Abstract

In this study, we used the probit model to find out the determinants of access to formal credit and then we applied the Cobb–Douglas production function to examine the impact of formal credit on sugarcane productivity. To elicit the choice and consequence of sugarcane productivity, we divided the farmers into two groups: borrowers and nonborrowers. A total sample comprised 120 sugarcane growers from Badin District—rich in sugarcane production—Sindh, Pakistan. For analysis purposes, we used a binary-choice probit model that reveals significantly positive relationship between access to formal credit and farmer’s education level, landholding size, farming experience, and household size. The main driver to access formal credit is landholding because it is used as collateral against the loan. The age of the farmers, which was found negative and significant, shows that aged farmers are risk-averse and reluctant to access credit. The results of Cobb–Douglas production function affirm significantly positive impact of formal credit on sugarcane productivity. The credit access and use in the production process can enhance the crop production and overall income of the farmers. Therefore, secure and timely availability of crop-specific credit can help the farmers to use inputs in a timely and recommended manner.

Introduction

Pakistan is predominantly agriculture and rural-based and the contribution of agriculture to gross domestic product (GDP) is 19.5% and employment engaged in agriculture is 42.3% (Government of Pakistan [GOP], 2017). Agriculture provides livelihood to 68% of rural dwellers in Pakistan (GOP, 2017; Rehman et al., 2015). Credit has a vital role and is considered an instrument for any business, which is traditionally used as a nonmonetary activity for a large portion of population of Pakistan that is engaged directly or indirectly in the agriculture-related activities (Aslam, 2016; Bashir et al., 2007; Jan et al., 2017; Rehman et al., 2017). Credit is a financial help to the smallholder farmers to fulfill the cash requirement of main agricultural inputs used in production process (Abdallah, 2016; Adjognon et al., 2017; Afrin et al., 2017; Akudugu, 2016).

It has been observed in rural Pakistan, in particular, Sindh, that most of the farmers are resource-deficient and faced liquidity constraints with buying necessary inputs. Therefore, in these circumstances, agriculture loan is essential to cultivate the next crop (Chandio et al., 2016, 2018; Saqib et al., 2016; Saqib, Kuwornu, Ahmad, & Panezai, 2018). Agricultural credit distribution sources are divided into formal and informal. Informal credit sources include fellow farmers, professional money lenders, shopkeepers, input suppliers, friends, relatives, and so on, whereas formal credit sources contain Zarai Taraqiati Bank Limited (ZTBL), Cooperatives, Domestic Private Banks (DPBs), Commercial Banks (CBs), and Microfinance Banks (MBs; Chandio et al., 2017; Hussain & Thapa, 2012; Jan & Khan, 2012; Nouman et al., 2013). These credit sources provide agricultural loans such as production loan and development loan to smallholder farmers for cash requirement of main agricultural inputs and contribute a significant role in the growth and the development of the rural economy. Secure and timely accessibility of formal credit is considered a productive change from informal agricultural credit market to formal rural credit market (Jan & Khan, 2012; Kumar, 2013; Saqib, Kuwornu, Ahmad, & Panezai, 2018; Saqib, Kuwornu, Panezai, & Ali, 2018).

Small-scale farmers in Pakistan are facing severe challenges, including several economic, technical, and social issues. In particular, for the sugarcane growers, the high needs for farm inputs and low access to institutional credit are primary problems. New policy implementation from the GOP for the improvement of farm production and food security has provided easy access to agricultural credit to the smallholder farmers. These policies had little success in addressing the farmer’s needs for a loan (Fayaz et al., 2006; Hussain & Thapa, 2012; Iqbal et al., 2003; Khandker & Faruqee, 2003; Rehman et al., 2017; Saqib et al., 2016).

In the previous studies, yet there is no work done to see the effect of formal agricultural credit on crop productivity in Pakistan. In this regard, only limited research conducted by Bashir et al. (2007) found a positive and significant effect on sugarcane productivity. Similarly, Javed et al. (2006) found the impact of credit positive and significant on wheat and sugarcane crop in Punjab. A recent study by Rehman et al. (2017) shows that the total food production and loan disbursed by ZTBL have a positive correlation with agricultural GDP. Saqib et al. (2016) found that access to formal credit in Pakistan is entirely squeezed and inequitable. Large farmers have more access and use to formal credit due to more reliable collateral availability.

Similarly, Chandio et al. (2017) found off-farm income and land availability as the foremost collateral determinants of access to credit. Therefore, we design this study to answer the question, “Does formal credit enhance sugarcane crop productivity?” We address this question in the following manner: At the first step, we answer the accessibility of credit and its determinants. In the second step, we explain the problem of the use of agriculture credit for crop productivity. We expect this micro-level study helps the policymakers to design crop-specific credit access and use policy in the future in particular to Sindh.

Agricultural Credit Distribution by ZTBL in Pakistan

In the year 2016–2017, agriculture lending institutes disbursed PKR473.1 billion to the farmers of Pakistan. The objective of the government is to enhance agriculture production and use agriculture credit as an instrument to achieve such goals. In 1951, the Zarai Taraqiati Bank Limited (ZTBL) was established and this bank is the first agricultural bank of Pakistan that provides different farm and nonfarm agricultural credit schemes such as Kissan Dost loan scheme, Asan Qarza loan scheme, Sada Bahar loan scheme, One Window Operation loan scheme, Awami Zarai scheme, Shamsi Tawanai loan scheme (solar pumps), Rural Development loan scheme, and Crop Loan insurance scheme for the development of farming sector. The ZTBL is the leading player among the credit disbursement institutions and simultaneously performs the function in all over Pakistan. Province-wise agricultural credit disbursed by ZTBL is reported in Table 1. At the country level, the ZTBL disbursed PKR78,772.3 million in 2016–2017. Of the total amount of credit, Punjab received the highest amount of credit of PKR65,628.7 million compared with Sindh and other provinces of Pakistan. The share of credit to Sindh province reduced from 13.17% to 11.31% and the share of Punjab province increased from 81.40% to 82.82% in 2015–2016. Sindh stands on the second position in the province list, but unfortunately, the credit disbursement in Sindh province is not encouraging. In rural Sindh, limited access to agriculture credit is attributed to lack of collateral, lack of land ownership, and low income level for small farmers. Large farmers have greater access to formal agriculture credit due to significant landholdings, political influence, and connections with bank managers. However, literature has accepted the importance of agriculture credit in productivity both in developed and in developing countries (Abdallah, 2016; Adjognon et al., 2017; Afrin et al., 2017; Khandker & Faruqee, 2003; Kumar, 2013; Thirtle et al., 2005).

Credit Disbursed by ZTBL in Pakistan (PKR Million).

Source. Government of Pakistan (2017).

Note. Percentages are calculated by authors. PKR denotes Pakistani rupees and KPK represents Khyber Pakhtunkhwa.

Sugarcane Status—Province Wise

The total area under crops is 22.63 million hectares. Sugarcane is a major Kharif crop, which is sown in monsoon season from April/May to October/November. The sugarcane production is contributing 0.7% to the GDP and 3.4% to agriculture value added (GOP, 2017). The total cultivated area under sugarcane crop during 2016–2017 was 1,217,000 hectare that has increased to 1,131,000 hectare compared with the previous year 2015–2016. The total sugarcane production and yield have also gradually increased from 73,607,000 tons and 60,428 kg/hectare to 65,482,000 tons and 57,897 kg/hectare compared with the previous year 2015–2016 (GOP, 2017). The sugar industry is one of the leading enterprises of Pakistan after the textile industry (Habib et al., 2014; Memon et al., 2010; Rehman et al., 2016; Yasar et al., 2015). This industry is dependent upon sugarcane to produce sugar and sugar-related products (Rehman et al., 2016). Pakistan has devoted the largest cultivated area to sugarcane cultivation, which stands at fifth area-wise, 11th in production, and, however, yield wise at 60th (Nazir et al., 2013). Figures 1 to 3 demonstrated province-wise land area under sugarcane crop, yield, and production from 2006–2007 to 2015–2016. The area under sugarcane crop is low in Sindh. In addition, the yield gap difference shows the farmers need funds to use appropriate technology to enhance the productivity of the sugarcane.

Province-wise area under sugarcane crop in Pakistan.

Province-wise yield of sugarcane in Pakistan.

Province-wise sugarcane production in Pakistan.

Method

Study Area

We conducted the present study in the Badin district of Sindh, Pakistan. The prime chunk of the population is rural and dependent upon agriculture. Farmers mainly grow sugarcane, rice, tomato, and wheat.

Data Collection

To fulfill the study objectives, we conducted a field survey in the district to collect information about sugarcane production and agriculture credit use. We selected the district due to the high frequency of sugarcane producers. We use a multistage random sampling technique: At first stage, we selected Taluka Matli (subdistrict); at second stage, three dehs, that is, Alipur, Nazarpur, and Ghari Bhiri picked out from Taluka Matli; and in the last stage, two villages from each deh; 10 loanee and 10 nonloanee sugarcane growers were randomly selected. Thus, in total, 120 sugarcane growers have been personally interviewed through a detailed questionnaire. Data collected on sugarcane growers include demographic variables such as age and household size, social variables such as education and farming experience, economic variables such as household size and landholding size, and contextual variable such as credit availability. Moreover, regarding the cost of farming inputs, the cost of improved seed used, fertilizer cost, irrigation charges, and plant protection cost were also collected from sugarcane growers.

Analytical Framework

In this study, we employed the probit and the Cobb–Douglas production function models to establish determinants of formal agricultural credit access and its impact on sugarcane productivity. The implicit and explicit forms of both models were used to determine the effect of the sugarcane growers’ demographic and socioeconomic factors:

where FCRA (formal credit access) is a binary (choice) variable that is equal to 1 for the sugarcane grower who accessed formal credit and 0 otherwise. That is,

and AGE is age of sugarcane growers’ (years), EDU is education level of sugarcane growers’ (years), HHSIZE is household size of sugarcane growers’ (members), FAEXP is farming experience (years), LHSIZE is landholding size (acres),

Cobb–Douglas production function is as follows:

where

We applied the Cobb–Douglas production function method to determine the following equation from existing literature (Ahmed et al., 2014; Bashir et al., 2007; Chandio et al., 2016, 2018; Javed et al., 2006; Nazir et al., 2013).

Equation 3 can also be written as follows:

We formulated the hypothesis to test the effects of formal agricultural credit on the productivity of sugarcane crop in the study area:

Results and Discussion

Socioeconomic Characteristics of the Sugarcane Growers

Table 2 reports the frequency distribution of education levels of borrowers and nonborrowers in the study and shows the majority of sugarcane growers in both categories of education level: 24 credit users (40%) had 5 years of education, whereas 18 noncredit users (30%) had 5 years of education. On the contrary, 20 borrowers (33.3%) had 10 years of education, whereas 17 nonborrowers (28.3%) had the same category of education level. The results are on par with Ayaz et al. (2011).

Distribution of Education Level of Sugarcane Growers.

Source. Authors’ calculations (2017).

Generally, it assumed that a farmer’s efficiency increased with the increase in experience (Olagunju & Adeyemo, 2007). Table 3 shows that 30 creditors (50%) had farming experience in the range of 15 to 20 years, whereas 25 noncreditors (41.7%) belonged to this category. Results further indicate that 36.7% of noncreditors had 21 to 30 years of farming experience in the study area, whereas 26.7% creditors belonged to the same category.

Distribution of Farming Experience of Sugarcane Growers.

Source. Authors’ calculations (2017).

Results presented in Table 4 revealed the distribution of household size of creditors and noncreditors that majority of sugarcane growers (creditors and noncreditors) in both categories had large family size, 31 creditors (51.7%) and 25 noncreditors (41.7%), falling within the range of six to 10 family members although this number is small in the case of noncredit user.

Distribution of Household Size of Sugarcane Growers.

Source. Authors’ calculations (2017).

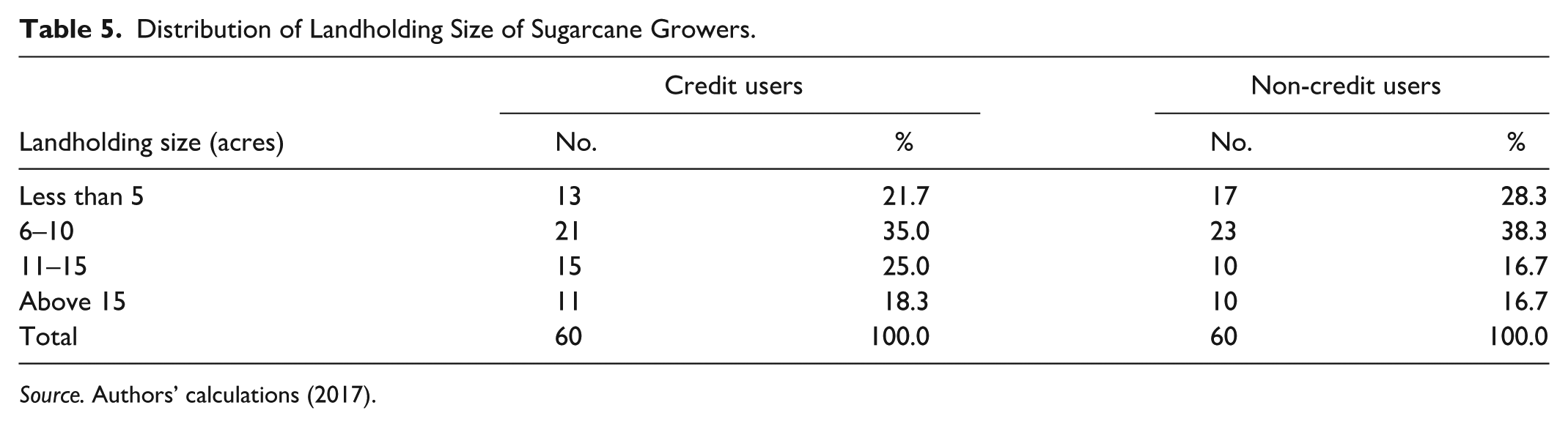

The landholding size is a significant contributor to the access credit formal sector (Duniya & Adinah, 2015; Hussain & Thapa, 2012; Ugwumba & Omojola, 2013). Table 5 presents the results of landholding size and shows that the majority of the noncreditors (23 [38.3%]) had within the range of 6 to 10 acres, whereas 21 (35%) of creditors belonged to this category. On the contrary, 17 (28.3%) of nonborrowers has less than 5 acres of landholding size, whereas 13 (21.7%) of borrowers had the same landholding size.

Distribution of Landholding Size of Sugarcane Growers.

Source. Authors’ calculations (2017).

Descriptive Analysis

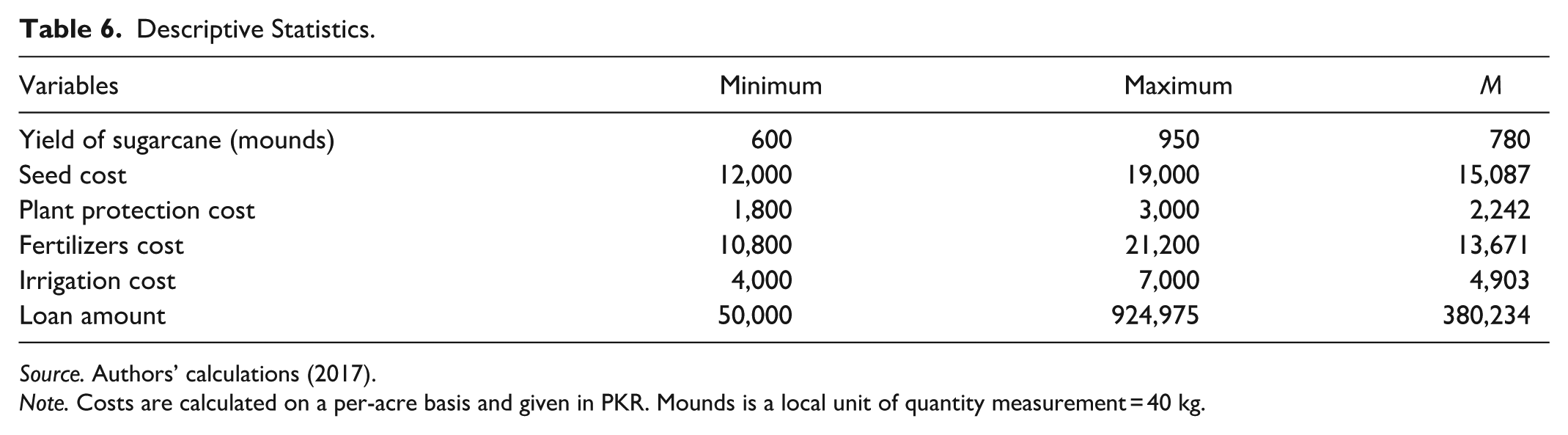

We presented a summary of the descriptive statistics in Table 6. The average yield of sugarcane per acre reported by selected respondents was 780 mounds, whereas the average seed cost of sugarcane reported by growers was PKR15,087 mounds per acre. Furthermore, the chemical cost spent by sugarcane growers in the study area reported the mean value of PKR 2,242 per acre. Moreover, the mean cost of fertilizers in terms of nutrient bags per acre was PKR 13,671. Also, the average cost of irrigation, including tube well and canal water per acre, reported by selected respondents was PKR 4,903. Finally, the maximum amount of loans taken by any of the sample respondents was PKR 924,975 with a mean value of PKR 380,234.

Descriptive Statistics.

Source. Authors’ calculations (2017).

Note. Costs are calculated on a per-acre basis and given in PKR. Mounds is a local unit of quantity measurement = 40 kg.

Empirical Results

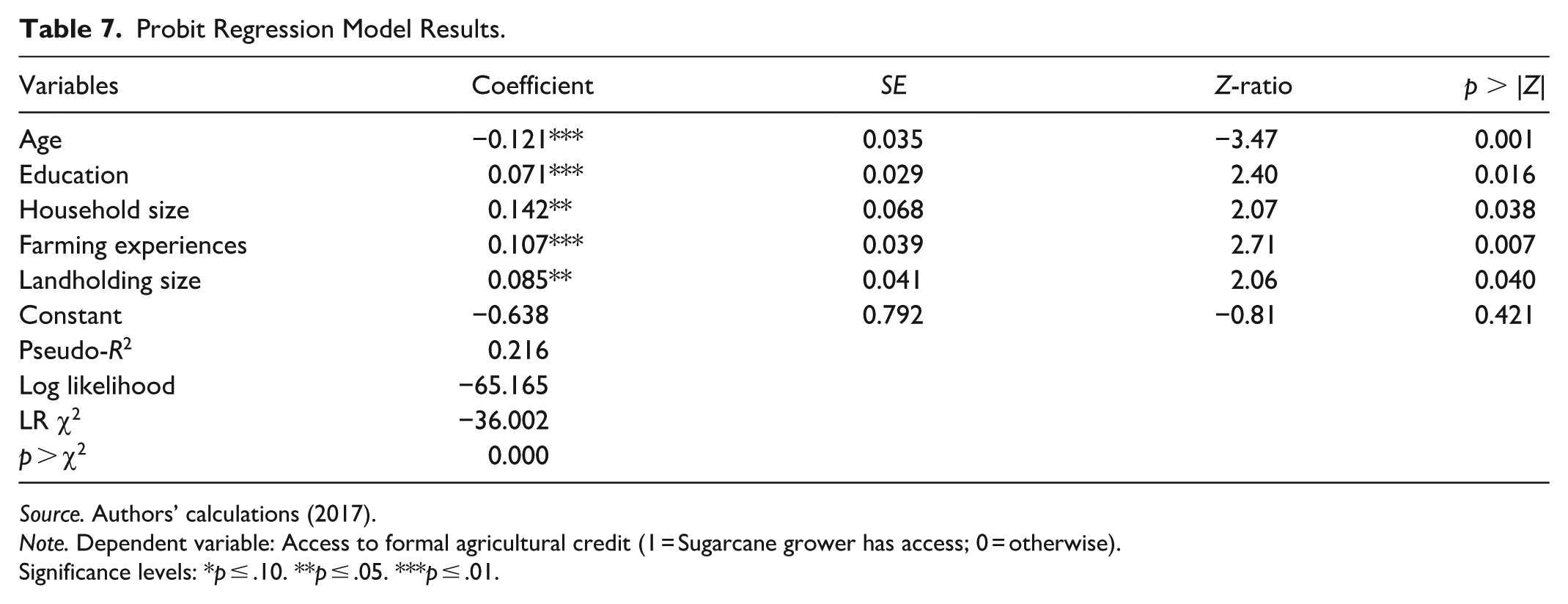

We provided the probit model results in Table 7. Our outcome variable is binary (0 and 1) and the predictors are age, formal education, farming experience, household size, and landholding size. We found age is negative and significant at a level of significance (p ≤ .01). The other predictors were found positive and significant at a level of significance (p ≤ .01). We provided the probit model summary at the bottom of the table.

Probit Regression Model Results.

Source. Authors’ calculations (2017).

Note. Dependent variable: Access to formal agricultural credit (1 = Sugarcane grower has access; 0 = otherwise).

Significance levels: *p ≤ .10. **p ≤ .05. ***p ≤ .01.

The estimated coefficient of age (β1 = −0.121) has a significant and negative association with access to credit. It attributes that an increase in the age of the sugarcane grower decreases the predicted probability of accessing formal credit. Similar kinds of results were reported in the literature by Denkyirah et al. (2016), Khoi et al. (2013), Saqib et al. (2016; Saqib, Kuwornu, Panezai, & Ali, 2018), and Sebopetji and Belete (2009). Formal education has a significant and positive relationship (β2 = 0.071) with access to formal agricultural credit. This result implies that as formal education level increases, the sugarcane growers had more access to institutional agricultural credit. The finding of the study is on par with Li et al. (2011), Saqib et al. (2016; Saqib, Kuwornu, Panezai, & Ali, 2018), and Ugwumba and Omojola (2013). Saqib, Kuwornu, Panezai, and Ali (2018) stated that high educated farmers with secondary education and above have higher access to formal agricultural credit from the formal sources. Li et al. (2011) investigated factors influencing the accessibility of microcredit by rural Chinese households in Hubei province of China by using logistic regression approach. Findings revealed that formal education, self-employment, size of household farmland, and household annual income had significant positive influence on rural Chinese households’ access to microcredit. Likewise, Khoi et al. (2013) examined the socioeconomic factors affecting rural households’ access to credit in Vietnam. The results from the study showed that education, farming experience, agricultural land area, and local government employee were positive and significantly influenced farmers’ access to formal credit.

Likewise, household size has a significant positive interrelationship (β3 = 0.142) with farmers’ access to formal agricultural credit. Moreover, farming experience also has a significant positive association (β4 = 0.107) with access to institutional agriculture credit. This result implies that with having more farming experience, the sugarcane growers had more access to formal agricultural credit.

Finally, landholding size has a significant positive coefficient (β5 = 0.085) with farmers’ access to formal agricultural credit. Therefore, the landholding size is a substantial factor in the sugarcane growers’ access of formal agricultural credit. The results of this study for landholding is consistent with findings of Afrin et al. (2017), Chandio et al. (2017), Dzadze et al. (2012), Hussain and Thapa (2012), Khoi et al. (2013), Sanusi and Adedeji (2010), Saqib et al. (2016; Saqib, Kuwornu, Panezai, & Ali, 2018), and Ugwumba and Omojola (2013).

Besides, we used Cobb–Douglas production function (CDPF) to estimate the coefficients. The results of the regression analysis reported in Table 8.

Cobb–Douglas Production Function Results.

Source. Authors’ estimations (2017).

Note. Costs are calculated on a per-acre basis and given in PKR.

Significance levels: *p ≤ .10. **p ≤ .05. ***p ≤ .01.

The results depicted in Table 8 are used as elasticities of inputs concerning output, in this case, sugarcane output per acre. The seed cost per acre mounds in rupees showed positive (β1 = 0.159) and significant interrelation with the yield of sugarcane. It implies that seed cost has the potential to increase output. Similarly, the coefficients of plant protection and irrigation showed positive (β3 = 0.246 and β4 = 0.182, respectively) and significant association with sugarcane output. These findings are consistent with previous works of Bashir et al. (2007), Habib et al. (2014), Memon et al. (2010), and Nazir et al. (2013).

It is evident that the coefficient of agricultural credit is positive (β5 = 0.203) and highly significant and enhances sugarcane productivity. The findings of this study are consistent with the empirical literature (Abdallah, 2016; Afrin et al., 2017; Ahmed et al., 2014; Asadullah & Rahman, 2009; Bashir et al., 2007; Besharat & Amirahmadi, 2011; Chandio et al., 2018; Hussain, 2013; Kassali et al., 2009).

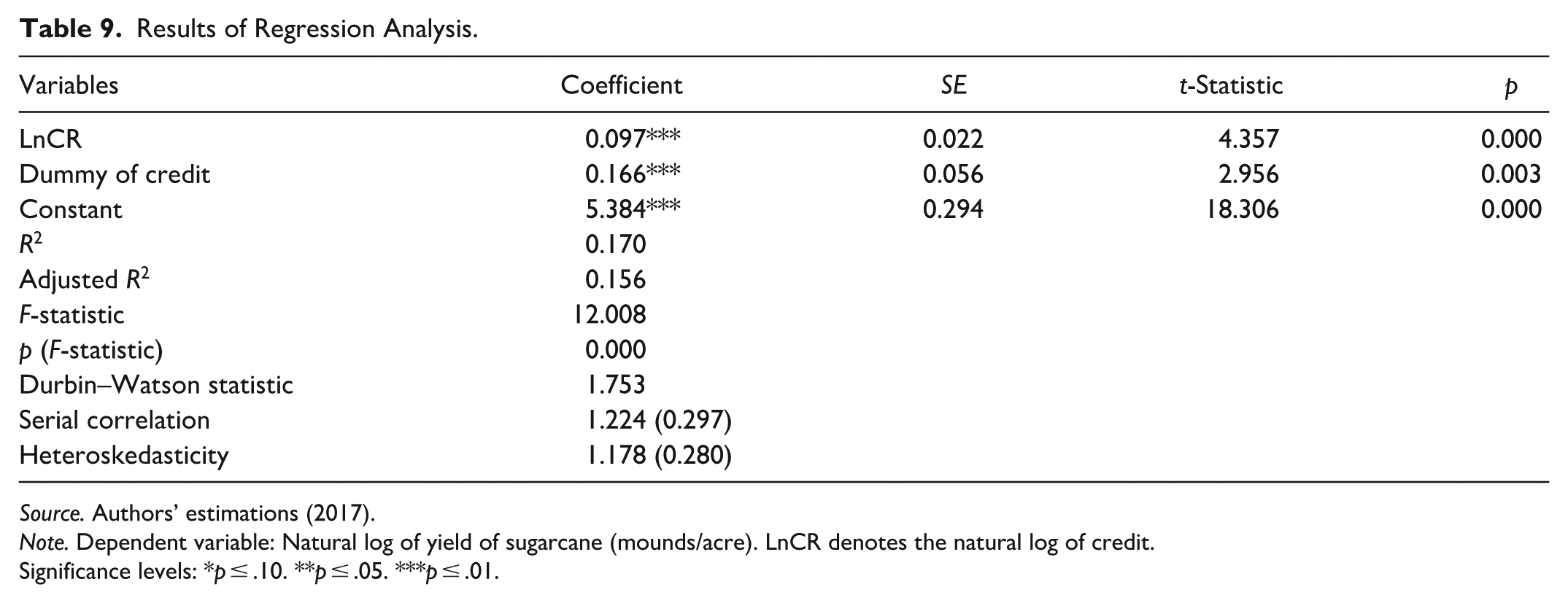

The results of regression analysis are reported in Table 9, indicating that both coefficients of formal agricultural credit have a positive and significant impact on sugarcane yield. The positive and significant interrelationship between formal agricultural credit and sugarcane productivity is consistent with the work of Khandker and Faruqee (2003), which reported that formal agricultural credit helps rural household finance their crop production costs and this, in turn, helps raise their output as well as increase the income, and is related to the study of Akudugu (2011, 2012) who explored that formal agricultural credit enables rural households to confidently invest more in advanced technologies of agricultural production, which help increase their production.

Results of Regression Analysis.

Source. Authors’ estimations (2017).

Note. Dependent variable: Natural log of yield of sugarcane (mounds/acre). LnCR denotes the natural log of credit.

Significance levels: *p ≤ .10. **p ≤ .05. ***p ≤ .01.

In addition, this study used the ordinary least squares (OLS) method to examine the effect of socioeconomic factors on sugarcane productivity in southern Sindh, Pakistan. The estimated outcomes are reported in Table 10. The formal education variable has a positive and significant impact on sugarcane productivity at the 5% level of significance. This result implies that a 1-year increase in formal education of sugarcane growers increases sugarcane productivity by 0.11%. Likewise, farming experience variable has a positive and significant influence on sugarcane productivity at the 5% level of significance. This means a 1-year increase in farming experience enhances sugarcane productivity by 0.12%. Furthermore, landholding size also has a positive and significant effect on sugarcane productivity at the 10% level of significance. This implies that an increase in the landholding size by 1 acre increases sugarcane productivity by 0.10%.

Results of the OLS Model.

Source. Authors’ estimations (2017).

Note. Dependent variable: Natural log of yield of sugarcane (mounds/acre). OLS = ordinary least squares.

Significance levels: *p ≤ .10. **p ≤ .05. ***p ≤ .01.

Conclusion

The present study analyzed the determinants of sugarcane farmers’ access to formal credit in the Badin district of Sindh, Pakistan, by applying the probit model. In addition, this study also examined the impact of formal credit on sugarcane productivity in the same study area by using the Cobb–Douglas production function. The study found that among the socioeconomic determinants, formal education, household size, farming experience, and landholding size were positive and significantly influenced farmers’ access to formal credit. The study concludes that the influence of these socioeconomic determinants should assist as a guide in efficient supply of formal credit through financial institutions to rural farming communities in the future. Furthermore, the study found that formal credit has a significant positive effect on sugarcane productivity. This means that the ZTBL is a leading formal institution and it has been playing a crucial role in supplying the agriculture credit to sugarcane growers in the country. Based on these findings, the study suggests that for further improvements of agricultural credit schemes, ZTBL should supply credit timely during the sowing season of sugarcane crop on relaxed preconditions and must ensure proper utilization of the loan through agriculture credit officers.

Footnotes

Acknowledgements

We are grateful to anonymous reviewers for their valuable comments that helped us to better the quality of this work.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Research on the Mechanism and Path of Rural Land and Finance Integration Development under the Background of “Separation of Three Rights” ReformKey Project of The National Social Science Fund of China, Project Code: 20AJY011.