Abstract

A number of studies have been conducted on the salient factors that influence consumers’ intention to adopt mobile banking services. However, none of these studies has explored the impact of personality traits on consumers’ intention to adopt mobile banking services. This study investigates the impact of personality traits on users’ intention to adopt mobile banking. Data gathered from 482 mobile banking users in Ghana via a convenience sampling technique using a questionnaire survey were analyzed using structural equation modeling. The results show that agreeableness, conscientiousness, and openness to new experience significantly impact users’ intention to adopt mobile banking through perceptions of usefulness and ease of use, with agreeableness showing the strongest total effect, followed by conscientiousness. The results also reveal that perceived usefulness and perceived ease of use are salient predictors of users’ intention to adopt mobile banking. The study underscores the need for service providers to focus on designing effective marketing strategies that recognize different user personality traits so as to improve adoption.

Introduction

As one of the utmost innovative technologies, mobile banking (MB) has steered a new era in the banking industry around the globe (Makanyeza, 2017; Shambare, 2013) and has gradually become an important banking channel alongside automated teller machines (ATMs), telebanking, and internet banking in recent years (Alalwan et al., 2016; Giovanis et al., 2019; Lee et al., 2007). It is a unique mode of executing banking services via a channel whereby customers are able to interact with a bank with a mobile device, for example, cell phones and personal digital assistants (Giovanis et al., 2019; Luo et al., 2010; Owusu Kwateng et al., 2019; Shareef et al., 2018). Thus, customers can access multifarious banks, and financial associated services anywhere and anytime through MB (Ahluwalia & Varshney, 2009; Luo et al., 2010). MB greatly benefits customers via time optimization, prompt connectivity and information, improved convenience, and many more, thereby enriching their satisfaction (Alalwan et al., 2016; Cruz et al., 2010; Zhou et al., 2010). In addition, banks and other MB service providers profit by advancing better adeptness and enhanced service quality via MB (Gu et al., 2009; Malaquias & Hwang, 2016). For these reasons, banks around the world have invested considerably in mobile services development and are providing MB technology to their numerous clients (Alalwan et al., 2017; Owusu Kwateng et al., 2019). Indeed, according to Complete Pulse (2013)’s report cited by Alalwan et al. (2017), banks worldwide spent or invested more than $115 billion at the end of 2013 in a bid to implement MB in their systems.

Mobile devices, for example, tablets and smartphones, that enable customers to carry out MB services are progressively existent in our lives (Urueña et al., 2018; Xu et al., 2016). The number of mobile phone users in the world in 2015 was 4.15 billion and is projected to reach 4.78 billion in 2020 (www.statista.com). Furthermore, a recent market analysis shows that about 78% of the world’s population has a smartphone and more than 50% owns tablets (Deloitte, 2017; Urueña et al., 2018). Despite the high adoption rate of mobile devices and the numerous benefits that customers can obtain from MB, the extant literature (Farah et al., 2018; Makanyeza, 2017; Malaquias & Hwang, 2016; Shaikh & Karjaluoto, 2015) indicates that MB adoption rate is still low across countries. According to Alalwan et al. (2017), the adoption rates of MB services are lower than originally anticipated particularly in developing nations, confirming Shaikh and Karjaluoto (2015)’s remark that performing banking-related transactions via mobile phones is not prevalent.

In Ghana, the National Communications Authority (NCA) reports that the total number of mobile subscription at the end of July 2017 stood at 37.1 million, denoting a whopping penetration rate of 130.35% in that month (NCA, 2017). Given the growth of mobile networks and services offered by telecommunication operators across Ghana, these numbers are likely to increase (Narteh et al., 2017). Similarly, internet users in the country, per www.internetworldstats.com, stood at about 10.1 million, accounting for 34.8% of the population. These developments undeniably offer huge growth prospects for raising MB services use. Moreover, it also spurs telecommunication companies and banks on to develop new mobile applications to grow their client base and satisfy their needs. Indeed, in line with these developments and as a competitive strategy, retail banks in Ghana provide assortment of financial and non-financial services via MB apps or platforms (Avornyo et al., 2019). Notwithstanding, the situation is no different, as adoption rate of MB remains low (Owusu Kwateng et al., 2019), prompting the need to explore the factors that impact its adoption.

Several studies (e.g., Afshan & Sharif, 2016; Alalwan et al., 2017; Chaouali et al., 2017; Farah et al., 2018; Giovanis et al., 2019; Gu et al., 2009; Mohammadi, 2015; Pedersen, 2005; Püschel et al., 2010; Zhou et al., 2010) via different theoretical frameworks, for example, the technology acceptance model (TAM; Davis, 1989), the theory of planned behavior (TPB; Ajzen, 1985), the theory of trying (Bagozzi & Warshaw, 1990), the decomposed theory of planned behavior (DTPB; Taylor & Todd, 1995), the innovation diffusion theory (IDT; Rogers, 1995), and the unified theory of acceptance and use of technology (UTAUT; Venkatesh et al., 2003, 2012) have studied and documented several salient factors that drive MB adoption. Also, in Ghana, few studies (e.g., Cudjoe et al., 2015; Owusu Kwateng et al., 2019) have also discussed some of the important factors that drive consumers to use MB services. While these studies, taken together, contribute meaningfully to the understanding MB adoption, much remains to be known about the influence of personality traits on users’ intention to accept and use MB in the MB literature. Moreover, there is scarcity of research that has examined the factors that influence customers’ intention to adopt MB services in Ghana. Thus, much of the existing empirical evidence have come from experiences derived from advanced countries where MB deployment and implementation is in advanced stages, unlike Ghana, where MB is still in its infancy stage (Owusu Kwateng et al., 2019). Hence, undertaking this research in Ghana is in the cards to enhance our comprehension of this phenomenon and help service providers to design effective and efficient marketing plans that take into consideration the different personality traits and can thus drive the uptake of MB services by customers.

Although the significant effect of personality traits on a person’s decision-making process has been confirmed in other study areas (Costa & McCrae, 1992; Sproles & Kendall, 1986; Xu et al., 2016), little is known about its role in information system (IS) adoption though earlier works such as that of McElroy et al. (2007) have highlighted the germaneness of personality traits in expounding individuals’ IS adoption behavior. More so, recent research evidence shows the existence of a link between a person’s personality and their use of internet (Landers & Lounsbury, 2006; McElroy et al., 2007), collaborative technology (Devaraj et al., 2008), mobile commerce (Zhou & Lu, 2011), web utilization (Davis & Yi, 2012), hypothetical software tool (Svendsen et al., 2013), mobile apps (Xu et al., 2016), and particular apps such as “Foursquare” (Chorley et al., 2015). However, none of the existing studies has thus far explored the effect of personality traits on users’ intention to use MB services. Consequently, this present study aims to fill this important research gap by examining the role of personality traits in the adoption of MB.

To attain this purpose, the study adopts the TAM as its theoretical basis. TAM is a relevant model that offers vital theoretical and practical contributions in the field of IS (Davis et al., 1989). So, this research proposes a new research model that investigates the effects of personality traits on behavioral intention to use MB through perceptions of usefulness and ease of use. This study contributes significantly to the existing literature. First, to the best of the authors’ knowledge, this study is one of the first attempts in MB literature to examine and establish the influence of personality traits on TAM constructs. Still, this study extends the present understanding of personality traits to a germane technological context, MB. In so doing, this article fills a relevant gap in the literature by responding to calls for further examination of the role of personality traits in new technology adoption (Devaraj et al., 2008; McElroy et al., 2007). Moreover, this study offers an empirical basis for guidelines to MB service providers such as banks that could lead to the design of effective policies and actions that will increase the uptake of MB.

The rest of this article is ordered as follows. The next section presents the literature review, followed by the research model and hypotheses development. The methodology, discussion of the results, and implications of the study are offered next. The last part presents the limitations and suggestions for future studies.

Literature Review

TAM

TAM (Davis, 1989; Davis et al., 1989) originated from the theory of reasoned action (TRA) proposed by Fishbein and Ajzen (1975), and was primarily devised for modeling user acceptance and use behavior of information technology. TAM argues that perceived usefulness (PU) and perceived ease of use (PEOU) are the fundamental factors that influence systems adoption and use (Bangole et al., 2011; Davis et al., 1989). Prior studies (Adams et al., 1992; Doll et al., 1998; Subramanian, 1994) have confirmed the soundness and reliability of the PU and PEOU constructs in the TAM model.

The desirability of this model lies in the fact that it is both specific and parsimonious and exhibits a high level prediction power of technology use (Alalwan et al., 2016; Lee, 2009). Moreover, these factors are common in technology usage milieus and can be widely used to solve the acceptance problem (Lee, 2009; Taylor & Todd, 1995). The theory has also been argued to have an empirical advantage over theories such as TPB (Mathieson, 1991; Narteh et al., 2017). Indeed, Yousafzai et al. (2010) cited by Mohammadi (2015) who compared TAM, TRA, and TPB in online banking domain similarly found TAM to be superior to the other models and underscored its significance in understanding online banking behavior. In MB domain, Shaikh and Karjaluoto (2015) revealed that TAM appears to be very popular and often used as a framework for investigating intentions to accept MB.

Nonetheless, according to Venkatesh and Davis (2000), the TAM apparently has restricted use for explaining users’ attitudes and behavioral intentions toward mobile service adoption since it does not include economic and demographic factors and external variables. This view appears to be consistent with that of other researchers who posit that PU and PEOU would not be able to provide a clear and complete picture of explaining individual intention and behavior-related technology (Alalwan et al., 2016; Gu et al., 2009; Luarn & Lin, 2005; Mehrad & Mohammadi, 2017). As such, various MB adoption studies have expanded the original TAM by incorporating new constructs such as self-efficacy and perceived risk (Alalwan et al., 2016), personal innovativeness and relative advantage (Chitungo & Munongo, 2013), trust (Kim et al., 2009), and perceived security(Hsu et al., 2011). TAM, indeed, offers the provision to include external constructs as the determinants of PU and PEOU (Davis, 1989). In this regard, we argue in this study that personality traits influence behavioral intention to use MB via PU and PEOU.

Personality Traits

Personality is defined as a stable set of characteristics and propensities that establish peoples’ differences and commonalities in thoughts, feelings, and actions (Maddi, 1989; McElroy et al., 2007). According to Devaraj et al. (2008), people’s attitudes, beliefs, cognitions, and behaviors are to some extent ascertained by their personality. Furthermore, they argue that personality echoes the unique features of every person, that is, traits that depict our essence, and it is reflected in all of our thoughts and actions (Devaraj et al., 2008). While there is no universal perspective regarding the components of personality traits (Devaraj et al., 2008; Zhou & Lu, 2011), there exists substantial understanding among personality scholars that five comprehensive personality factors satisfactorily encapsulate the domain of personality (Davis & Yi, 2012; Digman, 1990; McCrae & Costa, 1987). This theoretical style to personality taxonomy is referred to as the “Five Factor Model” (also known as the “Big Five Model”), which comprises agreeableness (i.e., a person’s orientation toward being courteous, cooperative, and tolerant), conscientiousness (i.e., an individual’s tendency to concentrate on being careful, organized, thorough, and focus on achievement), neuroticism (i.e., one’s propensity to be stressful, nervous, anxious, and insecure), openness to new experience (i.e., one’s inclination to accept new ideas or accept newness), and extraversion (i.e., a person’s tendency to be sociable, active, talkative, and interactive; Chorley et al., 2015; Islam et al., 2017; Jani & Han, 2014; John & Srivastava, 1999; Xu et al., 2016). Scholars suggest that these constructs theoretically capture the essentials of one’s personality (Digman, 1990; McElroy et al., 2007).

Since its development, a number of scholars have employed the Big Five Model in different fields. For example, the Big Five personality traits have been used to analyze a number of consumer behavior variables, such as product knowledge (Füller et al., 2008) and consumer problem-solving modes (Mooradian et al., 2008). Similarly, past studies have adopted the model in studying technology acceptance (Ross et al., 2009), web utilization (Davis & Yi, 2012), internet use (McElroy et al., 2007), mobile apps (Xu et al., 2016), and the adoption of productivity mobile applications (Urueña et al., 2018). Nonetheless, there are limited empirical studies linking these personality traits to MB adoption. Therefore, this current study seeks to fill this void by incorporating the Big Five personality traits into the TAM model to examine how these personality constructs influence consumers’ MB adoption intentions.

Research Model and Hypotheses

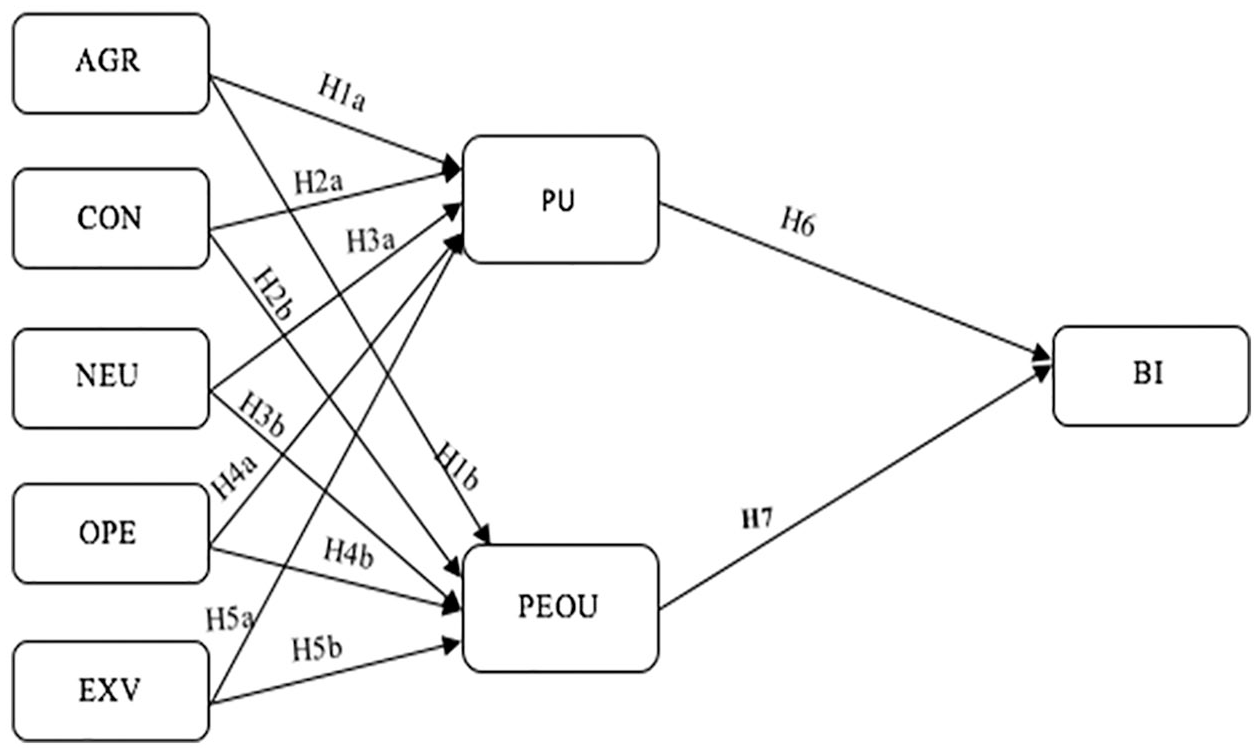

Figure 1 presents our proposed research model. The model is built on TAM and the Five-Factor model (also known as the “Big Five” personality traits). Behavioral intention establishes the behavior toward new technology (Farah et al., 2018), and is the key concept of the famous TAM. TAM is regarded as one of the most popular and acceptable models within the IS field (Alalwan et al., 2016; Venkatesh et al., 2003). The main precursors of TAM are PU and PEOU. The existing works show that personality traits could significantly affect TAM constructs (Devaraj et al., 2008; Svendsen et al., 2013; Uffen et al., 2013; Zhou & Lu, 2011). Thus, drawing inspiration from past studies, this study proposes a new model that explores the connection between the Big Five personality traits and the TAM constructs in MB context.

The proposed research model.

Agreeableness

Individuals with high agreeableness are kind, likable, considerate, forgiving, cooperative (Devaraj et al., 2008; McElroy et al., 2007; Xu et al., 2016), and also tend to build more trusting and friendly relationships with other people (Islam et al., 2017; Pervin et al., 2004). Moreover, people high in agreeableness give more consideration to maintaining harmony and avoiding conflict, compared to people scoring low on this facet. Research shows that the flexibility and tolerant nature of agreeable individuals makes them more likely to adopt new technologies effortlessly and expend more time on the internet (Devaraj et al., 2008; Urueña et al., 2018). Devaraj et al. (2008) also suggest that agreeable persons care more about the positive elements of a technology when it advances task execution. Researchers argue that personality may have a link to TAM constructs since it influences the rating behavior of the individuals (Barrick & Mount, 1996; Svendsen et al., 2013). In this sense, as MB allows customers to perform their financial-related transactions easily and at anywhere and anytime, people with high agreeableness may rate MB high on perceptions of usefulness and ease of use out of kindness or conformity and consequently adopt it. Agreeableness has been found to be a significant predictor of PU in a collaborative technology and mobile commerce settings (Devaraj et al., 2008; Zhou & Lu, 2011). In addition, Özbek et al. (2014) found that agreeableness is positively related to PEOU. It is, thus, hypothesized that:

Conscientiousness

Conscientiousness denotes traits such as self-discipline, being careful, self-control, being organized, and reliable (Islam et al., 2017; Jani & Han, 2014; McElroy et al., 2007; Xu et al., 2016). People with high conscientiousness actively plan, organize, and perform tasks. Uffen et al. (2013) assert that conscientious individuals are self-disciplined and inherently motivated to success. Studies indicate that highly conscientious people are not likely to use leisure mobile apps since they perceive them as unproductive and distracting (Xu et al., 2016). Indeed, Landers and Lounsbury (2006) uncovered that highly conscientious students were more likely to utilize the internet for academic purposes than leisure. Furthermore, according to Devaraj et al. (2008), conscientious individuals will be more probable to carefully consider means in which the utilization of technology would permit them to be more useful and perform at a higher level at a task. In addition, Hurtz and Donovan (2000) note that conscientiousness has motivational consequences, and suggest that it be considered not only as a direct predictor of behaviors but also as an indirect predictor via intentions. Given their deeper consideration, organized nature, and being planful, we anticipate that conscientious people will more likely use MB. Thus, we propose that:

Neuroticism

People with features of the neuroticism category are anxious, nervous, depressed, and worried (Jani & Han, 2014; John et al., 2008; Urueña et al., 2018). While people low in neuroticism are emotionally stable and well-adjusted (Xu et al., 2016), people high in neuroticism are self-conscious, fearful, prone to negative emotions and negative reactions to work-related stimuli (Devaraj et al., 2008), and are not likely to open themselves to new experiences (Zhou & Lu, 2011). This cluster of people lack confidence, which prompts them to regard new technologies and services as frightening and demanding, resulting in less internet use (Devaraj et al., 2008; Tuten & Bosnjak, 2001). Neuroticism has also been found to have a negative impact on PU and behavioral control, thereby reducing the intention to integrate new technologies into one’s daily life (Uffen et al., 2013). What is more, works by Devaraj et al. (2008), Zhou and Lu (2011), and Özbek et al. (2014) report that neuroticism has a negative influence on PU. Based on this, we expect people with high neuroticism to see MB as more complex and difficult to use, and consequently doubt its usefulness. Thus, we suggest the following hypotheses:

Openness to New Experience

Openness to new experience people are “imaginative, broad-minded, independent, and willing to try new things and seek for different experiences” (Xu et al., 2016). Furthermore, people with high openness to new experience also have the tendency to seek more thorough information, and have the desire to learn new things (Devaraj et al., 2008; Islam et al., 2017; Marbach et al., 2016; McElroy et al., 2007). They are independent thinkers who do not depend on tradition or norms (George & Zhou, 2001), unlike those low on this dimension who prefer stability and the status quo, and inherently feel very uncomfortable with change. Research shows that they are more likely to become innovators and early adopters of new technologies and services (Constantiou et al., 2006; Tuten & Bosnjak, 2001). While Özbek et al. (2014) and Svendsen et al. (2013) found a positive relationship between openness to new experience and PEOU, Uffen et al. (2013) found a positive link between openness to new experience and PU. Based on the ongoing discussion, we expect people high on the openness trait to hold positive attitudes and cognitions toward adopting new technologies such as MB, and therefore propose the following hypotheses;

Extraversion

“People who are high in extraversion are social, outgoing, active and talkative” (Xu et al., 2016). People high in extraversion are lively, social, and outgoing (John et al., 2008; Urueña et al., 2018), and put a great value on close and deep interpersonal relationships (Devaraj et al., 2008; Uffen et al., 2013; Watson & Clark, 1997). Past studies have linked extroversion to higher use of internet, social app, and social network (Amiel & Sargent, 2004; Correa et al., 2010; Xu et al., 2016). Moreover, according to Zmud (1979), extraverts largely have more positives toward IS than others. Similarly, Svendsen et al. (2013) uncovered that extraversion has positive effects on PU and PEOU. Given extraversion’s origins in adventurous behaviors, both in and out of social settings (Davis & Yi, 2012), we envisage that extraverts will be more probable to adopt MB. Thus, we suggest the following hypotheses:

PU

PU “reflects the degree to which a person believes that using a particular technology would improve his or her job performance” (Davis, 1989). PU is one of the main precursors of TAM (Sharma, 2017), and is regularly found to have a significant effect on new technology adoption (Chong et al., 2015; Liebana-Cabanillas et al., 2017; Venkatesh & Davis, 2000). According to IS scholars, PU mostly has a stronger effect on new technology adoption compared to PEOU, which is another essential TAM construct (Adams et al., 1992; Davis, 1989). Previous works show that PU is positively related to the acceptance of MB (Gu et al., 2009; Makanyeza, 2017; Shaikh & Karjaluoto, 2015). Moreover, it has been identified as having a significant and positive effect on MB acceptance across countries, including Jordan, Iran, Germany, and Australia (Alalwan et al., 2016; Koenig-Lewis et al., 2010; Mohammadi, 2015; Wessels & Drennan, 2010). Indeed, PU is one of the most extensively studied construct in the acceptance of any new technology, including MB (Sharma, 2017). Thus, we posit the following hypothesis:

PEOU

PEOU reflects “the degree to which prospective users expect the target system to be free of effort” (Davis, 1989). Studies suggest that PEOU has a significant effect on users’ intention to adopt any new IS (Adams et al., 1992; Chong et al., 2015; Davis, 1989; Sharma, 2017). For customers to use and access MB services, a certain degree of knowledge and skill is necessary; therefore, PEOU could play an important role in shaping customers’ intention to use such technology (Alalwan et al., 2016). This argument has been empirically supported by several studies in different areas, for example, in mobile payment context (Kim et al., 2010; Liebana-Cabanillas et al., 2014), in internet banking (Chong et al., 2010), and in MB settings (Alalwan et al., 2016; Hanafizadeh et al., 2014; Koksal, 2016; Sharma, 2017). Yet, some studies, including Makanyeza (2017) found no significant link between the PEOU and the intention to use MB. Thus, the studies relating to PEOU and behavioral intention toward new technology adoption show mixed results. So, we postulate the following hypothesis:

Research Methodology

Sample and Data Collection

The present study utilized a survey research design to address the research question. The population of the study was MB users of bank customers in Ghana. A convenience non-probability sampling approach was employed as a result of resource and time constrictions. This method, however, is in line with the method adopted in several prior technology acceptance research studies (Afshan & Sharif, 2016; Farah et al., 2018; Luarn & Lin, 2005). Before the questionnaires were distributed, a two-round pretest was conducted to revise items with unclear expressions and to ensure the validity of the measurement in MB context. The first of the two pilot tests was conducted with one information technology (IT) senior lecturer and three PhD students. The purpose of this test was to enable them confirm the validity of the measurement items and to detect any unclear expressions and points of confusion. Based on their suggestions, the scales went through minor revisions. The revised scales were then used in the second phase of the pilot test, involving 25 MB users conversant with MB services. The pretest at this stage revealed no major difficulties with regard to wording and structure. The questionnaire was considered simple to comprehend and complete, and needed only a few slight phrasing modifications which were done accordingly, and the final version of the questionnaire was produced. The questionnaire was in two sections. Section one measured the demographic features of the participants, and the section two measured the respondents’ perception of the constructs in the research model.

The survey was conducted from January 3 to February 28, 2018, by five trained senior students and two researchers. The questionnaires were administered at the head offices of five major banks in the capital city of Ghana, selected according to size and popularity. Accra, the capital city of Ghana, is the place where most banks are headquartered. It is the Greater Accra region’s administrative and economic hub with economic activities, including commercial and financial sectors, among others. First, we gained permission from the head office managers of the banks and then clarified the aim of the research to the respondents prior to distributing the questionnaires to them. Following past studies (Boateng et al., 2016; Hernandez et al., 2011; Wang et al., 2011), the present study concentrated on MB users aged between 20 and 49 years, as the youth have been classified as technology savvy. Only customers who have had prior experience with MB services were included in the study. Among the 500 questionnaires that were distributed, 18 were dropped due to invalid responses and missing data. Thus, 482 valid questionnaires were eventually used in the data analysis. As shown in Table 1, the sample involves 55.8% males and 44.2% females. In terms of age, the results indicate that the majority of the respondents are aged between 20 and 39 years (80.5%) whereas 19.5% are aged between 40 and 49 years. In addition, about 70.9% of the respondents had attained at least a bachelor’s degree. As regard the respondents’ relationship with banks, majority (63.3%) had been banking for more than five years.

Profile of Respondents.

Measures

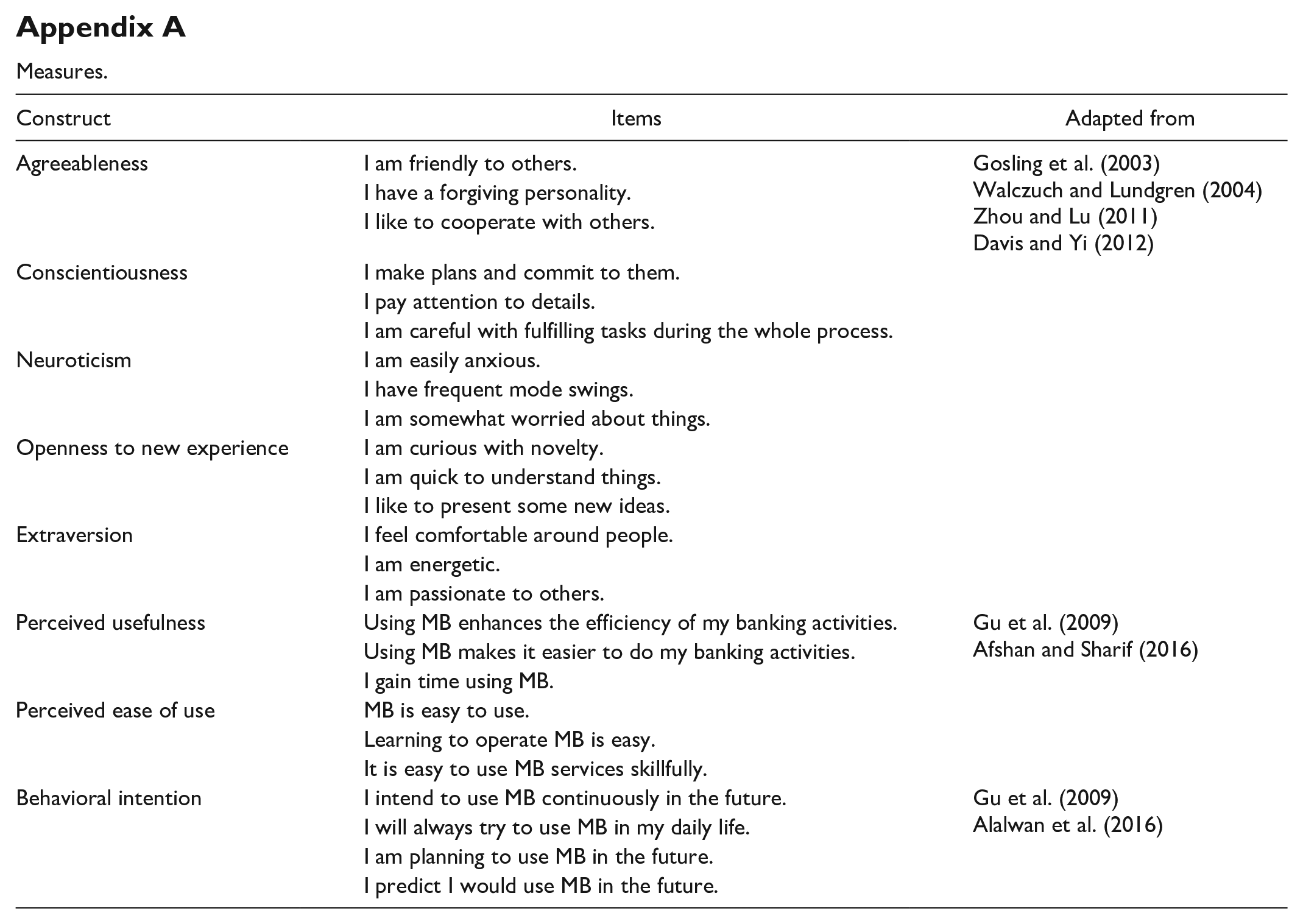

All the measures employed in this study were adapted from prior research to enhance the content validity, and were duly modified to suit this research. The Big Five personality traits items were sourced from Gosling et al. (2003), Walczuch and Lundgren (2004), Zhou and Lu (2011), and Davis and Yi (2012). PU and PEOU were measured by using scales taken from Gu et al. (2009) and Afshan and Sharif (2016). Finally, behavioral intention was gaged by employing items adapted from Gu et al. (2009) and Alalwan et al. (2016). The responses were collected on a five-point Likert-type scale ranging from 1= strongly disagree to 5 = strongly agree. Taken together, 25 items were employed to measure 8 constructs (Appendix A).

Analysis and Results

The statistical data analysis was done in two steps. First, the validity of the conceptualized research model was evaluated. The reliability of model constructs was determined by considering the value of Cronbach’s α coefficient. Furthermore, the convergent and discriminant validity, in addition to composite reliability, was examined using confirmatory factor analysis (CFA). Next, structural equation modeling (SEM) was employed to test the proposed research hypotheses. Data analysis was carried out in SPSS and AMOS.

The results of the reliability analysis as shown in Table 2 indicate that all α coefficients were well above the cut-off point of 0.700, suggesting a high level of internal consistency for every construct (Hair et al., 2010). Specifically, the values of Cronbach’s α coefficient ranged between 0.841 and 0.918. Furthermore, the composite reliability (CR) values for all constructs were within their respective level of 0.700, recommended by Hair et al. (2010) ranging between 0.860 and 0.924 (Table 2), signifying adequate construct’s internal consistency.

Measurement Scale and Scale Reliability Values.

Note. AVE = average variance extracted; AGR = agreeableness; CON = conscientiousness; NEU = neuroticisms; OPE = openness to new experience; EXV = extraversion; PU = perceived usefulness; PEOU = perceived ease of use; BI = behavioral intentions.

The validity analysis included both convergent validity and discriminant validity. An average variance extracted (AVE) shown in Table 3 for each construct was higher than the squared correlation coefficient for corresponding inter-constructs, thereby providing support for discriminant validity (Fornell & Larcker, 1981). Moreover, convergent validity was confirmed by the fact that all AVEs (see Table 2) were greater than 0.500, specifically ranging from 0.672 to 0.754. In addition, the CFA results shown in Table 2 provide further confirmation for the convergent validity of measures since the estimated loadings for all the indicators were significant at p < .001 (Anderson & Gerbing, 1988). To evaluate the fit of the proposed model, the values of the corresponding goodness-of-fit indices were analyzed, and the results from the CFA show that the overall fitness indices were satisfactory. The CMIN/DF was 2.418, which is within the suggested range of 1 to 3 (Carmines & McIver, 1981). Also, acceptable values were obtained based on other fit indices including (GFI = 0.902, AGFI = 0.869, CFI = 0.930, NFI = 0.901, IFI = 0.931, TLI = 0.913, RMR = 0.029, RMSEA = 0.058), indicating the model satisfactorily fits the data. Thus, since the AGFI value was greater than 0.800, the values of GFI, CFI, NFI, IFI, and TLI were greater than 0.900, and the RMSEA value was also within the desirable interval between 0.050 and 0.080 (Hair et al., 2010), it can be concluded that the proposed model adequately fits the data.

Means, Standard Deviation, and Discriminant Validity.

Note. AGR = agreeableness; CON = conscientiousness; NEU = neuroticisms; OPE = openness to new experience; EXV = extraversion; PU = perceived usefulness; PEOU = perceived ease of use; BI = behavioral intentions.

Bold values are the square root of variance shared between the constructs and their measures.

In addition, bearing in mind the validity of self-report questionnaires, this research checked the possibility of common method variance (CMV) with Harman’s single-factor test (Podsakoff et al., 2003). In the single-factor test, all of the study items are normally subjected to exploratory factor analysis (EFA). As an alternate to EFA, CFA can be employed in executing Harman’s single-factor test. The CFA approach, in particular, can model all of the manifested items as the indicators of a single factor that represents method effects (Malhotra et al., 2006). The single-factor model in CFA fitness indices (CMIN/DF = 4.832, GFI = 0.719, AGFI = 0.684, CFI= 0.567, NFI = 0.512, IFI = 0.536, TLI = 0.509, RMR = 0.063, RMSEA = 0.089) does not produce a better result than the current model, signifying that CMV is not a concern in this data set.

Structural Model

SEM with maximum likelihood estimation was used to test the posited relationships among latent variables. Table 4 and Figure 2 show the results. An examination of the goodness-of-fit indices revealed that the structural model fits the data well (CMIN/DF = 2.701 GFI = 0.906, AGFI = 0.870, NFI = 0.904, IFI = 0.928, TLI = 0.908, CFI = 0.927, RMR = 0.030, RMSEA = 0.063). In the path analysis, significance of a path is determined on the basis of its p value. As indicated, Table 4 indicates the standardized path coefficients (β) and p values, and Figure 2 shows the variance explained by the research model (R2). The results showed that 56.8% and 42.2% of the variances in PU and PEOU, respectively, are explained by the relevant personality trait dimensions, whereas PU and PEOU are able to explain 69.2% of the variance in behavioral intention to use MB.

Standardized Path Coefficients.

Note. PU = perceived usefulness; AGR = agreeableness; PEOU = perceived ease of use; CON = conscientiousness; NEU = neuroticisms; OPE = openness to new experience; EXV = extraversion; BI = behavioral intentions.

Result of the model.

The structural model results displayed in Table 4 and Figure 2 reveal that the effect of agreeableness (H1a: β = .401, t = 7.008, p = .000), conscientiousness (H2a: β = .402, t = 5.989, p = .000), (H3a: β = −0.090, t = 1.961, p = .050), and openness to new experience (H4a: β = .358, t = 5.133, p = .000) on PU were significant. However, the impact of extraversion (H5a: β = .084, t = 1.803, p = .071) on PU was insignificant. Hence, H1a, H2a, H3a, and H4a were supported, but H5a was not supported. In addition, while the effects of agreeableness (H1b: β = .344, t = 5.331, p = .000), conscientiousness (H2b: β = .214, t = 2.930, p = .003), and openness to new experience (H4b: β = .292, t = 3.672, p = .000) on PEOU were statically significant, the effects of neuroticism (H3b: β = −0.082, t = −1.467, p = .142) and extraversion (H5b: β = .078, t = 1.373, p = .170) on PEOU were not significant. Thus, H1b, H2b, and H4b were supported, but H3b and H5b were not supported. Furthermore, the results show that PU (H6: β = .693, t = 10.049, p = .000) and PUEOU (H7: β = .268, t = 4.848, p = .000) significantly affect behavioral intention to use MB, supporting H6 and H7.

Moreover, as exhibited in Figure 3, the total effects (direct + indirect effect) of the Big Five personality traits of agreeableness (0.370) was larger than conscientiousness (0.336), openness to new experience (0.326), extraversion (0.079), and neuroticisms (–0.085).

Total standardized effect on behavioral intensions.

Discussion

The study attempted to examine whether personality traits influence users’ intention to use MB via perceptions of usefulness and ease of use. Based on the results, our proposed research model was able to attain an adequate level regarding predictive power obtained by the dependent variables: PU (56.8%), PEOU (42.2%), and intention to use MB (69.2%). Moreover, the value of R2 accounted in behavioral intention was in the very acceptable limits and beyond the suggested values proposed by some scholars (Alalwan et al., 2017; Holmes-Smith et al., 2006; Kline, 2011; Sharma & Sharma, 2019; Straub et al., 2004). Also, the value of variance is fairly above other similar research studies that used the Big Five personality traits. For instance, while Zhou and Lu (2011) reported a variance explained in behavioral intention to use mobile commerce of 45.7%, Svendsen et al. (2013) obtained 63% of variance in behavioral intention to use a hypothetical software tool.

In terms of the path coefficient analyses (see Table 4), the results generally confirm the research hypotheses. The results indicate that all personality traits significantly affect PU of MB, but extraversion. Specifically, conscientiousness was uncovered to have a salient influence on PU. This relationship could be explained by the fact that users with high conscientiousness would carefully look for ways in which the use of MB would allow them to be more productive and perform at a greater level at a task (Devaraj et al., 2008). Thus, the result implies that conscientious users are more likely to find MB useful after having carefully considered ways to use it. Our result agrees with a similar finding obtained by Uffen et al. (2013). Agreeableness was also found to have a significant effect on PU, thereby corroborating prior studies (Devaraj et al., 2008; Zhou & Lu, 2011). This result backs the assertion that users scoring high on agreeableness might give a system such as MB a high rating in terms of its PU out of kindness or conformity (Svendsen et al., 2013). Moreover, we found a significant link between openness to new experience and PU, thus implying that users high on optimism are almost expected to assess an innovation such as MB as more valuable than users low in this trait. This finding supports Uffen et al. (2013). Similarly, neuroticism showed a significant and negative impact on PU, hence providing empirical backing for earlier studies by Devaraj et al. (2008), Özbek et al. (2014), and Zhou and Lu (2011). Indeed, given their nature, neurotic users cannot easily perceive the usefulness of MB. Nonetheless, the impact of extraversion on PU was insignificant. Although our result contradicts Svendsen et al. (2013) who found extraversion to be a salient predictor of PU, it confirms Zhou and Lu’s (2011) and Özbek et al.’s (2014) conclusions that extraversion does not have any significant impact on PU.

In addition, the results establish that conscientiousness, agreeableness, and openness to new experience significantly affect PEOU. These findings are largely in line with prior studies (Özbek et al., 2014; Svendsen et al., 2013). Conscientious users are strong-willed and reliable (Chorley et al., 2015; Islam et al., 2017; Jani & Han, 2014; Xu et al., 2016), and will find a considerable time to actively plan and figure out how to use MB services. Agreeable users tend to care more about the upbeat elements of a technology such as MB when it fosters task accomplishment (Devaraj et al., 2008; Xu et al., 2016), and may give MB services a high rating on PEOU (Svendsen et al., 2013). Likewise, users scoring high on the openness to new experience are more willing to try new and different things such as MB (John et al., 2008; Marbach et al., 2016; McElroy et al., 2007). Due to their curious mind and desire to keenly look for new and wide-ranging experiences (Islam et al., 2017; Madjar, 2008), they will find MB easy to use. While our result contradicts Uffen et al. (2013), it supports that of Özbek et al. (2014). Also, both neuroticism and extraversion did not indicate any significant effect on PEOU, thus agreeing with Özbek et al. (2014).

Furthermore, we found that both PU and PEOU significantly affect behavioral intention to use MB services. These results complement previous studies that have established a significant influence of PU and PEOU on users’ behavioral intention (Alalwan et al., 2016, 2017; Farah et al., 2018; Hanafizadeh et al., 2014; Liebana-Cabanillas et al., 2017; Sharma, 2017; Uffen et al., 2013). The results thus imply that MB users are not only interested in the usefulness of MB services but also prefer the ease in its usage. Finally, among the Big Five personality traits (Figure 3), agreeableness exhibited the highest total effects, followed by conscientiousness, openness to new experience, extraversion, and neuroticism.

Theoretical Contributions

Theoretically, this study has been able to move forward the literature relating to the role of personality traits in technology acceptance by exploring the relationships between the Big Five personality traits and users’ intention to use MB through PU and PEOU. Several studies (e.g., Farah et al., 2018; Gu et al., 2009; Makanyeza, 2017) have investigated the impact of several factors on customers’ intention to adopt MB. However, none of them has so far considered the important role of personality traits in driving the customers’ perceptions of usefulness and ease of use. From the findings, the Big Five personality traits accounted for more than half of the variance in PU (56.8%) and nearly half of the variance in PEOU (42.2%). Accordingly, this study’s proposed and validated model may be employed as a source of reference for other future studies interested in investigating the effect of the Big Five personality traits on PU and PEOU and their ensuing effects on users’ intention to MB. Also, the study is among the first to investigate the impact of the Big Five personality traits in MB context. As stated earlier, empirical evidence on the influence of personality traits on users’ intention to adopt MB is scant. This study attempted to fill this void, and the results show some significant findings on the relevance of personality traits in MB adoption from a developing country perspective, which significantly expands and enhances the extant literature.

Managerial Implications

From a managerial standpoint, the diverse impacts of the Big Five personality traits on user adoption through PU and PEOU suggest that MB service providers need to carry out market segmentation based on customers’ personality traits (Islam et al., 2017; Zhou & Lu, 2011), and take advantage of the specific personality traits that are anticipated to boost MB uptake. For instance, persons with high agreeableness and openness to new experience have a greater tendency to perceive MB services as more useful and easy to use. Neurotic users (who are presumed to be nervous, preservationist, and unconfident) represents the laggards (Jani & Han, 2014; Urueña et al., 2018; Xu et al., 2016; Zhou & Lu, 2011), so MB service providers (e.g., banks) need to adopt measures to ease these users’ fear and doubt with MB services by offering simple to follow user guides, specific awareness programs, and training about the advantages and use of MB services (Zhou & Lu, 2011). Moreover, to encourage adoption, service providers should focus on designing effective marketing strategies that will meet their needs and recognize different user personality traits. Again, practitioners and MB services providers such as banks can gain deeper insight from the findings of this study which could help in the design and expansion of MB services for their customers.

Limitations and Suggestions for Future Studies

Future study could take this research further by addressing the following limitations. First, our sample was mainly drawn from MB users, leaving out those users who use similar technologies such internet banking, mobile payment, and m-shopping. Therefore, future studies should extend the investigations to other user groups such as internet banking, and to ascertain potential differences between the user groups. Second, the findings of study have shown that the Big Five personality traits affect behavioral intention via PU and PEOU. However, past works (Barnett et al., 2014; McElroy et al., 2007; Urueña et al., 2018) show that the Big Five personality traits may drive actual adoption of a technology. Therefore, the effects of these personality traits on actual adoption of MB should be investigated. Third, future studies may also control the sociodemographic factors (e.g., age, gender, income) of the participants to establish the variations in the results.

Footnotes

Appendix

Measures.

| Construct | Items | Adapted from |

|---|---|---|

| Agreeableness | I am friendly to others. |

Gosling et al. (2003)

Walczuch and Lundgren (2004) Zhou and Lu (2011) Davis and Yi (2012) |

| I have a forgiving personality. | ||

| I like to cooperate with others. | ||

| Conscientiousness | I make plans and commit to them. | |

| I pay attention to details. | ||

| I am careful with fulfilling tasks during the whole process. | ||

| Neuroticism | I am easily anxious. | |

| I have frequent mode swings. | ||

| I am somewhat worried about things. | ||

| Openness to new experience | I am curious with novelty. | |

| I am quick to understand things. | ||

| I like to present some new ideas. | ||

| Extraversion | I feel comfortable around people. | |

| I am energetic. | ||

| I am passionate to others. | ||

| Perceived usefulness | Using MB enhances the efficiency of my banking activities. |

Gu et al. (2009)

|

| Using MB makes it easier to do my banking activities. | ||

| I gain time using MB. | ||

| Perceived ease of use | MB is easy to use. | |

| Learning to operate MB is easy. | ||

| It is easy to use MB services skillfully. | ||

| Behavioral intention | I intend to use MB continuously in the future. |

Gu et al. (2009)

|

| I will always try to use MB in my daily life. | ||

| I am planning to use MB in the future. | ||

| I predict I would use MB in the future. |

Acknowledgements

We thank the anonymous reviewers for their invaluable comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.