Abstract

The study examines the relative contributions of external shocks and institutional quality to macroeconomic performance in Nigeria, using Structural Vector Autoregressive (SVAR) approach. The study establishes the dominance of the relative contributions of external shocks measures over institutional quality to macroeconomic performance in the country. Even though the dominance of terms of trade and foreign aid is highlighted, the role of institutional quality is equally important as it also has significant positive effect on performance. The study concludes that both external shocks and institutional quality play significant roles, and hence, posits the existence of favorable institutional environments as a panacea to successfully absorbing the influence of external shocks which are exogenous to the economy.

Introduction

Most countries across the globe (Nigeria inclusive) are aspiring to attain virile economy. However, while the institutional arrangements in the developed countries give room for enriched employment opportunities, better productivity, and favorable balance of payments—all of which culminate in qualitative standard of living—the reverse happens to be the case in Nigeria (Iyoboyi et al., 2016). The economic performance in the country has, from time immemorial, been tainted by social vices in the form of institutionalized corruption which impedes the public office holders from diligently delivering services indispensable for better economy. Numerous attempts that have been made to revamp the economy have yielded abysmal results in spite of the plentiful human and natural resources in Nigeria (World Bank, 2012). This is closely linked to the poor quality of Nigeria’s institutions. The efforts of the government to transform the economy will not materialize unless the institutional arrangements are addressed. With the resources in the country, the Nigerian market ought to be able to produce a significant proportion of its national demand without necessarily relying on importation if given favorable institutional environments.

An economy that is highly vulnerable to shocks would not be appealing to investors. This, in addition to the structural factors, might have contributed to the closure and relocation of many companies from Nigeria to the neighboring countries in the recent years. The way Nigeria responds to these shocks is essential to its long-run potential growth. Hence, the fight against corruption by the current administration may be short-lived if the institutional capacity is not developed. There is need for institutions that can give room for extensive economic participation as well as effective checks and balances.

External shocks occur when unpredictable change in an exogenous factor affects endogenous economic variables. Hence, economies that rely on foreign resources and foreign markets are more susceptible to external shocks than others. It is common among policymakers to ascribe volatility in economic performance in developing countries to external shocks. Although the importance attached to external shocks is reasonable based on some prevalent structural features, this does not imply that external shocks are solely responsible for the volatility. Internal shocks emanating from corruption, political irresponsibility, and other forms of social vices are potential sources of volatility. Specifically, disparities in economic institutions are the main cause of disparities in economic performance across the globe (Acemoglu et al., 2003, 2005; Acemoglu & Robinson, 2008).

Studies by Calderon et al. (2012), Ushie et al. (2013), and Adigozalov and Rahimov (2015) point out the significance of institutions in influencing policy responses to exogenous shocks as well as enhancing equitable distribution of income. The studies maintain that the more qualitative institutions are, the greater the level of efficiency which will then propel economic development. Hence, it is the institutional quality that offers the framework upon which macroeconomic performance can be evaluated. Iyoboyi and Pedro (2014) attribute the poor implementation of policies in the developing countries to the prevalence of weak institutions in the countries. While good institutional quality in an economy helps to ameliorate the influence of external shocks on economic performance, the reverse is the case where the quality of institutions is weak.

Contrary to the International Monetary Fund (IMF; 2015) claim that the recent sharp decline in the global oil prices would help small states in maintaining low inflation and reinforcing growth prospects, Nigeria has been experiencing stagflation in the recent years. This, however, is not unconnected with the non-availability of supportive structural environment needed to absorb external shocks. To get a true picture of why a country is poor, one needs to understand why its institutions are malfunctioning.

The fluctuations in the price of crude oil over the years (getting to the highest level of $123.97 per barrel in the second quarter of 2008 but followed by a sharp decline to $42.95 per barrel in the first quarter of 2009, another boom between 2010 and 2011, and consistent decline since mid-2014 till the first quarter of 2018) have raised serious concern about its macroeconomic implications globally. This is more pathetic in Nigeria that is witnessing decline in both oil price and oil production level. The country is also experiencing enormous importation of refined petroleum products as a result of the comatose of the domestic refineries.

As developing countries are observed to be dependent on the rest of the world, the appraisal of external shocks becomes essential. Meanwhile, there is no consensus in the literature regarding the influence of external shocks on economic performance of these developing countries. One of the main gaps in the preceding studies on Nigeria is the failure to consider the possibility of institutions in ameliorating or aggravating the influence of external shocks on macroeconomic performance. The country is not devoid of policies and reforms over the years. However, all these have yielded abysmal results. The reason behind their woeful results might not be far from the fact that the quality of the domestic institutions as a transmission mechanism through which external shocks operate has not been given due attention.

While poor institutional quality may aggravate the menace of external shocks on economic performance, an economy with proper institutional quality may alleviate the adverse consequence of external shocks on economic performance. The possibility of these reverse relationships calls for investigation, and this necessitates the present study. While prior studies on Nigeria examined the influence of external shocks and institutions on macroeconomic performance individually, they are considered simultaneously in the present study in a single framework and their joint influence on macroeconomic performance are investigated. This is based on the realization of the importance of the institutional quality in designing sound macroeconomic policies and making rational economic decisions. This will consequently metamorphose into higher standard of living of the populace.

The remaining part of this article is organized as follows: The “Theoretical and Empirical Review of Literature” section caters for the review of literature while the “Method” section describes the methodology used. The section “Estimated Results” contains the estimated results and the “Conclusion” section concludes the study, followed by policy recommendations in section “Policy Recommendations.”

Theoretical and Empirical Review of Literature

There are controversies among economists regarding the necessity of stabilization policies in enhancing stable macroeconomic performance. While the monetarists believe that an economy is stable enough so that stabilization policies are not necessary, the non-monetarists, on the contrary, argue that an economy experiences instability that necessitates active stabilization (Modigliani, 1988). The neoclassical growth model posits that countries with the same production functions, savings rates, identical depreciation rates, and population growth tend to grow at the same rate in the steady state, and this leads to convergence in the long run (Solow, 1956). This assertion is premised on the assertion that poor countries with lower initial income experience higher growth rates than richer countries. In reality, however, the convergence theory does not always hold as production functions vary across countries. The variations in the production functions are usually attributable to the following factors: technological progress, human capital, and public and social infrastructure, which includes institutions and the rule of law.

However, the endogenous growth theory states that economic growth is an endogenous result of an economic system rather than the result of external forces (Romer, 1994). Hence, several scholars claim that political and economic institutions are fundamental to the improvement of macroeconomic performance of the developing countries (Burda & Wyplosz, 2009; Hall & Jones, 1999; North, 1994; Tornell & Velasco, 1992). This claim is given credence by the study of Franko (2007) which maintains that institutional quality is the key predictor for growth as it provides incentives to invest in technology, and thus, calls for its improvement in the developing countries.

Correspondingly, institutional quality plays a significant role in the effectiveness of foreign aid and terms of trade with respect to economic growth. For instance, a country with improved institutions tends to make judicious use of foreign aid received than the otherwise. Thus, Burnside and Dollar (1997) claim that foreign aid has a positive effect on economic growth in developing countries, but only when combined with proper economic policies. Also, Dollar and Kraay (2003) suggest that institutions and trade have a joint effect on economic growth in the long run. Likewise, the monetary authorities of the countries with improved quality of institutions tend to be proactive in their dealings with external shocks as well as stabilization of output and inflation. Hence, Calderon et al. (2012) posit that high institutional quality enables countries to apply counter-cyclical monetary and fiscal policies to combat external shocks—as countries with strong institutions will adopt contractionary policies during booms and expansionary policies during recessions.

Meanwhile, the neoclassical and the Keynesian theories of economics have not been able to proffer suitable explanation for the poor performance of macroeconomic variables in the developing countries. Despite enormous reforms in these developing countries, they fail to take the right actions necessary for them to coordinate the market economy for optimal performance. On a general note, while it makes economic sense to stabilize exogenous shocks in an economy, this may not automatically guarantee significant reduction in the macroeconomic volatility. As developing countries happen to be dependent on the developed ones, the appraisal of external shocks becomes imperative. Meanwhile, there is no consensus in the literature regarding the influence of external shocks on economic performance of these developing countries.

Study by Genberg (2003) estimates the relative importance of domestic and foreign shocks as sources of macroeconomic fluctuations in Hong Kong. Using Structural Vector Autoregressive (SVAR) approach, the study found that even though external shocks are principal sources of macroeconomic fluctuations, domestic factors still exert some reasonable degree of impact. However, the study fails to identity the precise sources of the domestic shocks. Likewise, Genberg (2005) investigates the transmission mechanisms between external shocks and deflation by using VAR model for seven small economies in Asia. The results show that external shocks from the United States have significant effect on inflation and gross domestic product (GDP) in the small economies while shocks emanating from China do not have significant effect.

Mackowiak (2006) examines the nexus among external shocks, U.S. monetary policy, and macroeconomic fluctuations in emerging markets. Using SVAR approach, the study found that external shocks constitute a significant proportion as a source of macroeconomic instabilities in the evolving economies. It also shows that the U.S. monetary policy shocks strongly affect interest rates and the exchange rate in the evolving economies. Inflation and real output in the economies react to the U.S. monetary policy shocks more than the inflation and real output in the U.S. economy. However, the U.S. monetary policy shocks are not imperative for the evolving economies relative to other kinds of external shocks.

Similarly, Raddatz (2008) compares the role of external and internal shocks as sources of macroeconomic fluctuations in selected African countries. The study portrays that the relative importance of external shocks as sources of output instability has risen based on the fact that the variance of output explained by internal factors has decreased coupled with the significant upsurge in the susceptibility of output to external shocks. Also, Andrle et al. (2013) estimate the role of domestic and external shocks in Poland by using trend-cycle VAR model. The results indicate that developments in the euro zone explains about 50% of country’s output and interest rate business cycle variance and about 25% of the variance of inflation. Nizamani et al. (2017) examine the impact of external shocks on macroeconomic variables of Pakistan, using SVAR. The results show that the impact of adverse external shocks is significantly negative on Pakistan economy. External variables are shown to be more important in accounting for the variability in domestic macroeconomic variables. Likewise, Alley and Poloamina (2015) explore the influence of private capital flow shocks on macroeconomic performance in sub-Saharan African countries. Using SVAR model, the results indicate that shocks to inflows of portfolio investment and inflows of bank lending reduce GDP per capita while shocks to inflows of foreign direct investment (FDI) increase GDP.

Meanwhile, Omojolaibi and Egwaikhide (2013) examine the impact of oil price dynamics on the economic performance of five oil-exporting countries in Africa. Using panel VAR technique, the results show that gross investment responds more to oil price volatility than fiscal deficit, real GDP, and money supply. In the same vein, Obi et al. (2016) explore the effects of oil price shock on macroeconomic performance in Nigeria. Utilizing VAR approach, the results indicate that a proportionate change in oil price leads to a greater proportionate change in real exchange rate, interest rate, and GDP in the country. Keji (2018) investigates the nexus between oil price collapse and economic growth in sub-Saharan African oil-based economies. Using panel random effects model, the result shows the existence of a negative relationship between oil price collapse and the economic growth in the case of Angola, Nigeria, and Sudan. The conclusion from all these studies is that external shocks have statistically significant effect on macroeconomic variables.

Conversely, a number of studies found that the same measures of external shocks do not significantly affect macroeconomic variables in developing countries. For instance, Raddatz (2007) examines whether the importance usually credited to external shocks by policymakers is empirically justifiable. Using a panel VAR technique, the results indicate that external shocks merely account for a small proportion of the output variance in the evolving countries. The study observes that internal factors are the major sources of the variations. Similarly, Lorde et al. (2009) uses VAR approach and found that unexpected shock in oil price volatility leads to haphazard swings in Trinidad and Tobago economies. Alley et al. (2014) adopt general methods of moment (GMM) to examine the impact of oil price shocks on the Nigerian economy. The study found that oil price shocks insignificantly retards economic growth while oil price itself significantly improves it. The significant positive effect of oil price on economic growth confirms the conventional wisdom that oil price increase is beneficial to oil-exporting country. Meanwhile, Ekesiobi et al. (2016) investigate the relationship between external shocks and government revenue in Nigeria using error correction model (ECM). The results indicate a long-run relationship between government revenue and external shocks.

Yet, Guillaumont and Chauvet (2001) assess the effect of aid on growth by using ordinary least squares (OLS) technique. The study reveals that the effect is not necessarily positive, but rather a function of the specific conditions in each recipient country. The findings of the study by Matos et al. (2011) suggest that external shocks have negative effect on economic growth. Bermingham and Conefrey (2014) analyze the sensitivity of the Irish economy to an unanticipated external demand shock using a Bayesian VAR model. The results show that 1% increase in the U.S. GDP growth leads to an increase in Irish GDP growth of 1.3% in the model.

Although the influence of external shocks on economic performance has attracted series of debates among scholars, most extant studies in Nigeria focus on the influence of oil price shocks. Olomola and Adejumo (2006) examine the effect of oil price shocks on output, inflation, real exchange rate, and money supply in Nigeria. The study utilizes VAR method and the results reveal that oil price shocks do not affect output and inflation in Nigeria. The result contradicts most findings for other counties in the literature. Also, Aremo et al. (2012) evaluate the effect of oil price shock on fiscal policy in Nigeria by using SVAR method. The results indicate that oil price has significant effect on government expenditure and government revenue in Nigeria. However, these studies, as well as Alley et al. (2014) and Obi et al. (2016), fail to incorporate the influence of other forms of shocks such as interest rate shocks, terms of trade shocks, and foreign aids shocks on macroeconomic performance. For instance, the interest rate was the major factor through which the 2008 global financial crisis affected developing countries generally, and Nigeria, in particular.

Oyelami and Olomola (2016) examine the effect of oil price shocks and macroeconomic shocks from developed trading partners on Nigerian macroeconomic performance. Using global VAR, the results portray that oil price shock has positive effect on real GDP as well as exchange rate in the country whereas inflation and interest rate do not portray instantaneous response to the shocks. The study concludes that Nigerian economy is vulnerable to external shocks. The study appears to be the only exception on Nigeria as it includes growth spill-over and financial shocks from developed countries. Yet, the study does not address the possibility of the quality of domestic institutions as a transmission mechanism through which the country becomes vulnerable to external shocks.

Even when external shocks are established to be significantly affecting macroeconomic performance, the identification of the exact transmission channel remains a great challenge. It is worthy of examination whether instability in macroeconomic performance may be solely attributable to external shocks. Rodrik (1999) asserts that countries experiencing the sharpest drops in GDP are “those with divided societies and weak institutions,” and institutional quality is claimed to be responsible for the cyclical nature of monetary policy and output growth (Duncan, 2011). Institutional quality plays a vital role in absorbing the effects of external shocks on macroeconomic variables. Several studies have emphasized that distortionary macroeconomic policies largely reflect institutional factors. These studies include Acemoglu et al. (2003) which observe that countries that have adopted distortionary macroeconomic policies happen to have experienced more macroeconomic volatility coupled with slower economic growth in the post-war era. The study, also, points out that countries with poor macroeconomic policies have weak institutions. Tello et al. (2005) query the results found by Acemoglu et al. (2003) which lay emphasis on the distortionary macroeconomic policies as portraying the institutional environment as being the foremost source of volatility. Using panel OLS and panel GMM, the study found similar result when the global sample of 115 countries are utilized.

Furthermore, Efendic et al. (2010) explore the relationship between institutional improvement and economic performance in transition countries (TCs) and found that institutions play significant role in explaining economic performances in TCs. Meanwhile, Ushie et al. (2013) examine the sensitivity of major macroeconomic variables to oil revenue shocks in Nigeria, using VAR approach with the inclusion of an institutional quality variable. The results show that fluctuations in oil revenues lead to hike in inflation, decreased output growth, and real exchange rate appreciation in Nigeria. The study found the institutional variable to be significant. Udah and Ayara (2014) explore the nexus among institutions, governance, and economic performance in Nigeria. The study adopts OLS technique and factor analysis. The results reveal that effective governance and institutions are of utmost importance for enhancing economic performance. The study by Ubi and Udah (2014) also shows that corruption and institutional quality have significant influence on economic performance in Nigeria.

Similarly, Iyoboyi et al. (2016) investigate the impact of institutional setting on industrialization in Nigeria. Using co-integration technique, the study found a long-run relationship between industrialization and associated variables. Quality of service delivery has significant direct impact on industrialization in both short run and long run. These studies maintain that countries deprived of qualitative institutional settings found it impossible to maintain orderliness in an economy, giving room for the economic agents to extort the economy, and hence, distortionary macroeconomic policies.

Nevertheless, some studies do not find significant relationship, or even found negative relationship, between the quality of institutions and macroeconomic performance. Thus, Sala-i-Martin and Subramanian (2003) maintain that natural resources, noticeably oil and minerals, exert an adverse as well as non-linear influence on growth through their harmful influence on the quality of institutions in Nigeria. The results reveal that waste coupled with corruption from oil is responsible for the country’s abysmal economic performance than the acclaimed “Dutch disease.” Simon and Zlatko (2010) use both OLS and panel fixed effects and found little evidence of a robust link between measures of institutions and economic performance. Asiama and Mobolaji (2011) focus on the influence of openness and quality of institutions on financial development in sub-Sahara Africa. Using dynamic panel data approach, the results reveal that trade and financial openness boost financial development, which metamorphoses to expansion in economic growth. Also, the institutional quality has significant negative effect on financial development in the region.

Iyoboyi and Pedro (2014) utilize VECM to investigate the effect of institutional quality on macroeconomic performance in Nigeria, and the result indicates that one standard deviation innovation on institutional quality leads to a decline in macroeconomic performance throughout the horizons, whereas the results of the variance decomposition reveal that a larger proportion of the variations in macroeconomic performance is not ascribed to the fluctuations in its quality of institutional arrangement. However, the study by Whitford and Pozzi (2014) which uses panel fixed effect least squares regression to explore the influence of institutional quality on macroeconomic volatility shows that higher institutional quality increases economic growth in Latin American countries. Similarly, Adigozalov and Rahimov (2015) found that the quality of institutions accounts for a significant role in carrying out counter-cyclical macroeconomic policy.

Khalid (2015) gives credence to studies that establish direct relation between trade openness and the quality of institutional setting in an economy. The study found that the effect of trade openness on economic institutions declines considerably. Likewise, Vitola and Senfelde (2015) portray that institutions play an imperative role in enabling technological advancement. Moreover, the study supports the fact that institutions significantly affect socioeconomic performance around the globe. Aynur and Gokalp (2016) reveal that the various measures of institution have direct influence on the macroeconomic performance of the developing countries.

The existing studies in Nigeria that even addressed some macroeconomic variables’ responses to oil price fluctuations rarely paved attention to the institutional settings, with the exemption of the studies by Sala-i-Martin and Subramanian (2003), and Ushie et al. (2013). However, these studies’ measurements of institutional quality are at variant with the standard measurements of the concept, and these do not properly portray the features of the Nigerian institutional structures. This present study overcomes these pitfalls by utilizing a measure of law and order, government stability, democratic accountability, bureaucratic quality, and corruption.

The conceptual framework depicted in Figure 1 illustrates how external shocks from world influential economies may affect economic activities in the less developed countries of the world. Thus, Nigerian macroeconomic variables are depicted to be influenced by two different factors. The global factors have direct influences on Nigerian macroeconomic variables through trade and price transmission channels while they have indirect influences through their influences on domestic institutional quality measures which, in turn, exert significant influences on the Nigerian macroeconomic variables. Second, there exist domestic factors (institutional quality measures) that influence and are also influenced by the domestic macroeconomic variables. These domestic factors are influenced by external factors while the reverse is not the case. That is, the external factors are exogenous to the domestic economy.

Relationships among external shocks, institutional quality, and macroeconomic performance.

Method

Model Specification

Based on the discussed framework, the implicit functional model for this study is stated thus:

where

Attention is given to GDP and inflation out of the five measures of macroeconomic performance by incorporating each of them into the estimated models, one after the other, along with all the measures of external shocks and the institutional quality component. However, this study takes after Kaldaru and Parts (2008) by using principal components analysis (PCA) to group the institutional quality measures into one component (INQ). The result of the PCA for constructing INQ is reported in Supplemental Appendix 1. Hence, Equation 1 invariably becomes

In the course of the analyses, the variables that already appear in their rate form are utilized directly (INF, TOT, INQ) while the logarithmic form of the remaining variables are utilized. This is in line with Iyoboyi and Pedro (2014) which transform RGDP, government expenditure, and money into the logarithmic form while the nominal form of institutional capacity is incorporated into the estimated models.

Estimation Method

This study considers the Nigerian economy to be a small economy compared with the global economy which is being represented by the U.S. economy. Therefore, the identifying restrictions for the external factors are taken to be contemporaneously exogenous to the domestic variables, and this justifies the suitability of the use of the SVAR technique in this study. Meanwhile, several studies (Adigozalov & Rahimov, 2015; Alley & Poloamina, 2015) have adopted the SVAR approach as a tool of investigating shocks transmission among variables and provide information on impulse response functions along with forecast error variance decomposition (FEVD). The major strength of this technique lies in its ability to capture feedback, shock transmission on variables, and dynamic relationships among macroeconomic variables in an economy (Udoh, 2009). Hence, this study focuses on how external shocks may transmit through institutional quality to macroeconomic performance (GDP and inflation rate) in Nigeria. Accordingly, the study considers seven endogenous economic time series at p lags. The endogenous linear equations are explicitly specified thus:

where

This is arrived at from Equation 2; and

The

For instance,

and shocks

Description and Measurement of Variables

Macroeconomic performance

In the course of analysis, GDP and inflation rate are basically considered as measures of macroeconomic performance, although PCA is used to group the five domestic macroeconomic variables into one component denoted as DMEV.

GDP

The real GDP is one of the measures of macroeconomic performance. This is an inflation-adjusted measure that reflects the value of all commodities produced in a country at a given year, and expressed in base-year prices (Leykun & Sharma, 2017).

Inflation rate

This indicator is the periodic percentage increase in the cost of living as measured expressed by the value of the consumer price index. It is one of the indicators considered by the authorities to set monetary policy.

External shocks

Five different variables are considered in this case.

Foreign GDP

This is utilized as a measure of external real economic activity.

Foreign interest rate

The 3-month inter-bank rate minus the average inflation rate of the United States is considered here. As Nigeria is fond of taking foreign loans coupled with its reliance on foreign capital, it is susceptible to the fluctuations in the international credit circumstances. Also, the high level of importation makes it very dependent on changes in foreign financial situation.

Oil price

This is one of the least endogenous as it is subjected to the impulses of external oil market cum exogenous economic conditions as Nigeria is just a price taker.

Foreign aid

This refers to economic or military assistance offered by one nation to another, or transfer of commodities (both final and intermediate) from one country to another with the aim of improving the standard of living in the recipient country. However, some aids may be given for political reason such as preserving peace.

Terms of trade

This is the ratio of the price of exports to the price of imports.

Institutional quality

The five institutional indexes extracted from the International Country Risk Guide (ICRG) database are considered as measures of INQ. It is believed that qualitative institutions engender income levels, and that citizens from developed countries have the tendency to prefer adequate qualitative institutions.

Scope and Sources of Data

The study covers the period between 1986 and 2016. This spans the period in which Nigeria adopts series of economic policies in its attempts to stabilize the economy. This study makes use of quarterly secondary data for all the variables. While data on the five measures of institutional quality (LAWO, BURQ, DEMA, CORR, and GOVS) are extracted from the ICRG database, data on all the remaining variables are sourced from the IMF’s International Financial Statistics (IFS) database. It should be noted that the data on the five variables extracted from the ICRG are originally on different scales. Specifically, BURQ is on the scale of 0 to 4, GOVS is on the scale of 0 to 12, while LAWO, DEMA, and CORR are on the scale of 0 to 6. Hence, to have uniform scale for all the five measures of institutional quality, the data extracted from the ICRG are rescaled from 0 to 10.

Estimated Results

Descriptive Statistics of Data Series

The descriptive statistics of the data used are considered based on its ability to overcome the problem of multi-collinearity among the explanatory variables which is capable of rendering regression result to be biased (Agun, 2009). The descriptive statistics of data series provides information about the sample statistics as reported in Supplemental Appendix 3. All the data are in their quarterly form and they range from 1986Q1 to 2016Q4. The descriptive statistics indicates that all the series display a high level of consistency as their mean and median values lie between the maximum and the minimum values of the series. However, the standard deviation values reveal that the data of some of the variables (LNGDP, LNFGDP, and LNFAID) are really different from their mean values while the standard deviation values of the remaining variables are not really different from their mean values. The standard deviation result further shows that LNFGDP and LNGDP are the most widely dispersed series (0.23 and 0.51) from their means of 30.13 and 26.04, respectively, while TOT and DMEV are the least dispersed series (0.46 and 1.55) from their respective means of 1.54 and 3.42E-15 of all the variables.

The skewness and the kurtosis statistics provide vital information concerning the symmetry of the probability distribution of various data series and the thickness of the tails of these distributions, respectively (Akinlo, 2012). Both statistics are imperative as they are utilized in the computation of the Jarque–Bera statistic which, in turn, is employed in testing for the normality or the asymptotic property of a particular series. The Skewness statistic suggests that four of the variables are negatively skewed while eight are positively skewed. Also, all the variables are normally distributed as the value of the Kurtosis is lower than that of the Jarque–Bera statistic. The normality assumption is further supported by the closeness of the mean and the median values for the data series. The closer the mean and the median values of data series, the greater the probability that such series will be normally distributed.

Optimal Lag Length Selection and Stability of SVAR Models

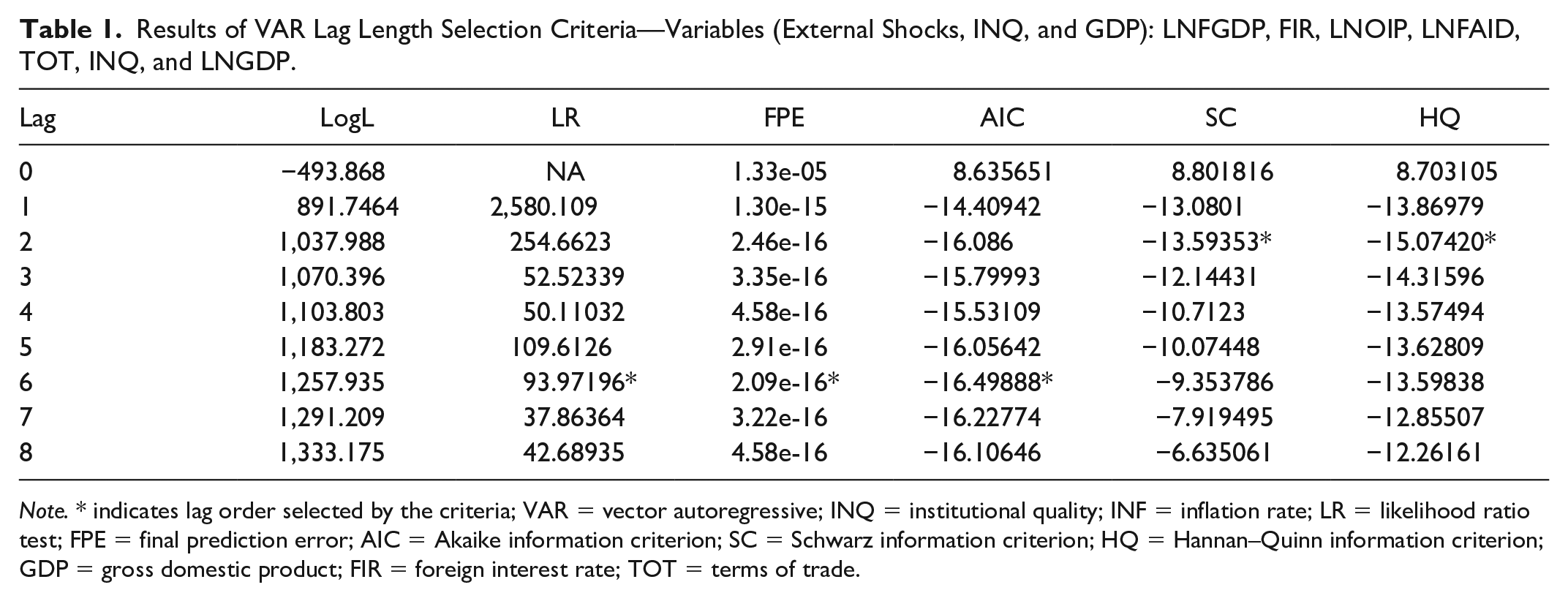

The theoretical elucidation of VAR approach rests on the inherent assumption that the lag order is known (Hamilton, 1994). Conversely, empirical evidence has shown that the optimal lag order is usually unknown, hence, its determination is vital. Tables 1 and 2 captures the results of lag selection for variables in the estimated SVAR models and the results of the tests suggest two diverse optimal lag lengths. While likelihood ratio test statistic (LR), final prediction error (FPE), and Akaike information criterion (AIC) suggest a lag length of six, Schwarz information criterion (SC) and Hannan–Quinn information criterion (HQ) suggest a lag length of two.

Results of VAR Lag Length Selection Criteria—Variables (External Shocks, INQ, and GDP): LNFGDP, FIR, LNOIP, LNFAID, TOT, INQ, and LNGDP.

Note. * indicates lag order selected by the criteria; VAR = vector autoregressive; INQ = institutional quality; INF = inflation rate; LR = likelihood ratio test; FPE = final prediction error; AIC = Akaike information criterion; SC = Schwarz information criterion; HQ = Hannan–Quinn information criterion; GDP = gross domestic product; FIR = foreign interest rate; TOT = terms of trade.

Results of VAR Lag Length Selection Criteria—Variables (External Shocks, INQ, and INF): LNFGDP, FIR, LNOIP, LNFAID, TOT, INQ, and INF.

Note. VAR = vector autoregressive; INQ = institutional quality; INF = inflation rate; LR = likelihood ratio test; FPE = final prediction error; AIC = Akaike information criterion; SC = Schwarz information criterion; HQ = Hannan–Quinn information criterion; GDP = gross domestic product; FIR = foreign interest rate; TOT = terms of trade.

As a result of the conflict in the choice of the optimal lag length chosen by the five criteria, stability test is carried out on the two selected optimal lag lengths through Autoregressive (AR) roots table and graph. Based on the results in Supplemental Appendices 5 to 7 (although AR roots tables are not reported), the suggested lag length of six is discarded while the lag length of two suggested by SC and HQ is adopted as the optimal lag length in this study as all their roots have modulus less than one and their dots fall within the unit circle. The results of the AR root stability test satisfy the stability condition of the estimated SVAR models.

In an attempt to test the validity, or otherwise, of the lag length selection results, this study carries out lag exclusion Wald test for each of the estimated SVAR models to authenticate the suitability of two lags. The results of the chi-square test (χ2) statistic reported in Tables 3 and 4 for the joint significance of all the endogenous variables in each of the estimated models with two lag lengths are jointly significant at 5% level. This buttresses the earlier assertion that the selected lag length of two is optimal.

Results of VAR Lag Exclusion Wald Tests of Endogenous Variables for the GDP Model.

Note. Numbers in [ ] are p values. VAR = vector autoregressive; FIR = foreign interest rate; TOT = terms of trade; INQ = institutional quality.

indicates statistically significant at 5% level.

Results of VAR Lag Exclusion Wald Tests of Endogenous Variables for the Inflation Model.

Note. Numbers in [ ] are p values. VAR = vector autoregressive; FIR = foreign interest rate; TOT = terms of trade; INQ = institutional quality.

indicates statistically significant at 5% level.

Unit Root Test Results

The literature has recognized the fact that most time-series data are non-stationary at levels because some variables tend to be either too small or too large to the extent that their probability of returning to their expected mean is almost equal to zero. This scenario, thus, necessitates the importance of carrying out unit root test or stationarity test at whatever time that a researcher is working on time-series data. In this present study, to test for the stationarity of the variables utilized, this study adopts both the Augmented Dickey–Fuller (ADF) test (Dickey & Fuller, 1981) and the Phillip–Perron (PP) test (Phillips & Perron, 1988) with intercept as well as with intercept and linear trend (Spiru & Qin, 2016). The results for both the ADF and the PP tests are as presented in Supplemental Appendix 4. The decision rule adopted here is that whenever the absolute value of the ADF test or that of the PP test is lower than the 5% critical value, the variable in question is said to be non-stationary. If, on the contrary, the absolute value of the ADF test or that of the PP test is greater than the 5% critical value, then the variable in question is said to be stationary. Alternatively, if the probability value of the ADF test or that of the PP test is significant at 5% level of significance, the variable in question is said to be stationary, and vice versa.

The ADF test result indicates that all the variables are stationary in their level form, that is, I(0), when tested with intercept alone as well as when tested with intercept and linear trend. Similarly, the PP test indicates that all the variables, except inflation rate, are stationary in their level form when tested with intercept alone at 5% level of significance. However, the PP test indicates that oil price and terms of trade are stationary at 10% level of significance when tested with intercept and linear trend. Based on the ADF test result and the PP test result when tested with intercept alone, this study concludes that all the variables are stationary in their level form, that is, I(0).

Meanwhile, the SVAR model is usually estimated in level irrespective of the stationarity condition of the variables. Studies by Sims et al. (1990), Hamilton (1994), and Guay and Pelgrin (2007) have established that the estimated coefficients of the VAR model consisting of non-stationary variables are consistent and that the asymptotic distribution of individual estimated parameters is standard, that is, a normal distribution. Hence, the studies state that a VAR can be estimated with non-stationary variables in level and that the resultant impulse responses in both the short run and the medium run are reliable estimators of the true impulse responses. Sims et al. (1990) and Guay and Pelgrin (2007) maintain that the result also holds for co-integrated variables as the VAR in level takes implicit account of the co-integrated relationships.

Impulse Response of Structural VAR Results

It has been established in the literature that there is no evidence of bias in the estimated impulse response functions when short-run restriction is used and that SVAR performs well with short-run restriction (Christiano et al., 2006). Similarly, Lutkepohl et al. (2018) suggest that the utilization of short-run identifying restrictions is preferable while the impulse responses of SVAR on the basis of long-run identifying restrictions may not be very accurate. Hence, this study adopts the short-run restriction in the estimated SVAR models. Blanchard and Perotti (1999) assert that the solid line depicts the point estimates while the broken lines depict one standard deviation bands computed by Monte Carlo simulations based on normality assumption. Thus, the “dashed lines” denote the intervals of two standard deviations whereas the “solid lines” signify the impulse function. The focus of this study is to determine the relative contributions of external shocks and institutional quality to macroeconomic performance in Nigeria. This is captured in Figure 2 to 4 along with Tables 5 to 7.

Response to structural one SD innovations in GDP to external shocks and INQ.

Response to structural one SD innovations in inflation rate to external shocks and INQ.

Response to structural one SD innovations in DMEV to external shocks and INQ.

Results of Variance Decomposition With Structural Factorization: Variance Decomposition of GDP to External Shocks and INQ.

Note. GDP = gross domestic product; INQ = institutional quality; FIR = foreign interest rate; TOT = terms of trade.

The impulse response result in Figure 2 indicates how GDP responds to external shocks measures and institutional quality. The result shows that GDP responds positively to shock in foreign GDP in all the time horizons. It is obvious that foreign GDP has positive but marginal effect on GDP in Nigeria—as the effect is in the performance range of 0.002% and 0.005% throughout the entire horizons. Specifically, one standard deviation shock in foreign GDP triggers domestic GDP to rise to 0.0029% in the first period and this slightly increases to its maximum of 0.005% in the fifth period but successively decreases marginally to 0.0027% and 0.0022% in the 10th and 16th periods, respectively. This result conforms with the findings of Genberg (2005) and Bermingham and Conefrey (2014) that an increase in foreign GDP leads to increase in the domestic output and of Hassan et al. (2017) that developing economies are interconnected to worldwide economy through real output.

The result further shows that domestic GDP responds negatively to shock in foreign interest rate throughout the horizons. One standard deviation shock in foreign interest rate causes GDP to decrease from −0.003% in the first period to −0.011% and −0.015% in the 10th and 16th periods, respectively. It reveals that GDP responds positively to shock in each of oil price and terms of trade throughout the horizons. Specifically, one standard deviation shock in oil price influences GDP to increase slightly from 0.0015% in the first period to 0.012% in the 16th period. This result fits in with the findings of Cologni and Manera (2008) and Alley et al. (2014) that oil price shock has significant effect on economic growth. The result is close to the claim by Tang et al. (2010) and IMF (2015) that decline in oil price stimulates investment which, consequentially, reinforces growth prospect in the small nations.

Similarly, one standard deviation shock in terms of trade causes GDP to increase slightly from 0.0010% in the first period to 0.0029% in the 16th period. This is in line with the studies by Dorsainvil (2011) and Alvarez and De-Gregorio (2014) which found that high terms of trade significantly affect economic performance. The effect of foreign aid shock on GDP is negative in the short term. This negative effect vanishes after the first four periods as the effect turns positive as from the fifth period all through the longer horizons. However, GDP reacts negatively to the institutional quality shock throughout the horizons even though the effect is marginal as it ranges between −0.0019% and −0.0008%. These results seem to buttress the claim of Whitford and Pozzi (2014) that foreign aid only improves economic performance in countries with good institutions.

The impulse response result in Figure 3 indicates the responses of inflation rate to external shocks and institutional quality. The result shows that inflation rate responds negatively to shock in foreign GDP in all the horizons. It is evident that foreign GDP has negative but stable effect on inflation rate in Nigeria—as the effect is in the performance range of −0.014% and −0.127% throughout the entire horizons. Precisely, one standard deviation shock in foreign GDP causes inflation rate to decrease to −0.014% in the first period, and this decreases marginally to −0.11% and −0.13% in the 10th and 16th periods, respectively. This result is consistent with a priori expectation in that global output growth is expected to result in decrease in the general price level across economies of the world. This is premised on the fact that expansion in the global output enhances healthy competitions which culminate in declined prices. This result is, however, inconsistent with that of Di-Maio (2012) that the changing patterns of global output growth leads to increase in the price level.

Moreover, the result shows that inflation rate responds negatively to shock in foreign interest rate in almost all the horizons. One standard deviation shock in foreign interest rate influences inflation rate to decrease to −0.03% in the first period but the effect temporarily turns to positive from the second period to the fifth period, reaching its peak of 0.049% in the third period. Subsequently, foreign interest rate causes inflation rate to decrease to −0.28% and −0.44% in the 10th and 16th periods, respectively. This result is in conformity with the previous studies (Hull & Imai, 2012; Mackowiak, 2006) which found that the U.S. monetary policy shocks have significant effect on the interest rate along with the price level of the developing economies.

The result further portrays that inflation rate responds positively to shock in each of oil price and terms of trade throughout the horizons. Specifically, one standard deviation shock in oil price influences inflation rate to increase slightly from 0.03% in the first period to 0.74% in the 16th period. This result toes the line of the study by Cunado and Perez-de-Gracia (2003) which found that oil price has marginal effect on macroeconomic performance, and that of Jimenez-Rodriguez and Sanchez (2010), Tang et al. (2010), and Ushie et al. (2013) which found that oil price has positive effect on inflation rate. This result, however, seems to contradict the findings by Olomola and Adejumo (2006) that oil price shocks do not affect inflation in Nigeria; by IMF (2015) that the recent decline in the oil price would give room for the small nations to maintain low inflation; and by Oyelami and Olomola (2016) that oil price shocks do not have instantaneous influence on inflation. Likewise, one standard deviation shock in terms of trade causes inflation rate to increase slightly from 0.02% in the first period to 0.57% in the 16th period.

The effect of foreign aid shock on inflation rate is positive in the short run. This positive effect vanishes after the first four periods as the effect turns negative as from the fifth period all through the longer horizons. This result seems to be unexpected in Nigeria given the fact that larger proportion of the aids received are not channeled into the real sector of the economy. Foreign aids are observed to be mostly abused by the successive governments in the country, and this invariably worsens inflation. However, inflation rate reacts negatively to the institutional quality shock in the first two periods, after which it turns positive, although with moderately stable effect throughout the remaining horizons as it ranges between 0.014% and 0.95%.

Finally, the impulse response result in Figure 4 summarizes the responses of the grouped domestic macroeconomic variables (DMEV) to external shocks measures and institutional quality. The study employs PCA to group the various domestic macroeconomic variables into one component denoted as DMEV (see Supplemental Appendix 2). This is to enhance cursory observation of the response of macroeconomic performance in Nigeria to external shocks and institutional quality. The result shows that the grouped DMEV responds positively to shock in foreign GDP throughout the horizons, with the effect ranging between 0.018% and 0.041%. Thus, foreign GDP has a stable and positive effect on the macroeconomic performance in Nigeria.

The result further shows that DMEV responds negatively to shock in foreign interest rate throughout the horizons while it responds positively to shock in oil price. Meanwhile, DMEV responds positively to shock in foreign aid in the first six periods while it responds negatively in the latter horizons. Also, DMEV responds positively to shock in terms of trade in the first period only while it responds negatively in the subsequent horizons. In addition, DMEV responds positively to the institutional quality shock throughout the horizons as it ranges between 0.02% and 0.03%. This result is close to the findings of Seputiene (2009) that high institutional quality plays significant role in determining the level of investment in an economy.

Variance Decomposition of Structural VAR Results

The FEVD usually depicts the percentage of forecast error in a variable that is attributable to its own shock as well as shocks in other variables in the model. The recursive cause order utilized in the computation of impulse response is maintained in this case. However, while the impulse response functions trace the effects of a shock in one endogenous variable to the other variables, the FEVD separates the variation in an endogenous variable into the component shocks in the SVAR model. Hence, the FEVD provides information about the relative importance of each random innovation that affects the variables in the SVAR model (Pfaff & Taunus, 2008). Tables 5 to 7 portray the report of forecast error variance of each variable accounted for by the innovations to the structural equation. The study adopts forecast horizons of 1, 2, 10, 16 ahead to analyze the forecast error variance for each variable that is ascribable to its own shock as well as to shocks in the other variables in the model. It is worthy of note that variable’s own shock contributes more than any other shock to its own forecast error variance and the results in Tables 5 to 7 conform to this postulate.

The results portray the report of forecast error variance of each variable accounted for by the innovations to the structural equations. Table 5 reveals that GDP’s own shock is responsible for approximately 91% of its forecast error variance in the first period and this slightly increases to its peak of 91.2% in the second period before its influence gradually decreases in the longer horizons as it accounts for about 58.1% in the 16th period. This same pattern is replicated in Tables 6 and 7 for inflation and the grouped domestic macroeconomic variables component (DMEV).

Results of Variance Decomposition With Structural Factorization: Variance Decomposition of Inflation Rate to External Shocks and INQ.

Note. INQ = institutional quality; FIR = foreign interest rate; TOT = terms of trade; INF = inflation rate.

Results of Variance Decomposition With Structural Factorization: Variance Decomposition of DMEV to External Shocks and INQ.

Note. DMEV = domestic macroeconomic variables; INQ = institutional quality; FIR = foreign interest rate; TOT = terms of trade.

Table 5 further shows that foreign GDP is temporarily dominant in the forecast error variance of GDP in the first three periods while oil price becomes dominant as from the fourth period all through the remaining horizons. Oil price accounts for barely 0.92% in the first period, but its contribution increases considerably in the longer horizons as it accounts for about 14.65% and 18.48% in the 10th and 16th periods, respectively. Thus, oil price is dominant in the forecast error variance of GDP in most of the periods. Foreign GDP accounts for about 3.43% in the first period but its contribution decreases slightly in the longer horizons as it accounts for about 2.74% and 1.95% in the 10th and 16th periods, respectively. Foreign interest rate accounts for about 2.65% in the first period but its contribution decreases slightly to its trough of 1.32% in the third period before it begins to increase steadily in the subsequent horizons as it accounts for about 5.38% and 14.99% in the 10th and 16th periods, respectively. Thus, oil price and foreign interest rate account for significant percentage of GDP forecast error variance in all the periods.

Furthermore, foreign aid accounts for less than 1% in the first eight periods even though its contribution increases all through the horizons. Specifically, foreign aid accounts for barely 0.16% of the forecast error variance in GDP in the first period but its influence increases slightly in the longer horizons as it accounts for about 1.55% and 3.35% in the 10th and 16th periods, respectively. Similarly, terms of trade accounts for barely 0.39% of the forecast error variance in GDP in the first period but its contribution increases slightly between the second and the 10th periods before it decreases marginally in the longer horizons as it accounts for about 2.58% and 2.40% in the 10th and 16th periods, respectively.

Institutional quality accounts for about 1.54% of the forecast error variance in GDP in the first period and its contribution increases temporarily to its peak of about 2.01% in the third period before it decreases slightly in the longer horizons as it accounts for about 1.12% and 0.75% in the 10th and 16th periods, respectively. The results in Table 5 imply the dominance of external shocks over institutional quality on economic performance (measured by GDP) in Nigeria. Meanwhile, the fact that the contribution of institutional quality decreases in the longer horizons coupled with the impulse response function result that institutional quality has negative effect on economic performance portrays that institutional quality has the tendency to affect positively on economic performance in the long run. A result of this kind is in conformity with the submissions of Genberg (2003) and Iyoboyi and Pedro (2014) that the effects of external factors are dominant on macroeconomic performance; and of Simon and Zlatko (2010) that marginal relationship exists between institutional quality and macroeconomic performance. The result is, however, at variant with the results of Efendic et al. (2010) and Alexiou et al. (2014) that institutions matter in explaining economic performance.

Table 6 shows that foreign aid is temporarily dominant in the forecast error variance of inflation rate in the first period while oil price becomes dominant as from the second period all through the remaining horizons. Oil price accounts for barely 0.61% in the first period, but its contribution increases substantially as from the second period all through the longer horizons as it accounts for about 2.97%, 18.370%, and 18.373% in the second, 10th and 16th periods, respectively. This result appears to be consistent with the realities in the economic environment of Nigeria. The result is, however, contrary to the submission of Olomola and Adejumo (2006) that oil price shocks do not affect inflation in Nigeria.

Although institutional quality accounts for negligible proportion of the forecast error variance of inflation rate in the first four periods, its contribution increases considerably in the subsequent horizons. It becomes the second most dominant, after oil price, between the ninth and the 13th periods and it even becomes the most dominant as from the 14th period all through the remaining horizons. Specifically, institutional quality accounts for barely 0.77% in the first period but its contribution increases noticeably as from the fifth period all through the longer horizons as it accounts for about 11.29% and 21.07% in the 10th and 16th periods, respectively. Thus, oil price and institutional quality jointly account for significant share of inflation rate forecast error variance in all the periods.

Furthermore, foreign GDP accounts for just 0.13% of the forecast error variance of inflation rate in the first period but its contribution increases temporarily as it attains its peak of 1.77% in the fourth period before it decreases slightly in the subsequent period all through the longer horizons as it accounts for about 1.0% and 0.73% in the 10th and 16th periods, respectively. Foreign interest rate accounts for barely 0.67% in the first period but its contribution oscillates between 0.26% and 0.70% from the second period to the eighth period before it begins to increase gradually in the subsequent horizon as it accounts for about 1.86% and 4.59% in the 10th and 16th periods, respectively. Although foreign aid is the most dominant in the forecast error variance of inflation rate in the first period, its influence gradually decreases as from the second period until it gets to its trough of barely 0.87% in the fifth period before it begins to rise in the subsequent period all through the longer horizons as it accounts for about 2.69% and 3.97% in the 10th and 16th periods, respectively.

Similarly, terms of trade accounts for just 0.30% of the forecast error variance in inflation rate in the first period but its influence gradually increases in the longer horizons as it accounts for about 5.53% and 8.32% in the 10th and 16th periods, respectively. The results in Table 6 imply that both external shocks and institutional quality are important in influencing the inflation rate in Nigeria. Thus, instability in macroeconomic performance in Nigeria may not be solely attributable to external shocks. The result corresponds to the discoveries of Efendic et al. (2010) and Alexiou et al. (2014) that improved institutional setting is sine qua non in determining economic performance.

Concisely, Table 7 indicates that both the external shocks measures and the institutional quality substantially account for the forecast error variance of the grouped domestic macroeconomic variables (DMEV) which serves as a measure of macroeconomic performance in Nigeria throughout the horizons. Specifically, foreign GDP is responsible for about 2.95% of the forecast error variance in DMEV in the first period and its influence increases slightly in the longer horizons as it accounts for about 3.61% and 5.55% in the 10th and 16th periods, respectively. Also, foreign interest rate accounts for about 2.13% of the forecast error variance in DMEV in the first period and its influence increases marginally in the longer horizons as it accounts for about 4.20% and 5.36% in the 10th and 16th periods, respectively.

Even though the contribution of oil price to the forecast error variance in DMEV is marginal in the short span as it contributes less than 1% in the first five periods, its contribution increases noticeably in the longer horizons as it accounts for about 3.53% and 5.39% in the 10th and 16th periods, respectively. Moreover, foreign aid appears to be the most dominant contributor to the forecast error variance in DMEV in nearly all the periods as it accounts for about 5.77%, 4.29%, and 9.22% in the first, 10th, and 16th periods, respectively. Terms of trade contributes less than 1% to the forecast error variance in DMEV in the first three periods, but its influence increases marginally from the next period until it reaches its peak of 3.17% in the eighth period. It then decreases slightly in the longer horizons as it accounts for about 2.98% and 2.38% in the 10th and 16th periods, respectively. Besides, institutional quality contributes relatively stable proportion to the forecast error variance in DMEV throughout the horizons as it accounts for about 4.34%, 5.71%, 5.84%, and 5.82% in the first, fourth, 10th, and 16th periods, respectively.

Conclusion

The study examines the relative contributions of external shocks and institutional quality to macroeconomic performance in Nigeria, using the SVAR approach. The study finds that oil price dominates the forecast error variances of GDP and inflation rate in most of the time horizons—portraying the possibilities of imported inflation in Nigeria. These reveal the dominance of the contributions of external shocks to domestic macroeconomic variables. Meanwhile, both external shocks and institutional quality substantially account for the forecast error variance of the grouped domestic macroeconomic variables (DMEV) which serves as a measure of macroeconomic performance in Nigeria throughout the horizons. Foreign aid happens to be the most dominant contributor to the forecast error variance in DMEV in most of the periods while institutional quality contributes relatively stable proportion to the forecast error variance in DMEV throughout the horizons. The study concludes that even though the contribution of external shocks to macroeconomic performance is higher than that of institutional quality, both external shocks and institutional quality play significant roles.

Policy Recommendations

As a result of the dominance of the contributions of external shocks to macroeconomic performance, all hands have to be put on deck to ensure the commitments of Nigerians to good governance which is essential for improved institutions. Weak institutional quality coupled with inappropriate economic policies in the country worsens the vulnerability of the economy to external shocks. Hence, there is need for setting up appropriate policies to coordinate the responses of macroeconomic variables in the country. This will serve as incentive to innovations and new investments in the economy. The development of investors’ confidence is fundamental to the private sector advancement.

Also, based on the dominance of the oil price in the forecast error variances of GDP and inflation rate, this study recommends diversification of the economy and setting up quality control measures on domestically produced commodities. These will enhance the country to get over the common problems associated with the mono-economy. Subsequently, the study encourages the policymakers to promote favorable institutional environments as a means of effectively absorbing the influence of external shocks which are exogenous to the Nigerian economy.

Supplemental Material

Online_Appendix – Supplemental material for External Shocks, Institutional Quality, and Macroeconomic Performance in Nigeria

Supplemental material, Online_Appendix for External Shocks, Institutional Quality, and Macroeconomic Performance in Nigeria by S. S. Abere and T. O. Akinbobola in SAGE Open

Footnotes

Author Note

S. S. Abere is now affiliated to Ajayi Crowther University, Oyo, Oyo State, Nigeria.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplementary Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.