most of the spontaneous spending of rural households. So, the following hypotheses are proposed.

H10: Medical requirements, auspicious events and lavish spending are the bases for spontaneous spending among rural households.

H11: Spontaneous spending has a direct and significant impact on the spending pattern of rural households.

H12: Spending pattern has a direct and significant impact on the financial planning of rural households.

Methodology

The primary purpose of this study is to examine the transformational impact of COVID-19 on the savings’ motive and spending patterns of rural households in Tamil Nadu, India. The sample for the study includes rural inhabitants. Collecting data from rural households poses many challenges like language barriers, lack of education, and getting correct responses, particularly their income and savings (Cheema et al., 2018). The researcher collected the data only from educated rural people to overcome these issues, with the questionnaire prepared in the local language using Google Forms. Further, the questionnaire was distributed only among the rural inhabitants who could operate smartphones, had experience in savings and spending, and the key decision-makers in the family were approached for data collection. The participants were assured that their data would be kept in confidence and would never be shared. The size of the population is infinite; hence 385 samples were planned (Cochran, 1963). Initially, 311 respondents participated in the study online across Tamil Nadu during May 2020. However, the responses received included 26 responses that were not fully answered, 23 came from urban households, and 12 were from migrated respondents. These responses were eliminated from the study, and the remaining 250 responses were considered for analysis. Purposive sampling was used to identify the sample, and the study was formulated using an exploratory research design. The questionnaire was designed with a five-point Likert scale, where five meant completely agree, and one meant completely disagree.

Before the actual survey, the questionnaire was pre-tested with 20 rural inhabitants and word usage, the scale and measurement items were finalized with field experts and academic professionals. Subsequently, changes were made to the questionnaire (Annexure I reproduces the finalized questionnaire). The study employs structural equation modelling (SEM) to evaluate how rural households transformed their savings and spending behavior during COVID-19. AMOS version 22.0 software was used to perform confirmatory factor analysis (CFA) and SEM. In SEM, the association between theoretical construct and objectives of the study was authorized by the path coefficients between the factors.

Results and Discussion

Socio-Economic Background

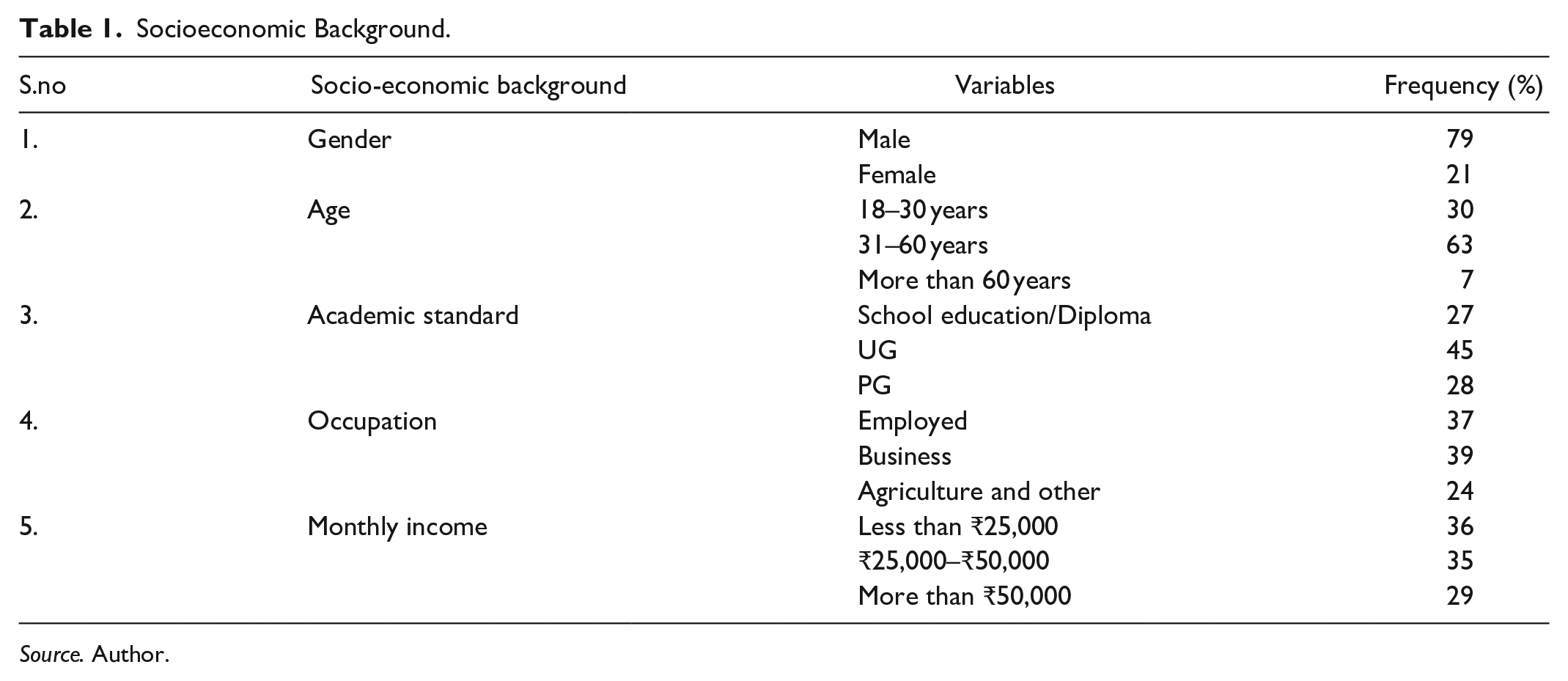

The socio-economic background of the rural inhabitants is presented in Table 1.

Socioeconomic Background.

Source. Author.

From the descriptive statistics, one can see that only around one-fifth are female (21%). This means that in most of the Indian rural households, males take the financial decisions. Further, about 60% were in the 31 to 60 years age group. Academic standard discloses that nearly half of the respondents (45%) were well-educated and completed a degree. Occupation reveals that about one-fourth of the respondents are in agriculture, and the remaining respondents are either employed or business people. Monthly income disclosed that 36% of respondents earn less than ₹ 25,000, 35% are in ₹ 25,000 to 50,000 monthly income group, and 29% are in more than ₹ 50,000 monthly income group. It clearly shows that the selected respondents fit the requirements of the study objectives.

Transformational Impact of COVID-19 on Savings Motive and Spending Pattern

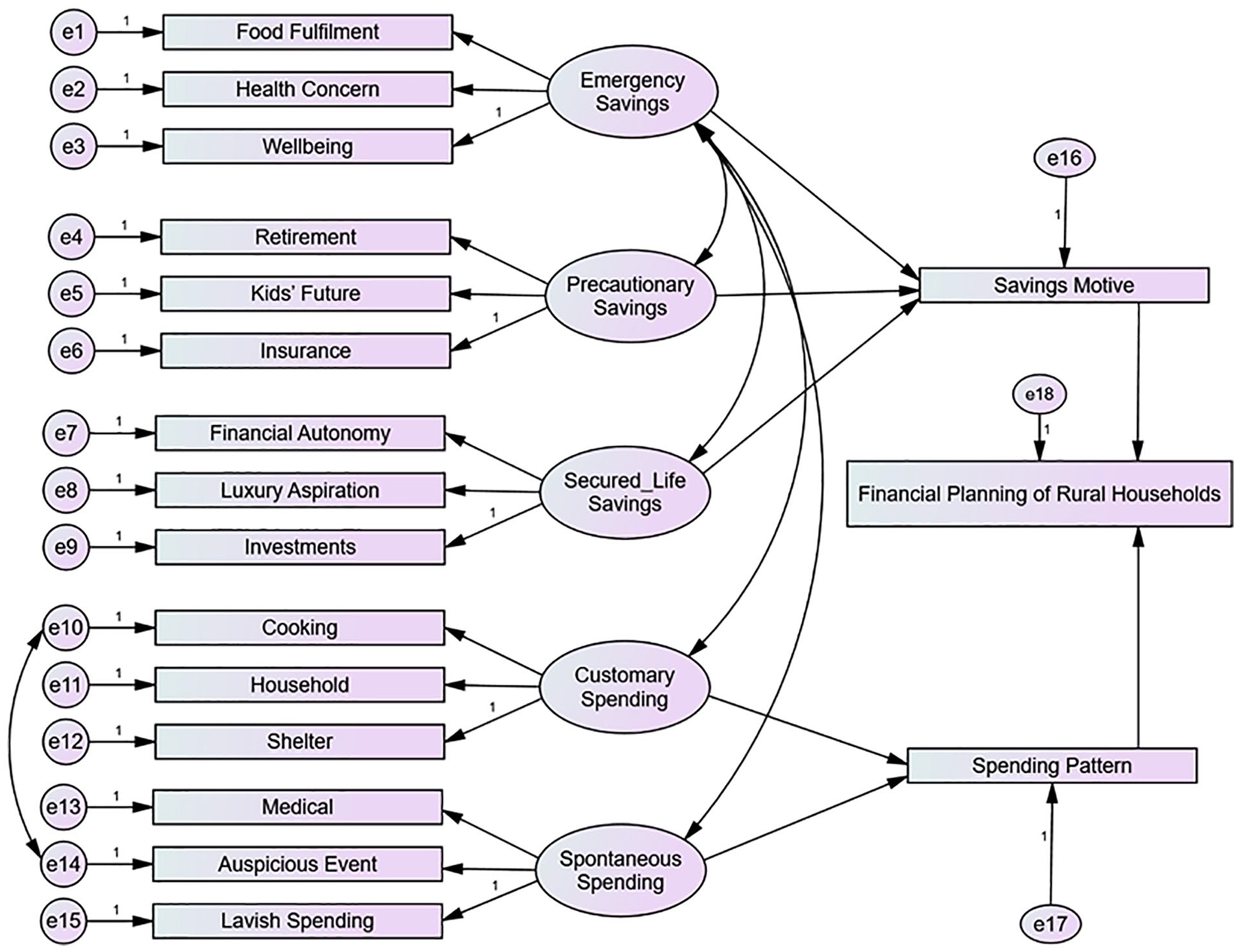

COVID-19 has transformed the savings motive and spending patterns of rural households significantly. They save money for three reasons: emergency, precaution and secured life. Similarly, their spending too can be segregated into customary spending and spontaneous spending. Thus, savings motive and spending patterns are essential in rural households’ financial planning, and their relationship can be examined using SEM with observed and latent variables.

SEM is an efficient tool to measure and inspect causal relationships among different variables. A latent construct is not observable directly but is derived from other variables measured and observed directly. SEM is mainly administered for confirmatory models than exploratory studies; hence, it tests the study’s hypotheses. It consists of two parts: measurement model and SEM. The relationship between latent variables with factor representation is explained under the measurement model, but SEM transmits the causal relationship amongst latent constructs (Fornell & Larcker, 1981).

The study designs a conceptual model for estimating the transformational impact of savings motive and spending pattern on the financial planning of rural households. Savings motive of rural households has transformed to emergency needs from precautionary and secured life needs who now make emergency savings plan to live a safe life, sacrificing a portion of their spending associated with both customary and spontaneous expenses after the spread of COVID-19. Financial planning of rural households constitutes their savings and spending to support their emergency needs as the ultimate result; hence it is tested with suitable hypotheses. The measurement model has been created by performing CFA that establishes a perfect model fit with the data. Reliability, which assures the internal consistency of each factor used to measure the latent construct, is also ascertained, as is the convergent validity and reliability.

Table 2 reveals that the value of Cronbach’s alpha ranges between .85 and .93, which are higher than the minimum threshold value of .70. Moreover, the computed correlation values are found in the range of .794 to .917, showing that multicollinearity is not an issue amongst the constructs because the standard error values are lower than the coefficient values.

Results of Correlation Coefficient Matrix.

Source. Author.

Significant at .01 level.

Measurement model

The impact of both exogenous constructs on the financial planning of rural households is determined by using SEM since it establishes a path for the simultaneous inspection of the whole model that seeks different hypothetical relationships. In this manner, a two-step test is executed. First, a measurement model is analysed with latent constructs, and then SEM is used to analyse its hypothetical relationship and all variables. Five latent constructs are outlined based on the hypotheses proposed above: emergency savings, precautionary savings, secured life savings, customary spending and spontaneous spending, from 15 observed variables. In this way, a measurement model is created to examine the reliability and validity of the latent constructs. The results are presented in Figure 1.

Measurement model.

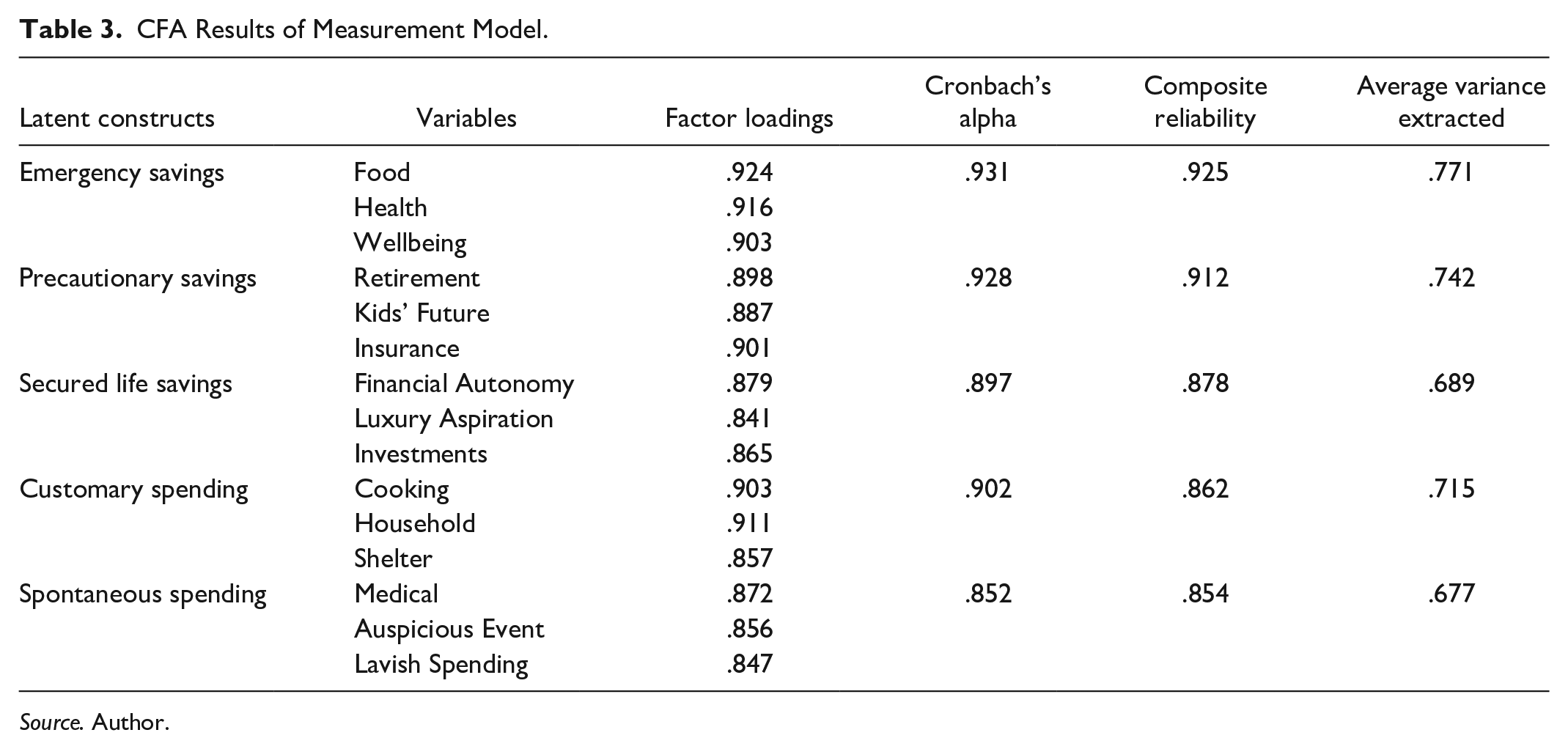

Table 3 shows the factor loading values of the latent constructs in the range of .841 to .924, strongly supporting the validity of each construct. The average variance extracted for emergency savings, precautionary savings, secured life savings, customary spending and spontaneous spending is higher than the threshold level of .50. Similarly, the composite reliability coefficient values are higher than .60 for all latent constructs, assuring high internal reliability of the model.

CFA Results of Measurement Model.

Source. Author.

Table 4 shows that all requisites for approving a first-order measurement model are almost met. The CFA results of the measurement model indicate that the value of chi-square is 1719.485, with p = .000, CFI = .907 and RMSEA = .046. Subsequently, the goodness-of-fit test results show that the model is perfectly fit. The model is tested after determining the validity and reliability of each variable.

CFA Results of Model Fit.

Source. Author.

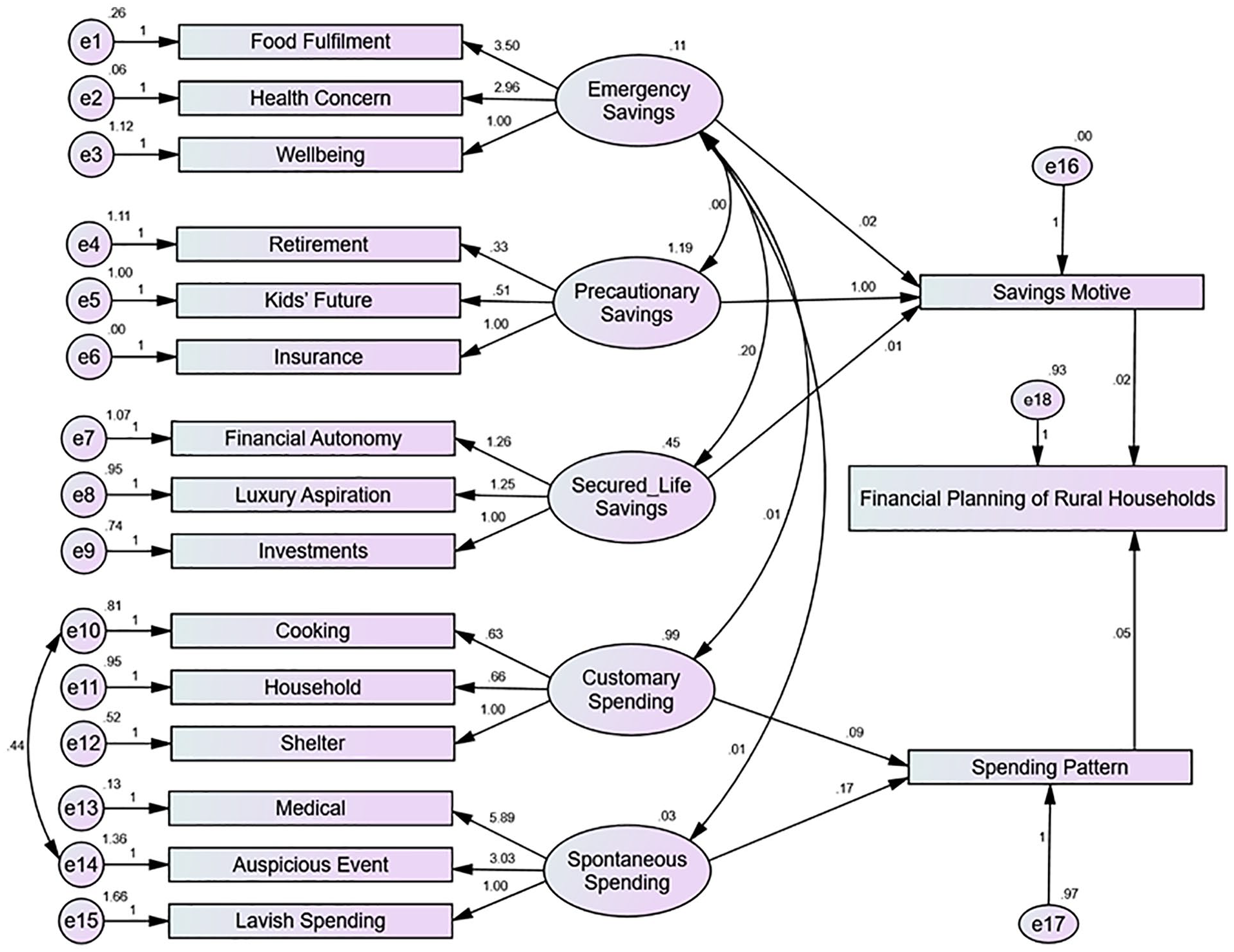

Structural equation modelling

The hypotheses are tested to measure the stability of the proposed measurement model with the data. Two hypotheses are developed in constructing the hypothetical relationship with a path significance of 5% (p = .05). These hypotheses were formulated to confirm whether there was any positive correlation among all hypotheses or not.

Figure 2 shows that in the different hypothetical paths in the model, all path values are significant at p < .05. The study examines the model presented; it helps prepare a flow chart for financial planning models among rural households. Generally, in SEM, the model fit estimated through chi-square is not easy because it relies on the size of the sample. Based on such restrictions, different kinds of fit indices have been calculated. However, the goodness of fit and its extensive relationship among different hypotheses are presented in Tables 5 and 6.

Structural equation modelling.

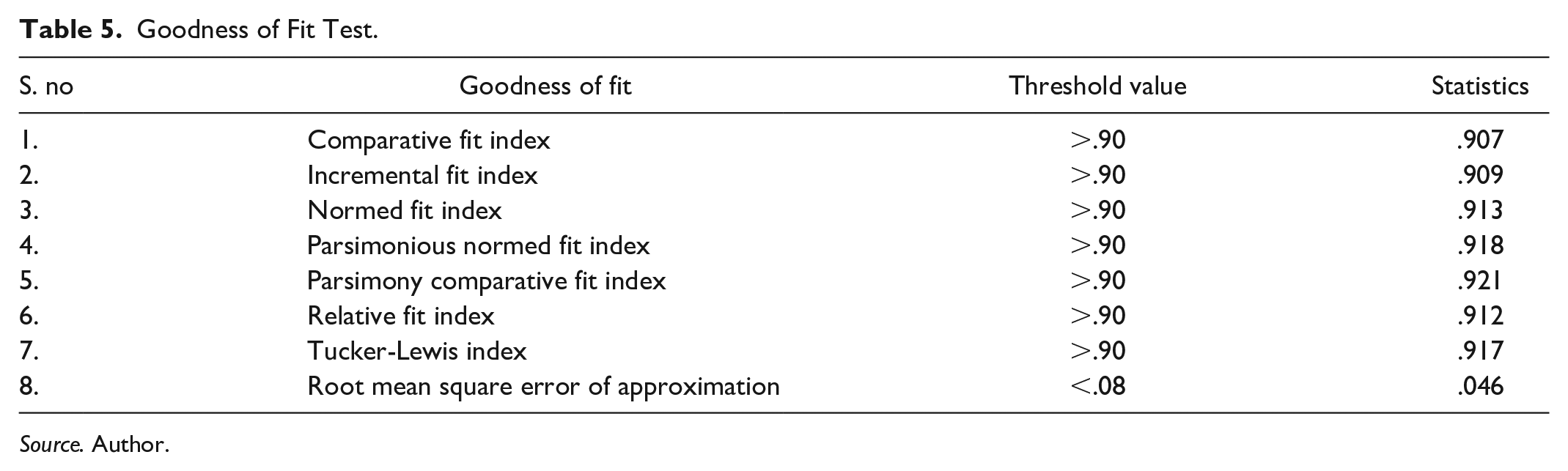

Goodness of Fit Test.

Source. Author.

Testing the Hypotheses.

Source. Author.

Table 5 shows the goodness of fit test of the structural equation model; it confirms that it has a good fit with the data among all index values. The computed values such as Comparative Fit Index (.907), Incremental Fit Index (.909), Normed Fit Index (.913), Parsimonious Normed Fit Index (.918), Parsimony Comparative Fit Index (.921), Relative Fit Index (.912), Tucker-Lewis Index (.917) are more than the threshold limit of .9. Furthermore, the Root Mean Square Error of Approximation value is .046, which is less than the threshold value of .08. SEM has a significant relationship with the goodness-of-fit indices since consistency is found on all suggested values. The results confirm the data reliability.

Table 6 shows that emergency savings have the coefficient value of .917 for food, .970 for health and .303 for well-being. The construct emergency savings has a positive and significant relationship with its all precursors. All these precursors contribute to the need of creating emergency savings. It confirms that emergency savings form an essential part of rural households’ financial planning due to the spread of COVID-19. Hypothesis (H1) is thus supported. Emergency savings have a direct and positive relationship with the savings motive since its coefficient value is .007; hence, Hypothesis (H2) is accepted too. Food requirements, health and other family well-being concerns are the most important reason for developing savings for emergency purposes. This is parallel with the results of Bi and Montalto (2004).

The coefficient values of precautionary savings are .320 for retirement, .482 for kids’ future and 1.000 for insurance. It has a direct and significant relationship with its precursors, and it motivates people to save for safeguarding against future financial needs. Hence it accepts hypothesis (H3). Precautionary savings has the coefficient value of .998 for savings motive; hence hypothesis (H4) could be accepted. Precautionary savings play a protective mechanism favouring peaceful retirement life, kids’ future, and insurance cover against unexpected evils. The results are similar to the findings of Kamarudin et al. (2018).

Secured life savings have coefficient values of .632 for financial autonomy, .650 for luxury aspiration and .613 for investments. It proves that secure life savings can be assured through debt-free financial independence, life sophistication with luxury and investments for wealth creation. Secured life directly and significantly relates to its precursors, leading to the accepting hypothesis (H5). Secured life savings have a coefficient value of .004 for savings motive, and it has a solid and positive relationship with savings motive, supporting hypothesis (H6). The results parallel those of Dilip and Zhao (2011) and show that financial autonomy, luxury lifestyle and personal investments will provide a secured life to rural inhabitants. The result validates that the savings motive has a direct and positive relationship with the financial planning of rural households. The coefficient value is found to be .021, and it leads to the accepting hypothesis (H7).

Customary spending has a significant relationship with expenses incurred on cooking needs, household uses and shelter purposes. It is verified with the coefficient value of .573 for cooking, .558 for household uses and .811 for shelter purposes, supporting hypothesis (H8). Further, customary spending is the main component in the spending of rural households and has the coefficient value of .095 for the spending pattern, which leads to the accepted hypothesis (H9). The results are consistent with Devi (2017). Day-to-day spending cannot be avoided but can be minimized for a short period to save for emergencies like the COVID-19 pandemic.

Spontaneous spending has a coefficient value of .949 for medical, .427 for the auspicious event and .139 for lavish expenditure. Unplanned expenditure does not come under regular expenses; it happens suddenly but consumes a significant amount of money. Rural households set aside a portion for such purposes. Hence hypothesis (H10) is accepted. Moreover, it has a direct and significant relationship with the spending pattern of rural households with a coefficient value of .032 and supports hypothesis (H11). Spending pattern has a direct and positive relationship with the financial planning of rural households with the coefficient value of .047, and it leads to accepting hypothesis (H12). The findings are similar to the results of Yusof and Duasa (2010). The findings validated that both savings motive and spending pattern directly influence the financial planning of rural households due to the COVID-19 pandemic.

The extent relationship between independent factors in the financial planning of rural households is also investigated. The test of the estimates of independent factors is depicted in Table 7.

Estimates of Independent Factors.

Source. Author.

indicate significant at 5%.

Table 7 shows that emergency savings have a 1% covariance with precautionary savings, meaning emergency savings is created out of 1% funds devoted for precautionary savings. It clearly explains that rural households set apart emergency savings from precautionary savings to face immediate food, health, and family well-being problems. Emergency savings has an 89% covariance with secured life savings. Due to COVID-19, rural households considerably reduced their secured life savings to set up an adequate amount of emergency savings to protect emergency needs. Similarly, emergency savings have a 2% covariance with customary spending, proving that rural households slightly sacrificed their routine expenses to save for emergency needs. Further, rural households avoided spontaneous spending to the extent of 22% to save money for emergency needs. Similarly, spending on an auspicious event is diverted to 42% towards current cooking purposes.

Conclusion

The motivation of the study was to measure the transformational impact of COVID-19 on the savings motive and spending pattern of rural households. Generally, most rural households tend to save more in the form of cash at home for immediate spending purposes. Rural inhabitants had limited opportunities to earn during this pandemic period compared to urban residents. The spread of COVID-19 increased the price of essential goods and reduced health safety. It also created a panic, which directly motivated them to save money for food, health and other well-being needs to safeguard their family.

The study expands the financial planning of rural households in two dimensions: savings and spending. Findings revealed that food, health, and well-being aspects lead rural inhabitants to save money. Savings in liquid cash, bank deposits and other cash equivalent sources are an essential part of emergency savings. Emergency savings act as a shield against the fall in income, rise in prices, health risks and survival of life during such circumstances. Emergency savings is for allocating money to discharge the basic and routine needs of life. Rural households have been seen in this study eager to save money to overcome financial emergencies due to this pandemic.

Precautionary savings are made with the intention of better retirement life, kids’ future and insurance against unexpected events. As a precautionary motive, rural inhabitants primarily save money in bank deposits and post office schemes. On some occasions, they purchase gold ornaments for future safety. Similarly, they make a perfect savings plan for their children’s future regarding their marriage, education, and career planning. Further, they prioritize purchasing a life insurance policy as a risk protection saving and financial support for their family in case of their death. Currently, rural households save for emergency needs by diverting a small portion of their precautionary savings.

Secured life savings are initiated with financial autonomy, luxury aspiration and investment for wealth creation. Economic autonomy is the way to a debt less life or attainment of self-sufficiency in all financial requirements. Rural inhabitants are interested in constructing a well-furnished home, purchasing a car and other luxurious products. Therefore, luxury aspiration motivates them to save money for the prospect of a comfortable life. In addition, they are willing to create wealth to show individuality. They are eager to invest in land, gold and other financial instruments to enrich their standard of living. However, with the lack of income due to COVID-19, their priority has shifted to emergency needs than secured life savings. Rural households have transformed a considerable portion of their savings for emergency purposes as a protective measure for COVID-19.

Customary spending is the expenses incurred on day-to-day affairs by the rural households, including cooking, household expenses, and other shelter expenses. Under such circumstances, lack of income induces them to cut unnecessary costs and divert the funds to the pool of emergency savings.

Spontaneous spending is not regular; it appears suddenly in medical treatment, an auspicious event or purchasing luxury products. The emergence of coronavirus has significantly increased sudden medical expenses, and rural people mainly seek government hospitals for treatment. In a few cases, auspicious occasions are carried out with fewer guests, and lavish purchases are wholly stopped. The corona virus has created an awareness among rural households regarding the importance of making emergency savings. To maintain better well-being, they are keen on purchasing medical insurance policies against the spread of COVID-19. Moreover, they also spend on medical protection measures such as sanitisers, clinical masks and healthy foods against the spread of the corona virus. This can be compensated from their pool of emergency savings.

Savings and spending are two sides of financial planning, and rural households have sufficient awareness to safeguard their life against the outbreak of COVID-19. Savings motive guides the rural families to learn about the purpose of savings, channelize and prioritize their savings. At present, they prioritize emergency savings followed by precautionary and secured life savings over other needs. Temporarily, they have cut down extra expenses to strengthen their emergency savings. Savings motive directs them towards financial stability, and spending pattern helps them to avoid needless expenditure. The independent relationship shows that emergency savings positively correlate with all constructs of precautionary savings, secured life savings, customary spending and spontaneous spending.

Similarly, auspicious events have a positive correlation with the cost incurred for cooking-related expenses. To sum up, COVID-19 has transformed the savings motive and spending pattern of rural households in India. Significantly, rural households save money for emergency purposes by cutting other savings and spending during such pandemic periods.

Research Implications

The present study has significant implications for policymakers and academicians. Given that COVID-19 has had a significant negative influence on income generation and price stability, rural households were required to save for emergency needs. Rural households often hold money for routine family expenses but do not keep the same in banks or any other mode. The spread of coronavirus has compelled rural households to save separately for emergencies. The study advocates keeping adequate savings for emergency reasons as a precautionary measure and secured life, ensuring and protecting their financial independence. Rural households are the ideal model for efficient financial planning to survive during odd situations. Cutting unnecessary expenses and postponement of secondary savings strengthen their confidence in fighting against critical situations. Policymakers and academicians should make a reasonable effort to offer them professional training and education to maximize the returns in savings of rural households.

Scope of the Study

The study was made an effort to test the transformational impact of Covid-19 on savings motive and spending pattern of rural households in India. The study considered only the savings and spending of rural people. It didn’t consider the size of income and source of income of rural households. Further, people living in rural areas are only taken into consideration. Migration from rural to urban or urban to rural was ignored.

Footnotes

Appendix 1

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

All procedures in studies involving human participants followed the ethical standards of institutional and/or national research committees. Ethical approval was obtained from the Research Ethics Committee at CHRIST (Deemed to be University), Bangalore, India.

Informed Consent

All participants gave their informed consent and were informed that they could withdraw from the study at any time.