Abstract

In recent years, China has vigorously promoted the construction of an ecological civilization, dual-carbon goals, and strengthened corporate environmental responsibility and information disclosure requirements. In this context, to meet regulatory pressure or market preferences, some enterprises adopt the practice of “greenwashing” to create a false image of sustainable development. This results in distorted financial reporting information. Such behavior not only undermines stakeholder trust but also heightens audit risk by significantly increasing audit complexity and risk exposure through hidden compliance risks as well as a management propensity for fraud and uncertainty around environmental liability. Hence, we took Chinese A-share firms from 2011 to 2023 as the research object, empirically tested the impact of corporate greenwashing behavior on audit risk by using a fixed-effects model, and explored the mechanism that affects the relationship between the two. The empirical results indicate that opportunistic greenwashing behavior increases audit risk; stable equity plays a negative moderating role between the two, and relational debt plays a positive moderating role between the two. Simultaneously, greenwashing increases audit risk by raising Type II agency costs. The effect of corporate greenwashing on audit risk is more significant in non-Big Four accounting firms and non-high-tech industries. This study provides directions for enterprises to optimize their capital structure and reinforce their internal controls, and helps regulators formulate precise regulatory policies to maintain the sustainable development of the market.

Introduction

Greenwashing behavior refers to when an enterprise caters to market needs by falsely publicizing its own environmental achievements and measures; on the surface, an enterprise may claim that environmental protection initiatives are underway, but in fact, the enterprise is concealing its non-environmental protection behavior (W. Li et al., 2023). Enterprises’ greenwashing behavior violates the concept of green development, hinders the healthy growth of industry, constitutes a threat to the veracity of ESG reports (Environmental, Social, and Governance) and raises concerns about the authenticity of an enterprise’s commitment to environmental protection (Coen et al., 2022; S. Hu, Wang, et al., 2023). Thus, the governance of enterprises’ greenwashing behavior requires attention.

From the behavioral science perspective, enterprises’ greenwashing behavior is due to opportunistic decision-making driven by bounded rationality and self-interest. With the advancement of dual-carbon goals, environmental protection policies and tax incentives create a dual incentive mechanism, prompting enterprises to determine appropriate reference points for achieving “green compliance” (Puppo et al., 2022). According to the reference dependence theory (Pennesi, 2025), enterprises typically assess the “gain” or “loss” of their environmental performance relative to policy standards or industry benchmarks. When actual environmental performance falls below the reference point, loss aversion (Gaechter et al., 2007) may prompt firms to engage in greenwashing; they opt to make misleading claims to avert reputational and financial harm, rather than substantively improving in their environmental practices.

According to the information asymmetry theory, there is an obstacle to the acquisition of knowledge between the enterprise and its stakeholders, and there is a discrepancy between the information acquired by the two (J. Liu & Chen, 2025). In the face of performance pressure, in order to obtain more short-sighted psychological satisfaction and alternative compensation, companies will choose to sacrifice the opportunism of high-quality growth (Buchanan et al., 2021) and conceal the corresponding information. Greenwashing is favored by opportunists. In addition, “greening” enterprises often only disclose environmental information in their favor, deliberately hiding the negative impact of corporate information so that other stakeholders and consumers are unable to comprehensively understand the actual situation of the enterprise’s products and environmental initiatives. This not only damages the interests of stakeholders but also increases the difficulty of auditing, thereby increasing audit risk (El-Deeb et al., 2023).

Patient capital mainly includes relational debt dominated by bank loans and stable equity dominated by institutional investors (Bergin et al., 2021). Compared with the short-sighted behavior and opportunism of drifting green, patient capital pays more attention to long-term returns and can provide long-term, stable financial support for investment projects and capital markets. As for relational debt, cooperation between creditors and debtors will increase information barriers and heighten pressure to meet performance standards. Moreover, it is difficult for auditors to obtain accurate and sufficient information to assess the authenticity and reasonableness of the transaction. This induces management to whitewash financial statements through greenwashing (Kallias et al., 2022), thus increasing audit risk. In terms of stable equity, institutional investors, as “long-term investors,” are more forward-thinking and pay more attention to manufacturing enterprises’ strategy and capacity for future development, which reduces audit risk and inhibits management’s short-sightedness (Tang et al., 2022). This differential moderating effect reflects the behavioral shaping effect of capital structure on managers’ risk preferences (Shang, 2021).

When equity is highly concentrated, the controlling shareholders’ control and cashflow rights are seriously deviated, and the conflict of interest between the dominant controlling shareholders and small and medium-sized shareholders intensifies (L. Chen & Yin, 2024). Type II agency costs are incurred by the controlling and minority shareholders due to conflicts of interest (Brogi et al., 2021).

Then, if the internal control aspects of the audited entity have deficiencies (Baer et al., 2023), and if the principal-agent problems among shareholders are exacerbated (Bona-Sánchez et al., 2024), makes Type II agency costs rising, insufficient monitoring and approvals of related-party transactions may cause claims to be inaccurately recorded. Auditors may fail to detect potential misstatements due to these defects, thus increasing audit risk (Moon et al., 2024).

Although existing studies have observed the relationship between greenwashing behavior and audit risk, almost no empirical studies have analyzed the impact of greenwashing behavior on audit risk (Wu, 2022). Most existing studies concentrate on the motivation and economic consequences of greenwashing behavior but fail to systematically explore the transmission mechanism of audit risk. Moreover, these studies predominantly rely on theoretical deductions rather than large-scale empirical evidence, and lack quantitative analyses of regulatory and intermediation pathways (Eliwa et al., 2023; O’Reilly et al., 2023). Additionally, concerning the effect of capital structure on greenwashing behavior, most studies examine only the general roles of equity or debt without differentiating among the distinct moderating effects of stable and relational debt. Furthermore, research from the agency cost perspective centers primarily on the first type of agency problem, thus neglecting the mediating role of conflicts between controlling and small/medium shareholders (Type II agency costs) in the relationship between greenwashing and audit risk.

Hence, we aimed to examine the impact of greenwashing behavior on the audit risk of Chinese firms by using data from Chinese listed firms. We also aimed to identify the moderating factors that regulate the relationship between them and the mediating factors that act as pathways.

Compared with the existing literature, the contributions of this study are as follows:

(1) We empirically investigate the impact of greenwashing behavior on audit risk using data from Chinese listed firms, which compensates for the lack of empirical research in related fields.

(2) We scrutinize the moderating role of patient capital under different dimensions (i.e., stabilized equity and relational debt), which provides references for introducing more appropriate capital for stakeholders.

(3) We analyze internal shareholders’ conflicts in relation to audit risk, thereby providing directions for internal control.

This study addresses these gaps by empirically analyzing Chinese A-share data. The contribution lies in constructing a multi-dimensional analytical framework of “behavioral motivation-capital structure-agency conflict,” which not only enriches theoretical understanding but also has practical implications for optimizing corporate governance, capital allocation, and audit regulation.

Theoretical Analysis and Hypotheses

Impact of Corporate Greenwashing on Audit Risk

Behavioral economics theory states that decision makers are not completely rational but are driven by cognitive bias and emotions (Bleda et al., 2025). Under the pressure of environmental protection policies, enterprises use policy requirements or the industry average as a reference point and evaluate the “gain” and “loss” of investing in environmental protection through loss aversion. When actual environmental performance is lower than the reference point, firms may choose to engage in greenwashing behavior to avoid perceived losses (Santos et al., 2024), rather than incur high costs for substantial improvements. This shortsighted opportunistic strategy leads to internal control failures (Cao et al., 2023) with distorted financial information (e.g., inflated green investments; Feng et al., 2021). This significantly heightens the risk of material misstatements in financial statements.

Impression management theory (G. Liu et al., 2024) suggests that companies selectively disclose environmental information to create a “green image,” but that concealing negative information will make it more difficult for auditors to verify it. Auditors face complex environmental terminology and technical indicators, and their professional competence may not be sufficient to identify greenwashing behavior, thus increasing inspection risk (M. Yang et al., 2025).

Due to reliance on references and loss aversion, corporate greenwashing behavior raises the risk of making material misstatements through internal controls and financial risk while increasing inspection risk through impression management strategies and professional competency requirements for auditors. Thus, we proposed Hypothesis 1 (H1).

Moderating Role of Patient Capital

As a long-term, stable source of financial support, patient capital can withstand short-term market fluctuations and provide a steady source of funding for firms due to its high degree of risk tolerance and long-term goals for returns (Breuer et al., 2024). Combining current findings and the realistic role of patient capital, we categorized patient capital into two dimensions: stable equity and relational debt.

Based on a stable equity structure, through the equity market, firms are able to more easily access long-term finance (Palea, 2022) to support their expansion and innovation activities. This type of financing is more flexible than traditional bank financing and can reduce firms’ financial leverage and financial risks (L. Yang et al., 2021). In addition, this capital structure reduces opportunistic behavior triggered by short-term performance pressure by reinforcing the alignment of interests between management and shareholders (Back & Colombo, 2022).To maintain a certain level of financial indicators and cashflow, avoid the supervision of creditors, obtain more lenient loan conditions, and reduce long-term financing costs, companies engage in greenwashing, embellish their financial statements and credit image (Kallias et al., 2022), and exaggerate the effectiveness of environmental protection. This prompts them to pay more attention to long-term environmental investment, reducing the incentive for greenwashing and thus reducing audit risk. That is, stable equity has a negative moderating effect on audit risk. Hence, we formulated Hypothesis 2 (H2).

According to goal gradient theory (Zou et al., 2024), when companies face debt repayment pressure, management tends to take shortcuts (e.g., greenwashing) to quickly achieve financial goals and avoid triggering the risk of debt default. This strategic action increases environmental data and transaction complexity; the auditor needs to invest more resources to verify the authenticity of information so that audit difficulty and risk increase (Bastos et al., 2021) (i.e., relational debt has a positive moderating effect on audit risk). Based on this, we developed Hypothesis 3 (H3).

Mediating role of Type II Agency Costs

The mediating role of Type II agency costs can be explained by the behavioral mechanisms of “private benefits of control” (Breugem et al., 2021) and “moral hazard” (L. Chen, 2024). To obtain private benefits of control, controlling shareholders may cover up their tunneling behaviors through greenwashing (D. Chen et al., 2022). Such behavior not only distorts financial statements but also forces the auditor to carry out additional verification of complex related transactions; this increases the auditing workload and the risk of misjudgment (Mwintome et al., 2024). Simultaneously, in firms with a high concentration of equity, controlling shareholders may weaken internal controls by manipulating the board of directors (J. Zhou et al., 2021), thereby creating a moral hazard. Lack of effective checks and balances for small- and medium-sized shareholders, may render management more likely to cater to the short-sighted needs of controlling shareholders and choose greenwashing over substantive environmental inputs. This leads to a decline in the quality of financial information; auditors need to rely on limited information to make judgments, which further amplifies inspection risk. Type II agency costs play a positive role as a mediating variable in the relationship between exemplary behavior and audit risk. Based on this, we proposed Hypothesis 4 (H4; Figures 1 and 2):

Framework of hypotheses 1, 2, 3.

Framework of hypotheses 4.

Research Design

Sample Selection and Data Acquisition

We selected data from China’s A-share listed companies spanning 2011 to 2023 as the research sample. As for the raw data, we excluded (1) samples belonging to the financial industry; (2) ST, *ST, and PT enterprises; and (3) the observations of the missing data samples. To attenuate the influence of outliers and extreme values on the findings, we use the winsor2 command to shrinkage the main continuous variables at 1% and 99% levels and logarithmically treated outliers to eliminate the effects of heteroskedasticity (Goes et al., 2025). We obtained a total of 24,882 sample data points and selected patient capital data from the WIND database. We obtained all other data from the CSMAR database.

Variable Definitions and Descriptions

Dependent Variable: Audit Risk (Ar)

To reflect the actual situation of audit risk more accurately, we considered the economic scale of the enterprise and the complexity of the audit work. Referring to Calderon and Gao (2021) on the relationship between audit risk and audit fees, we used the audit fee of the following year as a value to measure audit risk; the higher the value, the greater the audit risk.

Independent Variable: Greenwashing (Gw)

Referring to X. Hu, Hua, et al. (2023) on greenwashing behavior, we constructed the Gw variable based on the inconsistency between a firm’s oral and actual green performance. If a firm had a higher frequency of words related to environmental protection in its management discussion and analysis (MD&A) section than the median of firms in the same industry, but its actual environmental performance was poor (e.g., lower environmental ratings or environmental violations), we labeled the firm as engaging in greenwashing and assigned Gw a value of 1. Conversely, if a firm’s oral greenwashing was inconsistent with its actual greenwashing, then we constructed the Gw variable based on the inconsistency between the firm’s oral and actual greenwashing. If a company’s verbal green propaganda matched its actual green performance, or if its actual performance was good in spite of the propaganda (i.e., it was not “overly” propagandized for the purpose of misleading people), then we assigned Gw a value of 0.

Moderating Variable

Stable Equity (Invest)

Stable equity is the ratio of the proportion of total equity held by investors in firm i in year t to the standard deviation of their shareholdings over the past 3 years. The larger Invest is, the more stable institutional investors are in the time dimension.

Relational Debt (Rebt)

Relational claims are expressed as the ratio of long-term liabilities (e.g., long-term borrowings, bonds payable, long-term payables, etc.) to total liabilities for publicly traded companies.

Mediating Variable: Type II Agency Costs (AC2)

Referring to S. Zhou et al. (2024), the direct “occupation” of funds by major shareholders is reflected in financial statements, mainly in other receivables. We chose the ratio of other receivables to total assets to measure Type II agency costs; the larger the ratio, the higher the enterprise’s Type II agency costs.

Control Variables (Control)

Referring to prior literature (D. Chen et al., 2022; Desalegn & Tangl, 2022) and enabling a more precise estimation of the independent impact of corporate greenwashing behavior on audit risk. We selected the following variables are incorporated to mitigate potential confounding effects on audit risk for control in this paper: the number of years the company has been listed (Age), the gearing ratio (Lev), the cashflow ratio (Cashflow), the proportion of independent directors (Indep), the total asset turnover ratio (Ato), the growth rate of operating income (Growth), the two positions in one (Dual), the net profit margin of total assets (Roa), and return on net assets (Roe). Additionally, we controlled for industry (Ind) fixed benefits and year (year) fixed effects. Table 1 shows definitions and descriptions of the variables used in this study.

Definitions of the Variables.

We built Model (1) to verify H1, the effect of corporate greenwashing behavior on audit risk, and clusters at the corporate level to adjust for standard errors. On this basis, to further analyze the impact of the interaction between corporate greenwashing behavior and patient capital on audit risk, we built Model (2) and Model (3), which contain the moderating effect. The specific models are as follows:

where i and t denote belonging to the firm and year, respectively; ARi,t+1 is the explanatory variable of audit risk; Gw i,t is the explanatory variable of firms’ greenwashing behavior; and Invest i,t and Rebt i,t are the moderating variables of patient capital. Controls i,t refers to the control variables; ΣInd and ΣYear are the fixed effects of the year and the industry; and ε i,t signifies the random disturbance term. This is the same below.

To test H4, we used the 3-step regression method of Fang et al. (2023). First, we regressed Model (1) to test the effect of greenwashing on audit risk. Second, we regressed Model (4) to test the effect of greenwashing on Type II agency costs, and we built Model (5) by incorporating greenwashing and Type II agency costs to test the regression outcomes.

Empirical Results and Analysis

Descriptive Statistics

Variance inflation factor (VIF) tests were first conducted in this study, with all VIF values being below 2, indicating the absence of multicollinearity among the variables. Table 2 presents the descriptive statistics for each variable. As seen in Table 2, the mean value of audit risk is 13.979, and the minimum and maximum values are 12.543 and 16.244, respectively. This indicates that there is no significant difference in audit risk among the sample firms and that there is generally a higher risk, which highlights the importance of the need for all parties (such as auditors, regulators, and investors) to be more careful and prudent in assessing and controlling audit risk. The mean value of corporate greenwashing is 0.227 and the standard deviation is 0.419, implying that corporate greenwashing is widespread in the industry and varies greatly among different companies. This suggests that strict and precise regulatory crackdowns on corporate greenwashing are needed. Simultaneously, the table implies that the difference in stability equity between sample firms is large, while the difference in relational claims is small. However, there are extreme cases of the phenomenon, meaning that the shareholding structure of enterprises still needs to be optimized.

Descriptive Statistics.

Regression Analysis and Robustness Test

Table 3 presents the benchmark regression outcomes. After the Hausman test, we chose a fixed-effects model for analysis. Column (1) displays the standard full sample regression after controlling for the control variables, firm-year fixed effects, industry fixed effects, and clustering at the firm level. The results in Column (1) suggest that the coefficient of the impact of greenwashing behavior on audit risk is 0.043 and significant at the 1% level, which indicates that a one-unit increase in greenwashing is associated with a 0.043-unit increase in audit risk. This implies that a rise in greenwashing behavior increases the enterprise’s audit risk, thus supporting H1.

Regression Outcomes and Robustness Tests.

Note. t-Values are in parentheses; ***,**, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

To ensure the credibility of the main effects regression, we conducted a robustness test in terms of omitted variables, replacing the random effects model and adding uncontrollable factors, as follows.

Omitted Variables

A company’s governance structure may have an impact on greenwashing behavior. Since omitted variables can cause endogeneity problems, we further added board (the natural logarithm of the number of boards of directors) and Top1 (the number of shares held by the first largest shareholder/total shares) as a way of solving the problem of omitted variables. The regression results in Column (2) of Table 3 show that greenwashing behavior still positively affects audit risk at the 1% level, indicating the robustness of the main effects regression.

Random Effects

Since the data in this study are longitudinal, referring to we replaced the two-way fixed effects model with a random-effects model to exclude the influence of industry and time constraints on the regression outcomes. The regression results are displayed in Column (3) of Table 3, where greenwashing behavior still positively affects audit risk at the 1% level, illustrating the robustness of the main effects regression.

Uncontrollable Factors

To further control for the impact of unobservable factors at the district level that do not vary over time on the estimation outcomes, we added district fixed effects to the baseline regression model. The regression outcomes are depicted in Column (4) of Table 3, where greenwashing behavior still positively affects the audit risk at the 1% level, illustrating the robustness of the main effects regression.

Moderating Effects

Given that the impact of greenwashing behavior on audit risk may be affected by the role of heterogeneous patient capital, we introduced stable equity and relational debt as moderating variables to examine the moderating effect of patient capital on the relationship between greenwashing behavior and audit risk as well as the difference in the moderating effect under different dimensions. Table 4 presents the regression outcomes.

Moderating Effects and Heterogeneity Analysis.

Note. t-Values are in parentheses; ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Columns (1) and (3) of Table 4 portray the results without including the control variables. Columns (2) and (4) show the outcomes, including the control variables. The moderating effects of stabilizing equity and relational debt, respectively, are almost indistinguishable, regardless of whether control variables are included. In particular, stable equity depicts a negative moderating effect at the 1% level, indicating that stable equity reduces the impact of greenwashing behavior on audit risk, while relational claims positively moderates at the 5% level, implying that relational claims promote the impact of greenwashing behavior on audit risk. This finding underscores the difference in the moderating role of patient capital in different dimensions in the moderating role of greenwashing behavior on audit risk, thus validating H2 and H3.

Mediating Effect and Sobel Test

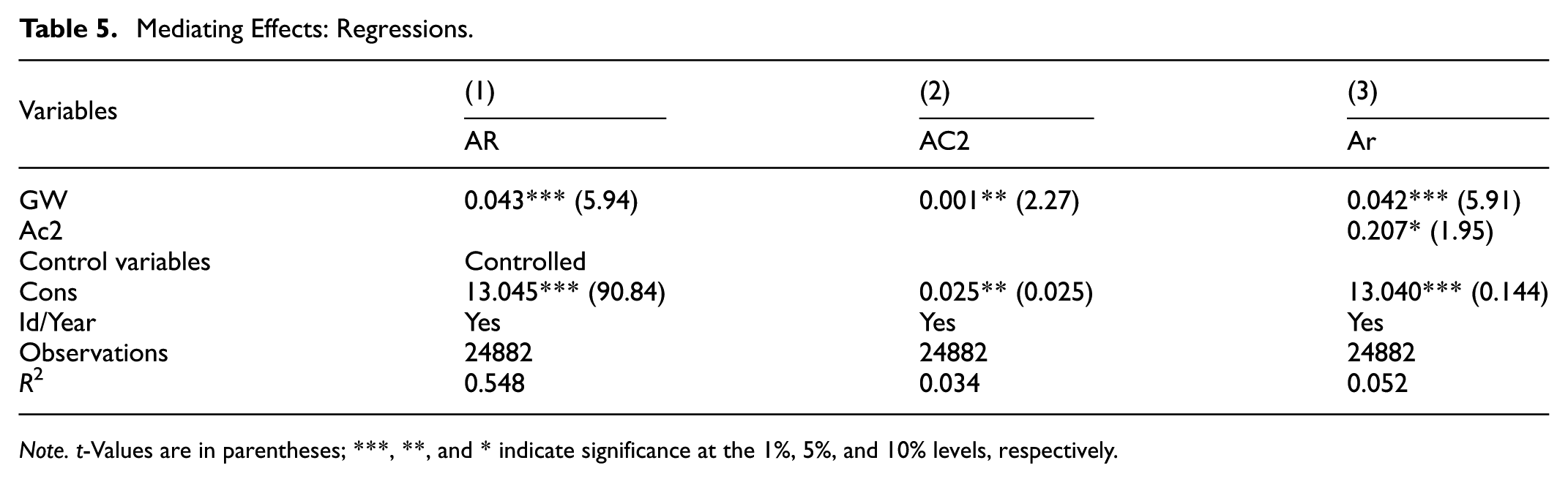

Table 5 displays the regression outcomes. The results in Column (1) of Table 5 indicate that greenwashing behavior is positively significant at the 1% level for Type II agency costs. After including the Type II agency cost variable, greenwashing behavior is also significant at the 1% and 10% levels, respectively, and the coefficient of greenwashing behavior declines after including the control variable, suggesting a mediation effect.

Mediating Effects: Regressions.

Note. t-Values are in parentheses; ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Since the testing power of the Sobel test is higher than that of the stepwise regression method, the Sobel test used in this study further validated the model. After the Sobel test, the p-values of Sobel, Goodman-1, and Goodman-2 were significant at the 1% level, which verified the existence of a mediation effect.

Heterogeneity Analysis

From the audit subjects’ perspective, exposure to greenwashing behavior serves as a critical indicator of audit quality. To determine whether there are differences in the relationship between greenwashing behavior and audit risk across different audit subjects, we incorporated the interaction term of Gw and the Big4 into Model (2). Column (5) in Table 4 shows the regression results. We can see that Big Four accounting firms are capable of mitigating the impact of greenwashing behavior on audit risk; this is attributable to their stricter audit procedures, more professionally qualified auditors, and richer audit experience.

From the perspective of audit objects, greenwashing behavior reflects an enterprise’s practices around disclosing information externally. Based on Model (2), we introduced an interaction term between high-tech industries and greenwashing. The regression results, displayed in Column (6) of Table 4, indicate that the interaction term positively influenced audit risk at the 5% significance level. This suggests that in addition to its inherent influence, impression management theory may lead auditors and other social groups to underestimate the behavioral risks associated with high-tech sectors, thereby amplifying the impact of greenwashing behavior. Moreover, high-tech industries possess strong resource endowments and a greater capacity to withstand audit risk, resulting in their direct impact on audit risk being negative and significant at the 10% level. Notably, the p-value for the effect of high-tech industries on audit risk is .098, suggesting the potential long-term difficulty of mitigating the negative effects of audit risk.

Discussion

The empirical results of this study establish that corporate greenwashing constitutes a significant determinant of audit risk. This finding addresses a critical gap in the extant literature, which has predominantly focused on the motivations and economic consequences of greenwashing (O’Reilly et al., 2023; Wu, 2022) while offering limited large-sample empirical evidence on its implications for the audit process. Our analysis grounded in behavioral economics and impression management theory, elucidates the mechanisms behind this relationship. Firms driven by reference dependence and loss aversion, engage in opportunistic greenwashing to bridge the gap between their actual environmental performance and regulatory or industry benchmarks. This strategic misrepresentation not only exacerbates information asymmetry but also intentionally obfuscates the firm’s true environmental footprint, thereby increasing the complexity of the auditor’s verification task and elevating both inherent risk and detection risk.

A key contribution of this study lies in introducing a nuanced perspective on patient capital by disaggregating it into stable equity and relational debt. While prior research often treats capital structure in a monolithic manner (Bergin et al., 2021), our findings reveal its heterogeneous moderating effects. Stable equity, characterized by its long-term orientation, mitigates the positive association between greenwashing and audit risk. Institutional investors’ forward-looking perspective helps curb managerial myopia, aligning managerial actions with long-term value creation and reducing the incentive for short-sisted greenwashing. Conversely, relational debt amplifies this relationship. The performance pressure and complex information environment associated with such debt can induce managers to employ greenwashing as a shortcut to meet financial covenants or maintain creditworthiness, thereby increasing transaction complexity and audit risk. This divergence underscores the critical importance of distinguishing between different forms of patient capital in corporate governance research.

Furthermore, this study breaks new ground by identifying Type II agency costs as a pivotal mediating channel. Moving beyond the conventional focus on Type I agency problems (Eliwa et al., 2023), we demonstrate that greenwashing serves as a veil for controlling shareholders’ expropriation activities (tunneling) and weakens internal controls. This exacerbates conflicts between controlling and minority shareholders, leading to higher Type II agency costs. The ensuing degradation in financial information quality and the obfuscation of related-party transactions force auditors to expend additional effort to assess the risk of material misstatement, thereby indirectly elevating audit risk. This mediation pathway enriches the theoretical framework for understanding greenwashing’s repercussions by incorporating a principal-principal conflict perspective.

In summary, this research bridges several critical gaps in the extant literature. It moves beyond theoretical deduction to provide large-scale empirical evidence, differentiates the moderating effects of patient capital, and introduces a novel mediation mechanism rooted in Type II agency conflicts. These contributions not only advance the academic understanding of greenwashing’s audit implications but also offer actionable insights for auditors, regulators, and firms aiming to enhance governance and risk management practices in the context of sustainable development.

Conclusion

This study reveals the positive effect of corporate greenwashing on audit risk through empirical analysis; it also innovatively introduces the moderating effect of patient capital and the mediating mechanism of Type II agency costs to deeply explore the complex relationship between greenwashing and audit risk. We drew the following conclusions.

First, corporate greenwashing behavior is driven by reference dependence and loss aversion psychology, significantly increasing audit risk. Firms tend to adopt policy standards or industry averages as reference points for environmental performance, engaging in myopic opportunistic behaviors to avoid reputational or financial losses associated with failing to meet environmental criteria. This exacerbates information asymmetry and undermines the reliability of financial statements. Such behavior not only challenges auditors’ ability to identify the authenticity of information but also threatens the credibility of ESG reports, thereby affecting investors’ sustainable financial decision-making based on environmental information. Second, stable equity structures mitigate managerial present bias, encouraging firms to focus on long-term sustainability, thus reducing the negative impact of greenwashing on audit risk. In contrast, relational debt intensifies short-term performance pressures, prompting firms to engage in greenwashing to embellish financial performance, indirectly escalating audit risk. This finding provides empirical support for policy formulation regarding capital structure optimization and green governance in sustainable finance. Third, at the auditor level, the “Big Four” accounting firms, with their professional expertise and rigorous audit procedures, are more effective in identifying corporate impression management strategies, reducing cognitive biases in information verification. As a result, they mitigate the impact of greenwashing on audit risk. This underscores the importance of enhancing attestation capabilities in ESG audits and provides reference for international investors when selecting audit institutions. Fourth, at the auditee level, high-tech firms leverage technological complexity to engage in greenwashing. Auditors may underestimate the authenticity of their environmental data through impression management mechanisms, masking short-term risks. In the long run, intensified principal-agent conflicts in these firms may lead to governance failure and a concentrated outbreak of audit risk, posing a potential threat to the stability of ESG rating systems. Fifth, further research reveals that greenwashing exacerbates agency conflicts between controlling shareholders and minority shareholders through rationalization mechanisms. Controlling shareholders, in pursuit of private benefits of control, may weaken internal monitoring mechanisms, further intensifying financial information distortion risks. Ultimately, this increases audit risk indirectly through Type-II agency costs, highlighting the importance of equity structure reform and the improvement of supervision mechanisms in ESG governance.

Suggestions

Based on the above conclusions, to effectively reduce the negative impact of greenwashing on audit risk and improve the quality of corporate disclosure and the effectiveness of auditing, we make the following suggestions: (1) Audit institutions need to construct a professional governance system, develop greenwashing behavior identification models through technological iteration, optimize greenwashing behavior audit procedures and risk assessment frameworks, guard against audit misleading caused by “impression management,” and strengthen the professional competence of auditors in fields such as environmental accounting and social responsibility. The “Big Four” accounting firms, relying on their rigorous audit procedures and experience advantages, promote the standardization of ESG audits and provide replicable audit frameworks for the industry. Small and medium-sized accounting firms can share technical resources through industry collaboration mechanisms and establish a collaborative audit quality improvement model. (2) Audited entities should optimize their capital structure to reduce greenwashing motives. They should improve internal supervision mechanisms, strengthen the supervisory functions of independent directors and audit committees in ESG information disclosure, and prevent agency conflicts. Additionally, they should enhance information transparency, strengthen stakeholder trust, and promote management’s long-term strategic awareness to fundamentally control the incentives for greenwashing behavior. (3) Regulatory authorities need to establish hierarchical identification standards and quantitative penalty systems for greenwashing behavior, promote the connection between auditing standards and ESG governance, strengthen supervision and guidance over audit institutions, and establish an associated regulatory mechanism between equity structure and ESG risks. They should also promote industry collaborative supervision and information sharing, and construct a dynamic monitoring system for audit quality to provide institutional guarantees for the quality of environmental information disclosure in the capital market.

Limitations

We mitigated the endogeneity problem through robustness testing and employed a three-step regression with a Sobel test to verify the mediation path; this enhanced the reliability of the conclusions. However, this study had some limitations. First, for the measure of greenwashing behavior, we relied on textual differences between publicity and performance, which may have led us to ignore hidden forms of greenwashing. Second, for the sample, we only studied Chinese A-share listed companies, and the external validity of the conclusions needs to be carefully generalized. Third, the endogeneity problem has been partially dealt with, but the instrumental variable method has not been introduced to completely exclude bi-directional causal interferences. Overall, this study provides a theoretical basis for optimizing capital structure, strengthening internal governance, and improving regulatory policies through a multidimensional mechanism and heterogeneity tests.

Future research could be deepened along two potential directions. First, it is recommended to expand cross-national comparative studies to explore the heterogeneous manifestations of greenwashing behaviors under varying national institutional environments, ESG regulatory intensities, and levels of capital market maturity, as well as their impact mechanisms on audit risk. Such research would provide theoretical support for the harmonization of global sustainable finance standards. Second, longitudinal tracking studies are suggested to analyze the evolutionary trends of greenwashing behaviors across different stages of the corporate life cycle and their dynamic relationships with corporate governance structures and capital allocation efficiency. This line of inquiry would further uncover the profound implications of greenwashing within ESG reporting frameworks for long-term firm value and the mechanisms of market trust.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.