Abstract

The purpose of this study is to estimate the economic value of intra-industry information transfers within Ghana’s banking industry due to the collapse of seven banks. This is a short-term study with an event window [−10, +10] and an estimation period of 200 trading days. The event study methodology is adopted to estimate the cumulative abnormal return (CAR) gained by other rival industry banks as well as to calculate the cumulative average abnormal return (CAAR) for the entire Ghana Stock Exchange (GSE). The results of the study show that the collapse of the seven banks does convey information that the market uses in revising stock prices. However, most of the rival banks experienced an insignificant share price reaction. This insignificant reaction can be attributed to the fact that GSE is not efficient. The study recommended among others, for the GSE to be reformed to improve the efficiency of the market and secure the flow of information to market participants.

Keywords

Introduction

A strong, well-functioning financial sector is crucial for any economy—be it industrial, emerging market, or even low income. It is essential for healthy, sustained growth. As an economy grows and matures, its financial sector must grow with it. It must be able to meet the increasingly sophisticated demands that are placed on it (Krueger, 2004). According to Duisenberg (2001), the functioning of an economy depends on the financial system of a country. The financial system includes banks as a central entity along with other financial service providers. Baily and Elliott (2013) also assert that the financial system of a country is deeply entrenched in the society and provides employment to a large population. Bakar and Sulong (2018) corroborate the enormous and significant contribution of a financial sector to an economy and postulate that the overall impact of financial sector in an economy is to ensure sustainable growth by helping to mobilize savings and direct funds into production sectors. Haldane and Madouros (2011) provide evidence of the contribution of the financial sector to the U.S. and U.K. economies. For the United States, the value-added of financial intermediaries was about US$1.2 trillion in 2010—equivalent to 8% of total GDP. In the United Kingdom, the value-added of finance was around 10% of GDP in 2009. The trends over time are even more striking as the authors reveal that the contribution of the financial sector to GDP in the United States has increased almost fourfold since the Second World War.

Other studies have been conducted to establish the relationship between the financial sector and the economic growth. For instance, Levine et al. (2000) and Al-Yousif (2002), using panel generalized method of moment (GMM) techniques and traditional cross sections for 71 countries, claimed that, financial development indicators are highly positive and significantly related to economic growth. Apergis et al. (2007) also confirmed a positive relation between finance and growth for both developing and developed regions. Kar et al. (2011) concluded that in MENA (Middle East and North Africa) countries, financial development is a source of growth rate in a period (1980–2007). Generally, Sen and Paul (2017) opine that the banking sector is deemed to be one of the most vital sectors for the economy to be able to function. As such, its importance as the “lifeblood” of economic activity is indisputable.

The same argument can be advanced for Ghana, as Ghana’s banks are regarded as playing a crucial role in driving the nation’s economy (Baah-Nuakoh, 2017). Baah-Nuakoh (2017) further highlights several significant contributions of Ghana’s banks to the nation’s economy. As financial intermediaries, Ghanaian banks channel funds from savers to borrowers, providing customers with the liquidity they need for investment in productive, profitable enterprises. For instance, 58% of Ghanaians had access to formal financial services in 2015, up from 41% in 2010 (The World Bank, 2018). By stimulating savings and investment, the nation’s banks effectively reduce the loss of capital and boost economic growth. Furthermore, the banks currently assist government agencies with linking customers’ bank accounts to national identification databases, house numbers, and street names, so as to facilitate domestic tax collections. In this way, Ghanaian banks are helping to ease the challenges of the nation’s public deficit by guaranteeing a strong, steady flow of government revenue (Baah-Nuakoh, 2017). On the international front, as a member country of the West African Monetary Zone (WAMZ), Ghana is playing a crucial role for a common currency (ECO) to be achieved by WAMZ in 2020 (Taylor, 2018). As such, Ghana’s banking industry is considered as the second largest in the WAMZ and has grown rapidly in the last years (Baoko et al., 2017; GCF, 2016).

Considering the enormous and significant contributions of the financial sector to the growth of Ghana’s economy and other economies of the world, the collapse of the whole financial sector or part of it can trigger devastating spillover effects to other parts of the economy. For instance, the global financial system suffered a profound and traumatic shock in September 2008 when U.S. investment bank Lehman Brothers collapsed (Sraders, 2018). These spillover effects may affect other firms or elements in the same financial sector or outside the financial sector. According to Antwi (2018), the financial sector is susceptible to contagion factors, where a negative occurrence in one institution affects other industry players and possibly the entire industry depending on the influence of the source institution wields over the industry. Consequently, this research focuses on the externalities experienced by other firms due to an occurrence in a peer firm. Such externalities are known as intra-industry information transfers.

In assessing intra-industry information transfers, Tawatnuntachai and D’Mello (1999) report that several studies have been undertaken to establish a relationship between equity value of firms releasing information and that of non-releasing firms within the same industry. Tawatnuntachai and D’Mello (1999) further highlight that intra-industry information transfers can result in net contagion effect (a direct movement between the reaction of the stock price for other companies and that of the announcing company) and net competitive effect (an inverse movement between the reaction of the stock price for other companies and that of the announcing company). A study by S. Chen et al. (2005) cites an example of an intra-industry information transfers to the effect that June 14, 1996, witnessed a drop in the share price of In Focus Systems Inc. by 34% as a result of new product introduced by one of its competitors, Sony Electronics Inc.

In 2017 and 2018, the general public in Ghana was greeted with shocking news to the collapse of seven commercial banks. The Bank of Ghana (BoG) withdrew the licenses of these banks over liquidity challenges, among others. Consequently, there were massive panic withdrawals in other banks by depositors with the fear that the other banks may suffer a similar fate. The events triggered a loss of confidence in Ghana’s financial sector, which led to such a reaction from depositors. Thus, there were extensive commentaries about the social and economic implications of the collapse of these banks on the citizens and the economy in general. For instance, Adombila (2018) reported on August 28, 2018, that about 1,700 jobs would be lost by the end of September 2018. However, no empirical research has been conducted to ascertain the impact of the collapse of the seven banks on other existing banks in the banking industry.

In view of the aforementioned irrefutable roles played by the banking industry and the financial sector as a whole in ensuring sustainable economic growth to Ghana’s economy, it is imperative for a study to be conducted to ascertain the financial value of the information signaled by the collapse of the banks. Therefore, this research generally aims at assessing empirically the economic value of intra-industry information transfers on the other banks due to the collapse of seven banks. Moreover, this article assesses the overall stock market reaction of Ghana Stock Exchange (GSE) due to the collapse of the banks. In view of this, the event study methodology is adopted to estimate the abnormal returns generated for the rival firms as well as the GSE as a whole. The estimation of the abnormal returns is conducted with the use of daily stock prices of the other banks and their corresponding daily GSE Financial Stock Index (GSE-FSI). The results of the study reveal that the collapse of the seven banks does convey information that the market uses in revising stock prices. This study contributes to the scanty literature that exists with regard to the impact of externalities caused by an event on rival firms. Another contribution of this research worth mentioning is the great insight it provides managers of other banks in reference to the gainers and losers due to the shutdown of the seven banks by BoG. Thus, this article creates and deepens their awareness about the market valuation of their actions on their firms and others, hence the need for due diligence and pragmatism in decision making to forestall or minimize the occurrence of adverse events in their firms. The remainder of this article is structured as follows: Section “Literature Review” covers the literature review, Section “Data and Method” captures data and methodology, and Sections “Event Study Results” and “Conclusion” present event study results and conclusion, respectively.

Literature Review

Intra-Industry Information Transfers and Hypotheses

Intra-industry information transfers emanate from events happening in a firm that have an impact on other rivalry firms in the same industry. In other words, intra-industry information transfers are defined as the events in which the valuation of other firms is affected by the information about one firm in the same industry (Foster, 1981; Guo, 2017). This information signal experienced by other firms may result in a positive or negative direction in the change of stock prices between the announcing firms’ and the non-announcing firms’ values. A positive direction occurs when the change in the stock price of non-announcing firm moves in the same direction as the change in the stock price of the announcing firm which is often known as contagion effect, whereas a negative direction occurs when the change in the stock price of non-announcing firm moves in the opposite direction as the change in the stock price of the announcing firm which is often known as competitive effect (Gonen, 2003).

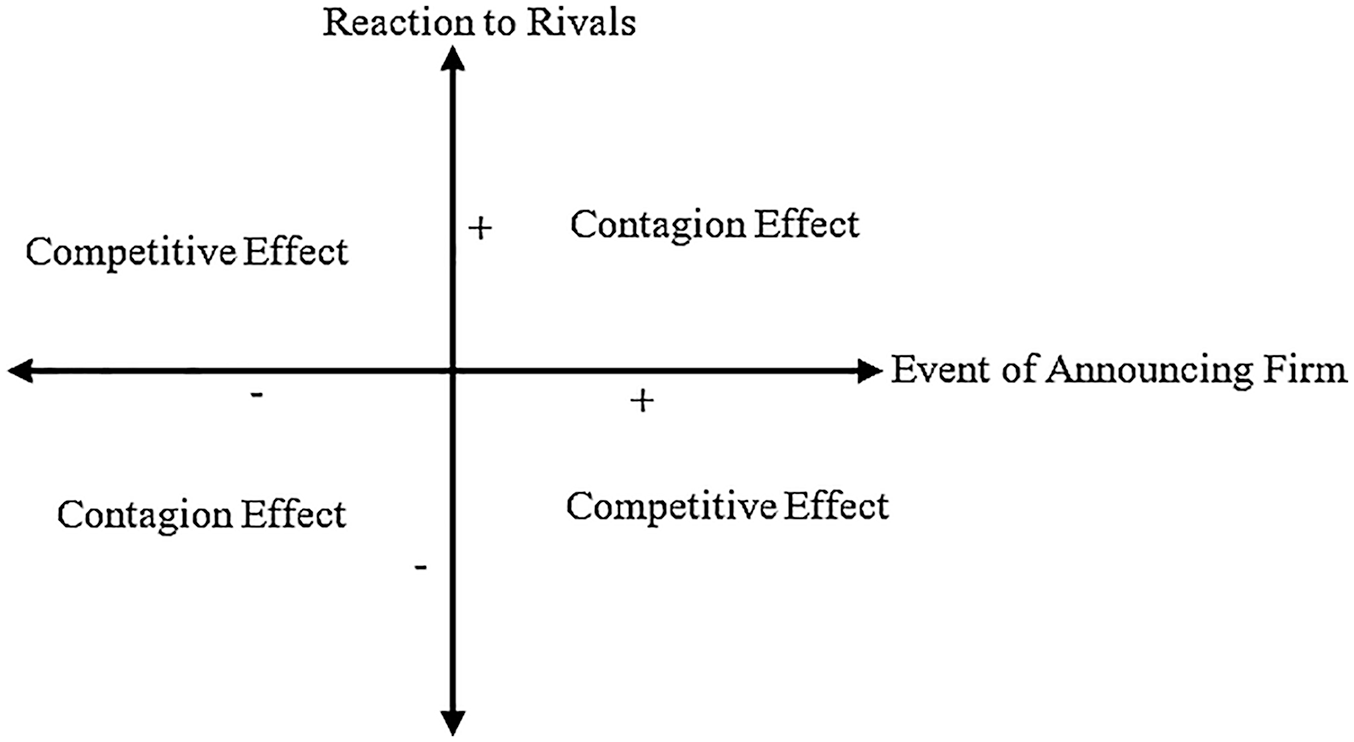

Lang and Stulz (1992) investigated into the impact of bankruptcy filings firms and concluded that information portrayed by bankruptcy filings’ announcements may impact positively or negatively the rival firms and therefore described the positive impact as competitive effect and negative impact as contagion effect. This is illustrated in Figure 1, which is referred to as axes of intra-industry information transfer.

Axes of intra-industry information transfers.

From Figure 1, the x-axis is represented by the event of the announcing firm or information emanating from one firm within an industry and y-axis is represented by the reaction to rivals in the same industry as a result of the event or happenings in another firm. In the first quadrant, both the x and y axes are positive, but they are negative in the third quadrant. This means that positive event in one firm will trigger positive reaction to other firms in the same industry (first quadrant) and vice versa as evidenced in the third quadrant. Hence, both the first and the third quadrants exhibit a contagion effect. The x and y axes are positive and negative, respectively, in the second quadrant, whereas the x-axis is negative and the y-axis is positive in the fourth quadrant. The second quadrant demonstrates that rival firms in the same industry experience negative reaction due to a positive event in one firm. However, it can be observed from the fourth quadrant that a negative event in one firm will impact positively on the market value of other firms in the same industry. Therefore, competitive effect occurs in both the second and the fourth quadrants.

The presence of competitive effect is explained by Gonen (2003) to the effect that information publicized about the announcing firm is firm-specific; however, the information revealed being good or bad news inform stakeholders, particularly investors, that rival firms in the same industry stand to be affected positively or negatively. Gonen (2003) also explains contagion effect by the fact that the industry as a whole is previously unaware of the information revealed by the announcing firm, thereby causing a change in stock price to move in the same direction for the announcing firm and other firms in the same industry. Firth (1976), Baginski (1987), Lang and Stulz (1992), Otchere and Ross (2002), Gleason et al. (2008), Guo (2017), and F. Chen et al. (2018) are some of the several studies that have been conducted empirically to document the existence of intra-industry information transfer.

Ghana’s banking industry and the financial sector as a whole were plunged into turbulence when seven commercial banks were collapsed in 2017 (two banks) and 2018 (five banks). Specifically, on August 14, 2017, BoG revoked the licenses of UT Bank and Capital Bank under a Purchase and Assumption agreement due to severe impairment of their capital (Ibrahim, 2017). Moreover, on August 1, 2018, the BoG created Consolidated Bank Ghana Limited to take over five banks, namely, Sovereign Bank, Royal Bank, The Beige Bank, Construction Bank, and Unibank, due to insolvency of these banks after investigations by the central bank (E. D. Frimpong, 2018). Since firms are interrelated within an industry, the other banks in the banking industry may be affected in one way or the other by these two events. As such, this research conducts empirical investigations into how the market value of each of the other listed banks in the banking industry is affected by the collapse of two banks in 2017 and the collapse of five banks in 2018. This study also aims at estimating the overall impact of each of these two events on the GSE. Therefore, based on the discussion on intra-industry information transfers, the hypotheses for this research are formulated as follows:

H1a: The other banks will react to the announcement of the collapse of two banks negatively.

H1b: The stock market will react to the announcement of the collapse of two banks negatively.

H2a: The other banks will react to the announcement of the collapse of five banks negatively.

H2b: The stock market will react to the announcement of the collapse of five banks negatively.

Data and Method

Data Collection

The purpose of this study is to estimate the economic value of intra-industry information transfers within Ghana’s banking industry due to the collapse of seven banks. The data for this research were obtained from the websites of Annual Reports Ghana (ARG) and the GSE. The daily stock prices of the other banks used in this research were obtained from GSE. The GSE publishes two indices: the GSE-CI (a market capitalization weighted index of all ordinary shares with the exception of those listed on other markets) and the GSE Financial Stock Index (GSE-FSI; same as GSE-CI but consists of only stocks from the financial sector) (Kwayisi, 2018).

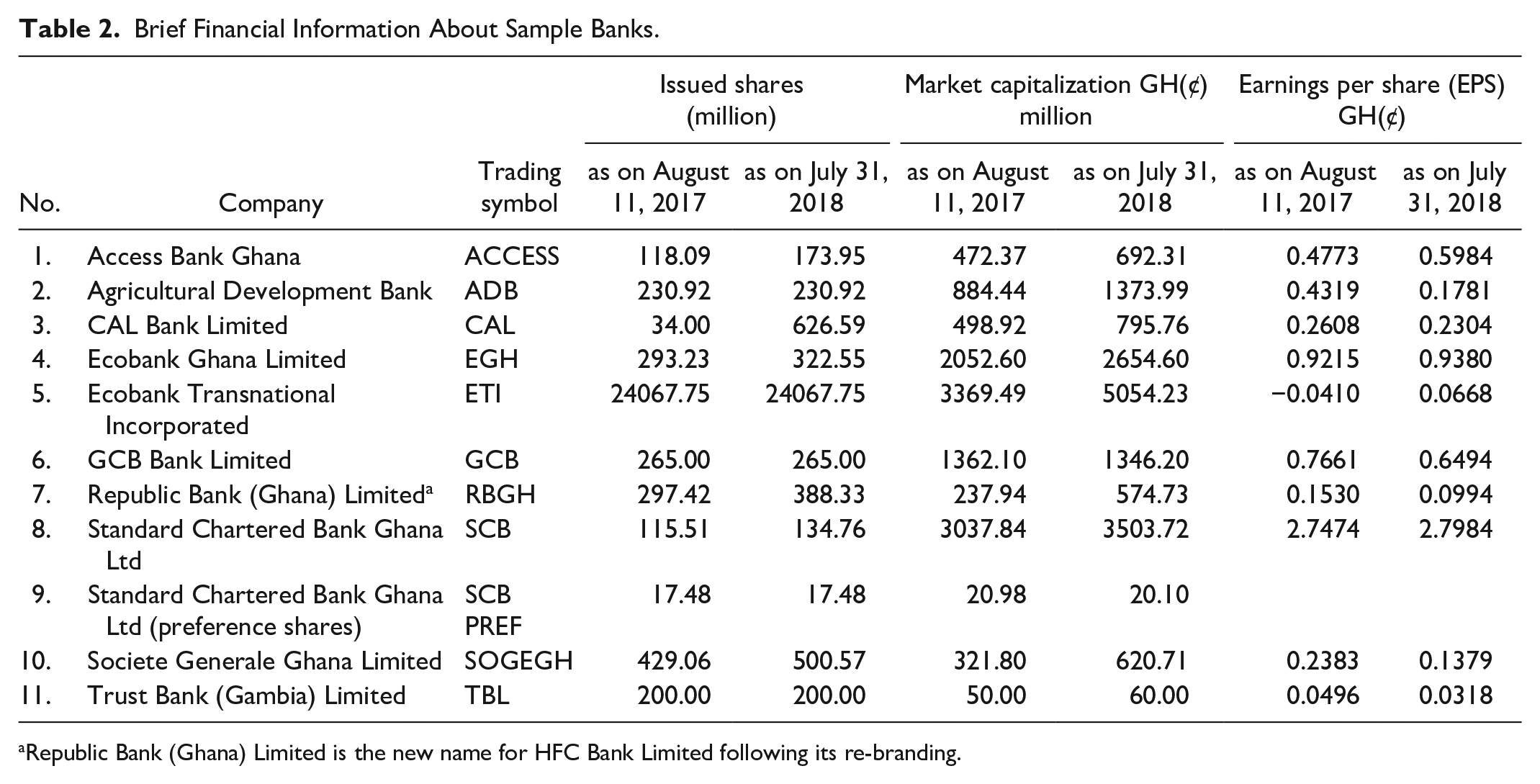

Since this article is about the banking industry and the financial sector as a whole, the GSE-FSI was chosen as a proxy for the market index. As such, the daily GSE-FSI were generated from the website of ARG. ARG houses financial information of companies listed on the GSE and collective investment schemes licensed by Ghana’s Security and Exchange Commission. The number of remaining listed banks, which had sufficient information required for this study, was 10 as on August 14, 2017, when the first event occurred (collapse of two banks). However, the number of other listed banks, which had sufficient information required by this study, was 11 as on the second event date of August 1, 2018. Therefore, daily stock prices used in this research were collected with respect to a sample of 11 banks. Table 1 presents the nature of businesses of the other listed banks, and Table 2 shows some brief financial information about them a day prior to each of the event dates and sourced from sikasem.org, kwayisi.org, and GSE platforms. With reference to Table 1, the Standard Chartered Bank Ghana Limited (SCB) can be regarded as a pioneer bank or pacesetter, as it was the first commercial bank to be listed on GSE, followed by the HFC Bank Limited, rebranded as Republic Bank (Ghana) Limited. Moreover, it can be observed from Table 2 that SCB has the highest earnings per share (EPS) for both periods under consideration: 2.7474 as on August 11, 2017, and 2.7984 as on July 31, 2018. This is an indication that SCB may be regarded as the most profitable bank, as EPS is considered as an indicator of a company’s profitability. Consequently, a higher EPS indicates more value because investors will pay more for a company with higher profits.

Nature of Businesses of Sample Banks.

Republic Bank (Ghana) Limited is the new name for HFC Bank Limited following its re-branding.

Brief Financial Information About Sample Banks.

Republic Bank (Ghana) Limited is the new name for HFC Bank Limited following its re-branding.

Method

The event study methodology is used for this study. An event study methodology is a statistical technique that estimates the stock price impact of occurrences or events such as stock splits, acquisitions, earnings announcements, bankruptcy, and many more (Corrado, 2011). Some of the events are within the firm’s control, such as dividend announcement, whereas others go beyond the firm’s control, such as enacting a new law for regulatory purposes. According to Cohen-Setton & Angeloni (2012), the basic idea underlying event study methodology is to use the high-frequency trading values of financial securities to assess the impact of news or events. If financial markets are efficient, in the sense that information about the future payoffs of the assets are factored in their prices, an event that affects these future payoffs should be translated into an immediate repricing. Therefore, the reaction of an event in terms of abnormal returns can be estimated by examining security prices surrounding the release of the information or the event.

The abnormal stock return in the presence of the event is recorded within a time frame called the event window. The size of the event window varies from study to study (Konchitchki & O’Leary, 2011). For instance, Bruner (1999) and Nielsen (2012) set a 2-day (−1, 0) and a 3-day (−1, 1) as the short event window period, respectively. On the contrary, some studies prefer a longer event window period, which may cover several months or years around the event date. Gregory (1997) used 60 months as an event window and Hertzel et al. (2002) studied a 36-month test period. Consistent with other studies, such as Chavez and Lorenzo (2006), Dewan and Ren (2007), and Prakash (2013), we estimate the abnormal returns over the event window [−10, 10] which is a 21-day event period.

A 21-day event window is specified as follows: −10 representing 10 pre-event days and +10 representing 10 post-event days plus the event day denoted by 0, as depicted in Figure 2. Through its Automated Trading System, the GSE opens for continuous trading from 10:00 to 15:00 Greenwich Meridian Time (GMT). The day in which the event occurred or new information released to the public is regarded as Day 0. The calendar days aided in deriving the event days as displayed in Table 3.

An illustration of the event study.

Event Days Derived From Calendar Days.

Note. GMT = Greenwich Mean Time.

The estimation window chosen for this study is made up of 200 trading days (−210, −11) starting 10 trading days before the event date. The estimation period is used to measure the stock’s normal movement and correlation with outside index or indices (Krivin et al., 2003). The estimation period set 10 trading days before the event date is necessary to avoid the returns in the estimation window to be affected by the event. A bank included in the sample of this study should have at least 40 return observations during the 200-trading day estimation window. There is no uniformity for the choice of the estimation window used in various event study researches. For instance, Cox and Peterson (1994) chose 100 days, Carow and Kane (2002) chose 200 days, MacKinlay (1997) chose 250 days, and Litvak (2007) chose 500 days. Figure 2 illustrates the event study with an event period of [−10, 10] and estimation window of [−210, −11] while Day 0 depicts the exact day the event occurred.

Giri (2016) outlines the following eight steps that can used to conduct an event study:

Step 1: Selection of an event

The first step in every event study is the selection of the event of interest to the researcher. There are many events that have the tendency of affecting the firm’s stock price, some of which are within the control of the firm or beyond the firm’s control. It is important for the researcher to determine the exact date on which the event occurred. The event of interest for this research is the collapse of seven commercial banks in Ghana which occurred in 2017 and 2018. Specifically, two banks collapsed on August 14, 2017, and the other five collapsed on August 1, 2018.

Step 2: Selection of event window

The next step is to select the event window for the event study over which the expected return and the abnormal return will be calculated. The event window chosen for this research is [−10, +10].

Step 3: Calculation of return

The next step is to estimate the return on share prices of the firm as well as the return on the market depending on the stock exchange on which the firm trades:

Estimation of return on share prices

The fundamental idea of event study is to estimate the impact of an event on the share prices of a firm. As such, the next step is to calculate the returns on the share prices using the following formula (Khotari & Warner, 2006):

where

Estimation of market return

To estimate the market return, a market index should be selected depending on the particular stock exchange on which the selected firms trade. The sample banks selected for this study trade on GSE, hence the choice of GSE-FSI as a proxy for the market index. The market return is then calculated as follows (Khotari & Warner, 2006):

where

Step 4: Calculation of expected return

The use of event study methodology helps to calculate the significant difference between the expected return and the actual return as calculated in Step 3. The expected return is calculated as follows (Khotari & Warner, 2006):

where

Step 5: Calculation of abnormal return

The abnormal return is the difference between the actual return and the expected return. It is calculated as follows:

Step 6: Calculation of average abnormal return

The average daily abnormal return for the event window is determined by calculating the arithmetic mean of the abnormal return and expressed as follows (Khotari & Warner, 2006):

where

Step 7: Calculating cumulative average abnormal return

The cumulative average abnormal return (CAAR) for the event study is estimated by the below formula (Khotari & Warner, 2006):

where

Step 8: Conducting the t-test

The last stage of event study is to test whether the event leads to abnormal return in the share prices or not using t-test, which is expressed as follows (Khotari & Warner, 2006):

It can be concluded that the event has significant impact on the share prices of the firm if the average return is significantly different from 0. Otherwise, the event does not affect the share prices of the firm significantly. The abnormal return is statistically significant at 0.90, 0.95, and 0.99 confidence levels.

Event Study Results

The results of this study are presented in two parts. The cumulative abnormal returns (CARs) earned by each of the other banks due to the two events are captured in the first part, whereas the second part presents the overall impact of each of the two events on the GSE by estimating the CAAR within the event period [−10, 10].

Impact of the Two Events on the Other Banks

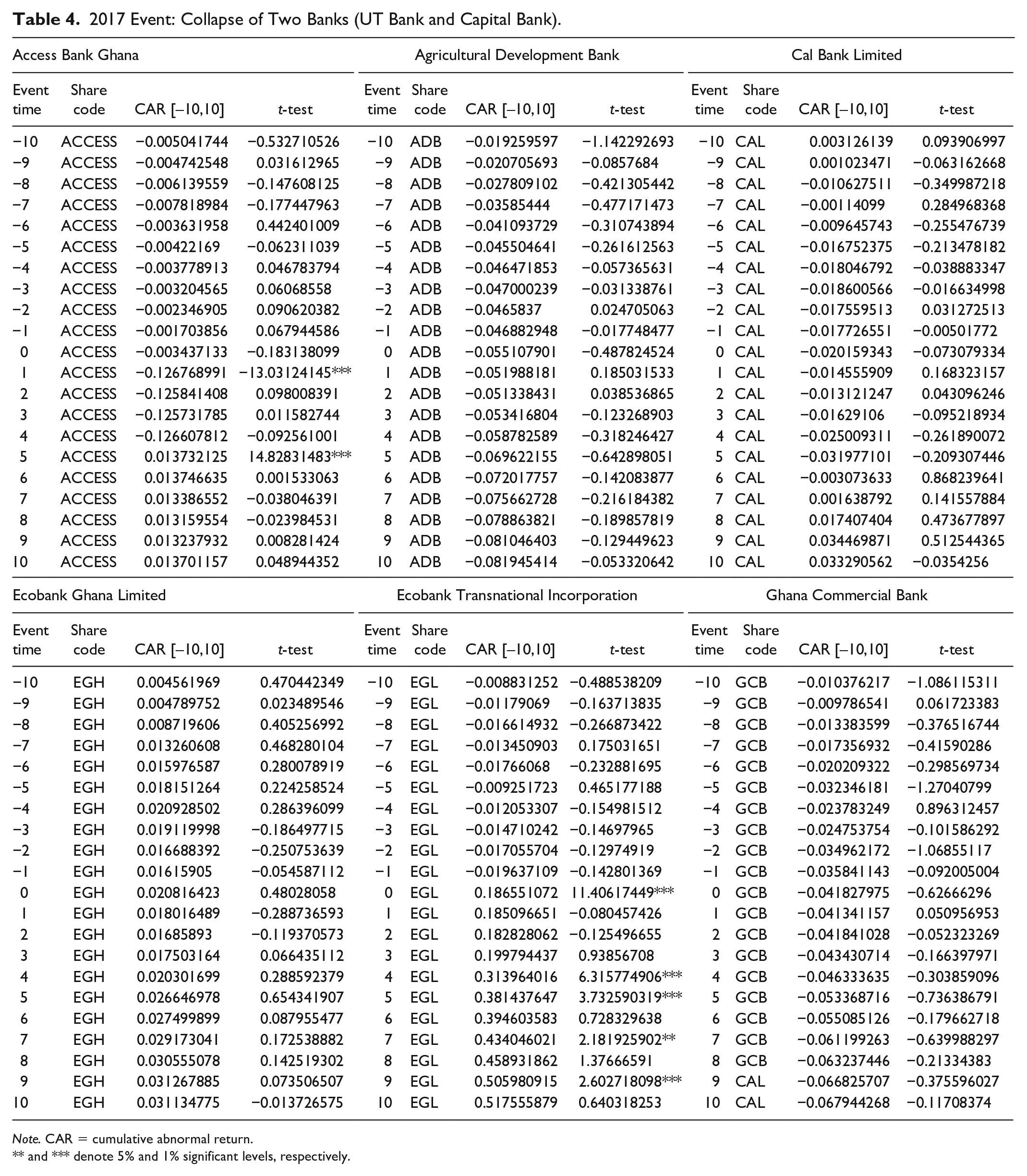

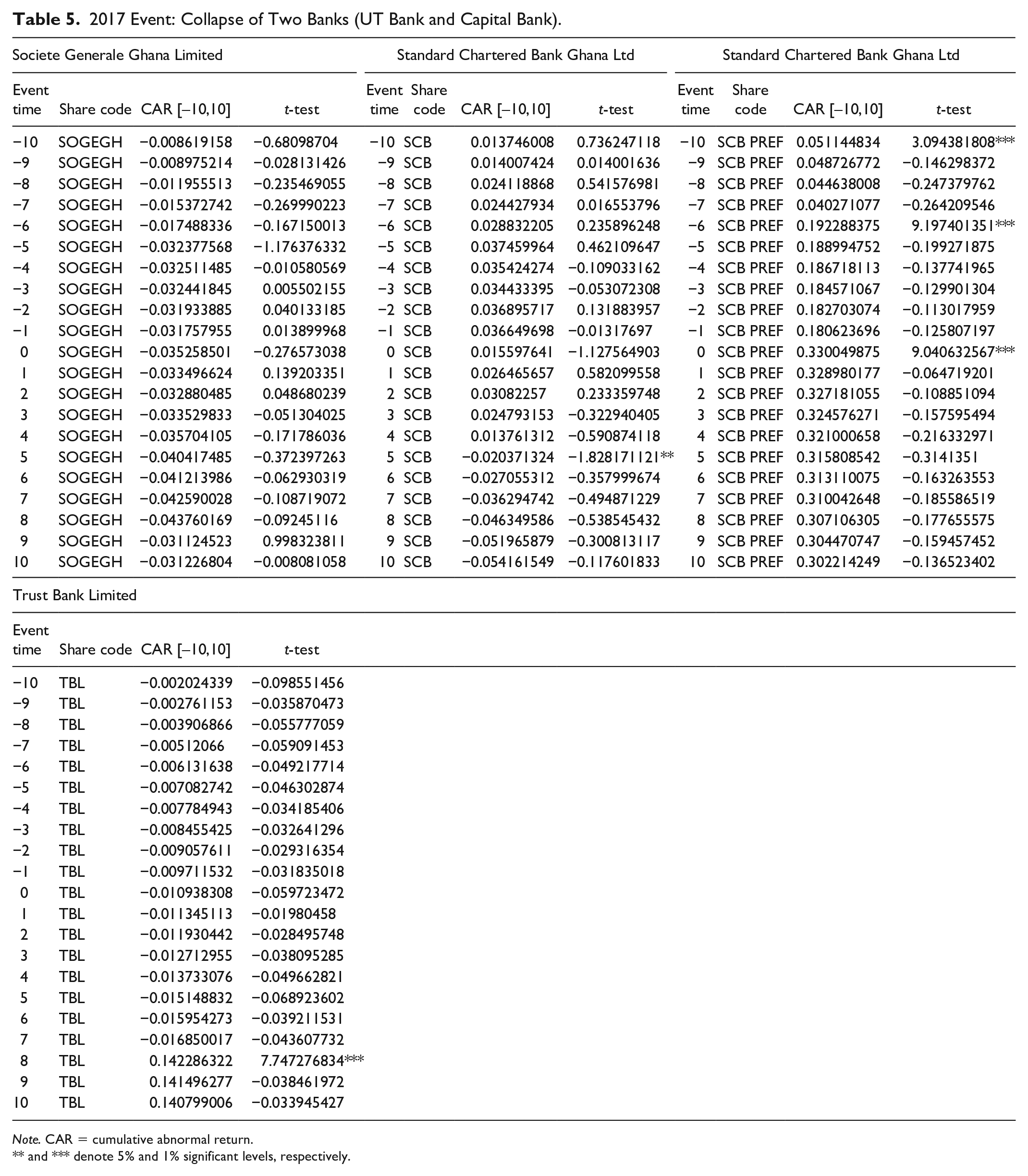

Tables 4 and 5 present the results of CARs accrued to the other banks in the banking industry of Ghana due to the first event (collapse of two banks). Access Bank Ghana, Agricultural Development Bank, Cal Bank Ltd, Ghana Commercial Bank (GCB), Societe Generale Ghana Limited, and Trust Bank Limited obtained negative CARs on the event day (Day 0). This means that the share prices of these banks witnessed negative stock market reaction due to the collapse of UT and Capital Banks on August 14, 2017. However, the negative reaction experienced by the other banks in the banking industry is not significant. The negative reaction continued for four consecutive days for all these banks after Day 0. This is an evidence of contagion effect which is consistent with Jorion and Zhang (2007), which concluded that Chapter 11 bankruptcies are mostly contagion effects. Furthermore, Acharya and Yorulmazer (2008) postulated that when bank loan returns have a common systematic factor, the cost of borrowing for a bank increases when there is adverse news on other banks since such news conveys adverse information about the common factor.

2017 Event: Collapse of Two Banks (UT Bank and Capital Bank).

Note. CAR = cumulative abnormal return.

and *** denote 5% and 1% significant levels, respectively.

2017 Event: Collapse of Two Banks (UT Bank and Capital Bank).

Note. CAR = cumulative abnormal return.

and *** denote 5% and 1% significant levels, respectively.

The share prices of Ecobank Ghana Limited, Ecobank Transnational Incorporation, SCB, and SCB PREF witnessed positive reaction on the event day (Day 0). However, the positive reaction for Ecobank Ghana Limited and SCB is not significant. But the positive reaction for Ecobank Transnational Incorporation and SCB PREF is both significant at 1% level. These four shares gained positive reaction due to competitive effects as it was evidenced in the study conducted by Lang and Stulz (1992), which found a positive abnormal return for rival firms in the same industry with regard to bankruptcy announcements. The positive CARs achieved by these four rival banks can be explained to the effect that investors re-evaluated the competitive atmosphere in the industry and perceived these banks to be unaffected by the collapse of the other two banks.

It can be observed from Tables 4 and 5 that six of the rival industry banks earned negative share price reaction on Day 0, whereas four of them had positive coefficient of the CARs accrued to them on the same day. Therefore, H1a cannot be supported by the share price reaction for each of the rival industry banks.

Tables 6 and 7 show the economic worth of intra-industry information in terms of CARs earned by the other banks due to the second event (collapse of five banks). The share prices of Access Bank Ghana, Agricultural Development Bank, Cal Bank Ltd, GCB, Societe Generale Ghana Limited, and SCB witnessed negative reaction on the event day (Day 0). However, the negative reaction is not significant. The negative reaction for these banks continued for all the 10 days after Day 0. Therefore, it can be concluded that there is the existence of contagion effects in Ghana’s banking industry which is in line with the studies by Francis and Michas (2013), Harding et al. (2009), and Kyle and Xiong (2001). These banks experienced contagion effects because investors and the general public perceived these banks to be in similar liquidity distress as the other collapsed banks. Such perception as well as the element of surprise reflected in the share prices of these other banks to earn negative abnormal returns.

2018 Event: Collapse of Five Banks (Sovereign Bank, Royal Bank, The Beige Bank, Construction Bank, and Unibank).

Note. CAR = cumulative abnormal return.

, **, and *** denote 10%, 5% and 1% significant levels, respectively.

2018 Event: Collapse of Five Banks (Sovereign Bank, Royal Bank, The Beige Bank, Construction Bank, and Unibank).

Note. CAR = cumulative abnormal return.

, **, and *** denote 10%, 5%, and 1% significant levels, respectively.

Ecobank Ghana Limited, Ecobank Transnational Incorporation, SCB PREF, Trust Bank Limited, and Republic Bank Ghana Limited gained positive CARs on the event day (Day 0). This means that the share prices of these banks witnessed positive stock market reaction due to the collapse of the five banks on August 1, 2018. Except for Republic Bank Ghana Limited, which had significant positive reaction at 1% level, the positive reaction for the rest of the banks is insignificant. However, that does not eliminate the presence of competitive effects in the industry which were also found in studies by (Goins & Gruca, 2008; Slovin et al., 1999).

General observations on Day 0 from Tables 6 and 7 is that five of the rival banks had positive share price reaction and the remaining banks earned negative share price reaction. Consequently, the negative share price reactions of six banks support H2a, whereas the positive share price reactions of the other banks do not support the hypothesis.

With respect to Day 0, overall Ecobank Ghana Limited, Ecobank Transnational Incorporation, and SCB PREF were affected positively by the two events, SCB was affected positively by 2017 event and negatively by 2018 event, but the reaction of both events for Trust Bank Limited was opposite to that of SCB. Moreover, Republic Bank Ghana Limited was affected positively by only one event. However, the rest of the other rival industry banks were affected negatively by both events. Table 8 illustrates the rankings of the combined effect on each of the rival banks on Day 0 from well-performing banks to the poor-performing banks in the midst of the two adverse events. In addition, Table 8 presents the type of intra-industry information transfers (contagion effect and competitive effect) for each of the other rival industry banks.

Rankings of Combined Effect at Day 0.

Note. Republic Bank Ghana Ltd is excluded in the rankings because it was not affected by both events.

Impact of the Two Events on GSE

The externalities due to events or the release of new information do not only affect the individual firms on a stock exchange but also the entire stock exchange by estimating the mean abnormal returns across the returns of the individual firms. Therefore, the CAAR for the entire GSE is measured on the basis of the CARs accrued to the other individual banks.

2017 event: collapse of two banks

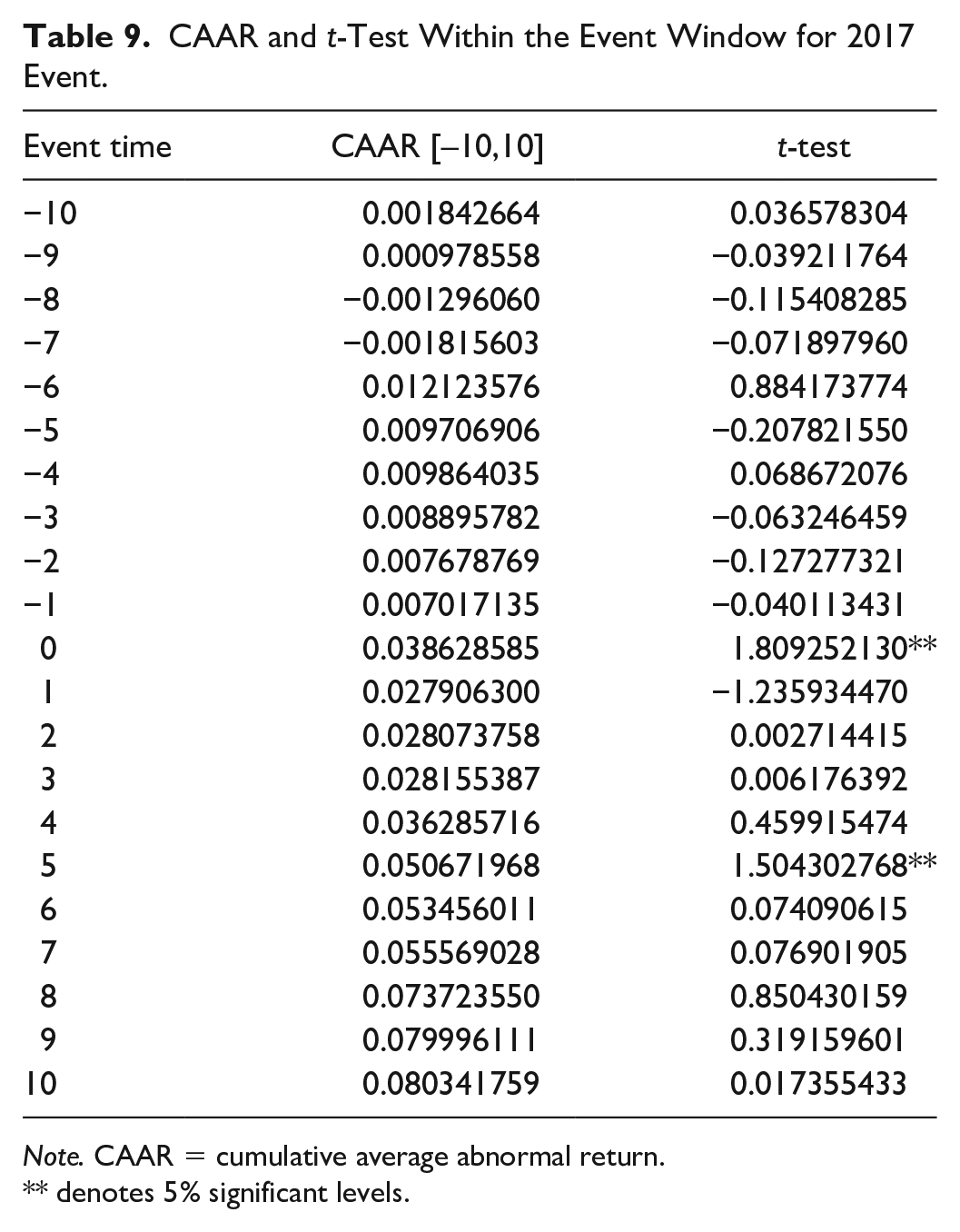

The stock market reaction for the entire GSE due the 2017 event is captured in Table 9. According to Table 9, the coefficient of CAAR estimated for GSE is positive for 6 days prior to the event day. On Day 0, the market recorded positive stock market reaction with CAAR of 0.039 statistically significant at 5% level. Other studies, which have concluded a positive stock market reaction for negative events or bad news, include Ghanem and Rosvall (2014) and Narayan and Narayan (2012). Irrespective of the marginal drops for some of the days after the event day, the positive stock reaction continued for all the 10 days after Day 0. Specifically, the event induced a marginal drop of 1.07% on Day 1, but the drop was short-lived as the market recovered the next day (Day 2) to a marginal increase of 0.02% and ensured a relative stability on Day 3. However, the marginal rise in CAAR increased at an increasing rate for Day 4 (0.81%) and Day 5 (1.44%) but increased at a diminishing rate for Day 6 (0.28%) and Day 7 (0.21%). The CAAR again increased at an increasing rate on Day 8 (1.82%) but increased at a diminishing rate on Day 9 (0.63%) and Day 10 (0.03%). The behavior of the CAAR curve for GSE during the event window is further illustrated in Figure 3. The positive stock market reaction caused by the 2017 event on the event day indicates that we reject H1b.

CAAR and t-Test Within the Event Window for 2017 Event.

Note. CAAR = cumulative average abnormal return.

denotes 5% significant levels.

Graph showing CAAR for 2017 event: collapse of two banks.

2018 event: collapse of five banks

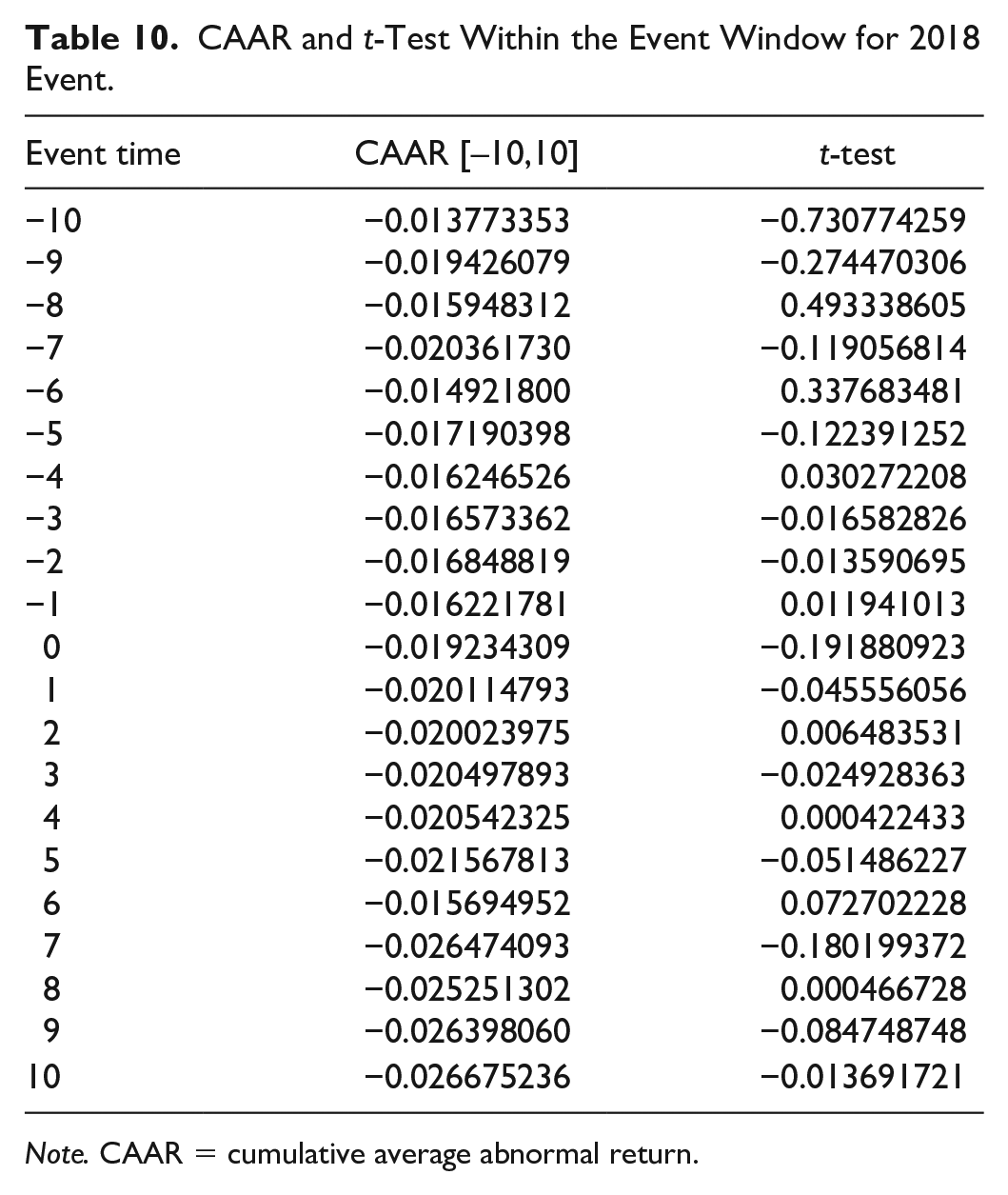

Table 10 presents the overall stock market reaction for GSE following the dissolution of five banks by BoG in 2018. It can be observed from Table 10 that GSE has not been performing well prior to the event day (Day 0), as all the 10 days preceding the announcement date generated negative CAARs. Moreover, event day (Day 0) recorded negative CAR (−0.0192). In line with the previous studies (Chambers & Penman, 1984; Hendricks et al., 2009; Jacobs and Singhal, 2017; Sturm, 2013), this is an indication that GSE witnessed negative stock market reaction on the event day but the reaction is not significant. The distress performance of GSE deepened the next day as the market plunged marginally by 0.09%. The market continued to plunge until Day 6 where it gained some strength by a marginal 0.59%, although the reaction is still negative. However, the gains could not be sustained as GSE suffered a heavy loss of 1.08% on Day 7 as compared with Day 6. Day 8 generated a marginal gain in CAAR by 0.12%. GSE returned to negative marginal gains on Days 9 and 10 by 0.11% and 0.03%, respectively. The behavior of the CAAR curve for 2018 event is further illustrated in Figure 4. The negative stock market reaction for the entire GSE caused by the collapse of the five banks supports H2b.

CAAR and t-Test Within the Event Window for 2018 Event.

Note. CAAR = cumulative average abnormal return.

Graph showing CAAR for 2018 event: collapse of five banks.

We also assessed which of the two events had greater adverse effect on GSE as presented in Figure 5. From Figure 5, it is obvious that the second event generated greater adverse effect on GSE than the first event, as 2018 CAAR curve lies below 2017 CAAR curve. This is because the whole 2018 CAAR curve located below the x-axis assumes negative values for most of the coordinates. However, most of the coordinates for 2017 CAAR curve are positive; specifically, half of the curve is located in the first quadrant where both x and y coordinates are positive. Superficially, the collapse of five banks will be more surprising and devastating to depositors, investors, and the general public than the collapse of two banks. The two events created uncertainties in the market but all other being equal, the level of uncertainties created by collapse of five banks will be higher than the collapse of two banks.

Graph showing degree of impact of both events on GSE.

The level of uncertainty determines the investors’ perception and expectation which will reflect in the share prices and the entire stock market reaction. Williams (2009) asserts that the reaction of investors to earning announcements is dependent on the prevailing level of uncertainty. Moreover, Zhang (2006) concludes that greater information uncertainty should generate relatively higher expected returns following good news and relatively lower expected returns following bad news. It is reasonable to assume that the collapse of five banks is of more bad news than the collapse of two banks. Hence, the collapse of the five banks produced more adverse impact on GSE than the collapse of the two banks as justified in Figure 5.

Conclusion

This article focuses on investigating empirically the financial implications on Ghana’s banking industry due to the collapse of seven commercial banks. Therefore, we assessed the informational value conveyed by the collapse of these banks as perceived by investors and the general public, thereby triggering share price reaction for other listed banks or stock market reaction for the entire GSE. In effect, this article assesses the externalities gained or suffered by the other rival banks in the form of intra-industry information transfers being contagion effect or competitive effect. Event study methodology is adopted to estimate the short-term abnormal returns accrued to the competitors of the collapsed banks. Most of the rival industry banks reported insignificant negative share price reaction for the two events. SCB PREF’s equity is the highest gainer of 0.33 CAR from the combined effect of the two events. The economic implication of this gains is that the market value of this equity (SCB PREF) increased by 33%. Conversely, equity from Societe Generale Ghana Limited’s equity (SOGEGH) is the worst performer with −0.11 CAR. This is an indication that the market value of this equity (SCB PREF) plunged by 11%. Moreover, GSE as a whole recorded insignificant negative stock market reaction for the 2018 event. The insignificant negative reaction can be attributable to the measures outlined and implemented by the regulator, BoG, to mitigate the effect of these events on depositors, financial institutions, and the general public. According to Slovin et al. (1999), it is the primary responsibility of regulators to monitor, assess, and determine when a bank’s financial situation has worsened to a level that regulators are justifiable to request the organization’s recapitalization, to exercise direct intervention in the management of the distressed bank, or to terminate the operations and liquidate the assets of the crisis firm. Slovin et al. (1999) further explained that this supervisory mandate exercised by the regulators is to curb the negative externalities that the actions of an adverse bank can cause for other banks, households, and firms.

In view of this empirical evidence and confirmed by the provisions of Section 123 of the Banks and Specialized Deposit Taking Institutions (SDIs) Act, 2016 (Act 930), the BoG, having revoked the operating licenses of UT and Capital Banks in 2017 and mandated to protect the interest of customers, approved a Purchase and Assumption agreement, allowing GCB to take over all deposit liabilities and selected assets of both UT and Capital Banks (Adogla-Bessa, 2017). Moreover, following the liquidation of five banks in 2018, BoG established a new bank called Consolidated Bank of Ghana Limited to acquire and assume the deposits and selected assets and liabilities of the liquidated banks (E.D. Frimpong, 2018). These measures were undertaken to protect the interest of depositors and also to maintain some level of public and investors’ confidence in the banking industry as well as the entire financial sector.

The insignificant reaction experienced by most of the banks and the entire stock market can also be attributed to the fact that GSE is not efficient. A market is efficient when at any given time prices fully reflect all available information about an individual stock and the market in general (Ayentimi et al., 2013). However, several studies have been conducted to establish that GSE is weakly inefficient (M. J. Frimpong, 2008; M. J. Frimpong & Oteng-abayie, 2007; Osei, 2002). The results of this research are further justification to the inefficiency of the GSE. The implication of GSE being inefficient is that market prices of common stocks and similar securities are not accurately priced and tend to deviate from the true discounted value of their future cash flows (Agyeman, 2010). Therefore, share prices are driven above or below their true value by market forces. This is a discouraging situation for managers when the share prices of their shares are frequently undervalued which most often is the case on GSE.

Consequently, other firms may be discouraged from listing on the GSE. Such inefficiency accounts for the small number of firms currently listed on the GSE. According to Kwayisi (2019), the number of equities listed on the GSE is 41 as on May 2019. The small number of equities traded on the GSE offers limited options to people who want to enter the market. To compound the situation of limited number of securities, Agyeman (2010) reveals that the bulk of issued shares on the GSE are held by non-resident Ghanaian investors, institutional investors, and parents’ companies who do rarely trade. The average floats of shares available for trade is about 25%. This makes the market very dormant, illiquid, and inefficient.

Accordingly, efforts should be made to get more firms to be listed on the GSE. First, it is imperative for the GSE to be reformed to improve the efficiency of the market and secure the flow of information to market participants. Second, some of the key factors underlining inefficiency of the GSE are the size of market capitalization and the lack of significant market makers. As such, stocks with greater market capitalization and trading activity should be the focus of individual investors. Moreover, transaction cost should be reduced so as to improve market activities and hence liquidity.

The collapse of the seven banks must also lead to rigorous and periodic reforms in the banking industry spearheaded by the BoG. The BoG, having admitted partial culpability in the collapse of these banks (Tetteh, 2018), is urged to intensify its oversight supervisory roles to forestall occurrences of similar negative events in future. These events in Ghana’s banking industry must be a wake-up call to other banks and financial institutions to ensure strict adherence to good corporate governance practices and abide by other laws, regulations, and standards. Furthermore, managers of firms are entreated to take cognizance of the economic value embedded in their strategic decisions by ensuring that such actions have the propensity to increase the market value of their firms.

This study is subjected to some limitations which provide room for future research. First, the results generated for this research is based on short-term analysis within the scope of 10-day period prior to the event day and 10 days after the occurrence of each event. Therefore, it will be interesting for a long-term study to be conducted to assess the long-term impact of the collapse of the seven banks on the other listed banks as well as GSE as a whole. Second, the authors focused on the externalities to the other banks in the banking industry. Other industries could be the focus of other studies to assess whether those industries also experienced spillover effects from the two events. Finally, the sample for this study is limited to the banks listed on GSE. As such, it will be revealing for a survey to be conducted with the focus on the non-listed banks to assess the impact of the two events on their operations.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.