Abstract

This study explored the effects of insurance literacy, perceived usefulness, attitude toward health insurance, subjective norm, and perceived behavioral control on the intention to purchase and the actual purchase of health insurance among working adults in Malaysia. This quantitative study adopted the cross-sectional design with data gathered from 1,308 working adults through a Google form link shared in social media. Upon analysis, the outcomes revealed that insurance literacy, perceived usefulness, attitude toward health insurance, subjective norm, and perceived behavioral control exerted a significantly positive effect on the intention to purchase health insurance. Intention to purchase health insurance exhibited a significantly positive impact on actual purchase of health insurance. Empirically, intention to purchase health insurance yielded a significantly positive mediating effect. Based on the multi-group analysis (MGA), the perceived behavioral control was significantly stronger among rural respondents than urban respondents, as well as among respondents with a bachelor degree than those with secondary school certificate. Referring to the retrieved empirical outputs, financial and health management policymakers, as well as insurance companies in Malaysia should concentrate more on the positive attributes of health insurance in order to improve the attitude of Malaysian working adults toward insurance and insurance literacy.

Keywords

Introduction

The primary aim of an insurance policy is to decrease the risk faced by people in case of unexpected costs of healthcare services, thus hindering one from being adversely affected by financial burden (Owolabi et al., 2016). This stipulates the significance of subscribing to medical care coverage in seek of healthcare services (Rahman, Newaz et al., 2021). Nevertheless, the decision to purchase health insurance is not easy, which is often misconstrued by buyers (Loewenstein et al., 2013) who typically have the right to claim through the insurance policy (Born & Sirmans, 2019). Referring to the vast range of insurance mechanisms, adults have been claiming healthcare insurance throughout the year. The significance of certain insurance contract parameters has become popular worldwide (one’s access to medical care providers). Health insurance denotes the source of funds for medical care financing (Ahmed et al., 2016; Cheah & Goh, 2017), in which one’s decision to purchase healthcare insurance is integral. Sustainable financial policy in healthcare insurance has turned into a global concern due to the escalating costs of medical care services.

Malaysia has been under immense pressure to control the skyrocketing medical care costs, so as to verify the capability of the upcoming medical care funding system (Rahman et al., 2018). As such, Malaysia has considered a new policy of national healthcare financing that not only supports healthcare services, but also to face future uncertainties (Rahman & Zailani, 2017; Yu et al., 2008). According to Shafie and Hassali (2013), and Rahman and Zailani (2017), the healthcare service in Malaysia suffers from lack of quality medical care, inconvenience, understaffing, low accessibility, overcrowding, and long waiting time; thus forcing more than half of Malaysians to strive in seek of quality primary care. In light of private medical care services, Yu et al. (2008) reported that most (73.2%) of the expenditures were out-of-pocket and merely 18.8% of adult Malaysians were covered by voluntary private health insurance. This trend may spiral toward the risk of devastating healthcare events for Malaysians.

The NHMRC (2019) reported that the total expenditure on healthcare services was 4.24% of the gross domestic product (GDP) in 2017. This reflects the limited GDP resources that were actually spent for the medical care services sector. Thus, a strategic finance plan has been devised for medical care services with its ultimate objective of re-engineering the Malaysian healthcare system by initiating a national health insurance scheme (NHMRC, 2019). Funding from the Ministry of Finance, along with supplementary funding, is offered through insurance agencies, social security organization, and employee provident fund (Yu et al., 2008). This could enhance the national health insurance strategy across the Asian region (van Doorslaer et al., 2007; O’Donnell et al., 2008).

As noted in most medical care services reforms, customers’ perceptions and purchase intention (Jiang et al., 2019; Wu et al., 2008) are the pillars of healthcare insurance policy objectives. Customers’ intention to purchase health insurance, which involves value judgment of fairness (Yu et al., 2008) based on the degree of purchase intention, was examined in this study by including a determinant, insurance literacy, into the Theory of Planned Behavior (TPB). In the context of healthcare insurance, the financial burden incurred as a result of seeking medical care services has been reckoned to a great extent by its structure. The extent of insurance literacy (Kim et al., 2013; McCormack et al., 2009), perceived usefulness of health insurance, attitude toward health insurance, subjective norm, and perceived behavioral control are crucial determinants of a customer’s intention to purchase health insurance (Innan & Moustaghfir, 2015). Given the potential impact of health insurance purchase intention on adult households in Malaysia with varied perceptions of purchase insurance packages; the evaluation of their insurance literacy is indeed beneficial and timely. Thus, this study had investigated the effects of crucial TPB determinants on the intention to purchase health insurance among working adults within the context of Malaysia.

This study is an extension of the literature that had looked into insurance literacy, financial literacy, and financial systems (Lin et al., 2019; Weedige et al., 2019; Williams et al., 2021). This present research work examined the impact of insurance literacy on working adults in Malaysia, so as to inform the health insurance policymakers. The next sections describe the theoretical foundation related to TPB, the health insurance policy in Malaysia, the factors the affect one’s intention to purchase health insurance, the proposed model for health insurance purchase intention, the methodology, the analysis of the outcomes, discussion, implications, and lastly, a conclusion of this study.

Literature Review

Theoretical Foundation

This study investigated on how well the TPB could predict the purchase behavioral intention for health insurance among Malaysian working adults. Prior empirical studies have unraveled that TPB does indeed play a crucial role in predicting behavioral intention in general, and health behavioral intention in particular (Hall & Fong, 2007; Rahman, Gazi et al., 2021; Sheeran, 2002), with discussion pertaining to the degree of perceived behavioral control, inclusive of predictability over intention (Armitage & Conner, 2001; Demir et al., 2019). As such, this present study embedded insurance literacy as the additional predictability over purchase of health insurance. A number of behavioral studies (Khresna Brahmana et al., 2012; Natashia et al., 2019) have highlighted that researchers need to assess psychological factors upon evaluating customers’ decisions in purchase intention. In the context of insurance, Rabin and Thaler (2001) asserted that risk aversion may clarify the variances noted in the insurance market, whereby people tend to purchase insurance products when they are actually in need. Having that mentioned, this study had adopted the behavioral approach to reveal the variances of planned behavior in the context of health insurance amongst Malaysian working adults.

The variances in the demand for health insurance may be identified by employing the TPB (Yu et al., 2008). Planned behavior denotes factors that reflect a consumer’s intention to purchase health insurance packages. The TPB, which is an extension of the Theory of Reasoned Action (TRA) (Ajzen & Fishbein, 1980), has been widely applied to study human behavior over their actions. The major determinants of TPB are subjective norm, attitudes toward behavior, perceived behavioral control, and intention. In this present study, insurance literacy (the additional independent variable) and perceived usefulness were hypothesized to affect intention, which in turn, could influence the purchase of health insurance. Additionally, this study proposes the mediating variable of intention to purchase health insurance, as well as the moderating variables of perceived product risk and average monthly income. Manning and Bettencourt (2011) studied health plan as a mediator to depict the intention to use healthcare services among cancer survivors, whereas Luszczynska et al. (2010) evaluated self-efficacy as a moderator to identify the intentions among Chinese and Polish adolescents.

The independent variables selected for this study are subjective norm, attitudes toward behavior, perceived behavioral control, perceived usefulness, and insurance literacy, while intention and purchase of health insurance serve as the mediating and dependent variables, respectively. The dominant factor of this study refers to intention to purchase health insurance, primarily because it demonstrates the extent one is willing to make the effort to perform the behavior. This study predicted that non-motivational factors and resources, such as perceived product risk and average monthly income, are likely to control a particular individual’s behavior. Many researchers (Armitage & Conner, 2001; McEachan et al., 2011), assessed the correlations among several factors and intention, had revealed subjective norm, attitudes toward behavior, perceived behavioral control, and perceived usefulness as crucial determinants of intention. For instance, McEachan et al. (2011), in a meta-analysis that explored the effectiveness of the TPB in social science research domain, concluded that the TPB had a strong predictive value.

The Health Insurance Industry in Malaysia

The health insurance industry has been acknowledged as one of the key mechanisms of the economy with a crucial role in securing personal and business risks in case of uncertainties. In 2015, the health insurance segment in Malaysia had accounted for 4.2% of the industry’s premium (Abdullah & Ng, 2017; Gupta, 2017). People’s changing lifestyle patterns and commonality of diseases (e.g., respiratory disorders, diabetes, and other critical illnesses) have increased medical care service expenditure, thus the escalating demand for health insurance. In seek of better-quality services; consumers are keen in receiving private medical care services (Rahman, 2019). As a result, the private healthcare domain has been gaining popularity despite the initiatives taken by the government to provide an exceptional public healthcare system. Azzeri et al. (2020) claimed that the medical care services provided by the government have been verified by the health insurance for international working adults. Nevertheless, insufficient healthcare centers and limited use of technology had led international workers to purchase private health insurance. The insurance agencies in Malaysia have been effectively promoting private health insurance packages, which include life and general insurance schemes. Jaafar et al. (2013) reported that 54% of medical specialists were attached to private emergency clinics. With a record of having 20% of the country’s emergency clinic beds, the private medical clinics reported around 20% of total admissions and above 12% of total outpatient attendances. These private emergency clinic beds have been projected to comprise half of all medical clinic beds by year 2020 (Tay et al., 2020). Along with industrial advancement, employment facilities, and increasing GDP, people with middle-income level have been expected to enhance the health segment. The World Bank reported that the average life expectancy of Malaysian male and female was 59.4 and 60.3 years in 1960, respectively, while 72.1 and 76.5 years for men and women in 2011 (Tong et al., 2011). These life expectancy figures are expected to hike by 2020. This escalating trend implies a requirement for insurers to offer effective health insurance plans to cover policymakers, thus improving the health segment.

Factors That Affect the Intention to Purchase Health Insurance

Insurance literacy

Insurance literacy in this study refers to the degree to which people are familiar with health insurance plans. Health insurance literacy denotes the degree to which one has the capacity, the knowledge, and the certainty to assess accurate information regarding a healthcare plan, as well as the capability to select the best scheme based on their financial and health conditions (Quincy, 2012; Williams et al., 2021). Mathur et al. (2018), and Paez et al. (2014) highlighted that insurance literacy is composed of health insurance knowledge, cognitive skills, self-efficacy, information seeking, and document literacy revolving health insurance plans. Insurance literacy, which also covers health literacy, is reckoned by the need to see how medical care benefits are organized, comprehended, and estimated in terms of cost-sharing responsibility (Lin et al., 2019; Weedige et al., 2019). Insurance literacy demands details about medical care services and the capability to apply the information in deciding and selecting the best health insurance plan. Adepoju et al. (2019) and Berkman et al. (2011) postulated that health insurance literacy is integral to gain better medical care services. Insurance literacy becomes a crucial factor regardless if one’s intention is to postpone or to abstain from seeking healthcare due to costly service. In a study that involved college students using the mixed-method approach, Nobles et al. (2019) discovered that most of the respondents were confused about purchasing a health insurance plan due to limited insurance literacy. Often, effort to explore health insurance literacy is limited (Nobles et al., 2019; Paez et al., 2014). Lin et al. (2019) claimed that insurance literacy is vital for buyers when purchasing health insurance, so that they can accurately decide on their medical care plans. As such, the following is proposed:

Hypothesis (H1): Insurance literacy has a significantly positive effect on the intention to purchase health insurance among working adults in Malaysia.

Perceived usefulness

Perceived usefulness denotes the degree to which people believe that improving a certain utility will increase their attitude toward purchasing health insurance (Dzulkipli et al., 2017; Liebenberg et al., 2012). Consumers’ perceived usefulness reflects innovative technology that enhances performance (Berkman et al., 2011; Davis, 1989). From the lens of the TPB, perceived usefulness can influence one’s intention to purchase health insurance. Berkman et al. (2011) reported that perceived usefulness displayed a significant influence on the attitude toward the intention to purchase health insurance. Similarly, Liaw and Huang (2013) asserted that perceived usefulness has an essential function in reflecting attitude toward one’s behavior. A similar correlation was highlighted for the purchase intention of health insurance by Aziz et al. (2019). Tennyson (2011) concluded that the more people perceived the usefulness of health insurance, the higher the intention to purchase insurance. Thus, insurance companies should weigh in the psychological role (perceived usefulness) to encourage more people to purchase health insurance. Both Technology Acceptance Model (TAM) and TPB upholds that perceived usefulness is correlated with attitude toward accepting a new technology (Iskandar et al., 2020), thus affecting the intention to purchase health insurance. Therefore, the hypothesis below is proposed:

Hypothesis (H2): Perceived usefulness has a significantly positive effect on the intention to purchase health insurance among working adults in Malaysia.

Attitude toward health insurance

Attitude is defined as a psychological tendency that is communicated by evaluating an object with some degree of favor or disfavor (Aziz et al., 2019). Attitude toward health insurance is an antecedent, as it may affect a customer’s intention to purchase health insurance. Attitude toward behavior denotes “the degree to which one has a favorable or unfavorable evaluation concerning a given object” (Ajzen, 1991; Fishbein & Ajzen, 1975). Attitude that measures usage in the TPB is composed of items that signify both instrumental and experiential elements of attitudes (Fishbein & Ajzen, 2005; Fishbein et al., 2001). A number of studies have used the TPB to assess the correlation between consumers’ attitude and intention to purchase products/services (Casidy et al., 2016; Chin et al., 2016; Hsu et al., 2017). Han et al. (2010), for instance, employed the TPB model to assess the intention of customers to visit a green hotel. Paul et al. (2016) used the TBB model to examine the correlations among the factors of attitudes with intention. Using an extended TPB, Chen and Tung (2014) explored the link between perceived moral obligations and intention of consumers to visit green hotels. With attitude serving as a crucial predictor of consumers’ intention to purchase health insurance, the following hypothesis is proposed:

Hypothesis (H3): Attitude toward health insurance has a significantly positive effect on the intention to purchase health insurance among working adults in Malaysia.

Subjective norm

Subjective norm refers to “the perceived social pressure to perform or not to perform the behavior” (Hsu et al., 2017; Norman & Conner, 2005). Subjective norm denotes one’s perceived social pressure to perform behavior (Ajzen & Fishbein, 1980; Bianchi et al., 2018). Al-Swidi et al. (2014) and Bianchi et al. (2018) revealed that subjective norm is a significant predictor of travelers’ intention to visit a holiday destination. In light of the TPB, subjective norm is a predictor that could affect a consumer’s behavioral intention to purchase health insurance. Ajzen (1991) highlighted that intention can be predicted with high precision from subjective norm, wherein the intent turns into the consumers’ actual behavior. Subjective norm reflects a function of people’s beliefs of how referent to family and friends (Ajzen & Fishbein, 1980). One is bound to feel the pressure to perform the behavior of purchasing goods/services. Subjective norm is a predictor of intention, which has been acknowledged within the social science domain (Bianchi et al., 2018; Cheng et al., 2006; Hsu et al., 2017). As such, subjective norm denotes consumers’ perception if this antecedent can influence their intention to purchase health insurance (Berkman et al., 2011). Besides, subjective norm influences intentions across multiple fields of studies differently (Hsu et al., 2017; Tarkiainen & Sundqvist, 2005). Thus, the following hypothesis is proposed:

Hypothesis (H4): Subjective norm has a significantly positive effect on the intention to purchase health insurance among working adults in Malaysia.

Perceived behavioral control

Perceived behavioral control refers to “the perceived ease or difficulty of performing the behavior” (Hsu et al., 2017). Perceived behavioral control is the perception that one has on the capability to perform the behavior (Al-Swidi et al., 2014; Bianchi et al., 2018; Lam & Hsu, 2006), such as purchasing health insurance products/services. A study showed that perceived behavioral control is a crucial antecedent of intention among travelers to visit holiday destinations (Bianchi et al., 2018). Perceived behavioral control is a fundamental function of one’s belief of how referent other people view the motivation to meet consumers’ expectations (Ajzen, 2002; Bianchi et al., 2018; Cheng et al., 2006). Hence, people are bound to feel the social strain in achieving a behavioral intention if they believe that the perceived behavioral control favors the behavior of purchasing a product/service (Bianchi et al., 2018). Elmorshidy (2018) revealed that perceived behavioral control is an essential determinant of intention to use dietary supplements. Berkman et al. (2011) empirically assessed the effects of perceived behavioral control and health values on consumers’ intention to purchase health insurance in developing countries. Therefore, the following is hypothesized:

Hypothesis (H5): Perceived behavioral control has a significantly positive effect on the intention to purchase health insurance among working adults in Malaysia.

Intention and Behavior

Use of health insurance services has been found to affect one’s health and quality of life, apart from the link with healthcare costs. Past studies (De Cannière et al., 2009; Wang & Hazen, 2016; Weedige et al., 2019) reported a positive correlation between intention and purchase behavior. Nursiana et al. (2021), and Hsieh et al. (2019) discovered that the intention to use adult preventive health services was more significantly explained by several enabling factors. In the context of health insurance, adult working consumers reckon that behavioral intentions may affect their actual behavior of purchasing healthcare insurance products or services. Many studies have explained about the consumers’ intention to purchase different types of products and services (e.g., green product, healthcare services, organic food products, halal products, and brand products) (Battour et al., 2019; Rahman et al., 2019; Rahman, Rana et al., 2021), however, this study focused on the consumers’ behavioral intention to purchase health insurance for their health safety and security. One’s comprehension of behavioral intention offers a crucial framework to influence consumers to purchase health insurance (Berkman et al., 2011). Yang and Su (2017) explored the correlation between intention and actual purchase behavior based on a research framework that incorporated the TAM and TPB as the core theoretical basis. As a result, consumers’ behavioral intention appeared to encourage the actual behavior, with an overall good model fit. Behavioral intention exerted a significantly positive impact on the actual purchase behavioral adoption (Alalwan et al., 2016; Elmorshidy et al., 2015). Based on the discussion above, the following hypothesis is proposed:

Hypothesis (H6): Intention to purchase health insurance has a significantly positive effect on the purchase of health insurance among working adults in Malaysia.

The Mediating Effect of Intention to Purchase Health Insurance

In light of robustness, this study expands the framework by looking into the mediating effect of the intention to purchase health insurance. Consumers’ insurance literacy, perceived usefulness, perceived behavioral control, attitude toward health insurance, and subjective norm may exhibit a significant impact on the intention to purchase health insurance. Nobles et al. (2019) claimed that health insurance literacy is significant to verify that people can accurately make decisions about purchasing health insurance products/services. The literature depicts that both attitude and perceived usefulness have a significant effect on intention (Jamal & Ahmed, 2007), while perceived behavioral control and subjective norm exert a positive impact on purchase intention (Shin & Hancer, 2016). Shao et al. (2004) and Karim et al. (2011) reported that purchase intention is linked with one’s willingness to purchase a particular product/service. This implies the scarcity in the literature pertaining to the mediating effect of consumers’ intention to purchase health insurance products and services. As such, this study proposes the following hypothesis:

Hypothesis (H7): Intention to purchase health insurance mediates the effect of insurance literacy, perceived usefulness, attitude toward health insurance, subjective norm, and perceived behavioral control on the purchase of health insurance among working adults in Malaysia.

The Moderating Effects of Perceived Product Risk and Income

To establish further robustness, this study expands the framework by exploring the moderating effects of perceived insurance product risk and average monthly income. Both TRA (Ajzen & Fishbein, 1980) and TPB (Ajzen, 1991) signify that people’s behavior is determined by their intention, which affects the actual purchase behavior of consumers. A wide range of studies reported that consumers’ intention displayed a significant influence on the actual purchase behavior (Berkman et al., 2011; Elmorshidy et al., 2015). Korgaonkar and Karson (2007) discovered a correlation between perceived product risk and retail shopping preference, whereas Snoj et al. (2004) found that perceive risk had a significant impact on perceived product value. Similarly, Ali et al. (2019) stumbled upon a positive link between income and purchase behavior; implying that people with higher income had higher purchase intention for goods/services for their living in the society. The literature seems to lack on the investigations regarding the moderating effects of perceived product risks and income on the purchase behavior of health insurance products/services. Therefore, the following are proposed:

Hypothesis (H8): Perceived product risk moderates the effect of intention to purchase health insurance on the purchase of health insurance among working adults in Malaysia.

Hypothesis (H9): Average monthly income moderates the effect of intention to purchase health insurance on the purchase of health insurance among working adults in Malaysia.

Based on the foundation of the TPB and the review of literature, Figure 1 illustrates the proposed hypotheses that form correlations between exogenous and endogenous variables.

Research Framework.

Research Methodology

Research Design

This study is the extension of the TPB model to investigate the Malaysian working adults’ health insurance purchase behavior. The unit of analysis of this study is working adults in Malaysia. For this study, the data were collected from individuals who were age group of above 18 years. Individuals who were age between 18 and above 50 years, suggested by Aziz et al. (2019). This is because this age group refers to earning individuals who are capable to support family and friends or others financially. The population of this study is 15.33 million working adults (Department of Statistics Malaysia [DOSM], 2021), however there is no available database of working adults. Therefore, we used non-probability convenience sampling method for the existing study, since this method is widely used in behavioral intention studies (Jin & Hye Kang, 2011; Letchumanan & Tarmizi, 2011; Md Husin & Ab Rahman, 2016). This technique is considered suitable since the existing sample has some characteristics, working adults, and an insurable age group.

The sample size in this study was determined using G-Power version 3.1. Upon considering the effect size of 0.15 and the power of 0.95, the required sample size was 160 to verify the research model with eight predictors. Data retrieved from more than 160 respondents were, thus, statistically adequate for this study. Nonetheless, due to the large population and to avoid the limitations that may arise from small sample size, data were gathered from more than 1,000 respondents.

Data in this present study were collected via online survey during the first 2 weeks of April 2020. This study designed a Google form that highlighted the purpose and the reporting procedure of the study, which was used to collect informed consent from all respondents prior to survey participation. The online questionnaires were distributed to respondents by sharing the Google form link of the questionnaire using social media (i.e., Facebook and WhatsApp). A total of 1,308 valid responses were yielded for this study.

Survey Instrument

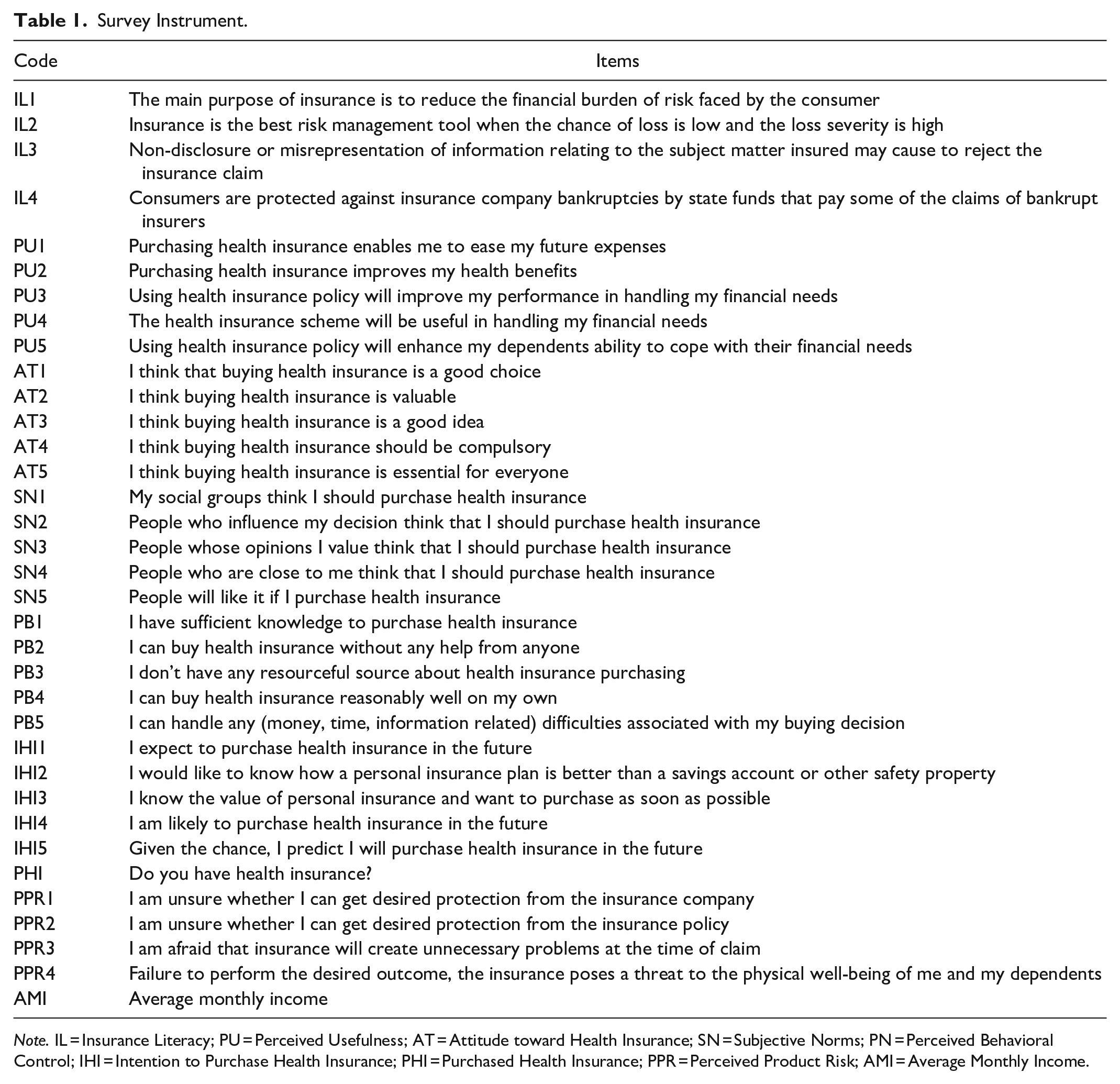

Data were gathered using self-administered questionnaires. The measurement instrument of this study was adopted from the literature. Four items were retrieved from Weedige et al. (2019) to assess insurance literacy, whereas five items were modified from Berkman et al. (2011) to examine perceived usefulness. Referring to Weedige et al. (2019), and Berkman et al. (2011), attitude toward health insurance was measured using five items. Five items on subjective norm were adopted from Berkman et al. (2011) and Md Husin and Ab Rahman (2016) to determine one’s social pressure linked with the purchase intention of health insurance products and services. Five items on perceived behavioral control were retrieved from Berkman et al. (2011) and Al-Swidi et al. (2014). Six items were adopted from Berkman et al. (2011), and Weedige et al. (2019) to evaluate the intention to purchase health insurance and the purchase behavior of health insurance. Perceived product risk was assessed using four items adapted from Weedige et al. (2019). Table 1 presents the survey instrument used in this study.

Survey Instrument.

Note. IL = Insurance Literacy; PU = Perceived Usefulness; AT = Attitude toward Health Insurance; SN = Subjective Norms; PN = Perceived Behavioral Control; IHI = Intention to Purchase Health Insurance; PHI = Purchased Health Insurance; PPR = Perceived Product Risk; AMI = Average Monthly Income.

Common Method Bias (CMB)

Prior to measurement model test, this study assessed the CMB. Since data were collected from single source in this study, common method bias may affect the study outcomes (Spector, 2006). As such, this study adhered to Podsakoff et al. (2003) by performing the Harman’s single factor analysis to address issues related to common method bias. This study examined the seven-factor analysis and found a total variance of 30.159%. This signified that CMB is not an issue in this study. This enabled the study to proceed with data analysis.

Data Analysis Method

Partial least squares structural equation modeling (PLS-SEM) was applied using the Smart-PLS software 3.1 for data analysis. The PLS-SEM is a multivariate analysis tool that assesses the study path model with latent constructs (Hair et al., 2018). The PLS-SEM allows scholars to work with non-normal and small datasets. The casual-predictive nature of the PLS-SEM is beneficial when working with complex models having composites and without assuming goodness-of-fit estimation (Chin, 2010). A two-step analysis scheme is suggested for data analysis in PLS-SEM. In the first stage, a measurement was performed on the model to test the reliability and validity of the study constructs (Hair et al., 2018). The second stage looked into the structural model associations and examination of study hypotheses with significance levels (Chin, 2010). Model estimation was implemented with r2, Q2, and effect size (f2) that describe the path effect from exogenous construct to endogenous construct (Hair et al., 2018). The importance-performance map analysis (IPMA) defines the study constructs into relatively high to low by importance and performance for endogenous construct (Chin, 2010).

Data Analysis

In studies concerning consumer behavior and other social science endeavors, the Partial Least Square (PLS) has been widely used for structural model analysis (Hair et al., 2011). Sarstedt (2008) claimed that PLS explains the causal relationship among constructs, while Vinzi et al. (2010) posited that PLS is a sophisticated software program that analyzes the dataset and is capable of identifying non-normal data distribution. Chin (1998) associated the PLS method with the component-based method that weighs in three major sets of relationships. First, the inner model works on the relationships with latent variables. Second, the outer or measurement model that stipulates the correlations among the latent variables and their corresponding observed variables. The last set refers to the weight relationships based on which the case values can be estimated for the latent variables. Hence, SmartPLS 3.0 was used to assess the research framework deployed in this study.

Demographic Characteristics

Referring to Table 2, out of the 1,308 respondents, male respondents (53.7%) exceeded their female counterpart (46.3%). Most of the respondents (56.6%) were 21 to 25 years, while 13.1% were below 21 years, and 11.9% were 26 to 30 years. As for ethnicity, 82.4% were Chinese, 11.3 were others, 4.1% were Malays, and the rest 2.1% were Indians. In terms of living areas, most of the respondents resided in urban areas (89%), while the others were from urban areas (11%). A majority of the respondents were single (82.3%), followed by married (16.6%), and divorced (0.6%). Most of the respondents held a bachelor’s degree or equivalent degree (59.3%), while 19.7% earned a diploma (19.7%) and 15.3% had secondary school certificate. About 56% of the participants earned below RM2500 a month, while 28.3% had a monthly income of RM2501 to RM5000.

Demographic Characteristics.

Measurement Model Analysis

The measurement model was assessed to determine the reliability and validity of this study. As presented in Table 3 the composite reliability (CR) of this study ranged between 0.914 and 0.816, which signified construct reliability, as Chin (2010) prescribed that CR should exceed 0.70. The AVE values ranged at 0.703 to 0.529, which indicates convergent validity. This range meets the criteria recommended by Hair et al. (2011) wherein convergent validity should be above 0.50. The Variance inflation factors (VIF) was assessed to measure the collinearity issue of the model. As a result, the highest and the lowest VIF scores of the construct were 2.136 and 1.013, respectively, confirming that the study is free from collinearity issue. As noted by Hair et al. (2011), collinearity issue exists if VIF value exceeds 5, while Diamantopoulos and Siguaw (2006) claimed that VIF score for each variable below 3.3 suggests that collinearity is not a concern in the study.

Reliability and Validity.

Source. Author’s data analysis.

Note. IL = Insurance Literacy; PU = Perceived Usefulness; AT = Attitude toward Health Insurance; SN = Subjective Norms; PN = Perceived Behavioral Control; IHI = Intention to Purchase Health Insurance; PHI = Purchased Health Insurance; PPR = Perceived Product Risk; AMI = Average Monthly Income; SD = Standard Deviation; CA = Cronbach’s Alpha; DG rho = Dillon-Goldstein’s rho; CR = Composite Reliability; AVE = Average Variance Extracted; VIF = Variance Inflation Factors.

Table 4 summarizes the discriminant validity. Fornell and Larcker (1981) criterion was used to determine discriminant validity. The results showed that the square root of AVE for each variable exceeded its correlation with other variables. For more robustness of discriminant validity, the Heterotrait Monotrait ratio (HTMT) was applied. As a result, the HTMT score was below 0.80; indicating that the discriminant validity was at satisfactory level. Gold et al. (2001) asserted that the cut-off point should be below 0.90 to ascertain discriminant validity.

Discriminant Validity.

Source. Author’s data analysis.

Note. IL = Insurance Literacy; PU = Perceived Usefulness; AT = Attitude toward Health Insurance; SN = Subjective Norms; PN = Perceived Behavioral Control; IHI = Intention to Purchase Health Insurance; PHI = Purchased Health Insurance; PPR = Perceived Product Risk; AMI = Average Monthly Income.

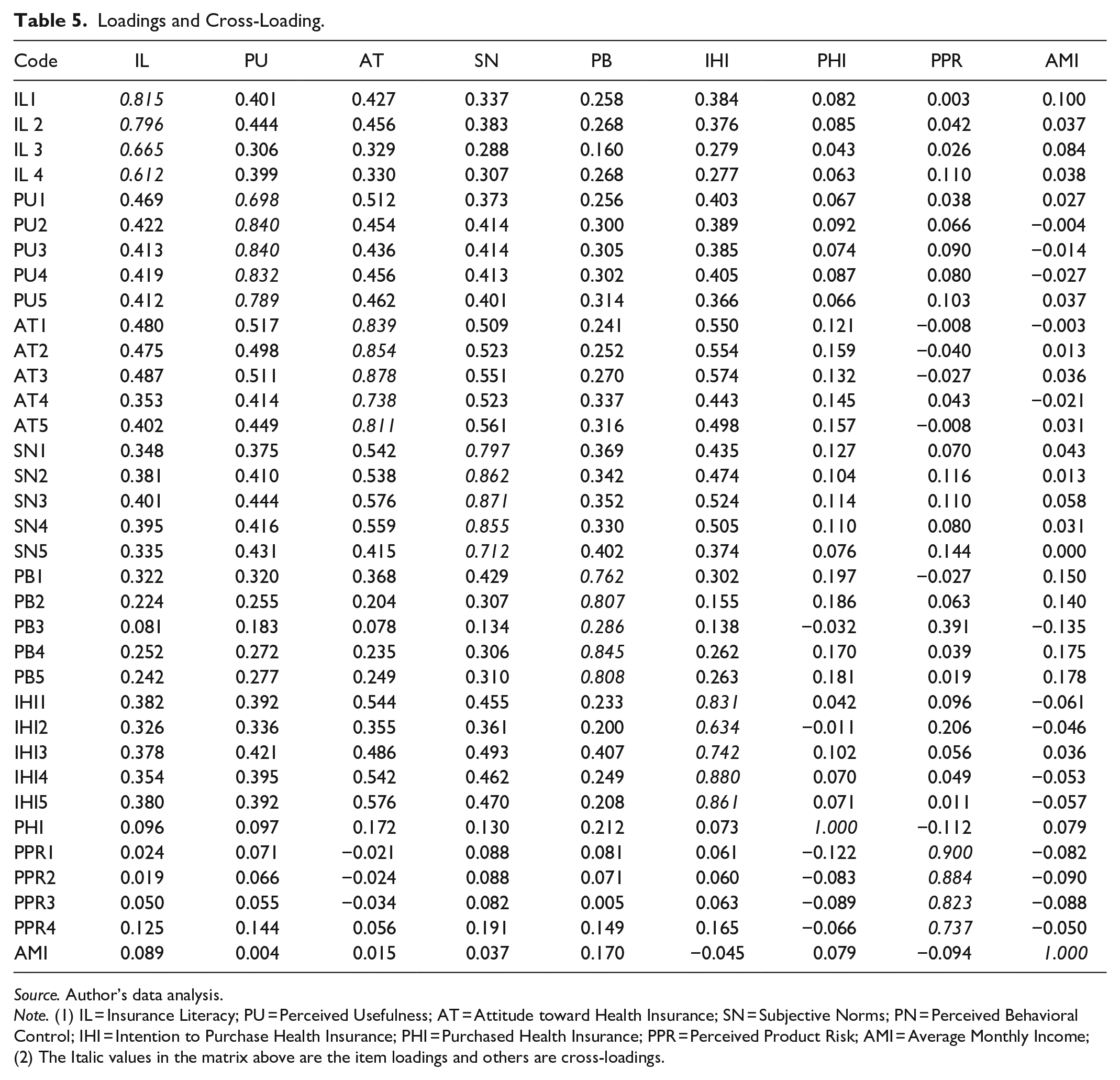

In further measuring the robustness of the model, cross-loading was performed to assess the discriminant validity of this study. Table 5 tabulates the cross-loading values of the constructs. Apparently, all constructs displayed a larger value on their corresponding indicators, thus implying that the discriminate validity was at satisfactory level, as prescribed by Hair et al. (2018). Findings of the robustness check presented in the Supplemental file including (a) Supplemental Table 1. Assessment of nonlinear effects and (b) Supplemental Table 2. Fit indices for the one to eight segment solutions.

Loadings and Cross-Loading.

Source. Author’s data analysis.

Note. (1) IL = Insurance Literacy; PU = Perceived Usefulness; AT = Attitude toward Health Insurance; SN = Subjective Norms; PN = Perceived Behavioral Control; IHI = Intention to Purchase Health Insurance; PHI = Purchased Health Insurance; PPR = Perceived Product Risk; AMI = Average Monthly Income; (2) The Italic values in the matrix above are the item loadings and others are cross-loadings.

Structural Model and Path Analysis

The bootstrapping procedure was carried out to evaluate the structural model. According to Hair et al. (2011), in order to estimate the structural model; R-square values, path coefficient, and t-values are some of the essential criteria that must be considered. R-square value of .75 is substantial, while .50 refers to moderate, and .25 denotes weak impact. Vinzi et al. (2010) stated that path coefficient is the degree of the predicted variation in latent variables. The PLS analysis of this study revealed that the variance of intention to purchase health insurance (R-square = .467) was moderately explained by insurance literacy, perceived usefulness, attitude toward health insurance, subjective norm, and perceived behavioral control. The variance of purchase of health insurance (R-square = .226) seemed to be weakly explained by the intention to purchase health insurance.

Referring to the outcomes (see Table 6), attitude toward health insurance (beta = .381, t-value = 13.328, p-value = .001), subjective norm (beta = .162, t-value = 6.616, p-value = .001), insurance literacy (beta = .093, t-value = 3.393, p-value = .001), and perceived usefulness (beta = .093, t-value = 2.908, p-value = .002) emerged as the most crucial factors for they exhibited highly significant and positive effect on intention to purchase health insurance. A significant correlation was observed between perceived behavioral control and intention to purchase health insurance (beta = .041, t-value = 1.764, p-value = .039). Besides, intention to purchase health insurance (beta = .092, t-value = 3.262, p-value = .001) exerted a highly significant relationship with purchase of health insurance. These findings signify that hypotheses H1, H2, H3, H4, H5, and H6 are accepted. Next, perceived product risk and average monthly income did not moderate the relationship between intention to purchase health insurance and purchase of health insurance. Therefore, hypotheses H8 and H9 are not accepted in this study. Table 5 presents the comprehensive summary of the path coefficients.

Path Coefficients.

Source. Author’s data analysis.

Note. IL = Insurance Literacy; PU = Perceived Usefulness; AT = Attitude toward Health Insurance; SN = Subjective Norms; PN = Perceived Behavioral Control; IHI = Intention to Purchase Health Insurance; PHI = Purchased Health Insurance; PPR = Perceived Product Risk; AMI = Average Monthly Income.

As for effect size (f2), Cohen (1988) reported that f-square .35, .15, and .02 reflect high, medium, and small effect sizes. Referring to Table 5, attitude toward health insurance displayed a moderate effect on the intention to purchase health insurance, whereas insurance literacy, perceived usefulness, subjective norm, and perceived behavioral control exemplified a small effect on the intention to purchase health insurance. Intention to purchase health insurance, perceived product risk, and average monthly income exhibited a minor effect on purchase of health insurance. The Q-square values determined the predictive relevance of the variable on the dependent variable (Fornell & Cha, 1994). Hair et al. (2013) asserted that values above zero signify the accuracy of the model. Based on Table 5, the Q-square values of intention to purchase health insurance (0.290) and purchase of health insurance (0.018) exceeded zero, which indicate the predictive relevance of endogenous construct.

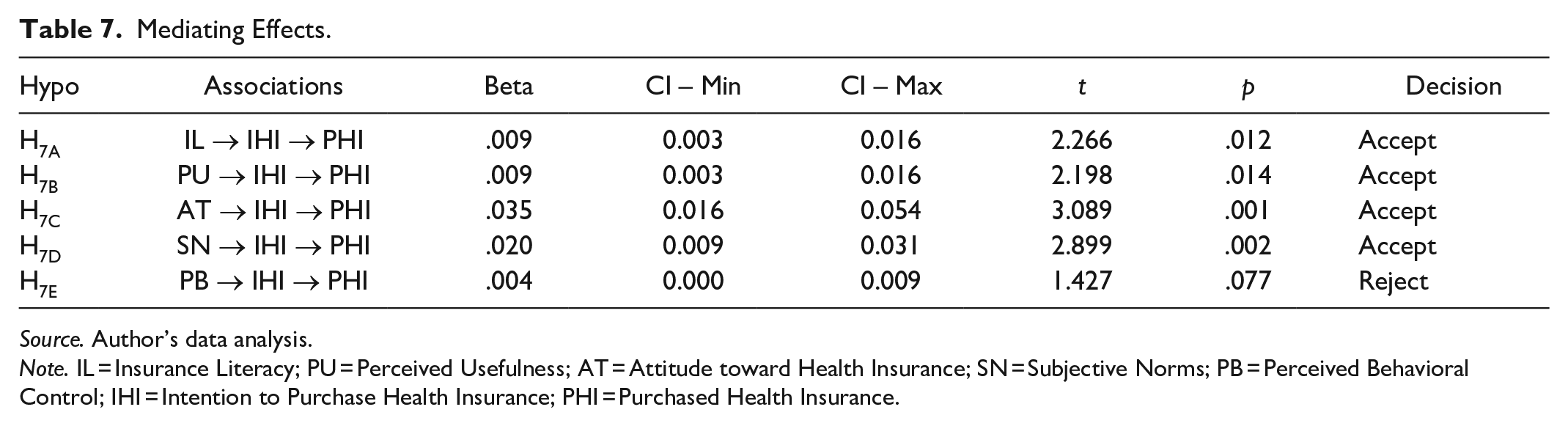

Mediation

Upon assessing the mediating effect of intention to purchase health insurance, coefficient of indirect effect, confidence intervals, t-values, and p-values were retrieved. Table 7 shows that intention to purchase health insurance mediated the relationship between insurance literacy and purchase of health insurance (beta = .009, t-value = 2.266, p-value = .012), perceived usefulness and purchase of health insurance (beta = .009, t-value = 2.198, p-value = .014), attitude toward health insurance and purchase of health insurance (beta = .035, t-value = 3.089, p-value = .001), as well as subjective norm and purchase of health insurance (beta = .020, t-value = 2.899, p-value = .002). Additionally, intention to purchase health insurance did not mediate the correlation between perceived behavioral control and purchase health insurance (beta = .004, t-value = 1.427, p-value = .077).

Mediating Effects.

Source. Author’s data analysis.

Note. IL = Insurance Literacy; PU = Perceived Usefulness; AT = Attitude toward Health Insurance; SN = Subjective Norms; PB = Perceived Behavioral Control; IHI = Intention to Purchase Health Insurance; PHI = Purchased Health Insurance.

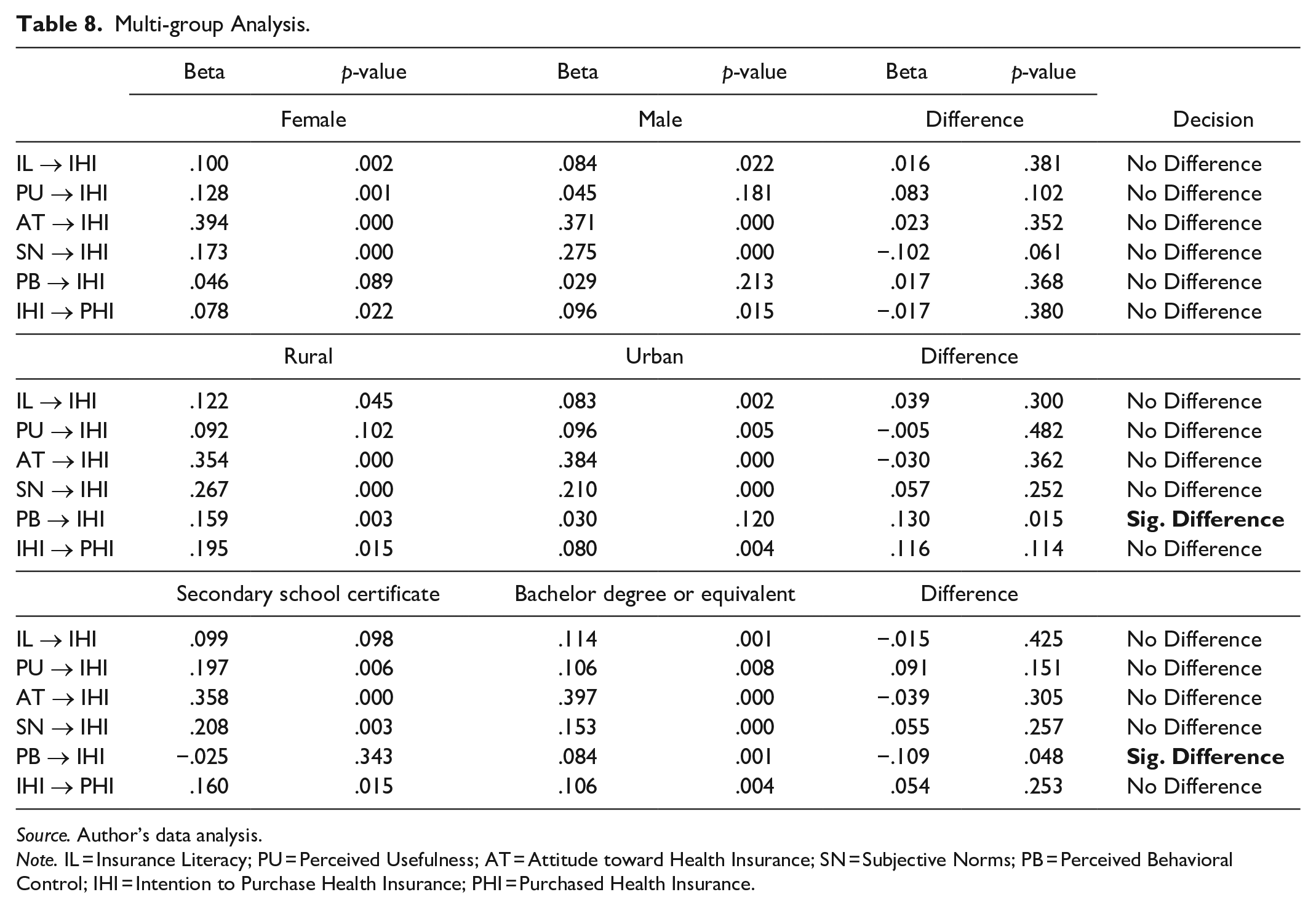

Multi-Group Analysis (MGA)

This study performed the MGA via PLS approach to better visualize the outcomes. Table 8 presents the variances in path coefficient assessments in three pairs of comparison (male vs. female, rural vs. urban, and secondary school certificate vs. bachelor degree/equivalent). These generate the findings of multi-group comparisons. Perceived behavioral control significantly differed from the rest. Although no significant variance was observed between male and female, the correlation between perceived behavioral control and intention to purchase health insurance emerged to be significant for the comparison between rural and urban samples (difference/beta = .130, p-value = .015), as well as for the comparison between secondary school certificate and bachelor degree/equivalent (difference/beta = −.109, p-value = .048).

Multi-group Analysis.

Source. Author’s data analysis.

Note. IL = Insurance Literacy; PU = Perceived Usefulness; AT = Attitude toward Health Insurance; SN = Subjective Norms; PB = Perceived Behavioral Control; IHI = Intention to Purchase Health Insurance; PHI = Purchased Health Insurance.

Importance-Performance Matrix (IPM)

The IPM was performed via PLS to determine the robustness of the study outcomes (Ringle & Sarstedt, 2016). The IPM concentrates on the construct to develop a target construct. The results revealed that the IPM attained the total effects of the links with other constructs (insurance literacy, perceived usefulness, attitude toward health insurance, subjective norm, perceived behavioral control, intention to purchase health insurance, perceived product risk, and average monthly income) on the target indicator of purchase of health insurance in order to highlight their significance. The data used for IPM of intention to purchase health insurance and purchase of health insurance as latent construct are tabulated in Table 9. Referring to Table 9, attitude toward health insurance appeared to be a crucial factor in predicting purchase of health insurance, as it was reflected by high importance and performance values. This was followed by intention to purchase health insurance, insurance literacy, perceived usefulness, subjective norm, perceived behavioral control, perceived product risk, and average monthly income. Figure 2 illustrates the IPM and elaborates the outcomes of purchase of health insurance as the target factor.

Performance and Total Effects.

Source. Author’s data analysis.

Importance-Performance Map.

Discussion

In this study, insurance literacy is a significant predictor of intention to purchase health insurance. This reflects the importance of insurance literacy amongst working adults to purchase a healthcare insurance plan. This result is in agreement with that reported by Nobles et al. (2019), Weedige et al. (2019), and Paez et al. (2014), whereby insurance literacy is a prerequisite for one to subscribe an insurance scheme. Perceived usefulness exerted an important effect on the intention to purchase health insurance, mainly because working adults believe that insurance company offers innovative technology that intensifies their intent to purchase health insurance products and services. Similarly, Cucinelli et al. (2021), and Berkman et al. (2011) discovered that perceived usefulness has a crucial role in deciding the purchase of health insurance. Attitude toward health insurance exhibited a significantly positive effect on the intention to purchase health insurance. This shows that working adults favor the evaluation of health insurance service quality and benefits, thus supporting the findings reported by Aziz et al. (2019).

This study reports that subjective norm is a crucial determinant of intention to purchase health insurance among Malaysian working adults. This means; consumers’ behavior toward purchase of health insurance products and services is influenced by family, friends, relatives, colleagues, and other people perceived as important. The view of others on subjective norm encourages the purchase of a health insurance plan. In a similar vein, Al-Swidi et al. (2014) and Bianchi et al. (2018) found that subjective norm as an integral predictor of consumer intentions. Insurance companies, hence, may offer a family package that covers the whole family for health insurance, use an influential figure for health insurance campaigns, and co-operate with the government to provide training to the public regarding the significance of purchasing health insurance.

This study highlights the significance of perceived behavioral control on the intention amidst working adults to purchase health insurance. This reflects the presence of both internal and external phenomena with a crucial role in deciding the purchase of health insurance. Working adults in Malaysia possess the financial ability that intensifies their intent to purchase a health insurance plan. In line with Bianchi et al. (2018), Al-Swidi et al. (2014), and Lee et al. (2010), financial ability appears to be a fundamental mechanism in purchasing a health insurance scheme. The intent amidst working adults to purchase health insurance is affected by other behavioral factors, including insurance information, perceived complexity, and regulation literacy. This implies that insurance companies need to provide training programs in order to educate people about the knowledge of health insurance, provide information, and formulate simpler procedures. By doing so, Liebenberg et al. (2012) ascertained that people would be encouraged to purchase health insurance products and services.

In this study, the intention of working adults to purchase health insurance exemplified a significantly positive effect on the behavior of purchase health insurance. This reflects that the working adult group with the intent to purchase health insurance may be influenced to actually purchase a health insurance plan. Apart from being in agreement with the TPB, the outcomes are also in line with that reported by Hsieh et al. (2019), Berkman et al. (2011), and Prabawanti et al. (2014), who found that consumer intention reflects the actual purchase behavioral adoption. Additionally, the mediating effect of intention to purchase health insurance on the relationships of health insurance, perceived usefulness, attitude toward health insurance, subjective norm, and perceived behavioral control with purchase of health insurance had been statistically significant. This signifies that the intention among working adults to purchase health insurance serves as a crucial component and is attributed to the above-mentioned correlations. These findings appear to complement the TPB and significantly contribute to the theory by using the intention amidst working adults to subscribe to health insurance as mediators.

Conclusion

The study outcomes associated the relationships between TPB components and intention of working adults, which in turn, leads to purchase of health insurance. A new component called “insurance literacy” was embedded into the TPB model, which appeared to be a crucial aspect for Malaysian working adults to purchase health insurance. This study adapted the TPB model to probe into the effect of insurance literacy of working adults, perceived usefulness, attitude toward health insurance, subjective norm, and perceived behavioral control on purchase of health insurance through the intention to purchase health insurance. Theoretically, the study outcomes contribute to the TPB, predominantly by assessing the mediating effect of intention to purchase health insurance within the context of Malaysian working adults. In this study, the TPB explains the psychological factors that affect the intention among working adults to purchase health insurance. Health insurance demand or purchase intention is motivated by one’s attitude toward health insurance, subjective norm, perceived behavioral control, and perceived usefulness.

The findings retrieved from this study serve as a guide to both the government and insurance agencies to better comprehend the importance of insurance literacy among working adults. Both the government and insurance companies may take the initiative to educate people regarding the significance of subscribing to health insurance, apart from motivating them to purchase health insurance. Insurance agencies can promote insurance literacy, perceived product risk, and average monthly income to create more demand for the intention to purchase health insurance. Moreover, insurance policymakers and marketing operators should weigh in insurance literacy, perceived usefulness, perceived behavioral control, attitude toward health insurance, and subjective norm to increase the number of working adults interested in purchasing health insurance and eventually purchase a health insurance plan.

This study has several drawbacks. Since the data were collected only from a single host country—Malaysia, the findings may not be generalized from the international stance. The data was collected using the social media platform to share the online questionnaire link and collected data from self-selected respondents. Besides, there is lack of previous studies on the topic, and the limited number of constructs investigated in this study is another shortcoming. Hence, future studies can include self-rated health (perceived need) and satisfaction toward purchase of health insurance services. Future endeavors may also weigh in the psychological aspects that were excluded from this present study, such as the role of social norms and the knowledge regarding consumers’ intention to purchase health insurance. As such, the social exchange theory may be applied, instead of the TPB, to evaluate consumers’ psychological role on the intention to purchase health insurance. Although this study has focused on only the perspective of Malaysian consumers’ intention to purchase health insurance, however the findings of this study may reflect intentional healthcare insurance market because customers’ psychological behavioral aspects can transform the niche market of world healthcare insurance.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440211061373 – Supplemental material for Predicting the Intention and Purchase of Health Insurance Among Malaysian Working Adults

Supplemental material, sj-docx-1-sgo-10.1177_21582440211061373 for Predicting the Intention and Purchase of Health Insurance Among Malaysian Working Adults by Abdullah Al Mamun, Muhammad Khalilur Rahman, Uma Thevi Munikrishnan and P. Yukthamarani Permarupan in SAGE Open

Footnotes

Authors’ Contributions

Abdullah Al Mamun contributed to the conception, research design, data analysis and interpretation of data, and prepared the final draft. Muhammad Khalilur Rahman, Uma Thevi Munikrishnan and P. Yukthamarani Permarupan contributed to the research design, questionnaire design, data collection and prepared the manuscript.

Availability of data and materials

All data generated or analyzed during this study are included in this Submission (Data File - Health Insurance)

Consent to Participate

Written informed consent for participation was obtained from respondents who participated in the survey. For the respondents who participated the survey online (using google form), they were asked to read the ethical statement posted on the top of the form (There is no compensation for responding nor is there any known risk. In order to ensure that all information will remain confidential, please do not include your name. Participation is strictly voluntary and you may refuse to participate at any time) and proceed only if they agree. No data was collected from anyone under 18 years old.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical Approval

Local ethics committees (UCSI University, Malaysia) ruled that no formal ethics approval was required in this particular case. Furthermore, this study has been performed in accordance with the Declaration of Helsinki.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.