Abstract

This study employs high-dimensional factors model to depict the development of monetary policy uncertainty (MPU) in China over the past decades and develops a logical analytical framework to analyze the effect of MPU on the dynamic adjustment of a firm’s capital structure through bank risk-taking channels. We investigate how MPU affects dynamic adjustment of a firm’s capital structure using a panel data set of China public manufacturers between 2007 and 2018 and find that the higher the MPU, the more detrimental it is to the dynamic adjustment of firm’s capital structure. Further, bank risk-taking plays the role of a financial stabilizer. In addition to the willingness to take risks in on-balance sheet operations and the scale of loans, the risk-taking of our banks may also be reflected in the adjustment of the off-balance-sheet shadow banking scale. This study also finds that in terms of on-balance sheet business, heighten MPU decreases the scale of bank credit and tightens loan approval criteria, in terms of off-balance sheet business, heighten MPU decreases the scale of shadow banking, thereby leading to a lower dynamic adjustment of firm’s capital structure.

Introduction

In recent years, the global economic growth has slowed down, the imbalance in growth has increased and the “black swan” events in the international political arena have increased the degree of uncertainty in the global economy. This highlights the importance of understanding its impacts on the real economy. Quite a few impressive studies show that the speed of the leverage adjustment is lower when uncertainty is higher (Çolak et al., 2018; Gungoraydinoglu et al., 2017; Im et al., 2020).

However, the impact of monetary policy uncertainty (MPU) on the dynamic adjustment of firm capital structure has been little explored. Grosse-Rueschkamp et al. (2019) show that the central bank’s activities influence the capital structure via the banking sector. And Cook and Tang (2010) find that term spreads and credit spreads are important factors affecting the capital structure and its rate of adjustment. But no matter how clear and efficient the communication of the central bank is, uncertainty always follows monetary policy (Kurov & Stan, 2018), and the monetary policy itself can be a source of uncertainty (Creal & Wu, 2017). Currently, most scholars focus on exploring the impact of MPU at the macro level, for example, it lowers economic growth (Sinha, 2016), influences unemployment (Wieland, 2003), inhibits the inflow of foreign direct investment (Albulescu & Ionescu, 2018). But there is little scholarly inquiry into how frequent adjustments of monetary policy affect the financial decisions of firms, especially the dynamic adjustment of capital structure that determines the profitability and even the survival of firms. In addition, using a partial adjustment framework is closer to the optimal capital structure (Im et al., 2020; Lambrecht & Myers, 2017; Leland, 1994). In this study, we examine the impact of MPU on the dynamic adjustment of firm capital structure and investigate the economic mechanisms through which MPU influences the dynamic adjustment of firm capital structure.

Due to China’s special institutional environment, monetary policy works mainly with the real economy through commercial banks. And commercial banks’ risk-taking behavior, which is influenced by their risk appetite, not only affects a firm’s access to capital for investment but is also particularly important for the stability of the financial system and the real economy (Bruno & Shin, 2015). Maddaloni and Peydró (2011) have argued that bank risk-taking is primarily based on perceptions and preferences for risk and that credit risk is assumed or controlled by changing credit criteria, hence the use of loan approval criteria as a bank risk-taking variable. However, it does not directly reflect the scale of credit provision behind risk-taking, nor does it reveal the extent of exposure to macroeconomic and policy influences. Angeloni et al. (2015) use the risk-weighted asset ratio as the bank risk-taking variable. But whether using loan approval criteria or risk-weighted asset ratios as measures of bank risk-taking, risk-taking behavior is analyzed in terms of on-balance sheet operations, ignoring the impact of off-balance-sheet shadow banking.

In fact, China’s shadow banking is mostly based on the commercial banking system, while the shadow banking system in developed countries is mainly based on financial markets and asset securitization, which is a more mature system developed independently of the traditional commercial banking system. So, we cannot analyze bank risk-taking by directly separating table operations from shadow banking as in (Bruno & Shin, 2015; Meh & Moran, 2010). In addition, commercial banks generally have credit misallocation, and the provision of loans will be subject to strict supervision, while China’s shadow banking is part of the replacement and complementary functions of commercial banks. Buchak et al. (2018) show that the regulatory burdens of the bank have promoted the growth of shadow banking. And affected by the four trillion-yuan economic stimulus package in 2009, China’s shadow banking business has grown rapidly after 2012 (Chen, He et al., 2020). Therefore, we include shadow banking in the analytical framework when examining risk-taking in Chinese banks.

To capture MPU we use the high-dimensional factors model in the big data environment proposed by Jurado et al. (2015) as the main measure of China’s MPU. Baker et al. (2016) measure overall economic policy uncertainty based on certain specific keywords that appear in newspaper coverage. To the best of our knowledge, the existing literature on MPU per se is predominantly based on market transaction data to measure, such as implied volatility computed from interest rate option price and realized volatility computed from the intraday price if interest rate future (Bauer and Neely, 2014; Swanson and Williams, 2014). Husted et al. (2020) use an approach similar to Baker et al. (2016) to measure MPU. But most of them are based on advanced economics, and rarely about developing economics. Li et al. (2020) follow the way of Jurado et al. (2015) on uncertainty to measure China’s MPU as the conditional volatility of purely unforecastable component of the future value of money supply. They just consider the money supply side, but the number of instruments used by the People’s Bank of China (PBoC) keeps growing, which makes it impossible to measure monetary policy by money supply alone. In our study, we use conditional volatility of unforecastable components of the future value of monetary policy-related variables based on Jurado et al.’s (2015) approach to provide a comprehensive measure of MPU.

To estimate the dynamic adjustment of firm capital structure, we follow on Flannery and Rangan (2006) and Im et al. (2020) to adopt a partial adjustment model of the capital structure, which is often used to study the speed of leverage adjustment. Due to various frictional factors such as bankruptcy costs, agency costs, and information asymmetry, it is clear that capital structure is closely related to enterprise value, which implies that there is an optimal capital structure from the perspective of enterprise value maximization, that is, an arrangement between equity and debt that minimizes the cost of capital and maximizes the value of the firm. If an enterprise does have an optimal level of debt, it will adjust its debt and equity ratios to reach the optimal level and gradually improve its operating conditions to increase its enterprise value and growth rate (Huang and Ritter, 2009). This is essentially the same as the requirements of “deleveraging,” which is not to reduce leverage to zero but to achieve a desirable level of leverage.

We may summarize our main contribution and the novelty of our approach as follows: First, economic policy uncertainty is largely regarded as homogeneous (Bordo et al., 2016; Creal & Wu, 2017), with little exploration of how different types of policy uncertainty affect firms, and whether the process and outcome are different. We first estimate a FAVAR model that includes factors and their polynomials and then compute the predicted variance to measure China’s MPU, and retrospectively validate it with China’s policy practice, which helps to further grasp the characteristics of China’s monetary policy fluctuations. Enriches the study of how MPU affects the real economy and expands the literature on the dynamic adjustment of capital structure.

Second, Zhang et al. (2015) study the path of China’s economic policy uncertainty affecting the capital structure of firms from the perspective of economic policy uncertainty but do not pay attention to the speed of corporate capital structure adjustment. We employ a partial adjustment model of capital structure to precisely estimate optimal capital structure. And we explore various economic mechanisms through which MPU influences the dynamic adjustment of firms’ capital structure. We conclude on-balance sheet loan approval criteria, bank loans, and off-balance-sheet shadow banking into the analysis framework of bank risk-taking, thereby making up for the deficiencies of the existing literature. Using theory-based proxies for MPU and optimal capital structure, we show that heighten MPU significantly lowers the dynamic adjustment of firm capital structure by decreasing the scale of bank credit and shadow banking, tightening loan approval criteria.

The remainder of the paper is organized as follows. Section 2 presents the theoretical analysis of the effects of MPU on optimal capital structure, while Section 3 describes the dataset, measurement of variables, descriptive statistics, and research design. Section 4 presents empirical findings. Section 5 concludes the paper.

Logical Analytical Frameworks

A growing number of literature focus on the effects of monetary policy on bank risk-taking, that is, they have discussed in depth the channels of bank risk-taking through which monetary policy is examined for its effectiveness (Borio & Zhu, 2012). Azofra et al. (2020) reveal that bank debt modifies the impact which macroeconomic variables of monetary policy have on a firm’s leverage. It is inferred that the bank risk-taking channel should be an indispensable role path for the dynamic adjustment of the capital structure of a firm affected by MPU in China.

Monetary Policy Uncertainty and Capital Structure Adjustment

Since the financial crisis in 2008, the global economic situation has continued to be sluggish, and the economic policies of various countries have changed frequently and the differences have widened, exposing the market to greater policy uncertainty. In particular, monetary policy, as one of the major economic policies, has often attracted widespread attention, and MPU has become the norm. Some studies have found that economic policy uncertainty can affect the real economy (Baker et al., 2016; Huang et al., 2018). Husted et al. (2020) further show that monetary policy uncertainty raises credit spreads and reduces output. In addition to the real economy, financial markets can react immediately to the monetary policy just introduced or to be introduced (Pástor & Veronesi, 2013). However, the impact of monetary policy uncertainty (MPU) on the dynamic adjustment of firm capital structure has been little explored.

As for the uncertainty of monetary policy, its measurement method is the difficulty of research. Currently, there are several main methods to measure MPU as follows: First, incident method. Ait-Sahalia et al. (2012) record specific events in the order of their development from occurrence to completion, especially the market reaction to policy announcements, and construct an index of policy uncertainty accordingly, but because there is a certain transmission process of information, the occurrence and completion of their defined events do not reflect the beginning and end of uncertainty. Second, Election method. Belo et al. (2013) use government elections as a proxy for uncertainty, but this index is not continuous due to the time interval of elections. Third, Baker et al. (2016) continuously quantify economic policy uncertainty based on continuous news coverage. However, the above three measures are comprehensive measures of economic policy uncertainty and do not distinguish between monetary policy or fiscal policy, and their uncertainty measures are not relevant. And the high-dimensional factors model in the big data environment proposed by Jurado et al. (2015) can solve these issues.

MM theory assumes that firm value is independent of the capital structure under a set of strict assumptions. Trade-off theory considers the optimal capital structure of a company after taking into account tax savings and costs of financial distress, agency costs, and signaling. Since companies are affected by various factors in the internal and external environment during the business, their capital structure tends to deviate from the optimal value. However, a company aiming at value maximization will not let its capital structure deviate from the optimal level for a long period of time, and will continuously adjust its debt-to-equity ratio during its dynamic development to make its capital structure reach the optimal value. Therefore, the capital structure of a company is still a dynamic adjustment process that is constantly optimized. However, the adjustment of a company’s capital structure does not happen overnight, and the speed of adjustment is influenced by the benefits and costs of adjustment (Leary & Roberts, 2005).

Drobetz and Wanzenried (2006) find that companies with higher growth and greater deviation of actual capital structure from the target capital structure had faster recapitalization. Chang et al. (2014) argue that the slower the quality of governance, the slower the recapitalization of a firm, whether it is a highly leveraged firm that recapitalizes downward or a less leveraged firm that recapitalizes upward.

The external environment is also an important factor affecting the speed of recapitalization, such as the institutional environment, and the macroeconomic environment. In terms of the institutional environment, Öztekin and Flannery (2012) find that a good level of legal system and property rights protection system can effectively reduce transaction costs and thus promote the speed of recapitalization. In terms of the macroeconomic environment, Cook and Tang (2010) find that firms recapitalize faster when the macroeconomy is doing well. Economic policy uncertainty is an important macroeconomic factor and an important external environment for firms. Im et al. (2020) show that high economic uncertainty lower optimal or target leverage ratio. And Lambrecht and Myers (2017) predict the negative impact of uncertainty on optimal leverage ratio. However, there is little literature examining the impact of MPU on capital structure adjustment.

Monetary Policy Uncertainty and Bank Risk-Taking

Compared with the early period of reform and opening up, the market access threshold of China’s banking industry has been gradually lowered, and small and medium-sized banks, represented by joint-stock commercial banks, urban commercial banks, and rural commercial banks, have gradually broken the geographical monopoly-type business model and integrated into the market-oriented competition after completing the shareholding reform. Among them, the proportion of interbank liabilities on the table of small and medium-sized banks once rose from 21.7% in 2010 to 30.4% in 2016. The proportion of interbank assets rose from 20.2% to 33.7% (Data source: Wind database.) in the same period. However, at the same time, the financial risks associated with the interbank business have gradually emerged. Since the financial crisis, the “shadow banking system” in the West and the “non-standard,” “off-balance sheet,” and “implicit guarantee” in China have received great attention from regulators and academics.

Since Borio and Zhu (2012) first explicitly proposed the bank risk-taking channel of monetary policy, this transmission mechanism has triggered extensive academic discussions and scholars have explained this effect from different perspectives. A number of earlier scholars have also systematically introduced financial factors into dynamic stochastic general equilibrium (DSGE) models. For example, Bernanke et al. (1999) Financial Accelerator model and Kiyotaki and Moore (1997) Credit Cycle model. Then, Rajan’s (2006) search-for-yield mechanism shows that monetary transmission operates through the relationship between low market rates and expected target rates of return. Facing lower incomes caused by lower interest rates, banks may increase risk appetite and invest in high-risk loans and securities (Borio & Gambacorta, 2017; Chodorow-Reich, 2014). Then, the low policy interest rate and abnormal term structure have compressed the bank’s net interest profit (Borio et al., 2017; Molyneux et al., 2019). At present, unconventional monetary policy is becoming more frequent, Matthys et al. (2020) use corporate syndicated loan data at the bank-firm level to analyze the bank risk-taking associated with unconventional monetary policy, showing that accommodating monetary conditions are associated with overall lower loan spreads.

There are significant differences between China’s shadow banking and that of developed countries. In addition to the risk-taking willingness of on-balance sheet operations and loan scale, Chinese banks’ risk-taking may also be reflected in off-balance-sheet shadow banking size adjustments. Chen et al. (2018) analyze the impact of China’s monetary policy on shadow banking using data from 2009 to 2015 and show that contractionary monetary policy has led to a rapid rise in shadow bank lending, offsetting the expected decline in traditional bank lending and hindering the effectiveness of the monetary policy on aggregate bank credit.

Bank Risk-Taking and Firm Capital Structure Adjustment

Constrained by the external macroeconomic environment, the game of control, and interest among the various internal stakeholders, and the existence of information asymmetry and transaction costs, the actual capital structure of the firm will inevitably deviate from its target level, that is, the optimal capital structure. Firms will adjust the capital structure if they deviate from their optimum (Flannery & Rangan, 2006), but the process of adjustment needs time, especially the adjustment cost is high (Byoun, 2008; Devos et al., 2017; Huang & Ritter, 2009). In China, firms with easy access to loans can adjust their leverage in time to achieve an optimal capital structure (Wu & Yue, 2009), and loans mainly come from commercial banks. Kahle and Stulz (2013) find that during the financial crisis, firms that relied on bank loans had to reduce their debt and capital expenditures due to the credit supply compression. Shen et al. (2015) confirm that differences in the availability of bank credit during China’s 2009 to 2010 credit exuberance growth led to differences in changes in corporate leverage.

In summary, the adjustment of monetary policy will affect the optimal capital structure through bank risk-taking and hence the uncertainty of monetary policy adjustment will also affect the dynamic adjustment of firm capital structure through bank risk-taking. Different monetary policies have different effects on capital structure adjustment. Therefore, whether the MPU will increase or decrease the speed of firm capital structure adjustment is an open question. Thus, this study aims to understand the MPU’s effect on a firm’s dynamic adjustment of firm capital structure and the underlying mechanisms that influence the dynamic adjustment of firm capital structure through bank risk-taking.

Data Sources and Methods

Sample Selection

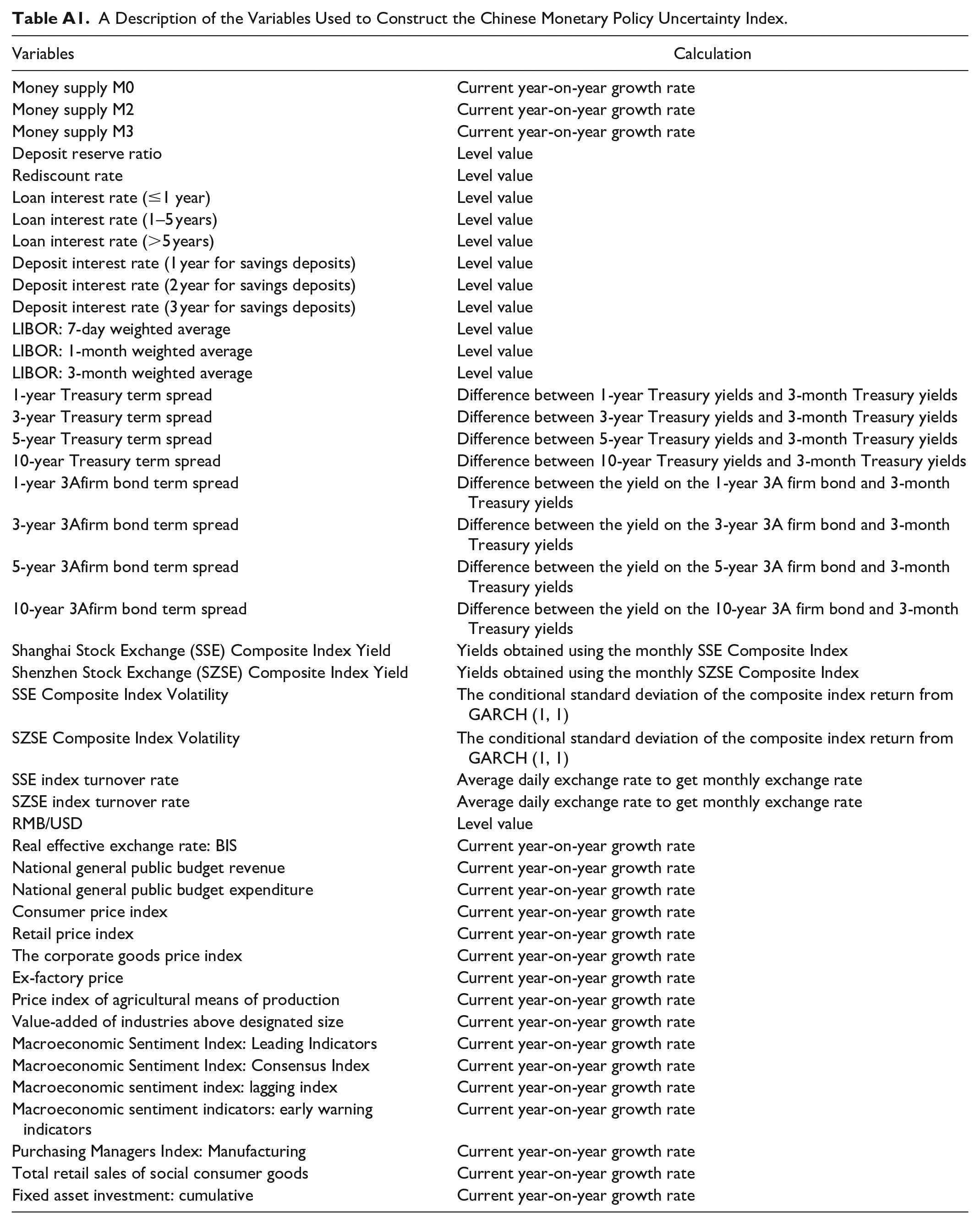

To measure monetary policy uncertainty, we use the CEIC database and China Economic Net statistical database for monthly monetary policy uncertainty data, the sample period is from January 2007 to December 2018. A detailed selection of indicators for estimating monetary policy uncertainty can be found in Appendix Table A1.

The bank loan approval criteria, bank loan, and shadow banking data are all from PBoC. In this paper, we select quarterly data of public manufacturing firms as the initial sample, and the financial data of the firm are from the CSMAR database; for the missing data, we use the Wind database to supplement. The sample period is from Q1 2007 to Q4 2018. The final sample is an unbalanced panel dataset comprising 16,072 observations.

Measure of Variables

Measuring China’s monetary policy uncertainty

According to the method of Jurado et al. (2015), our paper uses China’s monetary policy and related macroeconomic variables to measure China’s monetary policy uncertainty.

The uncertainty

where the

Using simple averaging to obtain an estimate of h period MPU denoted (See Jurado et al. (2015) for details of the estimation steps.):

where

Figure 1 plots China’s MPU index over time for h = 1, 3, and 12, that is, U(1), U(3), and U(12) denote for 1 (1 month h1), 3 (3 months h3), and 12 (12 months h12) periods in advance, respectively. Combined with Figure 2, we infer that the MPU index increases for periods 1, 3, and 12 ahead of time due to the greater uncertainty that accumulates over the longer forecast period, but the trend is consistent. It indicates that during the global financial crisis of 2008 to 2010, China’s MPU fluctuated wildly. This can be explained by the fact that controlling inflation was the key concern of China’s monetary policy in 2007 and early 2008, due to the rise in consumer price index (CPI) and the risk of real estate bubbles. However, when the crisis broke out in 2008, China’s central bank immediately switched its target from containing inflation to stimulating output. This sudden and dramatic change drove MPU to a record high. Loose monetary policy, coupled with the fiscal stimulus package in 2009, helped China gradually recover from the crisis. Later in 2010, China’s central bank switched back to prudent monetary policy, leading to another spike in MPU. Since later 2011, China’s monetary policy had remained prudent, and MPU has remained at a low level, but after the “cash crunch” in 2014, MPU had increased as interbank dismantled business associated with stricter regulation and the stock market crash in 2015. In 2018, inclusive financial targeted downgrades were fully implemented, leading again to a spike in MPU.

China’s monetary policy uncertainty index.

Orthogonalized impulse response.

Measuring control variables

This paper selects the influences on the capital structure and its rate of adjustment based on the following principles: first, the influences discussed in mainstream theories, including the trade-off theory; second, the variables that have been used by dynamic capital structure literature, such as (Faulkender et al., 2012; Flannery & Rangan, 2006; Im et al., 2020); third, the influences determined by China’s institutions and conditions and the actual economic situation; and fourth, the availability of data. All variables are computed for firm

Variables Definitions and Summary Statistics.

Descriptive Statistics

To minimize the effect of outliers, we winsorize variables at the top and bottom 1% of each variables’ distribution except the MPU index. Panel B in Table 1 provides the summary statistics for the main variables used in this study. The monetary policy uncertainty measure,

Before investigating the effect of monetary policy uncertainty on leverage targets. To exclude the effect of multicollinearity, the correlation coefficients, and variance inflation factors for the independent and control variables were calculated using the treated sample data in this paper, and the results are shown in Table 2. The calculations show that the correlation coefficients for almost all variables are relatively small. Even if the correlation coefficient between size and age is 0.4189, the effects of multicollinearity can be ruled out because the variance inflation factors are all much less than 10 (Table 3).

Variables Correlation Coefficient.

Variance Inflation Factor Test.

Monetary Policy Uncertainty, Bank Risk-Taking, and Firm Capital Structure

In this paper, we analyze the speed of capital structure adjustment through a partial adjustment model, and in this subsection, we use the panel vector autoregressive model (PVAR) proposed by Holtz-Eakin et al. (1988). We develop a three-variable PVAR:

where,

Granger causal relation test

The results of the Granger causal test are shown in Table 4, where MPU is the cause of capital structure (original hypothesis (8), (10), (19)), and also for loan approval criteria, bank credit scale, and shadow banking scale (original hypothesis (4), (17), (26)). Loan approval criteria, bank credit scale, and shadow banking scale can influence the capital structure of firms (original hypothesis (7), (11), (20)). Both MPU and loan approval criteria or bank credit scale or shadow banking scale can affect the capital structure of firms (original hypothesis (9), (12), (21)). However, the original hypothesis that “loan approval conditions or the scale of bank credit or shadow banking is not a granger of MPU (original hypothesis (1), (14), (27)” is significantly rejected, indicating that loan approval criteria or the scale of bank credit or shadow banking are a granger of MPU, indicating that loan approval criteria, the scale of bank credit and shadow banking can also affect MPU in the opposite direction to some extent, which may be because loan approval criteria, the scale of bank credit, and shadow banking are too high or too low to attract more attention of monetary policymakers, and hence to control and guide through the adjustment of monetary policy. And the original hypothesis (5), (13), and (16) are rejected at the 1% level, indicating that lev is a granger causal for loan approval criteria, bank credit scale, and shadow bank scale, indicating that the capital structure of the firm can also affect loan approval criteria, bank credit scale, and shadow bank scale to some extent, the reason may be that the capital structure affects the firm’s solvency and debt service risk, which is an important financial indicator considered by the bank’s credit decision.

Granger Causal Relation Test.

Impulse response analysis

The results of orthogonalized impulse responses made for the

In the PVAR model of

In summary, the depiction of China’s economic and financial reality based on the 2000 to 2018 period shows that from the perspective of the on-balance sheet business, the degree of monetary policy uncertainty tightens the conditions for loan approval and decreases the scale of bank credit, thus affecting the capital structure of firms and their adjustment behavior, and from the perspective of the off-balance sheet business, monetary policy uncertainty reduces the scale of shadow banking and hence negatively affects the capital structure of firms. Next section, we provide further analysis of the impact of monetary policy uncertainty on the speed of the firm’s capital structure adjustment (see Appendix B).

Research Design

To investigate the effect of MPU on dynamic adjustment of firm capital structure, we extend Flannery and Rangan (2006), Huang and Ritter’s (2009) partial adjustment framework:

where

where

Substituting the equation (6) into equation (5), we obtain the following model:

where

From the previous analysis, this paper develops three sets of extended models of dynamic adjustment of capital structure, based on three observational perspectives of the scale of bank credit, loan approval criteria, and shadow banking scale, respectively.

An extended model of the loan approval criteria perspective (

)

In order to examine the effect of monetary policy uncertainty (

where the inverse of the

where the inverse of the

Further, the speed of adjustment

Based on Baron and Kenny (1986), estimate the coefficients

An extended model of the scale of bank credit perspective (

)

Same steps as in section 3.4.1, the speed of adjustment

Then to test whether bank credit scale is a channel through which monetary policy uncertainty affects capital structure adjustment, the speed of adjustment

where the inverse of the

An extended model of the shadow bank scale perspective (

)

Similarly, first, we set

Second, we set

We can obtain the effect of the independent variable

Results and Discussion

The Effect of Monetary Policy Uncertainty on Leverage Targets

To examine whether monetary policy uncertainty affects the firm’s target leverage ratio. We first estimate equation (8). We employ the ordinary least square (OLS), within-group (WG), least squares dummy variables with a bias correction (LSDVC), and System-GMM estimators to ensure that the estimated effect of monetary policy uncertainty on target leverage is not attributable to the choice of estimation methods or instrument sets. The columns (1)–(4) in Table 3 report the results. The OLS and WG estimates of the coefficient of the lagged dependent variable tend to be biased upwards and downwards, respectively (Im et al., 2020). In this paper, the extended models all contain a first-order lagged term of the explained variable

From Table 5, as predicted by Bond (2002) and Im et al. (2020) the coefficients of lagged

Estimation of the MPU Effects on Leverage Targets.

Note. The IVs used in system-GMM reported in column (4) is the second to 10th lags of MPU and leverage. AR (1) and AR (2) represent the test statistic of the Arellano-Bond tests for first-order and second-order serial correlations in first-differenced residuals, respectively. **, *** Indicate statistical significance at the 5% and 1% levels, respectively.

The Effect of Bank Risk-Taking on the Speed of Firm Capital Structure Adjustment

In section 3.1, we use banks’ on-balance sheet risk-taking, that is, loan approval criteria, bank credit scale, and off-balance sheet risk-taking, that is, shadow banking scale, as proxies for bank risk-taking. In this subsection, we examine whether bank risk-taking increases target leverage ratios.

In column (1) of Table 6 the coefficient of

The Effect of Bank Risk-Taking on the Speed of Firm Capital Structure Adjustment.

Note. The IVs used in system-GMM reported in column (4) is the second to 10th lags of MPU and leverage. AR (1) and AR (2) represent the test statistic of the Arellano-Bond tests for first-order and second-order serial correlations in first-differenced residuals, respectively. Superscripts ** and *** indicate statistical significance at the 5% and 1% levels, respectively.

The loan approval criteria reflect the looseness of the bank’s approval of the firm’s loan application, which better reflects its willingness to bear risk, but does not directly indicate the number of funds lent to the firm. Thus, this paper uses the bank loan scale as another measure of banks’ on-balance sheet risk-taking, and the results of the analysis are shown in column (2) of Table 6. The estimated coefficient of

Commercial banks will also adjust their risk-taking through off-balance-sheet operations such as entrustment and trust lending. Some pieces of literature discuss whether shadow banking is pro-cyclical or counter-cyclical (Huang, 2018; Zhang, 2020). Whether shadow banking is pro-cyclical or counter-cyclical, it shows that bank risk-taking is closely related to shadow banking. Not only that, this paper argues that banks may also adjust their on-balance and off-balance sheet business structures to change their risk-taking. The coefficient

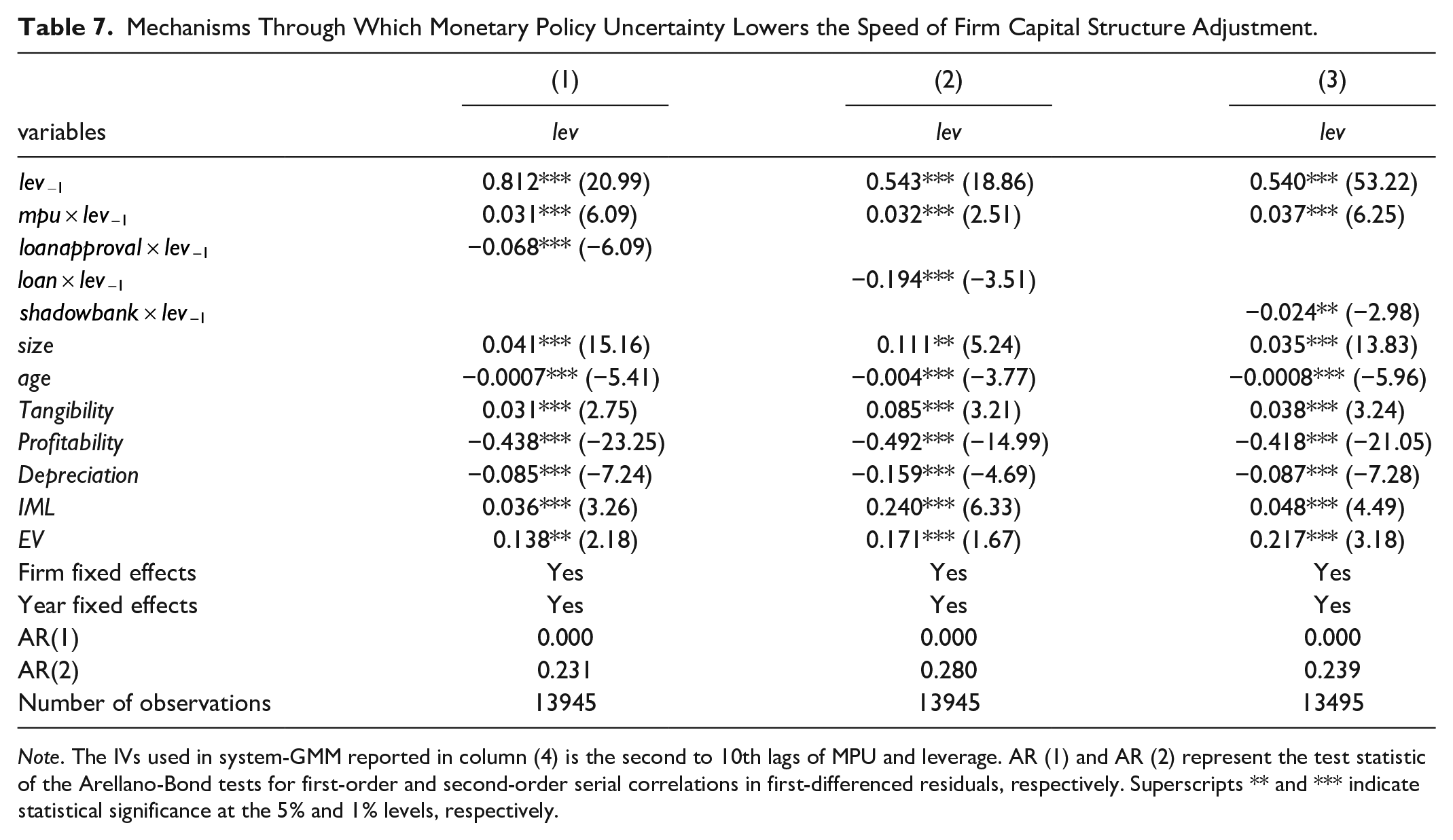

Mechanisms Through Which Monetary Policy Uncertainty Lowers the Speed of Firm Capital Structure Adjustment

In section 2, we have identified three potential mechanisms through which monetary policy uncertainty affects the adjustment of optimal/target capital structure, that is, the loan approval criteria, bank credit scale, and shadow banking scale. We have investigated whether monetary policy certainty affects leverage target in section 4.1, finding that monetary policy uncertainty lowers the speed of firm capital structure adjustment. In this subsection, we examine through which mechanism monetary policy uncertainty lowers the speed of firm capital structure adjustment. The results are presented in Table 7.

Mechanisms Through Which Monetary Policy Uncertainty Lowers the Speed of Firm Capital Structure Adjustment.

Note. The IVs used in system-GMM reported in column (4) is the second to 10th lags of MPU and leverage. AR (1) and AR (2) represent the test statistic of the Arellano-Bond tests for first-order and second-order serial correlations in first-differenced residuals, respectively. Superscripts ** and *** indicate statistical significance at the 5% and 1% levels, respectively.

Through the loan approval criteria

Based on Baron and Kenny [44], we introduce an intermediary variable: loan approval criteria, the results are reported in Table 7. In column (1) of Table 5 the coefficients

Compared to column (4) of Table 5, the coefficient on the impact of monetary policy uncertainty on target leverage ratios declines from 0.048 to 0.031. And compared to column (1) of Table 6 the absolute value of the loan approval criteria coefficient decreases from 0.077 to 0.068, with significance at the 1% level. Combined with the finding that monetary policy uncertainty negatively affects loan approval criteria in the impulse response analysis in section 2.3, it can be confirmed that loan approval criteria play a mediating role in the causal relationship that monetary policy uncertainty affects the adjustment of firms’ capital structure. The results provide evidence that high monetary policy uncertainty leads to a lower target leverage ratio by tightening the loan approval criteria.

Through the scale of bank credit

When there is a higher uncertainty in monetary policy, banks change their risk-taking by adjusting their on-balance sheet business structures. As higher monetary policy uncertainty tends to banks be more inclined to postpone lending or tighten credit scale and raise lending rates, the effects of monetary policy uncertainty on leverage target through bank credit scale is expected to be negative. Given that we find evidence that monetary policy uncertainty lowers leverage target.

Column (2) in Table 7 reports the result of system-GMM analyses designed to test the bank credit scale channel for leverage target. Compared to column (4) of Table 5, the coefficient on the impact of monetary policy uncertainty on target leverage ratios declines from 0.048 to 0.032. And compared to column (2) of Table 6 the absolute value of the bank credit scale coefficient decreases from 0.238 to 0.194, with significance at the 1% level. Combined with the finding that monetary policy uncertainty negatively affects bank credit scale in the impulse response analysis in section 2.3, it can be confirmed that bank credit scale plays a mediating role in the causal relationship that monetary policy uncertainty affects the adjustment of firms’ capital structure. The results show provide evidence that heightened monetary policy uncertainty leads to a lower target leverage ratio by narrowing the scale of bank credit.

Through the shadow banking scale

The effects of monetary policy uncertainty on leverage target through shadow banking scale is expected to be negative. Column (3) in Table 7 reports the result of system-GMM analyses designed to test the shadow banking scale channel for leverage target. Compared to column (4) of Table 5, the coefficient on the impact of monetary policy uncertainty on target leverage ratios declines from 0.048 to 0.037. And compared to column (3) of Table 6 the absolute value of the bank credit scale coefficient decreases from 0.028 to 0.024, with significance at the 1% level. Combined with the finding that monetary policy uncertainty negatively affects shadow banking scale in the impulse response analysis in section 2.3, it can be confirmed that shadow banking plays a mediating role in the causal relationship that monetary policy uncertainty affects the adjustment of firms’ capital structure. The results show provide evidence that heightened monetary policy uncertainty leads to a lower target leverage ratio by narrowing the scale of shadow banks.

The analyses reported above show evidence supporting the loan approval criteria channel, bank credit scale, and shadow banking scale channel. The results suggest that monetary policy uncertainty decreases the scale of bank credit and shadow banking, narrows loan approval criteria. These analyses are consistent with Taylor’s (2017) questioning of unconventional monetary policy, and the “Great Recession” following the global financial crisis was largely associated with central banks exhibiting an increasingly pronounced tendency to make camera decisions.

Additional Analyses

Analysis of why banks shrink their shadow banking

From section 4.3 we know that monetary policy uncertainty not only reduced the scale of bank credit and tightened credit approval criteria, but also reduced the scale of shadow banking. However, during the economic downturn, the speed of shadow banking increased very fast, which made up for the lack of loans to a certain extent and supported the development of small and micro-enterprises. An interesting question, then, is what causes banks to shrink their shadow banking.

Li et al. (2020) argues that the rapid expansion of shadow banking leverage has accumulated significant risk. For mortgage intermediaries closely linked to shadow banking, both the inherent instability and the risk of runs may affect the stability of the financial system (Claessens et al., 2012). In addition, shadow banking changes the legislative, incentive, and disciplinary models of the banking industry (Cabral, 2013). In this context, governments around the world have proposed that shadow banking should be governed in order to maintain the safety and stability of the financial system. For the governance of shadow banking in China, the CBRC issued a series of measures in March and April 2017: on March 28, it issued the Notice on Carrying out Special Control Work on “Regulatory Arbitrage, Short-Transfer Arbitrage, and Associated Arbitrage” in the banking industry, and on April 6, it issued the Notice on Carrying out Special Control Work on “Regulatory Arbitrage, Short-Transfer Arbitrage, and Associated Arbitrage” in the banking industry. “On April 10, it issued the Guidance Opinions on Risk Prevention and Control in the Banking Industry, and on April 12, it issued the Notice on Effectively Fixing Supervisory Shortcomings and Improving Supervisory Effectiveness.” This series of measures will undoubtedly have an important impact on the development of shadow banking. Therefore, to investigate whether these measures lead banks to reduce the scale of their shadow banking, the following test model is employed in this paper.

where

Table 8 reports that the regression coefficient

Analysis of Why Banks Shrink Their Shadow Banking.

Indicates statistical significance at the 1% level.

Robustness tests

As discussed above, our method as a monetary policy uncertainty measure has some advantages over alternative monetary policy uncertainty measures. However, many alternative monetary policy uncertainty measures have been used in the literature. And combined with the fact that China’s monetary policy intermediation target framework is in the process of changing from quantity-based to price-based, so this paper follows Li et al. (2020). in the robustness test to measure the degree of monetary policy uncertainty (

Regression Results Used M2 Growth to Measure MPU.

Note. The IVs used in system-GMM reported in column (4) is the second to 10th lags of MPU and leverage. AR (1) and AR (2) represent the test statistic of the Arellano-Bond tests for first-order and second-order serial correlations in first-differenced residuals, respectively. Superscripts *, ** and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Conclusion

This study investigates how monetary policy uncertainty affects the dynamic adjustment of a firm’s capital structure using a panel data set of China public manufacturers between 2007 and 2018. In this paper, we address this question by first identifying the directional effect of increased monetary policy uncertainty on dynamic adjustment of a firm’s capital structure and then considering through which mechanisms monetary policy uncertainty affects dynamic adjustment of a firm’s capital structure. Using a high-dimensional factor model to measure monetary policy uncertainty in China in a big data environment and the dynamic adjustment of a firm’s capital structure obtained by estimating a partial adjustment model, we find that monetary policy uncertainty lowers the speed of a firm’s capital structure adjustment. This paper also explores several possible mechanisms through which monetary policy uncertainty could influence the speed of a firm’s capital structure adjustment by empirically testing the effects of monetary policy uncertainty on loan approval criteria, bank credit scale, and shadow banking scale. The results suggest that heightened monetary policy uncertainty leads to a lower speed of firms’ capital structure by decreasing bank credit scale and shadow banking scale, tightening loan approval criteria.

Practical Implication

The above research conclusion responds to the second requirement of Friedman (1968) on how to operate monetary policy—monetary authorities should avoid sharp changes in monetary policy, because the basic elements of stable monetary policy are the real source of economic growth. Therefore, maintaining the monetary policy stable is of great significance to further dredge the transmission mechanism of monetary policy and enhance the ability to serve the real economy: First, pay full attention to the negative impact of the uncertainty of monetary policy on the real economy transmitted through bank credit channels, and earnestly “firmly implement the prudent monetary policy.” The results of this paper show that the intensification of monetary policy fluctuation is often accompanied by the relative weakening of bank credit growth and the relative increase of enterprise loan cost, which then constitutes a negative block to the dynamic adjustment of enterprise capital structure. Therefore, the monetary policy authorities should avoid putting the monetary policy into the position of “pushing on a string” due to frequent policy changes while implementing the core logic of the steady and neutral monetary policy of “currency matching economy.” Second, pay attention to the stability and consistency of monetary policy, improve the transparency and forward-looking guidance ability of monetary policy, and give full play to the positive role of reducing the uncertainty of monetary policy in alleviating the constraints on the supply side of bank credit and promoting “stable leverage.” One of the urgent tasks at present is to further improve the operational framework of the interest rate corridor, enhance its transparency and credibility, effectively carry out interest rate guidance and stabilize market expectations in combination with daily open market operations, and create a stable policy environment for macroeconomic transformation and upgrading. Third, in the face of the rising global economic uncertainty, China should closely track the changes in the international and domestic economic and financial situation, find problems in time, and form a scientific and reasonable prediction of the source of economic fluctuations.

Limitations and Future Research

Although a number of recent studies have confirmed the effectiveness of China’s monetary policy interest rate transmission channel (Chen et al., 2018). And using the high-level factor model proposed by Jurado et al. (2015) in the big data environment to estimate the uncertainty of China’s monetary policy can more effectively describe the uncertainty of monetary policy. However, the investigation area of this paper is relatively short. In the future, it is still necessary to further promote the research on the basis of improving the description method of monetary policy uncertainty and expanding the analysis range.

Footnotes

Appendix A

A Description of the Variables Used to Construct the Chinese Monetary Policy Uncertainty Index.

| Variables | Calculation |

|---|---|

| Money supply M0 | Current year-on-year growth rate |

| Money supply M2 | Current year-on-year growth rate |

| Money supply M3 | Current year-on-year growth rate |

| Deposit reserve ratio | Level value |

| Rediscount rate | Level value |

| Loan interest rate (≤1 year) | Level value |

| Loan interest rate (1–5 years) | Level value |

| Loan interest rate (>5 years) | Level value |

| Deposit interest rate (1 year for savings deposits) | Level value |

| Deposit interest rate (2 year for savings deposits) | Level value |

| Deposit interest rate (3 year for savings deposits) | Level value |

| LIBOR: 7-day weighted average | Level value |

| LIBOR: 1-month weighted average | Level value |

| LIBOR: 3-month weighted average | Level value |

| 1-year Treasury term spread | Difference between 1-year Treasury yields and 3-month Treasury yields |

| 3-year Treasury term spread | Difference between 3-year Treasury yields and 3-month Treasury yields |

| 5-year Treasury term spread | Difference between 5-year Treasury yields and 3-month Treasury yields |

| 10-year Treasury term spread | Difference between 10-year Treasury yields and 3-month Treasury yields |

| 1-year 3Afirm bond term spread | Difference between the yield on the 1-year 3A firm bond and 3-month Treasury yields |

| 3-year 3Afirm bond term spread | Difference between the yield on the 3-year 3A firm bond and 3-month Treasury yields |

| 5-year 3Afirm bond term spread | Difference between the yield on the 5-year 3A firm bond and 3-month Treasury yields |

| 10-year 3Afirm bond term spread | Difference between the yield on the 10-year 3A firm bond and 3-month Treasury yields |

| Shanghai Stock Exchange (SSE) Composite Index Yield | Yields obtained using the monthly SSE Composite Index |

| Shenzhen Stock Exchange (SZSE) Composite Index Yield | Yields obtained using the monthly SZSE Composite Index |

| SSE Composite Index Volatility | The conditional standard deviation of the composite index return from GARCH (1, 1) |

| SZSE Composite Index Volatility | The conditional standard deviation of the composite index return from GARCH (1, 1) |

| SSE index turnover rate | Average daily exchange rate to get monthly exchange rate |

| SZSE index turnover rate | Average daily exchange rate to get monthly exchange rate |

| RMB/USD | Level value |

| Real effective exchange rate: BIS | Current year-on-year growth rate |

| National general public budget revenue | Current year-on-year growth rate |

| National general public budget expenditure | Current year-on-year growth rate |

| Consumer price index | Current year-on-year growth rate |

| Retail price index | Current year-on-year growth rate |

| The corporate goods price index | Current year-on-year growth rate |

| Ex-factory price | Current year-on-year growth rate |

| Price index of agricultural means of production | Current year-on-year growth rate |

| Value-added of industries above designated size | Current year-on-year growth rate |

| Macroeconomic Sentiment Index: Leading Indicators | Current year-on-year growth rate |

| Macroeconomic Sentiment Index: Consensus Index | Current year-on-year growth rate |

| Macroeconomic sentiment index: lagging index | Current year-on-year growth rate |

| Macroeconomic sentiment indicators: early warning indicators | Current year-on-year growth rate |

| Purchasing Managers Index: Manufacturing | Current year-on-year growth rate |

| Total retail sales of social consumer goods | Current year-on-year growth rate |

| Fixed asset investment: cumulative | Current year-on-year growth rate |

Appendix B

In order to investigate the interaction between capital structure adjustment and monetary policy uncertainty from multiple levels, the variance decomposition of panel data prediction is the result of its own disturbance term, mainly to investigate the contribution rate of disturbance term to the prediction mean square deviation in PVAR model. According to the variance decomposition results in Table B1, the contribution of monetary policy uncertainty to capital structure adjustment is 7.1%.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: “Key Projects of Social Science Planning in Anhui Province of China (AHSKZ2019D026).”