Abstract

The article analyzes the role of driving m-commerce with social networking and therefore provides insight into how the application of mobile apps influences customers’ perceptions on purchasing products online and on the mode of payment. The consumers are engaged in social interactions through the internet by the new opportunities provided by social media. These interactions provide and generate certain values for both businesses and consumers. An upsurge in the application of social media on mobile phones by users is evident, giving optimism and the ability to view the role of the integration of m-commerce into social media. Certain criteria like mobile app compatibility, trust, perceived value of mobile phone apps for online shopping, and online payment are examined from the point of view of consumers who purchase products, save purchase time, and provide easy use and security through social networking sites and m-commerce. Adoption of a digital mode of payment is affected by the education level of the consumers as, if they are internet savvy, they will be more inclined to use the digital payment mode. The article not only discusses the role of education in the better understanding of consumers toward the application of online modes of transaction through mobile phones, but also indicates that there are security issues, although these have been resolved to some extent by technological advances. Yet, there is need for the retailers as well as the consumers to achieve further technological progress.

Introduction

All around the world, smartphones with intelligent-based software packages, social networking sites (SNSs), and a variety of mobile applications (apps) have taken over the global market (Capatina et al., 2020; Lai et al., 2011). The development of information technologies has led to applications that allow the user to carry out various tasks (Malik et al., 2017) or access services from all over the globe. Most, if not all, of the internet-enabled activities that previously required a desktop or notebook can be achieved with tablets and smartphones. SMS messages, quick response (QR) codes that scan intention, and other location-based services are some of the important specifications in mobile devices (Okazaki et al., 2019). The application of a wireless terminal, such as a cellular telephone, smartphone, or personal digital assistant (PDA), and a network to access information and conduct transactions that result in the exchange of information, services, or goods, is likely to test the regulatory structures that are in place to deal with traditional transactions and is referred to as mobile commerce or m-commerce.

Social media platforms are using this opportunity as a way to advertise content and improve revenue through various marketing strategies (Lai et al., 2011) or variety seeking (Hossain et al., 2019). Mobile marketing is defined as a set of practices that enables an organization to communicate and engage with its audience in an interactive and relevant manner with the use of any mobile device or network by the mobile marketing association (Ström et al., 2014). With the rise in both the number of users and the number of young users, m-commerce has gradually become central to expanding businesses beyond physical barriers. In the recent past, there has been an exponential increase in the number of people owning a smartphone. The adoption of cell phones is widespread, specifically among the younger generation, with around 75% of teenagers and around 93% of adults aged 18 to 29 years being mobile users (Y. Lee et al., 2012). Also, the trend of shopping has changed from in-store purchasing to online purchasing. This has led to m-commerce taking center stage in mediating the exchanges (Y. Lee et al., 2012). It was apparent through an evaluation made from the existing literature that most of the areas relative to the research topic have somewhat tried to be connected with increased venture creation tendency with social media (Hossain et al., 2020), multidisciplinary usage and impact of mobile phones and online shopping (OLSHOP; Jaller & Pahwa, 2020), the role of the privacy and internet usage (Bandara et al., 2020), the impact of new media (Hennig-Thurau et al., 2010), negative and positive experience of the customers, trust and perceived risk in online store purchases (Barari et al., 2020), and so on. However, this study is specific to social networking and driving m-commerce, with the specific focus of mobile phone usage. Therefore, we study the application of mobile devices and their applications in OLSHOP and online payments (OLPAYs), particularly regarding consumers’ payment factor. The study focuses on the literature and related findings regarding the participation of social media sites in driving m-commerce. It was found from the literature that although social media, such as Facebook, is involved in raising the privacy and trust among consumers (Ayaburi & Treku, 2020), and also indirectly encourage the buying intentions of customers through its involvement in SNSs with mobile phone payment systems (C. Kim et al., 2010), most of the buying decisions of the customers are based on observations made substantially due to social media influences rather that the perceptions of consumers about services and products. Furthermore, adoption of a digital mode of payment and priority of social media usage are affected by the education level of the consumers as those who are internet savvy will be more inclined to use digital payment modes because of trust (Gibson & Trnka, 2020; S. Kim & Park, 2013). Therefore, a gap exists in this domain, as the rate of literacy and ignorance of certain consumers also affects the use of online mobile payment for purchasing products, and therefore this area can further be highlighted in future research. Also, there are factors that impact the trust of consumers (S. Kim & Park, 2013) regarding frequent use of online transaction modes through mobile apps (Kourouthanassis & Georgiadis, 2014). From studies, it is clear that the identified trust and security concerns (Hossain, 2019; K. C. Lee & Chung, 2009; Mallat, 2007; T. Zhou, 2011) have positive impacts on the utilization of e-payment systems. It was found that the technical processes of transactions and exposure to security guidelines (M. Li et al., 2012; Vasileiadis, 2014) influence the perceived trust of customers, which impacts their use of online transaction modes. Security issues might affect the trust of consumers in OLPAY mode use (Shaikh & Karjaluoto, 2015; K. Yang, 2010) and further study is required to provide a better understanding and to bridge this uncertainty among consumers in the near future.

From the view of the scholarly articles, people now have easier and full-time access to content that can be purchased at the click of a button. This brings more profits when compared with shopping done over a desktop or even a laptop. Hence, m-commerce is looking at broader usage such as locative media and identity (Saker & Evans, 2016) and greater dependence in the coming years. The evaluation of social networking for the promotion of m-commerce is presently aimed for. Furthermore, this study attempts to infer a relationship between the purchase intentions of consumers and the mode of transaction they undertake due to m-shopping, which is still under shadow and need to be discovered.

Theoretical Background, Literature Review, and Hypotheses Development

Uses and Gratifications (U&G) Theory

This theory is about users’ gratification needs such as expressing feeling with likes or comments. The U&G theory explains the reason for choosing a particular media, especially SNSs, to express gratification (Katz et al., 1974). U&G has been widely used and applied by the researchers in using various traditional media such as radio, television, newspaper, and so on. However, the theory has been also used to identify and discover the role and intensity of internet usage, instant messaging (IM), Twitter, and Facebook (Alhabash et al., 2014). Although scholarly articles discussed about different types of gratification, such as hedonic gratification, social gratification, and utilitarian gratification (H. Li et al., 2015), this study focuses on gratification theory in general, which is choosing a particular SNS, especially for business purpose. Thus, it is appropriate that in this study the authors adopt the U&G theory as the theoretical base.

Analyzing the Role of Social Media in Driving M-Commerce

As per the studies provided by Hajli (2014), it has been found that social media is involved in raising trust among consumers and also indirectly encourages the buying intentions of customers through their involvement and commodification (Drakopoulou, 2017) in the SNSs. The consumers are engaged in social interactions through the internet by the new opportunities provided by social media. Social media has been used by the customers of online communities to develop content and also to generate networking with other users. The latest developments in social media and internet advances have facilitated mutual connections of consumers. The applications of social media have helped consumers to interact socially through online forums, communities, reviews, ratings, and other recommendations made toward products purchased from websites and social media (Pelet & Papadopoulou, 2015). Social commerce evolved as a new branch of e-commerce that helped in the empowerment of consumers for content generation and created impacts among others through developments. These interactions have provided and generated certain value for both businesses and consumers.

Again, there has been a rise in the application of social media (Malthouse et al., 2013) in mobile phones by users with optimism and perception, increasing the popularity of m-commerce (Zheng & Jin, 2018), specifically in terms of the integration of social media. Social media adoption (Mani & Gunasekaran, 2018) and m-commerce (Zheng & Jin, 2018) are affected by certain factors, such as product reputation and consumer trust related to product usage, security, and the ease of use. It was revealed from the studies that social media represents a method (Bekmagambetov et al., 2018) of rapid assessment of m-commerce websites and enables users to access a specific page without getting lost on the website. Online marketing landing pages are considered to be an essential component of m-commerce. Companies get engaged with m-commerce for the utilization of social media sites to increase popularity and develop interactive associations and obtain trust. In the age of evolving mobile technology, the establishment of trust in OLSHOP companies was shown to be significant, and social media generated a significant amount of this (Sunstein, 2018) by developing positive communication among consumers. Such direction has been attained by the application of certain social media, like Instagram, Pinterest, and Snapchat, which are used to generate prosperous and swift modes of communication between customers and business firms by texting with pictures or videos from them (Pelet & Papadopoulou, 2015).

In the contribution made by Malthouse et al. (2013), it was explored that technological advances, more specifically in the arena of social media, have influenced some e-commerce firms through verbal deals. Based on reviews provided by customers (Steward et al., 2017), the quality and authenticity of a particular brand or product can be understood by future customers. The reviews of those customers create and spread awareness about the information related to the product to other customers. Thus, these companies rely strongly on the comments and interactions with other individuals who consider the source of such product information to be reliable and valuable. Contrastingly, the e-commerce businesses have not been affected by the application of growing social media through communication. Most of the buying decisions of customers are determined by observations of the growing use and popularity of social media. Consumers’ perceptions on a product or company determine whether they opt a particular business (Malthouse et al., 2013). From the discussion above, we propose the following hypothesis:

Preference of Mobile Phones for OLSHOP and OLPAYs

A study by Jarrett (2016) and Jocevski et al. (2019) attempted to understand the perceptions of customers toward digital payment and mobile payment. It was revealed that except for education, demographic factors have little influence on the adoption of digital payment. The literature found no specific differences in consumer behavior based on their demographic profile, including their annual income. Adoption of a digital mode of payment, such as WeChat payment (Matemba & Li, 2018) was affected by the education level or geographical difference of the consumers. However, those who are internet savvy will be more inclined to use a digital payment mode if the vendor can ensure secure payment authentication (Song et al., 2017). Recent studies also revealed that for consumers with a higher level of education, the probability of using a digital payment mode was quite high. The growth of smartphone users and the internet penetration has also facilitated the adoption of digital payment (Barkhordari et al., 2017). As a result, social networking is now connected to OLPAY to make smooth OLSHOP due to trust among the existing and potential customers (Q. Yang et al., 2015).

In Finland, the online consumers are mainly older adults aged 55 to 74 years (Kuoppamäki et al., 2017). In the case of online purchases, the consumers mostly prefer personal computers as they are seen as reliable devices for shopping purposes. The young consumers in Finland do not often make online purchases with mobile phones. One third of the consumers stated that they purchase products online through smartphones advertisement and it enhances their purchase intention (Martins et al., 2019). The study confirmed that the majority of consumers hesitate to purchase products through an online mode of payment due to security issues with credit card transactions and payment information storage and loading credit card information onto their smartphones to make payments while purchasing products. Another issue that stopped the consumers from purchasing products directly online through mobile phones was that they consider the smaller screen size of smartphones to be an obstacle (Rintamäki et al., 2006). However, the extensive usage of social networking and smartphones motivate people to enjoy OLSHOP with various advertisements, offers, single-store promotions, and so on (L. Yang et al., 2019). From the discussion above, we propose the following hypothesis:

Factors That Affect Consumers’ Trust and Continuous Adoption of Online Transaction Modes Through Mobile Phones

The literature provided by Barkhordari et al. (2017) suggested that the banking system has been impacted by the introduction of internet technology due to its capability to enhance the presentation of financial operations. Customers’ perceptions toward security and trust have been revealed as a primary concern for internet banking systems. It was found that trust and perceived security have positive effects on the usage of e-payment systems. Technical and transaction processes and access to the security guidelines are the governing conditions to build trust in consumers and affect their buying behavior. The studies discussed that the determinants for perceived trust are based on statements of security, access to security guidelines, and the identification of security as authoritative; these factors led to the inclusion of a diverse population at a larger scale into the banking sector. Studies have suggested that access to security guidelines has the highest impact on security perception as an individual personality factor (Aldás-Manzano et al., 2009). Even for a shorter period, if services are inaccessible, this can cause fear to be associated with the use of those services as they are considered to be unreliable by the consumers. It was found that, in terms of their recent transactions, the customers might fear a loss of data, or they may reach the conclusion that online mobile banking services do not provide strong resistance against vulnerable occurrences. It was found that awareness among consumers contributes significantly to security risk reduction.

The literature provided by Malik et al. (2017) explored that, in terms of the adoption and continuous usage of hedonic and utilitarian apps by Indian consumers, certain factors are responsible for the recklessness of the consumers, and their disagreement with mobile applications has caused concern and been given importance for marketers. This may keep fluctuating in the near future. Organizations can interact with the emergence of consumers in new digital ways, and therefore, it is significant to explore and investigate the trends. One of the favorable tools for marketers is mobile apps, due to their global, mobile, and effortless accessibility with no downloads on diverse platforms. Thus, it is necessary to understand the behaviors and perceptions of consumers toward these latest technological advances. Marketers, therefore, understand the rising marketing opportunities anytime and anywhere, as per previous studies. Marketers have faced great challenges in longer term applications and commitment toward mobile apps, which has developed for research in the future. For the new age marketers, mobile apps are fascinating due to their availability for consumers. Also, a predicted edge for the marketers in the present cutthroat competitive environment is provided by the continuous use of mobile apps by consumers, as was observed through the scrutiny of the factors in the literature (Malik et al., 2017).

The literature provided by Pi et al. (2012) explored the six constructs of likewise awareness toward companies and their websites, website design and interface, security during transactions, prior experience with internet utilization, navigation and personalization, and the performance variables that are responsible for influencing affective and cognitive trust and that are responsible and affected in the adoption of online financial services. Studies revealed that affective trust is influenced by cognitive trust (Pi et al., 2012) and therefore both would influence the continuous adoption of a firm’s strategy in mobile commerce by online financial service customers (Buellingen & Woerter, 2004). Affective trust will be influenced by security concerns as cognitive and affective trust toward security are critical for financial website service providers and are what customers expect from a virtual store (Burke, 2002). Significant conditions like experience in internet usage and its navigation functions by consumers in m-commerce usage activities (Chan & Chong, 2013) is required to build up the reputation and awareness of a company’s website and enhance cognitive trust regarding mobile payments. From the discussion above, we propose the following hypothesis:

Research Method

Data Collection Procedure

The current research followed a descriptive research design and aimed to assess the conditions that affect the process of OLSHOP and the payment of consumers related to social media. As the opinion of people on set factors had to be gauged, a quantitative questionnaire was used. The questionnaire was closed-end and contained questions about mobile usage, social media and OLSHOP, usage of OLPAY modes through the phone, and application of social media and m-commerce websites through mobile devices. This was applied to gain ideas about the functionality associated with these applications and to investigate the amalgamation of social media in m-commerce that was estimated in prior studies. A qualitative questionnaire was deemed fit to estimate the collective opinion. The questionnaire was constructed based on prior literature on the use of mobile phones, purchase mentality in OLSHOP apps, trust while using OLSHOP apps, and other related topics. The questionnaire was rated based on the degree of agreeability on a 5-point Likert-type scale. The questionnaire was distributed among students of various universities, with 400 students chosen at random, as they are more into OLSHOP and OLPAYs. The questionnaire contained two parts; the first required the students to fill in personal information regarding age, sex, education, time spent on social media, and so on. In the next section, the questionnaire was developed with 17 questions placed under four sections, namely, SNSs Trust, Online payment in terms of online Shopping Network, Perceived value of mobile phone Apps for online shopping, and Mobile App Compatibility.

The questions were segregated to allow both the respondent and the researcher to understand the questions clearly and to provide segregated answers. The answers provided by the students were compiled into an excel sheet and processed using MPlus (Version 8.3).

Respondents’ Demographics

This section of the article concerns the collective work on the uses of new technologies, like the application of mobile phones for OLSHOP and transactions by customers, which was presented into society by reconnecting the association between people’s behavioral traits and user-generated applications. Precisely, it concentrated on social networking use and its role in driving m-commerce, an idea that captures what makes mobile phone users more comfortable. Traders gain more profits through this method as compared with shopping done over a desktop or even a laptop. Moving forward, m-commerce is considering comprehensive usage, better dependence, and therefore, trust building among consumers toward mobile commerce.

The study focused on the gathering of information through mixed approaches based on the detailed demographic information provided, along with other aspects like the time spent on SNSs, the frequency of the use of SNSs by consumers, and the intensity of goods purchasing that often influence m-commerce in gaining popularity among consumers. The statistical outcomes show that out of a total of 307 respondents, the majority of the respondents (chosen randomly) were male (73.3%), with the highest percentage being aged 24 to 29 years (60.9%).

Again, in terms of the highest percentage of time spent by the users on SNSs, the majority of the users stated that they spend more than 4 hr a day, on average, on social media, which supports the reviews provided by Hossain et al. (2020), who stated that mobile phones are considered as one of the key factors in retrieving the relationship between retailers and consumers and thereby building up an ideal and additional passageway for physical retail and distant promotion of products where SNSs are frequently applied. Furthermore, the highest percentage of frequent users was those using Facebook (60.6%).

As per the statistical analysis, 72% of internet users stated that they use SNSs through mobile phones and other portable devices to purchase goods (Brenner & Smith, 2013). According to the literature provided by Brenner and Smith (2013), social media sites stimulate the consumers by displaying the images that direct and lure them toward purchasing products. This is somewhat in contrast to the results obtained from an analysis where the consumers rarely showed interest in using mobile networking (Hossain, 2019).

Results

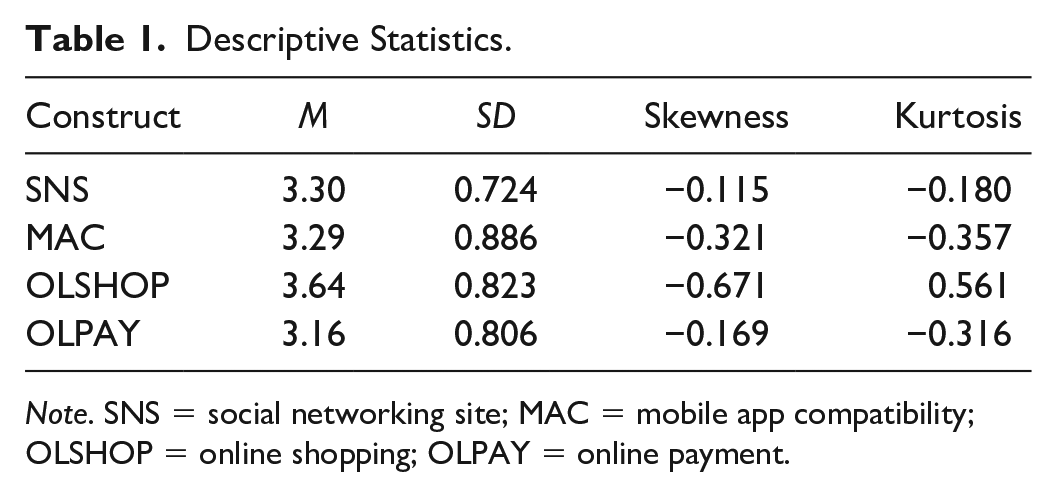

The current study adopts a two-step approach of data analysis by first conducting factor analysis to establish reliability and validity and then testing hypotheses through the structural equation modeling (SEM) technique. In addition, the current study employed covariance-based SEM with maximum likelihood estimation technique using MPlus (Version 8.3). The data are suitable for covariance-based SEM as the data are normally distributed as depicted in Table 1; the values of skewness and Kurtosis are less than 1, which is well under the criteria of normal distribution. In addition, we exposed the collected data to Harman’s single-factor test (Podsakoff et al., 2003) and found that a single factor explains only 32% of the variance, which is well under the cutoff criterion of 50%. Therefore, Common Method Bias (CMB) is not an issue for this study.

Descriptive Statistics.

Note. SNS = social networking site; MAC = mobile app compatibility; OLSHOP = online shopping; OLPAY = online payment.

The results of the confirmatory factor analysis in this study are presented in Table 2 and it indicated the suitability and reliability of the observed data along with the proposed theoretical model. The measurement model was assessed based on criteria recommended by Hair et al. (2010) and Hoe (2008) for model fit indices, reliability, convergent validity, and discriminant validity. Model fit indices in this study were as follows, representing a good model fit: chi-square (χ2/df = 2.02), comparative fit index (CFI = 0.945), Tucker−Lewis index (TLI = 0.930), root mean square error of approximation (RMSEA = 0.058), and standardized root mean square residual (SRMR = 0.062). The values of composite reliability (CR) of each multi-item measure are higher than 0.70, which represent high internal consistency among items. Whereas, the values of individual factor loadings and average variance extracted (AVE) of all measurement scales are higher than 0.50, which provide support for convergent validity.

Confirmatory Factor Analysis (Model Fit).

Note. CFI = comparative fit index; TLI = Tucker–Lewis index; RMSEA = root mean square error of approximation; SRMR = standardized root mean square residual.

Reliability test and factor loading

We determined the internal consistency of the questionnaire, developed using multiple Likert-type scale statements for the determination of the scales, to determine whether it is reliable for use or not. The Cronbach alpha value was found to be more than .7 in the data analysis, which reflects the high reliability of the measuring instrument (Table 3). Furthermore, this value indicates high internal consistency for the variables associated with SNSs in mobile devices, based on the intentions of the customers. We have removed two items of OLSHOP scale because of low factor loadings. The items are specifically indicated in the appendix.

Factor Loading and Cronbach α.

Note. SNS = social networking site; MAC = mobile app compatibility; OLSHOP = online shopping; OLPAY = online payment.

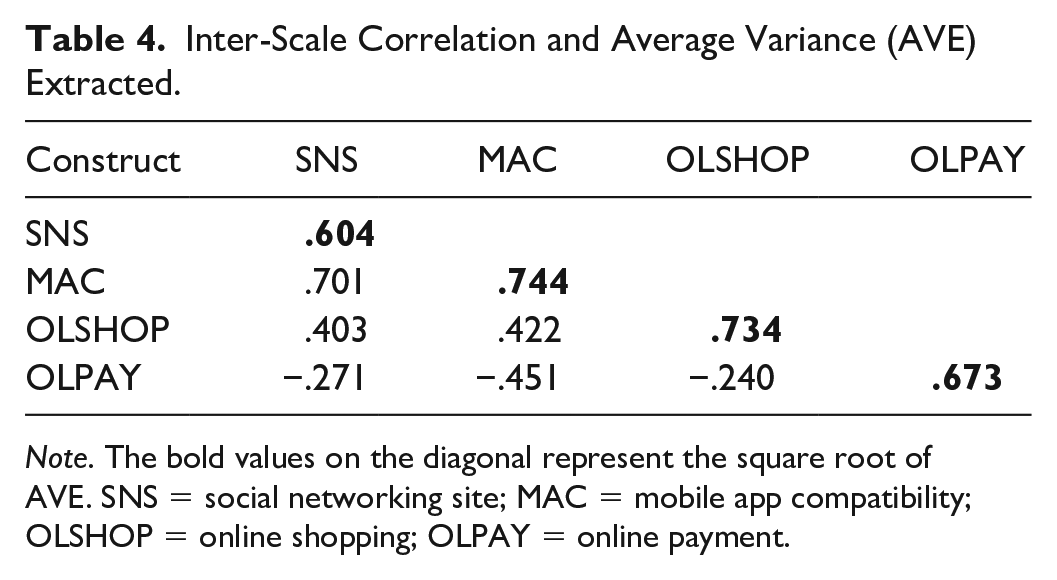

We assessed discriminant validity by comparing inter-scale correlations with the square root of each construct’s AVE. The results, shown in Table 3, indicate that discriminant validity is established, as the AVEs of all individual scales are higher than their corresponding inter-scale correlations, with the exception of SNS and MAC. Therefore, for this pair of constructs, we performed a chi-square difference test by comparing unconstrained and constrained (constraining their correlation to be 1) models to verify discriminant validity. The chi-square difference test (Δχ2 = 128.373, p = .000) is significant, indicating that the unconstrained model is superior to the constrained model and that the two variables cannot be combined into a single construct.

Table 4 shows the correlation analysis of the study along with AVE. A single number correlation, the mostly commonly used statistical tool, was used to interpret the relationships between sets of two variables. The correlation analysis in this research clearly showed very strong relationships among the variables. All three independent variables were strongly associated with the dependent variable.

Inter-Scale Correlation and Average Variance (AVE) Extracted.

Note. The bold values on the diagonal represent the square root of AVE. SNS = social networking site; MAC = mobile app compatibility; OLSHOP = online shopping; OLPAY = online payment.

Kaiser–Meyer–Olkin (KMO) and Bartlett’s test statistics

The sampling adequacy that was used to determine whether the responses obtained from the sample were adequate or not was determined from KMO measurements. In the present analysis, the results showed a value of 0.776, that is, it was highly acceptable for the factor analysis to proceed.

The strength of the relationships among different variables was indicated from Bartlett’s test. Bartlett’s test of sphericity was significant (0.000), meaning that the correlation matrix was not an identity matrix.

Table 5 displays the KMO and Bartlett’s test statistics of SNSs in a mobile phone on consumer intentions.

KMO and Bartlett’s Test.

Note. KMO = Kaiser–Meyer–Olkin.

Principal component analysis (PCA)

Table 6, Principal Component Analysis table, presents the amount of variance (i.e., the communality value should be more than 0.5 to be considered for further analysis. Otherwise, these variables should be removed from further factor analysis processes). The variables have been accounted for by the extracted factors.

Extraction Method: Principal Component Analysis.

Note. SNS = social networking site.

The total variance of the components and the extraction of components with initial total eigenvalues of more than 1 are presented in Table 7 below. From this table, only one component is extracted out of five.

Total Variance Explained.

Extraction Method: PCA

Similarly, the reliability and factor analyses were conducted with the same method as that used for conducting the analysis. The inputs reflected high reliability toward the questionnaire developed for conducting the analysis. The KMO value of 0.794 shows a low acceptability for the factor analysis to proceed. Again, regarding the use of a mobile app as compared with a desktop for OLSHOP, the Cronbach alpha value of .588 indicates the reliability of the measuring instrument. A higher level of internal consistency concerning the variables was indicated by these obtained Cronbach alpha values. The results for mobile applications concerning the ease of OLPAY transactions indicated a greater level of internal consistency among the variables.

Results and Discussion

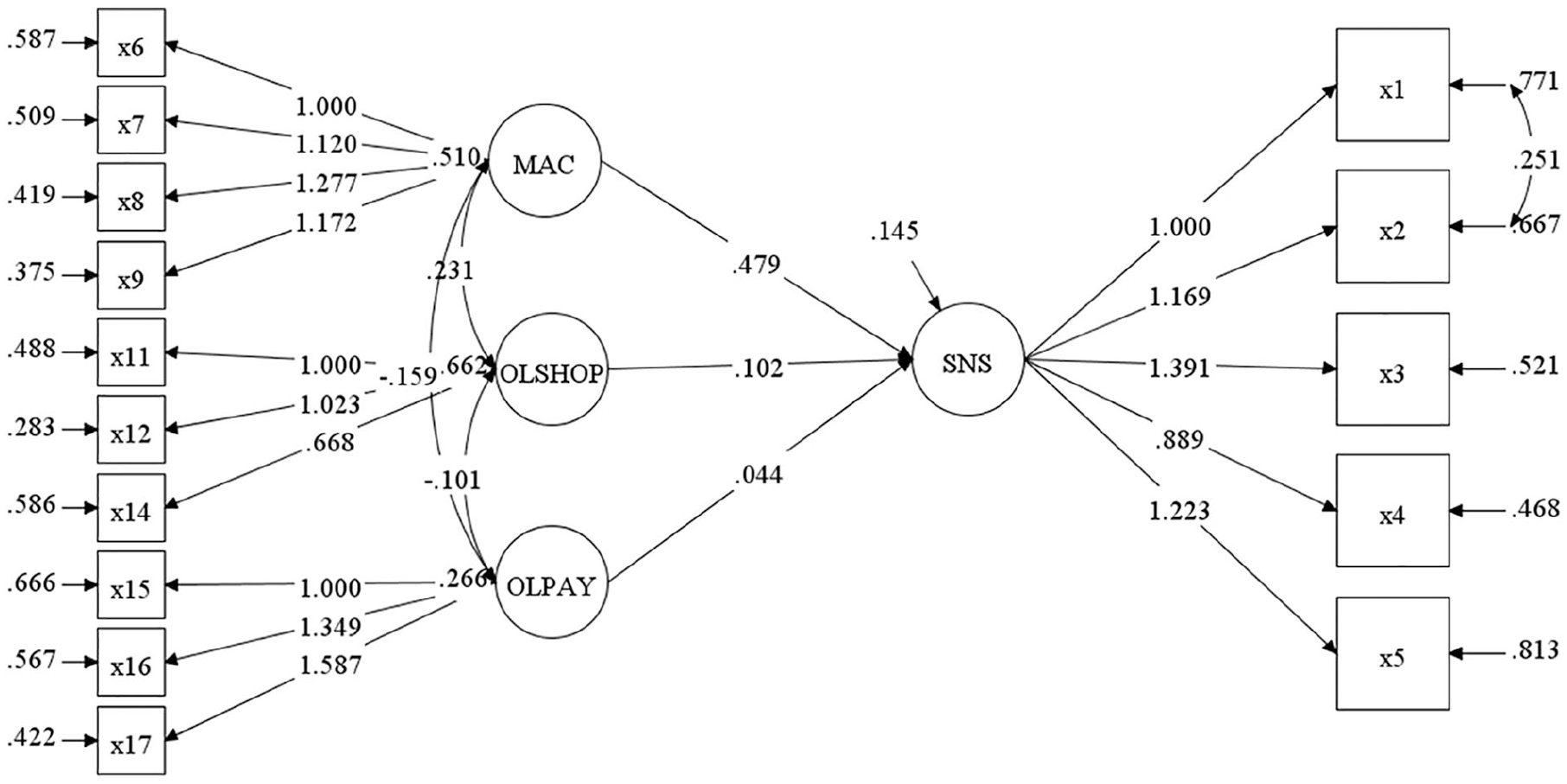

SEM Model and Results of Hypothesis Testing

The simulation research models showed an observed value of chi-square/df ratio = 2.211 (good fit: positive value), an RMSEA of 0.063 (good fit: <0.05), a TLI value of 0.918 (good fit: >0.90), and a CFI value of 0.935 (good fit: >0.90). Thus, the research model in this study may be accepted.

After confirmation of a valid reliability, we analyzed the data using Mplus (Version 8.3). The relationship and effects of all variables, along with the effects, are shown in Table 8 and the structural model with results is shown in Figure 1. The results obtained from Mplus clearly support all the hypothesis, except H3: (H1: β = .642, p < .001; H2: β = .156, p < .05; H3: β = −.99, p > .001). So H3 in this study is rejected. The possible reason could be sensitivity of payment procedure. Although, people depend a lot on SNSs, however, the scenario is different in the context of payment.

Hypothesized Path.

Note. R2 (SNS = .490). MAC = mobile app compatibility; SNS = social networking site; OLSHOP = online shopping; OLPAY = online payment.

Simulation research model with Mplus.

Discussion

The above-provided findings show that social media has an impact on the usage of m-commerce applications, advertising in social media websites, and trust development among consumers in making OLPAYs over mobile phones. All of the criteria showed significant effects on OLSHOP for products by consumers (H1 and H2 were accepted/supported). It was confirmed that these conditions have an impact on diverse consumers across different regions and drive the process of purchasing and making transactions online by consumers. The finding confirms that a relation exists between social media, m-commerce, and OLSHOP, as per the data analysis report. Based on the findings shown in Table 8 and Figure 1, the hypothesis test summary is presented in Table 9.

Summary of the Hypothesis Testing.

Furthermore, these findings also supported the literature provided by Pi et al. (2012), where it was explored that there are six constructs—the website and company awareness, design of the website and interface, transaction security, prior internet experience, personalization, and navigation functionality—that are responsible and influence cognitive trust and affective trust and that affect the adoption of online financial services. Again, H1 supports the literature provided by Hossain (2019), where it was found that social media is involved in raising trust among consumers and also indirectly encourages the buying intentions of customers through their involvement in the SNSs. Furthermore, the study results infer that m-commerce is evolving to be a more broadly used technological means (L. Zhou et al., 2013) that we will have greater dependence on in the coming years.

Conclusion

The present study explored the application of m-commerce, or mobile commerce, a wireless terminal, and network that can access information and, therefore, execute transaction processes that can result in value transfer by information exchange (Ström et al., 2014; Thakur & Srivastava, 2014). Also, goods and services are likely to test the regulatory structures in place to deal with traditional transaction processes. It can be inferred from the results that a high percentage of time is spent by users on various SNSs—35.2% of respondents reported an average of more than 4 hr on average. Furthermore, in terms of the usage of SNSs using mobile phones by the consumers, the contrasting view of the literature with the results obtained could provide a scope for further investigation to acquire a more detailed and flawless idea of the time consumed by mobile users for OLSHOP activities and the factors contributing toward this. The possibility is also there to shed more light on the different characteristics of the m-payment process.

Limitations

This research is limited by certain criteria. First of all, the size and number of transactions made by the consumers could not be measured in this study. Also, the product reputation and trust of the consumers may affect the result. Moreover, the hesitation of consumers to purchase products online due to security issues with credit card transactions and storage of payment information is difficult to measure with scientific research. Finally, the level of education of the users is another limiting factor, and the respondents could not be chosen from every part of the world due to the limitation of research funding, which may affect the generalizability of the research.

Managerial Implications

The study provides some managerial implications in the OLSHOP arena in the context of trust. Through the variables of the study, it is suggested that companies ensure that they have a secure payment method for the buyers to gain trust. Although there are other factors, trust regarding payment is a very sentimental and sensitive issue for buyers, which may severely affect future purchase intention from the same organization. Managers should not only update the secure payment system online and adopt new technologies and payment methods but also use the payment method as a tool to gain more trust. For example, managers may motivate consumers to pay online to receive a good discount for their next purchase. As a result, customers will be motivated to purchase a product, and they will continue further if they gain trust from the seller.

Theoretical and Practical Implications

This research contributes to present the U&G theory in a number of ways. First, in this study, we extend the contributions of the U&G theory with the ubiquitous usage of smartphones. Second, we integrate U&G theory in online purchase in the context of trust. Finally, this study contributes to present the U&G theory through a different way of online purchase based on payment and trust.

The study provides some practical implications too in the OLSHOP arena in the context of trust. People are usually sensitive for online or mobile payment. Only trust can ensure secure payment over time without any hesitation. In case of any technical or other difficulty of payment regarding OLSHOP, it may influence consumers’ future purchase intention. This study discovered the increased use of m-shopping behavior due to the availability and affordability of smartphones at present in the context of payment and trust. Customers with more trust with vendors can purchase more securely with social networking and m-shopping, which can ensure a peaceful and sustainable shopping environment.

Future Research

Social software tools and applications are crucial for the study to investigate to obtain and retain trust from a business perspective. Furthermore, the next goal is to consider the integration and advances to be made in the technological applications of mobile devices to support challenging issues related to personal security in the process of transactions of consumers. Thus, future work should provide more research on m-commerce and social media along with the resilience and improved versions of technological applications to build better trust among the consumers to encourage them to use OLPAY methods and make transactions freely without any fear or hesitation. It will also further help business organizations to reduce the fear from the customers in terms of losing data, or it will promote the conclusion that online mobile banking services can improve their reliability. This will further aid diverse organizations to identify and eliminate the risk of social media in terms of reliability and to aid different organizations to achieve their goals.

Footnotes

Appendix

Acknowledgements

The authors sincerely thank Professor Selina Nargis, IUBAT—International University of Business Agriculture and Technology, Dhaka, Bangladesh, for her encouragement and motivation towards scientific research and publication. The authors are also grateful to the anonymous reviewers and entire editorial team for their invaluable feedback and comments.

Authors’ Note

Syed Far Abid Hossain is also affiliated to IUBAT—International University of Business Agriculture and Technology, Dhaka, Bangladesh.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.