Abstract

For policymakers across the world, the importance of budget transparency is self-evident. However, most scholars mainly focus on the economic performance of budget transparency while ignoring satisfaction of the public as the recipients of this policy. Therefore, this study examines the main factors of public satisfaction with the local government budget transparency based on the theory of customer satisfaction in the context of the Chinese budget transparency policy. Data for this study were collected through an online survey involving 235 participants. Structural equation modeling (SEM) was employed to examine the proposed model. The results indicate that the budget information quality, budget information acquisition method, and public engagement are good indicators of budget transparency perceived quality, which are positively related to public satisfaction. The government image also exerts a positive effect toward public satisfaction. Furthermore, public satisfaction is also positively related to public trust toward the local government, even though the hypotheses linking public expectation to public satisfaction, and to budget transparency perceived quality are statistically insignificant. The implications of promoting budget transparency and suggestions for future work are also included in this study.

Introduction

The rise of new pubic management (NPM), which advocates a change in the government’s role from a command-oriented authority to a service-oriented organization, has triggered a worldwide upsurge in academic research on the citizens’ satisfaction with the local government (Brodkin, 2011). Serving as the core component of NPM, the theory of customer satisfaction originated by Fornell (1992) provides a comprehensive explanation of satisfaction (Beeri et al., 2019). When used in the public sector, the customer satisfaction is commonly transferred as public satisfaction (Magoutas & Mentzas, 2010). Researchers like Van Ryzin et al. (2004) also claimed that the satisfaction and trust of citizens toward their local government were associated with a broad array of political activities for a long time. In simple terms, elected politicians and public officials form a potential contractual relationship with citizens. As trustees, the politicians and officials are responsible for keeping the state machinery functioning well, so that their behavior is conducive to realizing citizens’ interest and maintaining citizens’ satisfaction.

Studies focused on fiscal transparency support the view that greater fiscal transparency plays a positive role in promoting benign governance (Cicatiello et al., 2016). Paler’s (2013) research creatively showed that transparency and taxes reinforce the need for good governance. As taxpayers want a good price, they asked for more budget information to figure out what they have paid for public goods and services. Therefore, one way of ensuring the reasonable prices for these public goods and services paid by taxpayers is to disclose budget-related information, which is relevant to taxpayers’ interests. As a key public accountability mechanism, disclosing budget-related information may observably minimize the opportunism of policymakers, reduce the costs of governance resulting from information asymmetry, and increase citizens’ trust (Guillamón et al., 2011; Worthy, 2010). Budget transparency has now been incorporated into the practice of government budget reform as a tool of improving governance, and such budget practices will be beneficial in creating a stable political environment for sustainable economic development (Kosack & Fung, 2014).

The Chinese academic community has also responded to the worldwide wave of promoting service-oriented governments in recent years, conducting research on the satisfaction-oriented government performance evaluation mechanism. A series of initiatives such as “sunshine budget” and “sunshine finance” unveiled China’s efforts in improving fiscal policy-related transparency. From the perspective of implementation efforts, the new budget law which came into effect on January 1, 2015, for the first time put the financial information disclosure of Chinese government into law. Subsequently, in 2017, a report of the China’s 19th Communist Party Congress reiterated the importance of establishing “a comprehensively standardized, transparent, scientific and powerful budget system with strong constraints.” Such measures reflect China’s seriousness regarding the improvement of budget transparency.

The public’s take on these efforts cannot be ignored because public evaluation and management will serve as reference for the government budget-related reforms. Although literature on both government budget transparency and customer satisfaction has been burgeoning, there seems to be very limited research mapping the two. To this end, this study proposes a budget transparency public satisfaction index (BTPSI) model to examine the factors affecting public satisfaction with budget transparency in Chinese policy practice. The model is based on the theory of customer satisfaction and the characteristics of local government budget information (Sun & Andrews, 2020), while acknowledging the difference between public and private sectors. To ensure a good estimation result, this study introduces the partial least square-structural equation modeling (PLS-SEM) for empirical analysis.

The contents are laid out as follows: Section “Literature Review and Hypotheses Development” includes literature review and the proposed model. Section “Methodology and Measurement Items” illustrates the proposed methodology and data collection. Section “Data Analysis” elaborates the relevant indices analysis and results. Section “Discussion” discusses hypotheses testing. The conclusions, limitations, and scope for future research are summarized in the “Conclusion” section.

Literature Review and Hypotheses Development

Budget Transparency Overview

Previous research has established the role that transparency plays in the capital market, the more open and transparent the capital market is, the more orderly and healthier it will be (Healy & Palepu, 2001). Similarly, for the government budget management, budget transparency can be regarded as the best disinfectant. As budget transparency gained significance in the academic and practical sense, a volume of literature on government budget transparency has emerged ample results. The concept of budget transparency, originally proposed by Kopits and Craig (1998), has two aspects: (a) the manner in which all relevant financial information and systems are disclosed timely and comprehensively and (b) the convenience of citizens within a certain district in accessing budget information on the allocation of different kinds of expenditures as well as the collection of fiscal revenue.

Researchers elaborated the necessity of budget transparency from the perspectives of institutional theory (Carpenter & Feroz, 2001; Hoffman, 2001), rule-of-law principle (Bingham et al., 2005; Patten, 1992), citizens’ right to know (Alt & Lassen, 2006), principal–agent relationship (Benito & Bastida, 2010; Sun & Andrews, 2020), restraints of public power, and anti-corruption (Lane & Milesi, 2004; Reinikka & Svensson, 2004).

According to institutional theory, when responding to public demands, organizations adopt a structure or practice mode which is considered legal and socially acceptable. In this context, transparency is a symbol of legitimacy and social acceptance, as well as a tendency of the governments to respond to public demands. In particular, the allocation and use of financial budget funds are related to the national economy and people’s livelihood, and require a greater transparency in governments’ budget information.

Rule-of-law principle argues that in formulation of a public policy, transparent enforcement procedures and independent adjudicatory mechanisms, on one hand, greatly reduce the space for the abuse of government power. On the other hand, they also provide public with stable information access channels. In addition, a more transparent decision-making mechanism and a wider dissemination of information will, in turn, increase the legitimacy of government decisions. Therefore, in the framework of rule of law, promoting the transparency of local government budget information is of great benefit to fiscal and tax reform.

The theory of citizens’ right to know considers that government activities need public funds. Only by obtaining information about the government fiscal activities can citizens have a better understanding of the aim of the government fiscal policies as well as its possible consequences.

The principal–agent relationship emphasizes the effect of elections on the behavior of incumbents. As higher transparency reduces the information asymmetry between voters and candidates, this theory organically connects the building of service-oriented government with transparency and accountability in government affairs.

Previous literature showed that budget transparency helps strengthen government accountability and public trust through the efficient allocation of public funds as well as supply of public goods and services (Piotrowski & Van Ryzin, 2007). Evidently, budget transparency provides a solid guarantee that allows the public to effectively check whether the government power is being abused. From the perspective of regulating the behavior of officials, budget transparency has been implemented to curb corruption to a certain extent.

Previous scholars proposed meritorious points on the evaluation of budget transparency. Ingram (1984) considered financial condition as a determinant of government fiscal information transparency. This argument was later supported by different studies to validate that there exist a positive association between the financial condition and the government fiscal information transparency (Laswad et al., 2005; Manuel et al., 2013). Especially in the work of Manuel et al. (2013), a more significant positive relationship between the financial condition and central government fiscal information transparency is shown than that between the financial condition and local one. Except for financial condition, Ingram (1984) also mentioned political competition as one of the influential factors of government transparency, though previous literatures reported contradictory results over this factor due to the different measurements of political competition (Baber, 1983; Baber & Sen, 1984; Carpenter & Feroz, 2001; Ingram, 1984). For example, the effect of parliamentary political competition was considered positive according to Baber (1983), while the result was not significant when political competition was measured by lobby groups according to Baber and Sen (1984).

Some researchers also focused on what contributes to explain the level of government transparency through a comprehensive index model. Da Cruz et al. (2016) constructed a model including organizational information, financial transparency, taxation, relationship with citizens and public expenditure, and validated a correlation between the socioeconomic indicators of municipals and the transparency of fiscal information. Renzio and Masud (2011) used the open budget index (OBI) to evaluate the budget transparency of 94 regions, discovering that the budget transparency within a region is positively correlated to exogenous variables like the income and democracy levels. Similarly, in the work of Giroux and McLelland (2003), it is mentioned that high-income residents are more active to express their demand for fiscal information transparency to confirm the taxation paid are in effective usage. Accordingly, in cities with lower per capita income, the government authorities may not have a strong sense of fiscal information transparency due to lower demand of resident (Ho, 2002). Bearfield and Bowman (2016) also affirmed the role of residents’ demand. They developed a model to examine cities’ propensity for transparency by analyzing the quality and quantity of budget information which was presented by some municipalities on their own government websites. They argue that the demands of urban residents will force the development of informatization and intellectualization of government services. The empirical results will be a good reference in fostering fiscal transparency across both developed and developing countries.

This study uses these aforementioned research conclusions for the selection of research variables. However, rather than a graded assessment toward the budget transparency of the local government, the major concern in this study is public satisfaction with the local government budget transparency, wherein citizens play a central role.

Public Satisfaction With Budget Transparency

Government budget is a plan for the allocation and use of financial funds approved through legal procedures, which defines the scope and direction of government activities in that year, also, closely related to the national economy and people’s livelihood. New public management emphasizes that the government administrative power and behavior should be based on public satisfaction, making the public satisfaction become one of the keys to appraise government performance (Brodkin, 2011). In addition, in the process of promoting government budget reform, it has been found in some developed countries that the core of establishing a comprehensive government budget performance management system is to complete the quality assessment of government budget information management (Manuel et al., 2013). Therefore, as the stakeholder of budget information disclosure and also the supervisor of government work, when facing low-quality information dissemination including interruptions, errors, and fragmentations, the public will misunderstand and even antagonize the work of the government (Falco & Kleinhans, 2018). From this point of view, public satisfaction has an important role in evaluating the work of government budget disclosure.

The prevailing literature about public satisfaction is mostly derived from the theory of customer satisfaction (Fornell, 1992). The core of the theory is the customer satisfaction index (CSI), which covers several indicators like consumer expectations and complaints, the quality of products, and services to analyze public assessments to the overall purchasing experience (Zhong & Duan, 2018). The research of customer satisfaction is mature in the field of enterprise management, and some researchers have even proposed the applicability of this theory in the field of public administration (Lai & Pires, 2010; Magoutas & Mentzas, 2010). The government can be regarded as the supplier of the goods and services, while the public can be regarded as the customers to enjoy those goods and services. Based on this idea, some researchers further transformed the concept of customer satisfaction into public satisfaction. Public satisfaction is used to evaluate the quality of goods and services provided by the government, which conveys a thorough public view of regional and national services (Van Ryzin et al., 2004). Magoutas and Mentzas (2010) employed the public satisfaction with government transparency to evaluate the performance of e-government, and the quality of services provided by government, such as the efficiency of administrative staff also affects public satisfaction.

Satisfaction, however, is a perception within people’s inner realm, and it is fuzzy and uncertain. Thus, by taking such inner psychological traits as latent variables and external behaviors as observation indicators, this study explores such a psychological law from a quantitative perspective by means of structural equation modeling (SEM). As SEM allows the measurement errors of variables and has less requirements for data and relationship specifications (Akter et al., 2017), it has been widely applied to satisfaction-related issues, such as intentions of tourists (Loi et al., 2017) and assessments of customer loyalty (Kesari & Atulkar, 2016).

Previous literature carried out abundant discussions on the importance of budget transparency, but many only focuses on the macrolevel, relatively ignoring the attention and research on the public objects. Moreover, it is also a new starting point to carry out systematic and in-depth empirical research on public satisfaction theory from the perspective of promoting government information disclosure. The proposed model of BTPSI was shown in Figure 1. The proposed model was constructed based on CSI and designed questionnaires which are based on the previous literature and current situation of the domestic government’s information publicity. The following sections describe the variables in the model and the hypotheses.

The proposed BTPSI model.

Definitions of Latent Variables and Its Relationship With Literature

Budget transparency perceived quality and public satisfaction

Importance of service quality in various fields is self-evident. An enterprise can differentiate itself from other organizations with its own comparative advantages by providing excellent service quality. Good service quality benefits for profits generation and customers retaining at the same time (Buttle, 1996). Therefore, it becomes indispensable to study the measurements for improving service quality (Zeithaml et al., 2002). But researchers not only examined the measurement methods of service quality but also the possible consequences of heterogeneous service quality, such as customer satisfaction (Howat & Assaker, 2013). Thus, in this study, budget transparency perceived quality is set to reflect the general public perception of the quality of local government budget disclosure, and three quality factors are introduced such as budget information quality, budget information acquisition method, and public engagement.

Bock et al. (2012) assumed that people often develop feelings, that is, satisfaction or dissatisfaction, for a particular object through a subjective comparison process. Before making a purchase, a customer will have a psychological expectation of its possible benefits and utility. After the purchase, the customer develops an actual perception and automatically compares it to the previous expectation. When the perceived quality exceeds the expectation, the customer will be satisfied, if not, then the customer will be dissatisfied (R. E. Anderson, 1973). In this study, customer satisfaction is translated into public satisfaction, which is used to express a psychological state or feeling of the public after they have a certain understanding of government’s work. Based on the above analysis, this study first assumes that:

The diverse channels of information disclosure include television, radio, and newspapers. As the audiences’ characteristics vary in terms of gender, age, education, occupation, and political orientation, they tend to derive government budget information through different channels. The emergence of new communication methods like news websites, social networks, and instant messaging services on mobile phones have also provided technical support to the public in obtaining this information. Therefore, factors affecting the perceived quality of budget transparency should also include budget information acquisition methods, and based on this, this study assumes that:

Petter and McLean (2009) reaffirmed DeLone and McLean’s claim that information quality can be regarded as a characteristic of the output provided by an information system. It can be measured through five factors, namely, accuracy, timeliness, integrity, relevance, and consistency (Fisher & Kingma, 2001). Improving data quality is also a challenge for the local government because of its fiduciary duties (Falco & Kleinhans, 2018). China has gradually begun using networked information technology to publicize government budget information. Thus, the wider the scope of budget information disclosure, the more the attention needed on the quality of budget information disclosure. Low quality information hinders the information from meeting the public demand, thus threatening the public satisfaction with the budget information disclosed by the government and endangering the public political trust. This study argues that the public will be ensured to have a clearer understanding of budget transparency if they are provided with timely, complete, and reliable budget information, and based on this, this study assumes that:

Shugars and Beauchamp (2019) probed that the growing volume of political information which individuals derived from social media indicated people’s willingness to engage in long-term political discussions. Fewer constraints while expressing their political opinions or establishing good interactions with the government will make the citizens think that their rights to know and express are greatly satisfied, and based on this, this study assumes that:

Public trust

Trust is multidimensional and so there are different definitions of the same. For individuals, trust can refer to a person’s belief that the credibility of others can be determined by their perceived character regarding integrity, kindness, and ability (Akroush & Al-Debei, 2015; Lin et al., 2011). The public can also determine their attitudes toward the government based on their perceived quality of public services. If the government fails to maintain public trust, it will lead to negative effects, such as a bad government image (Tao et al., 2014). Consequently, the public will withdraw from public services and turn to private ones (Dowding & John, 2011). The researchers also suggest that citizen satisfaction stimulates political effectiveness, trust, and participation, resulting in social well-being (Vigoda, 2007). Therefore, this study replaces the variable of “customer loyalty” with “public trust” when building the model. From the above argument, this study assumes the correlation between satisfaction with local administrative units and trust as below:

Public expectation

Expectation may be formed from previous experience, and also be increased or decreased by external influences, such as the mass media and advertisements. R. E. Anderson (1973) claimed that for a rational individual who is familiar with the goods and services he or she is experiencing, there may be a relatively small gap between expectations and perceived quality. This means that high expectations tend to lead to strong perceived quality. Forrest (2012) reported that higher expectations do lead to stronger perceptions of governance after experiencing in a survey of American citizens’ evaluation of local state governments. Scholars also claimed that public expectation is likely to adjust in the short term (Zeithaml et al., 1985). In addition, promoting budget information transparency is a key step in modernizing national governance, and it is important to understand the expectation and opinion of the public as the subject of supervision. The expectation disconfirmation model (EDM) has recently been used to study how citizens’ perception of government service-related satisfaction develops (Lobato et al., 2017; Oliver, 1980). To validate the relationship between expectation and satisfaction, researchers (Lobato et al., 2017) divided the concept of expectation into three types: general expectations, personalized expectations (Oghuma et al., 2016), and total expectations. The first attempt to apply EDM model in the field of government administration supported its function in clarifying the sources of citizens’ satisfaction with government services (Van Ryzin et al., 2004). From the above argument, this study assumes that:

Government image

Same as the enterprise image being largely affected by the products and services it sells, the government image is also reflected by public products and services it provides and the way how public views the use of public fund (Suaib et al., 2017). A study on Mexican government projects also examined that the image of administrative machinery had an impact on both public expectation and satisfaction (Lobato et al., 2017). Specifically, when the public perceives the rising unemployment and falling living standards to be the result of misallocation of public resources, a bad image of the local government’s inaction will take shape. This will directly incur the decline of public satisfaction leading to lesser expectations the government. This indicates that the cognition and loyalty of the public is more likely to be affected by the government image as directly perceived by the public. More intuitively, it is logical to state that compared to a bad-behaved government, the public is more prone to trust a well-behaved government. To sum up, this study suggests that the explanation of introducing government image as exogenous variable is worthy for consideration, then the assumption is as follows:

Methodology and Measurement Items

The data for this study were obtained through a questionnaire survey, the contents of which were adapted from the previous literature for content validity. A total of 370 questionnaires were collected out of which 235 were valid. The design of this questionnaire was as follows.

The first part of the questionnaire was a preliminary demographic survey of the respondents based on several indicators such as gender, age, education, occupation, and political background (Yang et al., 2018). The sample characteristic analysis is shown in Table 1. Approximately equal numbers of men and women were invited to take this survey. Among them, most were between the ages of 30 and 45 and nearly 60% of them had received a senior high school degree or higher. This ensured that the respondents involved in this survey had the ability to think and understand independently. The results also showed these respondents held different political positions: member of the Communist party of China (CPC) (10.32%), member of the Communist Youth League of China (CYLC) (37.30%), Non-CPC intellectuals (19.05%), and Masses (33.33%). In short, this survey comprised a wide variety of individuals in China.

Demographic Characteristics of Respondents.

Note. CPC refers to the Communist Party of China, which serves as the ruling party in China; CYLC refers to the Communist Youth League of China, which serves as the youth’s social organization of a communist nature; Non-CPC intellectuals refers to individuals who are not formally partisan but own the right to participate in political elections as independent candidates; Masses refer to the ordinary people who are not affiliated to any party or league in politics.

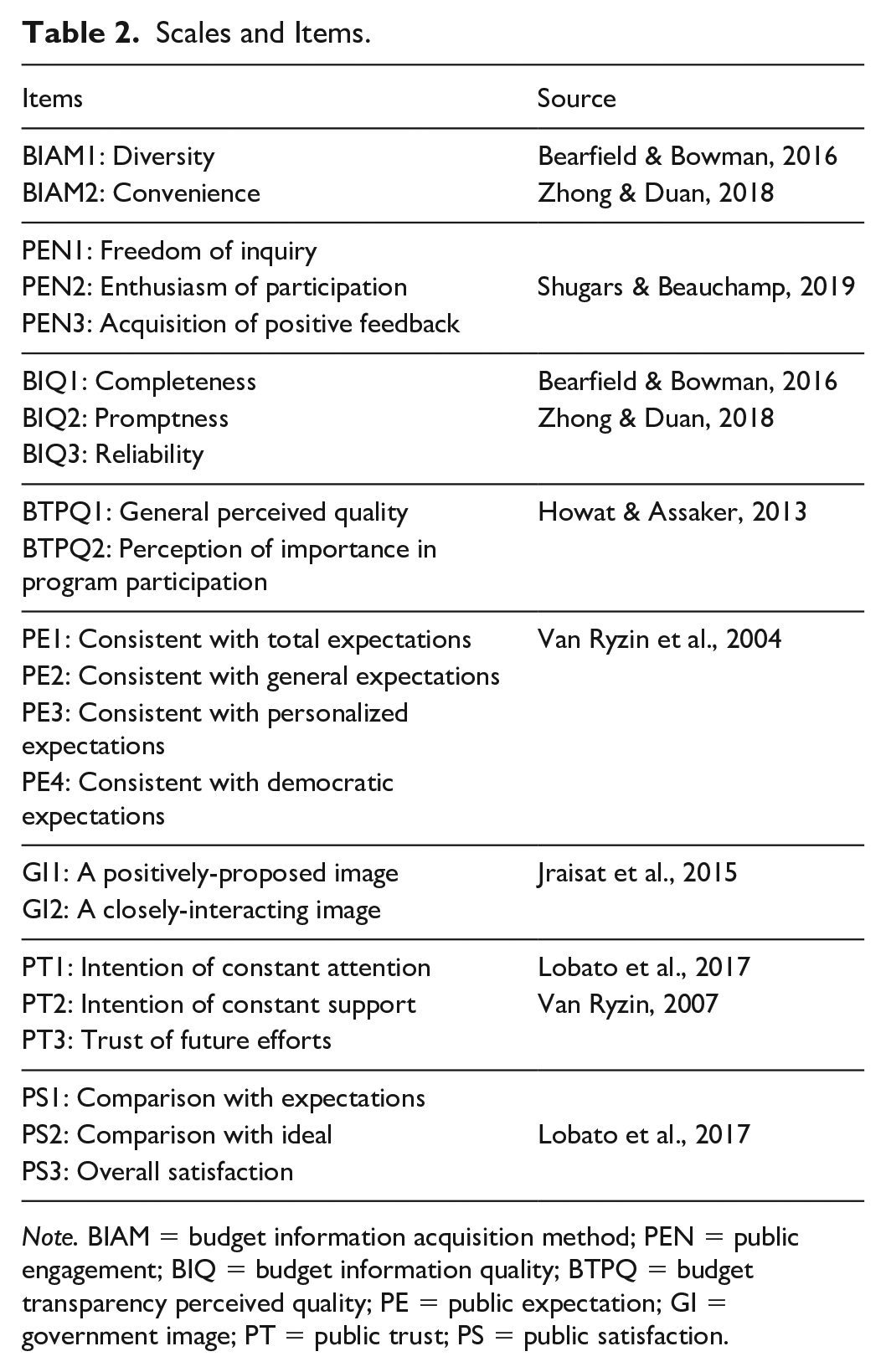

The second part of the questionnaire contained several measurement items that illustrated the constructs of the proposed model in this study. All the measurement items were marked using a 7-point Likert-type scale wherein the responses varied from 1 (strongly disagree) to 7 (strongly agree). The questionnaire and corresponding items are shown in Table 2.

Scales and Items.

Note. BIAM = budget information acquisition method; PEN = public engagement; BIQ = budget information quality; BTPQ = budget transparency perceived quality; PE = public expectation; GI = government image; PT = public trust; PS = public satisfaction.

Budget transparency perceived quality was measured using the items from Howat and Assaker (2013) to evaluate the public perception about the process of budget transparency with local government. Moreover, this study divided the budget transparency perceived quality into three quality factors: budget information acquisition method, budget information quality, and public engagement. By using the items focused on diversity and convenience proposed by Zhong and Duan (2018), this study measured what budget information acquisition method is available to the public, while the items focused on completeness, promptness, and reliability were used to measure what budget transparency is provided to the public. The items of public engagement were adapted from Shugars and Beauchamp (2019), where the importance of acquiring positive feedback in predicting users’ online conversations was elaborated. This study further developed the construct by adding another two items including freedom of inquiry and enthusiasm of participation. The items concerning public expectation which were adopted from Van Ryzin et al. (2004) showed how the public perception of budget transparency satisfaction takes shape. Government image was measured with a two-item scale derived from Jraisat et al. (2015). This study deals with the budget transparency policy with local government, which is different from the customer retaining policy with local tourists in the study by Jraisat et al. Therefore, in this study, the established image of tourism institutions described in the original scale is adapted to describe the internal image of government in the process of interaction with the public. The items of public trust and public satisfaction were adopted from Lobato et al. (2017) for measuring the public subjective feeling toward budget transparency and their attitude toward the local government.

Considering that the mainstream questionnaires were in English, two bilingual experts on government budget were invited to avoid potential linguistic misunderstandings. In addition, a pretest was conducted involving 45 applicants through one-by-one delivery to further validate the questionnaire. Based on the results of the pretest, the empirical data were collected through an online survey website (www.wjx.cn), which has a sample of 2.6 billion people and more than 1 million active users, therefore provides an effective guarantee to the questionnaire survey (Yang et al., 2018).

Data Analysis

Compared with factor analysis, multiple regression analysis, path model analysis, and other multivariate analysis methods (Aartsen et al., 2002; Hair et al., 2017), SEM is superior in the following aspects: calculating the measurement errors of all observable variables to ensure accuracy and identifying causal relationship rather than simple regression coefficients (Cheng et al., 2018). A structural equation model consists of a structural model and several measurement models. The former focuses on the relationship among the latent variables which are abstract and difficult to measure (Mainul & Faniran, 2005). The latter is usually composed of several observable variables and a latent variable, where the observable variables are indicated by items in the questionnaire. Here, confirmatory factor analysis (CFA) was applied to test the convergent validity and discriminant validity of the measurement components (Chin, 1998). The structural model was examined by testing the hypotheses relationship among all constructs (J. C. Anderson & Gerbing, 1988).

Reliability and Validity of Model

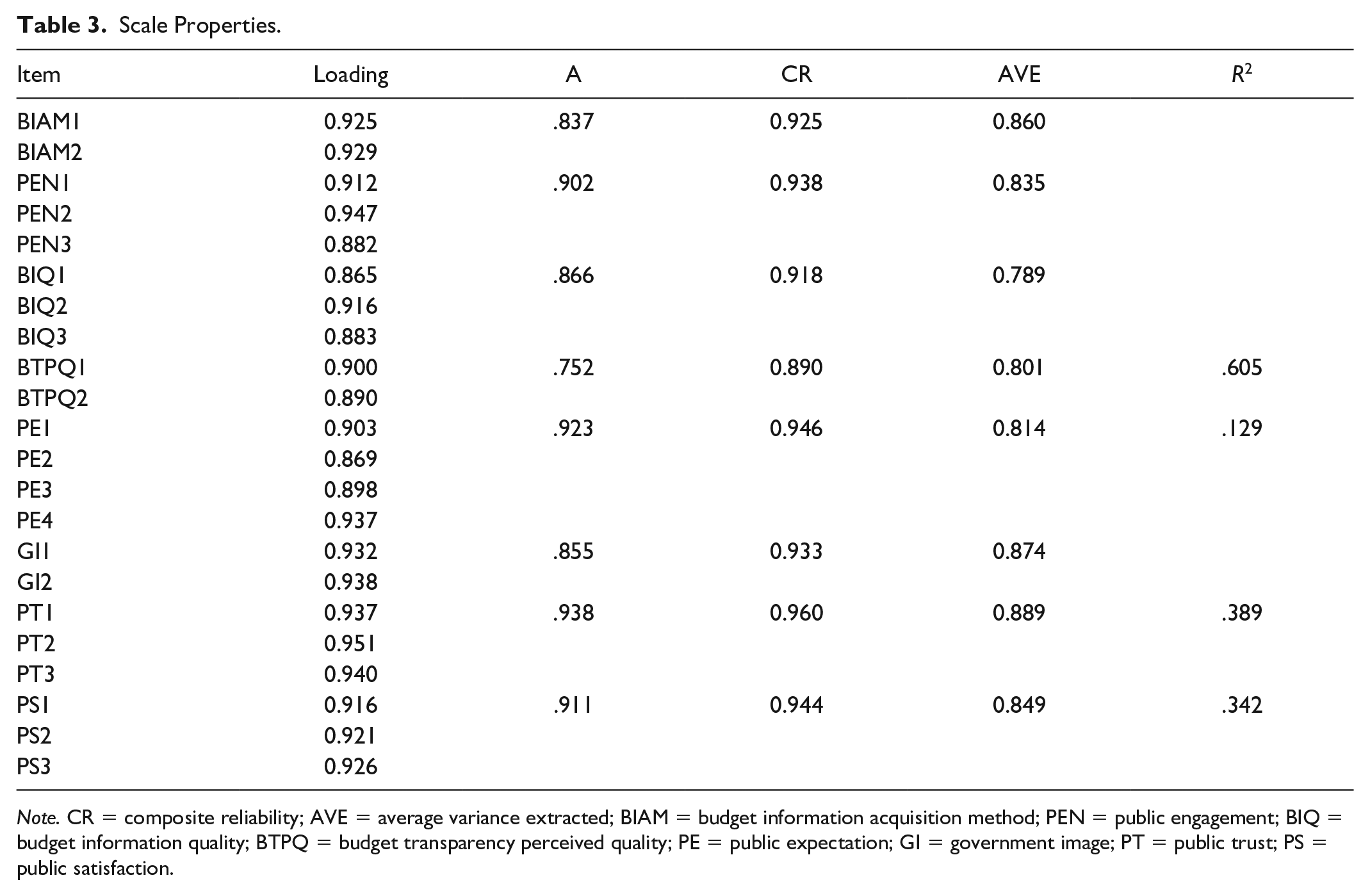

Fornell and Larcker (1981) suggested using standard loadings, Cronbach’s α (hereinafter referred to as α), composite reliability (CR), and average variance extracted (AVE) to account for convergent validity. Generally, a standard loading higher than 0.7 indicates that the corresponding factor is meaningful; a CR value higher than 0.7 indicates the consistency among different observable variables under the same latent variable; α higher than .7 indicates internal consistency of observable variables; AVE higher than 0.5 indicates the corresponding construct has good convergent validity. As shown in Table 3, the standard loadings of all constructs range from 0.865 to 0.951, α from .752 to .938, CRs from 0.890 to 0.960, and AVEs from 0.789 to 0.889. The discriminant validity was examined using two methods. First, the square roots of AVE of each construct were compared with the correlation coefficients between other constructs, with the former being higher than the latter, as shown in Table 4. Second, the loading on the corresponding construct was higher than cross loading on the other constructs, as shown in Table 5, which also proves that the items in this questionnaire can be distinguished from each other.

Scale Properties.

Note. CR = composite reliability; AVE = average variance extracted; BIAM = budget information acquisition method; PEN = public engagement; BIQ = budget information quality; BTPQ = budget transparency perceived quality; PE = public expectation; GI = government image; PT = public trust; PS = public satisfaction.

Correlations and AVE Square Roots.

Note. Diagonal parameters are the square roots of AVE, which should exceed the inter-construct correlations for better discriminant validity. AVE = average variance extracted; BIAM = budget information acquisition method; BIQ = budget information quality; BTPQ = budget transparency perceived quality; GI = government image; PE = public expectation; PEN = public engagement; PS = public satisfaction; PT = public trust.

The Results of Confirmatory Factor Analysis.

Note. Italics are the loadings of the principle components factors. BIAM = budget information acquisition method; BIQ = budget information quality; BTPQ = budget transparency perceived quality; GI = government image; PE = public expectation; PEN = public engagement; PS = public satisfaction; PT = public trust.

Furthermore, principal component analysis was used for Harman’s single-factor test. According to Chang et al. (2018), a single construct accounting for more than 50% of the variance implies that common method bias may affect experimental results. In this study, the combined eight constructs account for 84.540% of the total variance, while the variance of single constructs varies from 5.191% to 15.366%. Thus, the effect of common method bias can be excluded in this study.

Hypotheses Testing

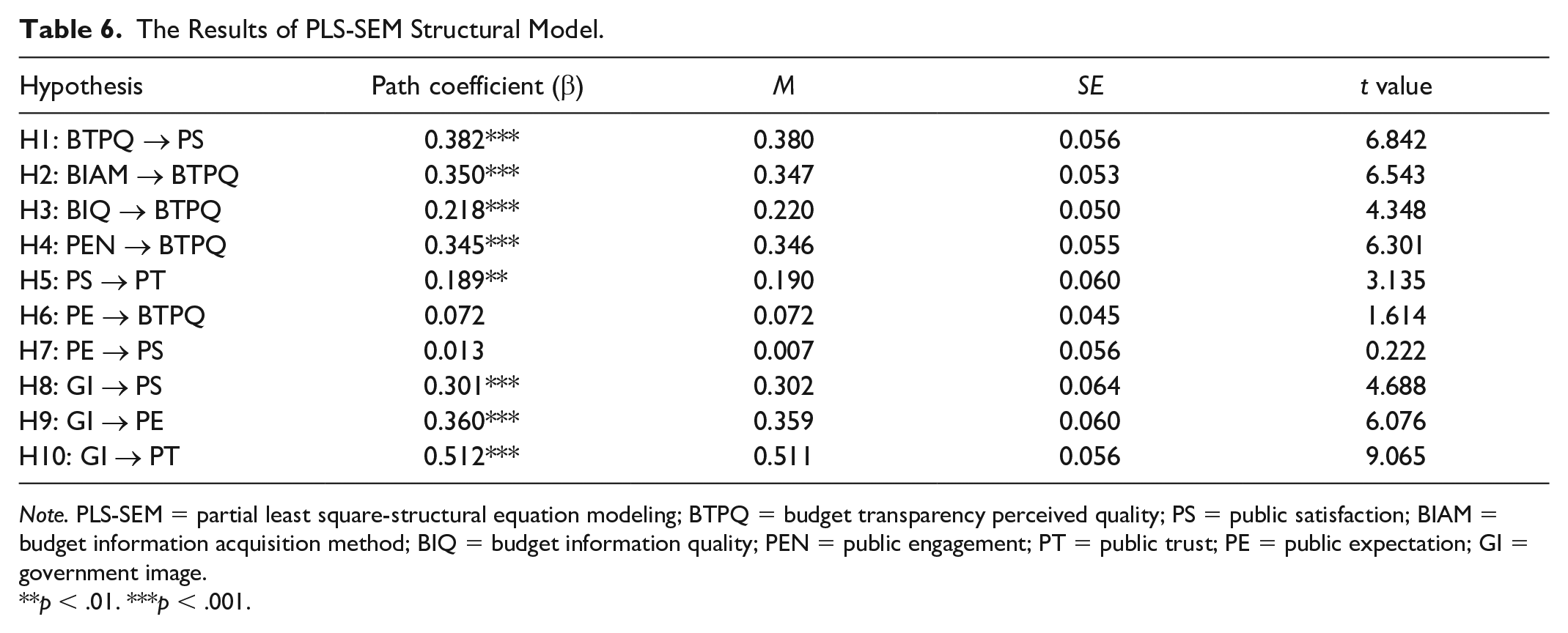

The structural model and the hypotheses were analyzed by partial least squares (PLS). Different from CB-SEM, the PLS-SEM reduces the requirement of data and specification of relationships, thus has fewer statistical identification problems and enable estimation based on a small-scale sample (Peterson, 1994). The results show that most of the hypotheses given in the “Definitions of Latent Variables and Its Relationship With Literature” section are supported. The hypotheses path from budget transparency perceived quality to public satisfaction is significant at p < .001 level, thus H1 is supported. The impacts of budget information acquisition method, budget information quality, and public engagement on budget transparency perceived quality are all significant at p < .001 level, thus H2, H3, and H4 are supported. The hypotheses path from government image to public satisfaction, public expectation, and public trust are all significant at p < .001 level, therefore H8, H9, and H10 are supported. The hypotheses path from public satisfaction to the public trust is also significant at p < .01 level, thus H5 is supported. However, the hypotheses path from public expectation to budget transparency perceived quality and public satisfaction are not significant, thus H6 and H7 are not supported. The results of PLS-SEM structural model are shown in Table 6.

The Results of PLS-SEM Structural Model.

Note. PLS-SEM = partial least square-structural equation modeling; BTPQ = budget transparency perceived quality; PS = public satisfaction; BIAM = budget information acquisition method; BIQ = budget information quality; PEN = public engagement; PT = public trust; PE = public expectation; GI = government image.

p < .01. ***p < .001.

The R2 for budget transparency perceived quality, public satisfaction, public expectation, and public trust are .605, .342, .129, and .389, respectively, which, according to Chin (1998), are moderate levels of explanations. This shows that the proposed model offers a reasonable explanation of the variance in evaluating public satisfaction with budget transparency.

Discussion

Based on the comparative analysis of previous research results, this study attempts to verify the significant factors that influence public satisfaction with the local government budget transparency based on the proposed model in the “Definitions of Latent Variables and Its Relationship With Literature” section. The model includes five aspects: budget transparency perceived quality, public expectation, government image, public satisfaction, and public trust. The first three aspects can be regarded as the antecedent determinants of overall satisfaction, while the last one, that is, public trust is taken as the resulting factor. Furthermore, this study measures budget transparency perceived quality by considering three quality factors which include budget information quality, budget information acquisition method, and public engagement. The SEM analysis presents several important findings and significant insights that can assist the local government in improving the practice of government budget management.

The following discussion is based on three subquestions of the study: How do antecedent determinants affect public satisfaction with local government budget transparency? How do antecedent determinants mutually influence each other? How does public satisfaction arouse public trust toward local government?

Determinants of Public Satisfaction With Budget Transparency

This study shows the budget transparency perceived quality to be significantly and positively correlated with public satisfaction. This is consistent with what Caruana (2002) claimed that perceived quality served as an important antecedent to customer satisfaction. In China, the heterogeneity of geographical location and resource endowment will lead to the inter-governmental differences in economic and social development. Therefore, compared with central government, local governments are more aware of the real situation in their areas and the real demands of citizens so as to provide public services tailored to local conditions. This highlights the characteristics of local government governance of being microcosmic, diversified, and direct. Also, from the perspective of citizens, they are more accustomed to judging the public services provided by local governments based on their perception. Such perception can be an important criterion to vote with their feet when faced with entering, staying, or leaving a region (Wang & Niu, 2019). In this sense, the budget information of local government is important on which the public can judge the performance of public services and ensure that government funds are in efficient use. Thus, public perception on budget transparency affects public satisfaction.

Furthermore, the budget transparency perceived quality is divided into three quality factors in this study: public engagement, budget information acquisition method, and budget information quality, each of which is shown to have significant effects on budget transparency perceived quality. Interestingly, when compared to the other two, budget information quality presents a weaker correlation to the perceived quality. Partly because that, although the public recognizes the importance of budget information quality, it is difficult for them to clearly understand the detailed budget reports disclosed by government departments. What the public can perceive directly is whether the government has provided diversified information disclosure channels and if public, as the audience of budget information disclosure, can have unimpeded access to information for their major interests and concerns. Owing to the professionalism of budget report and the public’s lack of financial knowledge, there is perhaps a gap between the acquisition and the understanding of budget information. So far, the results of this study have confirmed the hypotheses H1, H2, H3, and H4.

According to this study, government image also positively influences public trust and public satisfaction. This is consistent with what Lobato et al. (2017) claimed that the image of administrative machinery positively impacts public satisfaction in a case study of the Mexican government. A lesson from institutional theory is that the trust arises from the public’s response to the performance of the institution (Carpenter & Feroz, 2001). While in Chinese political institution system, there are distinct differences in power and responsibility between the central and local governments. Compared to central government, the responsibilities of local government lie in the coordination of public affairs and the provision of public services in their regions. Meanwhile, public has a subjective judgment on the government image, which directly affects their emotional preferences and behavioral tendencies. Against the misconducts of local government, the public will be disaffected and further erode their trust toward the government. Therefore, hypotheses H8 and H10 are also verified.

Unexpectedly, public expectation is not associated with public satisfaction according to the results. This is inconsistent with Oliver (1980) who claimed that satisfaction was regarded as a perception function of expectation level and confirmation. The possible explanation is that some additional variables such as time lapse and external information also shake public expectation. According to Latour and Peat (1979), individual expectations do not always influence their own emotional judgment directly in all cases. Imagine a scenario where a customer receives an unexpected inferior product or service. Even if he or she did not expect to be disappointed, this does not prevent her or him being dissatisfied with the purchase. In other words, the direct effect of expectation on satisfaction may be neutralized by additional variables. Thus, the impact of public expectation on public satisfaction appears to be more complicated than this study suggested, especially in case of the sensitive relationship between public policy and public response. This provides room to validate the relationship between public expectation and public satisfaction in the field of government governance in the future work. Therefore, hypothesis H7 is rejected in the course of this study.

Mutual Influence Among the Determinants of Public Satisfaction

As is evident from Table 6, the proposed hypothesis that government image is positively correlated to public expectation is supported. In general, the public expects more from a good government than a bad one. The probable reason is that the public has more confidence in a well-behaved government, and therefore, public expectation from the image of the local government will directly affect the disclosure of budget information. However, the correlation between public expectation and budget transparency perceived quality is insignificant. Scholars have disputed the relationship between public expectation and perceived quality, and only when the expectation is lower than perceived quality, the positive relation between these two variables holds (Forrest, 2012). Lobato et al. (2017) reported an insignificant relationship between these two variables, which is consistent with the result of this study. Such dispute also provides a mining perspective for the future exploration within the various subdivisions of government governance. Therefore, hypothesis H9 is supported, and H6 is rejected.

Analysis on the Resulting Factors of Public Satisfaction With Budget Transparency

Despite the modest significant verification results shown in Table 6, the hypothesis regarding the relationship between public satisfaction and public trust is statistically supported. Concluded from the empirical results of this study, public satisfaction is positively correlated with public trust. Indeed, satisfaction is a subjective feeling internalized in the mind, which can provide guidance to understanding an individual’s behavior. In this case, budget transparency policy is not only related to the improvement of national governance efficiency but also closely related to vital public interests. Therefore, public perception of the actual effect of policy implementation will affect their evaluation of the policy and their behavioral decisions. The proposed model considers public trust as a positive result of satisfaction, as is also evident in the theory of customer satisfaction that is examined by Beeri et al. (2019). Thus, the hypothesis H5 is supported.

Conclusion

This study provides several theoretical implications for the research on public satisfaction with local government budget transparency. First, differing from previous literature that mainly focused on the impact of various potential variables on public satisfaction, this study not only systematically explains the causes of satisfaction, but also its impact on public behavior. This is reflected in two components of the model, that is, the inputs and outputs of satisfaction. Besides explaining how and if government image, budget transparency perceived quality, and public expectation influence public satisfaction, this study also explains whether public satisfaction will foster citizens’ trust toward local government. A theoretical bridge between satisfaction and trust is built through the arguments offered. Second, where the past literature stopped at classical theories such as the citizens’ rights to know and principal–agent relationship to illuminate public satisfaction, this study takes it further. It incorporates the essence of these theories while extending the theory of customer satisfaction in the context of China’s budget transparency policy practice. Before that, the theory of customer satisfaction was used to explore the management mode of enterprises, only few studies combined it with government policies, let alone specific budget transparency policies. As an exploration of a new research method, this study provides a foundation for further research on public satisfaction with China’s budget transparency.

This study also provides some insights and enlightenments for policy makers. On the whole, from the perspective of budget information demand, the public is entitled to obtain the budget information reports of local governments and public utilities for the current year and bygone years. While from the perspective of budget information supply, local government should disclose relevant budget information in a timely, complete, and efficient manner. So, to eliminate the information asymmetry between the demand side and the supply side, local government should develop some strategies to improve the budget information transparency.

First, strengthen the information construction and maintenance of the municipal government website and expand the mobile terminal services, because the official website of the municipal government has higher credibility compared with alternative media. However, the webpage maintenance of most municipal governments and county and township governments is not good. Sometimes it is difficult for the public to find the information they want quickly and directly, or find the link window of citizens’ feedback easily. Poor information-seeking experiences reduce public patience, which contributes to the gap between public sector disclosure and public access. Local governments should make better use of the power of information and communication technology (ICT), strengthen the investment of talents and capital in information technology to improve the maturity of institutional portals, and create a better environment for informal interaction between government and citizens.

Second, local government should pay extra attention to promote their work on budget information transparency through local media. For a long time, government budget information has been considered as a state secret, and little was known about it because of its highly professional nature. Even though government has released relevant budget information, which consumes a lot of manpower and financial resources, the result is often counterproductive. Therefore, necessary publicity and education tools will, on one hand, strengthen citizen’s awareness as users of budget information and enhance their attention and understanding of government budget transparency. On the other hand, it is conducive to foster an atmosphere of political participation and discussion within the local community and other social groups. An informed society will put moderate pressure on the government, prompting to improve its own construction and improve the governance capacity (Da Cruz et al., 2016).

There are, however, some drawbacks that need to be overcome in this study. First, although this study collects data through questionnaires, the data set only involves a relatively short time, which makes it difficult to conduct a more dynamic analysis. Future research needs to further clarify the causal relationship by collecting cross-year data to analyze whether there is cross-time lag effect of budget disclosure policy on public satisfaction. Second, this study is based on China’s national conditions, although promoting budget transparency is a common path for global governance reform. Therefore, a cross-cultural perspective should be introduced into future research taking the differences in ideology and governance among nations into account. Finally, limited raw data was used in the process of analysis although the sample was well characterized and the empirical results are worth referring to. Further research can be explored based on larger sample so that more in-depth research conclusions can be obtained through demographic analysis. For example, multigroup analyses based on gender, political position, and registered location can also be established to compare the different effects of latent variables on different groups.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the National Natural Science Foundation of China (No. 51875503, No. 51975512), and Zhejiang Natural Science Foundation of China (No. LZ20E050001).