Abstract

Result disclosure of clinical trial posts a conflicting logic between private secrecy and public interest. Despite ethical and legal requirements for disclosing clinical trial results, clinical trials’ sponsors tend to withhold the results. We explored the location, timing, and rationale behind the withheld clinical trial results. Based on the entrepreneurial orientation (EO) perspective, we propose that organizational EO contingencies moderate the disclosure decision. We used the completed clinical trial projects in China by foreign and domestic sponsors. First, we found that a unit increase in the sponsor’s experience can increase the disclosure about 1.01 times. Second, we found that industrial enterprises disclose results about 3.7 times more than universities do. Third, we found that foreign clinical trial projects in China tend to disclose 3.9 times more than domestic projects. We link these findings to two types of audience. First, we inform the academic community on the theory and empirics regarding risk-taking behavior in the biopharmaceutical industry’s clinical trial activity. Second, we address the general audiences concerned about the ethical and socioeconomic wellbeing of the public.

Introduction

The disclosure of clinical trial results is critical for industrial and social development, but it raises its risk because it compromises its secrecy that conducts research and development (R&D) with high costs. Upon disclosure, its competitors learn, without investment, about the success or failure of the discoveries. Ethical standards and new regulations require the full disclosure of the clinical trial results for the public good, regardless of the positive or negative results of the R&D project. In the past, the ethical standards did not persuade firms to disclose clinical trial results, and now the newly introduced law has made only incremental progress. Despite the legal obligations, project sponsors deflect such pressure and do not disclose their findings to keep their findings secret from national and international competitors (Piller, 2020). For instance, industrial firms (pharmaceuticals) and universities keep their findings secret in more than 60% of the cases, increasing social costs and constraining public money development.

The secrecy of vaccine-related results can have social, economic, and moral costs in pandemics, such as in the recent coronavirus crisis. To understand when and why clinical trial sponsors hide their findings, we need to understand when and why disclosure occurs. Although a minority of studies by firms and universities provide their results, a comparative analysis of their motives and contingencies can improve our understanding. This article addresses this issue of disclosure and proposes a model to predict why some organizations risk disclosing their results compared with others. Using the entrepreneurial orientation (EO) perspective (D. Miller, 1983), which builds on the assumption of risk-taking behavior, we start with the baseline hypothesis that the project scope positively predicts the clinical trial results’ information disclosure. Firms with a broader project scope are more likely to disclose clinical trial results because of the opportunities and decreased risk from the broader scope.

Then, we turn to the main proposition that environmental contingencies (a firm’s project portfolio, industry, and foreignness) moderate this direct effect between the project scope and the resulting disclosure. The EO framework rests on the risk-taking assumption, and the resulting disclosure is a high-risk decision for the firm. In addition to risk-taking behavior, the EO framework points to innovativeness and proactiveness, and the resulting disclosure meets these assumptions in the context of a firm’s project portfolio, private versus public ownership and foreignness versus localness. Prior research shows that external contingencies such as the home country and China’s host location influence a firm’s decision on clinical trial projects (Malik, 2019b). When assessing these moderating hypotheses on the firm-specific contingencies, we can make a threefold contribution.

First, the clinical trial disclosure phenomenon has raised questions, but it has not explained the management and organizational literature. Second, the EO theory contends that firms vary their risk-taking behavior: the higher the risk-taking behavior of the firm is, the higher the firm’s EO may be. This study explicates this idea in the biopharmaceutical sector’s context by considering the disclosure of clinical trial results as a strategic decision. Third, this study addresses the policy issues for various stakeholders. The main stakeholders are the social and regulatory authorities on one side and the firm and industry on the other side. The public policy for science and technology bridges the link between the two sides.

Theoretical Framework

Clinical Trial Result Disclosure

The Helsinki Declaration (2013) draws on the ethical principles for global clinical trials with the following clause: “Every research study involving human subjects must be registered in a publicly accessible database before recruitment of the first subject” (World Medical Association, 2013). To extend this clause, the World Health Organization (WHO) states that the sponsor commits to following basic ethical principles, and one of these principles is transparency in method and results reporting. This reporting includes preserving the accuracy of the results and making both positive and negative results publicly available. The WHO notes that “a significant proportion of healthcare research remains unpublished and, even when it is published, some researchers do not make all of their results available.” It causes two harms. First, selective reporting increases technical bias because of incomplete results (https://www.who.int/ictrp/results/en/; accessed: June 5, 2020). Second, the withheld results comprise transparency, depriving society of progress in technology. Therefore, the disclosure principle applies to two stages.

The first stage requires disclosure at the entry level of a clinical trial project, dividing the project into exploratory or confirmatory purposes. Every project needs to clarify the purpose of the trial at the outset. The second principle requires disclosure at the exit level of a project, referring to the completed project and disclosing its results to the public. While firms find it easier to disclose their project’s purpose when they begin a clinical trial, they find it difficult to disclose the results due to many risk factors. Therefore, regulatory authors introduced the “Title VIII of the Food and Drug Administration Amendment Act” that became effective on January 18, 2017.

This legislation requires firms and universities to declare their results, both positive and negative. The regulation also introduced penalties for noncompliance. It began in the United States with “the trial transparency regulation,” and other developed countries have emulated it. However, differences exist across locations, within developed countries and between developed and developing countries. Confusion also persists between regulatory and ethical standards. In particular, the difference persists between the sponsors and locations of clinical trials. Universities and firms differ in their disclosure of results, and the same sponsor differs in their reporting behavior in different countries. Thus, one reason leads to firm-specific factors, and the other leads to environment-specific factors. For both factors, the EO and its moderation (contingencies) may explain when firms behave differently and why they do so.

EO View

EO theory suggests that firms differ in evaluating uncertainty, opportunities, and threats. A high EO predicts risk-taking behavior, suggesting that some enterprises take more risks than others because they see opportunities more than risks. Firm-specific contingencies predict a firm’s entrepreneurial decision (D. Miller, 1983). While prior research uses the EO perspective to assess a firm’s decision in a dynamic environment, it has applied these assumptions to its general risk-taking behavior. Based on this relevant framework, we build on the EO in the context of the moderating effects of a firm’s contingency. Because the EO is relevant to the international business context in risk-taking assumptions (D. Miller, 1986), the EO framework suits our argument that foreignness moderates risk-taking behavior, which implies that foreign sponsors differ from the domestic sponsors, the disclosure of the results because of their EO. In other words, the EO affects and reflects the context.

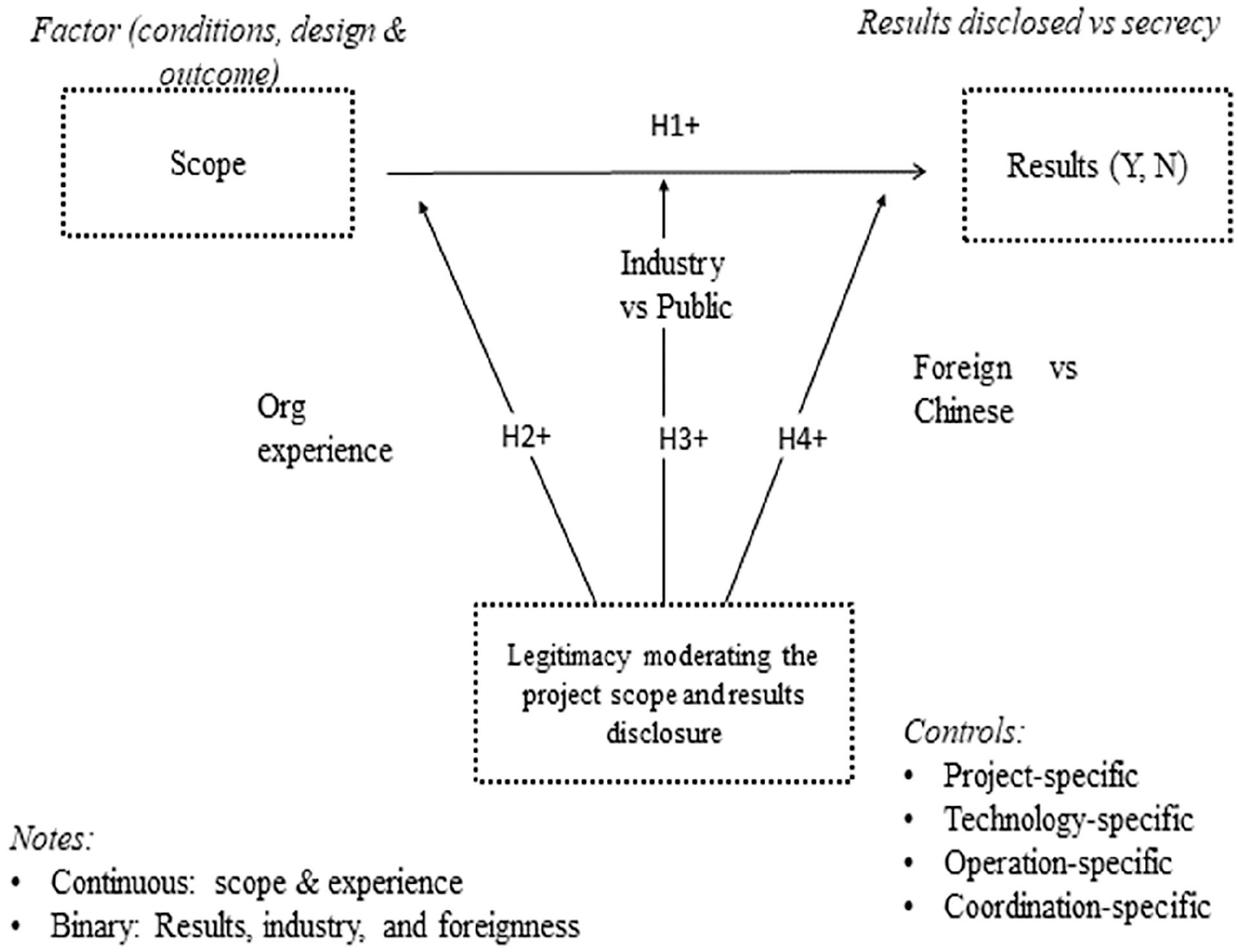

To start with EO’s baseline hypothesis, we propose that the project scope predicts the chances that the firm will disclose its findings to the public, which is a risk-taking behavior in the EO theory. Then, we propose three organizational contingencies as moderators in the decision to disclose results: (a) the firm’s project portfolio, (b) the industry, and (c) the foreignness versus localness. Figure 1 conceptualizes these moderating effects in the three contingencies between the project’s scope and the findings’ disclosure. Both the direct and indirect hypotheses depicted in the conceptual model reflect the EO theory’s original framework.

Conceptual model.

In explaining the EO framework, D. Miller (1983) highlights that the entrepreneurial firm (a) innovates rather than imitates, (b) takes any risk rather than avoiding it, and (c) engages in innovation related to new markets or technologies rather than exploiting existing ones (D. Miller, 1983). This foundational framework of the EO of the firm (risk-taking, proactiveness, and innovativeness) serves firms in an uncertain and dynamic environment, whereas the opposite (mechanistic strategies) serves firms in a stable environment (Covin & Slevin, 1989). For instance, high technology sectors are highly dynamic and increase the uncertainty for the firm in favor of risk-taking behavior across time and space. In contrast, low technology sector signals stable environments. The EO theory aligns with the dynamic environment, addressing risk-taking behavior in research and practice.

The research based on EO theory has diffused across contexts and levels on these issues due to its flexible application (Malik, 2019a). The proponents of this idea behind EO theory suggest that the “EO exists apart from its measures and that researchers are free to choose whichever measurement approach best serves their research purposes, recognising that unidimensional versus multidimensional EO measurement models are consistent with fundamentally different conceptualisations of the EO construct” (Covin & Wales, 2012). This flexibility allowed the diffusion of the EO literature across fields, and it allows us to explore a firm’s decision to disclose clinical trial results with the moderation of the contingencies. In short, a clinical trial project is a risky venture at the entry level, it is a risky venture at the disclosure level, and it is a risky venture at the foreign location level. We follow the conceptual depiction in Figure 1 and start with the baseline hypothesis based on the project scope.

Project scope and the disclosure of results

In the baseline argument, we propose that a firm’s project scope influences its decision to disclose clinical trial results in the EO theory for two reasons. First, the EO predicts a broader scope, and the broader scope involves higher project costs and risks (Malik, 2019b; Malik & Yun, 2016). In this sense, the EO predicts the scope. Second, the EO predicts that the broader scope predicts the risk-taking behavior of disclosing the results at the exit (completion) stage because it extends opportunities to pick and choose. In the first part of this claim, the project scope depicts high risk, innovativeness, and proactiveness. With the change in the scope, as many studies have shown, the risk and reward perspectives change (March, 1994). A narrow scope for a clinical trial project increases operational efficiencies (Huckman & Zinner, 2008), and broad scope for a clinical trial project increases the EO to meet the challenges of the uncertain and dynamic environment. The firm seeking a broad scope increases its learning capabilities and improves its potential for new product development in the biopharmaceutical sector (Garnier, 2008). Meanwhile, the project scope meets the conditions outlined in the EO, such as uncertainty, costs, and future-oriented behavior in national and international contexts (Malik et al., 2020), and it also cascades into the second part of the claim that the R&D project scope predicts the disclosure of the results.

In the second part of the claim that a firm’s EO influences its risk-taking behavior at the exit point in the project, the R&D project scope (clinical trial) predicts an increase in the disclosure patterns of test results. The project scope may signal many things to different readers. We highlight some basic aspects of a clinical trial (R&D) project scope. First, a project scope includes goals such as the problems it targets, the routines it needs to reach those targets, and the reports observed at the end. In principle, each additional task in an R&D project scope increases its breadth, complexity, and uncertainty, increasing the need for resources, effort, and time. For instance, marginal management input, financial resources, information processing, and coordination direct the attention from alternative paths to the focal scope (March, 1994; Ocasio, 2011). Hence, the attention to the scope of the focal project reduces the attention from other projects.

The above-defined project scope predicts the disclosure of the results for several reasons. First, the broader project scope increases the absorptive capacity of the sponsor of the clinical trial (W. M. Cohen & Levinthal, 1990). A firm’s capability posits that the organizational learnt behavior predicts the risky decision, and information disclosure is a risky strategy that prevents firms from disclosing their critical results (Piller, 2020). For instance, the absorptive capacity factor increases a firm confidence in the rewards in an uncertain environment, decreasing the risk evaluation (March, 1994). Second, a broader scope predicts the disclosure of clinical trial results for two reasons. First, the disclosure of the scope increases the project’s legitimacy (Suchman, 1995). For instance, a project that addresses multiple diseases expands the scope of the potential audience. As a result, high legitimacy increases both the confidence and the flow of resources to the project. Second, the project scope increases the choice for the sponsor to pick and choose. Based on the absorptive capacity of the project scope, we state the following baseline hypothesis.

Environmental contingencies

The next step in the framework in Figure 1 depicts that environmental contingencies moderate the link between the project scope and the results’ disclosure. An environmental contingency refers to an external context that may extend to any context. Our focus is on three firms-specific contingencies aligned with EO theory. The first one deals with a firm’s project portfolio, which implies an increase in a firm’s project portfolio alters the relationship between the scope and the disclosure. The second contingency deals with a firm’s ownership or orientation, which implies that industry-sponsored projects behave differently than university-sponsored projects. Because of this orientation, the relationship between the scope and the disclosure varies between private and public ownership. The third contingency deals with the foreignness of the sponsor of the R&D project, which posits that foreign and domestic enterprises interpret their effects of the situation differently. Foreign firms carry their home countries’ norms and regulations while adapting to the host market’s local situation. These three moderators influence the relationship between the clinical trial project scope and the EO framework disclosure.

The EO explains this moderation with several mechanisms to support the idea that environmental contingencies are responsible for a firm’s mixed decision and outcomes (Malik, 2011). First, the environment changes the resource endowment of an organization in the EO, and the access to these resources and information shape the level of EO decisions, increasing it or decreasing it (Becherer & Maurer, 1997; Covin & Wales, 2012). For instance, the environment’s financial resource flow is one mechanism, and the technological resource flow from the environment is another mechanism linking the EO to the scope and the disclosure decision. Second, a firm’s absorptive capacity differs across environments (Dougherty & Heller, 1994), especially in the biopharmaceutical sector (Trullen & Stevenson, 2006). Third, the environmental conditions influence the internal decision regarding the strategic scope and outcome (Rao et al., 2008). Together, EO theory in the framework in Figure 1 proposes that the environmental contingencies increase the potential for explaining why some firms decide one way or the other in their information disclosure strategies. Now we turn to the moderating hypotheses, starting with the project portfolio experience of a firm.

Project Portfolio Contingency

The firm’s experience moderates the effects of the scope of a clinical trial project on the disclosure of clinical trial results. The firm’s experience refers to the portfolio of completed projects before the focal disclosure. The EO framework posits that firms risk disclosure when they are confident based on their capabilities. A firm’s capability suggests that the absorptive capacity theory supports the EO framework. In support of this, the link between the EO and absorptive capacity shows a positive correlation, suggesting that a firm’s absorptive capacity moderates the EO (Engelen et al., 2014). A portfolio of clinical trial projects meets the absorptive capacity-based learning and EO theory conditions in several ways.

First, a portfolio of completed projects reflects a firm’s size, suggesting that larger firms tend to have more clinical trial projects in their portfolios. Likewise, large firms tend to have broader absorptive capacities (W. M. Cohen & Levinthal, 1990). Second, the portfolio of a firm’s R&D project reflects its learning by doing activities related to its absorptive capacity regardless of its size. The field-specific factors influence the risk and innovative projects, and these firms-specific factors predict the link between the EO and the outcome (Presutti & Odorici, 2019). Third, the project-specific absorptive capacity affects risk-taking behavior in other sectors, such as railways (Desai, 2008). Finally, the project portfolio increases the absorptive capacity, moderating the interfirm collaborative decisions in risky ventures. Because the project portfolio drives the firm’s EO toward risk-taking behavior, we propose the project portfolio’s moderating effects between the project scope (baseline hypothesis) and the disclosure of clinical trial results.

Organizational Orientation and the Disclosure of Clinical Trial Results

The organizational orientation moderates the clinical trial disclosure decision because of the differences in the ownership structure and enterprises’ types of clinical trial projects. The project’s ownership refers to the project’s financing, and it includes privately and publicly funded projects as the two main categories. Industrial firms draw on private funds, and universities draw on public funds. Likewise, the organizational type differs in the context of clinical trial development. Conventionally, pharmaceutical firms exploit a product through testing, and universities engage in exploring new knowledge. In recent decades, pharmaceutical firms have entered the university terrain, and universities have entered the clinical trial field. In other words, the organizational orientation and ownership differ within the same field of clinical trials. The organizational field refers to the buyers, suppliers, competitors, and regulators (DiMaggio & Powell, 1983).

Likewise, the overall strategy of clinical trials differs between pharmaceutical firms and universities. Goldacre (2012) makes two claims that pharmaceutical firms place in separate boxes because of their orientation compared with other organizations. First, the author shows that pharmaceutical companies spend approximately 24.4% of their sales revenues on marketing and promotion, and they spend 13.4% of their sales revenues on research and discovery. Second, the author claims that when pharmaceutical firms disclose their internal clinical trials, they report positive results more than negative results. Anecdotes indicate that firms often conduct seven clinical trials; they chose to report two of them that produce positive results, and “this behaviour is commonplace” (Goldacre, 2012, p. xiii). Therefore, the logical motives, conditions, and behavioral differences make sense as moderating contingencies.

Foreignness and the Disclosure of Results

The foreignness versus localness of the project sponsor is another firm-specific moderator that influences the EO and its decision to disclose clinical trial results. International business research has long recognized the differences in a firm’s behavior between its home and host markets. Compared with its home market, a firm faces the liability of foreignness in its host market (Hymer, 1972). Evidence from the banking industry shows foreignness’s liability in host markets (S. R. Miller & Parkhe, 2002). In the software industry, a qualitative study shows that foreignness liability exists and persists over time compared with the argument that the liability of foreignness decreases over time in China (Malik et al., 2021). Considering this evidence, we concur with the literature that foreignness moderates a firm’s entrepreneurial behavior in the same way that cultural differences moderate a firm’s EO (Richard et al., 2017). Oxford University’s tracker on the disclosure of results supports the difference in firms’ behavior between home countries in Europe/America and China in the context of the clinical trials and the disclosure of results patterns between foreign and domestic sponsors. Appendix A shows that, on average, the disclosure of results by the sponsor occurs 1.97 times more frequently in Europe/America than in China. Based on the literature and descriptive support, we propose the following moderating hypothesis.

Method

Research setting: The pharmaceutical sector, the value chain in the new product development, and the clinical trial projects define the research setting of this study. Because of the best fit between the research question, theory, and evidence, we chose the biopharmaceutical sector, and within it, we focus on the clinical trials located in China. The pharmaceutical sector differs from other sectors in the value chain in the duration, streams, costs, and uncertainty of its projects. A typical clinical trial can take 15 years from the start to the end of the commercial product. Unlike the conventional upstream and downstream division of labor, the value chain’s clinical trial segment adds the midstream as a special case. Likewise, a clinical trial project’s cost, which can reach a billion dollars, may exceed a billion-dollar firm’s market value.

Another character of the pharmaceutical sector is the structure of the industry actors in the clinical trial activity. Unlike other sectors, where similar organizations from the same industry engage in a competitive activity, clinical trial activities attract industrial firms and universities. This distinction between university- versus industry-sponsored projects becomes distinctive between foreign and Chinese enterprises. Foreign firms conduct more clinical trial projects than foreign universities in China, and domestic Chinese universities conduct more clinical trials than domestic industrial firms (Malik, 2019b). Together, the research setting of a clinical trial project and a firm contingency support the research context’s choice to assess the results’ disclosure.

Sampling: Once we determined China’s research setting in the biopharmaceutical sector, we turn to the sampling process with three stages. First, starting with clinical trials as the unit of analysis, we retrieved all clinical trials in China. The National Institute of Health (NIH) database stores the records of clinical trials and their location. The NIH maintains the database for two reasons. One reason is that the regulatory authority requires clinical trials to be registered at the entry stage with the declared purpose: exploratory versus confirmatory. Because some confirmatory studies may find some discoveries, the regulatory authorities prevent this afterthought shift from a confirmatory purpose to an exploratory purpose. Moreover, clinical trials are stored in the NIH database to conform to the Food and Drug Administration (FDA)’s protocol approval process. Global clinical trials must follow these protocols for clinical trials for commercial purposes after a successful outcome.

Second, the sample consists of all completed projects, which differ from active projects. Comparing completed projects and active projects, the former group meets our sampling purpose requirements to answer the research questions. Moreover, completed projects offer a reliable comparison between the disclosed versus undisclosed results because the starts and ends are clear. Because the sample includes all completed projects, we refer it to the completed projects’ population by the end of 2019. Except for three clinical projects with unreliable information, which we excluded from the sample, the final number of observations reached 5,231 completed projects for the analysis. Then, we began coding for our purposes.

Coding: Following the framework in Figure 1, we began coding the clinical trial projects in an Excel sheet, and we followed several steps to do so. First, we coded the scope of the clinical trial project, which includes multiple medical conditions. It refers to the targets in the R&D project for new product development. For instance, a discovery to solve multiple medical conditions increases those conditions compared with a single condition (Malik, 2019b). On average, a clinical trial tends to have more than one targeted condition in its scope of activities (Higashi et al., 2007). Then, we coded the tasks in clinical trial projects. Finally, we counted the preidentified output observations included in the project’s report at its completion. In a clinical trial activity, every project provides information about these three components of the project scope. Together, the conditions, tasks, and output observation protocols prepared the input for the composite variable for the scope of the project, which we define below.

Second, we linked the clinical trial projects to the project sponsors at the organizational and national levels. At the organizational level, we differentiated universities from industrial firms. At the national level, we coded the nationalities of the projects based on their sponsors. Appendix B shows the nationalities of foreign projects in China. After knowing the organization and its nationality, we could find other related information at this stage. Third, we coded the contingency factors based on the organizational identity. The organizational experience used to measure a firm’s absorptive capacity is the next step in the coding. This sponsor’s experience best suits the assessment of a firm’s experience in its current location. For instance, we traced the completed projects of GlaxoSmithKline in China throughout its history in the country, and the count of those project forms the experience variable.

Fourth, at this stage, we were able to trace the two types of coordination mechanisms: with or without partners. The governance literature refers to them as internalized versus alliance modes (Teece, 1985). In the case of internalized projects, the sponsors decided to go “solo” on the clinical trial projects, and the activities remained within the firms’ boundaries. In China, foreign firms created their subsidiaries, such as research centers or other similar facilities. In collaborative projects, foreign firms collaborated with other foreign firms and Chinese partners to develop clinical trials. The database clarifies the sponsor’s self-reported entries about the main sponsor, the lead sponsor, and collaborators.

Finally, we attended additional factors to use them as controlled conditions, which divide the relevant information into two groups. The first group included the durations of the completed projects to assess the efficiency of the projects. Each project recorded how many weeks it took to complete. The second group included a list of technologies as categorical values. Because technologies differ in their quality and frequency, we coded them as dummies to use them as the controlled conditions. For instance, anxiety/depression, viruses/vaccines, diabetes, and cancer, among others, differ in their quality and frequency, requiring different protocols, conditions, and processes. These coding protocols and procedures led to the variables’ development.

Variables

Dependent variable

The dependent variable is a binary variable that follows the baseline research question:

The completed project has the status: yes or no. We assigned 1 to the disclosed results (yes) and 0 to withhold results (no). This decision rests in 1-year window since the completed project.

Independent variables

Following the main hypotheses, one baseline hypothesis and three moderating hypotheses, we developed four independent variables. The first variable represents the scope, and it is composed of three input variables. We used factor analysis to define the scope variable as the baseline variable. This factorized variable is continuous, and it supports the baseline hypothesis regarding whether the project’s scope predicts the firm’s disclosure versus nondisclosure decision.

The second independent variable represents a firm’s experience and is measured as the completed projects’ count at the location. This portfolio of completed clinical trial projects of a firm represents its absorptive capacity, and the count variable is transformable into a continuous variable.

The third independent variable represents a firm’s orientation (ownership) and is divided into private and public organizations. We coded a private firm as 1 and a public organization (e.g., university) as 0. Because firms and universities differ in their decision logic—commercial versus social—we categorized it as a binary moderator.

The fourth independent variable has two categories: foreign versus domestic sponsors. Like the previous variable, it is also a binary variable and is the foreignness versus a firm’s localness. We coded the variable as 1 for foreign sponsors and 0 for domestic (Chinese enterprises). Together, these three variables (2–4) interact with the baseline variable (1), and these interactions form the following three moderators.

(Project scope)(project portfolio as experience)

(Project scope)(industry difference as private vs. public)

(Project scope)(the foreignness as foreign vs. Chinese)

Control variables

Technologies (a set of dummies)

Phases (multiple dummies)

Efficiencies (duration of completed projects in weeks)

Gender (binary)

Age (child vs. adult, binary)

Enrolment (number of volunteers used in the project)

Alliance versus internalized

Analysis and Model

Because of the categorical variable, disclosure (yes or no), we used logistic regression, a nonparametric model (J. Cohen et al., 2002). We performed a logistic regression to obtain the odds ratios for comparison based on the binary dependent variable, coded as 1 for disclosure and 0 for nondisclosure. As a nonparametric model, the largest model predicts the main category’s likelihood compared with the failure category. The formal specification of the logit model uses the maximum likelihood estimation (MLE) method as follows:

where

Thus, the probability of the outcome is the function of the odds

Results

Table 1 shows the summary statistics, where we focus on the dependent and main variables. About 19% of the completed projects have opted to disclose their results, and 81% of the projects have opted for secrecy. This disclosure is far lower than in Europe and North America. Furthermore, Chinese projects make up only 4% of the disclosures, leaving 15% for foreign projects. In addition to the dependent variable, the first independent variable shows a mean of 0 because it is a factorized variable (composite of three measures). The third variable shows a firm’s experience based on its number of completed projects, and on average, a firm has completed 64 projects.

Summary Statistics.

Regarding the ownership measures, the industry comprises 35% of the projects. Especially in China, publicly funded projects (universities) inflate this distribution. Finally, foreign projects comprise 40% of the sample.

Table 2 shows the intervariable correlations. The correlations appear to be less than 50%, except in the foreign and industry matrix (62%). High autocorrelations raise multicollinearity issues; therefore, we performed additional diagnostics in the next table.

Intervariable Correlations.

p < .05.

Table 3 shows the variance inflation factor (VIF) values. Conventionally, VIF less than 10 meets the social sciences threshold (J. Cohen et al., 2002). The concern rises when the VIF exceeds this convention. According to the table, the highest VIF value is less than 3, and the average VIF is even smaller. With this analysis’s support, we move to the next stage in the analysis.

VIF (Multicollinearity Analysis; N = 5,231).

Note. VIF = variance inflation factor.

Third, we performed multiple interaction term analysis and estimated the marginal values plotted in Figures 2 through 5. Figure 2 shows the interaction graph between the scope as the baseline variable and a firm’s experience. It shows the fluctuation in the two continuous variables’ projects, and the variable gaps between the two curves signal the interaction between the two concepts.

Scope and project portfolio interaction effect.

Scope and industry interaction effect.

Scope and foreignness interaction effect.

Specificity analysis (area under ROC curve).

Figure 3 shows the graph of the interaction between the scope and organizational experience. This interaction between a binary and a continuous variable shows the curve steepness at two points, suggesting support for the interaction effect.

Figure 4 shows the interaction graph between the scope of a clinical trial project and foreignness—an interaction between a continuous and a binary variable. Like the previous graphs, this interaction signals the existence of interactions between the two variables.

Table 4 shows the direct effects of the main predictors of the disclosure of clinical trial results. Regarding the direct effects, both the main predictors (scope) and organizational moderators (contingencies) predict the disclosure of the R&D results of a firm versus secrecy as the default.

Logistic Regression (Direct Effects).

Note. N = 5,206 (dependent variable = results disclosed; yes or no); odd ratios. The standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Hypothesis 1 (baseline) predicted that the R&D project’s scope positively correlates with the disclosure of clinical trial results. The result shows that an increase in one factor of the scope of the project tends to increase disclosure of results about 4.2 times (p < .001) more disclosures than the opposite. A firm’s experience based on earlier completed projects increases disclosures by a small margin among the contingency variables. Likewise, an industrial firm tends to disclose its results approximately 3.7 times (p < .001) more often than universities and other public organizations. This result is a surprise. Finally, foreign enterprises disclose their findings from R&D projects to the public approximately 2.2 times (p < .001) more often than their Chinese counterparts. With these direct effects considered, we turn to the moderating effects in the next table.

Table 5 shows the moderating effects of the contingency variables on the relationship between the scope and the results’ disclosure. In a stepwise analysis, after entering all the control variables used in the earlier table’s direct effects, we proceed to the moderating hypothesis testing.

Logistic Regression (Moderating Effects; N = 5,206.).

Note. The standard errors are in parentheses.

p < .01.

Hypothesis 2 predicted that organizational experience moderates the effects of the scope on the disclosure of results. The interaction effect shows an increase in the odds (p < .001). This result supports the hypothesis, and it reveals a positive moderation.

Hypothesis 3 predicted that ownership (a firm vs. a university) moderates the scope’s effects on disclosing the results The interaction effect (p < .001) shows a 3.7 times higher disclosure rate, which is higher than that of the direct effects.

Hypothesis 4 predicted that the contingency of foreignness moderates the effects of the scope on disclosing the results. There is a 3.87 (p < .001) times increase in the direct effects, suggesting support for the moderating hypotheses.

Finally, we assessed the goodness-of-fit of the model. The receiver operating characteristic (ROC) curve, which graphs the performance, shows that 86% are correct classifications.

Discussion

Legal and ethical communities have long stressed the need to disclose clinical trials for transparency, efficiency, and social wellbeing. The advent of COVID-19 has magnified the importance of the result disclosure from clinical trials. Yet, little is known whether and why clinical trial’s sponsor decides to disclose or withhold such results. In addressing this issue, we explored whether the sponsor’s contextual factors influence these decisions. In so doing, we explored the firm’s experience, the firm’s ownership (private-public), and the firm’s foreignness-localness. These three contextual factors influence EO: the risk-taking behavior of the disclosure of the result. The literature on EO contends that risk-taking behavior reflects the firm’s strategic intention.

Kreiser et al. (2002) explored EO’s environmental contingencies (innovation, risk-taking, and proactiveness), and they discovered that “environmental conditions play a significant role in the strategic decision-making process” across countries. They found that environmental hostility negatively correlates with innovation, and hostility induces risk-taking behavior between the two extremes—low versus high. These findings provide the environmental conditions for risk-taking in clinical trial result disclosure. Our findings show that the three contingencies (experience, ownership, and foreignness) moderate the decision to disclose clinical trial results. For instance, Joardar and Wu (2017) report that a firm’s foreignness changes its performance. In the biotechnology sector, a Chinese biotechnology discovery from Peking University faced hostilities in the United States (Malik, 2013).

In a general context, our findings support the earlier research on EO and risk-taking decisions. For instance, management research addresses information disclosure and transparency related to accounting performance (Brammer & Pavelin, 2004). Transparency increases the integrity of the firm and its technology; secrecy breeds doubts, opacity, and corruption. In the context of clinical trial results, the firms prefer to withhold results for strategic values; the society prefers to disclose it for the publicly funded research. The patterns of disclosure vary within countries and between countries during the internationalization process and its outcome. The internationalization of clinical trials has addressed some of the issues (Malik, 2020). Likewise, foreign clinical trials in China have captured some of these patterns (Malik & Yun, 2016). These previous studies allude to the different contingencies on EO. Our current focus exposed three such contingencies related to clinical trials in China.

In short, we find support for the variation in the clinical trial result disclosure in China in three contingencies. First, the sponsor’s experience, contingency predicts a positive moderation between clinical trial scope and the disclosure of results by the factor of 1.01. Second, firms tend to disclose about 3.72 times more than universities, although we expected the opposite. It confirms that university-industry difference moderates the scope-disclosure relationship. Third, foreign clinical trial sponsors tend to disclose results about 3.87 times from the increased scope. In other words, foreign-local sponsors moderate the scope of the clinical trial project and result disclosure. These findings contribute to the theoretical stream of EO theory. We visualize this interaction between the sponsor’s project scope and contingencies as a bricolage of the actor context. The context referred to the three contingencies, and the bricolage plays an integral role in the attention, evaluation, and decision about the clinical trial disclosure.

In addition to supporting the EO in the clinical trial’s result disclosure, we contribute a future research framework in similar or different contexts, for framework has relevance in high-technology industries, broad sector, and national and international institutions. We lend concepts, analytical tools, and contextual bricolage to other fields. Likewise, this study has social implication for various stakeholders—other than sponsors and academic experts. These social stakeholders include public institutions, regulatory authority, patients, and policymakers. Public institutions of federal governments invest in R&D; they deserve transparency of the outcome of the project. Regulatory authors need to approve public safety and efficiency through transparency; they need to make decisions based on result disclosure. Patients deserve to know transparent information on the drugs or technology they use. The policymakers need to allocate resources to cut cost and improve efficiencies of technological progress. Transparency saves the cost of the entire industry in the world. For instance, ineffective technology can save many others in the world to venture into the wrong projects. Besides these social implications, clinical trial results’ transparency had similar consequences with the transparency sought in other businesses (Brammer & Pavelin, 2004).

Conclusion

The disclosure of clinical trial project results has become ever more critical because secrecy harms lives and intellectual development and decelerates industrial progress. However, clinical trial sponsors prefer to keep the results of their projects secret for good reasons. The Helsinki Declaration, which came into being in 2017, proposed ethical arguments for disclosing clinical trial results, but it failed to produce the desired results. Likewise, only 20% to 35% of clinical trial project owners disclose their findings despite regulatory requirements. To deal with this tension between the normative requirement and strategic decisions, we combined two EO assumptions (D. Miller, 1983). First, the disclosure of results signals risk-taking behavior, and second, the contradictory logic creates threats and opportunities that vary with the firm-specific contingencies. The literature on EO accommodates flexible concepts and proxies in the analysis.

Despite these disclosure requirements (ethical and legal), clinical trial sponsors withhold results most of the time in most places. From this variation in spatial and temporal clinical trials and their result disclosures, the theory suggests that uncertainty plays a role in this transparency decision in two ways. One is behavioral uncertainty, and the other is technical uncertainty. Behavioral uncertainty deals with intention, and technological uncertainty deals with the capabilities of the sponsor. In the former case, the firm’s preference indicates behavioral issues against the regulatory pressure. For instance, the disclosure of clinical trial results raises the challenge for scientists who intend to publish their research. The sponsor might lack resources (time, space, and attention) to disclosure results in the latter case. Sponsors withhold results because of the complex administrative process rather than a motive (Piller, 2020). Thus, both types of uncertainties create a threat and opportunities in response to the environmental pressure in the theoretical setting.

We provided empirical answers in robust analysis. First, we refined the data on clinical trials located in China, and we focused on the 1-year window period for the disclosure analysis. Second, we used multiple models for comparison—with and without confounding variables. In so doing, we introduced input, output, and environmental variables. Third, we introduced the clinical trial project’s scope before invoking the moderating effect of environmental contingencies. The scope of the project sets a direct link between the complexity of the test and the decision for the disclosure. A broader scope creates opportunities for sponsors for commission or omission of studies. Fourth, we perform multiple tests for the fitness of the model and its reliability. Finally, we conformed to the conventions in the multicollinearity diagnostics and interaction plots in various figures. Hence, we believe we have applied relevant tools to improve the internal validity and external reliability.

Nevertheless, this study has its share of limitations. First, this study lacks global implications because the data are limited to China. Foreign clinical trials have spread all over the world. Second, this study analyzed secondary data, which lacks the richness of the contextualized processes. For instance, clinical trial managers and senior management’s views can reveal their intention to disclose or withhold clinical trial results. Third, the cross-section offers a snapshot of the phenomenon. A longitudinal study is preferred for theoretical strength. Fourth, this study used random effects, ignoring the fixed effects of the sponsor, national, and cultural levels. Fifth, the study compares university versus firms, but American universities differ from Chinese Universities. Therefore, we propose several research directions for future studies.

First, we suggest authors use primary data. Second, we recommend that authors include multiple countries and multilevel design. Third, we foresee differences in communicable infections (vaccines) versus genetic infections (such as cancer and diabetes). Separating those technologies in the disclosure decision can reveal insights. Finally, we allude to the clinical trials that far exceed in numbers than those listed in the NIH database. For instance, a fraction of clinical trials in China has entered the NIH database.

Footnotes

Appendix A

Patterns of the Disclosure of Clinical Trial Results of the Top Sponsors in the World.

| Sponsor name | % in Europe/America | % in China |

|---|---|---|

| Abbott | 95.9 | 57 |

| AbbVie | 98.9 | 57 |

| Actelion Pharmaceuticals | 100.0 | 83 |

| Alcon | 100.0 | 40 |

| Allergan | 93.8 | 71 |

| Amgen Inc | 96.6 | 86 |

| Astellas | 100.0 | 14 |

| AstraZeneca | 97.8 | 42 |

| Baxter | 93.3 | 0 |

| Bayer | 100.0 | 38 |

| Biogen | 96.4 | 0 |

| Boehringer Ingelheim | 100.0 | 82 |

| Bristol-Myers Squibb | 96.1 | 73 |

| Celgene | 91.9 | 71 |

| Daiichi Sankyo | 100.0 | 63 |

| Eisai Inc. | 97.1 | 44 |

| Eli Lilly | 97.8 | 74 |

| Genentech | 100.0 | 100 |

| Gilead Sciences Inc. | 98.7 | 67 |

| GlaxoSmithKline | 99.8 | 62 |

| H. Lundbeck A/S | 97.4 | 20 |

| Ipsen | 100.0 | 20 |

| Johnson & Johnson | 98.8 | 39 |

| Merck KGaA | 97.7 | 71 |

| Merck Sharp & Dohme (MSD) | 99.3 | 42 |

| Novartis | 99.6 | 58 |

| Novartis Vaccines | 100.0 | 58 |

| Novo Nordisk | 98.8 | 40 |

| Otsuka | 91.9 | 12 |

| Pfizer | 99.6 | 65 |

| Roche | 91.7 | 56 |

| Sanofi SA. | 98.8 | 25 |

| Shire | 100.0 | 0 |

| Solvay Pharmaceuticals | 44.4 | 0 |

| Takeda | 97.3 | 69 |

| Teva | 88.9 | 0 |

| Tibotec Pharmaceuticals | 100.0 | 100 |

| UCB pharma | 93.2 | 50 |

| Average | 96.1 | 49 |

Note. Projects in China: Foreign average: 36.4%; foreign average (excluding Hong Kong): 42%; domestic average: 6.4%.

Appendix B

Nationalities of R&D Project Sponsors.

| Country | No. of firms | No. of projects | Firms (%) | % |

|---|---|---|---|---|

| China | 599 | 3,115 | 67.8 | 59.63 |

| United States | 131 | 694 | 14.8 | 13.28 |

| Hong Kong | 24 | 312 | 2.7 | 5.97 |

| Switzerland | 8 | 247 | 0.9 | 4.73 |

| United Kingdom | 15 | 245 | 1.7 | 4.69 |

| Germany | 13 | 196 | 1.5 | 3.75 |

| Japan | 22 | 130 | 2.5 | 2.49 |

| France | 7 | 93 | 0.8 | 1.78 |

| Denmark | 4 | 53 | 0.5 | 1.01 |

| Belgium | 2 | 20 | 0.2 | 0.38 |

| Ireland | 2 | 17 | 0.2 | 0.33 |

| Sweden | 6 | 14 | 0.7 | 0.27 |

| Taiwan | 6 | 14 | 0.7 | 0.27 |

| Australia | 4 | 12 | 0.5 | 0.23 |

| Canada | 4 | 10 | 0.5 | 0.19 |

| Korea, South | 4 | 8 | 0.5 | 0.15 |

| The Netherlands | 3 | 7 | 0.3 | 0.13 |

| Singapore | 5 | 7 | 0.6 | 0.13 |

| Italy | 5 | 5 | 0.6 | 0.10 |

| Israel | 2 | 4 | 0.2 | 0.08 |

| Spain | 4 | 4 | 0.5 | 0.08 |

| Austria | 2 | 3 | 0.2 | 0.06 |

| Russia | 2 | 3 | 0.2 | 0.06 |

| Egypt | 1 | 2 | 0.1 | 0.04 |

| Finland | 2 | 2 | 0.2 | 0.04 |

| South Africa | 1 | 2 | 0.1 | 0.04 |

| Brazil | 1 | 1 | 0.1 | 0.02 |

| Hungary | 1 | 1 | 0.1 | 0.02 |

| India | 1 | 1 | 0.1 | 0.02 |

| New Zealand | 1 | 1 | 0.1 | 0.02 |

| Thailand | 1 | 1 | 0.1 | 0.02 |

Note. R&D = research and development.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.