Abstract

The e-commerce market of Pakistan has phenomenally fostered in recent years as a result of cyberspace expansion and launching of various national and international vendors. While country’s e-commerce scenario has significantly reshaped, customers are still reluctant to adopt e-payment methods and cash on delivery (COD) prevails as the method of payments for online shopping. This study was conducted to empirically investigate major factors which influence Pakistani customers to opt for COD while shopping online. A framework was proposed based on seven constructs and the data were collected using 5-point Likert-type scale. Statistical Package for the Social Sciences (SPSS) v. 22 and Amos v. 23 were used for statistical analysis and structural equation modeling (SEM). Cronbach’s alpha values above .85 were found suggesting good internal consistency. The goodness-of-fit index and adjusted goodness-of-fit index values were observed to be 0.933 and 0.866, respectively. In SEM analysis, perceived security against online scams and perceived control over the buying process were observed to be the key role players instigating Pakistani customers to use COD. Interestingly, perceived trust and perceived satisfaction did not show significant impact. Moreover, the moderator of ease of use positively mediated the influence of perceived security on the use of COD. This study presents imperative implications for online businesses as well as government agencies. The investigation provides an insight into purchase behaviors of Pakistani e-customers and has paramount importance for e-commerce retailers and marketing startups in evolving e-commerce scenario of the country.

Introduction

Electronic commerce (e-commerce) is firmly defined as the use of electronic communication and digital information processing technology in business transactions to create, transform, and redefine relationships for value creation between or among organizations, and between organizations and individuals (Chanana & Goele, 2012). E-commerce vendors trade products and services to the customers directly through the websites’ portal, social media platforms, or messaging apps. Many of the customers use internet as a source of information to compare the prices of products and services or to look for the offers before purchasing the products online. Usually, the vendors’ website portal provides a digital shopping cart for selected products and allows payment through credit card, debit card, or electronic funds transfer.

E-commerce is in earlier stages in Pakistan; however, it is growing at an enormous pace and has huge potential. Pakistan is a country of 207 million people with a median age of 22 years. Youth makes 63% of the country’s population and the estimated number of internet users in the country is over 40 million. Pakistan recorded e-commerce sales of US$622 million in 2017, while e-business was estimated to experience 52% to 60% rise in 2017–2018 (APP, 2018; Sarfaraz, 2018; H. Usman, 2018; S. Usman, 2018). Moreover, the number of internet users is rapidly rising with the spread of cellular coverage, the launch of 3G and 4G internet, and landline expansion that would flourish the e-commerce businesses even more as growth and visibility increases (Saleem, 2015). Daraz.pk and Olx.com are famous e-entrepreneurs in this regard. In addition, new online merchants and customers are increasing all around the country (Adam, 2017).

Several payment methods have been introduced for e-commerce. These include e-payment options such as credit/debit cards, prepaid cards, and mobile wallets. Developed nations have already adopted such e-payment approaches, but in developing countries like Pakistan, a substantial proportion of e-customers is using cash on delivery (COD) (Hira, 2017). Pakistan has a cash-based economy and the customers feel convenient to use currency for shopping (T. A. Khan, 2017). Either a significant fraction of customers do not have access to e-payment platforms or they do not prefer using such means. Conversely, COD is deemed to be a famous payment method in the country. It allows the customers to order a product without having to pay for the same instantaneously. COD is also a prioritized payment method in India, Bangladesh, Myanmar, and United Arab Emirates (Chiejina & Olamide, 2014; Halaweh, 2017; Jana, 2017). Although the ratio of online orders through COD is higher in Pakistan as compared to other South Asian countries, no extensive investigation has been conducted to analyze the key role players in this context.

This study was conducted to dissect unique factors that influence e-customers’ behavior to opt for COD while shopping online. The research also aimed to evaluate the nature of Pakistani e-customers and relate it to major elements urging them toward COD. Hence, this research provides some interesting insights into Pakistan’s phenomenal e-market of 70 million broadband internet users. Exploring the motives for the most widely chosen payment option for e-shopping in this exceptionally emerging market carries significant importance. To the researchers’ best knowledge, this is first report in this context as no empirical studies have earlier been conducted relevant to the factors which dictate the use of COD for e-commerce in Pakistan. The investigated factors were selected from previous studies conducted in other backgrounds.

Regarding the order used in this article, the next section presents work on e-commerce in Pakistan and the available payment methods on the basis of which the framework and hypotheses were built. The third section describes methodology, and the fourth section documents data analysis and results. The fifth section presents discussion while sixth section denotes theoretical and managerial implications. The last section focuses on the conclusion, limitations, and future work.

Review of Related Literature

E-commerce stability is not a new-fangled matter. Concerns about payment methods have been perceived since a while. Nevertheless, as e-commerce and e-payment approaches bourgeon, issues around payments for e-commerce would become more insistent for vendors and suppliers (Abu-Shamaa & Abu-Shanab, 2015). Payment options have ascended as one of the major strategies of e-commerce vendors to discriminate and get market adage. Therefore, we aimed to focus on e-customers’ behaviors in online purchases, while examining the factors influencing the use of COD in Pakistan’s e-market.

E-Commerce and Payment Methods

E-commerce activities are rapidly expanding in Pakistan because of incredible pace of technology adoption, cellular coverage, landline availability, and access to computers and smartphones. Daraz, homeshopping, and olx are the most prominent e-merchants in the country (Aadil, 2017). Cosmetics, daily use products, food, medicines, and groceries are already being provided to customers through e-commerce. Even the trend of major investments through e-platforms is also establishing and customers are intending to buy property, cars, laptops, and other electronic products online (H. Usman, 2018; S. Usman, 2018). International online commerce companies like Alibaba have also entered Pakistan’s market (Pakistan Telecommunication Authority, 2017). To pay for online shopping, COD is widely used in the country and the percentage of COD-based customers is estimated to be higher as compared to figures from India, Bangladesh, and Myanmar in South Asia (Chiejina & Olamide, 2014; Halaweh, 2017; Hamid, 2014; Pakistan Telecommunication Authority, 2017).

Various means of payment have been introduced for e-commerce-based purchases including credit and debit cards, smart cards, mobile payments, e-checks, and e-wallets. E-payments facilitate in transferring money to retailers in real time. Adoption of secure and trustworthy e-payment systems have progressively grown e-commerce activities in developed countries. However, in Pakistan, COD is estimated to be widely used as a payment method for transactions between customers and e-commerce retailers as per some unconfirmed news reports (Sarfaraz, 2018; H. Usman, 2018). Debit and credit cards are generally used to withdraw cash in Pakistan through ATM machines. Many of the bank cards do not provide support for payment on e-commerce sites at all, and if they do, a prior activation is required before transaction through phone banking, complicating the payment process.

Customers in Pakistan lack technical knowledge for online shopping as 60.78% population of the country live in rural areas and literacy rate of the country is also very low (Rehman et al., 2015). Moreover, there is a deficit of trust among the customers against sharing their e-payment information online. Therefore, COD is perceived as a prioritized alternative for online shopping. Studies from various backgrounds have indicated that privacy and security are the main factors which make customers reluctant toward using other e-payment methods (Maqableh et al., 2015; Mekovec & Hutinski, 2012; Ponte et al., 2015).

E-commerce is still evolving in Pakistan and the customers lack prior experience of online payments. In addition, online payment rules and cyber laws are not mature and fail to provide enough sense of security to the customer. Therefore, events of hacking and misuse of e-payment information are frequently reported. Such scams hinder the prospects of adoption of e-payment methods. The COD transactions are considered safe in this scenario as no sharing of private banking information is involved. According to Guo et al. (2012) and Jana (2017), COD is a source of satisfaction for customers attributed to such reasons. Furthermore, COD is also an alternative for youngsters and those customers who do not have credit/debit cards or other e-payment facilities (Investopedia, 2018).

COD is a payment approach where customers select to pay for the purchased product once it is delivered. Hence, a customer would have to pay for the product only after receiving it at the doorstep (Amit, 2011; Chiejina & Olamide, 2014). When opting for COD, customer can make the purchase without cash. The retailer issues an invoice cum with the consignment and then a logistic company is involved for product delivery and payment collection. Therefore, this approach provides a sense of security and trust to the customer.

Research Model and Hypotheses Development

COD is widely used in Pakistan. However, no research-based evidence has been established to quantify its use and influence of elements determining the same. Jana (2017) explored the Indian e-market and noticed significant use of COD in the country. Likewise, Pencarelli et al. (2018) investigated the role of COD in Italian context. This study explores the use of COD in Pakistani e-market and assesses the impact of different role players in this reference. Below is an overview of the review of literature followed by relevant hypotheses.

Perceived alternative of E-payment methods

A number of studies show that the Pakistani customers are reluctant to adopt e-payment methods (Haider & Nasir, 2016; S. H. Khan & Arshad, 2010; A. S. Khan et al., 2014; Sheheryar et al., 2015). A significant fraction of the population do not possess credit cards and therefore need other methods of payment for e-purchasing (A. S. Khan et al., 2014). COD provides a convenient access to e-commerce as an alternative of e-payments. Also, it is the only choice for people having less technical knowledge and low education (Chiejina & Olamide, 2014; Toyin & Damilola, 2012). Therefore, it is assumed that COD will be perceived as an alternative of e-payments by Pakistani customers intending to shop online.

Perceived control over the buying process

Pakistani e-market is yet evolving and most of the retailers are new startups which have not established brand loyalty among customers. Customers have serious fear of fake and low-quality product while placing an order online (Chiejina & Olamide, 2014). Therefore, they prefer to check the product quality before paying for it. COD offers a human interaction as suppliers have to communicate with the customer over phone before sending the product, which gives an opportunity to get their concerns addressed (Chiejina & Olamide, 2014; Halaweh, 2017). Moreover, COD reduces the possibility of low-quality product, wrong delivery, or no delivery at all (Chiejina & Olamide, 2014; Jana, 2017). Likewise, COD also offers a chance of product replacement if the purchase is not in good condition. Therefore, customers perceive more control over the buying process as they have to pay for the product after checking the product physically. Also, more details of the customers are on record when they use e-payment methods for purchases. This information can be used at any time to track customers’ particulars and preferences (Halaweh, 2018). Customers perceive more control over the buying process in case of COD as there are fewer chances of tracking personal information for future advertisements.

Perceived satisfaction

Customer satisfaction is very important both for e-payment and e-commerce providers. The satisfaction of online customers involves a number of factors. A customer is expected to purchase through e-commerce only when he is satisfied of the payment method he adopts. Hence, online payments have become one of the most decisive aspects of e-commerce (Raza et al., 2015). Many studies have reported that customers’ dissatisfaction regarding online transactions stops them from shopping online (Guo et al., 2012; Reddy & Reddy, 2015). Raza et al. (2015) and Rouibah (2015) also proposed a significant relation between customer satisfaction in online payments and e-shopping. Although e-payments may offer some advantages in certain cases for customers as well as e-retailers, cash is still customers’ source of satisfaction in cash-based countries (Halaweh, 2017; Rouibah, 2015). Hence, it can be hypothesized that perceived satisfaction of the customers will make them opt COD in e-commerce.

Perceived security

Security is an important concern in customers’ viewpoint when they buy a product online (Barkhordari et al., 2017). Most of the developing countries lack strict implementation of cyber laws which encourage hackers to target online users from such locations. E-payment systems and vulnerable e-merchant websites are focus of hackers to steal personal information and misuse the same (Singh, 2013). Therefore, customers feel insecure when providing such data on e-retailers’ websites. Security of personal data, as per many reports, is one of the most important components of e-commerce activities (A. S. Khan et al., 2014; Li et al., 2007; Polasik & Fiszeder, 2010). Frequent reports of identity theft and misuse of payment information compel the customers to refrain from using such information anywhere online. Pakistani customers also have such fears regarding their e-payment data (Adnan, 2014). According to Pencarelli et al. (2018), customers feel secure when they use COD for e-shopping. Halaweh (2017) suggested that sense of security is one of the main variables regarding customers’ intentions to use COD in e-commerce. Hence, it can be speculated that Pakistani customers feel secure against online scams when they opt for COD.

Perceived trust

Lack of trust is a major obstacle in the adoption of online payment systems (Polasik & Fiszeder, 2010; Reddy & Reddy, 2015; Roozbahani et al., 2015). As eminent international retailers are not established in many of the developing countries, e-markets from such locations are occupied with indigenous startups which have not won the trust of many (Roozbahani et al., 2015). A significant proportion of e-commerce customers withdraw from online shopping because of rust deficit on online payment gateways or e-retailers’ website (Barkhordari et al., 2017; Lim et al., 2007). COD offering retailers are relatively more trusted as it ensures the identity of the e-vendor. In a COD-based purchase, payment is collected through a logistic company; hence, customers would know the origin of the company sending the consignment. Moreover, COD also warrants that the product will actually be delivered. Therefore, it can be hypothesized that customers’ trust on e-retailer increases when they find COD among the payment options.

Ease of use

E-commerce and online payments heavily rely on skills, abilities, and internet expertise of users (Barkhordari et al., 2017). The complexity of online payments negatively affects e-customers (S. H. Khan & Arshad, 2010). COD makes the online buying process very simple because there is no need of having already available e-payment resources. Customers can just order the product without having to pay while placing the order (Halaweh, 2018). COD does not involve any activation for online sessions or funds readiness. This ease of use (EU) of the COD-based payment system increases customers’ sense of security and builds trust to buy online (Haider & Nasir, 2016). Although perceived security and trust are separate hypotheses; from cited literature, we consider EU as a possible moderator on trust and security in use of COD.

Use of COD

Customers’ behaviors toward online payments play a vital role in e-commerce and a business cannot excel its revenues ignoring the same. Jana (2017) mentioned that in cash-based societies, customers prefer COD for online shopping. Apart from numerous other reasons, use of COD is also a matter of conventional behavioral preference. Moreover, Pakistani e-market faces trust deficit about newly evolving e-payment systems (Sabir et al., 2014). COD offers a cash-based approach that is deemed to be trustworthy among customers (Jana, 2017). Furthermore, e-payments heavily rely on internet expertise of customers (Barkhordari et al., 2017). Complexity in online payments negatively affects customers intending to shop online, while COD is an incredibly simple approach to use e-commerce. Hence, COD mitigates the reservations of conventional customers instigating them to avail the comfort of online shopping (S. H. Khan & Arshad, 2010). Therefore, it can be hypothesized that the use of COD positively influences the customers to use e-commerce.

The framework of the study presented in Figure 1 was developed on the basis of conceptual research. The emphasized factors can be speculated to play important role toward use of COD for e-purchasing in Pakistan. The perception of COD as an alternative of e-payment methods, perceived security, control over the buying process, trust, satisfaction, and EU are all expected to positively influence COD adoption. However, the impact of these constructs regarding COD has not been quantified in context of Pakistan. Therefore, this study was designed to empirically investigate and measure the factors which act as stimulus to increase Pakistani customers’ intention to use COD in e-commerce.

Proposed framework on use of cash on delivery.

Method

The questionnaire for the survey was developed following the guidelines of Peter (1981). Data were collected from Pakistani e-commerce customers having an online buying experience, through an online survey. Convenience sampling technique was used for collecting the sample data. The questionnaire comprised two sections: the first section contained information about the demographics of the respondents’ gender, age, and education, while the second section based on the information about the impact of the constructs on use of COD.

A structured questionnaire was employed for pilot test for pre-testing purpose. The questionnaire was distributed among 15 online customers to assess whether the questions used in the document were understood by the respondents. All variables were found to be supportive in the pilot test. Therefore, the variables and the items were kept the same in the actual survey.

The survey form was created and distributed via Google Forms. The survey was conducted during November 2018–February 2019. Data were collected from Pakistani e-commerce customers. The intent public of this research was the consumers who had some online buying understanding. A total sample of 175 respondents was received, but only 151 were used while the rest were rejected because of improperly filled forms. All items were evaluated on a 5-point Likert-type scale of I strongly disagree (1), I disagree (2), Neutral (3), I agree (4), and I strongly agree (5).

The questionnaire contained seven constructs and each construct had two items representing the same (Table 1). The sample size was confirmed to be appropriate and meeting the conditions of the minimal sample size required. Following the reports of Chin and Newsted (1999), Hair et al. (2014), and Sarstedt et al. (2017), the minimum sample size for the study (six latent variables and one dependent variable) was determined to be 70. As this study had 151 samples, the data were processed further keeping in view that the conditions of minimum sample size were met.

Constructs and Items of Survey.

Note. COD = cash on delivery.

After collecting and coding the measurements, the data were entered into SPSS Statistics v. 22 and Amos v. 23 for analysis. The data were analyzed using structural equation modeling (SEM) in Amos software.

Data Analysis and Results

A seven-construct model was developed to analyze the influence of COD on customers for online payments. First, reliability of the constructs was tested in SPSS. In reliability test, Cronbach’s alpha values were found to be above .85 and were considered acceptable (Homburg et al., 2019). Cronbach’s alpha for the variables ranged from .72 to .86 which suggested good internal consistency and reliability. Maximum Cronbach’s alpha value was observed for perceived trust on e-commerce (.86), whereas the minimum was noticed for perceived security against online scams (.72). According to the scale, analysis of the constructs has been shown in Table 2.

Results of Reliability Test.

Note. COD = cash on delivery.

The demographic information of the participants is shown in Table 3. Respondents were in the age of 23–30 years, which indicated that the youngsters are taking more interest in online shopping in Pakistan. The number of male online buyers (60.9%) was greater than the females (39%.1). Overall results showed that bachelor (43%) and master (37%) degree holders were more involved in online shopping in the country.

Demographic Information of the Survey Participants.

Confirmatory Factor Analysis

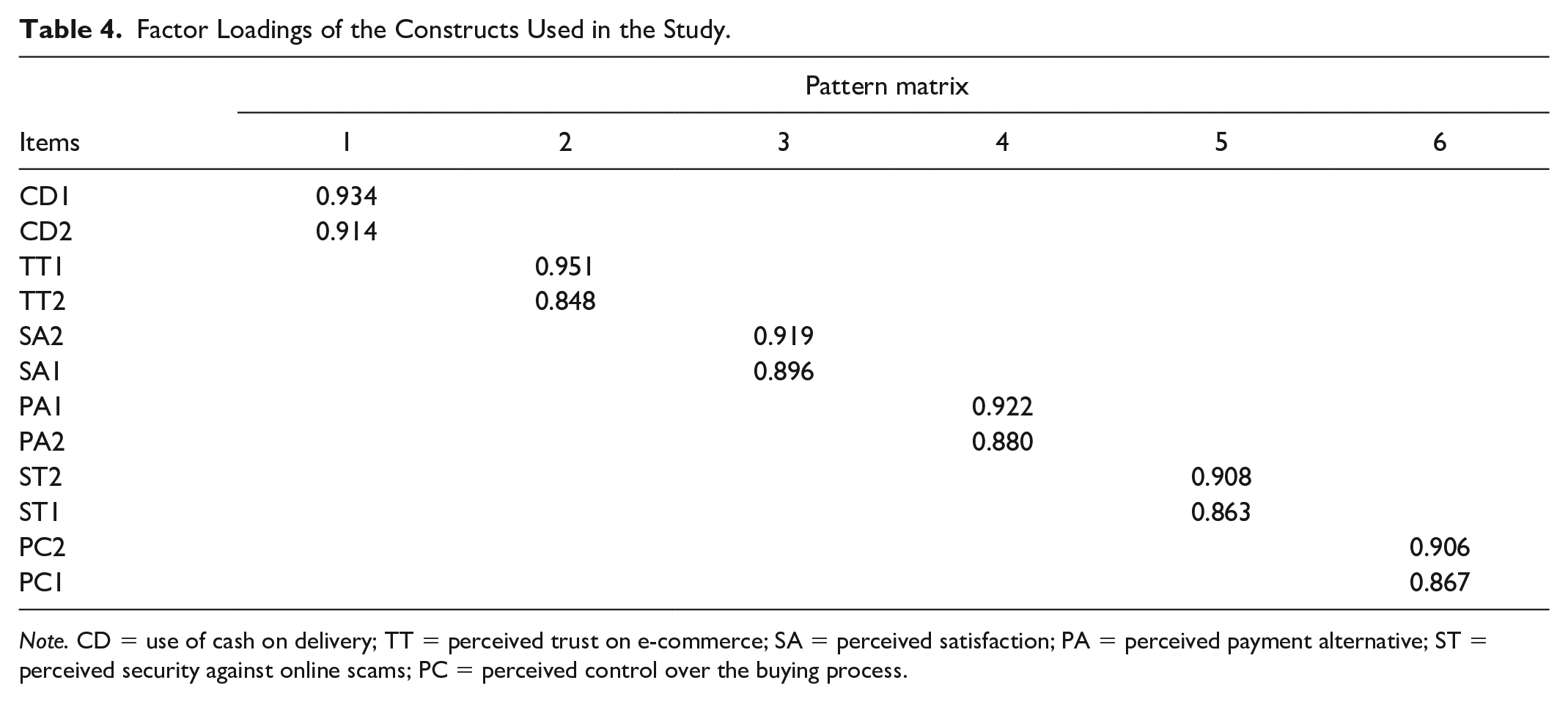

In this study, exploratory factor analysis (EFA), confirmatory factor analysis (CFA), and SEM were used for analyzing the data. EFA analysis was conducted to measure the significance of the hypothesized variables. All factors were accepted to be interpretable. The variables accounted for 83% of the variance (Appendix). Then, CFA was applied to the six fixed components obtained from EFA using Varimax Rotation and Maximum Likelihood Extraction method. CFA reflects relation between observed constructs and the latent constructs. For construct validity, the Varimax with Kaiser Normalization technique was employed. Items loaded well under each construct as indicated by the pattern matrix (Table 4).

Factor Loadings of the Constructs Used in the Study.

Note. CD = use of cash on delivery; TT = perceived trust on e-commerce; SA = perceived satisfaction; PA = perceived payment alternative; ST = perceived security against online scams; PC = perceived control over the buying process.

Convergent and Discriminant Validity

Convergent validity of the model was evaluated using two standards as suggested by Hair et al. (2014) and Henseler et al. (2012) who proposed that first, the average variance extracted (AVE) for each latent construct should be greater than 0.5; and second, the latent factor loadings should exceed 0.5 (AVE > 0.5). The convergent validity of the constructs indicated that the values for all constructs were greater than the 0.5 thresholds (Table 5). The measurement of the model showed great convergent validity.

Square Roots of Average Variances Extracted.

Note. Square roots of AVEs have been shown on diagonal in bold. CR = composite reliability; AVE = average variance extracted; MSV = maximum shared variance; CD = use of cash on delivery; TT = perceived trust on e-commerce; SA = perceived satisfaction; PA = perceived payment alternative; ST = perceived security against online scams; PC = perceived control over the buying process.

p < .100. *p < .050. **p < .010.

Discriminant validity, conversely, was calculated using the Fornell–Larker standard, which suggests that the AVE of each latent item must be higher than the maximum squared correlations among any other maximum shared variance (MSV) (Fornell & Larcker, 1981). Table 5 presents the values of composite reliability (CR), AVE, and MSV of the constructs. All the values were within satisfactory ranges as cited.

Model Measurements

The SEM was applied to investigate the causal relations between the hypotheses. SEM is a statistical method that analyzes the relation of factors with each other. It is a powerful multivariate technique that measures direct and indirect effects and encompasses multiple regressions (Bollen, 1989). Amos was employed to compute an overall goodness-of-fit index (GFI) for confirming whether the statistical findings were supported in our model. The GFI measures the fit of a model matched to other models (Hair et al., 2013). Moreover, statistical computing was conducted to produce the model fitting indices.

Table 6 shows the results of model fitness developed through the CFA method. According to Bentler (2007), a model is a good fit if GFI value is closer to 0.90 or higher, while the value of adjusted goodness-of-fit index (AGFI) is around 0.80 or greater. The measurements of the model were observed to be a good fit as its GFI and AGFI values were 0.933 and 0.866, respectively. Furthermore, the comparative fit index (CFI), which examines the internal model fitting, was also determined. The values of CFI may range from 0 to 1 (Bentler, 2007). In this study, the CFI values of 0.955 were observed, which suggested a good fit. The index of root mean square error of approximation (RMSEA) was also investigated to assess the average of residuals not accounted for by the model. The value of RMSEA was recorded to be 0.065, which indicated that the model was acceptable (Bentler & Yuan, 1999). Figure 2 shows the CFA path model; the values reconfirmed the model fitting results of this study (Figure 2; Table 6).

Model of confirmatory factor analysis.

Summary of Model Fit Statistics for Confirmatory Factor Analysis.

Note. CFI = comparative fit index; GFI = goodness-of-fit index; AGFI = adjusted goodness-of-fit index; RMSEA = root mean square error of approximation; CMIN = chi-square mean; DF = degree of freedom; SRMR = standardized root mean square residual.

SEM Path Analysis

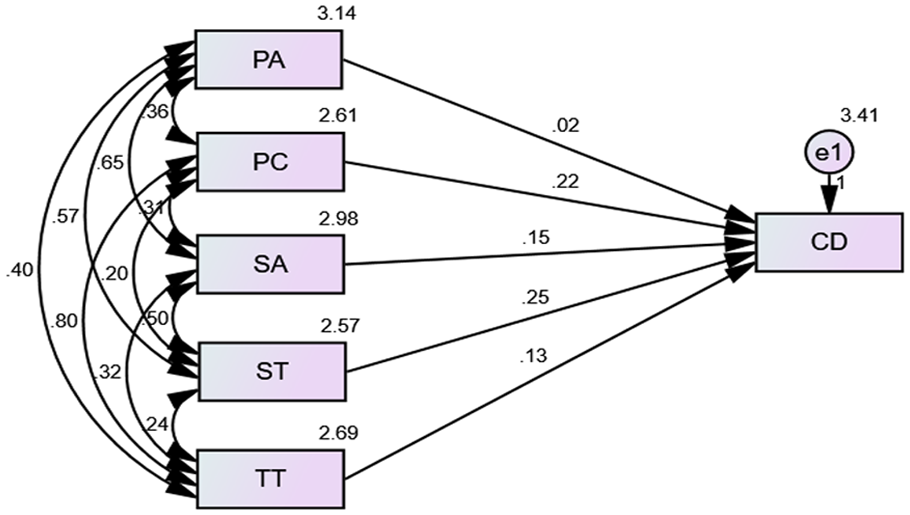

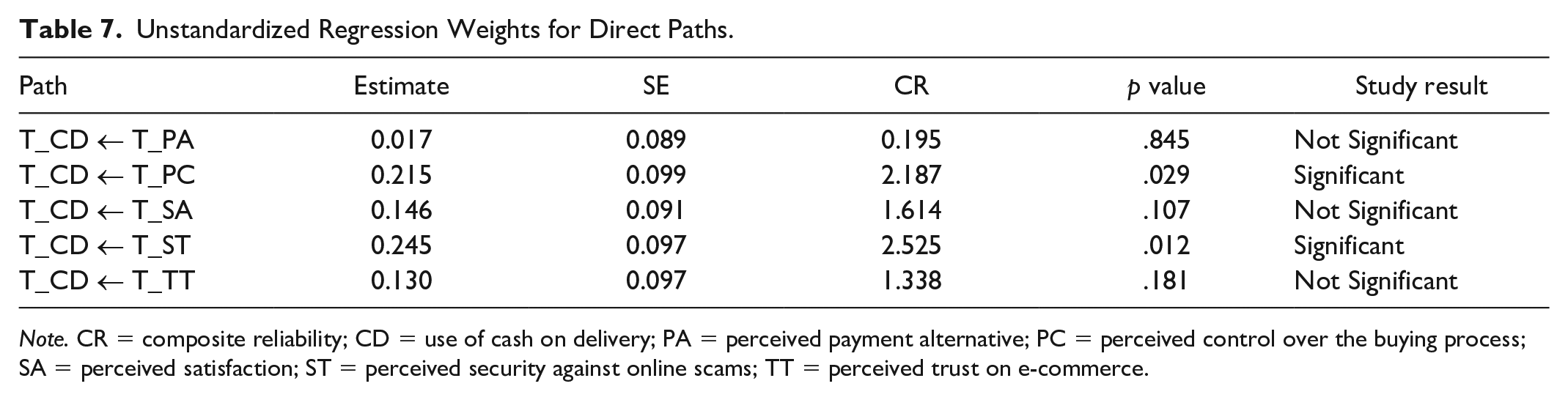

SEM clarifies the relationship between two or more latent constructs, and the relation between unobserved and observed variables in a model (Bentler & Yuan, 1999). The model of the path analysis, as shown in Figure 3, illustrated the direct paths of the model, and the impact of independent variables of perceived payment alternative (PA), perceived control over the buying process (PC), perceived satisfaction (SA), perceived security against online scams (ST), and perceived trust on e-commerce (TT) on the dependent variable, that is, use of cash on delivery (CD). The figure indicated the whole fit of the model. The results of the direct paths test have been shown in Table 7. The results depicted that PA had no significant impact on CD. However, PC held a direct significant effect on CD (β = .215, p = .029). Moreover, SA did not show a significant and direct impact on CD, whereas ST was observed to be providing support for CD (β = .245, p = .012). Furthermore, TT also did not show a significant effect on CD.

Structural equation modeling (SEM) path analysis showing direct paths.

Unstandardized Regression Weights for Direct Paths.

Note. CR = composite reliability; CD = use of cash on delivery; PA = perceived payment alternative; PC = perceived control over the buying process; SA = perceived satisfaction; ST = perceived security against online scams; TT = perceived trust on e-commerce.

Moderation Analysis

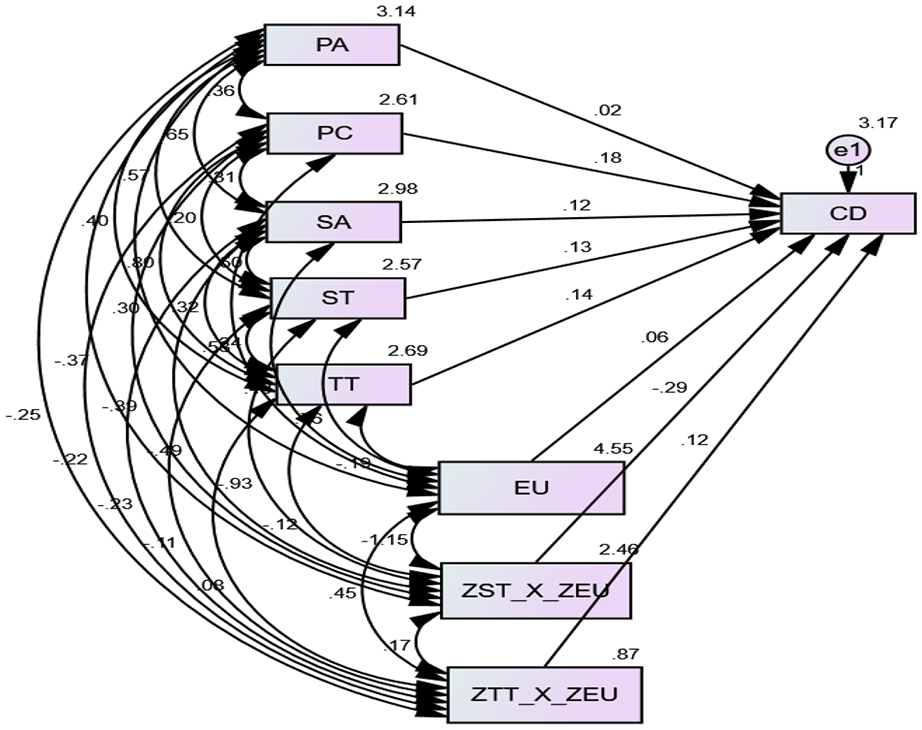

The moderating effect of EU was examined using SEM path analysis (Figure 4). The regression weights of the direct and indirect paths (after the introduction of the moderator) were determined (Table 8). EU, as a moderator, showed a significant effect on the relationship between ST and CD, which revealed presence of a moderating effect on the association (β = −.293, p = .006). However, EU did not demonstrate significant impact on the relationship between TT and CD. The results of this analysis revealed that people prefer to make decisions independently, rather than only relying on the EU in decision-making.

Structural equation modeling (SEM) path analysis showing paths with a moderating effect of ease of use (EU).

Unstandardized Regression Weights for Direct and Indirect Paths.

Note. CR = composite reliability; CD = use of cash on delivery; PA = perceived payment alternative; PC = perceived control over the buying process; SA = perceived satisfaction; ST = perceived security against online scams; TT = perceived trust on e-commerce; EU = ease of use.

Discussion

E-commerce activities have surged in Pakistan during recent years (T. A. Khan, 2017). Pakistan, being a country of huge population and a location where internet coverage has dramatically expanded within the last decade, is one of the most promising locations regarding e-commerce (Syed, 2017). COD is playing a paramount role in e-commerce adoption among Pakistani customers. It is serving as a primary medium of payment for online purchases. This study was designed to investigate the use of COD in the country and the role players influencing its adoption. The framework was developed on seven vital constructs which significantly influence customers’ intention to use COD as a prioritized payment method. As per our best knowledge, this is one of the first reports exploring the use of COD among Pakistani customers and its quantitative relationship with the contributing elements. Hence, this study has great importance in reference to the Pakistani e-commerce market.

SEM was used to evaluate the fitness of the proposed model. A significant impact of constructs was observed on the use of COD, illustrating that Pakistani customers perceived COD as a convenient payment alternative in e-commerce (Figure 5). The major factors influencing the COD adoption were identified to be security against online scams, perceived control over the buying process, and EU. COD was noticed to be a choice of highly educated people as well, who were expected to have technical knowledge as well as access to other possible payment options. This observation indicated that Pakistani customers have reservations against sharing their financial information over e-commerce platforms (Chiejina & Olamide, 2014; Halaweh, 2017; Hamid, 2014; Li et al., 2007). The absence of strict cyber laws and the high frequency of online scams increase the sense of insecurity among Pakistani customers (Institute of Business Administration, Karachi, 2015; Sarfaraz, 2018; H. Usman, 2018). However, it is worth mentioning that Pakistan’s cyber laws are evolving, which might change the scenario in coming years regarding e-commerce payment options (Pakistan Telecommunication Authority, 2017).

Hypotheses and their significance results.

It was observed that the customers perceived higher control over the buying process when they selected COD. By opting for COD, customers can inspect the product before payment that enhances customers’ confidence on e-retailer and gives a sense of control over the buying process. Moreover, COD provides the option to return the product in case of low-quality augmenting customers’ perception of control over the buying process. Such observations were parallel to the reports of Barkhordari et al. (2017) and Li et al. (2007) from other backgrounds. The mentioned results were also in agreement with the study of Chiejina and Olamide (2014) who investigated Nigerian e-market in this context.

Perceived satisfaction and perceived trust were not found to be significant factors for Pakistani e-customers. Likewise, Halaweh (2017) found that perceived trust had a weak relationship with the use of COD in United Arab Emirates. Conversely, Chiejina and Olamide (2014) proposed these elements to be significant role players in this context among Nigerian customers. The variation in results from different backgrounds indicated a paramount role of characteristics of distinct populations toward customers’ behaviors.

The results of this study also indicated that Pakistani customers perceive greater security against online scams when they choose COD. E-market users feel reluctant to share banking information on e-commerce sites because of the fear of hacking and data theft (Halaweh, 2017). In addition, EU was also found to be a key role player. Opting COD in e-commerce is convenient because an order can be placed without paying for it instantaneously, and without providing private details. Moreover, COD offers the customers a human interaction. The suppliers communicate with the customer over the telephone before sending the consignment, which provides an opportunity to the customers to get any queries addressed (Chiejina & Olamide, 2014; Halaweh, 2017; International Finance Corporation, 2014).

The results of this study were similar to the report of Jana (2017) who investigated the percentage of COD usage in India. Halaweh (2017) also documented results parallel to our report while analyzing the role of COD in e-commerce market of United Arab Emirates. This tendency toward COD in developing nations is contrary to the adoption of credit cards–based payments in developed countries (European Central Bank, 2002). Such difference could be attributed to the fact that customers from developed nations have more trust on cybersecurity as well as access to well-known international e-commerce platforms. On the other hand, most of the e-commerce providers in developing nations are not already known. There are various new start-ups in these evolving e-markets, and many of the retailers have not established brand loyalty as well. These facts make customers reluctant to share their payment information on e-commerce platforms (S. Usman, 2018).

Pakistani customers are habitual of conventionally shopping from markets and shopping malls (Badar, 2008). E-commerce is a new phenomenon for them. COD is a trouble-free and readily available option for Pakistani customers, as it does not demand any prior activation from banks as required for other ways of payment. Generally, in Pakistan, credit and debit cards are not meant for e-payments and they have to be activated for “online sessions” of limited time for any such transaction (T. A. Khan, 2017). Pakistani customers are also not very familiar with the usage of credit and debit cards online (Sheheryar et al., 2015). Therefore, perceived security, control over the buying process, and EU make Pakistani customers choose COD in online purchases.

Theoretical and Managerial Implications

This study has vital inference for scholars, academics, and online retailers. The work has a greater applicability in developing nations, where the e-payment adoption ratio is very low as compared to the western world. The outcomes of this study recommend that perceived control over the buying process, perceived security, and EU are crucial aspects regarding the use of COD in e-commerce. This investigation refines the scale of use of COD mode of payment as an applicable method in the Pakistani e-market. The Government of Pakistan is very interested in digital revolution in the country. The cashless economy has also recently emerged as one of the priorities of the state. The study suggests the authorities to focus on cybersecurity issues in e-payments to realize any such objective.

The study indicated that COD is a prevalent payment method in Pakistan. The insinuation of this research suggests that the new vendors entering the e-market should provide COD option among payment methods. In earlier reports, it has also been proposed that the COD option appeals more customers of different demographic backgrounds (Chiejina & Olamide, 2014; Halaweh, 2017, 2018). Online firms can offer COD as a strategical direction to enhance their sales. The findings of this research also suggested that COD increases the customers’ trust toward an online retailer; e-commerce companies could use this fact as a tool to mitigate customers’ reservations against online scams (Kidane & Sharma, 2016). As per the report of Kidane and Sharma (2016), approximately 67% customers dismiss transactions by deserting e-commerce when vendors ask to verify banking information. Therefore, COD has great prospects for online business, especially in developing countries like Pakistan.

Regarding the drawbacks of COD, it is presumed that this mode of payment increases the “risk of returns” from customers. When a customer has already paid online through an e-payment gateway, the chances of product returns are marginal. Whereas, in case of COD, vendors may face losses when customers return the items without paying for them. Another big demerit of COD is the delay in cash cycle days. In online payments, vendors receive payments before the actual delivery of the product. On the other hand, in COD, vendors have to wait for cash until the product is delivered to the customer. From the consumers’ perspective, generally, discount offers are not available in case of COD and thus customers may have to pay extra when choosing this method of payment. Other e-payment providers frequently offer price deductions or cash-back campaigns through partnership with e-retailers. Moreover, availability of cash at the time of delivery is also an issue from customers’ standpoint. Nevertheless, the selection of the payment system is totally dependent on customer’s preferences.

Conclusion, Limitations, and Future Work

The e-commerce market of Pakistan has phenomenally fostered in recent years. This study explored the factors and major role players that make Pakistani customers choose COD while purchasing from e-platforms. It was observed that COD is a desired payment option of Pakistani customers as it provides them a sense of security and ease. In addition, Pakistani customers prioritize COD as they consider it a tool to have more control over the buying process. Hence, COD is a convenient payment method for cash-based markets of developing countries including Pakistan. Interestingly, perceived trust and perceived satisfaction did not show significant impact while EU positively moderated the influence of perceived security on the use of COD.

This study determined that perceived security, control over the buying process, and EU were the most important factors prompting Pakistani customers to choose COD. The insinuation of this research suggests that only providing e-payment methods is not adequate to attract customers for e-commerce in Pakistan. Therefore, new vendors entering the e-market should provide the option of COD as it allays the concerns of customers and enhances their confidence on e-commerce. The study depicted that e-payment for online shopping is not a popular approach among Pakistani customers. As a result, Pakistani customers opt for COD while shopping online; attributed to the paramount factors of perceived security, control, and EU. The study gave an insight into customers’ behaviors and provided a direction to e-commerce vendors targeting the Pakistani market.

Regarding limitations of the study, this research is based on a single background among the developing countries. Future research might empirically test other countries that would help to have an overview of customers’ behaviors from different backgrounds. The impending research might also contemplate testing other factors and consider the locations where e-payment methods also prevail. Also, this research used convenience sampling technique; advanced sampling techniques could be used in forthcoming investigations. Furthermore, this study explored COD from customers’ viewpoint, and the prospective research might examine e-commerce vendors’ viewpoint instead, which would be an interesting aspect to explore.

Footnotes

Appendix

Total Variance Explained.

| Component | Initial eigenvalues | Extraction sum of squared loadings | Rotation sum of squared loadings a | ||||

|---|---|---|---|---|---|---|---|

| Total | % of variance | Cumulative % | Total | % of variance | Cumulative % | Total | |

| 1 | 3.062 | 25.521 | 25.521 | 3.062 | 25.521 | 25.521 | 2.046 |

| 2 | 1.777 | 14.808 | 40.329 | 1.777 | 14.808 | 40.329 | 1.972 |

| 3 | 1.484 | 12.369 | 52.697 | 1.484 | 12.369 | 52.697 | 1.883 |

| 4 | 1.341 | 11.173 | 63.871 | 1.341 | 11.173 | 63.871 | 1.848 |

| 5 | 1.181 | 9.844 | 73.715 | 1.181 | 9.844 | 73.715 | 1.864 |

| 6 | 1.119 | 9.323 | 83.037 | 1.119 | 9.323 | 83.037 | 1.903 |

| 7 | 0.531 | 4.423 | 87.460 | ||||

| 8 | 0.437 | 3.645 | 91.105 | ||||

| 9 | 0.322 | 2.687 | 93.792 | ||||

| 10 | 0.280 | 2.335 | 96.126 | ||||

| 11 | 0.246 | 2.048 | 98.174 | ||||

| 12 | 0.219 | 1.826 | 100.000 | ||||

Note. Extraction method: principal component analysis.

When components are correlated, sums of squared loadings cannot be added to obtain a total variance.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: National Natural Science Foundation of China (71872028) funded this research.