Abstract

This paper examines the impact of the drivers of change, that is, digitalization, demonetization, and consolidation of banks as factors affecting training and development. Banking institutions are the real contributors of the GDP in today’s world. The study is based on the data collected from senior bank officers, middle and lower level officers from India. The balanced scorecard is used to determine the performance of the banks with the help of four perspectives, that is, financial, customer, innovative, and growth perspective. Job enrichment helps in adding value to an employee through various techniques and programs. Partial Least Square-Structured Equation Modeling (PLS-SEM) was applied for examining the relation among the drivers of change and job enrichment with Banking Sector Performance. It also examines the mediating role of training between drivers of change and banking sector performance. The results suggest that training along with selected drivers and job enrichment influenced bank performance and value of adjusted R2 is .668. The current research suggests that the role of digitalization, demonetization, and consolidation of banks on banking performance improved with mediation effect of training. This research also highlights that in types of training, special training has higher loading, which implies the need to focus on training and specifically of special training to enhance banking performance.

Introduction

Today, banks are not just places to deposit and withdraw money. They are the real contributors of the GDP of the country. The GDP of India was adversely affected and dropped to 6.1% from 6.8% and 7.6% in subsequent quarter and December 2016, respectively (Reserve Bank of India, 2021). To enhance the banking performance, we need to study various drivers of change, that is, digitalization, demonetization, and consolidation of banks.

Digitalization is the major cause of aiding the processes and simplifying the work making us merely professionals. Digitalization is the new technique to deliver better and efficient services to the customers with the use of technology specially designed for it. The banking sector has been evolving almost every year and trying to adopt to the latest technological advancements. This process is called the “digital banking” or “cyber banking.” Digital banking has not only made it easier for the employees to improve their work efficiency and professionalize but has also helped the customers to gain momentum in advancements around them. There are three levels of digital banking namely the initial level, that deals with the websites of banks to provide information to the general public; next level, deals with handling the customer requests and queries and the last level helps customers in operation of their accounts through websites and applications, as explained by Dara (2017). The services have contributed to easing out the pressure on bank employees and reduced the manual labor to a great extent. But this cannot be denied that the risks and frauds have been multiplying with digitalization. The security is penetrated and mishandled hence creating a threat to adopting digitalization. Cybercrimes are growing at a much faster rate than expected. Also, upgradation is quite expensive and the staff required has to be expertise. As the internet connectivity and penetration increases digitalization in the banking sector is a natural progression. The latest technologies, professionalism, innovative products and services, and job opportunities have been increasing and improving with the progression of the Indian banking sector, according to Malik and Prakash (2008).

Demonetization has made it an important factor to adopt to digitalization to ease the workload of the employees, saving time, and improving the work efficiency. Post demonetization due to cash crunch and availability of e-sources, it made it easier for the customers to switch to electronic modes of transfer for their transactions on the daily basis. Demonetization policy of 2016 estimated a large share of old cash was held by tax evaders and feared that they will not exchange it for new currency. According to Rajagopalan (2020) the Indian government expected a revenue increase of almost 23% currency in circulation through unreturned notes. The impact of demonetization has been drastic, but the networks of the money laundering may persist and continue in future making other instruments difficult to implement. Demonetization has been one of the biggest driving change lately, which has increased the need to provide upgradation in the banking training techniques and processes.

The third driver of change namely consolidation of banks has led to increase in the workload and pressure on the employees which generates an urgency to train the employees appropriately with the demanding changes. Consolidation of banks is driven by a variety of factors like globalization, deregulation, technological advancements, and overcoming financial distress. Consolidation of banks helps in resorting to capital infusion. It increases the capital efficiency and also helps to recover the bad loans. Furlong (1994) concluded that consolidation in banks result in increase in the scale of economies, gains in the operational efficiency, profitability improvement, and resources maximization. Therefore, it is of utmost importance to empower the employees by providing suitable training and developmental programs to face the consequences post consolidation of banks.

In enriched jobs people complete their jobs with increased independence, freedom, and responsibility. It gives more control over work. Jobs design play a fundamental role in augmenting employees’ performance. Sharma and Khanna (2014) opined that performance of the employees is directly related to the extent of positivity, attitude, and satisfaction toward the job. Therefore, it becomes of vital importance to incorporate training and development strategies to meet the requirements of the employee’s performance and the performance of the banks.

There is a gap in providing efficient and good training to the employees to overcome the difficulties in adoption of technological advancements with the advent of demonetization and consolidation of banks for enhancing the banking performance and also seeing the influence of job enrichment on performance of the banks. There is an aggravating need for providing special training to the employees’ due to the changes brought in by the drivers of change. There are several studies suggesting the importance of training to enhance the banking performance, but these have not focused on examining the mediation effect of training between drivers of change and banking performance. The current study is an attempt to find out the influence of the drivers of change on business performance with mediating effect of training on business performance. It also examines the influence of job enrichment on banking sector performance.

The present study has been commenced with these objectives:

O1: To examine the impact of the drivers of change viz. digitalization, demonetization, and consolidation of banks on the banking performance.

O2: To examine the impact of job enrichment on banking performance.

O3: To examine the mediating role of nature of training between drivers of change and banking performance.

O4: To design a model to examine the impact of the drivers of change with mediating role of nature of training, and job enrichment on the banking performance.

This paper primarily builds on the insights from existing literature to identify the influencing Banking Performance. Further the details of the drivers of change, nature of training, and job enrichment are given in the Section 2. this section also resents details of Banking Performance. Section 3 provides description of sample, scale along with research methods applied. The research attempts to design a model relating drivers of change, job enrichment, and nature of training with the banking performance using PLS-SEM which is present in Section 4. Finally, Section 5 covers the discussion and conclusions. It also suggests directions for further study.

Literature Review

The study is based on banking performance. It is an attempt to examine how, drivers of change, nature of training, and job enrichment influence banking performance. thus, it is important to review literature related with banking performance. This is presented in Section 2.1

Banking Performance and Its Perspectives

The banking performance is evaluated through balanced scorecard with financial perspective, customer, internal business perspective, and growth perspective. The financial perspective includes capital adequacy, revenue growth, cash deposit ratio, credit deposit ratio, etc., the customer perspective includes good after sales services, customer retention, quality, customer complaints redressal, etc., internal business perspective includes productivity growth, profit per employee, error rates, credit growth, development of new products, etc. and growth perspective includes social and environmental perspective which includes revenue from new products, digitization of products and services, e-waste recycled, emissions per employee, etc.

The public sector banks control almost 80% of the market, leaving substantially a very meagre part for the private sector. According to Srivastava (2018) after demonetization SBI showed a high increase in their income as compared the Axis Bank showed fluctuating results. Post-demonetization had a significant influence on banking performance, as liquidity ratio escalation paved the way for cashless economy, making the basic operations easy for the employees. The major factors that affect the banking performance are Bad-loans, fraudulent practices, under-capitalization, frequent changes in government policies, insufficient supervision, over-dependence on forex, and absence of skill development and training programs for the employees from time to time according to Okpara (2009). With the help of digitalization, the performance of the banking sector has surely improved over the years but there is still a lot of scope for further growth and expansion (Maiti & Kayal, 2017). The other factors that affect banking performance are increased stress, emotional inability to strike the work-life balance and physical illness, but with an enriched job an employee can meet the requirements of the banks (Uduji, 2013). With the increased deposits due to demonetization, the share prices are also affected and net earnings of the banks have increased which further has a enormous influence on banking performance (Priyadharshini & Lourthuraj, 2015). Job satisfaction depends on self-belief; self-competence, ability to adopt new information technology approaches to solve difficult problems at work (Rahayu et al., 2018).

H1: Drivers of change, viz. digitalization, demonetization, and consolidation have a significant influence on banking performance with mediation of nature of training.

Drivers of Change With Banking Performance

Literature based on the drivers of change have been examined to focus on important drivers, as analyzed through earlier researchers. Drivers of change examined are: digitalization, demonetization, and consolidation of banks. Literature on these is presented in this section.

Digitalization

Indian banking system has grown in terms of technological advancements, that is, products and services, technology, banking system, trading facility, etc. (Anbalagan, 2017). It is with the help of training and development strategies that banks are able to meet the profitability and productivity. The primary aim of the banks is to equip the employees for immediately addressing customer’s requirements (Kumar & Jain, 2017). Digitalization has thus increased employees’ workload and made it difficult for them to meet performance goals or to satisfy customer’s immediate demands. Our economies have become well-equipped, productive, and have grown drastically over the past few years (Hitt & Brynjolfsson, 1996; Lee & Werner, 2018). According to Sanatani (2017) demonetization has paved a way for digitalization in India with increasing security hazards. There is a need for massive improvement in this sector. Digitalization in India has improved the performance of banks and assisted in moving toward cashless economy (Vally & Divya, 2018b). This was supported by Kaul and Mathur (2017) who opined that digitalization paves the way for innovation, enhances job opportunities and thus supports and promotes growth. Technology needs to be harnessed from time to time and must be adequately utilized to derive benefits of it. As India is moving cashless, the economy is largely affected because of adoption of digitalization at the rural banking sector (Paria & Giri, 2018). The existing level of digitization & infrastructure for adoption of digital means have a significant bearing on the magnitude of demonetization (Aggarwal et al., 2021). Digitalization helps the employees by decreasing their workload and fastening the processes, but has also helped the customers in gaining momentum with the advancements The very first driver of change in the banking environment has been digitalization and with the invent of technology it has made it crucial for the banks to upgrade their training methods and techniques for better efficiency of the employees and banks.

Digitalization has not only helped in increasing the productivity but has also increased the employment opportunities, improved the standard of living and increased the e-literacy rate also (Tigari, 2018). According to Hassani et al. (2018), data mining is crucial in banking sector, as unbalanced exploration status can be caused due to limited access of the big banking data. This could be due to dearth of skilled researchers or techniques to mine the data, system constraints, and inadequacy of advanced data analytic tools. Post demonetization, digitalization has become a necessity. Banks ought to train their staff with regards to solving problems of the clients and increasing the productivity of the banks (Suriya & Veni, 2020). There are plenty of security hazards, lack of customer awareness, fear factors like one of losing money especially for the elderly and the illiterate, lack of appropriate training that makes it difficult to accelerate the banking performance (Harchekar, 2018). With the introduction of block-chain facility the banks would be able to meet the customer requirements, as it has the potential to change the front/back office operations. Moreover, in the coming years the complex architecture would be broken down in smaller bits for upgradation for specific functions (Anbalagan, 2017). All this is a cumbersome project and requires trained and skilled staff with adequate potential to adapt to the dynamicity of the banking sector aid the banking performance. According to Druhova et al. (2021), the fintech companies took over the banking industry. Economies with greater usage of internet for payments have lesser returns on banking assets, but have a higher share of problem assets in their portfolios. Thus, use of internet and digital modes is beneficial for the banks to increase their sales and improve their customer services for better functioning, further improving their monitoring systems. Digitalization has paved the way and created opportunities, but at the same time increased the risks for the banks to handle. Gul et al. (2021) concluded that the productivity of the banking sector increased by investing in those analytics which have predictive, visualizing, and analytical capabilities. With digitalization, the disadvantages of the multiplying fraudulent activities and crime rates peaking also emerge. Pre-demonetization, digitalization was an important factor in the technologically uplifting the economy, lately, post demonetization the need for digitalization accelerated to bridge the cash crunch during the crisis. Digitalization has surely made a huge difference and eased many operations for the employees working for the banking sector but has also increased the need to adopt the skilled and trained staff for proper functioning of the banks and influence the performance of the banks.

The Figure 1 depicts that with demonetization the usage of online payment applications had increased drastically from November 2016 and dropped in June 2017 and kept increasing thereafter. Indian economy was drastically affected due to demonetization. It took some time to stabilize itself but it has been accepting the nature of advancements by adopting online payment methods of transactions by gradual increase over the years as shown in the Figure 1.

Self-constructed.

Demonetization

Demonetization has made it an important factor to adopt to digitalization to ease the workload of the employees, saving time, and improving the work efficiency. Post demonetization cash crunch and availability of e-sources made it easier for the customers to switch to electronic modes of transfer for their transactions on the daily basis. There was fear that people may not exchange currency. Further Rajagopalan (2020) reported that government expectations were high. The impact of demonetization has been drastic, but the networks of the money laundering may persist in future too leading to difficulty of use of other monetary instruments.

Demonetization was resorted to by the government as a step to condense corruption, counterfeiting terrorist activities and bring out black money. The ultimate goal was to convert to digital economy, according to Narain and Patnaik (2017). By the end of the first month 77% cash was received by banks opposing the notion of amassing of black money. Largely the middle and lower classes were affected as they conducted the transactions up to 98% in cash, with many living without bank accounts and lived in cash income. The trouble aggravated with the passage of time as many had to stand in long queues waiting for their turn to withdraw money and deposit cash. After studying the card usage on GDP of 51 countries, according to Moody’s Analytics (Zandi et al., 2013). The electronic card usage added 1.1 trillion USD to real dollars for private consumption and GDP from 2003 to 2008. With 1% rise in card transactions, GDP will increase each year by 0.039%. Global non-cash transactions were 358 million in 2013 as per Mukhopadhyay (2019). Demonetization has paved a way toward the cashless digital economy but the question here arises that how does the cashless economy fuel itself?

In India to sustain a cashless economy, the businesses 50 crore turnover, were asked to offer low-cost digital modes of payments. Further facilities included no charges or merchant discount rates to be imposed on them or their consumers. Supporting infrastructure and technologies are required by India to become a cashless economy. Demonetization has nudged India to become a cashless economy with witnessing 5 million daily usage of Paytm post demonetization. According to Karthick (2019), demonetization has led to term investments in PMJDY, as a result of which several number of bank accounts are being opened in rural and urban areas with zero balance. Further, he concluded that demonetization will help to eradicate 5% of black money in cash and push the banks to lower interest rates by 0.5%. Numerous measures have been adopted by the government to reduce populations’ dependence on cash, that is, Pradhan Mantri Jan Dhan Yojna (2014, https://pib.gov.in/Pressreleaseshare.aspx?PRID=1649091) which is a national mission on financial inclusion so that banking facilities are provided to all the households across India. This has played a significant role in opening bank accounts for the poor. Secondly, schemes like DBT (Direct Benefit Transfer) have helped in providing old age pension, LPG subsidy, MNREGA, scholarships, etc. and Unified Payment Interface (UPI) helps in merging several bank features, seamless fund routing, and zero transaction costs. Savings are increased with the use of cashless payment instruments.

Mohanty and Mahendra (2020), concluded that the banks post-demonetization disburse the funds cautiously, but at the same instance the asset creation through investments make the banks less focused on meeting future needs. Bose (2019) highlighted that the government considered digitalization as favorable, due to increase in income tax (17.3%) and advance tax collection (41.79%). Moreover, cash/GDP ratio has declined (1.6%). Mobile payment technology has helped in financial inclusion. Pal et al. (2018) developed a framework for sustainable development which could be possible through low-cost technology and with features of easy operability. Protective security should be provided in mobile payments even during the crisis periods (Pal & Herath, 2020). Donner and Tellez (2008) find mobile payments to have larger impact due to wide usage of mobiles. It is rightly observed that during the crisis periods, too mobile payments played a vivacious role in the unorganized sectors as SMEs were able to switch to mobile payments without obtaining additional costly equipment’s like POS (point of sale) machines.

Consolidation of banks

Consolidation of banks leads to potential expansion of the banks with regards to their assets, liabilities, and other financial items of two or more entities. Some authors are of the opinion that banks’ expansion would lead to increased efficiency and enhance their competitiveness in the international market as well. There are various factors that drive the consolidation of banks, that is, deregulation, technological improvements, globalization, and financial distress. According to T. R. Mohan (2005), Consolidation of banks in India has increased the profitability making the Indian Banking System the second most profitable in the world. Kaur (2019) explained that the largest and the most recent consolidation in India (1st April 2017) was of the State bank of India with five associates, namely State Bank of Bikaner, State Bank of Patiala, State Bank of Travancore, State Bank of Mysore, State Bank of Hyderabad, and Bhartiya Mahila Bank. This enabled SBI to enter into the league of top-50 global banks with 24,017 Branches and 59,263 ATMs and serving approximately 42 crore customers. Performance of the banks measured via stock values has risen over the period. Performance of the banks is evaluated by branch expansion, deposits, credit priority sector advances, DRI advances, and net profit over the period with regards to consolidation (Vashisht, 1987). High level of Capital is required to compete in the market as an impact of merging (Srinivas, 2011). K. Mohan (2006) concluded that the objective behind consolidation of the banks would be strengthening of Banks, economies of scale, global competitiveness, cheaper financial series, and retention of employees.

Mantravadi and Reddy (2007) observed that merging between the same group of companies leads to dip in performance and return on investment. According to Ambica (2017) the findings form the study pertaining to the selected banks with the help of parameters of CAMEL model for rating system, financial performance ratios, and ANOVA to understand the impact of merging by evaluating and comparing the premerger performance to post merger performance has revealed to be beneficial. Kotnal (2016) opined that mergers and acquisitions are important tools for growth and expansion in the Indian Banking Sector to assist in survival of weak banks and to make them competitive. Jayadev and Sensarma (2007) analyzed some critical issues of consolidation and supported that Indian financial system required large banks to absorb numerous risks arising from operating nationally and internationally. The various challenges faced by the employees of the merging banks are the larger banks are already filled in with all the vacancies so the employees have difficulty in absorption in the merger banks and the employees lose their identities and increase their efficiencies to meet the requirements of the larger banks and to match their counterparts already working there, as explained by Kambar (2019). According to Joshi (2020) the experts believe that if the banks are running in losses, it becomes crucial to merge as merging the banks weans off the surplus number of the employees, reduces the management expenses and also helps to utilize each other’s resources. Consolidation of Banks is a herculean task and requires the employees to be trained efficiently to attain the organizational performance and goals. The need for training strategies and programs is extremely important as they are the human capital of the banks and investment in human capital gives increased financial and growth gains.

H2: Nature of training has a positive influence on banking performance.

Nature of training

Training and development is the subsystem of any organization which helps the employees to enhance their skills and adapt to the latest technological advancements and changes in the environment of the banks. It is with the help of training and development strategies that the banks are able to meet the profitability and increase the productivity. The primary objective of every bank is to equip itself to meet the requirements of the customers. (Kumar & Jain, 2017) There levels of needs that are analyzed to meet the goals of the banks are the needs of organization; needs of individual employee, skills knowledge, and attitudes; and their functional responsibilities and departmental needs (Desimone et al., 2002). Training helps firms’ to expand, assist in their potential development, and to increase their profitability (Cosh, 1998). At every level Training plays an important role, initially the induction training or the orientation course is of utmost importance to meet the job requirements efficiently and understand what is to be done by the employees in their jobs. For the existing employees’ it is of vital importance to provide training through training programs to develop their capabilities and acquaint them with the latest technological advancements or dynamicity of the work environment. According to Cooper et al. (2019) employee resilience can be developed through training interventions, however, teams, information sharing, and supportive leadership are also very important. The study suggests a need for multilevel, multi-source research design aggregating data from employees on HRM practices and also considering the social climate at work place. Training is essential for the employees when they get promoted or when they are shifted internally from one department to another to familiarize them with the job requirements and so that they are able to attain the goals efficiently. Training and development is also necessary for overall growth in an employee’s career. Otoo (2019) suggested employee performance can be a promising mediating mechanism that can be enhanced through exhaustive HRM practices and organizational effectiveness.

On the job training

On the job (OJT) training refers to training provided within the workplace environment to enhance skills, knowledge, and competencies of employees to assist them perform their jobs efficiently. Structured and effective on the job training has proved to be the most effective form of training given to the employees as it helps to acquaint them and provide them with skills to perform the day to day jobs efficiently as explained by Rothwell and Kazanas (1990). As analyzed by Van der Klink and Streumer (2002) factors like self-efficacy, previous experience, managerial support, and workload are important for improving effectiveness of the jobs. OJT has proved to be partially effective in realizing the training goals of the banks. Effective use of tools and techniques for OJT can enhance competencies of employees (Khan et al., 2011). OJT can enhance the teamwork, coordination, morale, and attitudes of the trainees and the trainers. In some cases, the trainers are hired from outside to provide training and in some cases mentoring the managers and employees’ relationships can provide guidance and serve as an approach to OJT New employees learn better from their mentors. Job rotation serves as an important technique to train the employees and acquaint them with the inter-departmental work. Job Instruction Training JIT helps in the employee’s development of skills, knowledge, and attitude. On the Job training if structured provides with better results than unstructured.

Off the job training

Off the job training is provided to employees outside the organizational premises. The employees. It often includes classroom lectures, case studies, role playing, and simulation. They are systematically planned training and efficiently created programs that add a lot of value to the employees’ overall growth. The trainees and apprentices are often expected to learn more from on the Job than Off the Job training, even though the latter one provides them with greater qualifications. This is reflected through Harris et al. (1998), as the researchers regard that Off the job training provides extra dimension to employees and help them to learn new techniques and skills being employed in other organizations.

Special training

Special training included skills like analytical skills, commercial awareness, attention to details, work ethics, stress management, technical skills, competitive skills, etc. other than for which training is already being provided. Communication skills and customer handling also form a part of special skills. There are a few training strategies being adopted by the banks to enhance customer handling skills and communication but no proper training programs are being catered for enhancing the soft skills and special skills of the employees. Performance of the banks is directly linked with the employee’s performance and it can only be enhanced by providing proper training to the employees. Soft skills training doesn’t only help in enhancing the knowledge of the employees but also provide them with confidence to communicate efficiently with the customers. According to Vetrivel (2019) stress management in the bank employees is an important tool for them to handle the work-related stress and other stress so that it doesn’t interfere with their work and reduces their efficiency. Employees grievances must be handled well, so that they can they can mingle up in the work culture well. Ahlawat et al. (2013) opined that training in soft skills must be provided at all levels especially at the managerial level to connect better with the customers and build enduring relationships with them. Knowledge and practice of soft-skills facilitate in building healthier relations among the employers, employees, and customers. Goleman (1995) found self-awareness, self-regulation, empathy, motivation, and social skills as vital competencies that enhance individual’s performance. Therefore, it is of utmost importance to incorporate the special skills training to the employees for their overall development.

The related hypothesis is:

H3: Banking Performance is composed of financial perspective, customer, internal business perspective, and growth perspective.

H4: Job enrichment has a positive influence on banking performance.

Job enrichment with banking performance

Training and development managers consider job enrichment as an alternative to training strategies adopted by the banks. An increase in absenteeism, employee turnover make us think and focus on job enrichment. It has a direct impact on improvement of an individual employee and has more influence on planning, executing, and evaluating the jobs performed by the bankers.

The extent of workload on the employees and the job designs need to be altered from period to period to meet the requirements of the banks with respect to employee’s performance and bank’s performance. An increase in absenteeism, employee turnover, low turnover of the organization, and tardiness when occurs, job enrichment is considered and the job designs are altered to meet the requirements by the training and development managers. An enriched job comprises of fuller utilization of workers valued existing skills and an opportunity to acquire new skills. Job enrichment suggests increasing the degree of responsibility, to monitor the performance of the employees themselves, how to do the work and find new ways to meet the customer requirements as explained by Uduji (2013). Job enrichment and its dimensions reinforce employees’ motivation. (Rastogi & Chaudhary (2018) Enrichment in the jobs increases self-sufficiency, self-restraint, and confidence of the employees which augments their performance. Improvement in the work environment leads to increase in employee’s productivity (Dost et al., 2012). Muneer et al. (2017) concluded that the employees did not find their jobs enriching hence the results were insignificant. Job enrichment is the process associated with information, learning, and employee’s or staffs skills according to Asl et al. (2015). Enhancing the skills by incorporating training programs and strategies to meet the current requirements of the employees of the banks and providing with the job design and suitable conducive environments will help employees reach the targets efficiently. Raza and Nawaz (2011) defined job enrichment as alterations in job dimensions, variations in physical conditions, or fundamental tasks to increase employee satisfaction. A lot of times the jobs are accompanied by demotivating factors for the employees, that is, deferring promotion, excessive load, increased working hours, and lack of appreciation from the managers (Omollo & Oloko, 2015). High level of job satisfaction has a direct impact on improved performance and increases employee’s work involvement as concluded by Mallika and Ramesh (2010). According to Koontz and Weihrich (1990) job enrichment enhances achievement and improves individual’s capability to tackle challenges. Job enrichment could be by improving work methods, sequence, and pace of the jobs. On the other hand providing with responsibility to the employees with defined tasks to be performed, making changes in their physical environment, and focusing on the training and developmental strategies from time to time with the dynamic environment of the banks. Also familiarizing the employees with the latest technological advancements by providing them with accounted skill sets and training.

The next section describes the details of sample, research instrument, and research methods used for achieving the objectives.

Research Design and Methods

Target Population and the Sample Size

The current study covers Public Sector Banks, Private Sector Banks, and Foreign Sector Banks employees, managers, that is, Branch Heads, Assistant Managers, Regional Heads, Senior Managers, Associates, Probationary Officers, Clerks, and Chief Managers. The study focused on a sample from four emerging states of India, viz., Punjab, Haryana, Delhi, and Uttar Pradesh. Public Sector Banks contribute 66%, Private Sector banks contribute 28%, and the Foreign Banks contribute 6%. Thus, the targeted banks had more numbers from Public sectors as compared to other two categories of banks.

In all 76 responses were received from the Public Sector 25 from the Private Sector Banks and 10 from the Foreign Banks. There are in all 12 Public Sector Banks, 22 Private Sector Banks, and 46 Foreign Banks functioning in India as in 2020. The study covers State Bank of India, RBL, HDFC, HSBC, Citi Bank, Bank of Baroda, Central Bank of India, Sarva Haryana Gramin Bank, Union Bank of India, Standard Chartered Bank, Kotak Mahindra, Axis, Punjab National Bank, SIDBI, IDBI, YES Bank, J&K Bank, Canara, Punjab and Sind Bank, Punjab Gramin Bank, Mudra Bank, and Syndicate Bank. The main focus of this research is to find the factors that influence Banking Sector Performance, as banks contribute a major chunk toward the Indian Economy. Initially received reasonable responses, but later due to the current situation and COVID-19 the response rate went quite low but 111 responses are recorded for further analysis and interpretation.

The study is based on data collected through a structured questionnaire. The questionnaire was validated by experts from the banking sector and academicians and also through reliability index the consistency was checked. The same are presented in Section 3.3. This was further examined through discriminant and construct validity reported with SEM-PLS results.

Research Methods

The present study used (PLS-SEM) model for estimating the proposed measurement and structural model. PLS SEM is an alternative to covariance based SEM-AMOS. It gives increased flexibility for data requirements, for specifying the relations. The analysis of mediating effects has further led to wide acceptance among researchers (Sarstedt et al., 2014). As the measurement provided satisfactory, we moved to structural model, as suggested by Hair et al. (2014). PLS-SEM helps to estimate multiple interrelated dependent relationships between the variables and use of latent construct measurement (Ittner et al., 1997)

Validity and Reliability

Confirmatory factor analysis (CFA) is examined to test the hypothesis that a relationship between observed variables and their underlying latent construct exists. Fornell and Larcker (1981) suggested that convergent validity of constructs is observed through factor loadings and average variance extracted (AVE). In the present study, the value of the factor loadings were higher than 0.50. AVE is also greater than .50 (Table 2). Nunnally (1978) supported that the values of composite reliability (CR) should be more than .70. The resulted composite reliability lies is greater than .739 and Cronbach’s alpha were >.721 (Table 1). This reflects good construct validity and reliability of the model.

Construct Reliability.

Source. Self-constructed.

Further, the discriminant validity was measured by comparing the values of square-root of AVE. It is recommended that value of square root of AVE should be larger than the inter construct correlations (Table 2). The discriminant validity as shown through Table 3 was also acceptable.

Discriminant Reliability.

Source. Self-constructed.

Variance Inflation Factor.

Variance Inflation Factor VIF values >3 reflect the presence of collinearity (Hair et al., 2011). As reflected through Table 3, both outer and inner the VIF values are all lesser than the threshold value of 3, therefore no indicator was removed.

Results

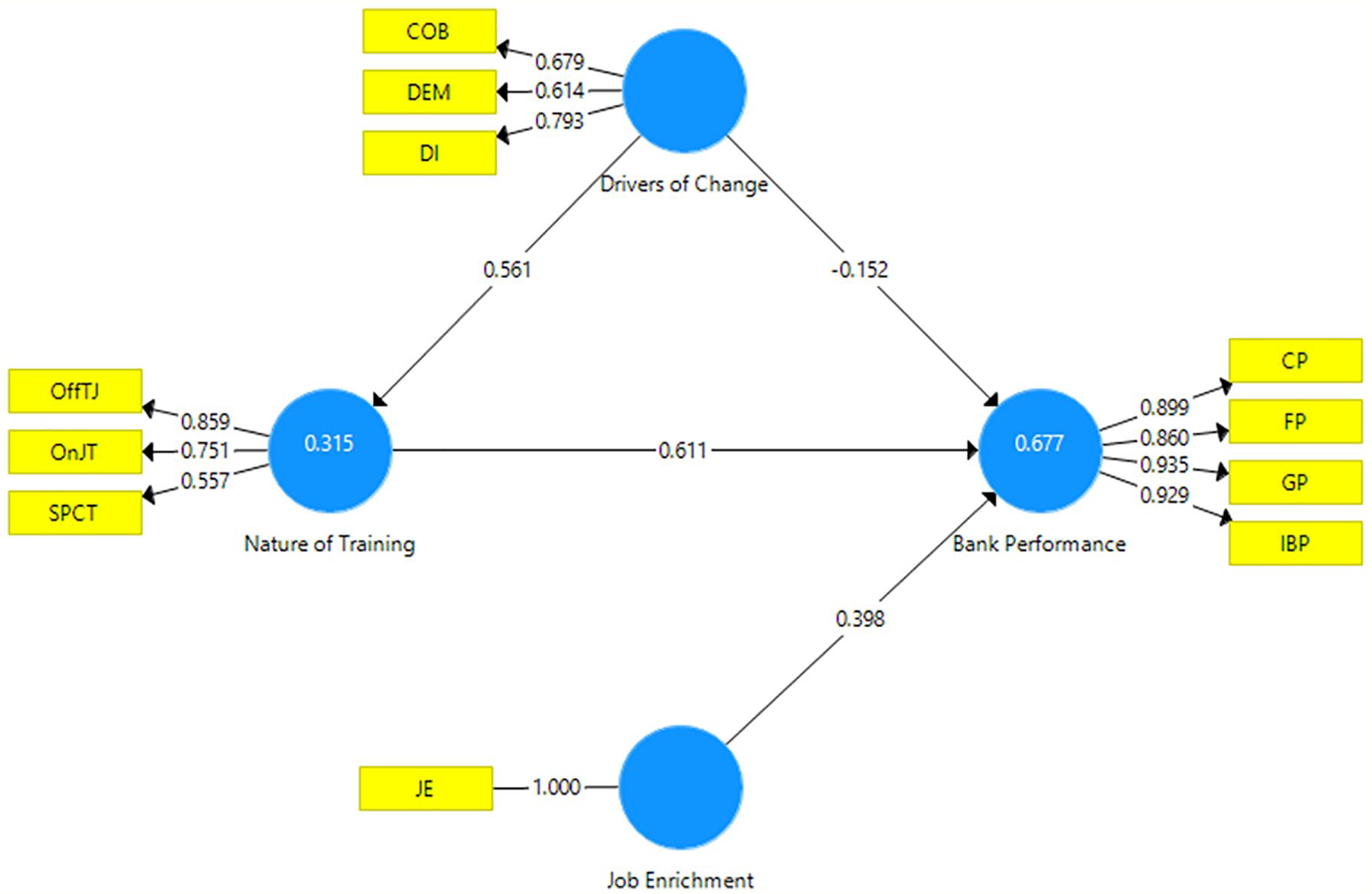

This research was taken with the objective to design a model to examine the influence of the drivers of change, nature of training, and job enrichment with mediating role of nature of training on banking performance. The model has been depicted through Figure 1 and results of path coefficients are presented in Table 4. The structural model represents the constructs and the relationships (paths) between the constructs. The measurement model exhibits the relationship between the constructs and indicator variables. The study uses a reflective model.

Outer Loadings of Components of Banking Performance.

As is obvious from Table 4, outer loadings of all components are good. Highest loading is for growth perspective, followed by internal business perspective, customer perspective, and financial perspective. Thus, hypothesis H1: Banking performance is composed of financial perspective, customer, internal business perspective, and growth perspective has been empirically supported.

The basic objective of the current study was to examine the impact of the drivers of change viz. digitalization, demonetization, and consolidation of banks on the banking performance with mediation effect of nature of training. The study also examined the impact of nature of training on banking performance. Results highlight that path coefficient are shown in Table 4. As reflected through Figure 2 and Table 5, beta value drivers of change and nature of training is .561 and that of nature of training and bank performance is .611. Both these are significant. This highlights the mediation effect of nature of training between drivers of change and business performance. Thus, hypotheses H2: Nature of training has a positive influence on banking performance and H3: Drivers of change, viz. digitalization, demonetization, and consolidation have a significant influence on banking performance with mediation of nature of training have been accepted.

PLS SEM model examining the influence of the drivers of change, nature of training, and job enrichment with mediating role of nature of training on the banking performance.

Path Coefficients of Constructs.

p ≤ .05. **p ≤ .01. ***p ≤ .001.

The next objective was to examine the impact of job enrichment on banking performance. The β-value is .398 and p ≤ .01, which is indicative of the influence of job enrichment on banking performance. Hence H4: job enrichment has a positive influence on banking performance has been empirically supported.

Overall results indicate that with nature of training as the mediating variable, the influence of drivers of change on banking performance has improved. Job enrichment also has emerged as important predictor. The value of R2 is .677 and adjusted R2 is .668. This indicates that the designed PLS-SEM model indicates 66.8% of variation. Thus, job enrichment along with drivers of change, viz. digitalization, demonetization, and consolidation with mediation effect of nature of training significantly influences banking performance. The study highlights the important role of nature of training and job enrichment on banking performance. The results are of great significance to induce banks to focus on training programs and job enrichment for enhancing banking performance.

Discussion and Conclusion

The results support that drivers of change with the mediating role of nature of training and job enrichment influence the banking performance. Demonetization, digitalization, and consolidation of banks has increased the workload of the employees and also increased the need for training. Nature of training plays a crucial role in deciding that the kind of training plays an important role in enhancing the performance of the banks. The drivers of change have an incredible impact on the banking performance with mediating effect of the nature of training. The researchers in this field have positive ideologies and have justified that the factors like demonetization, digitalization, and consolidation of banks have a credible impact on the banking performance (Kambar, 2019; Kaul & Mathur, 2017; Maiti & Kayal, 2017). The current study also supports the same. Consolidation of banks’ is good due to their ability to attract loans, employee contribution toward productivity, profitability, and overall banking performance (Cornett & Tehranian, 1992). In the current study consolidation emerges as an important driver. The impact of digitization, demonetization, and consolidation of banks have made it necessary for the baking sector to review their training and development programs for enhancing banking performance. However, digitalization is emerging as strongest driver. Job enrichment helps in retention of employees in the organization and also helps to develop a sense of satisfaction by alteration in the job designs with changes in the environment (Caudron, 2001). High performance of the employees results in satisfaction with the job and has an impact on the future performance of the employees (Velnampy, 2008) There is a positive relationship between job satisfaction and organizational commitment according to Verma and Upadhayay (1986). Job enrichment doesn’t only augment employee performance by increasing job satisfaction, but also influences the banking performance. The current research highlights the importance of job satisfaction as an important predictor of banking performance.

Further the employees who are trained on a regular basis are the ones who provide better services to the clients. To enhance the banking performance, there is a need to develop cohesive and active training and development strategies as a prerequisite of the corporate culture than adhoc programs (Rani & Garg, 2014). In training, the outer loading of special training is low, which highlights the need to focus on this important aspect of training. The impact of drivers of change on Banking performance has improved with mediating role of nature of training. This is important contribution of research.

Growth of the banking sector is an outcome of skilled manpower. Top level management plays an important role in development of training programs providing core expertise and setting up tremendous work design for the employees (Tan et al., 2003). Training at the probation period is given greater importance for overall performance of the banks and the employees. Private sector Banks are paying focus on the training and development to retain employees for increasing their reliability (Noe & Kodwani, 2018). There are several independent studies of the factors affecting the banking performance or the impact of training and development on the banking performance, but this study incorporates the drivers of change, that is, demonetization, digitalization, and consolidation of banks and job enrichment also and discusses their influence on the banking performance with nature of training playing a mediating role in enhancing the performance of the banks. Thus, the study contributes to the literature by examining this relation and through the mediating effect of nature of training between drivers of change and banking performance.

Implications of the Study

This study will be a starting point for further exploration into the current situation of the banking sector performance and what other factors have a major impact on the performance of the banks. The study highlights the importance of balanced score card in measuring banking performance. All the components emerge important, viz. financial perspective, customer, internal business perspective, and growth perspective. The study focuses on importance of training in banking performance. Though both off the job training and on the job training are important, however low outer score of special training indicates more importance need to be focused on this. The interview with banking professionals highlighted that banks in India focused on regular training, however with digitalization, demonetization there is a need to develop special training programs. This would help banks to focus on this to enhance performance. Next important result highlighted was Job enrichment. The present research offers some insights for enhancing the performance of employees by incorporating better training and enriching their jobs.

However, this study is based on a comparatively small sample and selected banks in India. The current research is cross sectional in nature; the relationships could be strengthened and reinforced in the longitudinal study.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.