Abstract

Arab intra-regional trade in agro-food accounts for more than half of the total Arab agro-food trade, displaying strong “trade-intensity” over the past decade. This indicates the potential of developing agro-food regional production networks aligning with the region’s comparative advantage in agro-food products. However, intermediates trade, as an indicator of value chain integration, has been low and sluggish due to various structural and policy factors. This article aims to analyze the determinants of trade in agro-food intermediates in the Arab region, focusing on the role and significance of regional trade arrangements and trade facilitation. The Broad Economic Category (BEC) classification is used to categorize goods into intermediate and final goods. Our analysis, using the gravity model, shows that regional trade arrangements in their current form do not significantly affect regional trade (except in the Gulf Cooperation Council [GCC]). We also reveal that timeliness in export delivery is an important determinant of trade in agro-food intermediates. Thus, Arab countries should simplify their customs clearance procedures and engage in a deeper form of regional integration to help build trade corridors and enhance regional value-added chains (RVCs).

Trade in intermediate goods—goods used as inputs for further processing—has been steadily growing over the past decades. The export of intermediates accounts for about 42% of the total merchandise trade and has increased almost twofold since 2004, reaching around US$8,000 billion in 2014 (World Trade Organization [WTO], 2019). The increase in trade of intermediates has been driven by the global fragmentation of production and the emergence of global value chains (GVCs), where different production stages are more frequently located in different countries. GVC-linked trade takes place particularly in the manufacturing and service sectors, and also in the agricultural and food sectors (Greenville et al., 2017). However, compared with the manufacturing sectors, less is known about the agricultural pattern of trade in intermediates as well as the policy factors driving the development of value chains in the agro-food sector at the global and regional levels (Greenville et al., 2017).

There is growing evidence that the rise in intermediates trade (and GVCs) is strongly associated with regional trade agreements (RTAs; De Backer & Miroudot, 2013). Research on trade in value-added has shown that much of the trade in intermediates tends to take place within trade blocs in Europe, North America, and Asia (Miroudot et al., 2009). Trade cost is the driving force of the regional dimension of GVCs. Because they reduce border and “behind-the-border” costs, RTAs are arguably considered to be drivers of GVCs and trade in intermediates (Economic and Social Commission for Asia and the Pacific [ESCAP], 2015).

In this context, the Arab countries have, over time, witnessed the creation of various RTAs designed to boost economic growth and enhance regional integration. These include the Greater Arab Free Trade Area (GAFTA), the Gulf Cooperation Council (GCC), the Arab Maghreb Union (AMU), the Agadir Free Trade Area (AFTA), and many other bilateral trade agreements. However, despite the multiplicity of these trade arrangements, intra-regional trade is still below its potential and the region did not witness the economic transformation that has accompanied trade arrangements in other parts of the world (Al-Atrash & Yousef, 2006; Economic and Social Commission for West Asia [ESCWA], 2014; O’Sullivan et al., 2012; World Bank, 2013). In addition, trade in intermediates is lagging behind despite the existence of resource complementarity in the region, which is potentially conducive to high trade intensity in intermediate agro-food products, paving the way for the development of regional production networks (ESCWA, 2014). For example, the capital-intensive food-processing sector in the GCC region is sourcing its intermediate raw materials from outside the region despite the existence of highly competitive primary agricultural production in non-GCC Arab countries.

The objective of this article is to analyze the determinants of agro-food trade in intermediates in the Arab region, focusing on the role and significance of regional trade arrangements (RTAs) and trade facilitation. Using the Broad Economic Category (BEC) classification to categorize goods into intermediate and final goods, we test whether RTAs and trade facilitation boost Arab agro-food intra-regional trade. Trade facilitation is measured by the time it takes to export and import, as reported in the World Bank’s Doing Business surveys (World Bank, 2018).

The remainder of this article is organized as follows. The next section presents an overview of trade patterns in the region for both overall and intermediate trade. This is followed by the sections on data and methodology, and the interpretation and discussion of the results; the final section concludes the study.

Patterns of Intra-Arab Trade in the Agro-Food Sector

Overall and Agro-Food Trade

Numerous studies have pointed to the low level of intra-regional trade in the Arab region, in comparison with other regional groupings, despite several initiatives to promote regional integration (Abedini & Péridy, 2008; Al-Atrash & Yousef, 2006; Behar & Freund, 2011; ESCWA, 2014; Organisation for Economic Co-operation and Development [OECD], 2018). Arab intra-regional trade as a share of Arab total exports to the world stood at 12% in 2018 and has shown little growth over the past 20 years (International Trade Center [ITC], 2020). This compares unfavorably with other groupings, such as the European Union (EU), where intra-regional trade accounts for more than two thirds of the overall EU trade (OECD, 2018).

Whereas overall Arab intra-regional trade remained comparatively low, Arab agro-food intra-regional trade showed stronger intensity (Figure 1). Intra-Arab agro-food exports as a percentage of overall Arab agro-food exports accounts for more than 50% and has remained nearly so for the past 20 years. This suggests that, with greater trade facilitation measures reducing trade cost, agro-food trade could be a potential driver of stronger regional integration leading to the development of regional production networks (ESCAP, 2015).

Arab agro-food intra-regional trade (%).

Composition of Intra-Arab Agro-Food Trade

The composition of the intra-Arab agro-food trade provides insights into changes in regional consumption patterns as well as changes in revealed regional comparative advantages. Fruits and vegetables, dairy products, cereals, and sugar products constituted more than two thirds of the total intra-Arab agro-food trade in 2016 (Figure 2). Other products such as meat and meat preparations, fish and fish preparations, coffee, and tea are also important traded components, but their shares do not individually exceed 6%. Intra-Arab agro-food trade witnessed some diversification compared with that in 2007, as the share of the predominant categories (fruit and vegetables, dairy products) fell and the share of other food categories rose significantly, although from a smaller base. The share of cereals and sugar products increased from approximately 7% in 2007 to 10% in 2016, whereas the share of beverages fell considerably from 9.7% to 3.4% during the same period.

Structure of intra-Arab agro-food trade.

The structural changes in the composition of intra-regional trade over the years may be indicative of changes in the patterns as well as the competitiveness of Arab trade. Appendices A and B present the revealed comparative advantage (RCA) and trade intensity indices calculated for the Arab region during the period 2007-2016. The Arab region’s comparative advantage seems to be quite robust for dairy and eggs, vegetables and fruits, and sugar products, as indicated by an RCA larger than 1 in 9 years during a 10-year period. In addition, the region gained comparative advantage in recent years for fish and vegetable oil products. On the contrary, Arab intra-regional trade was quite intensive for all commodities throughout the past 10 years, as indicated by the large TI index (greater than 1) shown in Appendix B. Comparatively, meat, fruits and vegetables, and dairy and eggs showed greater intra-regional trade intensity than other products.

Trade in Intermediates in Agro-Food Products

There are two approaches to measuring trade in intermediates: The first is to use the trade in value-added database, which is based on input-output tables providing the value of foreign inputs used in the production of goods and services. The second is the BEC’s classification (provided by United Nations Comtrade), which breaks down the trade flows of goods according to their use, indicating whether the product is for industrial use (intermediates) or for household consumption. In the context of this study, the Comtrade BEC classification is used as it provides bilateral trade flows and covers nearly all trading partners, including the Arab countries.

The BEC classification breaks down the food and beverage groups (Code 1) into primary (11) and processed product categories (12). The primary products are classified into products “mainly for industry-use” (111) and products for household consumption (112). The processed products are classified in a similar fashion (121 and 122). The “mainly for industry use” products are considered to be intermediates, whereas the household consumption products are the final goods.

Data indicate that, on average, during 2007-2016, about 66% of agro-food intra-regional trade in the region comprised processed products, whereas the remaining (34%) was traded as primary products (ITC, 2020). The share of intra-regional trade in agro-food intermediates (industry use) amounted to an average of 12.5%, changing little over the 2007-2016 period (Figure 3). The proportion of agro-food intermediates trade in the Arab region’s trade is relatively low compared with that of global intermediates trade in agro-food products. For example, the share of intermediate exports for primary agriculture and processed food within the Asia-Pacific economies is 58% and 61%, respectively, in 2013 (Asia-Pacific Trade and Investment Report, 2015).

Arab agro-food intra-regional trade according to end use (2007–2016).

The Determinants of Bilateral Trade in Agro-Food Intermediates

The Model

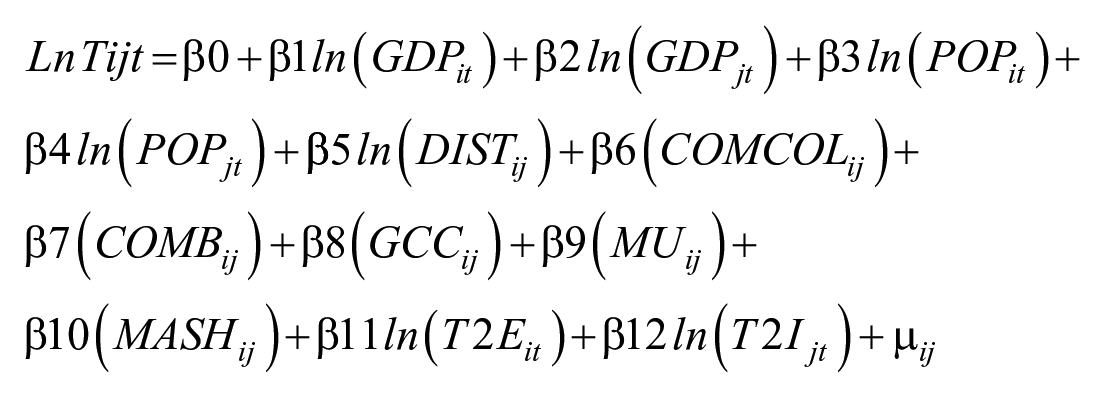

The gravity model in international trade is the most common econometric model used to explain the determinants of bilateral trade among countries. The model postulates that (bilateral) trade between two countries is positively affected by the size of their GDP and inversely proportional to the geographical distance between them. Empirically, the model has performed very well in fitting trade data and has become, for a long time, the workhorse of international trade analysis (Yotov et al., 2016). It has been employed and augmented in several ways to estimate the effect of regional integration, foreign direct investment (FDI) flows, trade facilitation, currency unions, and other related issues. The gravity model was shown to be deeply rooted in traditional and new trade theory, including the Heckscher–Ohlin model, the monopolistic trade-based model, and trade in differentiated goods with firm heterogeneity (Anderson, 1979). Empirically, Anderson and Van Wincoop (2003) were the first to develop a theory-consistent model that efficiently estimate a gravity equation and use the same to conduct comparative statics analysis on the effect of trade barriers on trade flows. The theory was enhanced by adding a multilateral resistant variable that reflects the average distance of a country from all other countries. In the more recent literature, the gravity model was applied to a variety of trade issues, including trade integration patterns (Rasoulinezhad & Jabalameli, 2018; Rasoulinezhad et al., 2020), energy exports (Rasoulinezhad & Jabalameli, 2019), agro-food exports (Crescimanno et al., 2013), and fishery exports (Bose et al., 2019).

Following the literature, the model to be estimated in this study takes the following empirical form:

where

The time-to-export and time-to-import are indicators of trade facilitation, as reported in the World Bank Doing Business reports: the time associated with exporting and importing cargo in a 20-ft, full container load by sea transport. The time required to complete the export or import process accounts for document preparation, customs clearance, inland transport, as well as port and terminal handlings.

Gravity models are commonly estimated in log-transformed multiplicative models using the classical linear estimation method, including panel data methods such as fixed effects (FE) and random effects (RE) models. However, log transformation has been increasingly criticized for its inefficiency in the presence of both heteroscedasticity and zero trade data, which are very common in bilateral trade (Silva & Tenreyro, 2006). Silva and Tenreyro (2006) showed that heteroscedasticity is quite prevalent in the logarithmic transformed data of international trade. They also showed that, in the presence of heteroscedasticity, the assumption of the independence of the error term from the regressors is violated, leading to inconsistent estimator. Because of these issues, Silva and Tenreyro (2006) suggested estimating the model in its multiplicative form using nonlinear methods such as the Poisson pseudo-maximum likelihood (PPML) approach, which provides consistent estimates of the original nonlinear model and has a number of desired properties useful for applied policy research (ESCAP, 2015).

Data Set and Sources

The data set includes a panel of bilateral trade data for 22 Arab countries for the 10 years covering the period 2007-2016. The list and subregional groupings are shown in Appendix C. Data on agro-food intermediate exports were compiled from the World Integrated Trade Solution (WITS)/COMTRADE database using BEC classification (Table 1). Data on GDP and population are from the World Bank, whereas data for geographical proximities (distance, common border, and colony) are from the Center d’Études Prospectives et d’Informations Internationales (CEPII) database. Data on country membership in RTAs were obtained from the WTO (WTO) Regional Trade Agreements Information System (RTA-IS) portal. Finally, trade facilitation indicators were obtained from the World Bank Doing Business reports.

Broad Economic Category (BEC) Classification for Agro-Food Products.

Source. Comtrade.

Results and Analysis

The results were obtained using various panel estimation techniques (pooled ordinary least squares [OLS], FE, RE, and PPML estimators). However, the Hausman test indicates that the RE model is more appropriate than the FE or OLS models. Table 2 reports the results of the RE model as well as the PPML estimators, given the various estimation advantages provided by the latter, especially in relation to bilateral zero trade.

Gravity Estimates for Intermediates Agro-Food Products.

Note. Standard errors are in parentheses. RE = random effects; PPML = Poisson pseudo-maximum likelihood; MU = Maghreb Union trade bloc; MASH = Mashreq trade bloc.

p < .05. **p < .01.

Economic Size and Demographic Variable Effects

The first general comment regarding these results is the small and largely nonsignificant effect of the exporting country’s GDP on intermediate goods trade, particularly the primary products. This does not follow the common gravity literature dealing with final goods trade, but is compatible with the development literature that reveals a switching trade structure with economic growth. As countries develop and the GDP increases, country export patterns switch to processed and more sophisticated value-added products and less of primary products. These results are compatible with Baldwin and Taglioni (2011), who found a low explanatory power for GDP for intermediate trade in the context of trade flows within GVCs. The importing country’s GDP, on the contrary, exerts a significant and positive effect on its exports, indicating that, as the level of income increases, the demand for primary inputs for further processing increases. The population variable effect is more in line with the traditional literature (significant and positive), indicating, for both primary and processed intermediates, that countries that are larger and more populous trade more with each other, thereby supporting the hypothesis that population is a trade facilitator (economy of scale effect). This is in contradiction to the “absorption effect” hypothesis where countries with larger population export less to satisfy large domestic demand (Nuroğlu, 2010; Zarzoso & Lehmann, 2003).

The coefficients of the distance variable have a negative sign, as expected, and are highly significant for both primary and processed intermediates. The distance represents a natural barrier and increases the trade cost between trading partners. The RE model estimates showed a higher impact for distance, than that of PPML, for both products. This finding is compatible with the results of Silva and Tenreyro (2006), who noticed that the distance elasticity is substantially lower under PPML, compared with OLS panel data FE and RE estimators. Primary agro-food input trade is more sensitive to distance than that of processed intermediates, as shown by the higher negative coefficient estimate. This is explained by the perishability of primary agricultural products and their sensitivity to time as they reach their final destination (Ebeke & Etoundi, 2016). Similar results were obtained by Ghazalian (2014), who examined the effects of geographic distance on primary and processed food trade among OECD countries.

Subregional Trade Arrangement Effects

The common economic argument for contracting RTAs is to expand intra-regional trade as a “stepping stone” to global integration. However, empirical evidence for this argument is ambiguous as many studies have shown little response of intra-regional trade to RTAs, particularly for south-south RTAs (Pant & Paul, 2018). The results of this study show that the formation of trade blocs in the Arab region is either not significant or has a negative impact on intra-regional trade (Mashreq and Maghreb trade blocs). These findings, although not easy to interpret, are consistent with the literature on integration of the Arab region (Abu Hatab, 2015; Hoekman, 2016; World Bank, 2013). Factors such as similar production structure, high trade costs, and low commitments to regional integration are identified in the literature as reasons explaining the low performance in Arab regional trade (World Bank, 2013).

However, in contrast to the Mashreq and Maghreb subregions, the effect of the GCC arrangement is positive and significant for promoting intermediate intra-regional trade (PPML model) for processed food, but not for primary products. This indicates that the GCC trade arrangement was more favorable to intra-regional trade in agro-processed products than trade in primary products. The higher performance of the GCC subregional arrangement is due to its deeper form of integration (through the Common Market), which has led to a significant increase in the flows of trade and capital among the members of GCC countries (World Bank, 2013). Heavy investment in logistics has helped some regional cities like Dubai to emerge as a major food reexporting hub, becoming a significant link in the region’s food chain (Oxford Business Group, 2014). About half of United Arab Emirates (UAE) import value is reexported to the region. According to our estimates, the GCC trade arrangement has increased intra-regional trade in agro-processed intermediates by 553% ([1.876 – 1] * 100), including reexports.

Trade Facilitation Effect

The estimated coefficients for both T2E and T2I are highly significant and have the expected negative sign, indicating that a longer time to export or import negatively affects bilateral trade. The time to export for processed products affects bilateral trade more than the time to import. The T2E coefficient is higher than unity for processed products, indicating that the value of exports would decrease by a higher percentage for every percent increase in the time to export between trading partners. The value of processed product exports would decrease by about 1% to 1.4% for every percent increase in time to export and by 0.3% to 0.4% in time to import. These results are in line with studies such as Djankov et al. (2010), who found that trade would be reduced by at least 1% for each additional day of delay for a product prior to being shipped. Similarly, Wolde and Bhattacharya (2010) argued that exports of the Middle East and North Africa (MENA) region to the world would increase by 11% if the average number of days taken for customs clearance was reduced to the world-average level. They find that imports increase by 30% if import clearance time is reduced to the world-average level.

These results underscore the necessity for Arab countries to improve the quality and performance of logistics as well as custom clearance procedures. The survey report by ESCWA (2017) shows that the level of implementation of trade facilitation in Arab economies, relative to the best practices, ranges from 30% to 71%, and is highly dependent on the state income level. In other words, high-income Arab countries are able to achieve a high standard of trade facilitation, particularly in the GCC region. The report also points out the differences in performance among Arab countries, especially in “cross-border paperless trade,” and calls for reducing the formalities associated with them. The World Bank Doing Business survey published in 2018 classifies most of the Arab countries as poor performers in terms of the time and cost of documentary and border compliance procedures.

The results of our study reveal that the time effects on agro-food exports (processed and primary) are greater in magnitude than those found in literature (Djankov et al., 2010; Freund & Rocha, 2011; Hummels, 2001). This is expected, as most studies were concerned with the time effect in the final products rather than in the intermediates. Intermediate products are traded within global and RVCs, and timeliness plays an important role in the just-in-time needs of production networks (Lanz & Piermartini, 2010). Improving trade facilitation by reducing export time delays would facilitate the integration of GVCs and regional production networks, particularly for time-sensitive agro-food products.

Conclusion and Policy Implications

This article highlighted the role of regional trade integration and trade facilitation in boosting or hindering bilateral trade, in addition to other intra-regional trade determinants.

Results from a gravity model show that time to export and import as a cross-border cost measure negatively and significantly affects regional bilateral trade in agro-food intermediates. It is estimated that the value of processed product exports would decrease by about 1.0% to 1.4% for every percent increase in the time to export, compared with about 0.3% to 0.4% in the time to import. This is consistent with the findings in existing literature that trade would be reduced by at least 1% for each additional day’s delay for a product prior to being shipped. This implies that the Arab countries should focus on improving the quality and performance of logistics as well as the customs clearance procedures. This has become even more pertinent, given that most Arab countries have fared poorly in terms of cross-border trade indicators, highlighting the need for simplifying the border compliance procedures for exports.

The results also indicate that, among the regional trade blocs, only the GCC trade arrangement had a positive and significant effect on subregional trade. This also supports the literature on Arab regional integration, which argues that high trade costs and low commitments to regional trade, among other things, hinder trade performance in the region. Its integration model, which in addition to tariff barriers has abolished most nontariff barriers and permits easy access to investment capital to upgrade its trade, port, and transport logistics, explains the better trade performance of the GCC region.

The development of RVCs is quite sensitive to time and transaction costs as efficiency requires the quick movement of intermediate inputs for further processing and value addition. Reducing trade costs through better regional connectivity would help build trade corridors and enhance RVCs.

Although most of the results of this study are in line with the literature on regional trade integration and trade in intermediates, listing some limitations of the study is in order. First, there is the issue of the causal link between RTAs and trade flows (endogeneity), which is inherent to all gravity-based studies and could affect the econometric estimates. Second, analysis of trade in intermediates could be enhanced by using the more detailed data on trade in value-added rather than the BEC of Comtrade. This is the subject of further research as the data on trade in value-added for Arab countries become available. Finally, structural shocks such as the Arab spring are not considered in the gravity model of this study due to the limited time series data.

Footnotes

Appendix A

RCA Index for the Arab Region in Selected Agro-Food Commodities.

| Product | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|---|---|---|---|

| Meat | 0.10 | 0.10 | 0.14 | 0.11 | 0.12 | 0.15 | 0.15 | 0.15 | 0.31 | 0.29 |

| Fruit and veg. | 0.40 | 0.90 | 1.38 | 1.22 | 1.05 | 1.12 | 1.17 | 1.19 | 1.76 | 1.77 |

| Dairy and eggs | 0.45 | 0.79 | 1.45 | 1.13 | 1.06 | 1.29 | 1.34 | 1.25 | 1.81 | 1.81 |

| Cereal | 0.12 | 0.32 | 0.62 | 0.46 | 0.32 | 0.44 | 0.55 | 0.46 | 0.64 | 0.63 |

| Veg. oils | 0.24 | 1.29 | 1.09 | 0.59 | 0.75 | 0.98 | 1.08 | 0.87 | 1.74 | 1.34 |

| Sugar | 0.88 | 1.31 | 1.17 | 1.34 | 1.06 | 1.25 | 1.57 | 1.49 | 1.96 | 2.15 |

| Fish | 0.05 | 0.15 | 0.29 | 0.26 | 0.42 | 0.48 | 0.40 | 0.43 | 1.15 | 1.37 |

Source. Author’s calculations using World Integrated Trade Solution (WITS)/Comtrade data.

Note. RCA index is calculated as follows:

Appendix B

TI of the Arab Intra-Regional Trade in Selected Agro-Food Products.

| Product | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 |

|---|---|---|---|---|---|---|---|---|---|---|

| Meat | 44.89 | 14.79 | 13.38 | 11.20 | 11.99 | 11.36 | 11.55 | 12.74 | 10.66 | 11.88 |

| Fruit and veg. | 21.63 | 13.16 | 10.98 | 10.70 | 11.21 | 10.89 | 11.00 | 10.57 | 7.85 | 8.16 |

| Dairy and eggs | 12.00 | 9.37 | 8.77 | 8.59 | 9.25 | 8.56 | 8.78 | 7.97 | 7.89 | 8.58 |

| Cereal | 5.67 | 4.99 | 5.66 | 5.01 | 4.64 | 5.40 | 4.84 | 5.37 | 5.63 | 5.74 |

| Veg. oils | 11.60 | 4.13 | 4.84 | 4.92 | 5.10 | 5.53 | 4.87 | 5.29 | 3.07 | 4.44 |

| Sugar | 12.48 | 5.04 | 3.99 | 3.62 | 3.41 | 3.75 | 4.03 | 4.11 | 3.90 | 3.78 |

| Fish | 22.37 | 7.83 | 13.18 | 12.07 | 9.00 | 7.58 | 11.00 | 10.49 | 5.02 | 3.78 |

Source. Author’s calculation using World Integrated Trade Solution (WITS)/Comtrade data.

Note.

Appendix C

List of Arab Countries Include in the Econometric Analysis.

| In | Mashreq | Maghreb | Others |

|---|---|---|---|

| Oman | Egypt | Tunisia | Sudan |

| Qatar | Iraq | Morocco | Yemen |

| Kuwait | Jordan | Algeria | Djibouti |

| United Arab Emirates (UAE) | Syria | Libya | Comoros |

| Saudi Arabia | Lebanon | Mauritania | |

| Bahrain | Palestine |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.