Abstract

This article identifies reputation-risk-relevant factors for banks, and the focus will be placed on the development of an indicator-based model for the assessment of reputation. Requirements and insights are based on a survey of credit institutions in Germany and Switzerland, which have been predominantly affected during the financial crisis by aptly nascent risks and which are thereby also partially affected even today. Reputation level can be considered as a temporally dynamical phenomenon which predominantly develops depending on the changes in the reputation drivers and expectations of the groups of stakeholders. This control parameter can be determined with the aid of Reputation Index Points (RIP). Efficient reputation risk management can, in the future, help prevent negative spillover effects from banks which face difficulties from the society or the taxpayers.

Introduction

The reputation of a bank refers to a public reputation of the bank in terms of competence, integrity, and trustworthiness, which results from the perception of the stakeholders. The reputation is a decisive factor for ensuring long-lasting profitability. The reputation risk in a broader sense refers to a negative or positive deviation from the expected reputation. Active reputation management, in this case, represents an indispensable component of the integrated controlling cycle of a bank. This impressively demonstrates the controversy pertaining to holocaust funds held on Swiss bank accounts at the beginning of 1990s, the collapse of the new market in Germany in 2001, the subprime crisis that started on the U.S. real estate market and its effect on the reputation of many banks such as, for instance, UBS, the scandal with respect to Société Générale in France or the difficulties which the Italian Banca Monte dei Paschi di Siena is facing recently. Negative effects, not least on the turnover of individual institutions, were or are the consequences. In particular, examples from the most recent past show the explosive nature with respect to the current issue of specific handling in the respective banking operation. This is all the more due to the fact that cross-industry studies repeatedly reflect the proportionally lower reputation which has been awarded to the banks by the public. According to one reputation study, the following three banks belong to the group of 50 “most admired companies” in the world: JP Morgan Chase, Goldman Sachs, and Wells Fargo (Fortune, 2016b); at the same time, Industrial & Commercial Bank of China, China Construction Bank, Agricultural Bank of China, Bank of China, BNP Paribas, Fannie Mae, and Société Générale and seven—other—credit institutions belong to the group of the hundred largest companies in the world (Fortune, 2016a). Furthermore, several banking supervisory bodies worldwide expressly call for—for instance—reputation risk management within the framework of national implementation of Basel II and III. A holistic definition which would integrate the issue pertaining to the reputation, identification, assessment, and control of the risks to which the financial service providers are exposed in the global competition is therefore obligatory (see also Ogrizek, 2002).

The scholarship on reputational risk management in banks is still limited in size. The purpose of this document is to elaborate an effective approach of managing reputational risks in banks. It is the first study which develops a holistic approach to measure and manage reputation risk to be implemented in banks in practice.

The main focus will be placed on the development of an indicator-based model for the assessment of reputation. On this basis, it is derived as how the control measures can be prioritized and controlled in the area of reputation risks. A basis for the inclusion of reputation risks in the comprehensive controlling cycle of a bank can be developed with the aid of such an indicator-based model. The comparison between the target and actual results and thus the efficient implementation of the model are particularly important in this process for the perception of the reputation of banks in the public.

This includes empirical surveys carried out with the banks in this approach as well. Insights into the current state of processes in identifying reputation-risk-relevant factors will be provided. The empirical part of this document is based on a survey of the biggest players on the German and Swiss banking market. Both countries have been predominantly affected during the financial crisis by aptly nascent risks and they are thereby also partially affected even today. Unlike in many other countries, several so-called system-relevant banks in Germany and Switzerland were in an existence-threatening state and could only survive due to heavy government interventions. Moreover, the access to survey numerous banks in those countries has been secured by pertinent local and regional contacts. Although the geographical radius of investigation needs to be extended in further research, it was possible to accumulate first relevant knowledge.

Literature Review

First, the literature review focuses on the definition of reputation itself. No uniform definition of “reputation” has been reached in the literature so far. The range goes from a macro level which considers the reputation as a resource, all the way up to a micro level which considers the reputation as a social view of the company (Fombrun, Gardberg, & Barnett, 2000; Fombrun & Van Riel, 1997; see also Brady, 2005; Scott & Walsham, 2005). Fombrun (1996) does not consider the reputation as a procedural but rather as a strategic intangible asset, by means of which tangible profits and an increased added value could be generated (e.g., greater turnover, lower operating expenses, integration of employees; see Fombrun & Shanley, 1990; Little & Little, 2000; Milgrom & Roberts, 1986; Roberts & Dowling, 2002). Based on this literature and based on practical observation, the following definition of the term “reputation,” which focuses on the creation of a potential of success and prevention of failure, is taken as a basis for the analysis of bank-specific reputation risks in the text to follow: Reputation is the public reputation of a bank which pertains to its competence, integrity, and trustworthiness, which results from the perception of the group of stakeholders of a bank (customers; shareholders; external creditors; employees; business partners; competitors; financial community such as rating agencies, analysts, and fund managers; government and regulatory authorities; interest groups, e.g., consumer association; and social environment).

In practice, the reputation risk is—for instance—defined as follows: risk of possible damage to Deutsche Bank’s brand and reputation, and the associated risk to earnings, capital or liquidity arising from any association, action or inaction which could be perceived by stakeholders to be inappropriate, unethical or inconsistent with the Bank’s values and beliefs. (cf. Deutsche Bank, 2017)

Within the framework of this article, based on the construct of the reputation, the following definition of the reputation risks can be taken as a basis: risk of a negative and chance of a positive deviation of the reputation of a bank from the expected level.

This definition does not expressly restrict the reputation risks to the risk of losing reputation, but it also includes a chance of gaining reputation in a broader context in the reputation risks—both active and targeted, as the case may be. It is therefore not only possible to sustain a loss of reputation due to, for instance, tardy investment consultancy, insufficient support, or conditions in credit business which would not be in line with the market, but it is rather also possible to increase the reputation of the bank by a customer-oriented process organization, competent consultancy services, or attractive conditions.

In the text to follow, a positive effect of the reputation on the success of a company is provided as an example, and it can also be empirically verified (cf. Fombrun & Wiedmann, 2001):

Increased attractiveness of jobs (e.g., for graduate students);

Increased payment readiness in case of investors—when the risk remains the same—and profit expectations;

Profitability above the industry average;

Mainly positive connection between the reputation and the financial success of a company (e.g., determined by means of ROI parameters).

Against this backdrop, active reputation management can significantly contribute to safeguarding and increasing the market value of a bank, by means of identifying the reputation risks, prevention and limitation of reputation losses, and preparing measures for generating a reputation gain at the same time. Reputation management can, in this process, be defined as a target-oriented process of definition, identification, assessment, and control of reputation risks.

Second, the literature has addressed the issue of the reputation specifically in banks, in particular following the new economic crisis after 2000 (e.g., Ogrizek, 2002, in a branding context; Fang, 2005, specifically for investment banks; Perry & de Fontnouvelle, 2005, in the context of operational loss announcements) and in the aftermath of the financial crisis after 2007.

In one of the recent studies about the issue, Fiordelisi, Soana, and Schwizer (2013, 2014) are investigating the connection between the announcement of operational losses and reputational losses for a European and U.S. sample (see also Gillet, Huebner, & Plunus, 2010; Sturm, 2013, focusing on the same issue for the European market). They also state that “despite its importance, the number of studies dealing with reputational risk in the financial industry is still limited.” A study on Spanish financial institutions is dealing with their risk profile that should incorporate regulators’ reports on customer’s complaints. Herewith, the customer orientation can be increased (Gambetta, Zorio-Grima, & García-Benau, 2015).

More recent studies on the reputation risks pertaining to banks focus their attention on the topic of corporate social responsibility (CSR). Fatma, Rahman, and Khan (2015) determine in this process both the direct and indirect influences on CSR activities on the reputation of the bank. Chomvilailuk and Butcher (2013) examine the comparative influence of CSR on customer satisfaction in various cultural areas of Australia and Thailand and determined that the perception of the current CSR performance and the new CSR initiatives had a significant influence on the reputation of the banks—in contrast to CSR orientation. The influence in this case was subject to massive fluctuations with regard to the extent of community orientation of potential customers. In a survey carried out on the Brazilian market, Scharf and Fernandes (2013) ascertain as a result with the aid of inspecting a large Brazilian bank that brand awareness of the companies can also be enhanced by means of CSR-specific advertising, where preference of the clients toward individual benefits instead of preference toward commercial benefits is taken as a starting point. Similar findings have been elaborated by Mattila, Hanks, and Kim (2010), who questioned faculty and staff of a university in the United States about the reputation of mortgage companies.

In empirical research, Marinkovic and Obradovic (2015) state, among other things, that trust has the greatest influence on customers’ emotional responses, followed by social bonds and image. The connection of the trust and customer relationship was also addressed in Dahlstrom, Nygaard, Kimasheva, and Ulvnes (2014). They conclude that a relationship of trust between the business customers and the bank can significantly reduce the risk awareness of the customers. A special influence of ethical reputation was detected by Mulki and Jaramillo (2011) in their study carried out with 299 customers of two large Chilean financial institutions. Customer satisfaction, customer value, and customer loyalty can also be manifested and enhanced if the bank is focused on its ethical reputation. Roy and Shekhar (2010) also ascertain the same connections for Indian retail banking sector (see also Roy, Davlin, & Sekhon, 2015; Sekhon, Enew, Kharouf, & Devlin, 2014). According thereto, the central aspects for the trustworthiness are “customer orientation, integrity and honesty, communication and similarity, shared values, expertise, and ability and consistency.”

A rare conceptual survey carried out by Parente, Costa, and Leocádio (2015) is focused on retail banking area in Brazil. They develop a scale for measuring the customer perceived value. Ahmad (2005) proposes a “triplex bond” model, according to which the banks should primarily focus on the product with respect to its functionality as well as secondarily on the personnel and infrastructure; hedonistic motives such as a feeling of satisfaction with the bank are—among other things—of superior importance in this case. However, no holistic suggestion regarding the actual implementation of the reputation management in banks has been developed by now. It is clear here that the banks still suffer from a partially significant loss of trust (Hurley, Gong, & Waqar, 2014; Nienaber, Hofeditz, & Searle, 2014).

Method

At first, the results of an empirical study carried out in 2017 provide an insight into the current status of the reputation risk management in the nowadays banking practice and show the practical significance of the topic. For this purpose, 53 banks were surveyed via e-mail in Germany and Switzerland during the second half of 2017, whereof 43% (23 banks) have actually participated. (17 banks answered in a first round of questioning and a follow-up after 4 weeks led to the feedback of six more banks.) Among the respondents are five “big banks” and 18 savings and Cantonal banks.

The questionnaire (see Figure 1) has been developed and validated in four interviews with Chief Risk Officers of three Swiss banks and one German bank. These experts have been chosen according to the size of the banks: two “big banks” with a balance sheet total of more than 500 billion Swiss Francs, another private bank below that threshold, and one state-controlled regional bank with a balance sheet total of approximately 150 billion Swiss Francs. Those experts shared experience in specific incidents affecting the reputation of their institute and information on practical means to identify specific reputation-risk-relevant incidents. They also explained about which institutional units possibly hold responsible for monitoring, reporting processes, and taking action with regard to reputational risks and their management.

Questionnaire on reputational risks in banks.

Anonymity has been guaranteed for the experts as well as for the participants of the survey. There was no willingness to make internal bank management issues—in combination with personal names or names of their banks—public without that commitment. The responses have been received from chief risk officers, risk management officers, operational risk officers, investor relations officers, and media relations directors.

Based on the empirical insights, the type and manner in which classification, gathering, as well as assessment of the key factors can be carried out for the bank-specific reputation risks are defined (indicator-based model). Finally, a reputation risk profile will be derived.

Empirical Findings

Awareness of the Significance of Reputation Risks in Practice

A majority of the participants who were involved in the empirical study think that reputation risks are of extreme significance (see Figure 2). More than a quarter of the parties participating in the study attach even greater importance to them than, for instance, to credit risks or risks associated with the market price—and, at the same time, 13% of the participants attach less importance to them. Furthermore, the overall relevance of reputation risks in the course of the last 10 years for only six out of 23 banks that participated in the study has not increased in the meantime (see Figure 3).

Significance of reputation risks in relation to other risk categories.

Different significance of reputation risks.

Obviously, not all banks have the same level of awareness with respect to reputation risks. This inevitably leads to the fact that they react in different ways and manners in the case of a (potential) reputation-risk-relevant event and that they can—as the case may be—develop adequate measures.

Practice-Relevant Risk Drivers

The completed empirical study results in a classification into four main reputation risk drivers (see Table 1). Customer satisfaction is considered by all participants in the study as the most important factor of influence for the reputation of the respective bank (23 nominations). Social requirements in the broadest sense are considered as almost equally important (21 nominations). The financial performance of the bank is also considered to be decisive for the perception by the public (20 nominations). The quality of internal processes is of major importance for the questioned banks as well (20 nominations).

Reputation Risk Drivers.

The following drivers are considered to be decisive for the change of the reputation of the respective bank as well, although deemed as relatively subordinate: crisis in other banks (16 nominations), legislative and regulatory requirements (16 nominations), the media (12 nominations), and increasing orientation of the management toward capital markets (three nominations).

It must be pointed out now that a model for quantification of reputation-risk-relevant factors can be expanded beyond the identified key drivers by other classes or factors of influence—in particular bank specific. The basic prerequisite for the control of every risk category is as exact an identification or analysis thereof as possible, which means that it must be determined what types of reputation risks could arise at what level or in what areas of the bank operation.

Handling the Reputation Risks in Practice

The illustrated management process begins in the current banking practice mostly with a structured media response analysis, on the basis of which the issues of any relevance of the bank are distilled, aggregated, and prioritized. The method developed by communication technology and called “Issues Management” is applied in such cases. In this connection, “issues” refer to conflict-leading topics which could, in return, result in public debates in mass media. “Issues management” refers to the systematic monitoring, analysis, and strategic influencing of public communication within the meaning of the reputation of a bank. The issues management is applied systematically, particularly in large banks. The organizational integration in this case usually takes place via the communication system of the company. Occasionally, media analysis is restricted to image-related articles in leading media about the bank and its relevant competitors. This is complemented by internal risk management, such as involvement of specialist departments, and through individual feedback from customers, investors, and other stakeholders. The potential future dynamics of various issues (e.g., manager salaries, power of banks, behavior in case of restructuring and downsizing) can be forecasted in this way, and the potential effects of the reputation can be estimated with the aid of IT-based and scenario-based analyses. The analysis can, in this case, be carried out separately for each subsector (e.g., bulk business, leasing, investment banking), region, and so on. A communication plan is usually derived out of the results of this analysis, which determines how and whose influence should exert influence on the way in which the respective issue is addressed vis-à-vis the groups of stakeholders. Furthermore, inward sensitization is understood as the most important task of reputation management, on one hand vis-à-vis the managers and, on the other, vis-à-vis individual sales and specialist departments in which the inherent reputation risks associated with their respective business area are recognized and assessed in the cross-divisional teams with regard to the risk potential.

In addition to influencing the reporting system, the diversification of the reputation as an important instrument is considered, that is, it must be supported by several representatives and by several areas of responsibility to prevent unilateral dependencies and thus an increased reputation risk. Limitation of the reputation risks is usually a task performed in practice by the respective business sector, that is, in the private business sector, attention must be paid as whether the investment counseling corresponds to the risks involved or, in the borrowing sector, parties must be aware of the financing instruments which are not allowed (e.g. armament).

All in all, it must be noted that this communication-based approach is suitable under the conditions of today’s media-oriented society, in particular in cases of complex issues which the public and the society associate with the bank. However, non-media perception of all groups of stakeholders (e.g., direct experience of the customers in dealing with a bank) is neglected. Likewise, a holistic, cause-oriented detection and control of reputation risks is not realized due to the fact that no systematic detection of internal, potential reputation risks—such as, for instance, non-uniform regulation, vulnerable business practices, or non-transparent products—has taken place and thus the issues created from the bank outwards cannot be gathered in a target-oriented manner. Conceptual broadening of this—for a long time solely applicable—industry standard is therefore necessary and mostly established in practice, as will be illustrated below.

Near the end of the empirical studies, the banks were asked—as per the significance and the reputation risk influence factors—to describe the manner in which they themselves deal with reputation risks. In this respect, they first described the means for identifying these risks (see Figure 4).

Means of identifying reputation risks.

Against the backdrop of the scandals that happened to banks in the past few years, it is not particularly surprising that the banks have oriented themselves meanwhile primarily toward the requirements and expectations of all stakeholders or the company as a whole (17 nominations). In particular, the banks identify the reputation risks by comparing positive with negative press reports as well as by determining the absolute amount of (negative) customer feedback (15 nominations each). Furthermore, seven banks also take into consideration the feedback of their own employees, and one bank only considers this. Survey of rating agencies, analysts, and fund managers (five nominations) and assessment of process quality (four nominations) were, in this respect, pushed to the side. Furthermore, in one case, scientific observations and trend research were used in addition to specific analysis of the environment, analysis of the exact reasons for complaints of the customers, and special consideration of business dealings associated with reputation risks. One bank pointed out that they only take an across-the-board approach to the issue of reputation risks within the framework of their assessment of risk-bearing capacity—without carrying out any particular measurement. Another bank has not been detecting the reputation risk systematically, although it intends to establish one system for this purpose.

A key indicator of the actual and problem-conscious dealing with reputation risk is their organizational assignment in the respective institution (see Table 2).

Organizational Responsibilities With Regard to Reputation Risks.

Including the media spokeswoman or the department for company/corporate communication.

In this respect, corporate management has 15 nominations, the department for investor relations 11 (and/or the media spokesman or the department for company/corporate communication), and risk control 10. In addition, the responsibilities within individual banks are assigned to marketing or market research or integrated in the principles of general compliance. In addition, the responsibilities within individual banks are assigned to marketing or market research or integrated in the principles of general compliance.

Furthermore, the banks were asked to describe the treatment of the reputation risks and to tell whether regular internal communication or, in particular, an internal reporting system has been established for this purpose:

This was the case in only four banks.

The internal reporting system of four banks deals only with customer complaints.

Furthermore, another bank stated that reputation-relevant considerations and suggestions are contained in the quarterly reports of the risk control department.

Subsequently, a question was asked pertaining to the specific use of reputation-related information. The answers can be summarized as shown in Table 3.

Use of Risk-Relevant Information.

Reputation-Risk-Relevant Factors and Their Quantification

Based on the empirical findings, the following drivers of overall bank reputation have been chosen to be used in a suggested controlling model for reputational risk management in banks: social requirements (e.g., level of assumed social responsibility), financial performance (e.g., return on equity), quality of internal processes (e.g., process complexity level), and customer satisfaction (e.g., number of customer complaints/number of concluded deals).

Indicator-Based Model for Assessing the Reputation

The level of a reputation can be considered as a temporally dynamic phenomenon which, in principle, develops depending on the changes in the reputation drivers and the expectations of the groups of stakeholders. These control parameters will be assessed in Reputation Index Points (RIP). Standardization of the measurement scale was carried out in such a way that a level of 100 RIP corresponds to a level of reputation which has neither a positive nor a negative reputation-relevant signaling effect. Consequently, it can be assumed that the expectations of the members of the groups of stakeholders are completely fulfilled at the level of 100 RIP. This level can be described as a critical standard within the framework of which neither losses occur due to too low reputation nor are profits generated from a reputation which is positively contrasted toward expectations. It can be seen from Figure 5 that Bank A has a reputation level in all periods except for the last one, which exceeds general expectations. The external effect is consequently positive, all things being considered. In contrast, Bank B cannot fulfill the expectations in any period in question. One such level of reputation will have negative effects on the business activity and thus on the success of the bank.

Reputation index.

Employee and customer web-based surveys represent key factors within the framework of assessing the reputation. These instruments have already been used regularly for some time by large banks such as

Now, a process must be deployed on the basis of the fundamental structure obtained hereby, in the course of which it should be attempted by the persons in charge to quantify the individual driver with the aid of both internal and external data with respect to the cause. This quantification does not necessarily have to replace the measurement approach of the previous phase. However, it can replace it if the parameters have been determined, which have a higher (mostly cause-based) clarification power.

The following considerations can be applied to the issue of the transfer of the change rate of individual reputation drivers into the change of the level of reputation for the overall bank:

It must be assumed that the influence of individual risk drivers on the change of the reputation level for the overall bank is different and subject to significant temporal variability. The extent of the influence of individual reputation drivers is reflected in the so-called sensitivity factors.

The weighting applied near the end does not have to correspond to the sensitive factors (determined by means of a factor analysis). Subjective elements such as opinions of experts, for instance, can be taken into consideration as well.

The individual sensitivity factors (or weightings) of the reputation drivers must equal 1 in the total (see Table 4).

Weighting of the Reputation Drivers (Own Calculation With the Aid of SPSS).

The method for determining the optimal weighting of the risk drivers should be illustrated with the aid of the following example. The deviations from the reputation level expected for the banks, which have been recorded across 10 cycles, are recorded for the individual risk driver. At the same time, the reputation level of the overall bank was raised by including surveys. The exemplary database is illustrated in Table 5.

Output Data Obtained With SPSS.

Note. RIP = Reputation Index Points; S = social requirements; F = financial performance; I = quality of internal processes; C = customer satisfaction; OB = overall bank reputation.

Weightings of individual risk drivers can be estimated on this basis. For instance, a linear multifactor regression can be carried out here for this purpose, in which the total amount of the standardized beta coefficients is standardized to the value of 100%.

In this example, the coefficient of determination amounts to 99.8%. The four selected risk drivers would, in this form—for the example applied to more than 10 periods—thus offer an excellent basis for explaining the deviation of the overall bank reputation.

The specific application should be clearly illustrated with the aid of the following practical example. Using various types of surveys of groups of stakeholders, the index values (in RIP) will be collected for three periods (X1 through X3) for all four reputation drivers (see Table 6).

Temporal Development of the Actual Level of Reputation (Practical Example).

Note. RIP = Reputation Index Points.

The influence of the driver affects, with the following (fictitious) weightings, the level of the overall bank reputation (see Table 7).

Weighting of the Reputation Drivers (Practical Example).

The deviations of the reputation level from the expected level of 100 RIP can be determined from these specifications at the end of the assessment periods X1, X2, and X3

It must be noted that the reputation of the overall bank is constant and deteriorates significantly in the third period. The levels which are higher by 20% than the expected levels can be observed in periods X1 and X2. The level in the period X3 is 14% lower than the general expectations. Furthermore, Figure 6 illustrates the process of developing the reputation level of the overall bank which would take place if one would assume equal weighting as an alternative to the differentiated weightings of the reputation drivers. It must also be noted that the basic information content of a reputation level which first improves and then deteriorates does not change in the process.

Change of the reputation level of the overall bank.

Developing a Reputation-Risk Profile

A differentiated reputation risk profile, which takes into consideration both the specific structure of the bank and its respective environment, is obtained as a result of an according management process. The reputation risk of, for example, a transaction bank cannot in this case be compared with any of the private banks due to its effective structure. There are, in principle, a variety of factors in the foreground: Certain individual factors which are relevant in a transaction bank can be totally neglected in a private bank. It is therefore not possible to transfer the results of the differentiated risk analysis pertaining to the reputation risk of a bank to any other random bank.

A so-called self-assessment represents the basic approach for identifying practice-relevant, industry-specific risk drivers. The self-assessment can follow a “bottom-up” approach and first identify the existing reputation risks on the basis of the opinion of the managers and employees working with individual business areas as per their respective area (e.g., structured interview, carried out by a reputation manager or external consultant, moderated “reputation workshop,” creative “brainstorming”).

The four-level classification of the reputation drivers is used as the basic framework for the surveys and self-assessments and is illustrated as an example in the text to follow: Every area must check within the framework of the process to determine whether reputation risks belonging to the basic classes of drivers and so on are given as well as what effects they could have. The self-assessment is also carried out in different departments and finally implemented at the level of the entire bank, assuming the management is involved. The results must then be collected and placed at the disposal of all bank employees for the purpose of sensitization of behavior. Furthermore, the interaction with other risk categories must be worked out at the level of the entire bank (for instance, how a change in the credit portfolio policy influences a possibility of a resulting occurrence of reputation risks). To complete the self-assessment and risk profile, it is recommended to refer to external sources as well, for example, analyses of media reports on the bank, which circulate in practice.

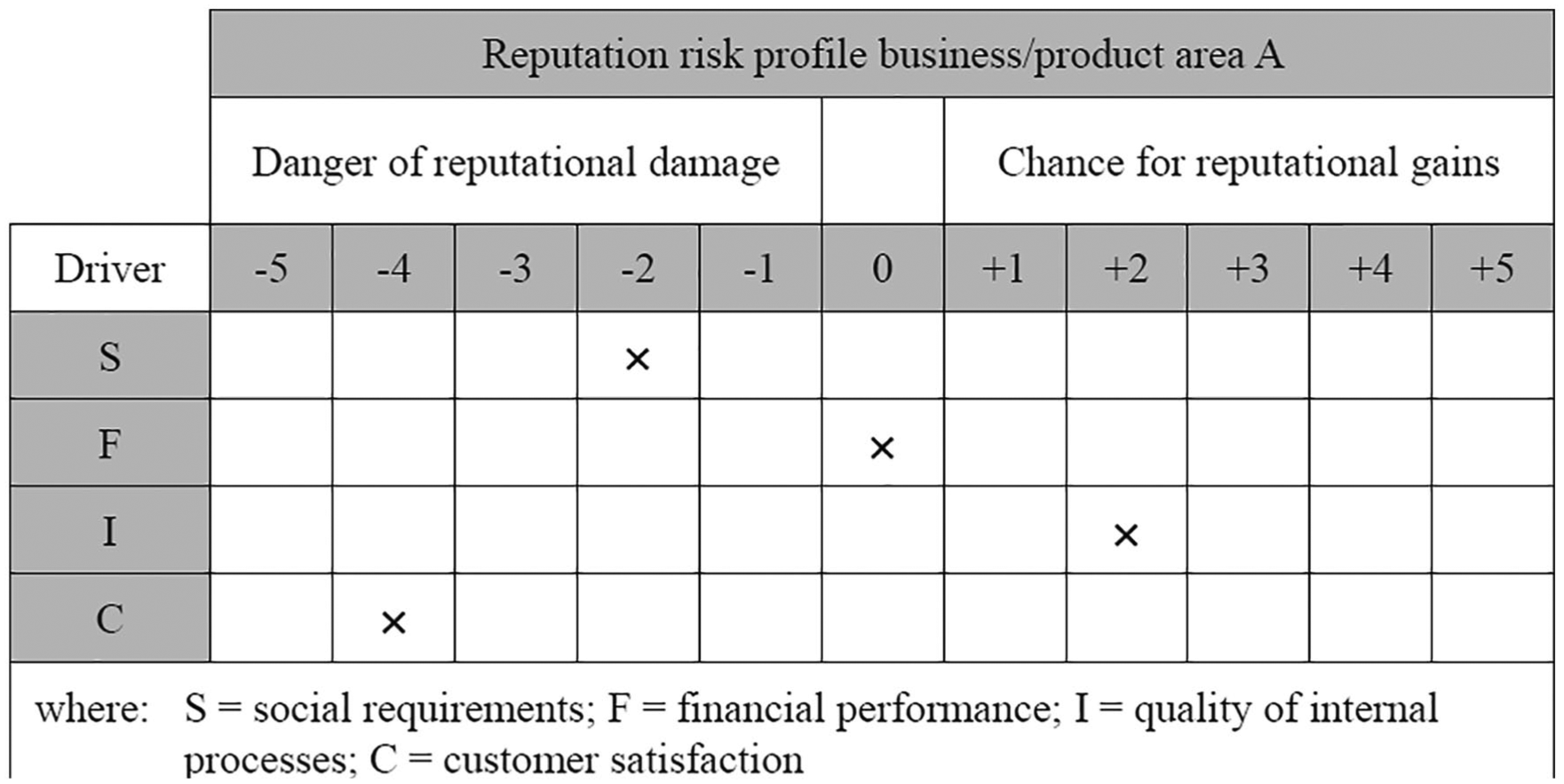

The following proposal is made hereinafter for the purpose of preparing a reputation risk profile: As a first step, the self-assessment is carried out at the levels of individual business or production areas and separately for each driver, and the extent to which the specific individual factors within the respective driver contain reputation risks is determined therein. The assessment is carried out with the aid of a range of whole numbers from −5 to +5. Value 0 in this case describes the neutral range, that is, the respective individual factor is assessed in such a manner that it can have neither a positive nor a negative influence on the reputation. Values −1 through −5 describe a potentially negative reputation risk, where −5 stands for the greatest degree. Likewise, values +1 through +5 reflect positive reputation risks: In the example to follow (see Figure 7), the self-assessment starts with the Business/Product Area A and with the quality of the drivers in internal processes, which are divided into individual factors such as corporate governance, communication, and human resources. A differentiated risk analysis can only result in a conclusion that an individual factor “corporate governance” is associated with a slightly negative reputation risk (value −1). It is extremely possible for both other individual factors to generate reputation gains (value +3). The facts behind the respective classification must be provided in a supplementing report.

Reputation risk profile (I).

The self-assessment can be continued on the upper level, where the risk profiles of individual business/product areas are summarized and transmitted for all four drivers (see Figure 8). The following can be derived for the driver “quality of internal processes” assuming an adequate weighting from the aggregation of the assessments for individual factors, for instance, a value of +2 for Business/Product Area A. (The illustrated results are fictitious.)

Reputation risk profile (II).

Subsequently, the figures determined in that way for all business/product areas can be consolidated for the entire bank (see Figure 9). It is obvious from the illustration in the figure that the Business/Product Area D is associated with extremely pronounced and slight to medium negative inherent reputation risks, which result from the type and structure of the business operated therein. Business/Product Area B taken as a whole remains within the neutral range. In Business/Product Area C, there are only medium chances of generating reputation gains.

Reputation risk profile (III).

This process of self-assessment should be repeated on a regular basis and implemented institutionally, that is, for instance, the requirement of a central reporting system for potentially reputation-relevant transactions or the remuneration of managers and employees should be influenced in a negative manner if (internal) reputation risks were to materialize which were never actually disclosed due to a faulty self-assessment in the respective area.

Discussion

Serious reputation risks have an effect on actions and reactions of various groups of stakeholders to the advantage or disadvantage of the bank and, in the case of loss of reputation, lead to a sinking market value of the bank. In extreme cases, a massive loss of reputation can actually threaten the very existence of a bank. Analogously, reputation gains are reflected in an increased market value. The actions and reactions of groups of stakeholders, which have been triggered by changes in reputation, can be various and mostly manifest themselves in ex ante, non-quantifiable changes in the amount of costs and turnover.

In the group of stakeholders who are clients, loss of reputation leads to a lower rate of new business and the loss of existing relationships with customers. External borrowers demand an increased risk premium which again leads to higher capital costs for the bank. Shareholders think it is reasonable to withdraw the equity capital or to sell it on the secondary market, which again leads to a decreased share price (in the case of listed banks). The motivation of the employees and their identification with the bank decreases. Expressions of critical opinions of interest groups and negative attitude of the media when reporting close the “vicious circle” of the reputation loss.

In the case of a reputation gain, a “virtuous circle” is closed analogously, in the form of an increased rate of new business, lower capital costs, enhanced motivation of employees, sufficient possibilities of equity capital financing, and more advantageous public image of the bank in the media.

If a bank should decide to have its own reputation risk management, then it is necessary to establish a differentiation from other bank-specific risk categories, in particular operational risks, within the meaning of a coherent conceptual framework for risk management at the level of the bank as a whole. Based on the formation of dichotomous conceptual pairs illustrated in the literature that pertains to bank-specific risk management and, in particular, to the differentiation of risk categories (e.g., financial risks vs. operational risks), the risk events first should be grouped into risks which affect the reputation (= reputation risks) and into risks which do not affect the reputation when it comes to reputation risks. The regulatory approach to the definition can be used as a starting point for this differentiation. The Bank for International Settlements (BIS; 2016) in this case expressly excluded the reputation risks in addition to the strategic risks from the category of operational risks (p. 144). However, this has taken place less for the logical reasons pertaining to classes and more for the reasons pertaining to inadequate quantifiability of reputation risks and thus to non-existing opportunity to calculate the equity cover, as it is basically necessary for the operational risks within the Basel framework.

In the course of this document, it was possible to carry out the differentiation of reputational and operational risks on the basis of the following consideration: Operational risks can constitute the reputation risks at the same time. It is not difficult to imagine that, for example, a failure of the central server of a bank and loss of customer data caused thereby due to inadequate backup systems could lead to a loss of reputation of the respective bank. However, it does not mean that all operational risks could constitute the reputation risks at the same time. In case of natural disasters, for instance, it should not be expected that the operational losses associated therewith would necessarily lead to a loss of reputation of the bank, due to the fact that the loss trigger is outside of the area of the influence of the bank and the groups of stakeholders can therefore not draw any conclusion pertaining to the quality of the bank. If one should continue with this reasoning, he could on one hand conclude that financial risks might also partially represent the reputation risks at the same time. For instance, if the media report on high credit default or serious loss of proprietary trading of a bank—as it was the case in the subprime crisis—a loss of reputation could be associated therewith. On the other hand, not all serious financial risks can be necessarily associated with the reputation risks. As the case may be, a bank can actually enhance its reputation during the period of the market stress by means of relatively low losses. All in all, there are overlaps both between operational risks and reputation risks as well as between financial risks and reputation risks. The latter can therefore be comprehended as a portion of operational and financial risks which has an effect on the reputation of a bank.

The overall bank reputation can, in principle, be assessed as good or bad. A good reputation can be assumed when the perceived reputation develops beyond a certain level which is expected for the respective industry within the meaning of a minimum level. Analogously, a bad reputation (with damaging effects) can be assumed when this minimum level cannot be reached. These considerations transfer the core to an even deeper level, in particular the level of reputation risk drivers. The assessment of an overall bank reputation on the basis of the identified four classes of drivers conceptually presupposes the aggregation of the reputation level of individual drivers. In the case that the associated partial reputation driver should exceed the expected level, the influence of one single driver on the overall bank reputation can therefore be assessed as positive.

Development of a system for assessing the reputation risks represents an ongoing process. The tension between the potential conceptions ranges between simple, non-differentiated, and thus partially significantly simplified all the way up to extremely complex, expensive, and differentiated. Significantly simplified parameters can be relatively easily determined in the initial phase for all drivers. For instance, when it comes to customer satisfaction, simply the number of complaints can be used as a measure. In one subsequent phase, every single driver must be differentiated with respect to its actual cause and the changes in the driving causes must be assessed. Again, based on customer satisfaction, this would mean that one specifically addresses the reason for complaint and tries to capture it in its diverse dimensions. Depending on the driver in question, it will be associated with smaller or partially serious problems.

Within the meaning of a holistic identification of the causes of reputation losses and gains, a management process must also be implemented which brings forth as extensive information as possible regarding the explicit and implicit reputation risks of the bank.

Limitations

The limited database is a consequence of the banking landscape of Germany and Switzerland. In Germany, almost 25% of the total bank assets are covered by the four big banks Deutsche Bank, Commerzbank, UniCredit Bank, and Postbank (Deutsche Bundesbank, 2018). The total assets of the six Federal state banks contribute further 10% of all banks in the country. Besides, the market is represented by more than 1,800 mostly small banks (e.g., 385 savings banks and 875 credit cooperatives) usually without institutionalized reputational risk management processes. However, we find several large players among the savings banks, which—due to their size and according processes—were eligible for participating in the survey. For instance, the largest savings bank comprises 4% of all savings banks’ assets or 0.6% of the whole market in Germany (own calculations based on Deutsche Bundesbank, 2018; Deutscher Sparkassen- und Giroverband [DSGV], 2019). The main players in Switzerland are the two big banks Credit Suisse and UBS, the Raiffeisen Cooperative, and the 24 Cantonal banks. In 2017, those altogether accounted for almost 75% of the total bank assets in Switzerland (own calculations based on Swiss National Bank [SNB], 2018). The rest is widely dispersed and mainly allocated to numerous regional banks and savings banks that usually do not run a systematic reputational risk management. Altogether, this confines the number of possible participants in both countries and does not allow a valid distinction of the analysis results according to the category (type) of the banks. These survey results do not show a remarkable variety in the answers across types of banks.

Future research should expand the questioning used in this article to further countries. This should comprise not only other developed countries, but also developing countries, for example, in Asia, South America, and Central Europe for instance. By doing that, the findings of this research article can be underlined, validated stepwise, and increasingly generalized. Moreover, the practical implementation of the suggested controlling steps should be validated with regard to their feasibility and effectiveness later on. Nonetheless, a focus on those two countries which have been heavily affected by the banking and financial crisis of 2007 and in its aftermath, Germany and Switzerland, is providing fundamental first insights.

Conclusion

Reputation risks and their management represent an area characterized by most recent, bank-related conflict. As it was confirmed with the empirical study, banks consider reputation risks as an important risk category, and they are fully and well aware of their growing importance. However, unequal attention has been paid to handling the risks and identifying them, especially when one considers the manner in which various banks address them in practice. Scientific models for structuring and quantification of reputation-risk-relevant factors offer potential chances in this respect: A basis for integration of reputation risks in the holistic controlling cycle of a bank can be obtained with the aid of the indicator-based model proposed above. Last but not least, special attention must be paid to the comparison between the target and actual situation and analyses, as well as the measures associated thereby.

Key reputation risk drivers of a bank can be identified on the basis of a structured risk analysis. Changes in the relevant drivers are reflected in an overall bank reputation which differs from the initial reputation. Based on the empirical findings, four drivers of overall bank reputation have been chosen to be used in a suggested controlling model for reputational risk management in banks: social requirements, financial performance, quality of internal processes, and customer satisfaction. Furthermore, bank-specific drivers must also be taken into consideration on a case-by-case basis. Having said that, the problems of a sufficiently selective differentiation when trying to classify reputation risk drivers into classes are obvious here as well. For instance, overlapping is possible with respect to the satisfaction of the customers and social requirements.

In an overall view, it should be noted that there is an enormous need for action for banks, not least due to macroeconomic considerations. Current, highly volatile events—described as affairs or scandals by the international media and also recognized as such by a vast majority of the people—show this as well. It seems that the efforts to develop bank-related, integrative controlling systems must be intensified, at least in some banks. Willingness to use adequate instruments is, in principle, indispensable as a key factor on such “sensitive,” global markets. Banks are particularly dependent on trust. Efficient reputation risk management can make a decisive contribution to this.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.