Abstract

The purpose of this article is to investigate the role of securities analysts in Chinese stock market. Taking the earnings announcements of listed companies, analysts’ earnings forecast and analysts’ recommendations in Chinese stock markets from 2014 to 2018 as the samples, this paper explores the influence mechanism of investor sentiment on the market reaction to announcements, and investigates the influence mechanism of investor sentiment on the role of securities analysts under the framework of behavioral finance theory. On the basis of theoretical analysis, this paper empirically tests the relationship between the information content of analysts’ reports and the information content of the earnings announcements from the perspective of behavioral finance, and discusses the role of securities analysts in the stock market. The results show that during the periods of high investor sentiment, securities analysts do not demonstrate the role of information competition or information supplement. On the other hand, during the periods of low investor sentiment, securities analysts play the role of information competition or information supplement. Furthermore, after excluding the investor sentiment component of the market reaction to announcements, securities analysts do not demonstrate the role of information competition, but play the role of information supplement. The findings of this study offer new insights into the role securities analysts play in Chinese stock market, which is conducive to improving the quality of analysts’ reports, thus enhancing the efficiency of the securities market.

Introduction

Securities analysts are an important information intermediary in securities markets. They use various channels to collect private information and provide the market with forecast information about the future business performance of listed companies. They also use their professional knowledge to analyze the financial reports of listed companies and provide investment suggestions to market participants. Reports provided by analysts and competition among analysts improve the information efficiency of securities prices (Fosu et al., 2017; Livnat & Zhang, 2012). The securities market in China has developed rapidly in recent years, but it is still not mature compared with that in Europe and America. On the one hand, financial fraud of listed companies still occurs frequently, and information asymmetry is still serious, and the protection of minority investors still needs to be improved (Wang, Chen, et al., 2017; Yiu et al., 2019). On the other hand, the size of securities analysts has reached 3595 by 2020, and they have become more and more important participants in China’s securities market (Li et al., 2020). Under the context of securities market in China, it is of great theoretical and practical significance to study whether securities analysts provide investors with incremental valuable information and what role securities analysts play. The research helps to promote the development of the securities analysts industry, protect the interests of minority investors, and improve the efficiency of the securities market. At the same time, this study also has reference significance for the development of securities market and analyst industry in other developing countries.

Extant studies usually judge the role of securities analysts in the financial market by examining the relationship between the market reaction of securities analysts’ reports and the market reaction of earnings announcements of listed companies. But this approach ignores the impact of investor sentiment on the market response to the announcements. Behavioral finance theory points out that investors often have some psychological bias when facing new information, such as overconfidence, representativeness, and prudence (Baker & Wurgler, 2007). In the short term, the psychological bias among individual investors is not mutually offset, but contagious and converging among them, so that the market is often controlled by certain sentiment (Bekiros et al., 2017). Under the influence of investor sentiment, arbitrage in traditional financial theory is difficult to play a role, so there is a systematic deviation in investors’ response to the announcements (Seok et al., 2019). The securities market in China was set up late, the system construction is relatively backward, the market speculation atmosphere is relatively strong, and the market often experienced boom and crash. China’s Shanghai composite index, for example, went from the bull market to the bear market in 2007 to 2008 and again in late 2014 and 2015, with a rise and fall of more than 60% in 1 year. It is difficult to use the traditional financial theory to explain the drastic fluctuation of the securities market based on the changes of macroeconomy and corporate fundamentals. Undoubtedly, investor sentiment has played a role in the irrational rise and panic decline of the securities market (Guo et al., 2017).

Based on the above theoretical and practical background, we aim to answer the following questions: first, do security analysts provide incremental valuable information to investors? What role have they played in the securities market? Second, how does investor sentiment affect the role of securities analysts? Third, after removing the investor sentiment component of the market reaction of information announcements, do securities analysts play a role of information competition or information supplement? In order to answer the above questions, we first explore the influence mechanism of investor sentiment on the role of securities analysts based on cognitive coordination theory in experimental psychology and behavioral finance theory. Then we select the source indicators that can reflect the investor sentiment in China’s securities market, and construct the composite index of investor sentiment through the principal component analysis. We construct a two-stage regression model to test the relationship between the market response of securities analysts’ reports and the market response of earnings announcements of listed companies, so as to judge the role of securities analysts, and put forward policy suggestions for improving the development of the securities analyst industry according to the research conclusions.

The contributions of this paper are as follows: Firstly, we select individual sentiment indicators and eliminate the influence of macroeconomic factors, and construct a composite index reflecting investor sentiment in China’s stock market through principal component analysis. Secondly, based on the behavioral finance theory, we explore the impact mechanism of investor sentiment on the role of securities analysts. Thirdly, we consider the impact of investor sentiment on the market reaction to announcements, and divide the market reaction of the announcements into investor sentiment component and non-investor sentiment component. After removing the investor sentiment component, we test the relationship between the market reaction of securities analysts’ reports and the market reaction of earnings announcements of listed companies, so as to determine the role of securities analysts.

The remainder of this paper is arranged as follows. Firstly, we conduct the theoretical analysis. Secondly, we present the literature review and theoretical hypotheses. Thirdly, we describe the construction of variables, econometric methodology, and sample design. Then we test the theoretical hypotheses. Finally, we discuss the results, and summarize the theoretical and practical implications.

Theoretical Analysis

The Theoretical Basis of the Influence of Emotion on the Actor’s Decision Making

Most of the research on decision making in capital market has ignored the influence of emotion. The decision-making of investors is considered as a cognitive process, in which a variety of alternative actions will be evaluated and those that produce the most positive results will be selected. Actors are supposed to evaluate the possible results of their decisions without any emotional factors and choose the actions that can maximize their “utility.” However, a large number of experimental psychological evidence shows that emotion has a significant impact on actor’s judgment and decision-making, and adding emotional factors into the decision-making model can significantly improve the explanatory power of the model.

According to the cognitive coordination theory in psychology, emotions can influence the decision making of actors from two aspects: information processing mode and risk preference (Loewenstein, 2000). On the one hand, the actor’s mood reflects the environment he is in, pessimism reflects the adverse environment, and optimism reflects the favorable environment. The actors’ information processing strategy is to adjust to the environment. The adverse environment will lead the actors to adopt the systematic and detail-oriented processing mode spontaneously. On the contrary, the favorable environment encourages the spontaneous use of a processing style that relies on existing knowledge structures and practices (Schwarz, 2002). The evidence from experimental psychology shows that, compared with actors in negative emotions, actors in positive emotions are unreasonably optimistic about their own abilities and future environment, so positive emotions encourage actors to rely on their own intuition and instincts instead of comprehensive and careful analysis of information (Constantinescu & Constantinescu, 2017). On the other hand, emotions have an impact on risk appetite, which may not be as stable as economic theory suggests (Lee & Andrade, 2015). When experimental subjects are faced with the same decision problem, they often make different choices under different conditions (Lerner et al., 2015). Kugler et al. (2012) found that when the probability of loss was high, pessimism would discourage risk-taking, and subjects tended to be more cautious or self-protective. When the probability of loss is low, optimism encourages risk-taking (Heilman et al., 2010).

The Role of Security Analyst Under the Framework of Behavioral Finance Theory

Some studies have found that securities analysts play a role of information competition or information supplement (Chen et al., 2010; Francis et al., 2002; Frankel et al., 2006). These literatures usually judge the role of securities analysts by analyzing the relationship between the market reaction of securities analysts’ reports and the market reaction of earnings announcements of listed companies. However, these literatures often follow the efficient market theory when studying the market reaction of the information announcements in the securities market, believing that asset prices have rapidly and fully absorbed the available information in the market (Pevzner et al., 2015). Researchers usually use the event study method to take the accumulative abnormal return of stock price in the announcement event window as the impact of events on investors’ value, but this view ignores the impact of investors’ psychological bias on the market reaction of announcements. Therefore, more and more researchers begin to study financial problems from the perspective of experimental psychology, in an attempt to correct the defects of traditional theories. Based on the research results of experimental psychology, behavioral finance theory studies and explains the phenomena in financial market basing on bounded rational individuals, group behavior and inefficient market, and from the actual decision-making psychology of investors (Kahneman & Tversky, 2013).

Behavioral finance theory provides a new perspective for investigating the market reaction of announcements in capital market. Various announcements in the capital market bring information about the company’s future earnings and cash flow. The response of stock price to these announcements includes investors’ valuation of incremental cash flow (Rogers & Van Buskirk, 2013). During periods of high sentiment, investors are more likely to give optimistic estimates of the incremental cash flow reflected in the announcements, thus the positive market reaction to good news increases, while the negative market reaction to bad news decreases. On the contrary, during periods of low sentiment, investors are more likely to give pessimistic estimates, thus the positive market reaction to good news will decrease, while the negative market reaction to bad news will increase (Mian & Sankaraguruswamy, 2012). Therefore, the market reaction of announcement in the capital market contains two parts: emotional component and non-emotional component. Figure 1 summarizes the theoretical mechanism of the impact of investor sentiment on market response to announcements.

Theoretical mechanism of investor sentiment influencing announcements.

In the framework of behavioral finance theory, the analysis of the role of securities analysts must consider the impact of investor sentiment. In the period of high investor sentiment, the overoptimism of actors leads them to rely on their own intuition and instinct rather than comprehensive and careful analysis of information, thus paying little attention to analysts’ earnings forecasts and reports (Hirshleifer, 2015). Therefore, during periods of high investor sentiment, there may be no significant correlation between the market reaction of analysts’ earnings forecast or reports and the market reaction of earnings announcement of listed companies, and securities analysts do not show the role of information competition or information supplement. In the period of low investor sentiment, the investors pay more attention to the details of information (Corredor et al., 2013), so as to strengthen the attention and response to analysts’ earnings forecasts and reports, which leads to a negative correlation between the market response of listed companies’ earnings announcement and the market response of analysts’ earnings forecasts, and a positive correlation between the market response of analysts’ reports and the market response of listed companies’ earnings announcements. Therefore, during periods of low investor sentiment, the earnings forecast issued by securities analysts reflects the role of information competition, while the analyst report reflects the role of information supplement. Figure 2 shows the theoretical mechanism of the impact of investor sentiment on the role of securities analysts in the framework of behavioral finance theory.

The theoretical mechanism of the impact of investor sentiment on the role of securities analysts.

Literature Review and Theoretical Hypothesis

Investor Sentiment

Investor sentiment is the belief of investors about future cash flow or discount rate, but this belief can not be supported by fundamental information (Baker & Wurgler, 2006). The extant researches on investor sentiment mainly include the following aspects: the measurement of investor sentiment, the impact of investor sentiment on financial asset prices and the impact of investor sentiment on corporate decision-making behaviors. The measurement of investor sentiment includes objective indicators and subjective indicators. The objective indicators are based on the actual trading behavior of investors and measures investor sentiment with the trading statistics in the stock market. The objective indicators commonly used in literature include the discount of closed-end fund, turnover rate, IPO issuance, IPO first-day return, and the number of newly opened accounts in the stock market, etc. (Baker & Wurgler, 2006; Wu et al., 2018). The subjective indicators usually obtain data through questionnaire survey, which reflects investors’ expectations and judgments on the future trend of the market. Subjective indicators mainly include the survey data of American Association of Individual Investor (AII) and Investors Intelligence (II) (Brown & Cliff, 2005). But there is still controversy about these indicators in reflecting investor sentiment (Brown & Cliff, 2005). In order to overcome the defects of a single indicator, Baker and Wurgler (2006) selected six single indicators, such as the discount of closed-end fund, and used principal component analysis to construct a composite index of investor sentiment. Since then, many studies have used this method to construct the investor sentiment composite index of many countries and regions in the world (Dash & Mahakud, 2012; Ding et al., 2017; Finter et al., 2012). After solving the measurement of investor sentiment, many scholars turn to study the impact of investor sentiment on financial asset prices. The researches in this field mainly include investor sentiment and stock returns (Baker & Wurgler, 2006; Brown & Cliff, 2005; Ni et al., 2015), and investor sentiment and capital market anomalies (Ali & Gurun, 2009; Livnat & Petrovits, 2009; Mian & Sankaraguruswamy, 2012). The effect of investor sentiment on corporate decision-making behaviors is another area of concern. Researches in this area mainly include investor sentiment and corporate financing (Alti, 2006; McLean & Zhao, 2014), investor sentiment and corporate investment (Polk & Sapienza, 2009), investor sentiment and corporate information disclosure (Bergman & Roychowdhury, 2008; Brown et al., 2012), investor sentiment and corporate M&A (Rhodes-Kropf et al., 2005).

Securities Analysts

Both managers and securities analysts try to solve the uncertainty of the company’s future earnings and cash flows. Although they get information in different ways, they can find valuable information. If one party discovers and discloses the information first, there will be a substitution effect on the subsequent information announcement of the other party (Chen et al., 2010). Empirical evidence supports the information substitution role of securities analysts. Piotroski and Roulstone (2004), and Kim et al. (2011) found that the information content of the earnings announcement decreased with the analyst’s report. Choi et al. (2011) found that when the annual stock returns were regressed to the earnings of the same period and the future earnings, the coefficient of the earnings of the same period decreased with the number of analysts tracking, while the coefficient of the future earnings increased with the number of tracking analysts. These results suggest that the more analysts follow a company, the more timely information about future earnings from analysts is incorporated into its share price, consistent with the news that analyst report replacing earnings. The evidence of Loh and Stulz (2011) shows that the information content of analysts’ earnings forecast increases sharply in the week before the earnings announcement, while it is the lowest in the week after the earnings announcement.

Market participants have different abilities to interpret public information, so the role of securities analysts is particularly important (Ioannou & Serafeim, 2015). Securities analysts can use their expertise to help investors understand the accruals, discuss the effects of changes in accounting methods and restate financial reports to ensure the comparability of accounting information after mergers and acquisitions, thus providing investors with information of incremental value (Chen et al., 2010). Kim and Song (2015) found that the analyst recommendation did not replace the earnings announcement information, and the positive correlation between the market reaction to analyst report and the market reaction to the earnings announcement was significantly enhanced during the sample period. The evidence of Merkley et al. (2017) shows that the information content of analysts’ reports and the timeliness of financial reporting information are mutually complementary. Therefore, more timely financial reporting information is associated with more informative analyst reports, rather than hollowing out the information content of analyst reports.

However, in the context of the Chinese stock market, some studies have found evidence that contradicts the prevailing view. Zhang et al. (2017) found that the market reaction of analyst reports was not significant and investors did not pay attention to analyst reports. Li, Li, et al. (2017) studied the market reaction of analysts’ stock recommendation, and the empirical results showed that stocks recommended by analysts had significantly negative excess returns. These studies support some characteristics of China’s stock market that are different from those of European and American countries. On the one hand, there are a large number of minority investors in China’s stock market, and the market efficiency is low. Analysts’ earnings forecasts largely rely on private information, and investors underreact to analysts’ earnings forecasts (Zhang et al., 2017). On the other hand, there are still some irregularities in the securities analyst industry in China, such as the quality of securities analysts is uneven, and the interest collusion between analysts and listed companies, etc. (Wang, Wei & Han, 2017). Therefore, in China’s securities market, whether securities analysts provide valuable incremental information, whether they play the role of information competition or information supplement, is still worthy of further discussion.

Theoretical Hypothesis

A limitation of the above research on the role of securities analysts is that it ignores the impact of investor sentiment. China’s stock market has developed rapidly since its establishment, but compared with the stock markets of developed countries in Europe and the United States, it is still in a relatively developing stage. China’s stock market has institutional features such as restriction on rise and fall and restriction on short selling, which makes many risk factors in the market unable to be eliminated in time, it is difficult to arbitrage, and noise trading often dominates the market price. Secondly, individual investors play a dominant role in China’s stock market. Individual investors lack professional investment knowledge and are in information disadvantage, so they often show irrational investment behavior. Therefore, the price in the stock market contains the irrational factors of investors. Reviewing the development course of the Chinese stock market over the past 30 years, the boom and crash happens from time to time. The stock market rose sharply in the first half of 2015, reaching a record high of 5,176 in June, and the market index fell by nearly 50% in the following 3 months. China’s stock market suffered a huge drop of nearly 7% on its first day of trading in 2016, when the circuit-breaker system was formally implemented. In a short period of about 1 month from February to March 2021, China’s growth enterprise index fell by 25%. However, these sharp ups and downs in China’s stock market can not be explained by macroeconomic fundamentals, and investor sentiment has a significant impact on the market. Therefore, the behavioral finance theory based on investor irrationality, limited arbitrage and limited market efficiency is more suitable for the research in the context of Chinese stock market (Han & Li, 2017).

Extant literature often studies the role of analysts by examining the relationship between the market reaction to analyst reports and the market reaction to earnings announcements. But these studies ignore the effect of investor sentiment. Based on the behavioral finance theory, a growing number of studies have found that investor sentiment has a significant impact on the market reaction to announcements in China’s stock market (Li et al., 2021). Behavioral finance theory draws on the research results of experimental psychology. According to the cognitive coordination theory in psychology, emotions can influence actors’ decision-making from two aspects: information processing mode and risk preference (Loewenstein, 2000).On the one hand, emotion reflects the actor’s environment, pessimism reflects the adverse environment, and optimism reflects the favorable environment. The actor’s information processing strategy is to adapt to the environment. The adverse environment will lead the actor to adopt the systematic and detail-oriented processing mode spontaneously. On the contrary, favorable environment will encourage the spontaneous use of processing styles that rely on existing knowledge structures and practices (Schwarz, 2002).The evidence from experimental psychology shows that, compared with actors in negative emotions, actors in positive emotions are unreasonably optimistic about their own abilities and future environment, so positive emotions encourage actors to rely on their own intuitions and instincts instead of comprehensive and careful analysis of information (Constantinescu & Constantinescu, 2017).On the other hand, emotion has an impact on risk preference. When the subjects face the same decision-making problem, they often make different choices under different conditions. When the probability of loss is high, pessimism will hinder the risk of trying. Optimism encourages risk-taking when the probability of loss is low (Lerner et al., 2015).Experimental results show that in an environment with a high probability of loss, actors tend to be more cautious or protect themselves (Kugler et al., 2012).

Cognitive coordination theory and its experimental evidence provide a basis for investigating the impact of investor sentiment on the market response to announcements. Under the framework of behavioral finance theory, during the periods of high investor sentiment, investors tend to overestimate the company’s future earnings and cash flow. They tend to invest depending on the market situation and personal experience, ignore the risk factors in the market, and pay less attention to the earnings announcements of companies and analysts’ reports. Therefore, there is no significant relationship between the market reaction to earnings announcements of companies and the market reaction to analyst reports. On the contrary, during the periods of low investor sentiment, investors are overly pessimistic about the company’s future earnings and cash flow, and they tend to favor a more cautious investment style. Meanwhile, investors tend to pay more attention to earnings announcements of companies and analyst reports, and try to dig out the details of information, so as to be more sensitive to the announcements in the market. Therefore, there is a significant relationship between the market reaction to earnings announcements of companies and the market reaction to analyst reports. Based on the above analysis, this paper proposes the following theoretical hypotheses:

H1: During the period of high investor sentiment, securities analysts do not demonstrate the role of information competition or information supplement.

H2: During the period of low investor sentiment, securities analysts demonstrate the role of information competition or information supplement.

Earnings announcements of companies and analyst reports convey information about the company’s future earnings and cash flows, and the reaction of the stock price to the announcements includes investors’ valuation of these incremental cash flows. According to behavioral finance theory, investors are more likely to be optimistic about the incremental cash flow reflected in announcements during the periods of high sentiment, and more likely to be pessimistic about that during the periods of low sentiment. Good news usually reflect positive incremental cash flow. Optimistic estimates during the periods of high sentiment and pessimistic estimates during the periods of low sentiment mean stock price rises more in the periods of high sentiment than in the periods of low sentiment. On the other hand, bad news usually reflect negative incremental cash flow, and optimistic estimates during periods of high sentiment and pessimistic estimates during periods of low sentiment mean that stock prices fall less during periods of high sentiment than during periods of low sentiment. Obviously, the market reaction to the announcements can be decomposed into investor sentiment component and non-investor sentiment component. Therefore, after removing the investor sentiment component of the market reaction to earnings announcements and analysts’ reports, we can more accurately find the correlation between them and thus judge the role played by securities analysts in the Chinese stock market. There are two opposite views on the role of securities analysts in China’s stock market. One view is that securities analysts provide investors with incremental valuable information, so analysts play the role of information competition or information supplement (Fang et al., 2018). However, another view is that the quality of securities analysts in China is uneven, and some analysts are even reported to collude with listed companies. Investors pay little attention to analyst reports due to their poor quality (Wang, Wei & Han, 2017).Therefore, analysts do not play the role of information competition or information supplement. Therefore, this paper puts forward the following two opposite theoretical hypotheses:

H3a: After removing the investor sentiment component in the market reaction of the information announcement, securities analyst demonstrate the role of information competition or information supplement.

H3b: After removing the investor sentiment component in the market reaction to the information announcement, securities analysts do not show the role of information competition or information supplement.

Variables, Econometric Methodology, and Sample Design

Variables

Investor sentiment

Baker and Wurgler (2006) first used the principal component analysis to construct a composite investor sentiment index based on six sentiment proxy variables: the discount rate of closed-end funds, the turnover ratio of the stock, the number of IPOs, the first day return of IPOs, the share of equity issues in total equity and debt issues, dividend premium. Since then, this method has been used in many studies. However, the sentiment proxy variables used by Baker and Wurgler (2006) may not be fully applicable to the construction of investor sentiment index of Chinese stock market, because the stock market in China has its own characteristics. For example, China adopts IPO approval system, which results in that the number of IPOs is largely affected by the government regulation. In addition, the dividend policy of China’s listed companies lacks continuity, and many listed companies in China don’t pay dividends for years. All these lead to the fact that some sentiment proxies are not appropriate for the Chinese stock markets. Therefore, in order to select the sentiment proxies suitable for China’s stock markets, and exclude subjectivity in choosing them as much as possible, we select nine proxies that may reflect investor sentiment in Chinese stock markets. Specifically, these proxies include the closed-end fund discount, market turnover rate, trading volume, IPO first-day return, number of newly opened investor accounts, equity issue in total issue, the ratio of the number of rising and falling, price-earnings ratio of the market, consumer confidence index. The results of correlation analysis between China’s stock market index and the above single sentiment proxies show that the correlation coefficients of the five proxies (the closed end fund discount, equity issue in total issue, the ratio of the number of rising and falling, price earnings ratio of the market and consumer confidence index) are not significant, so they are excluded. For the discount of closed end fund (DCEF) and consumer confidence index (CCI) that are commonly used in studies, we draw the line diagrams of the comparison between the two proxies and China’s stock market index in the appendix to further prove the inapplicability of these two proxies. Finally we obtain the following sentiment proxies: market turnover rate (TURN); trading volume (Volume), IPO first-day return (IPOR); number of newly opened investor accounts (NIA). Furthermore, the cumulative variance contribution rate of the principal component analysis of the above four proxies reached 91.9%, indicating that the elimination of the remaining proxies had almost no impact on the overall information content. According to the principle of marginal effect, with the increasing of selected proxies, the overall information content will gradually increase, but the information content of individual proxy will gradually decrease. Here the sentiment proxies decreased from nnie items to four items, and the overall information content only decreased by about 8%, but the information content of single proxy increased by 2.53 times, which proved that the four proxies selected in this paper were reasonable. It is worth noting that these sentiment proxies are affected by both investor sentiment and macroeconomic factors. Here we call sentiment proxies excluding the influence of macroeconomic factors the purer sentiment proxies. To remove the effect of macro economy, we extract the residuals as the purer sentiment proxies by regressing each sentiment proxy on macroeconomic variables. These macroeconomic variables include the growth rate of industrial added value, macroeconomic prosperity index, consumer price index and producer price index. After standardizing the purer sentiment proxies, we use the principal component analysis to construct the Chinese investor sentiment index, the resulting index is as follows:

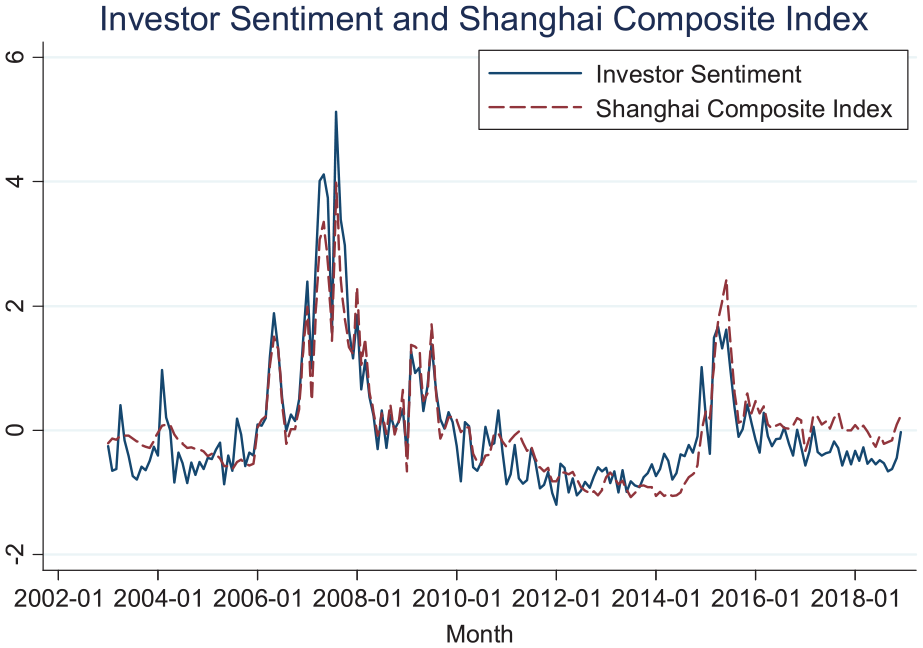

Figures 3 to 6 show the time series charts of market turnover rate (TURN), trading volume (VOLUME), IPO first-day return (IPOR), and new investor account opening number (NIA) and investor sentiment index, respectively. These figures show that the source indicators and investor sentiment index basically maintain the same trend of change, indicating that the four source indicators selected in this paper are reasonable, reflecting the changes of investor sentiment in China’s stock markets. Furthermore, the period of positive investor sentiment index is defined as the periods of high investor sentiment, and the periods of negative investor sentiment index is defined as the period of low investor sentiment. Figures 7 and 8 show the relationship between investor sentiment and China’s Shanghai Composite Index and Shenzhen Component Index. It can be seen from the figures that the investor sentiment index constructed in this paper is roughly consistent with the volatility of the stock index, indicating that there is a significant correlation between investor sentiment and China’s stock market index.

Investor sentiment and market turnover.

Investor sentiment and volume.

Investor sentiment and IPO first-day return.

Investor sentiment and the number of new investors opening accounts.

Investor sentiment and Shanghai Composite Index.

Investor sentiment and Shenzhen Component Index.

Information content of information announcement (IC)

This paper measures the information content of analysts’ reports and earnings announcements by the cumulative abnormal return (CAR) of the event window. The calculation window of the information content of the earnings announcement includes the trading day of the earnings announcement and the trading day before and after the earnings announcement day, namely [−1, 1]. The calculation window of analyst report information content is the release date. The information content of the earnings announcement is recorded as EAIC, the non-investor sentiment component as EAIC_NS, and the investor sentiment component as EAIC_S. The information content of the analyst report is recorded as ARIC, the non-investor sentiment component is recorded as ARIC_NS, and the investor sentiment component is recorded as ARIC_S.

Unexpected earnings (UE)

This paper adopts the following method to measure unexpected earnings:

Where Earnings i,t is the actual earnings of the current period; Earningsi,t–1 is the actual earnings of the previous period and represents the expected earnings of the current period. Pi,t–1 is the stock price at the end of last period. In the analysis, this paper divides the earnings announcement into good news and bad news. If UE > 0, the earnings announcement is a good news, recorded as UEUp; If UE < 0, earnings announcement is a bad news, denoted as UEDown.

Unanticipated analyst earnings forecast (UAF)

This paper uses the following methods to measure the earnings forecast of unexpected analysts:

Where AFi,t is the analyst’s earnings forecast of this period; Earningsi,t–1 is the actual earnings of the previous period; Pi,t–1 is the stock price at the end of last period. In the analysis, this paper divides analysts’ earnings forecast into good news and bad news. If UAF > 0, analysts’ earnings forecast is a positive news, recorded as UAFUp; If UAF < 0, the analyst’s earnings forecast is a negative news, recorded as UAFDown.

Analyst recommendation (EV)

The recommendations of analysts’ reports on stocks are divided into five grades: sell, underweight, neutral, overweight and buy. If the five grades are represented by 1 to 5, the explanatory variable EV is the analyst recommendation adjustment variable. If more than one analyst issues the recommendation on the same company on the same day, we measure it by the median of all analysts recommendations. If an analyst’s recommendation is upgraded, recorded as EVUp; if an analyst’s rating is upgraded, recorded as EVDown.

Econometric Method

Test the information content of earnings announcement and the information content of analyst report

We construct equations (4)–(6) to estimate the stock cumulative abnormal returns of earnings announcement, analyst earnings forecast, and analyst recommendation in the event window period respectively.

In the equations (4)–(6), the CAR1, CAR2, and CAR3 represents the stock cumulative abnormal returns of earnings announcement, analyst earnings forecast and analyst recommendation in the event window period respectively. Specifically, the estimated coefficients α1 and α3 represent the earnings response coefficient of positive earnings news and negative earnings news respectively, that is the market reaction caused by unit unexpected earnings. The estimated coefficients α2 and α4 represent the influence of investor sentiment on the earnings response coefficients of positive earnings news and negative earnings news respectively. The estimated coefficients β1 and β3 represent the response coefficient of analysts’ positive earnings forecast and negative earnings forecast respectively, that is the market reaction caused by unit unexpected analyst’s earnings forecast. The estimated coefficients β2 and β4 represent the impact of investor sentiment on the response coefficients of analysts’ positive earnings forecasts and negative earnings forecasts respectively. The estimated coefficients γ1 and γ3 represent the response coefficient of analysts recommendation upgrades and downgrades respectively, that is the market reaction caused by the unit measure of analysts recommendation change. The estimated coefficients γ2 and γ4 represent the effect of investor sentiment on the response coefficients of analyst recommendation upgrades and downgrades respectively.

Test the Relationship Between the Information Content of Analysts Earnings Forecasts and the Information Content of Earnings Announcements

Referring to the method of Heckman (2013), this paper constructs the following two-stage model to test the relationship between the information content of analysts’ earnings forecast and the information content of earnings announcement:

When studying the relationship between the information content of analysts earnings forecast and the information content of earnings announcement, there may be endogeneity. The information environment may affect the information content of earnings announcement and the probability of analysts’ publishing forecast report. The self-selection problem results in biased coefficients obtained by OLS regression. To solve this problem, we use the two-stage regression method of Heckman (2013).

The first stage regression equation (7) researches analyst’s decision in releasing earnings forecast before earnings announcement. Where ISSUE_ARi,t–1 is a dummy variable, before the earnings announcement, if the number of analyst’s earnings forecast report of a company is more than the mean of analyst’s earnings forecast for the same period, the value of ISSUE_AR is 1, otherwise it is 0. The second stage regression equation (8) studies the relationship between the information content of analysts’ earnings forecasts and the information content of earnings announcements. Where EAIC is the information content of earnings announcement, ARIC is the information content of analysts’ earnings forecast, and the rest are control variables. Referring to Chen et al. (2010), Livnat and Zhang (2012), the following control variables are added into the models above. Std_CAR and Mean_CAR are the standard deviation and mean of stock returns in the quarter of earnings announcement date. Size equals to the natural logarithm of the total assets of the company; BM is the ratio of book value to market value of the company’ equity; Turnover equals to the volume of trading divided by the total number of shares outstanding. Coverage is the number of analysts followed, equal to the natural logarithm of the number of analysts followed; EXP is the analyst’s forecasting experience, equal to the natural log of the number of days since the analyst’s first earnings forecast; N_shareholders is the number of shareholders, equal to the natural logarithm of the number of shareholders; Inst is the shareholding ratio of institutional investors; PARIC is the information content of analyst’s earnings forecast of previous period; IMR is the Inverse Mills Ratio obtained in the first stage of regression, which is used to control the self-selection effect of analysts’ earnings forecast. QuarterDummy and IndustryDummy are quarterly control variables and industry control variables, respectively. If β1 is significantly negative, it indicates that the analyst’s earnings forecast published before the earnings announcement weakens the market reaction of the earnings announcement, and the securities analyst is demonstrated as the information competition role.

Test the Relationship Between the Information Content of Analyst Recommendation and the Information Content of Earnings Announcement

This paper constructs the following two-stage model to test the relationship between the information content of analyst recommendation and the information content of earnings announcement:

The first stage regression equation (9) has the same meaning as the equation (7). The second stage regression equation (10) studies the relationship between the information content of analyst recommendations and the information content of earnings announcements. If β1 is significantly positive, it indicates that the analysts interpret and evaluate the earnings announcement information after the earnings announcement and put forward investment suggestions. Thus, the information content of analyst recommendations is positively correlated with the information content of the earnings announcement, and the securities analysts is demonstrated as the information supplement role.

Sample Selection and Data

This paper takes the companies listed on the Shanghai and Shenzhen stock markets of China from 2014 to 2018 as samples. Stock market index, share prices and earnings of corporations, the closed-end fund discount, market turnover rate, trading volume and IPO first-day return come from the CSMAR database and RESSET database. Institutional investors holding data are from WIND database. Consumer confidence index is derived from the National Bureau of Statistics web site. The data of new investors opening accounts come from China securities registration and settlement statistic reports. The earnings announcements of listed companies and analyst earnings forecasts data come from CSMAR database, analyst recommendations data are from the web site of security company.

This paper screened the samples according to the following criteria: (1) excluding financial listed companies; (2) excluding ST and PT listed companies. ST is the abbreviation of special treatment. According to the regulations of China’s securities regulatory authorities, if a listed company suffers losses for two consecutive years or its net assets per share are lower than the par value of its shares, it shall be given special treatment. PT is the abbreviation of particular transfer. According to the regulations of China’s securities regulatory authorities, if a listed company suffers losses for three consecutive years, its shares will be suspended from listing. During the suspension of the listing of the company’s shares, the stock exchange provides special transfer services for investors; (3) removing samples with missing financial data; (4) basing on past experience, the analyst reports of each 30 trading days before and after the earnings announcement are selected, and the analyst reports published during the [−1, 1] window period of the earnings announcement are excluded. In order to eliminate the influence of outliers, this paper conducts 99%winsorize processing on variables except investor sentiment. Finally, this paper obtained 13,143 samples of earnings announcements of listed companies, 74,065 samples of analysts’ earnings forecasts (released before earnings announcements), and 69,323 samples of analysts’ recommendations (released after earnings announcements).

Empirical Results

The Relationship Between the Information Content of Analyst Reports and the Information Content of Earnings Announcements During Periods of High Investor Sentiment

Table 1 reports the regression results of the relationship between the information content of analysts’ reports and the information content of earnings announcements during the periods of high investor sentiment. Columns 2 to 5 show the relationship between the information content of analysts’ earnings forecasts (published before earnings announcements) and the information content of earnings announcements. The regression results of the overall sample within 30 trading days before the earnings announcement date and subsamples within every 10 trading days before the earnings announcement date show that the coefficient of the information content (ARIC) of analysts’ earnings forecast is negative, but not statistically significant. The results indicate that analysts’ earnings forecast (released before earnings announcement) does not weaken the information content of earnings announcement, and securities analysts do not demonstrate the role of information competition during the periods of high investor sentiment. This result provides evidence to H1.

The Relationship Between the Information Content of Analyst Reports and the Information Content of Earnings Announcements During Periods of High Investor Sentiment.

Note. t value is shown in parenthesis. ***, **, and * represent statistically significant at the level of 1%, 5%, and 10%, respectively.

Columns 6 to 9 report the relationship between the information content of analysts’ recommendations (issued after earnings announcements) and the information content of earnings announcements. The regression results of the overall sample within 30 trading days after the earnings announcement date show that the coefficient of earnings announcement information content (EAIC) is positive, but not statistically significant. The regression results of the subsamples within every 10 trading days after the earnings announcement date show that the coefficients of EAIC are all positive, but only the sample group within the window period [2, 11] is significant at the level of 10%, and the other two sample groups are not statistically significant. In general, there is no significant positive correlation between the information content of analysts’ recommendations (issued after earnings announcements) and the information content of earnings announcements, and securities analysts do not play the role of information supplement during the periods of high investor sentiment. This result provides evidence to H1.

In addition, the coefficient of the inverse mills ratio (IMR) obtained from the first stage regression is only significant in the [−22, −31] sample group, but not in the other sample groups, indicating that there is no significant self-selection problem in the analyst reports samples.

The Relationship Between the Information Content of Analyst Reports and the Information Content of Earnings Announcements During Periods of Low Investor Sentiment

Table 2 reports the regression results of the relationship between the information content of analysts’ reports and the information content of earnings announcements during the periods of low investor sentiment. Columns 2 to 5 show the relationship between the information content of analysts’ earnings forecasts (published before earnings announcements) and the information content of earnings announcements. The regression results of the overall sample within 30 trading days before the earnings announcement date and subsamples within every 10 trading days before the earnings announcement date show that the coefficient of the information content (ARIC) of analysts’ earnings forecast is significantly negative. The results indicate that analysts’ earnings forecast (released before earnings announcement) weakens the information content of earnings announcement, and securities analysts demonstrate the role of information competition during the periods of low investor sentiment. This result provides evidence to H2.

The Relationship Between the Information Content of Analyst Reports and the Information Content of Earnings Announcements During Periods of Low Investor Sentiment.

Note. t value is shown in parenthesis. ***, **, and * represent statistically significant at the level of 1%, 5%, and 10%, respectively.

Columns 6 to 9 report the relationship between the information content of analysts’ recommendations (issued after earnings announcements) and the information content of earnings announcements. The regression results of the overall sample within 30 trading days after the earnings announcement date and subsamples within every 10 trading days after the earnings announcement date show that the coefficient of earnings announcements information content (EAIC) is significantly positive. The results indicate that there is a significant positive correlation between the information content of analysts’ recommendation and the information content of earnings announcement, and securities analysts play the role of information supplement during the periods of low investor sentiment. This result provides evidence to H2.

The Decomposition of the Information Content of Earnings Announcement and the Information Content of Analyst Report

Table 3 reports the impacts of investor sentiment on the market reactions of earnings announcements of listed companies and analysts reports, and the market reactions of these information announcements have been decomposed into the non-investor sentiment component and the investor sentiment component. Columns 1 and 2 report the market reaction of earnings announcements of listed companies. The coefficients of UEUp and UEDown are both positive, which indicates that the market has made a positive response to the positive earnings news and a negative response to the negative earnings news. The coefficient α2 of the interaction term UEUp × Sent is significantly positive, and the coefficient α4 of the interaction term UEDown × Sent is significantly negative, indicating that the market’s response to positive unexpected earnings increases with the rise of investor sentiment, and the response to negative unexpected earnings decreases with the rise of investor sentiment. The response coefficients of positive earnings news and negative earnings news are α1 + α2Sent (0.549 + 0.235sent) and α3 + α4Sent (0.791–0.306sent), respectively, in which α1 and α3 represent the non-investor sentiment component of the market reactions of earnings announcements, α2Sent and α4Sent represent the investor sentiment component of the market reactions of earnings announcements.

The Decomposition of the Information Content of Earnings Announcement and the Information Content of Analyst Report.

Note. t value is shown in parenthesis. ***, **, and * represent statistically significant at the level of 1%, 5%, and 10%, respectively.

Columns 3 and 4 report the impacts of investor sentiment on the market reactions of analysts’ earnings forecasts. The coefficients of UAFUp and UAFDown are both positive, which indicates that the market has made a positive response to the positive analysts’ earnings forecast and a negative response to the negative analysts’ earnings forecast. The coefficient β2 of interaction term UAFUp × Sent is significantly positive, and the coefficient β4 of interaction term UAFDown × Sent is significantly negative, indicating that the market’s response to the favorable analysts’ earnings forecast increases with the rise of investor sentiment, and the response to the negative analysts’ earnings forecast declines with the rise of investor sentiment. The response coefficients of positive and negative analysts’ earnings forecasts are β1 + β2Sent (0.221 + 0.174sent) and β3 + β4Sent (0.275–0.206sent), respectively, in which β1 and β3 represent the non-investor sentiment component of market reaction of analysts’ earnings forecasts, and β2Sent and β4Sent represent the investor sentiment component of market reaction of analysts’ earnings forecasts.

Columns 5 and 6 report the impacts of investor sentiment on the market reactions of analysts’ recommendations. The coefficients of EVUP and EVDOWN are both positive, indicating that the market has made a positive response to the analysts’ positive evaluation and a negative response to the analysts’ negative evaluation. The coefficient γ2 of the interaction term EVUP × Sent is significantly positive, and the coefficient γ4 of the interaction term EVDOWN × Sent is significantly negative, indicating that the market’s response to analysts’ positive evaluation increases with the rise of investor sentiment, and the response to analysts’ negative evaluation declines with the rise of investor sentiment. The response coefficients of positive and negative analysts’ recommendations are respectively γ1 + γ2Sent (0.379 + 0.244 sent) and γ3 + γ4Sent (0.431–0.174sent), respectively, in which γ1 and γ3 represent the non-investor sentiment component of market reaction of analysts’ recommendations, γ2Sent and γ4Sent represent the investor sentiment component of market reaction of analysts’ recommendations.

The Relationship Between the Information Content of Analyst’s Earnings Forecast Report (Released Before the Earnings Announcement) and the Information Content of the Earnings Announcement After Removing the Investor Sentiment Component

Table 4 reports the relationship between the information content of analyst’s earnings forecast and the information content of the earnings announcement after excluding the investor sentiment component of information content. The results show that the coefficient of the non-investor sentiment component (ARIC_NS) of the information content of the analyst’s earnings forecast is negative in all samples of the window period [−2, −31] before the earnings announcement, as well as in the subsample of the window period [−2, −11], [−12, −21], and [−22, −31], but it is not statistically significant. The results indicates that the analyst’s earnings forecast does not weaken the information content of earnings announcement and the securities analyst does not demonstrate the role of information competition after removing the investor sentiment component of market reaction of information announcement. This result provides evidence to H3b.

The Relationship of Non-investor Sentiment Component Between the Information Content of Analyst’s Earnings Forecast Report and the Information Content of the Earnings Announcement.

Note. t value is shown in parenthesis. ***, **, and * represent statistically significant at the level of 1%, 5%, and 10%, respectively.

In addition, the coefficient of the inverse mills ratio (IMR) obtained from the first stage regression is not significant in each sample group, indicating that there is no significant self-selection problem in the analyst’s earnings forecasts samples.

The Relationship Between the Information Content of Analyst’s Recommendation Report (Released After the Earnings Announcement) and the Information Content of the Earnings Announcement After Removing the Investor Sentiment Component

Table 5 reports the results of the relationship between the information content of analyst’s recommendation and the information content of the earnings announcement after excluding the investor sentiment component of information content. The results of all samples in the window period [2, 31] after earnings announcement show that the coefficient of non-investor sentiment component (EAIC_NS) of earnings announcement information content is positive and statistically significant at the level of 10%; The results of each subsample group show that the coefficient of EAIC_NS is positive, and the coefficient of EAIC_NS is statistically significant in the window periods [2, 11] and [12, 21] after earnings announcement, but it is not significant in the window period [22, 31] after earnings announcement. The results indicate that there is a significant positive correlation between the information content of analysts’ recommendation and the information content of earnings announcement. Securities analysts play the role of information supplement after excluding the investor sentiment component of market reaction of information announcement. This result provides evidence to H3a.

The Relationship of Non-investor Sentiment Component Between the Information Content of Analyst’s Recommendation Report and the Information Content of the Earnings Announcement.

Note. t value is shown in parenthesis. ***, **, and * represent statistically significant at the level of 1%, 5%, and 10%, respectively.

Robustness Test

The following robustness tests are carried out in this paper. Firstly, the momentum index, that is, the accumulative return of stocks in the previous period, is used as a measure of investor sentiment (Polk & Sapienza, 2009), and equations (4)–(6) are re-regressed. Secondly, the past empirical evidence shows that the stock price continues to move in the direction of earnings change after the earnings announcement, which is the PEAD. In order to control the possible impact of stock price drift after earnings announcement on the relationship between the information content of analyst’s recommendation report (released after the earnings announcement) and the information content of the earnings announcement, this paper adds unexpected earnings variables into equations (7) and (8). The regression results are basically consistent with the above conclusions, indicating that the model constructed in this paper is robust and the results obtained are reliable.

Discussion

Taking the earnings announcements of listed companies, analysts’ earnings forecast and analysts’ recommendations in Chinese stock markets from 2014 to 2018 as the samples, this paper explores the influence mechanism of investor sentiment on the market reaction to announcements, and investigates the influence mechanism of investor sentiment on the role of securities analysts under the framework of behavioral finance theory. On the basis of theoretical analysis, this paper empirically tests the relationship between the information content of analysts’ reports and the information content of the earnings announcements from the perspective of behavioral finance, and discusses the role of securities analysts in the stock market. This study has the following theoretical and practical implications.

Theoretical Implications

The extant literature usually studies the role of security analysts in the market by examining the relationship between the market reaction of earnings announcement of companies and the market reaction of analyst reports. These studies follow the efficient market theory, which holds that asset prices have rapidly and fully absorbed the available information in the market (Pevzner et al., 2015). Researchers usually use the event study method to take the accumulative abnormal return of stock price in the announcement event window as the impact of the event on investor value, but this view ignores the impact of investor sentiment on the market reaction of the announcements. Behavioral finance theory is based on experimental psychology theory and experimental evidence, which believes that emotions will have a significant impact on investors’ judgment and decision making, and adding emotional factors into the decision model can significantly improve the explanatory power of the model. A growing number of empirical studies show that investor sentiment has a significant impact on market reaction to announcements (Mian & Sankaraguruswamy, 2012). Based on behavioral finance theory, this paper discusses the influence mechanism of investor sentiment on the market reaction to the announcements, and studies the relationship between the market reaction of earnings announcement of companies and the market reaction of analysts’ reports after eliminating the investor sentiment component of the market reaction of these announcements, so as to judge the role played by securities analysts. This paper studies the role of securities analysts based on behavioral finance theory, which provides a new perspective for the research in this field.

Practical Implications

As for the role of securities analysts, there are two main views in the extant studies: information competition and information supplement (Chen et al., 2010). As an important information intermediary in the securities market, securities analysts, with their professional analysis ability and information advantages, provide valuable incremental information for investors, improve the information environment of the capital market and enhance the efficiency of the capital market (Fang et al., 2018). However, evidence to the contrary has been found in the Chinese stock market. On the one hand, there are a large number of minority investors in China’s stock market, and the market efficiency is low. Analysts’ earnings forecasts largely rely on private information, and investors underreact to analysts’ earnings forecasts (Zhang et al., 2017). On the other hand, There are still some irregularities in the securities analyst industry in China, such as the quality of securities analysts is uneven, and the interest collusion between analysts and listed companies, etc. (Wang, Chen, et al., 2017).

In this context, it is of great practical significance to investigate whether securities analysts provide investors with incremental valuable information and what role they play in the securities market. We select the proxies that can reflect the investor sentiment of China’s securities market, construct the investor sentiment composite index of China’s securities market through principal component analysis, and decompose the market reaction of announcement into investor sentiment component and non-investor sentiment component. After removing the investor sentiment component, this paper finds that there is no significant correlation between the information content of earnings announcements and the information content of analysts’ earnings forecasts, and securities analysts do not play the role of information competition. There is a significant positive correlation between the information content of analysts’ rating reports and the information content of earnings announcements, and securities analysts play the role of information supplement. The above research results show that the earnings forecasts of securities analysts do not provide valuable information for investors, and in China’s securities market, securities analysts are more likely to be interpreters after the financial reports of listed companies have been released. Therefore, China’s securities regulatory authorities should strengthen the regulation of securities analyst industry, maintain the independence of securities analysts, guide them to strengthen the field research on listed companies, and strive to improve the quality of earnings forecast. When securities analysts can provide investors with valuable earnings forecast information, they will play the role of information competition, which is conducive to improving the allocation of resources in the securities market, thus enhancing the efficiency of the securities market.

Research Limitations and Future Prospects

Although this paper attempts to do some extended research on the role of securities analysts in China, there are still some limitations. The main limitation of this paper is that it does not consider the differences between individual investors and institutional investors. Some studies have found differences between institutional investors and individual investors in terms of sophistication and investment behaviors (Kalay, 2015; Li, Rhee & Wang, 2017). There are three theories about the interaction between institutional investors and individual investors and their impact on the market. The first theory is the rational market view, which argues that individual investors’ trading behavior may be irrational, but such trading will not have a significant impact on the price, because smart institutional investors will quickly offset the deviation of stock price from intrinsic value caused by the irrational trading of individual investors, so as to keep the market rational and stable (Boehmer & Kelley, 2009). The second theory takes into account the frictions in the market, such as short-selling restrictions, noise trader risk, and capital constraints. Due to these factors, sophisticated institutional investors may not be able to eliminate the bubble in share prices caused by high market sentiment, which is driven by noise trading of individual investors (Lewellen, 2011).The third theory suggests that institutional investors may actually be fueling irrational sentiment. Institutional investors expect that positive feedback traders will buy stocks with higher price in the future, which will aggravate the fluctuation of stock price (Gabaix et al., 2006).In view of this theoretical divergence, future research should distinguish between the market reaction of individual investors and institutional investors to the announcements, explore the possible differentiated role of securities analysts among these two types of investors, and consider the impact of investor sentiment. This extended research is helpful to investigate the sources of rational investment and irrational investment, and to provide suggestions on how to improve the quality of analysts’ reports and give full play to their information intermediary role in the securities market.

Footnotes

Appendix

Figures A1 to A4 describe the trend relationship between the Discount of Closed End Fund (DCEF) and Consumer Confidence Index (CCI) and China’s stock market index. As can be seen from the figures, the trend deviation between DCEF and stock market index, and between CCI and stock market index, is very large, which proves that these two proxies can not well reflect the investor sentiment of the Chinese stock market. Therefore, it is reasonable to exclude these two proxies in the construction of investor sentiment index.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

This paper does not deal with animal and human studies.