Abstract

The purpose is to explore whether the CEO’s personal and professional attributes affect corporate social responsibility (CSR) disclosure or not in particular context of Pakistan. This article attempts to bridge this gap using the data set of 1,790 firm-year observations comprising of firms listed at the Pakistan Stock Exchange. For this purpose, the logistic regression technique is employed while taking CEO personal and professional attributes as explanatory variables and CSR disclosure as the dependent variable. Results indicate that firm size and CSR disclosure has a positive relationship. The outcomes based on binary logistic regression demonstrate that CEO ownership has a negative impact, whereas CEO tenure, CEO education, CEO age, and CEO compensation are the variables that have a positive impact on CSR disclosure. In addition, duality, ownership, and gender of the CEO are found to be insignificant. Evidence on CEO demographics and their impact on disclosure choice might be helpful for policymakers and regulators. This study lacks generalization due to the unique setting of Pakistan. Our research contributes to the body of knowledge containing upper echelons theory in several ways. First, it answers the call for an extension of research toward social responsibility disclosures and individual’s traits impact on it. Second, our study adds to the scarce literature available on CSR research and practices in developing countries. Third, it is one of the first quantitative studies in the specific context of Pakistan as data for these variables is not available in organized form publicly.

Introduction

Disclosure regarding corporate social responsibility (CSR) is a crucial part of the strategic policy of the firm. The concept of CSR genuinely prevails in developed countries in contrast to the majority of developing countries where understanding, implementation, and evaluation of the term is still in its inception stage (Freeman & Reed, 1983; Jones, 1995; Porter & Kramer, 2006). CSR literature mainly covers developed economies, for example the United States and Europe and Australia (Argenti, 1976; Blackburn, 1994; Cheng et al., 2010; Huang & Lien, 2012; Subrahmanyam, 2008). The extent and quality of disclosure choice vary depending on various factors such as institutional environment, market forces pressure, and national setting. Vast research on CSR determinants is conducted in the context of developing countries, yet there is a scarcity of literature available focusing on understanding different contexts, national, and institutional differences in developing nations (Eisenhardt, 1989). Few studies emphasized on institutional differences such as conception, implementation, and evaluation of CSR concept (Dahya et al., 1996; Grimm & Smith, 1991; Huang & Lien, 2012; Miller, 1991; Rechner & Dalton, 1991). Others focused on implicit and explicit organizational determinants affecting CSR such as environmental management strategy, risk management, firm size, and export policy decisions. (Eng & Mak, 2003; Fabrizi et al., 2014; Hambrick & Fukutomi, 1991). There is scant literature available on individual characteristics of organizational figures responsible for making strategic decisions, including corporate social responsibility disclosure (CSRD) as identified by a review study (G. Chau & Gray, 2010). This study aims to contribute toward filling this gap in CSR literature by incorporating CEO attributes as independent variables.

For this purpose, widely used theory in the behavioral literature, including psychology and finance domains, upper echelons theory (UET) seems appropriate to study individual beliefs, values, and behaviors (Hambrick & Mason, 1984). According to this theory, some of the observable personal attributes can hamper/trigger the decision-making process, including CSR decisions. Moreover, if the CEO and Chair of a firm are the same person, does it affect the functionality of the Board of directors’ decision-making power or not? Also, if Chief Executive Officer of the firm owns shares in his or her name, does it influences the disclosure policy of CSR activities or not? Does monetary or nonmonetary compensation paid to the CEO has an impact on CSRD. These important questions need to be explored, especially in the context of developing country like Pakistan.

This study aims to contribute to developing countries literature by undertaking Pakistan in this particular context. There are several reasons to study an emerging economy like Pakistan. First, it stands in top countries in terms of the population both in South Asia and the World, that is, current population 204.6 million representing 2.65% of the world population reported by the latest United Nations estimate (Oh et al., 2011), therefore, provides a stable ground to explore the globally hyped CSR phenomenon in Pakistan. Second, CSR reporting and practices are still in infancy stage in Pakistan so, there is a pivotal need to study the underexplored dimensions of CSR such as the impact of managerial attributes on socially responsible behavior of corporate sector. Third, the current study aims to fill the missing gap by studying the internal contextual factors in the context of developing economies to which little attention have been paid previously. In this regard, most of the studies focused on overall attitudes of executives toward disclosure and found positive outcomes (Barker & Mueller, 2002; Fabrizi et al., 2014; Farh et al., 1998; Jensen & Meckling, 1976; Jensen & Murphy, 1990; Khan et al., 2013). Our study aims to contribute by focusing on the influence of CEO attributes, specifically on disclosure using the lens of UET.

A reasonable number of studies are available as regard to the impact of CEO’s attributes over firm financial performance, but there is still a scarcity of literature on the issue that whether characteristics of CEO affect disclosure of corporate social activities or not (Cheng et al., 2010; Huang & Lien, 2012). Characteristics of decision makers are under consideration of an emerging body of knowledge related to behavioral finance literature (Huang & Lien, 2012; Subrahmanyam, 2008). In this context, UET explains this matter in behavioral finance. According to Nielsen and Nielsen (2011), the more complex a strategic decision is, the more it matters to consider the characteristics of the decision makers. He further explains that managers’ education, tenure, gender, and age are the different factors that affect the strategy and structure of the firm, and as a result, strategic choice and firm’s performance.

Our research contributes to the body of knowledge containing upper echelons literature in several ways. First, it responds to the call for an extension of research toward social responsibility disclosures and individual’s demographic and professional traits’ impact on it (Anderson & Reeb, 2003). Second, our study adds to the limited evidence available on the executive influence on voluntary reporting practices for developing countries (Daily & Dalton, 2003; Ting et al., 2015; Zhang et al., 2013). Third, it contributes to the emerging economies literature in particular context of Pakistan from this unique underexplored perspective (Huang & Lien, 2012). Moreover, our results are in correspondence with the existing literature and relevant theories.

In the following section, we will develop our argument further. First, a brief literature review of the independent variables included in this study is presented that leads to the development of specific hypotheses. To test these hypotheses, we have explained the econometric model and variables. Finally, a presentation of results as well as discussion and conclusive remarks are provided in conjunction with the limitations of the study.

Literature Review & Hypothesis Development

Institutional Background of Pakistan

According to developing economies literature, CSR is a dynamic and socially constructed concept, which means that the same kind of corporate behavior may not be acceptable in every culture and society (Hambrick & Mason, 1984; Herrmann & Datta, 2002; Huang & Lien, 2012). Instead, it varies according to the laws, regulations, economy, values, cultural differences, and so on, of the country under study. Securities and Exchange Commission of Pakistan (SECP), the regulatory body responsible for the monitoring of listed and nonlisted firms in Pakistan issued CSR voluntary regulations for companies in 2013 (Frank et al., 1993). The intent was to guide and encourage firms to disclose more by providing material and timely information to its investors and stakeholders. Recently, SECP issued the listed companies code of governance regulation to promote CSR practices (Manner, 2010). This regulation stresses sustainable environmental, social, and governance aspects as well as workplace safety, charity, and philanthropic acts.

Moreover, according to Udayasankar (2008), CEO of listed companies in Pakistan are held responsible for taking initiatives to identify issues regarding environmental, social, and governance matters so that board of directors can make decisions and introduce supporting policies in this regard. Despite having these initiatives by regulatory bodies, the implementation of CSR is still weak in Pakistani setting because of the informal institutional environment (Cox, 1958). CSR literature mainly comprises of studies featuring developed countries as compared to the developing economies, and the same is case with Pakistan, therefore, this study attempts to fill this gap taking Pakistan as a developing country (Duru et al., 2016; Palaniappan, 2017; Peng et al., 2002; Vintila & Gherghina, 2012; Yan Lam & Kam Lee, 2008).

Based on the above background, we propose the subsequent hypotheses to perform empirical testing afterward.

CEO Duality and Disclosure

Another phenomenon of corporate governance is the concentration of decision power. There are two types of structures; one in which CEO is the same person as Chairman of the Board, whereas other in which CEO and Chairman are two different persons. This may affect the decision making of the firm concerning CSRD.

There are two theories that prevail in this regard. Proponents of agency theory demand the separation of roles to ensure some checks and control system over management policies and decisions. If the CEO is the same person as chair of the board, the effectiveness of the board members will be at risk, as he or she may intervene in board matters, which may result in compromised performance. Argenti (1976) and Blackburn (1994) supported this view. The contrasting view of agency theory is the stewardship theory, which advocates the concentration of decision power in one person. The proponents of this view hold that there could be better management, active control, less intervention, and progress toward organizational objectives. This theory views corporate managers as protectors of organizational interests and working in the best interests of the organization. Several studies hold this view as a positive indicator of decision power (Dahya et al., 1996; Eisenhardt, 1989; Rechner & Dalton, 1991).

Nevertheless, separation of roles is an indicator of effective monitoring, better control, and lower the risk of biased disclosure, enhancing the quality of disclosure. In the Pakistani context, listed firms are observed to have separation of roles in general; therefore, it is worth testing whether CEO duality has an impact on disclosure or not. Therefore, we put forward the following hypothesis:

Tenure and Disclosure

The more the length of time spent by a manager in the office handling office tasks/challenges, the more he or she tends to be experienced and knowledgeable. Tenure/time spent in a particular position makes a person more responsible, organized, confident, autonomous, and strategically aware (Miller, 1991). In a similar context, Huang and Lien (2012) and Cheng et al. (2010) demonstrate that tenure posits a significantly viable impact on firm performance. Strategic changes are made for the long term usually; therefore, as the length of tenure progresses, several changes in corporate strategic approach might be evidenced (Grimm & Smith, 1991; Hambrick & Fukutomi, 1991). Longer tenure signifies less insecurity, more power, and entrenchment resulting in a lower focus on CSR investment (Fabrizi et al., 2014). On the contrary, being a newbie as a CEO requires more effort to need to legitimize one by engaging in CSR thereof (Fabrizi et al., 2014).

In the light of above argument, we propose that a CEO who is more experienced tend to be more aware and conscious about CSR practices and its disclosure whether it be legitimacy purpose or it may support stakeholder perspective.

CEO Ownership and Disclosure

Managerial ownership has remained a matter of great interest to corporate finance researchers. CEO ownership concentration is a fast result in dominated strategic decisions, and such firms do not recognize the need for accountability. Since such companies are closely held, the public interest is relatively small. They do not invest in broader social activities, as they believe that these costs may outweigh the benefits associated with investing and disclosing such endeavors. The limited evidence available in this regard documents a negative association between the managerial ownership and CSRD (G. Chau & Gray, 2010; Eng & Mak, 2003; Khan et al., 2013; Oh et al., 2011). Considering the above evidence, we propose the following hypothesis:

CEO Compensation and Disclosure

Monetary and nonmonetary incentives can play a pivotal role in a person’s decision choices. CEO being the driving force of the firm’s strategic direction is the key official whose monetary and nonmonetary interests may affect the CSR-related decisions. Following agency theory, compensation in monetary terms, for example, equity shares and annual bonus has a negative impact on the CEO’s disclosure choice as in such a situation, CEO’s will safeguard their own interests that become similar as of shareholders instead of making investment in CSR (Fabrizi et al., 2014; Jensen & Meckling, 1976; Jensen & Murphy, 1990). On the contrary, nonmonetary benefits such as time horizon, age, power, and entrenchment affect the CEO positively.

Therefore, we put forward the following hypothesis:

CEO Age and Disclosure

Top managers’ tendency to indulge in innovative activities is reduced as the age progresses, probably due to risk aversion and playing safe attitude (Barker & Mueller, 2002). On the contrary, experience and knowledge of an older executive are assumed higher than that of a younger executive, and it makes them more mature, more competent and able to make rational decisions (Farh et al., 1998). Another strand of research argues that since young CEOs are at the beginning of their career would not like to take long-term investments as such investments yield future returns, yet their concentration is to enhance short-term market performance. However, older CEOs having no career and reputation concerns would go for endeavors that are beneficial for the firm in the long run (Yuan et al., 2019).

Although Huang and Lien (2012) found no significant relationship between CEO age and CSR performance; however, there is sufficient literature support to develop the following hypothesis:

CEO Gender and Disclosure

UET deals with values, beliefs, and thinking patterns of upper-level management that may influence corporate decisions (Hambrick & Mason, 1984). A review of antecedents, elements, and consequences of UET suggest gender as an essential construct to study in the context of corporate social performance (Vintila & Gherghina, 2012). The executive’s gender plays a vital role in opting for the right strategic choice and its outcome (Anderson & Reeb, 2003; Barako et al., 2006; Naser, 1998). In a study taken into account publicly listed companies in Bursa stock exchange for 10 years, Ting et al. (2015) advocate that female CEOs are more prone to risk-taking as compared to their male counterparts. Although a large number of listed firms in Pakistan are categorized as family firms, female representation on board may be considered as a mere representation of gender diverse board; still, there is an ever increasing number of female entrepreneurs in Pakistan, it is of vital significance to determine whether gender diversity plays a role in CSRD choices. Some researchers have posited that female directors are more sensitive as a matter to fulfill stakeholders’ anticipations, therefore, making rest of the board members conscious about disclosure too (Daily & Dalton, 2003; Zhang et al., 2013). G. K. Chau and Gray (2002) document CEO gender differences in terms of risk-taking and capital allocation efficiency and report that female CEO proves to be more successful in lowering leverage levels and maintain less volatility in earnings. These results present a vivid picture of the impact; managerial traits have on decisions and organizational outcomes. Keeping in view the above arguments, we hypothesize that the following hypothesis:

Education and Disclosure

Level of education, as well as the quality of education of top management both, plays an equally important role in determining the disclosure policy of the firm. An educated individual tends to be well aware of the importance and significance of disclosure of social and environmental activities. Well-educated CEOs may prove as better decision makers, as they are exposed to better knowledge and open-minded approach (Hambrick & Mason, 1984; Herrmann & Datta, 2002). Despite this view, another school of thought believes that except MS and MBA degrees, other degrees do not influence the CSR performance of the firm, that is only specialized education may affect CSR performance (Huang & Lien, 2012).

Educational background is considered as a means of determining the moral and ethical approach of an individual, as these grounds shape up one’s thinking process and one reacts accordingly (Frank et al., 1993; Hambrick & Mason, 1984; Manner, 2010).

Following this literature, we propose that the following hypothesis:

Size and CSRD

The decision of an organization about whether to opt for disclosure of its social activities largely depends on its size. One school of thought argues that organizations at their inception stage usually operate at a small level and do not prefer adopting CSR policies and its disclosure. The reasons behind maybe that small-scale and medium-scale organizations have restrained access to resources, lower visibility, and small operating capacity. Another viewpoint is that firm size and CSRD have a U-shaped relationship, which indicates that small as well as large firms regardless of their size are equally enthusiastic toward CSR participation and disclosure; however, their objectives may differ (Udayasankar, 2008). Thus, we hypothesize that,

Methodology

Sample and Data

In this study, the positivist approach is employed in the development of the hypothesis, which is then tested using statistical analysis. According to Burrell and Morgan (1981), positivists “seek to explain and predict what happens in the social world by searching for regularities and causal relationships between its constituent elements.” The deduction is allied to positivism and aids in establishing the causal links between or among variables of the study to make a generalized conclusion (Saunders et al., 2007). However, the type of sampling and sample-selection procedure are the vital concerns for generalizability and the risk of standard method bias and common method variance (Fuller et al., 2016). Thus, in this study, we used the deductive approach instead of an inductive approach.

To overcome the possibility of common method bias, the sample is selected in stages as proposed by Podsakoff et al. (2012). At the first stage, six leading sectors of Pakistan’s economy are selected based on their contribution toward gross domestic product (GDP) over the years, and then the firms are selected based on their market capitalization, availability of their balance sheets, and annual reports on their websites. Finally, 179 firms from six different sectors are selected from 2009 to 2018 comprising of 1,790 firm-year observations. Gujarati (2014) stated that panel data provide “more information, more variability, less collinearity among variables, more degrees of freedom, and more efficiency.” Table 1 presents the sector-wise distribution of our sample companies. Annual reports, websites, and CSR reports; all these sources are taken into account for the measurement of CSRD.

Sample Distribution.

Conceptual Model

Figure 1 depicts the conceptual model comprising of main constructs and their relationships.

Conceptual representation of model.

Variables

Table 2 describes the dependent variables, explanatory variables, and their respective definitions. CSRD is the dependent variable, which is measured in two ways; that is, one in binary term and second, by taking the CSRD index. CSRD index is obtained by dividing the sum of disclosed dimensions by the total number of dimensions of CSR, adapted from the dimensions proposed by Ernst and Ernst (1978). The firms that disclose their CSR information are assigned “1,” whereas the firms that do not disclose their CSR information are marked with “0.” CEO duality, CEO tenure, CEO age, CEO education, CEO gender, CEO ownership, and CEO compensation are the explanatory variables. Firm size measured by two indicators describing financial impact over CSR is taken as a control variable.

Description of Variables.

Note. CSRD = corporate social responsibility disclosure; CSR = corporate social responsibility; CSRDI = Corporate Social Responsibility Disclosure Index; CEOD = CEO duality; CEOT = CEO tenure; CEOWN = CEO ownership; CEOS = CEO annual compensation; CEOA = CEO age; CEOG = CEO gender; CEOEDU = CEO education; LTA = total assets; LSH = log of total number of shares; GOWN = Govt. ownership.

Econometric Model

Cox (1958) presented a method, that is, binary logistic regression analysis to determine the likelihood of a binary variable on account of a single or several independent variables that whether they are categorical or quantitative by nature. Since the assumptions of classical linear regression are invalid for binary logistic regression, we performed a logistic regression analysis for our dependent variable. As recommended by Peng et al. (2002), the appropriate number of observations for logistic regression analysis is no less than 100; our observations count is 1,790; indeed, a safe number to proceed.

Accordingly, the econometric model of this study is as follows:

Discussion of Results

Descriptive Statistics

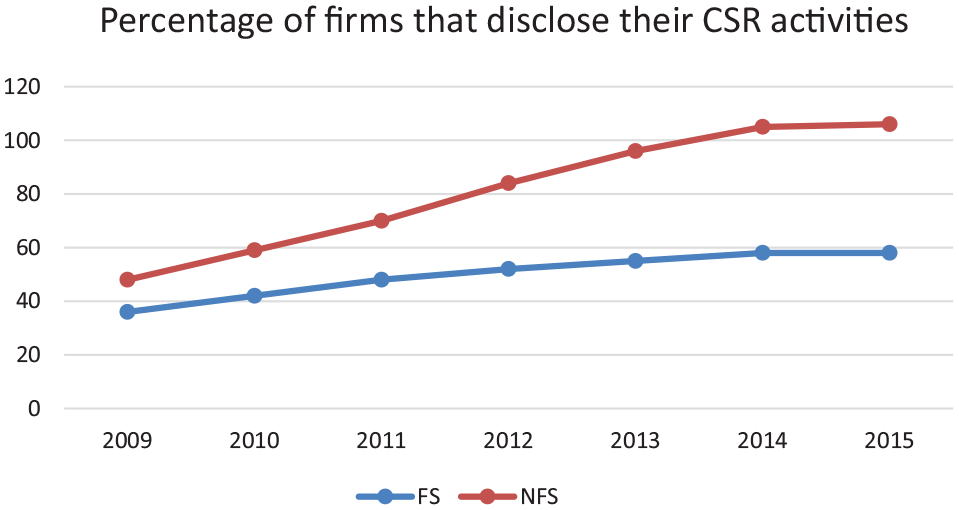

As we are discussing a developing economy in this study, Figure 2 shows that disclosure of social activities is gradually increasing in the financial sector as well as in the nonfinancial sector for the period 2009 to 2018. As for the financial sector is concerned, 30% of our sample represent those firms that disclose their CSR activities, while 49% of companies from the financial sector appeared to disclose CSR activities.

Percentage of firms that disclose their CSR activities.

Panel A in Table 3 posits the descriptive outline of categorical variables. Among the selected firms, CEO duality exists in 17% of the firms, that is, the Chair performs the functions of CEO, whereas in the majority of firms, that is 83% of the firms; separation of roles is observed. A study carried out in the Hong Kong context, 41% of the firms had possessed CEO duality (Yan Lam & Kam Lee, 2008). However, the United States was experiencing a decline in CEO duality, for example, from more than 75% in the 1990s to just 50% in 2016 with the increasing awareness of separate ownership; however, Pakistan, being a developing country is still far behind developed countries such as the United States (Duru et al., 2016). CEOs ownership concentration ensures the safety of shareholders’ interests. European firms disclose more in terms of managerial ownership in their balance sheets and annual reports, whereas, among our selected firms, 5% of the firms are observed to possess at least some proportion of shares whether it is due to the dual role of CEO or it is the part of their compensation, hence disclosing comparatively lesser.

Descriptive Statistics of Variables.

Note. CEOT = CEO tenure; CEOWN = CEO ownership; CEOS = CEO annual compensation; CEOA = CEO age; CSRDI = Corporate Social Responsibility Disclosure Index.

Our sample has only 23% firms with female CEOs that is undoubtedly inadequate but following the traditional context of Pakistan where the corporate sector is male dominated in contrast to the United Kingdom, where 41% of the firms are led by female CEOs (Palaniappan, 2017). In Pakistan, female participation in the corporate sector is meager and significantly lower in managerial positions. There are many reasons for the low participation, that is, typical characteristics of society including (a) women bearing more family responsibilities than men, (b) allocation of distinct roles by the society for males and females, and (c) male dominance in corporate culture. The mere existence of a small proportion of female CEOs also points toward family-owned firms, where a female CEO is the indication of gender diversity and not for the actual representation. MS in Business Administration or MS in public administration is considered as specialized education for CSR awareness, and only 16% of our sample firms are found to have such qualified CEOs.

Descriptive statistics for continuous variables consisting of CEO characteristics and control variables are provided in Table 3 Panel B, stating their minimum, maximum, average values, and variation. CEO’s tenure lies between 1 to 5 years, with an average of 1.4 years serving in the same firm that indicates the reluctance of the firms to hire the CEO for a longer tenure. Average tenure being 1.4 years is relatively short as compared to the average tenure of 10 years for the firms listed in New York Stock Exchange (Vintila & Gherghina, 2012).

Age of CEO ranges between 32 to 69 years, and the average age is 46 years denoting majority of CEOs falling in the age category of 40s. Comparing our results to a developed country (e.g., the United States), CEOs’ average age is 55 years with a range of 34 to 75 years (Vintila & Gherghina, 2012). The average compensation of the selected firms over the sample period is found to be 14 million rupees. Similarly, the average number of shares and total assets of all the firms over the sample are 0.49 and 18 billion rupees, respectively.

Correlation Analysis

Correlation analysis based on the scale of measurements of the variables of interest. Pearson correlation is measured to examine the interdependence of quantitative explanatory variables. Pearson correlation is considered as the best way to examine the strength as well as the direction of the interdependence of the continuous variables because of this method based on the covariance of the variables of the interest (Bobko, 2001).

Table 4 suggests that the correlation between CEO compensation and tenure is observed to be positive as well as significant; CEO age and compensation are positive and statistically significant, whereas the relationship between CEO age and tenure is observed to be positive but statistically insignificant. The strength of relationship also helps to know which pair of explanatory variables cause multicollinearity problem in causal studies. Table 4 indicates that multicollinearity is not a severe problem for this study (Bobko, 2001).

Correlation Matrix.

Note. CEOD = CEO duality; CEOT = CEO tenure; CEOEDU = CEO education; CEOWN = CEO ownership; CEOS = CEO annual compensation; CEOA = CEO age; CEOEDU = CEO education; GOWN = Govt.ownership; CSRDI = Corporate Social Responsibility Disclosure Index; LTA = total assets; LSH = log of total number of shares.

Significant at 10% level. **Significant at 5% level. ***Significant at 1% level.

Logistic Regression Outcomes

To ensure the robustness of results, we applied the tests of linearity and to remove outliers from the data, Box–Tidwell transformation is utilized. From results, we found that total assets and some shares appear to be significant, that is (p < .01). Total assets and number of shares have been transformed via Natural log transformation to validate the linearity. To estimate the outlier effect, several techniques such as Student residuals, deviance, and Cook’s distance (D) are employed. These techniques showed that our model is unaffected by the extreme value effect.

The logistic regression model is based on CEO characteristics and control variables as discussed above, taking CSRD as the dependent variable. The significance of chi-square determines that sample data describes the proposed model.

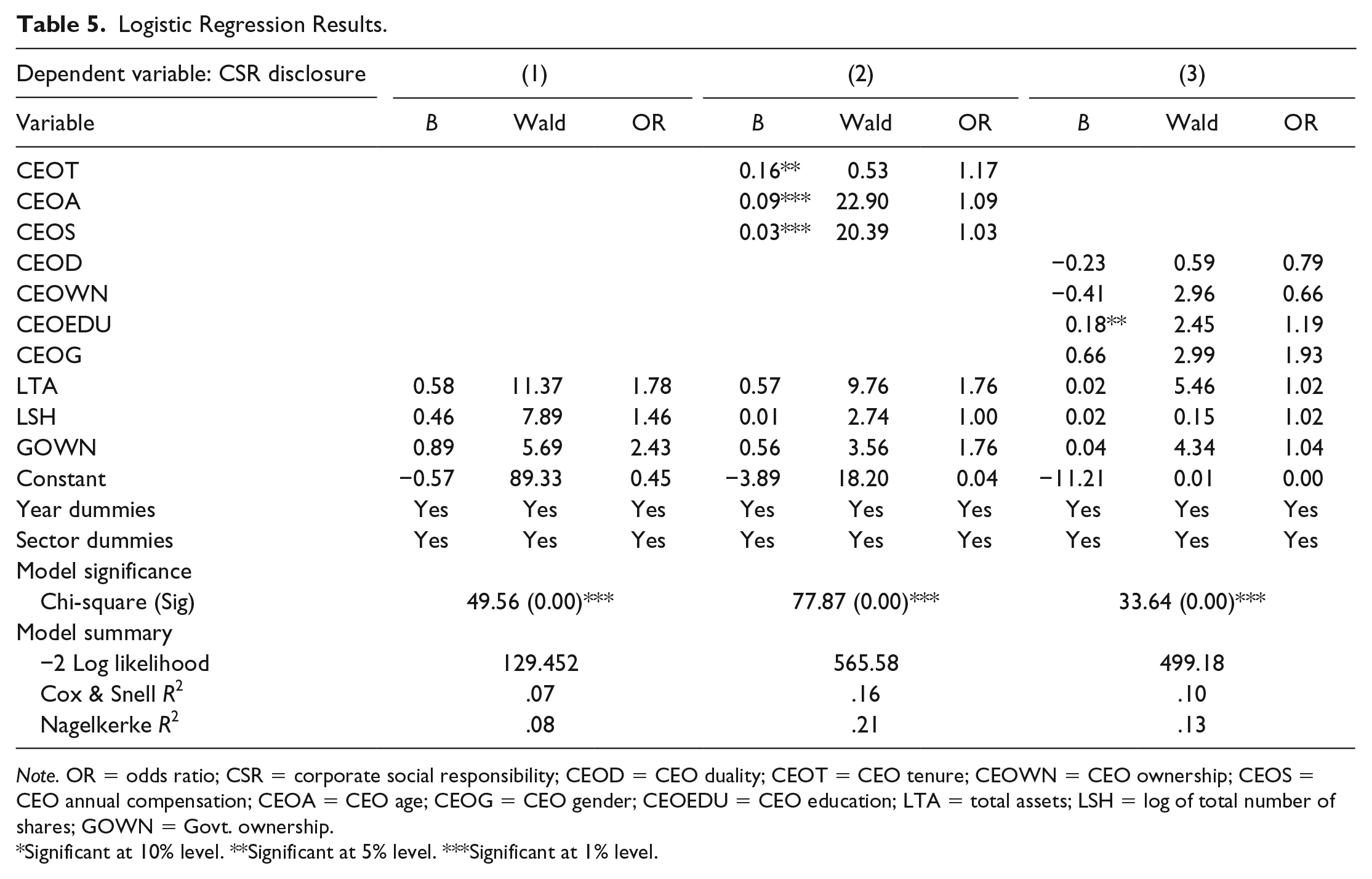

Table 5 displays the results of logistic regression in the form of coefficient (B), Wald statistic (Wald), significance (Sig.), and odds ratio Exp (B). Among CEO characteristics, coefficients of CEO tenure, CEO age, and CEO compensation, CEO education, are positive as well as significant at 1% and 5% level supporting the formerly stated hypothesis 2, 4, 5, and 7; however, the hypotheses related to CEO duality, CEO gender, and CEO ownership are found to be insignificant.

Logistic Regression Results.

Note. OR = odds ratio; CSR = corporate social responsibility; CEOD = CEO duality; CEOT = CEO tenure; CEOWN = CEO ownership; CEOS = CEO annual compensation; CEOA = CEO age; CEOG = CEO gender; CEOEDU = CEO education; LTA = total assets; LSH = log of total number of shares; GOWN = Govt. ownership.

Significant at 10% level. **Significant at 5% level. ***Significant at 1% level.

The negative impact of CEO ownership over the CSRD implies that the lower the number of shares a CEO possesses in the firm, the higher the odds of the disclosure. Our findings confirm our proposed hypothesis as well as what previous literature suggests (G. Chau & Gray, 2010; Eng & Mak, 2003; Khan et al., 2013; Oh et al., 2011). Prior literature suggests that a well-educated CEO is likely to be more aware of firm disclosure needs and tends to make better decisions as such individual may possess an open-minded and knowledgeable approach (Hambrick & Mason, 1984; Herrmann & Datta, 2002; Huang & Lien, 2012; Manner, 2010). Our results coincide with the literature such that if CEO formal education improves, the likelihood of CSRD raises 1.2 times. Likewise, the firm will likely to disclose CSR one times more if the CEO will be older in age implying that older CEOs have better ability to perform, are more mature, competent, and future-oriented regarding firm’s long-term progress as evidenced by previous studies (Farh et al., 1998; Huang & Lien, 2012; Yuan et al., 2019). In addition, an increase of one point in CEO compensation may result in the probability of an increase in CSRD. The same way, odds of CSRD grow 1.18 times as the CEO tenure is increased by one point suggesting that experienced CEOs tend to be more mature, confident, autonomous, and strategically aware (Miller, 1991). These traits imply an improvement in firm performance that occurs as a result of intelligent strategic decisions made by the CEO (Cheng et al., 2010; Huang & Lien, 2012). Another implication of this outcome may be an indication of lower insecurity, more power, and entrenchment of CEO while taking CSR decisions (Fabrizi et al., 2014; Grimm & Smith, 1991; Hambrick & Fukutomi, 1991). Summing up the above discussion, all the three models are significant, as the value of chi-square is found significant at 1% level and values of Cox and Snell R2 and Nagelkerke R2 are less than one referring to the reliable explanatory power of the models. We have also carried out robustness tests for these results as follows.

Robustness of Results

Additional robustness tests have been incorporated by taking CSR index (quantitative measure) as a dependent variable following Ernst & Ernst (1978). Fixed-effects pooled regression analysis has been carried out using clustered standard errors. The findings are consistent with those of the results of logistic regression reported in Table 5. CEO tenure, age, compensation, and education are found to be significant in all three models. Overall, the results in Table 6 support our hypothesis 2, 4, 5, and 7 and show that CEO tenure, age, education, and compensation have a positive and significant impact on CSRD.

Panel Regression Results.

Note. CSR = corporate social responsibility; CEOD = CEO duality; CEOT = CEO tenure; CEOWN = CEO ownership; CEOS = CEO annual compensation; CEOA = CEO age; CEOG = CEO gender; CEOEDU = CEO education; LTA = total assets; LSH = log of total number of shares; GOWN = Govt. ownership.

Significant at 10% level. **Significant at 5% level. ***Significant at 1% level.

Conclusion and Recommendations

There are contrasting views about the factors that become the reason behind disclosure of social and environmental activities like profitability (Barako et al., 2006; Naser, 1998), level of disperse ownership (G. K. Chau & Gray, 2002), development of positive perception by customers (East et al., 2016) as well as complying with regulatory standards (Zhao, 2012). However, the purpose of this study is to bring forward a relatively neglected area of corporate governance literature, that is, whether the CEO’s personal and professional attributes affect CSRD or not. Taking 179 companies from six sectors listed at Pakistan Stock Exchange for the years 2009 to 2018, we test the hypotheses developed in this study. The outcomes based on binary logistic regression demonstrated that CEO tenure, CEO education, CEO age, and CEO compensation are the variables that have a positive impact on CSRD. In addition, duality, gender, and ownership of the CEO are found to be insignificant. Robustness is checked by employing the panel regression technique, and all results are consistent with our base model results.

The dual role performed by the CEO is found to be negative however, insignificant in case of Pakistani firms. As there is family involvement in more or less 80% of Pakistani firms in direct or indirect ways so, it is evident that such firms being in the majority does not have a significant impact on CSRD.

Coinciding with the previous literature, our results indicate that the larger the firm size, the better the CSRD (Yuan et al., 2019). Larger firms, in general, disclose more as compared to smaller ones. In Pakistan, larger firms in terms of size have more resources; keep a larger share of market capitalization needs to legitimize their existence through disclosure of their CSR activities that are similar to the legitimacy hypothesis. CEO’s education and age both imply toward better exposure and enhanced experience. Possessing these attributes, the CEO may have a better understanding of the advantages and importance of disclosure. Besides, a well-compensated CEO may play a decisive role in disclosing CSR activities and compensation could be in nonmonetary terms. CEO ownership concentration affects disclosure negatively, as it causes strategic autonomy of CEO and does not encourage the need for accountability.

Our findings are not free from limitations. Other demographic attributes such as marital status, orientation toward religion that could also be an influential factor are missing in this study. Moreover, data from one country is taken, which limits its application. Our dependent variable is binary that does not account for the extent and quality of CSRD. Future research may incorporate these factors into consideration. Despite these limitations, the study provides useful insights.

Outcomes of this study might provide evidence for policymakers and regulators, as CEO is the crucial factor in determining the organization’s progress toward its strategic direction. Moreover, requirements for the selection and functional role of the CEO should be standardized so that the quality of disclosure is improved. To ensure transparency and separation of power between the CEO and Chairman, Pakistani policymakers may encourage listed firms to induce more independence to enhance the proportion of independent directors. Countries with a corresponding corporate setting and regulatory structure may benefit from our results.

Footnotes

Author’s Note

Muhammad Akram Naseem is also affiliated with Lahore Business School,The University of Lahore, Pakistan and School of Internet Economics and Business, Fujian University of Technology, China.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.