Abstract

The dogma of conscious environmental behavior has laid the paradigm for sustainable consumer behavior. Modern-day corporates have introduced innovative business models to add a new value to manage fluctuations in consumer behaviors and rejuvenate their financial performance. Similarly, in fashion industry, textile firms have warmly embraced the new business models and widely adopted environmental management systems (EMSs) to contribute to environmental sustainability. This research aims to explore eco-consumerism and its impacts on the financial performance of textile firms in Malaysia. The secondary data of textile firms’ performance from 2013 to 2015 were collected from an online database and annual reports of firms’ web portals. The findings reveal that the textile firms which successfully adopted EMS such as ISO 14001 show significant changes in performance compared with firms which are yet to adopt EMS certification. Moreover, eco-consumerism directly impacts EMS-adopted firms’ performance. Our findings are robust for practical, research, and managerial implications to classify and understand the impacts of consumers’ green behavior on corporate performance. This study contributes to understand the influence of consumers’ eco-behavior to adopt EMS and its impact on the financial performance of textile firms in Malaysia.

Introduction

The foundation of environmental paradigm laid by Catton and Dunlap (1978), the 2030 Agenda of Sustainable Development, and the Paris Agreement have increased the attention toward the interface between society and natural environment and the significance of humans’ conscious environmental behavior (Rahman & Reynolds, 2019). One of the facets of conscious environmental behavior is known as eco-consumerism (EC), which is practiced by modern-day industries and markets. The onset of green products and EC has diverted practitioners and scholars’ attention to analyze specific stimulus of EC. Arguably, corporates and marketplace are influenced by the huge potential and impact of EC, as clear opportunities exist to influence the current market dynamics through effective and environmentally appealing strategies. A prominent strategy is enhancing consumers’ knowledge and awareness pertaining to the dilemmas of human environmental impact (Owens, 2000; Stern & Dietz, 1994). The supplementary strategies include the production of affordable, safe, eco-friendly, and proficient goods which can generate financial incentives for corporates (Vugt et al., 1995). In addition, socially driven motives are characterized as a potential influencer of demonstrating green behavior (Vugt, 2009).

Environmental concern or belief and consumption of green products refer to green consciousness or green behavior (Kim & Damhorst, 1998). Consumers’ sustainable consumption is a decision-making process which incorporates social responsibility and social needs according to his or her taste, price, and convenience (Vermeir & Verbeke, 2008). Sustainable consumption is a relatively recent terminology that emerged due to United Nations (UN) Agenda 21 and UN’s 1992 Earth Summit in Rio (Vitterso & Tangeland, 2014). This Agenda focuses on promoting sustainable environment consumption to encounter basic human needs (Vitterso & Tangeland, 2014). A few studies claim to have analyzed consumers’ attitude toward environmental activities of corporates (Creyer, 1997; Ogle et al., 2004), yet there is a dearth of analytical studies on the relationship between consumers’ green consciousness and corporates’ environmental actions in response to global demand for green products especially in apparel industry. In addition, the implementation of environmental strategies and its impact on the financial performance of apparel firms largely remain unexplored. The findings of previous studies are inconclusive as these studies do not analyze the implemented environmental strategies, particularly in response to consumers’ green behavior (Moneva & Ortas, 2010; Nakamura, 2011; Pérez-Calderón et al., 2011, 2012). The broad objectives of this study are to explore the green strategies implemented by the apparel fashion firms of Malaysia, the developed international standards of being labeled as a green corporate, and the financial outcomes of the environmental standards.

Recent studies have extensively explored the relationship between responsible behavior and socially sustainable behavior of corporates and their financial performance (Lassla et al., 2017). Corporates contribute to sustainability through corporate social responsibility (CSR), which broadly involves all stakeholders of the society (Adams, 2002). The key terminology “triple bottom line” was developed in business management to incorporate people (social), profit (economic), and planet (environmental), which are known as the main aspects of the modern-day corporates. These aspects are implemented together with sustainability due to emerging demand of deep globalization experienced by the current markets. The improvisation of these actions improves corporate image as it is perceived the best possible response to stakeholders’ demand (Oh et al., 2017). In the context of today’s complex business environment, it is predicted that corporate sustainability resulted due to social responsibility practices that may influence financial performance. Aggarwal (2013) advanced that the inclusion of sustainability criteria in the main business model generates strategic benefits and contributes to firm’s value creation.

Like many other manufacturing and service industries, the fashion industry has also amiably incorporated EC phenomena and has started to shift its business operations to sustainability and ethical conduct (Joy et al., 2012). As water scarcity and climate change agitation continue to propagate, the fashion industry continues to intensify the situation through 10% global CO2 emission, 20% global industrial wastewater, 24% insecticide usage, and 11% pesticide usage (Koll, 2018). Interestingly, 70 to 150 L of freshwater is wasted during the manufacturing process just to dye 1 kg of cloth (Razzaq et al., 2018). Hence, sustainability has become one of the core components of operational priorities of global apparel industry as consumers have started to demand where, how, and in what capacity their goods are made (Adegeest, 2017). In addition, a sustainable and ethical apparel industry operation may contribute to minimize pollution, conserve resources, peg safety at work, and promote innoxious, durable, and quality products for consumers (Dickson et al., 2009; Shen et al., 2017). EC has simultaneously stimulated the demand for eco-friendly apparel market and has developed the methods to grow cotton without the use of pesticides, which is harmless to the environment (Organic Trade Association, 2016).

An empirical survey of past studies indicates that most studies are concentrated on analyzing consumers’ value and motivation behind sustainable apparel consumption (Ciasullo et al., 2017; Gwozdz et al., 2017; Lundblad & Davies, 2016). In addition, a few studies explore the gender difference in sustainable apparel consumption (Tung et al., 2017). These studies conclude that, based on consumers’ eco-behavior, a significant difference exists that may differently impact the corporates. The financial impact of consumers’ eco-behavior on corporates has largely remained unexplored especially in the apparel industry. Building on this knowledge gap, we seek to move forward to examine the financial impact of eco-behavior on Malaysian apparel fashion industry. The Malaysian apparel industry was specifically adopted due to the fact that despite significant ethical manufacturing and recycling initiatives of apparel fashion giants such as H&M, Uniqlo, Kloth, and Dresstal, the fashion industry is unable to exhibit exceptional performance.

The remaining article is organized as follows: Section “Literature Review” discusses literature related to EC, green initiatives of Malaysian fashion industry, and financial impact of EC on firms. Section “Methodology” details the methodology deployed in this study, and section “Results and Discussion” describes the results and discusses the findings. Finally, section “Conclusion” summarizes this study and its practical implications.

Literature Review

EC in Fashion

EC is generally characterized as a type of prosocial consumer green behavior (Wiener & Doescher, 1991). Moisander (2007) explicated it as a form of socially conscious (Anderson & Cunningham, 1972) or responsible (Antil, 1984) consumer behavior, indicating the positive consumers’ concern toward fairer, safer, cleaner, and transparent fashion industry (Fashion Revolution, 2019), which leads to an increase in environmentally concerned consumption (Cerchia & Piccolo, 2019). Eco-consumers generally prefer to purchase and consume green, environment-friendly, pro-environmental, or sustainable products. Hence, for the purpose of this study, EC is referred to as environmentally significant and responsible behavior, proactive environmental behavior, and ecological safe behavior in terms of product consumption, which in short is described as sustainable consumption. It is a decision-making process which represents consumers’ needs, taste, price, and convenience along with social responsibility (Vermeir & Verbeke, 2008). Pro-environmental behavior can be described through attitude-action gap theory, which is a phenomenon that specifies consumers who are concerned with environment but find it difficult to transform their behavior into sustainable consumption (Liu et al., 2017). Ethical decisions during the purchase involve consideration of environmental safety, protection of animals, and welfare of humans (Young et al., 2010). The ethical consumption statistics indicate that when it comes to the purchase of ethical products, consumers spent approximately £41,142 million in year 2019 (Ethical Consumers Markets Report, 2019); however, in terms of ethical and secondhand clothing purchase, only 19.9% and 22.5% increase was seen in the United Kingdom (Ethical Consumers Markets Report, 2018).

The authors in the past have regarded sustainable fashion consumption as a complex phenomenon. Therefore, researchers and practitioners highly disagree on any specific definition of sustainable fashion consumption (Jackson, 2008). It is not a mere replication of environmentalism; instead, sustainable fashion consumption is a broad spectrum which has extended its scope beyond its consequences (Thomas, 2008). Marketers often use terms such as ethical fashion, environment-friendly fashion, and green fashion to achieve higher sales and to attract the customers. This has further complicated the situation, as both customers and researchers often fail to interpret the exact meaning of sustainable fashion consumption (Peattie, 1995). In addition, these days global apparel manufactures have established their companies in South Asian countries such as India, Bangladesh, and Pakistan, which is increasing cynicism among customers as it becomes impossible for consumers to determine whether the entire aspects of supply chain comply with the merits of sustainability (Razzaq et al., 2018).

Although consumers represent increasing concerns toward sustainability and environmental protection, however, in reality consumers are not motivated to practice sustainable fashion consumption (Goworek et al., 2012). Furthermore, during the purchase of their clothes, consumers often do not investigate the compliance with environmental protection standards in the manufacturing process (Ritch & Schroeder, 2012). Hence, it is contemporary to investigate what motivates the consumers to represent eco-friendly behavior during the purchase of their clothes (Hustvedt & Dickson, 2009; Niinimäki, 2010). Usually, consumers use systematically planned behavior to initiate the purchase of eco-friendly clothes. First, consumers develop a relevant strategy to change their behavior through awareness of green clothes. Second, fashion consumers use self-efficacy known as a nudging in fashion industry to understand the underlining value offered by the green clothes (Steg & Vlek, 2009). A survey conducted in 2019 by Hotwire shows that global consumers abandoned 47% of internet-based brands that fail to comply with sustainability and their personal beliefs (Rosmarin, 2020), which indicates that ethical values play a significant role in sustainable behavior of consumers (Finegan, 1994). Another major factor that influences consumer behavior is the emergence of fast fashion, which has resulted in speedy manufacturing and poor disposition of clothes (Jung & Jin, 2014).

Green Initiatives of the Malaysian Fashion Industry

The US$44 billion Malaysian textile industry produces 2 million kilograms of textile waste every day, and a single cotton t-shirt takes about 6 years to decompose (Chng, 2018). The sustainable fashion awareness remains low among Malaysians, which means global fashion brands may place a heavy burden on landfills that will escalate shortage of freshwater. However, recent changes in the political environment and the historical fusion of Malay, Chinese, Indian, and indigenous people have forced the global apparel manufacturers such as H&M, Bershka, Forever 21, and Kloth to focus on producing and marketing eco-friendly textiles (Rabimov, 2018).

The apparel industry is generally categorized as less sustainable because of its negative impact on the environment, such as described by Deloitte (2013); approximately 100 billion clothes are manufactured around the globe, which is 13 times higher than the world’s total population (United Nations, 2017). Besides financial gains, human needs, status consciousness, thoughts, and the role in society remain the major reasons of today’s massive cloth production (Niinimäki, 2010). Yet, consumers have a decisive role to transform the clothing consumption into a sustainable one (Razzaq et al., 2018).

Malaysian fashion industry recognized sustainable fashion issue in 2018 when various global brands made pragmatic steps to address the environmental impact. The awareness of sustainable fashion consumption and its impact on the environment remain low among Malaysian fashion consumers (Rosli, 2018). The rapid expansion of fast fashion, which is a phenomenon that began in 2000 based on low-cost model used by the fashion industry, has resulted in the lack of awareness of sustainable fashion consumption. The companies in fast fashion clothing industry frequently introduce cheap and latest trending clothes in the market to easily attract consumers. This creates an addiction to short-lasting clothes among consumers, which generates profits for the companies; however, such addictions incorporate severe damages to the environment (Rosli, 2018).

EC is gradually shifting to developing countries, and Malaysia is no exception (Tiwari et al., 2011). The increase in consumers’ awareness and the performance of green fashion companies are the major reasons. The past studies on sustainable apparel fashion in Malaysia generally investigate green firms’ performance (Hasan & Ali, 2015), environmental management systems (EMSs) and its impacts on textile firm performance (Lo et al., 2012), cognitive and self-effects of eco-friendly apparel consumption (Tung et al., 2017), and the fashion and pro-environmental involvement of sustainable clothing consumption (Razzaq et al., 2018). However, no specific study has analyzed the impact of consumers’ sustainable fashion consumption on Malaysian apparel firms’ performance, despite government’s and apparel fashion firms’ generous efforts to protect the local environment such as the development of Ministry of Energy, Green Technology and Water (KeTTHA) in 2009 to promote and encourage the public to utilize green technology and consume eco-friendly products.

Other local initiatives include Kloth’s 100% recycled polyester yarns made from plastic bottles, which are then used for the production of high-quality fabrics (Rosli, 2018). Malaysian Green Technology Corporation awarded MyHIJAU Mark certification to Kloth under the textile and waste sector category. Similarly, H&M has initiated a recycling campaign throughout the country to handle its end-of-life project. H&M collected 17,771 tons of textiles by the end of year 2017 to recycle the textile waste. The government-led initiative of Malaysian Green Technology Corporation (MGTC) is predicted to promote sustainability as the government has set a certain quota for each industry to produce and utilize green products. A fashion revolution week in collaboration with FIBERS organized a boot camp for fashion designers to develop their fashion enterprise based on triple bottom line framework which aims to comply with the triple bottom line approach (Rosli, 2018).

Financial Impacts of EC

The eco-fashion market has grown tremendously in recent years. The average consumer today purchases 60% more clothes compared with 20 years ago, which has made the apparel industry a hallmark of the fashion industry (Koll, 2018). The organic apparel industry manufactured clothes worth US$65.8 billion worldwide (Organic Trade Association, 2018). These figures indicate that consumers’ interest and preferences have shifted toward environment-friendly fashion products. The survey indicates that 53% of consumers are willing to pay more for sustainable products; when it comes to clothing, 56% of consumers are directly motivated by retailers to purchase ethical clothes (PriceWaterhouseCoopers [PWC], 2019). Consumers these days prefer to use suppliers’ EMS as a criterion to purchase green apparel products (Boiral & Sala, 1998; Hamner, 2006; Lo et al., 2012; Meyer, 2001). Modern-day apparel industry firms in the United States such as Levi Strauss, Nike, Gap, and Eddie Bauer have developed their own environmental compliance criteria standards. Yet, many firms are highly dependent on globally recognized EMSs and third-party verification to evaluate suppliers’ environmental performance (EP).

Although the fashion industry has taken steps to become green to cater to consumers’ needs and contribute to sustainability, corporate sales of eco-products have shown a significant decline such as in the U.S. market (Clifford & Martin, 2011; Gleim et al., 2013). Even some eco-apparel lines failed to grab consumers’ attention (Kobori, 2015; Osborne, 2006) due to their unconscious environmental damage on water consumption and increase in water and washing pollution (Hornor, 2019). Consumers identified several barriers to acquire eco-friendly apparel, for instance, escalating prices, lack of knowledge, uncertain quality, trust on certain corporates, and product availability (Connell, 2010). The product categories are described as a major reason for these barriers, which is an indication of corporates’ failure to develop efficient green marketing strategies to adopt environmental innovations as a competitive advantage (Gleim et al., 2013). The exclusive attributes of eco-products, consumers’ behavior, and its financial impact on corporates’ profit have diverted scholar’s attention to re-examine the impact of sustainable marketing on corporates’ profit to implement effective marketing mix (Belz & Peattie, 2009).

Apparel manufacturers have implemented a number of EMS standards in the past since the 1990s. The most popular ones are the Green Dragon Environmental Management Standard introduced by the environmental groups in the United Kingdom and the European Union’s Eco-Management and Audit Scheme (EMAS) standard. In addition, apparel and textile industries follow industry-specific standards of the Global Recycling Standard (GRS) of the Control Union (Lo et al., 2012). Recently, the Spanish clothing retailer Zara has introduced trendy collection designed by sustainable materials (Brittlebank, 2016). Similarly, 43 fashion businesses including Stella McCartney, Hugo Boss, Burberry, and H&M collectively developed a new Fashion Industry Charter for Climate Action which aims to minimize the greenhouse gas emission and focuses on sustainable development (Malaymail, 2018).

However, there is no specific organization to assess the validity, impact, and performance of these fashion giants. The development of these standards represents the lack of international recognition and results in the variation in customer acceptance of EMS standards, which alternatively impact the performance of apparel manufacturers. The widely accepted and implemented EMS in the manufacturing industry in Malaysia is known as ISO 14001. It was introduced by the International Organization of Standardization (ISO) based in Geneva (Corbett & Kirsch, 2001). ISO 14001 require firms’ management processes and procedures to recognize, measure, and minimize their negative impacts on the environment (Hazudin et al., 2015). An independent third party performs audit and certifies the compliance with the established standards, which confirms the improvement in firms’ performance under the agenda of environmental protection (Jiang & Bansal, 2003). The number of ISO 14001–certified firms in Malaysia declined to 1,519 in the fourth quarter of 2018, which represents the lack of focus on environmental protection by Malaysian firms (Department of Standards Malaysia, 2018).

Hypothesis Development

Past studies have analyzed the EP and its influence on stock returns in the general manufacturing industry and found a positive relationship (Jacobs et al., 2010; Klassen & McLaughlin, 1996). Nonetheless, these findings were limited as these studies were based on short-term responses which were established on Efficient Market Theory assumptions, whereas EMS adoption and its actual impact need to focus long-term accounting measures to reinforce the understanding of mechanism corroborated to preserve the environment and enhance financial performance (Jacobs et al., 2010; Klassen & McLaughlin, 1996). Therefore, to analyze the actual impact of EMS such as ISO 14001 on firms’ financial performance, this study focuses on sales revenue minus the cost of goods sold (COGS), and selling general and administration expenses (SGA). The operating income is preferred over net income as it is unaffected by the variations in the interest rate and tax consideration. Operating income divided by total assets is equal to return on assets (ROA), which is known as the most popular tool to measure profitability.

Various studies have suggested that EMS directly improves EP, which helps the firms to become more profitable by improving cost-efficiency and sales performance (Achim & Borlea, 2014; Petros & Enquist, 2007). The cost-efficiency is measured by dividing operating income by sales, which is equal to return on sales (ROS). The sales performance is measured by dividing sales by total assets (SOA). This is an actual representative of firms’ efficiency to generate revenue from its total assets; therefore, SOA is preferred over other options to measure a firm’s efficiency. To gauge a better understanding of the EMS adoption and its effects on apparel manufacturers in Malaysia, this study postulates a relationship between EMSs and firm’s profitability (represented by ROA), cost-efficiency (represented by ROS), and sales performance (represented by SOA).

The EMS certification and adoption encourage corporates to surpass their EP through reduction in waste, energy, and water consumption, which alternatively increases profitability (Hazudin et al., 2015). EMS adoption requires firms to reduce waste and pollution levels, and implement mandatory corrective actions. In the context of this study, through effective EMS adoption, fashion and textile manufacturers need to maximize recycled fabric utilization, and water- and energy-saving potential. The firms that managed to successfully adopt EMS are expected to redesign products and processes to achieve the goals of optimized material usage. This can be achieved by increasing the use of environment-friendly technology for textile processing, such as fluctuation in the technology used for the treatment of dyeing mill effluent (Vandevivere et al., 1998). Modern-day processing techniques and technology are expected to enable firms to attain a competitive advantage among the fashion and textile manufacturers, which will help the firms to outperform the less environment-friendly firms (Russo & Fouts, 1997). Based on the proceeding discussion, this study aims to test the following main hypothesis:

As the profitability is empirically determined by focusing on ROA, we postulate the following:

As discussed earlier, firms that adopted EMS are expected to show higher cost-efficiency. The EMS adoption signifies the textile firms to reduce pollution to minimize environmental spills, crises, and liabilities which result in devastating penalties and restoration cost (Bansal & Hunter, 2003; Brio et al., 2001; Klassen & McLaughlin, 1996). Fashion and apparel designers are involved in the use and emission of toxic chemicals in the environment during textile processing and often face strict regulatory action on chemical usage as these firms are expected to reduce air pollution through efficient processing. Popular EMS standards such as ISO 14001 require apparel manufacturers to incorporate procedures of waste control during manufacturing and production processes (Berry & Rondinelli, 1998). These procedures directly impact the costs, as recycled materials and efficient processes minimize the processing cost of the firms (Christmann, 2000; King & Lenox, 2002).

Moreover, Potoski and Prakash (2005) found that firms which adopted and obtained EMS certification are perceived as less risky compared with non-EMS-certified firms. Hence, it is expected that EMS-adopted firms often encounter less environmental inspection from the regulators, which results in cost savings. EMS-adopted firms enjoy economies of scale as the manufacturing cost of each unit is reduced and the firms have access to a wide market. Hence, it is postulated that EMS adoption will result in a higher cost-efficiency. The cost-efficiency is represented by ROS, which leads to the following hypothesis:

The EMS performance of firms and their reputation are crucial for some groups of customers, social community, and the environmentally conscious investors (Delmas, 2001; Poksinska et al., 2003). Ann et al. (2006) suggested that in today’s globalized economy, focusing on “triple bottom line” engenders discrete financial, insurance, marketing, regulatory treatment, and other benefits. Stakeholders’ pressure is particularly critical in manufacturing industries, as some cultural sentiments might cause boycott of products, especially from environmentally conscious consumers. EMS adoption may influence shareholders’ preferences for investment and dividend policies such as suggested by Salman (2019). Proactive environmental measures to avoid environmental crises and refraining from procurement by nonenvironment-friendly suppliers will help the apparel manufacturers to establish a positive corporate image among customers. A better corporate image will result in market expansion as customers will show a higher tendency to pay extra cost for the green products and services (Delmas, 2001). Fashion consumers these days are more concerned to discover how and in what capacity their clothes are manufactured and the environment-friendly procedures used during the manufacturing of their clothes (Koll, 2018).

In addition, EMS is important for the markets particularly operating within the environment-conscious regions and imposes strict regulations on environmental protection (Delmas, 2002). According to Green Technology Malaysia Master Plan 2017–2030, the key function is to minimize carbon emission by 10%, which represents its strategic plan to develop green technology and low carbon-emitting economy (KeTTHA, 2017). A green technology–adopted product shall only be considered for registration as a MyHIJAU Mark Product provided it minimizes greenhouse gas emission, promotes health and/or improves the environment, and conserves the energy, water, and other natural resources (Green Tech Malaysia, 2017). Apparel and textile firms are no exception to these standards as the EMS adoption will enable these firms to expand their markets under the regulatory compliance compared with the competitors which are unable to comply with these standards. Arguably, EMS adoption would lead to higher sales. The sales performance is analyzed through SOA, which will be measured through the following hypothesis:

Method

Sampling Criterion

This study utilizes secondary quantitative methods for data collection. ISO 14001–certified fashion and textile firms in the manufacturing industry are focused in this research. The sampling population comprises the firms in the fashion industry, which contain keywords such as “textile,” “apparel,” and “fabric.” The secondary data of the firms’ performance were drawn for 2013–2015 from the online databases. The objective data sources such as Department of Standard Malaysia and firms listed on Bursa Malaysia Stock Exchange are used to identify ISO 14001–certified firms and their performance. The data from 2013 to 2015 are considered due to the fact that the majority of the firms adopted EMS after year 2012. Therefore, the financial performance statistics before and after adoption of EMS will analyze whether these firms have experienced improvement in financial performance. ISO 14001 is a well-established and highly recognized EMS for textile firms in Malaysia, and its adoption is used as a general proxy of EMS adoption. Initially, 72 textile firms are identified, which have multiple certifications such as ISO 9001 and ISO 27001:2005 (Department of Standard Malaysia, 2018). However, this research adopted the work of Corbett et al. (2005) and Naveh and Marcus (2005) to incorporate the adoption of ISO 14001 only. The initial analysis of the raw data reveals that only seven textiles and textile-related firms in Malaysia have ISO 14001 certification (Department of Standard Malaysia, 2018).

Measurement of Variables

The adoption/certification status of ISO 14001 is determined through the firm’s official website and/or annual reports. Adoption of ISO 14001 is used as a proxy for EC, which is an independent variable (Predictor), whereas financial performance is a dependent variable (outcome), which is measured by ratios of ROA, ROS, and SOA. The variables of this study are briefly outlined below.

Dependent variables

ROA: The ratio of ROA determines the net income generated through per dollar assets. Higher ratios represent profitability and better financial performance of firm (Siraj & Pillai, 2012).

ROS: This ratio indicates profitability and growth potential of firms. It is the rate of return to shareholders or the percentage of return on each invested dollar equity (Kumbirai & Webb, 2010).

SOA: The financial performance of firm is also interpreted by sales performance. It is determined by dividing sales by total assets, which is represented by SOA ratio. A firm generating more revenue from its total assets represents higher efficiency, which indicates higher financial performance.

Independent variables

The adoption of EMS, that is, ISO 14001, is used as a proxy of EC, where the year before formal adoption of EMS certification is the event year (year 0).

Controlled variables

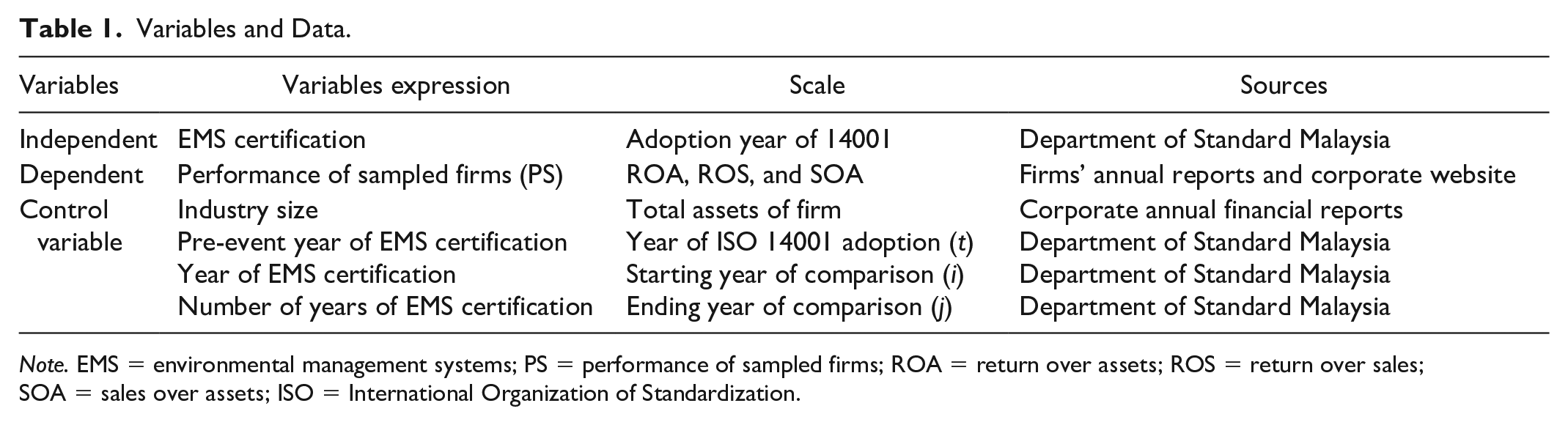

The controlled variables in this study are industry size, ISO 14001 year of adoption, starting year of comparison, and ending year of comparison. Table 1 outlines the variables of our study.

Variables and Data.

Note. EMS = environmental management systems; PS = performance of sampled firms; ROA = return over assets; ROS = return over sales; SOA = sales over assets; ISO = International Organization of Standardization.

Model Description

In the initial sample, 72 textile firms are identified as having EMS certification, whereas only seven firms are found to have ISO 14001 certification. The performance of both certified and noncertified firms will be estimated. During estimation, six noncertified firms are excluded due to the lack of financial information (ROA). The remaining 66 firms’ (59 noncertified and seven certified) financial performance is matched in Step 1 (93.6%), whereas in Steps 2 and 3 no firm is matched. The controlled match pairs and the number of the sample decrease from the ending period Year 1 to Year 1 (Table 2) due to the lack of financial performance in either sample firms or control firms.

Performance Abnormality Test Results of ISO 14001–Certified Firms.

Note. ROA = return over assets; ROS = return over sales; SOA = sales over assets.

p < .1 for one-tailed tests.

p < .01 for one-tailed tests.

Abnormal financial performance within the event window is calculated as the difference between sample post-event performance, which is actual performance in Year 1 and the expected performance in Year 1. Expected performance is calculated as the total of sample pre-event performance in Year 2 and the average change in the performance of control firms during the period from Year 2 to Year 1. The following formula is used for performance calculation:

where AP is the abnormal performance, EP is the expected performance, PS is the performance of sampled firms, PC is the performance of control firms, t is the year of ISO 14001 certification, i is the starting year of comparison (i1/4, 2), and j is the ending year of comparison (j1/4, 1, 2, or 3).

Data Analysis Method

The abnormal change in the performance over long-term period (event window) is the base year which is set as no impact on the performance as the firm was preparing for ISO 14001 adoption. According to Corbett et al. (2005), it takes approximately 6 to 18 months for a firm to pass the certification criteria; hence, in Year 2, the firm is expected to be free from the impacts of ISO 14001 implementation.

As ISO 14001 requires a third-party audit to determine its effectiveness, the firm’s performance should depict the changes during the year certification was obtained. Moreover, the certified firms’ performance should continue to increase, which must represent in the following year (Year 1). It is suitable to examine the firms’ performance prior to the year of obtaining the certification (Year 0). The event period in this research is Year 2, which is used for the comparison of the performance with the measure (Year 0) and the changes over two subsequent years (Year 1, Year 2).

The abnormal changes in the financial performance within the event window are compared with the actual and the expected performance. The abnormal changes in the financial performance are analyzed through Barber and Lyon’s (1996) criteria. These criteria suggest that the control firms’ selection should be based on the combination of three events: pre-event performance, industry, and firm size.

First, pre-event matching of performance helps to avoid mean reversion problem of accounting data and control factors that may impact the firm’s performance (Barber & Lyon, 1996). Second, the economic status of the industry can account to 20% changes in the financial performance (McGahan & Porter, 1997), while environment and its management are strictly industry-specific issues (Russo & Fouts, 1997). Therefore, it is mandatory to control the type of industry during sample and control firm matching. Third, past studies concluded that operating performance is dependent on the firm size (Fama & French, 1995). Therefore, matched sample and control pairs in this research are based on these three matching criteria.

Pre-event performance matching is a highly crucial factor as suggested by Barber and Lyon (1996), matching industry type and 90% to 110% event performance results in the ideal matching groups between sample and control firms. This approach generates a tight performance match and results in specified statistics. The sample control pairs are generated following the steps suggested by Barber and Lyon (1996). These generated pairs are regarded as the performance-industry-matched group. First, each firm is matched with the portfolio of control firms using two-digit code and 90% to 110% of performance in Year 2. Second, when no control firm is matched, one-digit code and 90% to 110% of performance are used. Finally, when no control firm is matched in the previous step, 90% to 110% performance is used as a matching criterion.

The financial performance data are retrieved from the firms’ online databases. The median of abnormal performance is calculated through Wilcoxon signed-rank (WSR) test. Nonparametric tests are used for analyzing financial performance as the t-statistics are more reliable compared with the parametric test (Barber & Lyon, 1996). The percentage of abnormal performance is estimated through the sign test as it is significantly higher than 50%. To ensure the robustness of findings, the results of the parametric t-test on the mean abnormal performance are also estimated.

The impact of EMS is estimated through sensitivity analysis using firm size as a proxy, which is determined by the number of firm’s consumers (Barber & Lyon, 1996). To estimate whether the abnormal performance persists after controlling for firm size, the performance-industry size-matched groups are developed within 50% to 200% range of total assets while firm size was controlled.

Results and Discussion

Performance Abnormality Test Analysis

The abnormality test is performed to analyze the 3 years of abnormal performance after obtaining ISO 14001 certification. The test results are tabulated in Table 2. The cumulative analyses of 3 years of performance provide a comprehensive outline of the long-term impact of financial performance after ISO 14001 certification by textile firms in Malaysia.

The findings of performance-industry-matched group from the year prior to ISO 14001 certification (Year 2) to post year (Year 1) of obtaining certification represent that the median (mean) cumulative change in ROA is 3.2 (25%), which shows significance at 1% level. Approximately 70.57% of firms show a positive change in ROA. The median (mean) abnormal change in ROS is 4.4% (22.8%), which shows significance at the 1% level with the improved performance of 72.8%. Similarly, the median (mean) abnormal change in SOA measure is 5.1% (7.0%), which represents significance at the 10% level with the improved performance of 71.57%.

The abnormal changes in performance from Year 2 to Year 1 and Year 2 to Year 0 indicate the pattern of abnormal changes after firms obtained ISO 14001. The test results indicate that the performance started to increase from Year 2 to Year 0, whereas the changes in performance started to become significant from Year 2 to Year 0. These abnormal changes in performance are due to the fact that in Year 0 firms were in the process of obtaining the certification, which might have motivated firms to show a better performance. It is also notable that during Year 2 to Year 1, there are no substantial changes in SOA. This finding is in parallel with the studies of Fujii et al. (2013), Hart and Ahuja (1996), and Koe (2009) which indicate that firms with a proper environmental certification such as ISO 14000 are able to show higher average ROA but not necessarily on sales and capitalization. These results can be supported by predicting that the true benefits can only be expected after obtaining the certification, which is represented by the increase in SOA from Year 2 to Year 0. This confirms that corporates with proper green marketing mix strategy outperform that firms lack effective implementation of environmental strategies (Goh et al., 2019). It further supports the argument that Malaysian fashion firms can truly yield financial benefits through competitive environmental capabilities (Ong et al., 2019).

Another abnormality test is performed to estimate whether the performance indicators show any significant changes for the non-ISO 14001–certified firms. The cumulative analyses of 3 years of performance of 59 textile firms provide a comprehensive outline of the long-term impact of financial performance without ISO 14001 certification. The test results of the performance-industry-matched group from the year prior to other environmental certification represent that the median (mean) cumulative change in ROA, ROS, and SOA does not experience any significant changes from Year 2 to Year 1, Year 2 to Year 0, and Year 2 to Year 1, which proves that firms without an ISO 14001 certification are unable to show any significant changes in performance. The test results of non-ISO-certified firms are reported in Table 3. This result is consistent with Zeng et al. (2005), which confirms that the proper integration and adoption of EMSs such as ISO 9000 and ISO 14000 allow firms to avoid duplication of manufacturing processes and reduction of resources which can contribute to performance. Therefore, firms both in developing and in developed countries may experience positive and significant increase in financial performance through the adoption of environmental practices (Manrique & Martí-Ballester, 2017).

Performance Abnormality Test Results of Non-ISO 14001–Certified Firms.

Note. ROA = return over assets; ROS = return over sales; SOA = sales over assets.

Impact of EC on Financial Performance

The sample and control firms are matched using three steps to develop the performance-industry-matched group and applied additional 50% to 200% total asset constraint in each step. The findings of sensitivity analysis are tabulated in Table 4.

Sensitivity Test Results.

Note. ROA = return over assets; ROS = return over sales; SOA = sales over assets.

p < .05 for one-tailed tests.

p < .01 for one-tailed tests.

The EC impact results represent that the median (mean) cumulative change in ROA from Year 2 to Year 1 was 2.3% (5%), which shows significance at the 5% (5%) level. Approximately, 68.25% of firms’ ROA improved due to EC. The median (mean) abnormal change in ROS was 2.1% (6.3%), which represents significance at the 5% (5%) level, whereas 79.77% of firms show an increase in SOA. Similarly, the median (mean) abnormal change in SOA was 3.2% (6%), and about 62.27% of firms show improvement in SOA. This result is in parallel with the study of Fryxell and Szeto (2002), which reinforces that stakeholders such as consumers’ increasing interest and awareness toward environmentally caring society influence firms to obtain ISO 14001 certification. It also supports the argument that the firm’s EP can be improved by environmental training, customer pressure, and stakeholders’ pressure (Rohati et al., 2016). Moreover, a broad spectrum of consumers’ environmentally responsible behavior can increase corporate sales, which is a key strategy often used by marketers in ethical, environment-friendly, and green fashion (Thomas, 2008).

The systematic bias between the sample and control firms which are deployed to obtain the results in this study is another significant issue which requires further analysis to ensure that the obtained results are free from systematic bias. For this purpose, additional data analysis especially from Year 3 to Year 2 is performed to observe abnormal changes in performance prior to the sample firms that obtained ISO 14001 certification in Year 2. The test results are tabulated in Table 5. It can be noted that there are no significant changes between all three indicators during Year 3 to Year 2, which reinforces that abnormal changes in Year 2 to Year 1 are free of systematic bias.

Abnormality Test Results From Year 3 to Year 2 Based on the Performance-Industry-Matched Group.

Note. ROA = return over assets; ROS = return over sales; SOA = sales over assets.

The overall results represent that our test results are consistent between two matching groups; hence, H1 and H2 are supported. In the case of SOA, abnormal change is only consistent during performance-industry-matched group; hence, H3 is not fully supported. This could be due to the fact that firms in emerging countries like Malaysia are still at nascent phase; therefore, it is yet to pick the “low-hanging fruits” of practicing environmental strategies (Manrique & Martí-Ballester, 2017). The comparison of median change and the percentages of positive abnormal ROA and ROS shows that abnormal changes in ROS are more significant between two performance measures. This result indicates that the ISO 14001 certification has a major effect on cost-efficiency, and the abnormal ROA is due to the improvement in cost-efficiency pathway instead of the revenue-gain pathway. This indicates that the benefits of adopting environmental activities exceed the cost of implementing, which means that the firm’s performance improves through reduction in manufacturing cost instead of generating more sales (Nakao et al., 2007; Russo & Fouts, 1997).

The performance estimation of non-ISO-certified firms specifies that these firms are unable to show any significant changes in performance. Finally, it is found that EC has a significant impact on all three indicators of performance, which signifies that consumers’ search for green textile products will directly influence the firm performance, which proves that the null hypothesis H0 is also supported. This result is consistent with the findings of Angus and Westbrook (2019), reinforcing that EC is the solution to minimize the negative impacts of apparel fashion consumption that alternatively increases corporate sales (Binet et al., 2019).

These findings contribute to the literature in three different ways. First, it fills the knowledge gap of the dearth of studies on impact of EC on financial performance of fashion firms in Malaysia. Previous studies widely focused on analyzing the apparel industry’s impact on EP, gender-based impact on financial performance of fashion firms, and the effect of green marketing mix on financial performance. Second, studies related to the impact of environmental strategies on financial performance are mostly concentrated in manufacturing industries in developed and underdeveloped countries. Our study presents a deep insight of financial performance of fashion industry influenced due to environmental and eco-friendly manufacturing strategies in one of the emerging economies in Asia. Finally, the measurement model of this study is robust and effective in measuring the actual impact of financial performance due to environmental strategies as it incorporated SOA which is directly related to the cost reduction and profitability due to the implementation of eco-friendly strategies.

Conclusion

The manufacturing process of the fashion industry, specifically of textile industry, has recently escalated social and environmental issues. The global fashion industry has started to integrate and focus on the sustainable paradigm in its entire corporate operations. This holistic approach by fashion industry was introduced due to increased interests of consumers to discover the capacity in which their clothes are manufactured by the reputable fashion giants, especially in the environment-conscious society such as Malaysia. The increasing consumer awareness and desire of environment-friendly clothes have influenced the textile manufacturers in Malaysia to obtain EMS certification such as ISO 14001, which is suggested to directly influence the firm’s performance. This study investigates whether consumers’ eco-behavior influences textile corporates’ performance. The data collected from seven ISO 14001–certified and 59 noncertified firms reveal that firms which have obtained EMS certification show a significant change in ROA, ROS, and SOA over the 3-year period, whereas textile firms which are unable to obtain EMS certification do not experience significant changes in its performance. In addition, it is found that EC positively influences the firms’ performance.

Implications

This research has various practical, research, and managerial implications. The empirical validation of this research provides a paramount implication for practitioners to understand the impact and significance of consumer behavior and further develop environmental management protocols to engage consumers with the corporate. This will help to improve consumers’ patronage intention, willingness to bear extra cost for green products, and sacrifice for the sake of the environment. An exclusive literature review of environment-related fashion research reveals the dearth of studies especially on the impact of consumer influence on textile firms’ performance by understanding the insight provided in this study of the importance of consumers’ impact on performance and obtaining an EMS certification. Practitioners may better understand its customers and the protocols to obtain and retain a label of environment-friendly corporate. This will help the firms in developing countries to harvest the fruits of environmental strategies through reduction in operational cost. Moreover, practitioners in developed countries may use these findings to seek investment in research and development to develop new environment-friendly products. This research provides various managerial implications for marketers to promote eco-friendly apparel. Especially during financial crises, governments cut budgets and consumer demand becomes lower; hence, managers of the firms with budget constraints in less developed economies may use these findings to achieve economies of scale by investing in environmental projects as these are cost-effective and increase overall profitability of corporates. Diverse barriers may exist to identify and acquire an eco-friendly textile product; based on the significance of consumers’ influence of corporate profits, this study encourages marketers to initiate communication with consumers to decrease lack of product knowledge, uncertainty toward the quality, and trust on the corporate. This will allow the firms in developed countries to continue to survive during financial crises as consumers in developed countries will be willing to pay extra cost for newly developed environment-friendly products.

Limitations and Future Research

As with most other researches, this study exhibits numerous limitations. Although the financial performance data were collected from the recent years, it is not ideal to generalize the findings as corporates’ performance before the adoption of EMS certification might show fluctuation due to other macroeconomic factors. The performance data during financial crises and data of firms’ other subsidiaries could have an effect on the estimation of financial performance. Therefore, future studies may undertake the influence of macroeconomic factors such as gross domestic product, inflation, and exchange rate on consumers’ purchasing behavior and repeat the analysis in intervals to estimate whether performance fluctuates based on time. The approach to financial performance was based on robust and well-treated score, yet it is limited in its scope, measurement, and methodology. Finally, this study is established on large firms; however, future studies may extend and incorporate recent data especially of small firms to compare the findings.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.