Abstract

The outbreak has created an unprecedented crisis that influences macroeconomic variables. These circumstances are predicted to be contagious for banking performance. To understand the related influences, this study attempts to examine the asymmetric relationship between macroeconomic variables and non-performing loans/financing of the Indonesian banking industry before and during the COVID-19 pandemic. The nonlinear autoregressive distributed lag (NARDL) is adopted based on the time-series data from 2005Q1 to 2021Q1. The study provides evidence that an asymmetric relationship between macroeconomic variables and the banks’ non-performing loans/financing exists both before and during the pandemic. In addition, asymmetric relationships of macroeconomic variables on Islamic banks are more prominent before the pandemic even though it occurs inversely during the pandemic. As for policy implication, the financial authority needs to be prudent in implementing financial policies due to the presence of an asymmetric relationship between macroeconomic variables and the banks’ non-performing loans/financing. Moreover, the authority must ensure that all financial policies will be effective to all types of banks regardless of conventional or Islamic banks.

Keywords

Introduction

The COVID-19 pandemic has been influencing world economic condition significantly both in the real economic and financial sectors (Sukharev, 2020). The real economic sector has experienced severe impact from the pandemic especially in the tourism and transportation sectors. Furthermore, the International Monetary Funds (IMF, 2020) announced that the world economy plunged by −3.3%. Similarly, in Indonesia, the impact of the pandemic is inevitable. Data released by the Indonesian Statistic Bureau (2020) reveals that in the first quarter of 2020, Indonesian economic grew by 2.97% but then it plunged to −5.32% and −3.49% in the second and third quarter, respectively, due to the pandemic. All economic sectors in Indonesia had negative growth during 2020 except for agriculture and communication industries. A negative economic growth had a severe impact to the financial sectors particularly the banks due to the increasing non-performing loans (NPLs)/financing (NPF; Rachid et al., 2020). Accordingly, the performance of the banks under current unprecedented crisis matters being the banks’ function as intermediaries and the importance role it has to the economy.

Bearing this in mind, this study aims to examine the presence of asymmetric impact of macroeconomic factors on NPLs/NPF in the Indonesian banking industry, focusing on the period of before and during the COVID-19 pandemic. Indonesia is chosen as the subject of the study because of several reasons. Firstly, Indonesia is the most populous Muslim countries in the world (Trinugroho et al., 2018). The large number of Muslim populations makes the country as one of the largest Islamic retails banking in the world. Moreover, Indonesia practices a dual banking system that comprises of Islamic (non-interest based bank) and conventional (interest based bank) thus provides a broader analysis of the banking industry under the dual banking system (Khattak et al., 2021). The regulation about dual banking system in Indonesia is currently legalized under the National Law No. 21 (2008). Furthermore, the Indonesian banking industry is considered as having a robust banking stability because the industry was able to handle the economic turmoil taken place during the Asian financial crisis of 1997/1998 as well as the global financial crisis of 2008 (Khattak et al., 2021).

The current study is expected to contribute in twofold. First, the study comprehends and enriches the previous empirical studies conducted in the field of banking peformance in relation to financing acvitives. Several studies have been conducted to examine the impact of macroeconomic variables on the quality of banks’ financing reflected by NPLs such as Nkusu (2011) who studied in advanced economic countries, Castro (2013) in GIPSI Countries (Greece, Ireland, Portugal, Spain, and Italy), Chaibi and Ftiti (2015) in cross-countries sample, Gulati et al. (2019) in India, and Messai and Gallali (2019) in Europe. All of the studies find that macroeconomic variable symmetrically impacts the quality of banks’ lending.

During the pandemic, Nicolaides (2020) based on European banking industry and Pratheeesh and Arumugasamy (2020) using Indian banking industry data, find that the COVID-19 pandemic worsens the macroeconomic condition and subsequently increased the number of NPLs in the banking industry. In general, previous empirical studies also conclude that the NPLs can be used as an early warning on the financial stability of a country. Therefore with the information from the NPLs, it can be utilized to assist financial authorities in issuing effective policies to prevent the occurrence of crisis in the financial sectors (Agnello et al., 2012; Agnello & Sousa, 2011).

Secondly, the paper provides a different view to assess the influence of macroeconomic variables on NPLs in the Indonesian banking industry. In contrast to the previous researchers that examine the determinants of NPLs from the symmetric approach, this study examines the analysis from the asymmetric approach. The asymmetric analysis is needed because the impact of macroecomic factors is possibly dynamic. Further, such observation in the Indonesian banking industry remains meagre especially for the studies that utilize the sample period of before and during the pandemic crisis. Hence, this study attempts to answer several questions; (1) What is the influence of macroeconomic variables to the banks’ NPLs/NPF in the period of before and during the pandemic? (2) Is the relationship between macroeconomic variables and the banks’ NPLs/NPF symmetric or asymmetric in the period of before and during the pandemic? (3) What is the impact of the asymmetric relationship of macroeconomic variables to the banks’ NPLs/NPF in the short-run and long-run period? (4) Do Islamic banks better off or worse off compared to their counterparty in the period of before and during the pandemic?

After the introduction, the remaining sections discuss the literature review which will delineate theoretical framework and prior empirical studies. Then it is followed by the explanation of data and method while the results and discussion will be explained in the next section, to be followed with the conclusion and recommendations.

Literature Review

Bernanke and Gertler (1998) state that business cycles determine the condition of loan borrowers. The borrower tends to be pro-cyclical rather than contra-cyclical. It argues that the borrower will be more solvent during the good financial condition but not in the financial turmoil. Moreover, Kiyotaki and Moore (1997) explain that the economic condition affects the credit activities performed by the borrowers and lenders. During unstable financial circumstances, borrowers’ ability to service their loans is uncertain whereas, during a stable and growing economy the ability to service will be higher. In contrast, Bernanke et al. (1998) argue that the credit activities are the one that influences macroeconomic conditions, referring to the 1930s’ great depression experience in which credit market exacerbated the macroeconomic condition at that time. Both arguments show that macroeconomic condition can influence the credit risk but at the same time, NPLs at certain level can also worsen the economic condition.

Empirical evidence documented that NPLs are closely related to the economic and business cycles. Salas and Saurina (2002) reveal that every financial crisis is strongly influenced by macroeconomic factors, such as a decline in economic activities. Furthermore, Salas and Saurina (2002) explain that economic slowdown or negative economic growth causes lower cash flows of firms, such as sales and payment of wages. This causes the firm profit to decline while the household sector is affected by layoffs. This condition makes it difficult for firms and the household sector to pay interest and principal loans to the banks. Thus, the slowdown in economic activities will eventually lead to an increase in NPLs.

Similarly, Grigoli et al. (2018) reveal that economic contraction was associated with an increase in the ratio of NPLs of banks. The economic downturn is generally accompanied by an increase in the number of unemployed which has a negative impact on the ability of borrowers to meet their obligations. On the other hand, good economic growth has enabled the household and firms to maintain smooth debt payment, which is reflected by the higher quality of bank loan portfolios.

Concerns on the weakening of economic activities and the occurrence of credit problems emerged when the spread of the COVID-19 pandemic ravaged financial markets throughout the world (Lucchese & Pianta, 2020). Studies on the impact of the pandemic on banking continue to grow to this day being a new global experience. Despite this, the 2008 global financial crisis can somehow be used as a lesson because the effects are similar (Barua & Barua, 2021). Rizwan et al. (2020) examine the systemic impact on the financial sector due to the COVID-19 pandemic with time-series analysis approach. Their studies provided evidence that economic slowdown due to the COVID-19 pandemic caused financial institutions to experience an increase in NPLs and liquidity risk. The existence of linkages between financial institutions causes the impact to spread and eventually the instability of the financial system as a whole.

A similar study was also conducted by Elnahass et al. (2021) which measures the impact of the pandemic on global banking stability. Their research provides empirical evidence that the COVID-19 outbreak has adversely affected financial performance and bank stability as measured by default risk, asset risk, and liquidity risk. Laing (2020) revealed that COVID-19 has the potential to badly affected the business sector, industry and the economy as a whole. Further, the economic slowdown due to the pandemic is predicted to cause the failure in the private sector debt repayment. According to the OECD, the world’s private companies have a very large debt amounting to 13.5 trillion US dollars (Goodman, 2020).

More specifically, Hardiyanti and Aziz (2021) examine the impact of the spread of COVID-19 on credit risk as measured by NPLs in Indonesia. Their findings revealed that the virus outbreak was an external factor that caused the debtor’s business situation to deteriorate. This has resulted in an increase in the number of NPLs at conventional commercial banks in Indonesia. Disemadi and Shaleh (2020) also conduct a study on banking credit restructuring policies as a result of the spread of COVID-19 in Indonesia. The increasingly widespread pandemic in Indonesia affects economic stability and has disrupted the capacity and performance of borrowers to pay their loans. This condition has resulted in the deterioration of bank performance and stability. They also revealed that one of the government’s efforts to minimize credit risk was to implement credit restructuring policy.

Several past studies that measure the impact of the pandemic on banking stability mostly show similar results, the weakening macroeconomic conditions resulted in deteriorating banking stability as reflected in increased NPLs. Thus, there is a significant relationship between macroeconomic variables and credit risk as measured by NPLs. The relationship between macro conditions and NPL has also been revealed by previous studies such as Louzis et al. (2012). They provided evidence that macroeconomic conditions in the form of GDP growth is the main cause of NPLs among Greek banks. The weakening macro conditions will reduce the ability of economic agents to meet their debt obligations, and vice versa. GDP growth as reported has a significant negative effect on NPLs in banking (Carey, 2002; Makri et al., 2014; Männasoo & Mayes, 2009; Messai & Jouini, 2013; Roman & Bilan, 2015; Skarica, 2014; Tanasković & Jandrić, 2015). A similar view is expressed by Quagliariello (2007) that the expansionary phase of economic growth is associated with low level of NPLs, and vice versa.

In addition to the economic growth, another macroeconomic variable that can affect NPLs is inflation (Klein, 2013). Inflation can have both positive as well as negative impacts on NPLs (Chaibi & Ftiti, 2015). The negative effect of inflation on NPLs can be explained in two reasons. The first reason is that a high rate of inflation will reduce the real value of loans. The second reason is that, high inflation is associated with a low unemployment rate as explained by the Philips curve (Castro, 2013). Meanwhile, the positive effect of inflation on NPLs is due to the high inflation rate that will reduce the real income of borrowers, hence reducing the ability to pay debts (Chaibi & Ftiti, 2015). The positive effect of inflation on NPL was also found by Ćurak et al. (2013) and Skarica (2014). Meanwhile, Fajar and Umanto (2017), Bayar (2019), and Roman and Bilan (2015) find a negative influence of inflation on NPLs.

The positive relationship between exchange rate and NPLs was revealed by De Bock and Demyanets (2019) and Klein (2013), who demonstrated that the appreciation of exchange rates results in the price of local products to be higher, thus reducing the competitiveness of export-oriented firms. This situation if prolong, will adversely affect the ability of debt payment service of the firms.

The focus of this study is to examine the effect of macroeconomic conditions on the banking stability of Indonesian banks as measured by NPLs during the COVID-19 pandemic. This study adopts the asymmetric approach in which the observation from this perspective is still currently understudied.

Data and Methodology

The use of asymmetric approach is important to measure how significant is the effect of an increase/decrease in certain independent variables (X) on dependent variable (Y) being the impact may not be symmetric. As explained by Bussiere (2012), in many cases, an increase in certain degree of X variable impacts differently to Y variable compared to a decrease of the same degree of the X variable. Due to this phenomenon, measure by symmetric approach could lead to a bias and misleading results. Hence, asymmetric approach is needed to assess the phenomenon more precisely. The use of asymmetric approach will provide a more accurate understanding on how macroeconomic variables influence the banks’ NPLs in Indonesia.

Moreover, the study uses quarterly data from 2005Q1 to 2021Q1 retrieved from the Indonesian Financial Service Authority, Indonesian Statistics, and Central Bank of Indonesia. In the analysis, the period is separated as before COVID-19 pandemic (2005Q1–2020Q1) and during the COVID-19 pandemic (2020Q2-2021Q1). Generally, the model used in the study is as below,

The explanation of the variables is provided in Table 1 while

The Explanation of the Variables.

Furthermore, as suggested by Shin and Greenwood-Nimmo (2014), to examine the asymmetric effect of the observed variables, nonlinear autoregressive distributed lag (NARDL) was adopted as formulated below,

MACROVAR is macroeconomic variables as explained in Table 1, where the POS (positive) and NEG (negative) of macroeconomic variable values are generated from:

The calculation of the long-run coefficients, which consist of negative and positive results, is

After calculating the value of POS and NEG in the determined variables (Cheah et al., 2017; Haron & Ibrahim, 2019), as explained by Shin and Greenwood-Nimmo (2014), the NARDL method was performed by taking several steps similar to the ARDL test which are (1) the ADF unit root test proposed by Dickey and Fuller (1979) to check the level of stationary, (2) bounds testing co-integration as suggested by Pesaran et al. (2001) to assess the presence of long-run relationship, (3) Wald test as explained by Sriyana and Ge (2019) to determine the symmetric and/or asymmetric movement of the observed variables in which H0 of the Wald test is, if the relationship of the observed variables is symmetric, (4) Bootstrapping analysis to understand the movement of independent variables towards dependent variables during the observation periods, and (5) a cumulative sum (CUSUM) test to examine the robustness of the tested model based on 5% level of significance.

Results and Discussion

Summary of the Data

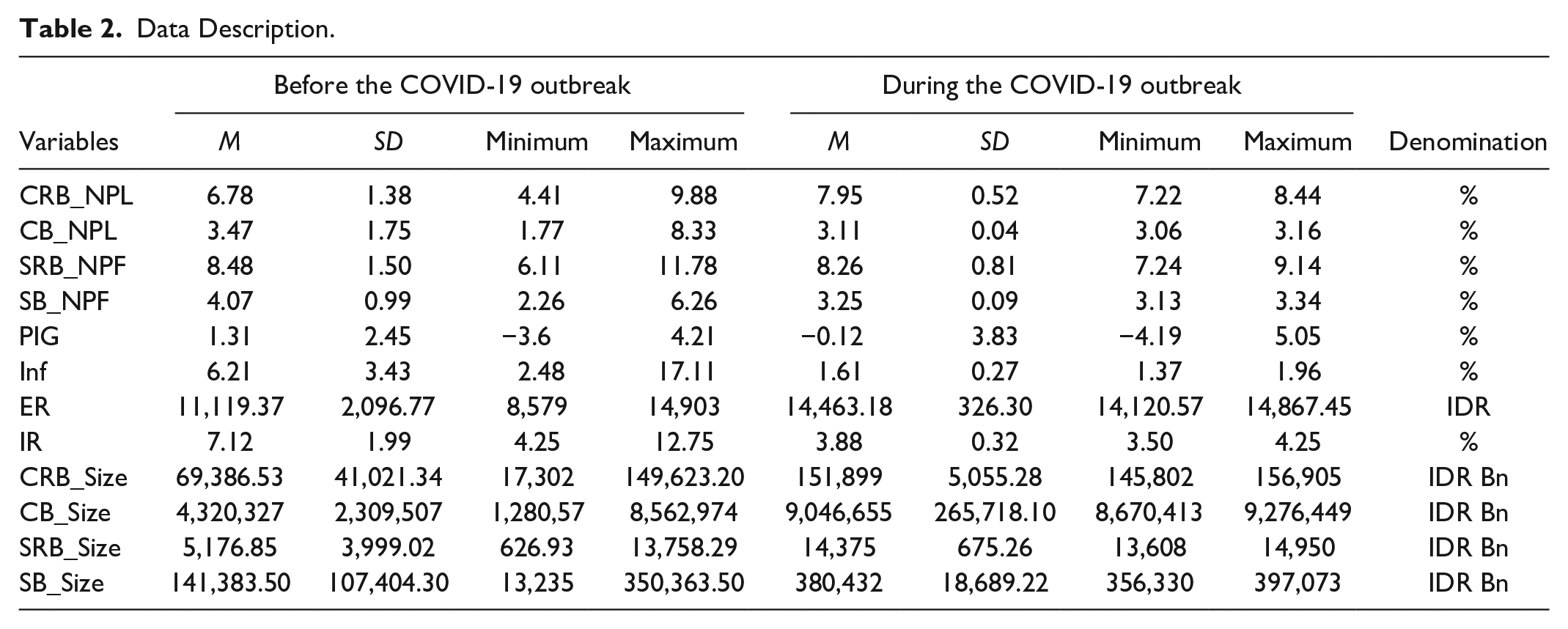

Table 2 presents a description of the data during the observation periods which consists of before (2005Q1–2020Q1) and during (2020Q2–2021Q1) the COVID-19 pandemic. According to the data description, it shows that the mean of NPLs/NPF percentages varies across the banks. Before the pandemic, the value of NPLs/NPF for interest-based banks (conventional rural bank and conventional bank) are lower than the non-interest based banks (Islamic rural bank and Islamic bank). The same situation also occurs during the pandemic. These facts indicate that non-interest based banks are less prudent than their counterparties. In terms of size, both conventional banks and conventional rural banks are accumulatively larger than Islamic or Islamic rural banks in both periods.

Data Description.

In addition, the difference of mean value of variables also exists in the before and during the pandemic periods. The value of inflation and interest rate are lower during the COVID-19 pandemic which reflect lower purchasing power of the society during the pandemic and the attempts by the central bank to stimulate the economic growth with lower interest rate regime. The financial turmoil during the pandemic can also be seen from the negative value of economic growth, on average. In contrast, the exchange rate of Indonesian rupiah to US dollar is higher during the pandemic which means the Indonesian currency is weakening against the US dollar.

Unit Root Test

To perform NARDL analysis, unit root test must first be applied (Shin & Greenwood-Nimmo, 2014) in which to fufill the requirement, the variables in the model must be different in the order of stationary. According to Table 3, the results of unit root test based on Dickey and Fuller (1979) approach, all the dependent variables are stationary at first difference, I(1) except CB_NPL—at level, I(0). Moreover, beside ER which is I(1), other macroeconomic variables (PIG, Inf, and IR) are stationary at I(0) as well as for all banks’ size variables. The unit root test results justifies the use of the NARDL as the method of analysis.

The Result of Unit Root Test.

, **, and * explain the level of stationary at a = 1%, 5%, and 10%, respectively.

NARDL Estimation

To examine the asymmetric relationship between the observed variables, NARDL was adopted. Table 4 presents the NARDL results on the observed variables in line with Equation 2. In the table, the period of observations is separated between before and during the COVID-19 pandemic in which each period consists of four models that represent each type of bank: conventional rural banks (model 1), conventional banks (model 2), Islamic rural banks (model 3), and Islamic banks (model 4).

NARDL Estimation.

, **, and * explain the level of significance for 1%, 5%, and 10% in each specific symbol.

In general, the NARDL estimation considers the lag classification criteria which is before the pandemic, model 1 and 2 utilize two lag selections and for the model 3 and 4, are four lag selections. Moreover, all models during the COVID-19 pandemic adopt two lag selections. The value of R-squared in both observation periods varies between 73% and 94%. The number reflects the explanatory power of the model in explaining the influence of Xs on Y.

In addition, bounds testing co-integration analysis was conducted to identify the presence of long-run relationships between the observed variables. The value of co-integration results (Fpps) shows that all the models in both periods produce significant results at 1% to 10% significance levels, which means that there exist long-run relationships between the observed variables in all the models.

Short- and Long-Run Symmetric Results

To assess the existence of asymmetric relationship between the variables, Wald test analysis was conducted. Table 4 presents the results of the symmetric test for all the models. Before the COVID-19 pandemic, only PIG and ER have the short-run asymmetric relationship as in model 1, shown by the values of WSR for POSPIG = NEGPIG and WSR for POSER = NEGER, which are statistically significant. These findings imply that the conventional rural banks need to be aware of the asymmetric nature of the relationship between economic growth and exchange rate and NPL in the short-run period.

In model 2, the presence of long-run asymmetric relationship is evidenced from the significant value of WLR for POSInf = NEGInf and WLR for POSER = NEGER to the NPL. It means that in the long-run, inflation and exchange rate have asymmetric relationship with the NPLs of conventional banks. In addition, the negative and significant value of NEGInf reflects that a fall in the inflation rate will increase the number of NPLs in conventional banks. This is due to a lower inflation rate indicates a lower purchasing power and eventually leads to an increase in NPLs because of the inability of borrowers to serve their loans. This result is also supported by Fajar and Umanto (2017), Bayar (2019), and Roman and Bilan (2015) who revealed that inflation has a negative impact on NPLs (Table 5).

Symmetric Test Results.

, **, and * explain the level of significance for 1%, 5%, and 10% in each specific symbol.

Furthermore, conventional rural banks possibly have a higher risk exposure to business transactions made in foreign currencies, as they will be at a disadvantage if the exchange rate of the Indonesian rupiah to the USD is weak. This finding is evidenced from the asymmetric and significant relationship between POSER and NPLs of conventional banks. These results are in line with Castro (2013), Tanasković and Jandrić, (2015), De Bock and Demyanets (2019), and Klein (2013), who concluded that the exchange rate had a significant effect on NPLs.

Interestingly, the results for both Islamic rural banks and Islamic banks are different from those of the conventional banks. In both types of Islamic bank, an asymmetric relationship exists in the short-run which are ER and IR for model 3 and PIG for model 4. In the long-run, both types of Islamic banks have asymmetric relationship with all macroeconomic variables except for ER. The asymmetric and significant relationship between interest rate and NPF of Islamic banks and Islamic rural banks indicate that even though the banks claim as a non-interest based bank, both banks evidently still utilize interest rate as a benchmark to determine the profit rate in their financing activities. For the Islamic banks and Islamic rural banks, a rise in the interest rate will increase the rate of NPF in their financing portfolios. In contrast, a drop in the interest rate reduces the value of NPF in Islamic banks. The significant relationship between the banks’ NPF to interest rate is consistent with those of Castro (2013), Louzis et al. (2012), and Chaibi and Ftiti (2015).

During the pandemic period, the impact of macroeconomic variables on the banks’ NPLs/NPF seems different. Conventional rural banks have the same risk exposure to the short-run asymmetric relationship such as before the COVID-19 pandemic. The exposure of asymmetric relationship of PIG and ER in the short-run is also experienced by conventional banks. Hence, in the short-run, conventional rural banks’ NPLs is much riskier and have significant asymmetric relationship to economic growth and exchange rate compared to before the pandemic. In the long-run, exchange rate also influences asymmetrically on conventional banks’ NPLs. It indicates that when Indonesian rupiah is strengthened against the US dollar, the value of NPLs increases. The finding is supported by Tanasković and Jandrić (2015) and De Bock and Demyanets (2019) who stated that exchange rate is an important determinant of banks’ NPLs.

For Islamic banks and Islamic rural banks, there is insignificant asymmetric impact of interest rate on NPFs during the pandemic. It reflects that the movement of interest rate during the COVID-19 pandemic does not asymmetrically influence the banks’ NPFs either in the short-run or long-run. The findings are in contrast to before the pandemic and differs from Castro (2013), Louzis et al. (2012), and Chaibi and Ftiti (2015). The result also clearly sheds light on the fact that Islamic banks may already have good risk management to manage interest rate exposure, especially during times of financial crisis.

Moreover, Islamic rural banks have the same risk exposure as conventional rural banks in the short-run while Islamic banks’ NPFs has short-run and long-run asymmetric relationship to exchange rate. In the long-run, NEGER has asymmetric, positive, and significant influence on Islamic banks’ NPFs. The finding indicates that a stronger Indonesian rupiah to US dollar may cause exported goods to be expensive, erode firm profit margin and later negatively impact the performance of the firm. This eventually increases the risk profile of the firm, hence financing portfolio of Islamic banks. The result is also supported by Castro (2013), Tanasković and Jandrić (2015), De Bock and Demyanets (2019), and Klein (2013), who concluded that exchange rate had a significant effect on NPLs.

Several points are to be discussed in the comparison between before and during the COVID-19 pandemic. It is evidenced that the macroeconomic variables have been weakening during the pandemic and then it also affects the banking performance as mentioned by Nicolaides (2020) and Pratheeesh and Arumugasamy (2020). However, the study reveals conversely in which Indonesian banking industry is considered to be robust because the asymmetric impact of macroeconomic variables is not significant during the pandemic except for the exchange rate and economic growth in the short-run and exchange rate in the long-run. The findings suggest that during the pandemic, the coordination of the stakeholders in the Indonesian banking industry were well coordinated and the banks are able to adapt to the current financial turmoil. In addition, the findings also confirm that during the pandemic, Islamic banks are better off compared to the conventional as the impact of macroeconomic variables on NPF is not asymmetric.

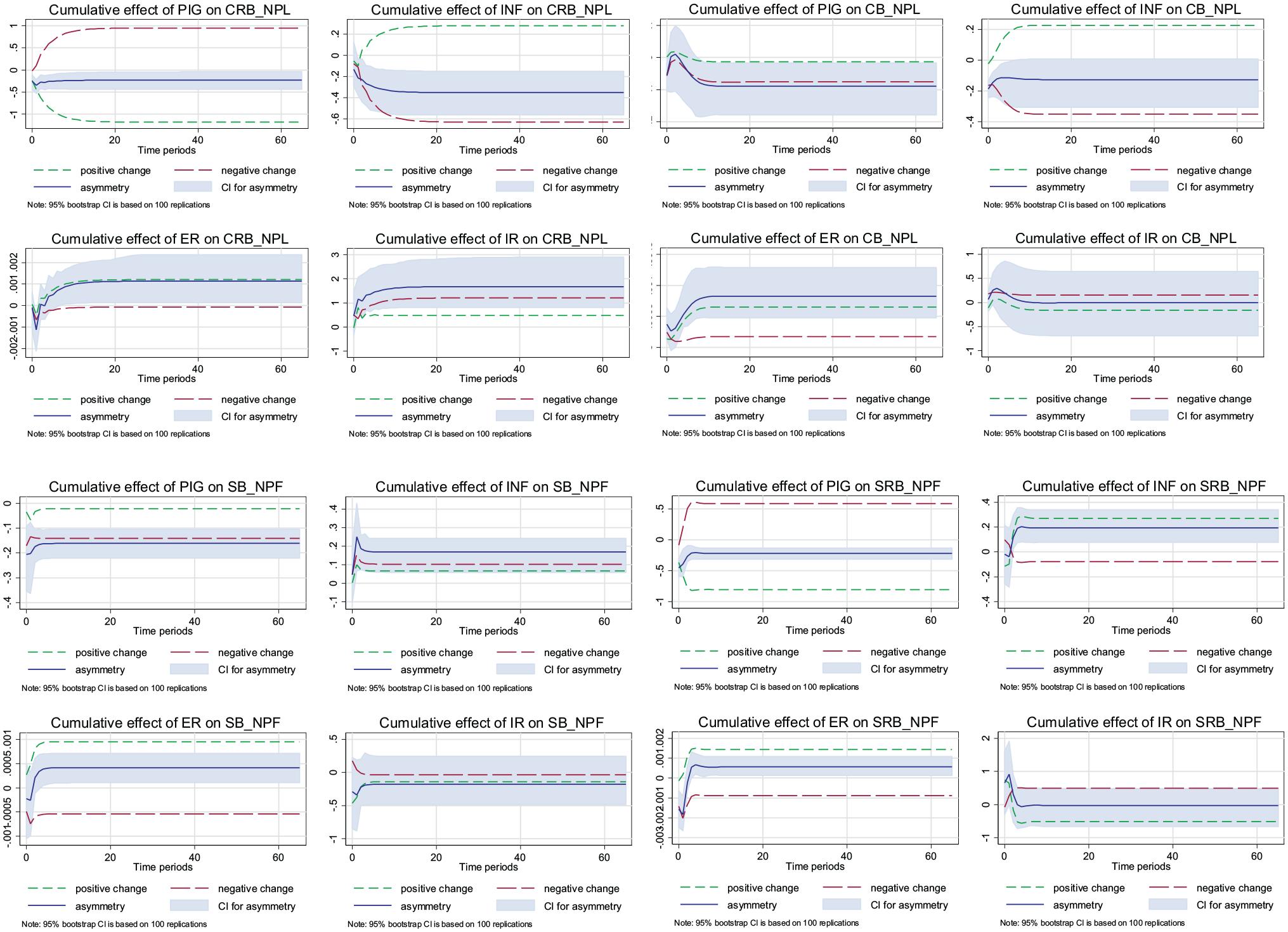

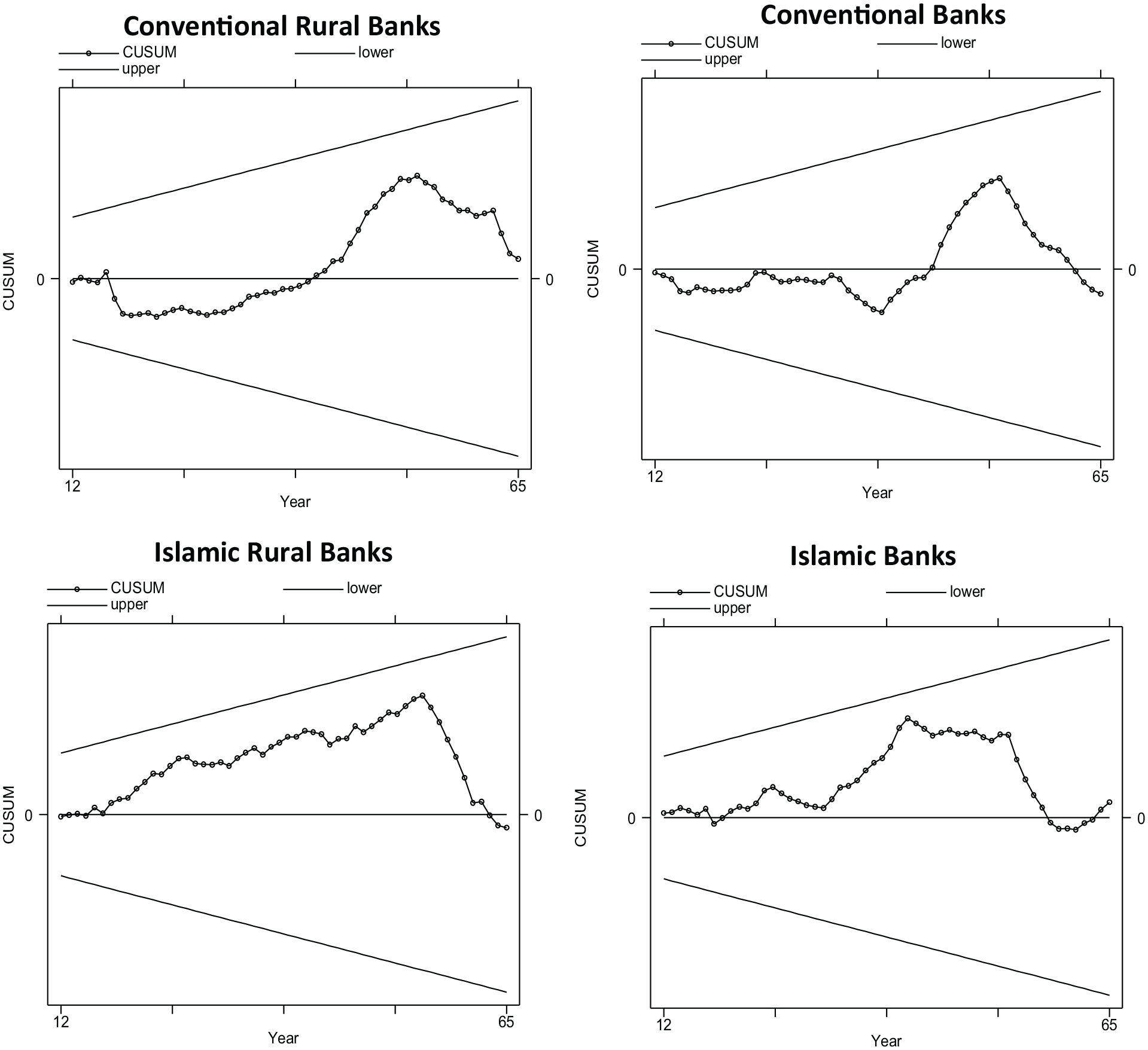

In addition, as proposed by Shin and Greenwood-Nimmo (2014), to further understand the impact of macroeconomic variables on NPLs/NPF in the Indonesian banking industry, bootstrapping analysis is adopted. The result of the analysis is shown in Figure 1 which explains symmetric and asymmetric patterns based on the Wald test. Lastly, to assess the robustness of the model, cumulative sum (CUSUM) analysis was employed. According to Figure 2 on stability tests, all models have stable parameters, which reflects the stability of the parameters used in the model. This is further illustrated by the plots of the CUSUM statistics which do not exceed the critical bounds line under the 5% level of significance.

Bootstrapping analysis of the Indonesian banking industry.

CUSUM stability test.

Conclusion

The objective of the current study is to examine the asymmetric relationship between macroeconomic variables on NPLs/NPF before and during the COVID-19 period. The results show that asymmetric relationship between macroeconomic variables and NPLs exist either in the before or during the pandemic periods. In addition, before the pandemic, Islamic banks are much riskier than the conventional banks as evidenced from the asymmetric relationship exposure of NPLs/NPF with macroeconomic variables in the short-run and long-run. However, during the pandemic, Islamic banks are better off compared to their counterparties. Further, the performance of Indonesian banking industry during the pandemic is only influenced by exchange rate and economic growth in the short-run and long-run.

Based on the findings, the banks must be aware of the existence of asymmetric effect of macroeconomic variables on NPLs/NPF. Following this, the banks need to simulate many scenarios to plan for their risk management and to address the issue of asymmetric relationship. Moreover, the finding of the study also reflects that the response of Indonesian financial authority during the pandemic is considered to be effective. This is exhibited by the lower exposure of asymmetric influence of macroeconomic variables during the COVID-19 pandemic compared to before the pandemic. However, the Indonesian financial authority still needs to scrutinize the performance of the banking industry during the COVID-19 pandemic. Since the pandemic is still on going and causing havoc to the global economy, the monetary policies such as credit relaxation, lowering interest rate and other relevant policies to the banking industry need to be strengthened further. Additionally, the Indonesian financial authority must understand the characteristic of Islamic and conventional banks because both banks have different business models and any relevant policies can be implemented effectively and provide benefit to all sorts of banks.

Finally, the study has limitation because it only observes the Indonesian banking industry and focuses on the presence of asymmetric effect of macroeconomic variables on the banks’ NPLs/NPF. Moreover, the data used in this study is also limited particularly during the pandemic due to the unavailability of relevant data. Therefore, for future research, the observation is suggested to be widened and to include cross-countries analysis with the inclusion of additional variables to measure the asymmetric relationship with banking stability. Future studies may also utilize panel data analysis to capture a more comprehensive and robust findings.

Footnotes

Acknowledgements

Thank you to all contributors who helped in completing this research.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported from Pusat Pengkajian Ekonomi (PPE), Department of Economics, Universitas Islam Indonesia..