Abstract

This study examines the association between CEO temporal focus and corporate engagement in philanthropy, and considers the moderating role of ownership. This association is investigated based on upper echelons theory and the conceptual framework of temporal focus. Using a sample of 2,285 observations of Chinese listed firms from 2010 to 2015, our results show that the relationship between CEO past focus and corporate philanthropy is positive in state-owned firms but negative in private firms. In addition, CEO future focus is negatively associated with charitable activities in state-owned firms, but positively associated with such activities in private companies. For present-oriented CEOs, the relationship between temporal focus and philanthropy is negative in both public and private firms, but the negative effect is stronger in private firms. The findings of this study show how CEOs’ time perspectives shape their decisions on company engagement in philanthropic projects.

Introduction

Does the chief executive officer’s (CEO’s) subjective view of time affect firm-level engagement in corporate philanthropy? Previous studies have investigated a variety of explanations for corporate charitable contributions. In particular, external factors such as stakeholder expectations or institutional pressures have been emphasized, because engaging in corporate social responsibility (CSR) related activities, including corporate giving, is a way for firms to align their strategies with stakeholder interests. Meanwhile, as decisions related to philanthropic projects are characterized by managerial discretion (Carroll, 1979; Wood, 1991a, 1991b), it is also important to examine the internal determinants of philanthropic behavior, particularly the influence of the CEO. Some findings have illustrated the effects of demographic and background factors (Boal & Hooijberg, 2001; Cha & Rew, 2018; Manner, 2010), CEOs’ attitudes toward stakeholders (Buchholtz et al., 1999; Lerner & Fryxell, 1994), executive incentives (e.g., Deckop et al., 2006; McGuire et al., 2003), CEO narcissism (Al-Shammari et al., 2019; Petrenko et al., 2016), and CEO political ideologies (Chin et al., 2013). However, investigations of executive managers’ personal values as predictors of corporate giving are still at an early stage.

In this study, we attempted to assess one particular aspect of CEOs’ values and psychological perspectives, namely CEO temporal focus, which, to the best of our knowledge, has never been examined as a predictor of corporate philanthropy. The psychological literature has long identified and validated the role of CEOs’ subjective view of time in strategic contexts, because it shapes a wide range of individual behaviors and outcomes related to goal setting, decision-making, and learning behavior (Bluedorn, 2002; Gevers et al., 2006), followed by corporate strategic activities such as the introduction of new products (Nadkarni & Chen, 2014), corporate entrepreneurship (Chen & Nadkarni, 2017), competitive aggressiveness (Nadkarni et al., 2016), and, as more recently examined, mergers and acquisitions (Gamache & McNamara, 2019). However, the connection between managerial temporal focus and corporate social behaviors has yet to be explored, although decisions related to philanthropic projects are characterized by managerial discretion and acknowledged to have strategic value, making it relevant to consider corporate philanthropy as an outcome of executives’ subjective temporal cognition.

To fill this gap in the literature, we raised and answered a question about the association between CEO temporal focus and corporate engagement in philanthropic activities. We based our premise on upper echelons theory, which emphasizes the influence of top executives on the behavior of their firms. According to upper echelons theory, executives perceive and interpret the situations they encounter through a personalized lens, based on their experiences, values, and personality traits, before making strategic decisions (Hambrick, 2007). As one aspect of an individual’s cognitive framework, time perception involves a similar mechanism, acting as a temporal filter to select and prioritize elements of objective situations (Nadkarni & Chen, 2014). Based on this premise, we expected CEOs’ temporal focus to significantly affect their firms’ propensity to engage in strategic projects, especially discretionary decisions that allow a high level of managerial discretion. By considering philanthropic investments from a strategic perspective and by emphasizing that the decision-making process for such projects leaves managers a great latitude of action, we empirically investigated the relationship between CEO temporal focus and corporate philanthropic activities.

Our study also examined the moderating effect of a firm’s ownership type. Firms with different types of ownership (i.e., state and private ownership) have their own forms of management and culture, reflected by heterogeneous governance structures, different levels of legal and institutional protection, and different types of managerial autonomy and accountability (Liao et al., 2019; Lioukas et al., 1993; Mintzberg, 1973; Tan, 2002). We considered the different ways that CEO temporal focus affects strategy in state-owned and private business environments, and examined how these differences influence philanthropic practices. More specifically, we drew on the literature on executive job demands and proposed that the compatibility between the distinctive environments in different types of firm ownership and CEOs’ perception of time will determine the degree to which their time perception is used in the strategic cognitive process of their firm and in turn affects corporate philanthropic practices.

We tested our hypotheses in the context of China. Although our theoretical arguments were built from a general perspective, we agree with H. Wang and Qian (2011) that the socio-political context of China provides a relevant environment for investigating corporate philanthropy. In particular, the influence of Buddhist, Daoist, and Confucian philosophies on Chinese traditional values is deeply rooted in Chinese culture, leading Chinese society to appreciate compassion and altruism with the strong belief that people should live to fulfill the needs of others (Angle & Tiwald, 2017; Fu et al., 2020; Ma & Tsui, 2015). Contemporary communist ideologies in China share this traditional view and base their ideological core on the principle of equal distribution of wealth in society (H. Wang & Qian, 2011). Therefore, the manifestation of the personal traits that drive philanthropic engagement should be easy to observe. In addition, based on our consideration of ownership as a moderating factor related to differences in governance structures, legal and institutional protection, and managerial autonomy and accountability, these differences are relatively conspicuous in the Chinese context. Government authority exists in almost all major functions of state-owned enterprises (SOEs) through the representation of the State-owned Assets Supervision and Administration Commission of the State Council (SASAC) at the central and local levels. As Du et al. (2012) pointed out, SASAC closely supervises the use of state-owned assets through frequent audits, drafts organizational regulations and laws, and has the right to appoint, dismiss, and evaluate CEOs. At the same time, Chinese SOEs control important sectors, enjoy favorable political connections and better access to institutional resources than non-SOEs (Y. Gao & Yang, 2021; Huang & Chang, 2019; Wei et al., 2016). Therefore, the differences between state and private ownership and the extent to which these differences determine the relationships between firm-level variables could be clearly identified in our sample of Chinese firms.

This study contributes to the literature on temporal focus and strategic philanthropy in two ways. First, we explicitly explored the connection between CEO temporal focus and corporate philanthropy. Using upper echelons theory and the conceptualization of corporate philanthropy, we described the mechanism by which temporal biases can be reflected in corporate philanthropic decisions, thereby adding another temporal consideration to the literature on strategy formation. Given the role of CEO characteristics in a firm’s strategic decisions, as indicated by upper echelons theory and the assessment of corporate philanthropy from a strategic perspective in previous studies, it is relevant to consider CEOs’ subjective time perception as a predictor of firms’ philanthropic spending. In addition, the results of our research contribute to upper echelons theory by expanding our understanding of how the characteristics of executive managers are reflected in the social behaviors of firms. With growing interest in the various dimensions of social responsibility in corporate strategies, considering corporate philanthropy as a result of CEO temporal focus can reaffirm the important role of the upper echelons and broaden research on their effect on corporate strategic outcomes.

Second, we sought to identify the moderating effect of ownership types on this relationship. We adopted the approach used by Nadkarni and Chen (2014) to introduce an environmental factor to our model to test the effects of different types of ownership. Based on the premise outlined in the job demand literature (Hambrick, 2007; Hambrick et al., 2005), we explored how time perspectives operate in relation to different types of ownership to investigate the varying effects of the level of compatibility between different dimensions of CEO temporal focus and different types of ownership on attitudes toward corporate philanthropy. Our emphasis on compatibility, rather than the CEO’s temporal disposition or the context separately, as a determinant of strategic social behaviors and outcomes simultaneously confirms and adds value to the findings of previous research. While prior findings are based on the premise that suitability determines managers’ ability to understand and respond to demand (e.g., Hambrick et al., 2005; Nadkarni & Chen, 2014; Waldman et al., 2001), we expected compatibility to foster managers’ confidence, self-capacity, and other positive characteristics, further encouraging the manifestation of their characteristics in firm outcomes.

The rest of this article is organized as follows. First, the theoretical foundations related to temporal focus, strategic philanthropy, and their relationship, as well as the moderating effect of ownership, are presented. Next, based on these theories, three hypotheses regarding the effects of each dimension of temporal focus (i.e., past, present, and future focus) on corporate philanthropy and the moderating role of ownership on these effects are developed. Next, we explain in detail our empirical tests, including variable measures, data collection and analysis procedures, and our empirical results. The results are discussed in depth. The article concludes by discussing the limitations of the study, offering useful suggestions for future research.

Theoretical Foundations

Temporal Focus

Temporal focus is one of the constructs of a psychological concept called “time perspective.” An individual’s time perspective is defined as the totality of his or her psychological sense of the past, present, and future (Lewin, 1942). Although time is an objective and unidirectional progression, and although all people experience the same inevitable “ticking of the clock,” the ways they perceive the past, present, and future are different (Rappaport, 1990; Shipp & Fried, 2014; Shipp & Jansen, 2011). People’s different personalities, backgrounds, experiences, and environments lead them to experience time in a very particular way, which we can describe as subjective time (Bluedorn & Denhardt, 1988; George & Jones, 2000; Shipp & Cole, 2015). This fundamental premise underlies research into the psychological factors of time. As an important component of time perspective, temporal focus indicates the degree to which an individual pays attention to different temporal dimensions: the past, present, or future (Bluedorn, 2002).

Regarding the motivations for research on the sense of time, Zimbardo (2012) emphasized that time perspectives are among the most powerful factors shaping human behavior. A large number of empirical studies have been conducted based on the Zimbardo Time Perspective Inventory (ZTPI), demonstrating that people’s time perspectives have significant effects on their fundamental life outcomes in terms of health (Hall et al., 2015), happiness (Cunningham et al., 2015), financial success (Klicperová et al., 2015), and social or environmental integration (Milfont & Demarque, 2015). The importance of time perspectives is also evidenced by a wide range of studies showing that a person’s considerations of the past, present, and future are related to his or her personal goal setting, motivation, and performance (Bandura, 2001; Fried & Slowik, 2004; Nuttin, 1985), study and self-regulation (Carver & Scheier, 1981), affection (Wilson & Ross, 2003), and strategic decision-making (Back et al., 2020; Bird, 1988; Das, 1987; Gamache & McNamara, 2019). Temporal focus, and particularly the time perception bias of executive managers, is therefore relevant to the context of strategic management, because this type of focus influences the attention, interpretation, and ultimately decision-making of CEOs when they consider their firms’ strategic options (Nadkarni & Chen, 2014).

Strategic Philanthropy

Corporate philanthropy has been defined as “an unconditional transfer of cash or other assets to an entity or a settlement or cancellation of its liabilities in a voluntary nonreciprocal transfer by another entity acting other than as an owner” (Godfrey, 2005, p. 2). Should a rational, profit-maximizing firm allocate its scarce resources to social philanthropy? It has been almost a century since this question was first raised in the famous Berle–Dodd debate in the 1930s. Even today, this question is the subject of intense debate among researchers in both empirical and theoretical contexts, and the issues raised by the two lawyers remain largely unresolved (Ferrell et al., 2016).

Standing somewhere between the two ideological schools of shareholder theory, which argues that the sole responsibility of a business is to increase its profit and that of its shareholders (Friedman, 2009), and stakeholder theory, which claims that the “success of an organization depends on the extent to which the organization is capable of managing its relationships with key groups, such as financers and shareholders, but also customers, employees, and even communities or societies” (Van Beurden & Gössling, 2008, p. 408), some analysts have proposed the notion of strategic philanthropy. This approach emphasizes a “convergence of interests” between society and business, in that both social and economic gains can be attained through philanthropic efforts (Porter & Kramer, 2002). Bruch (2005) categorized corporate philanthropy into four main types (shown in Figure 1), among which strategic philanthropy is the most effective approach, as it considers both internal competencies and external expectations. Therefore, firms can benefit society by using their unique capabilities. As such, if charitable efforts are considered in terms of business strategy, then charity can be used to help firms generate intangible strategic assets while enhancing their core competencies. Such assets can take the form of reputational capital (Fombrun et al., 2000; Gardberg et al., 2019; Peterson, 2018), employee commitment (Aguinis & Glavas, 2012; Block et al., 2017), stakeholder trust (Brown et al., 2016; Park et al., 2016), or acquiescence by regulatory institutions and legislative bodies (Dickson, 2003; Jenson & Murphy, 1990). Porter and Kramer (2002) saw the “competitive context” (or the social environment in which a business is located or operates) as the truly strategic perspective for considering philanthropy. Corporate philanthropy has also been described as a process that can co-align with strategic marketing to enable cause-related marketing (Szőcs et al., 2016; Varadarajan & Menon, 1988).

Approaches to corporate philanthropy.

Due to growing concern about the sustainability of business operations, many companies have expanded their view on value creation. Their focus has shifted from optimizing short-term financial returns to creating shared value that simultaneously benefits them and the surrounding society. In this expanded view, there is less sense of a trade-off relationship between economic efficiency and social development. If philanthropy is defined as part of the strategic management portfolio of firms, and if executives think carefully about where and how to donate, then corporate philanthropy can lead to optimal economic and social impacts. The notion of strategic philanthropy is therefore the fundamental premise underlying the proposed connection between CEO temporal focus and their corporate philanthropic decisions.

CEO Temporal Focus and Corporate Philanthropy

No previous study has directly or explicitly described the effects of CEOs’ individual temporal focus on corporate philanthropy. However, the relationship between temporal focus and philanthropic strategy has been implicitly mentioned and strongly supported by studies based on upper echelons theory (Hambrick, 2007; Hambrick & Mason, 1984) and by much of the literature on corporate social performance (CSP) (Carroll, 1979; Wood, 1991a, 1991b).

According to upper echelons theory, an organization’s outcomes tend to reflect the personal characteristics of its upper echelon leaders (Hambrick & Mason, 1984). More specifically, when executives encounter a strategic challenge, they tend to perceive and interpret the situation from their personalized perspectives, which are shaped by their own experiences, values, and personality traits (Hambrick, 2007). Therefore, their decisions directly reflect their personal perceptions. The underlying premise of this theory is the notion of bounded, perspective-limited rationality (e.g., Cyert & March, 1963; Díaz-Fernández et al., 2020; G. Wang et al., 2016). It is assumed that managers have certain cognitive limitations, making it impossible for them to consider all of the factors involved in the business environment. Instead, managers must guide, evaluate, and process environmental stimuli based on their limited field of vision. As an aspect of each individual’s cognitive frame, time perception works through a similar mechanism, as a temporal filter to perceive, select, and prioritize the multiple features of objective situations (Nadkarni & Chen, 2014). Based on this premise, we proposed that CEO temporal focus is an important predictor of corporate engagement in philanthropy.

The CSP literature has generally interpreted decisions related to philanthropy and other social responsibility projects as highly discretionary (Carroll, 1979; Wood, 1991a, 1991b). Compared with other investments, corporate giving has been described as “last in, first out” in a typical company’s action inventory (Wood, 1991a, p. 698). Such investments are considered to be highly discretionary because they are assumed to have little urgency (Aupperle et al., 1985; Carroll, 1979; Godfrey, 2005). However, the high level of managerial discretion involved means that philanthropic decisions fit the echelons perspective model perfectly. We expected managers’ personal characteristics to have a greater influence on firms’ strategy and performance in areas in which they have the greatest discretion in decision-making (Hambrick, 2007).

A strategic choice differs from a tactical or operational decision, in that strategic decisions concern the long-term future (a longer time horizon) and the entire company (a wider scope). As corporate philanthropy involves this type of strategic consideration, choices involving CP are expected to reflect the views and priorities of top managers (Hambrick & Mason, 1984). Strategic decisions have a lower degree of predictability or computability than other types of decisions, so strategic decisions in areas such as corporate charity tend to display the idiosyncrasies of decision makers. These decisions reflect managers’ own sets of “givens,” including their cognitive biases and personal values (Hambrick & Mason, 1984).

The Moderating Effect of Ownership

Different types of ownership (i.e., state or private ownership) have distinct corporate environmental conditions, including different levels of environmental stability (Jakob, 2017; Tsui et al., 1997). Job demand theory indicates that executive managers differ in the extent to which their own characteristics and values are suitable to deal with specific environmental conditions, and that the level of suitability will determine the degree to which their characteristics and values influence strategic behaviors and outcomes (Finkelstein & Hambrick, 1996; Hambrick, 2007; Hambrick et al., 2005). Our proposition is consistent with job demand theory, as it suggests that a CEO’s time perspective has more influence on corporate engagement in philanthropy in one type of ownership structure than in the other. Specifically, while SOEs provide a relatively stable environment with slowly changing conditions, high job security, but less room for managerial discretion, which is likely to suit a past-oriented leadership style, the dynamic working environment of private firms is characterized by rapid changes, unpredictable conditions, and a high level of market competition and managerial discretion, which could be a compatible context for CEO present focus and future focus. The higher the degree of compatibility between CEO temporal focus and the firm’s ownership environment, the stronger the temporal orientation to influence strategic behaviors such as philanthropic engagement, because the CEO will feel more confident and have a higher level of self-efficacy about how his or her time perspectives are used in corporate strategy. Therefore, we expected the type of ownership to moderate the relationship between CEO temporal focus and corporate engagement in philanthropy.

Hypotheses

CEO Past Focus

“Past focus” refers to the degree of attention devoted to the past. A past focus may gravitate toward memories, people, events, or experiences that have happened to a person in the past (Mohammed & Harrison, 2013; Zimbardo & Boyd, 1999). People with such a nostalgic outlook on life typically possess emotional and sentimental personality traits, which may predict altruism and moral obligation, because charitable giving could generate emotional benefits for givers (Carlo et al., 2005; Matsuba et al., 2007; Okun et al., 2007). These benefits could be a warm glow (Andreoni, 1990), prestige and self-esteem (Mathur, 1996; Olson, 2009), recognition (Kottasz, 2004), and less negative feelings (Cialdini et al., 1987). A person’s fondness for the past is associated with better emotional capacity (Batcho, 1998). For example, in a charitable giving context, a nostalgic person can easily find an emotional connection with loved ones or memories, which makes the donation a source of warmth and happiness. Therefore, we proposed that when a CEO’s time perception is biased toward the past, he or she tends to perceive a higher level of emotional benefit from philanthropic activities. As a result, we expected CEO past focus to be positively related to corporate philanthropy.

We further proposed that the effect of CEO past focus on corporate engagement in philanthropy is influenced by the type of ownership, because a person’s level of focus on the past may be driven in a positive or negative direction by the conditions prevailing in a state-owned or private work environment.

The argument is that as SOEs offer more legal protection, less pressure to make profits, and higher job security, they provide a more stable organizational environment for their CEOs than private firms. Therefore, SOEs tend to encourage feedback-based learning (Nadkarni & Narayanan, 2007), which is the strength of past-oriented CEOs. Past-oriented CEOs have the ability to remember, analyze, and appreciate the lessons learned from their organization’s successes and failures, and to use these past experiences to address current and future situations (Mohammed & Harrison, 2013; Thoms, 2004). In stable environments, where all conditions are relatively predictable and change occurs slowly, past-based learning tends to be particularly valuable. Therefore, past-oriented CEOs tend to be more compatible with state-owned business environments. The fact that previous experiences and lessons are seen as useful resources makes past-oriented CEOs feel more positive about the past, which can lead to voluntary behaviors (Carlo et al., 2005; Matsuba et al., 2007; Okun et al., 2007). People tend to give more when they are happy, successful, and competent (Moore et al., 1973; Wolfson, 1978). This psychological process can also be interpreted as a kind of reciprocity to society, in that people wish to offer something when they feel lucky or grateful (Hamilton, 1964; Trivers, 1971). Hence, we expected CEOs’ strong past focus in such a business environment to facilitate their firms’ engagement in charitable projects.

Conversely, private firms face fierce market competition. Their work environment is uncertain or even highly unpredictable, with frequent changes requiring flexible adaptation to new conditions. In such situations, the value of a past orientation and feedback-based learning is reduced, because knowledge and experience are quickly outdated in a rapidly changing environment. Excessive reliance on the past may even prevent the detection of new ideas and therefore interfere with the perception and resolution of current issues (Nadkarni & Chen, 2014; Song & Montoya-Weiss, 2001). In addition, CEOs of private firms typically face great pressure to meet their financial goals, and poor performance in the short term may put them at risk of being replaced.

Based on this analysis, we predicted that private sector CEOs with a strong past focus would experience negative emotions regarding their past experiences, including feelings of depression, unhappiness, anxiety, selfishness, low self-esteem, or difficulty in interpersonal relationships (Carelli et al., 2011; Zimbardo et al., 2012). Although in general past-oriented people tend to be nostalgic and are more likely to find emotional benefits in charitable activities, pessimistic and negative attitudes toward the past are less strongly associated with altruism than positive nostalgia (Krueger, 1999; Krueger et al., 2000), because their cognitive and emotional attention is typically focused on their own grief rather than on developing interpersonal connections and accepting social responsibility. Hence, in private firms, the association between CEO past focus and their attention to charitable projects is not as strong as it is in SOEs.

CEO Present Focus

People with a strong present focus have a tendency to adopt a “here and now” psychology, emphasizing immediate and spontaneous behaviors (Nadkarni & Chen, 2014; Shipp et al., 2009; Zimbardo et al., 1997). In general, a present focus tends to prioritize the present without considering future consequences. People with this type of temporal focus are often either reluctant to sacrifice their enjoyment of the current moment (present-hedonistic) or they feel pessimistic that their present experience presents no new opportunity for their life, because they believe that everything has been prearranged by fate (present-fatalistic) (Zimbardo & Boyd, 1999). In an organizational context, individuals with a present focus have a “here and now” orientation. They tend to focus on the current time frame and usually make short-term plans (Mohammed & Harrison, 2013; Nadkarni & Chen, 2014). CEOs with a “here and now” focus are therefore unlikely to engage in philanthropic activities, because it takes time for the effects of philanthropic projects to materialize. The literature on corporate philanthropy has pointed out that the benefits of corporate investment in societal programs take time to mature. Benefits such as improved brand image, increased respect and privileges granted by governmental elites (Gautier & Pache, 2015), and improvements in the competitive environment (Porter & Kramer, 2002) or in employee commitment (Godfrey, 2005) all require long-term efforts to materialize. Defining and making a real contribution to meaningful philanthropy requires a long-term strategy. However, a present-oriented, highly spontaneous CEO is much more interested in real-time information and the pursuit of short-term goals. Therefore, a present-focused leader who wants to act rather than deliberate is likely to neglect philanthropy in favor of other projects that involve a short-term time horizon. The “here and now” leadership style is incompatible with longer-term visionary investments such as engagement in philanthropy. Therefore, we proposed that CEO present focus is negatively related to corporate philanthropic activities.

In addition, we predicted that the negative relationship between present focus and philanthropic activities would be even stronger for CEOs of private companies than for those of SOEs. In making this prediction, we assumed that due to the dynamic environment and competition for financial goals in private companies, CEO present focus is further biased toward short-term targets and neglects long-term projects such as corporate philanthropy compared with the stable situation in SOEs. The “here and now” cognitive style of present-oriented CEOs is compatible with the environment in which conditions are constantly changing, and there is little room for experience-based knowledge, because what is needed is an updated view of the situation and agility to discover new opportunities (Crossan et al., 2005; Eisenhardt & Martin, 2000; Nadkarni & Chen, 2014). Thus, the short-term bias of CEO present focus is further encouraged and employed in the dynamic environment of private firms. Conversely, when the environment is more stable and each consequence has a lasting effect because the environment changes slowly, any decision will require cautious consideration for a longer-term scenario. Therefore, we predicted that the manifestation of CEO present focus in long-term projects such as corporate giving would be mitigated in this situation.

CEO Future Focus

Compared with past and present focus, the characteristics of future focus make it the most obvious predictor of corporate philanthropy. Indeed, a future focus is associated with a long-term vision in the cognitive process. The values characterizing future-oriented people, such as resilience, self-efficacy, and generative concern, strongly predict social volunteering behaviors (McAdams & de St. Aubin, 1992; Rossi, 2001), because people with these traits are likely to have altruistic concerns and to be socially responsible. They believe that their contribution will make a difference for the future, so once they set a goal, they are willing to work hard and take responsibility for achieving it. In addition, corporate philanthropy is likely to be fostered by future-oriented CEOs when it is approached as a strategy rather than pure altruistic behavior. From a strategic perspective, corporate philanthropy is an effective tool for firms to build strong relationships with their key stakeholders. Charitable contributions can enable firms to greatly increase their levels of customer loyalty (Porter & Kramer, 2002), employee engagement and retention (van Kranenburg & Zoet-Wissink, 2012), and trust and influence of government and legislative bodies (Gautier & Pache, 2015; van Kranenburg & Zoet-Wissink, 2012). As Freeman (1984) argued, stakeholder management is among the top priorities in the strategic management process and the ultimate survival of the firm. Based on this analysis, we expected corporate philanthropy to attract the attention of future-oriented CEOs who can envision, anticipate, and invest in creating the conditions for long-term success.

We further hypothesized that ownership structure moderates the relationship between CEO future focus and corporate engagement in philanthropy, such that this relationship is stronger in private companies than in SOEs. The environment in SOEs is generally stable, with lower levels of job demand, competition, or pressure to make profits than in private firms. Concurrently, managerial discretion is significantly lower in SOEs than in private firms with a lack of real autonomy and little latitude for managerial initiatives or decision-making, due to the presence of political supervision (Grout & Stevens, 2003; Lioukas et al., 1993; Organisation for Economic Co-Operation and Development, 2005). CEOs with a strong future orientation will see and detect what is yet to come and will therefore be better suited to dynamic environments with a high level of managerial discretion to turn their future vision into real strategic decisions (Chandy & Tellis, 1998; Gibson et al., 2007; Nadkarni & Chen, 2014). In such situations, CEOs’ future vision for long-term projects such as strategic philanthropy will be appreciated and promoted. We also noted that SOEs take on various social responsibilities according to government guidelines and supervision (Putnins & Talis, 2015). Therefore, the strategic attributes of corporate philanthropy tend to be less valued in the state-owned context, because stakeholders may perceive corporate philanthropic behavior as compliance with government guidelines rather than a voluntary concern for society. As a result, for CEO future focus, the legitimacy-enhancing role of corporate philanthropy will not be as significant as it is in private firms.

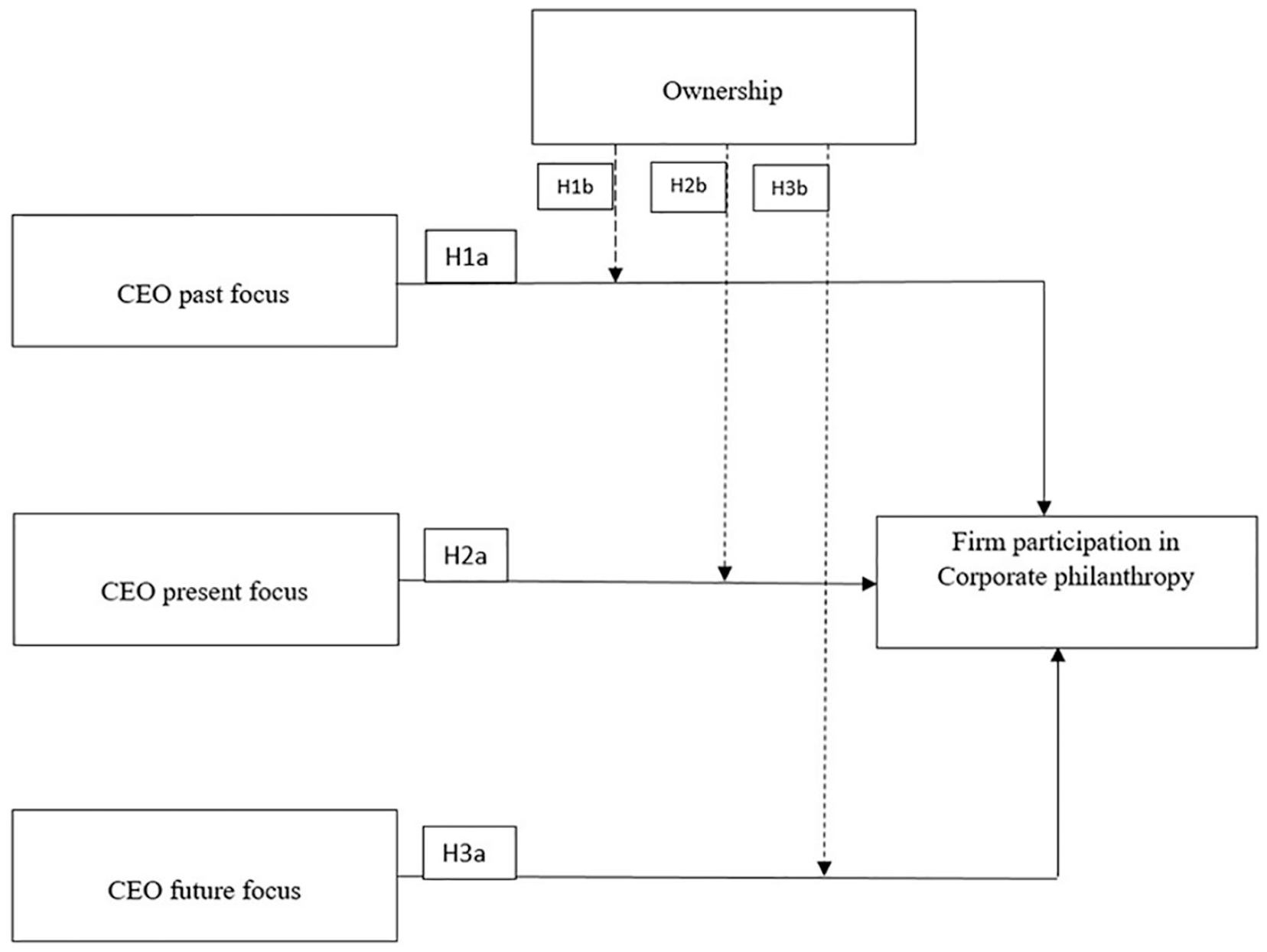

The theoretical model is presented in Figure 2.

Research model.

Methodology

Sample and Data Collection

The sample of companies used in this study was drawn from the A-share manufacturing companies listed on the Shanghai Stock Exchange in China. We obtained the data from two main sources. The first source was the Management Discussion and Analysis (MD&A) reports of the sampled companies (which are part of the annual report of each company). We extracted several specific categories of words from these reports, which were used to measure the three dimensions of temporal focus: past, present, and future focus. Our second source of data was the China Stock Market and Accounting Research (CSMAR) database, which provided information on each firm’s annual social contributions, ownership type, and various key financial data needed to measure our control variables. Using these types of archival data sources increased the accessibility of information and eliminated biases such as social desirability bias or meeting researchers’ expectations (Chatterjee & Hambrick, 2007; Cycyota & Harrison, 2006).

The MD&A is a section of the annual report of each registered company. The data presented in this section encompass managers’ discussions and analyses of their company’s performance over the previous year, along with an outline of their firm’s future goals and prospects (Cole & Jones, 2005; Schroeder & Gibson, 1990). The MD&A better reflects the psychological processes of CEOs than other board-approved documents, because it presents executives’ insights in ways that are not available in other types of financial statements (Barth & Murphy, 1994; Bernstein, 1993). More importantly, the MD&A gives managers more discretion in deciding the style, format, and items to be discussed (Chartered Professional Accountants of Canada, 2014; Hooks & Moon, 1993).

As a comprehensive database of Chinese stock returns, the CSMAR covers all companies listed on the Shanghai and Shenzhen stock exchanges. We obtained from the CSMAR all data related to stock markets and companies’ financial statements. However, it is inevitable that some data will be missing from any single data source. Therefore, we compensated for all missing data by using several websites, such as Sina Finance and CNINFO indices.

Data on the variables were collected from 2010 to 2015. We chose 2010 as the starting year because CSR data, including charitable contributions, have only been available since 2008, when the China Securities Regulatory Commission (CSRC) made CSR reports mandatory for three types of firms listed on the Shanghai Stock Exchange. As there is always a time lag between the emergence of intentions and the actual implementation of corporate projects, we compared the data on managers’ temporal focus for each year with those on charitable contributions one year later. The sample includes between 440 and 480 companies for each year, resulting in an unbalanced panel dataset of 2,285 observations. Among them, 46% of the firms are privately owned and 54% carry state investments. The firms belong to 26 industries in the manufacturing sector and have an average IPO age of 12.5 years.

Measures

CEO temporal focus

Text analysis (or content analysis) is a technique that systematically compresses various words of a text body into a smaller number of content categories, according to precise coding rules (Krippendorff, 1980; Kuckartz, 2014; Nord, 2005; Weber, 1990). The premise of text analysis is that an individual’s language use patterns can reveal his or her thought patterns (Sapir, 1944). The language that we typically use reflects our personality, our thoughts, or the context in which we operate (Chung & Pennebaker, 2007; Tausczik & Pennebaker, 2010). Therefore, by analyzing the word frequency in a large volume of text, we can relate an individual’s usage of everyday language to his or her personal traits, social behaviors, and cognitive styles (Tausczik & Pennebaker, 2010). By analyzing the frequency of keywords in specific categories in manager reports, we can identify their primary temporal focus and perspective.

We used Linguistic Inquiry and Word Count (LIWC2007) text analysis software to analyze CEO temporal focus on various dimensions. LIWC counts words in psychological classifications across various bodies of text. This program was invented by the team led by Pennebaker in 2001. More than 10 years after its invention, LIWC has achieved fairly stable validity and reliability and has become an effective tool for translating textual data into quantitative data, which is useful for further analysis (Pennebaker et al., 2015). The core of LIWC is its dictionary. SC-LIWC2007 (LIWC2007 Simplified Chinese Dictionary) consists of 71 dimensions. Each of a total of 7,450 words corresponds to at least one dimension of meaning (“Chinese version of LIWC,” n.d.). After going through the word categories, we identified a set of 37 words representing an individual’s past focus (e.g., the Chinese word for “old times,” “some days ago,” “in the past,” or “previously”), a set of 43 words for present focus (e.g., the Chinese word for “nowadays,” “this life,” “these days,” or “normally”), and a set of 36 words for future focus (e.g., the Chinese words for “will,” “in the future,” “later,” or “tomorrow”). LIWC analyzed whether each word in the texts was also found in the dictionary, and if it was, it determined the category (or categories) to which the word belonged. The results show all LIWC categories and the rate of occurrence of each word classification in the surveyed texts. The rates are reported in percentage form to normalize the scores by the total length of the text (Eggers & Kaplan, 2009). Through the measurement and analysis provided by SC-LIWC2007, we identified three sets of words reflecting an individual’s levels of past, present, and future focus. The degree to which each CEO focused on each temporal dimension was represented by the word frequencies (in percentage) of the respective word sets. The validity of the Chinese version of LIWC in examining psychological expressions in texts has been demonstrated in previous studies (e.g., R. Gao et al., 2013; Huang et al., 2012; Zhao et al., 2016).

Corporate philanthropy

The level of corporate philanthropy for each firm was captured by the amounts of charitable donations that were made by each company in each specific year (Makki & Lodhi, 2008; H. Wang & Qian, 2011). As this variable was highly skewed, we used a log-linear form of the model, in which the values of the donated amounts were transformed into logarithmic terms and applied to express the marginal effects of temporal focus on charity levels in multiplicative terms (Adams & Hardwick, 1998; Galaskiewicz, 1997).

Ownership type

Ownership type was a binary dummy variable, taking the value of 1 if a firm is state-owned, and 0 if it is private.

Control variables

Prior studies have emphasized the roles of market-level (including market munificence and market dynamism), firm-level (including firm resources and financial performance), and individual-level drivers (management team) as relevant antecedents of the level of charitable contributions (Atkinson & Galaskiewicz, 1988; Burlingame & Frishkoff, 1996; Campbell, 2007; Chih et al., 2010; Giannarakis et al., 2014; J. Wang & Coffey, 1992). Therefore, we controlled for market munificence, market dynamism, return on equity (ROE), ownership, leverage, duality (i.e., whether the CEO is also the chairman of the company), asset size, Tobin’s Q, cash, and slack resources in the model.

Details of the definitions and measures of the variables are presented in Table 1.

Variables Definition and Measurement.

Note. ROE = return on equity.

Analyses and Results

We tested the hypotheses using three regression models on the 2,285 firm-year panel dataset. The moderating effects were examined using a multiplicative moderation approach (Aiken et al., 1991). In Model 1, only the control variables were included. We then included the main effects of CEO past focus, present focus, and future focus in the model. Finally, we added the interactions between ownership and the three dimensions of temporal focus. Firm fixed effects were used to control for time invariant variables, while year–firm fixed effects were included to control for unobserved annual fluctuations that are not caused by any explanatory variable (Wooldridge, 2003). To provide a more robust causality test, we lagged the data on charitable contributions by one year. Due to the potential for multicollinearity, we used the standardized values of the predictor variables to minimize this issue (Aiken et al., 1991).

As visualizing the interaction effects was essential to accurately interpret the moderating effects (Hoetker, 2007; Nadkarni & Chen, 2014), we plotted interaction graphs based on the predicted amounts of charitable contributions, using separate regression lines for the two nominal types of ownership, namely state ownership and private ownership. We then obtained three graphs representing the levels of corporate giving predicted by the three dimensions of temporal focus: past, present, and future focus.

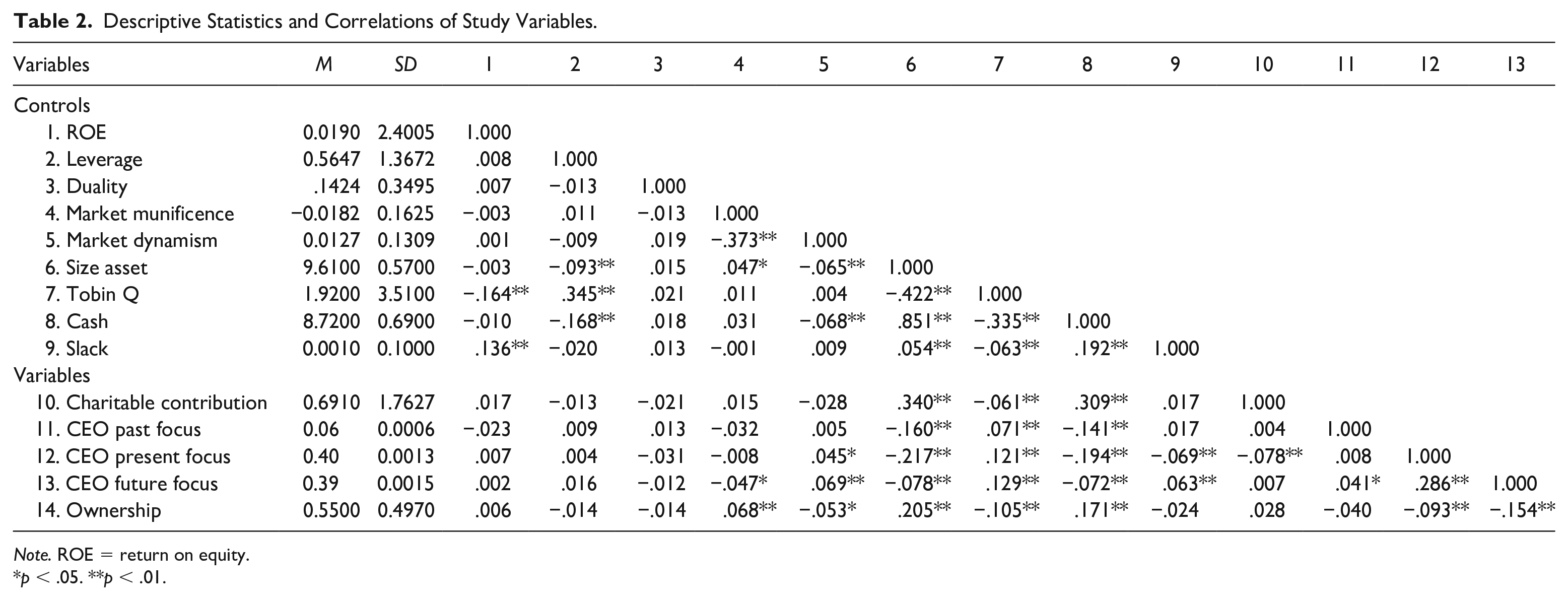

The descriptive statistics and correlations between the study variables are presented in Table 2. The regression estimates for the effects of CEO temporal focus on the levels of engagement in corporate philanthropy are shown in Table 3. In addition, as mentioned above, we plotted the interaction graphs in Figure 3 to clarify the comparative strength levels and moderation directions regarding the three dimensions of temporal focus.

Descriptive Statistics and Correlations of Study Variables.

Note. ROE = return on equity.

p < .05. **p < .01.

Regression Results.

Note. ROE = return on equity.

p < .1. *p < .05. **p < .01. ***p < .001.

Interaction plots of CEO temporal focus, ownership and charitable contributions.

The main effects reflecting the influence of the three dimensions of temporal focus without the moderator were significant, except for the effect of CEO past focus. Specifically, the effect of CEO present focus on the level of charitable contributions was significant and strongly negative (B = -0.8990, p < .01). In contrast, CEO future focus was positively associated with the level of charitable contributions (B = 0.4604, p < .1). The effect of CEO past focus was positive but not significant. Therefore, Hypotheses 2a and 3a were supported, but Hypothesis 1a was not supported.

The three interaction coefficients representing the moderating effects of ownership on three dimensions of temporal focus were significant. Hypothesis 1b proposes that the positive effect of CEO past focus on the level of philanthropic activities is stronger in SOEs than in private companies. The interaction between CEO past focus and donation level was positive and statistically significant (B = 0.1681, p < .05). The interaction plot in Figure 3 shows an upward sloping line for state ownership and a downward line for private ownership, indicating that the effect was positive for state ownership but negative for private ownership. Thus, Hypothesis 1b was partially supported. Furthermore, the theoretical mechanism we used to explain the influence of the private and state-owned environments remained relevant, and the empirical results even confirmed that it was stronger than hypothesized. Indeed, the dynamic environment in private firms drove the relationship between CEO past focus and corporate social contributions in a negative direction instead of remaining positive (although weakened) as Hypothesis 1b predicts.

Hypothesis 2b predicts that the negative effect of CEO present focus on the level of corporate charitable contributions is stronger in private firms than in SOEs. As the regression results show, the interaction term between CEO present focus and the level of charitable contributions was positive and significant (B = 0.2063, p < .01). In addition, the interaction lines in Figure 3 are downward sloping, with that of private firms being steeper than that of SOEs. Therefore, Hypothesis 2b is supported.

Hypothesis 3b proposes that the positive effect of CEO future focus on corporate charitable contributions is stronger in private firms than in SOEs. As shown in Table 3, the coefficient of the interaction term between CEO future focus and the level of charitable contributions was negative and significant (B = -0.1768, p < .05). According to Figure 3, the interaction line representing the relationship between CEO future focus and charitable contributions in private firms is upward sloping, indicating a positive relationship, while the line representing the relationship in SOEs is downward sloping, indicating a negative relationship. Therefore, Hypothesis 3b was partially supported. Again, similar to Hypothesis 1b, our proposition that CEO future focus is less compatible with the state-owned environment than with the private environment was supported. Furthermore, the empirical results suggest that the stable environment of SOEs with less managerial discretion reduces the level of engagement in social contributions of future-oriented CEOs.

Discussion

Theoretical Implications

Temporal focus has been studied in psychological science for many years and has a wide range of applications in management science. The philanthropic roles of corporations have also been widely studied (Chen et al., 2019). However, our study was one of the first empirical investigations to explicitly connect these two concepts in a direct relationship. One possible reason for the previous neglect of this relationship is that these two constructs do not seem conceptually related. As temporal focus is defined as an individual’s subjective perception of time, this concept has been linked (in most organizational or management studies) to strategic contexts such as goal setting (Bandura, 2001; Fried & Slowik, 2004; Nuttin, 1985), decision-making, teamwork (Gersick, 1988; Harrison et al., 2002; Labianca et al., 2005), and corporate entrepreneurship (Chen & Nadkarni, 2017). This set of associations seems logical because time is a type of limited resource and the consumption or allocation of time has a direct influence on the strategic activities that organizations choose to undertake. Meanwhile, the common understanding of philanthropy remains focused on a purely altruistic interpretation, so that this type of activity is generally seen as a “last in, first out” priority in a company’s action inventory (Wood, 1991a), rather than as a strategic investment. In recent years, however, this perspective on philanthropy has become increasingly obsolete, as it separates economic objectives from social objectives, although companies cannot effectively or sustainably operate in isolation from the societies around them. As Porter and Kramer (2002) pointed out, in the modern knowledge-based and technology-based world, the basis of competitive advantage has shifted from low-cost productivity to high-quality productivity. This transition largely stems from the improved integration of interrelated elements in the competitive environment (i.e., local policies and incentives, high-quality work and specialized resources, demanding local customers and related or supporting industries). Regardless of the size or wealth of a corporation, it is costly to make a small change in the business environment if a direct and fully self-reliant strategy is chosen. Philanthropy, as Porter and Kramer (2002, p. 61) recognized, is “the most cost-effective way to improve competitive context,” because “it enables companies to leverage not only their own resources but also the existing efforts and infrastructure of non-profits and other institutions.” In other words, philanthropy enables the collective strength of multiple companies and parties to spread costs, which might be unaffordable for an individual company. This is the fundamental premise underlying the notion of strategic philanthropy, in turn highlighting the relevance of our topic when considering CEO temporal focus as a predictor of corporate philanthropy.

Except for the effect of CEO past focus on corporate philanthropy, which was not empirically significant in our study, all of the dimensions of temporal focus (i.e., CEO present focus and CEO future focus) significantly influenced the level of engagement in philanthropic activities. The non-significant effect of CEO past focus may be attributed to the opposing emotional and cognitive processes associated with past focus. As Zimbardo and Boyd (1999) and Mohammed and Harrison (2013) explained, a past focus may be conducive to a warm, sentimental, and positive construction of the past, primarily focused on memories, people, events, and experiences of previous years (past positive focus). It may also involve negative, averse, and pessimistic views of the past, which may be due to unhappy past experiences (past negative focus). Whereas past positive people may engage in voluntary and altruistic behaviors, past negative people may “get stuck in the past” and be too biased by their own grief to care about social responsibility.

The results of this study contribute to the literature on upper echelons theory. These results are important because so far, the management literature has paid only limited attention to CEO temporal biases. The most in-depth examinations of time perspective theory can be found in psychological studies, which have mainly focused on defining the origins and operations of time perspectives, and the relationships between the dimensions of time perspectives and different aspects of human cognitive functions, such as goal setting, ambition, risk taking, sensation seeking, addiction, and rumination (Zimbardo & Boyd, 2015). These cognitive traits have rarely been linked to managerial contexts such as philanthropic decision-making. Previous research has examined the influence of subjective time perceptions on work practices, but analyses have been limited to identifying the various manifestations of past, present, and future focus on well-known corporate strategies, such as the introduction of new products (Nadkarni & Chen, 2014), corporate entrepreneurship (Chen & Nadkarni, 2017), competitive aggressiveness (Nadkarni et al., 2016), and more recently, mergers and acquisitions (Gamache & McNamara, 2019), leaving out corporate social behaviors, which have received increasing attention in research and practice. In addition, our analysis considered the positive and negative sides of each temporal dimension (i.e., past positive and past negative; present-hedonistic and present-fatalistic). Therefore, our research adds a temporal consideration to the conceptual literature. In addition, our approach to temporal focus with a more detailed categorization opens up new avenues to explore further implications.

The results of our study highlight the moderating effect of ownership type, which can either strengthen or weaken the relationship between CEO temporal focus and the level of corporate social giving. Almost all of the predicted effects are supported by our data. Specifically, the hypothesis related to CEO present focus is fully supported, but in the cases of CEO past focus and CEO future focus, the empirical results indicate a stronger moderating effect of ownership type than predicted. We proposed that the relationships between CEO past focus and charitable contributions, and between CEO future focus and charitable contributions, should be weaker in private firms and in SOEs, respectively. However, the results show that the moderator drives the relationships in the opposite direction. China’s collective context, often reinforced by control through state ownership, was expected to tightly restrict managerial discretion in decision-making. In addition to determining the level of managerial discretion, with its distinct characteristics and evolutionary history, state ownership in China has created a working environment distinct from the culture of private enterprises. These contextual factors, including governance structures, objectives, environmental stimuli, executive appointments, and evaluation or dismissal processes, all tend to change the levels and directions of the effects of CEO time perspectives on corporate philanthropic decisions. Environmental effects have been used as moderators in prior studies of the subjective attributes of CEOs (Finkelstein & Hambrick, 1996; Hambrick, 2007; Hambrick et al., 2005). However, examining these environmental effects in relation to firm ownership type is particularly relevant in the Chinese setting, due to the country’s special role for SOEs. Our results support this prediction, showing the significant effects of ownership type on all dimensions of temporal focus.

Empirical evidence of the manifestation of temporal focus in strategic and organizational outcomes has been found primarily in developed economies due to data availability. In developing countries, the lack of published raw documents and text analysis software adapted to the local language has prevented researchers from conducting in-depth examinations of the topic. Meanwhile, it is important to be able to generalize the results from Western countries to countries in transition, given the differences in institutional conditions and social values. For example, the less effective institutional framework highlights the motivation to engage in corporate philanthropy as a tool to gain the trust and support of stakeholders. In addition, compared with Western cultures, which are more individualistic and independent in terms of sense of self, and less influenced by social norms and the expectations of others, East Asian cultures tend to be more collectivist and dependent on group opinion. In the latter cultures, therefore, individual perceptions are more likely to be affected by the ideology and general values of society (e.g., Endo et al., 2000; Fiske et al., 1998; Hofstede, 1980; Yuki et al., 2005). This fundamental difference in cultural stereotypes may drive the manifestation of personal characteristics in philanthropic decision-making in an organization. We obtained empirical evidence from a sample of Chinese firms. First, our results are consistent with those previously found in Western contexts by acknowledging the strategic relevance of temporal focus in management research. Second, our findings open avenues for further investigation in Western countries involving the relationships between the different dimensions of CEO temporal focus and corporate philanthropic behaviors, as well as the contingent factors that determine the level of these relationships, so far unexplored in the literature on temporal focus and corporate philanthropy in general.

Practical Implications

In addition to their theoretical contributions, the findings can be used in management practice. Given the significant influence of subjective time perceptions on philanthropic strategies in firms with different ownership types, CEOs need to be aware of their individual biased view of time and control its effect on important decisions related to their firm’s charitable investments. When aligned with the personal attributes of the decision maker, a strategy can be initiated in an effective and authentic way, especially when it is related to issues involving altruism and allowing managerial discretion, such as philanthropic projects. However, when considered strategically based on a match between internal capability and external demand, instead of being purely driven by the personal characteristics of executives, such investments will yield optimal returns. Therefore, full awareness and adequate control of personal perceptions in accordance with an assessment of the external environment are essential in management practice.

Limitations and Directions for Future Research

This study has several limitations, which offer recommendations for future research. First, as Nadkarni and Chen (2014) pointed out, there are inherent biases in using secondary data and a psycholinguistic approach to measure psychological constructs such as temporal focus. Second, as mentioned in the theoretical framework, the internal differences in the subsets of past focus (past positive and past negative) and present focus (present-hedonistic and present-fatalistic) are not separated in the data, although these subsets may have different effects on the outcome variable. Future researchers should therefore consider measuring the effects of these subsets separately to obtain better and more comprehensive results. Third, we provide empirical evidence in China, representing a country in transition with distinct institutional conditions and social values. Future research could conduct similar assessments in different institutional and socio-cultural settings to better generalize the theory of CEO temporal focus and its effects on corporate philanthropy.

Conclusion

This study provides empirical evidence of the relationship between CEO temporal focus and corporate engagement in philanthropy. The differences between CEOs in terms of time perspective are shown to have different effects on the levels of corporate engagement in philanthropy, which differ between private firms and SOEs. The results of this study suggest that firms should consider temporal focus as an important criterion when selecting their CEOs. This is especially important for firms that regard the practice of strategic social responsibility as a high priority.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China under the grant numbers 71672127 and 71672108.