Abstract

Thailand has now become the aging society. However, the fact that the majority of Thai wageworkers do not effectively save for their retirement may result in several elderly living below the poverty threshold during retirement. The objectives of this research article were to find the factors determining Thai wageworkers’ retirement contribution. Founded on the theory of life-cycle hypothesis, this article employed a sample of 300 wageworkers in the Northeast of Thailand and performed a statistical analysis using the structural equation modeling (SEM) approach using age as a moderator. The empirical results revealed that expected income, wealth accumulation, career status, and health status were the main constructs influencing an individual’s ability to contribute to his or her retirement. This article suggested that a wageworker should first contribute his or her income through wealth accumulation schemes such as investment in financial assets, for example, stocks, bonds, mutual funds, and properties, investment in other business as a second job, and simply cash deposit. The results suggested that wealth accumulation was the most important mediator allowing a wageworker to contribute to retirement effectively in the long term. This article also proposed thoughtful research implications for wageworkers, employers, and the Thai government. This article recommended that the government and authorized bodies (e.g., the Bank of Thailand and the Stock Exchange of Thailand) should provide more investment alternatives and improve investment knowledge of the citizens. This would allow the citizens to have sufficient financial knowledge to invest in riskier financial instruments that potentially give better returns such as stocks.

Introduction

There has been a drastic change in the pattern of Thai population during the past two decades. Generally speaking, the population growth rate decreased from 3.0% in 1960 to only 1.1% in the recent year (Samutjak, 2015). The change in this population pattern has resulted from alterations in mortality and reproduction rates of the country’s population, where mortality rates have played a relatively more crucial role in determining the pattern of Thai population. To be more explicit, a continual and dramatic decrease in mortality rates after World War II coupled with constantly a high birth rate has caused a significant increase in the Thai population. Interestingly, due to medical technology advancement, increases in the number of health service centers and hospitals, and educational development, life expectancy of Thai people has greatly increased accordingly (Samutjak, 2015). People who were born after World War II have gradually become older and eventually approached or reached their retirement age. At present, the mortality rate in Thailand is at the low level (six out of 1,000 people) (Thai Institute of Aging Research and Development, 2016). Due to family planning policies imposed by the Thai government, the total fertility rate (the number of children) per one Thai female had gradually decreased from 6.3 in 1960 to approximately 2 presently (Ministry of Public Health, 2014). In 2015, the number of aging population was approximately 7 million and was forecasted to be 17 million in 2020 which accounted for a quarter of the total number of Thai population. It is expected that the number of aging population in Thailand will surpass all other Asian Pacific countries in 2020 (Vapattanawong & Prasartkul, 2006).

According to the United Nations (UN), a country is classified as “Aging Society” when either at least 10% of its population are above the age of 60 or 7% above the age of 65. However, a country is perfectly defined as “Aged Society” when the same proportions of aging population elevate to 20% and 14%, respectively (World Population Ageing, n.d.). Retirement is defined as a stage where a person, aged 55 and older, is not employed in the labor force and receives 50% or more of his or her total income from retirement-like sources (Bowlby, 2007). In Thailand, the Department of Older Persons (DOP) defined the elderly as people with the age 60 or above as referred to the Older Persons Act 2006 (DOP, 2006). In 2018, World Health Organization (WHO) reported that life expectancy in Thailand was 71.8 years for men and 79.3 years for women, and the total life expectancy is 75.5. With these figures, Thailand was ranked 69th in the World Life Expectancy ranking (Life Expectancy in Thailand, n.d.). At present, Thailand is now categorized as an aging society as the population with the age above 60 accounts for 15.07% of the total population (dop.go.th., n.d.). It is predicted that a declining number of working-age population will negatively impact the Thai economy. For instance, the aggregate household saving will reduce because the working-age population may incur financial obligations to support their old-age relatives, whereas a number of retired people have already been restricted from their saving capacity due to unemployment (Prompakdee, 2016). Using 2015 as the base year, Thailand Consumer Price Index (CPI) for 2019 was reported at 102.94 (Thailand Consumer Price Index | 2019 | Data | Chart | Calendar, n.d.). The three most essential categories in the Thailand CPI are food and nonalcoholic beverages (36% of total weight), transportation and communication (24%), and housing and furnishing (23%). During the past few years, inflation rates in Thailand have moved sideways in a narrow gap around 0% to 2%. As for 2019, the monthly minimum cost of living in Thailand is approximately the same as the average monthly wage of around US$400 to US$500 (14,000 Baht/month), which negatively impacts the poor’s ability to save in the long term (Thailand Average Monthly Wages | 2019 | Data | Chart | Calendar | Forecast, n.d.). In addition, Thailand Household Saving Ratio—personal saving to household net disposable income—was reported at 11.20% in 2019 (Thailand Thailand Household Saving Ratio | 2019 | Data | Chart | Calendar, n.d.). However, it appears that the majority of savings are from middle- to high-income citizens which accounts for less than 20% of its total population (Pootrakool et al., 2005; The World Bank, n.d.). In addition, young couples tend to have either fewer or no kids, thus also lowering their propensity to save. It was highly concerned that a lot of Thai citizens, especially those with low income, may have insufficient income/financial assets to live their lives after retirement due to lacking preretirement planning schemes at the individual level. The situation like this took place in several developed countries around the world previously (Singleton & Keddy, 1991; P. Taylor & Walker, 1996).

Retirement planning is beneficial to Thai employees as it influences their overall quality of life in the long term. In general, most private and governmental organizations in Thailand expect workers to retire at the age of 60. During their work lives, workers are provided with either mandatory or voluntary retirement benefits such as social security and provident fund. Although private sector workers receive a lump sum as a result of their provident fund contribution and a very small retirement pay (approximately US$100–US$200/month) from their contribution to the social security fund, governmental officers retire with monthly annuity pension and enjoy this benefit until the end of life. As referred to the Three-Pillar Retirement Principles established by the World Bank, the retirement saving schemes should include the following: first pillar—public-mandated, publicly managed, defined benefit system; second pillar—public-mandated, privately managed, defined contribution system; and third pillar—privately managed, voluntary savings, defined contribution system. As for Thailand, the first pillar includes (a) elderly benefits under the social security scheme distributed as the minimum standard monthly pay to all the elderly which can hardly beat the expected future inflations and (b) governmental pension scheme distributed as monthly annuity after retirement, managed by the Comptroller General’s Department, and created for civil servants only, which in 2016 account for only 9.4% of the Thai population (National Statistical Office of Thailand, n.d.). The second pillar involves the Government Pension Fund (GPF) which is expected to overcome the future inflation, however, only accessible by Thai civil servants. The third pillar involves several voluntary schemes managed by private financial institutions which are mostly income tax deductible, for instance, retirement mutual funds, long-term mutual fund, and retirement saving insurance. Considering the Three-Pillar Retirement Principles, there is a disparity between wage employees in governmental and private sectors. More explicitly, Thai civil servants are able to access to all the three pillars, whereas privately employed workers only receive elderly pay under the social security scheme which could barely win inflation in the long term. Hence, most wageworkers in the private sector, which account for 39.5% of the population (National Statistical Office of Thailand, n.d.), need to determine their own retirement planning. It is concerned that the fact that the majority of Thai wageworkers are not covered by pension programs and do not effectively save for their retirement will result in several elderly living below the poverty threshold during retirement.

To address the problems associated with retirement planning of wageworkers in Thailand, this article attempts to better understand the factors underlying an individual wageworker’s motive to financially plan for his or her retirement. More explicitly, this article studies factors determining an individual’s retirement contribution and how it affects an individual’s short- and long-term financial goals. As the proportion of citizens with retirement age continues to increase steadily, it means that the country will have to be responsible for these elders if they do not save and plan for their retirement now. Understanding this relationship would allow policymakers and individuals to understand the motives of financial planning. In addition, it would let policymakers precisely tackle retirement planning problems in Thailand with the variable manipulation technique at the policy level, which optimistically lead to sustainable retirement planning for the nation. To test the significance of these relationships, the structural equation modeling (SEM) approach was employed. The SEM approach begins with evaluating the measurement model and continues with creating the structural model (Hair et al., 1998).

This article is constructed as follows. Section “Saving Behavior in Thailand” begins with an explanation of saving behavior in Thailand. Next, Section “Review of Related Literature” lays the foundation for the research framework with related theories and academic literature. Section “Proposed Model, Constructs, and Variables” describes variables and their measures. Section “Method” outlines the research method involving sampling and data collection as well as statistical models. The findings and analysis of the results from the test models are deliberated in Section “Results and Discussion.” Finally, Section “Conclusion” summarizes this research article by discussing the major conclusions drawn from this study as well as suggesting policy implications.

Saving Behavior in Thailand

Pootrakool et al. (2005) used micro-data to obtain the household monthly saving trend against the average monthly income trend for different age groups. According to Figure 1, the data indicated that a maximum income of around 16,000 Baht was revealed when people reached the age of 50 to 54. Then, their income would rapidly fall after the age of 75. On the contrary, their average monthly saving reached the first high at the age of 30 to 34 (around 2,000–3,000 Baht) due to the fact that they have to save for houses, cars, and young families. The highest saving was reached again at the age of 55 to 59 (around 4,000–5,000 Baht) and later declined after the age of 60 mostly due to unemployment after the retirement age. This study also found a rising trend of the aggregate saving rates during 1990 to 2020 (Pootrakool et al., 2005). However, this study found that demography was not the primary factor explaining the fall of household saving rates. Rather, the easy credit environment expressed by the rise in credit card debt and altering attitudes toward saving of the younger generation to consume now and save later would have a more essential role.

Saving and income profile.

Using the data from Office of the National Economic and Social Development Board (2019) from 1990 to 2017, we calculated the ratio of per capita saving/per capita disposable income which indicates an individual’s ability to save. The result revealed that the mean of this ratio was 10.88% with the standard deviation of 3.56%, which implied that at the national level an individual saved around 10.88% of his or her income. The same data set was utilized to construct the trend of personal income, expenditure, and saving per capita as shown in Figure 2. According to this figure, although the per capita saving continued to increase slightly, this did not guarantee that saving would be enough for retirement at the individual level. This was because the low-income citizens saved a rather small portion of their income (Pootrakool et al., 2005) and the majority of the aggregate saving was derived from the top income ranges. In Thailand, a study also found that savers were likely to save in more conventional saving forms such as bank deposits, insurance policies, gold, and properties, rather than in financial assets such as government bond, mutual fund, corporate bonds, and stock (Suppakitjarak & Krishnamra, 2015). Nevertheless, they were reluctant to save in conventional forms but were likely to save more in capital markets as their income increased. Most of the respondents in this study also believed that investing in physical assets such as real estate created greater returns than in financial assets.

Personal income, expenditure, and saving per capita.

However, compared with savers in advanced economy like the United States, Thai savers kept around 60% to 70% of their savings in deposit accounts (The Stock Exchange of Thailand, n.d.), whereas American savers accumulate only around 15% in cash/deposits, 21% in bonds, and 55% in stocks (Bank of America Private Bank, n.d.). The lack of diversity in investment portfolio allocation in Thailand is due to limited saving instrument alternatives available and insufficient financial knowledge about riskier financial instruments that potentially give better returns.

Review of Related Literature

Retirement is defined as an event within a rite of passage that can be celebrated for an individual to trade his or her role of an employee to a nonworker (Donaldson et al., 2010). Retirement is defined due to an individual’s own expectation and satisfaction. The worker can understand retirement by gathering information and expectations of retirement role from social media such as TV, newspapers, magazines, and news programs. Social media can come across more cliché than realistic. That expectation through media gives workers a nonaccurate understanding of retirement (Carling et al., 1996). Retirement planning benefits to be able to retire early before an individual’s health becomes insufficient and creates a stable plan (realistic expectations) of when to retire (Lusardi & Mitchell, 2011). Previous scholarly research articles have investigated individual retirement decision making and planning in various aspects. During the 1990s, scholars have examined the timing and reasons of employees leaving the workforce (Hershey & Wilson, 1997; M. A. Taylor & Shore, 1995) as well as employees’ attitudes during their postemployment period (Richardson, 1993; Turner et al., 1994). The main interest of these studies demonstrates how individuals’ knowledge of finance and investment impacts the way they process the acquired financial information and the overall quality of decisions they make.

Nevertheless, most modern research articles relating to retirement place importance on individuals’ financial literacy—the basic concepts of inflation, compound interest, and so on—and their abilities to effectively plan for retirement. In addition, a study conducted in Chile tried to investigate the relationship between financial literacy and retirement planning and found that an improvement in financial literacy of individuals elevates the level of preparedness for retirement planning (Moure, 2016). On the flip side, a study conducted in Israel expressed contradictory results demonstrating no significant correlations between financial literacy and retirement knowledge when controlling for demographic and behavioral variables (Meir et al., 2016). Interestingly, retirement saving knowledge significantly increases with individuals’ tendency to check bills and bank account statements. Using a secondary panel data set from the United States, the relationship between financial literacy and retirement planning was explored using small business owners as a sample (Gurley-Calvez et al., 2015). Moreover, a research paper used mattering—individuals’ perception of making a difference in the world—to explain one’s retirement process and was found to be the only scholarly article employing the SEM approach to explain this relationship (Froidevaux et al., 2016).

Scholarly articles in Thailand neither explain the retirement planning relationships with mediating variables through the SEM approach nor use wageworkers as primary respondents. In this research article, life-cycle hypothesis was employed as a grounded theory for structural model development which illustrated the interplay of expected future income, consumption, and saving. In addition, this research connected the grounded theory with new factors, for instance, career status, health status, and wealth accumulation, to establish a more meaningful explanations on how people contribute to their retirement saving. The following sections give details regarding economics theories and related literature that helped create a framework and hypotheses for this research article.

Life-Cycle Hypothesis

The life-cycle hypothesis illuminates how people spend and save over the course of their lifetimes. An assumption underlying this economic theory is that spending and saving over lifetimes depend on an individual’s expected future income (Modigliani & Ando, 1957). Based on Figure 3, young individuals take on debt expecting that future income will allow them to pay off the debt. In other words, young individuals spend on consumption by either borrowing others or spending the assets inherited from their parents. During working years, they consume less than the level of income earned and hence create net positive savings. After the retirement age, individuals start and continue to dissave, that is, they consume more than their income. This is because retired individuals maintain their consumption despite the reduction in the income earned.

Graphical illustration of life-cycle hypothesis.

According to life-cycle hypothesis, suppose that there is a consumer who expects to live for another T years and has wealth of W. The consumer also anticipates to obtain annual income Y until he retires R years from now. Hence, the consumer’s resources over his or her lifetime include his or her initial wealth endowment (W) and his or her expected future income (R times Y). Therefore, the individual’s consumption is said to be a function of wealth (W) and expected future income (R × Y).

Permanent Income Hypothesis

The permanent income hypothesis is also an economic theory that explains the consumer spending behavior. This theory terms two types of the consumer’s income: temporary income and permanent income (Friedman, 2018). The theory states that an individual will spend money at a level consistent with his or her permanent income (expected long-term average income) rather than temporary income which varies according to inadvertent factors such as receiving an unexpected bonus or getting no pay due to temporary unemployment. Therefore, only permanent income influences an individual’s consumption. Saving will occur when an individual has his or her current income greater than the anticipated level of permanent income, which helps secure his or her financial stability due to a potential decrease in future income (Friedman, 2018; Meghir, 2004). In addition, the permanent income hypothesis states that changes in the consumption behavior are unpredictable as they are dependent on individual expectation (Wu, 2011). For instance, suppose that an individual acknowledges that he or she may earn an annual income bonus. Instead of spending more in advance, he may choose not to increase his or her spending based on possible temporary shortcomings. Consequently, he could make an effort to elevate his or her saving based on the expected increase in income.

Retirement Contribution

Individuals’ retirement contribution and saving behavior have been proved to influence successful retirement planning. Past economists described the causes of individuals’ failure to save for retirement (Poterba et al., 1996). For instance, individuals may fail to accumulate assets due to the inability to recognize the increased future value assets. They may experience shortage in earnings preventing them from reserving money for the long-term saving. They may also have misunderstanding of retirement income earned from social security, private pensions, and other sources incorporating with unforeseeable consumption needed after retirement. Workers who have to take care of retired family members have experienced their seniors’ retirement planning and this may influence the workers’ amount of planning. In addition, according to time value of money (TVM), future value of an asset depends on its present value, amount of time, and the rate of return on that particular asset (Richardson, 1993). Hence, the ability of an individual to contribute to his or her retirement portfolio today will affect the expected value of his or her retirement fund which will in turn become a source of retirement income.

According to life-cycle hypothesis and permanent income hypothesis, this study derived the following hypotheses. H1 indicated that expected future income (permanent income) influenced individual short-term financial goals (short-term consumption). According to the life-cycle hypothesis and permanent income hypothesis, expected future income (permanent income) was denoted by the number of years before retirement multiplied by the level of current income (Friedman, 2018; Meghir, 2004; Modigliani & Ando, 1957). H2 demonstrated that expected future income associated with retirement contribution. H3 proposed that short-term financial goals influenced retirement contribution. Finally, H4 proposed that individual wealth accumulation affected short-term financial goals because we assume that an individual would save before his or her current consumption.

H*1: Age has a moderating effect on Path H1.

H*3: Age has a moderating effect on Path H3.

Wealth Accumulation

A number of scholarly papers have indicated the association between individuals’ wealth and saving behavior. Personal wealth could be created from personal inheritance or savings (Wu, 2011). For wageworkers, savings could be deducted from either salary or other temporary income such as bonus, income from a second job, and passive income from portfolio investment. Personal wealth also reflected financial assets held by each individual. A cross-sectional study was conducted on 300 working-age participants to investigate the relationship between personal wealth and investment behavior (Sailaja & Madhavi, 2016). The results demonstrated that individual wealth accumulation derived from investment planning and retirement goal clarity were crucial for successful retirement planning. Furthermore, using a multistage stochastic programming approach, a research article found that real annuities were essential assets in retirement portfolio because real annuities helped reduce volatility and balance the retirement portfolio (Konicz et al., 2015). On one hand, accumulation of residential assets influenced individuals’ retirement decision as well. As changing house needs and sustainable financing of senior citizens were prevalent, the reverse mortgage approach is a strategy designed for elderly homeowners to convert the equity in their homes to income. It also maintains the opportunity to liquidate those properties and move to more suitable properties under the same contract given that mortgage schemes and longevity insurance are tied to the single property. However, scholars proposed a new approach called the flexible reverse mortgage (Bogataj et al., 2015). As for this new method, the reverse mortgage schemes and longevity insurance were tied to the life of the senior homeowner. The simulated model of the new method demonstrated lower transaction costs incurred by the homeowner. A study regarding financial attainment capacity conducted in Thailand suggested that an individual could accumulate wealth through investment in financial assets with long-term growth including stocks, mutual funds, and real estate and other investments with potentials for increased value in the future (Ketkaew, Wouwe, & Vichitthammaros, 2019). Accordingly, we summarized that wealth accumulation involved investment in several types of financial assets. As for Thai wageworkers, H5 hypothesized that their expected future income first influences wealth accumulation. In addition, H6 then assumed that wealth accumulation enhanced individuals’ ability to contribute to their retirement fund.

Short- and Long-Term Financial Goals

Financial goals can be categorized as long- and short-term goals. Short-term financial behavior is referred to as day-to-day and emergency spending (current consumption) and temporary saving behavior, whereas long-term financial behavior is referred to as retirement saving and investing behavior (Henager & Cude, 2016). Short-term financial behavior such as planning for short-term life events and keeping them on track helps reduce uncertainty and influences the process of retirement (Davis, 2007). Workers should focus on attaining short-term goals as soon as possible (Gruber & Wise, 1997). As a common sense, meeting an individual’s short-term financial goals occurs before accomplishing long-term financial goals. A financial plan can help workers plan for other short-term goals such as setting up saving accounts, setting up daily or weekly budgets for personal requirements, vacation, and to keep track of all financial transactions (McGarry & Schoeni, 1995).

Long-term financial goals may include, for instance, owning full ownership of a house/property, paying off debt such as mortgage on your home or student loans, or starting a family at 5 years after graduation. When accomplished, workers will be completely out of debt which means that they will possess full control of income (Kawakami & Haratani, 1999). Research shows that workers that meet long-term goals have less depression and anxiety and have an overall well-being. Stress influences how effective a worker can plan retirement, for instance, if a worker meets the long-term goal of being able to pay off monthly debt, then he or she will be more relaxed as he or she have no pressure (Tuomi et al., 2001). Workers with less pressure will work more effectively as they have nothing to worry. Of course, this allows a worker to focus on high-level commitment to continue meeting future goals (Barsky et al., 1997). Therefore, it is important to have a stable behavior of setting own short- and long-term goals (Davis, 2007). In this research, H7 hypothesized that meeting short-term financial goals occurred before and influenced long-term financial goals of a wage employee.

Health Status

Health status could influence a wage employee’s spending behavior and ability to save for retirement. A worker is faced with two different types of health status: mental and physical health. Mental health is the well-being of the mind which is affected by social satisfaction, happiness, and stress. Physical health for Thai workers is the overall well-being of the body’s living organisms. Evidence showed that health status affected individual retirement. Good health of workers allowed workers to retire at an early age of 62 to 65 (Asch et al., 2005). The age of 62 to 65 is not the age where workers receive benefits from the health insurance or pension money (Asch et al., 2005). Therefore, workers will have an average working career of 40 years because the average age for an individual to start work is 20 years.

Mental well-being determines individuals’ health. Statistics show that after retirement many workers return to the work field not for income, but for well-being (Wise & Gruber, 2000). Retirement is related to mental preparation. Social activities could boost positive influences on retirement (Bernasek & Shwiff, 2001). Workers that are involved with social activities related to human interaction such as religious groups have a greater concern upon retirement planning (Do Vale et al., 2016). These workers tend to be single adults. Social activities create a link between health and retirement planning because social activities help reduce stress. Research proves that individuals that feel social life is important tend to plan for their retirement well (Asch et al., 2005).

Stable health means that workers can work hard constantly so that when they want to retire, they can do so. Therefore, it is important to ensure that an individual monitors his or her own health as it will benefit the future finance. The goal for health should be to be able to be healthy enough both physically and mentally so they can work every business day (May et al., 2004). A worker that can work every business day will have more savings than a worker with health disorders (Croon et al., 2005). This explains how a healthy worker can build up more savings because he or she can physically be capable of working for a long consistent period. However, an individual with health disorders would have so many sick leaves and many absences (Hansson et al., 1997). This suggests that a worker with sick leaves will receive less revenue and will have lower retirement saving (Asch et al., 2005). Workers with health disorders incur less net worth than those who stated no disease (Kim et al., 2015). Hence, this article hypothesized that an individual’s health status influenced his or her ability to contribute to the retirement fund (H8) and health status affected the ability to meet short-term financial goals (H9).

Career Status

Different career status associated with professional characteristics may affect individuals’ saving behavior differently. A qualitative longitudinal study was conducted on 15 Olympic athletes to assess their retirement process (Torregrosa et al., 2015). The results illustrate that five out of 15 athletes revealed unexpected difficulties and anxieties in the transition to their retirement. It is also suggested that athletes pursue dual careers and participate in retirement saving scheme to facilitate their retirement in the long term. In addition, a qualitative study regarding physician retirement planning reported that physicians retire around the age of 60 to 69. They retire early due to excessive workload and burnout but delay their retirement due to financial obligations (Silver et al., 2016).

The amount of knowledge and skills a wageworker has attained from academic degrees and experiences may affect a higher job status. The higher job position influences the higher income earned by a wageworker and, hence, more ability to save for retirement. Workers with higher education and larger income are more devoted and motivated to save for retirement (Lusardi & Mitchell, 2007a). A worker with a college degree will be able to retire earlier than one with a lower level of education. A study in Thailand revealed that skilled laborers with the level of education of a bachelor degree or higher with professional expertise were unintended to continue working after the retirement age, whereas unskilled ones with lower levels of education still demanded for jobs after retirement (Ketkaew, Wouwe, & Vichitthamaros, 2019). Moreover, labor market demand also affects an employee’s career status. Evidence also shows that individuals that have high job status and receive good social relationships or high monetary rewards plan less for retirement (Lusardi & Mitchell, 2007b). Therefore, this article proposed the following hypotheses. H10 assumed that career status influenced a worker’s wealth accumulation and H11 assumed that career status affected one’s contribution to retirement fund.

Proposed Model, Constructs, and Variables

Concerning the review of related literature and established hypotheses, we proposed the structural relationship among different variables as shown in Figure 4. A questionnaire was developed to meet the required information in the proposed model. The questions in this questionnaire were designed to collect both nominal and ordinal scale variables. Most of the ordinal scale variables followed the form of a five-point Likert-type scale, where 1 indicates the lowest degree and 5 signifies the highest degree, with the mid-point (3) representing the state of uncertainty or neutrality. The questionnaire was divided into two parts. The first part consisted of four questions related to the demographic information of wageworkers including basic demographic information such as age, educational level, income, and working sector (details reported in Table 2). The second part consisted of six constructs representing latent variables and their measures representing manifest variables. Table 1 reveals the variables and their measures. All the indicators for each construct were derived from the literature review.

Proposed model.

Variables, Scales, and Measures.

Source. Data adapted from authors (2019).

Method

Sampling and Data Collection

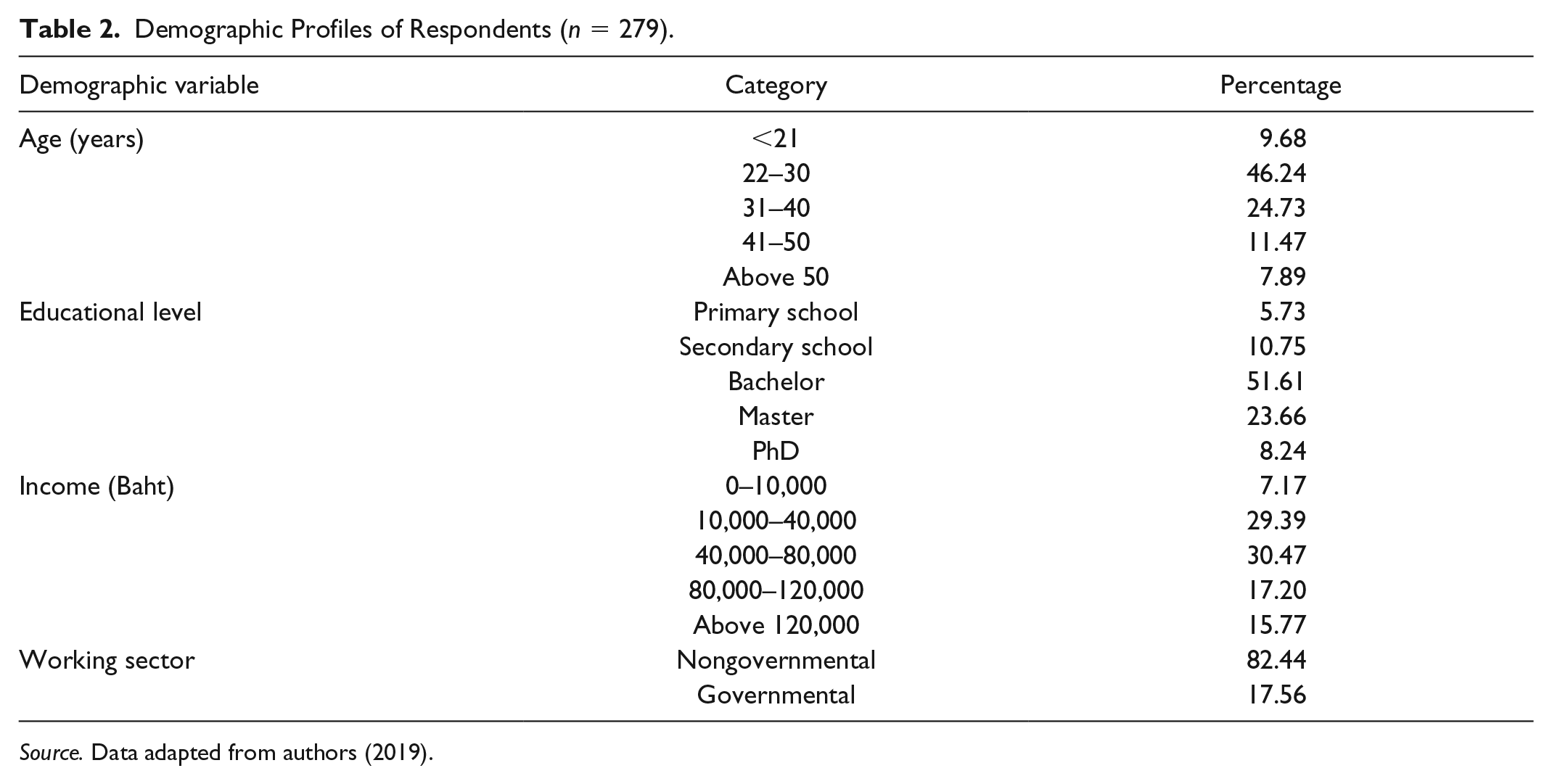

Data for this research were purposively gathered from respondents who were wageworkers residing in the Northeast of Thailand. It is recommended to have a minimum sample size of 200 for any SEM analysis (Kline, 2005; Weston & Gore, 2006). From the total population of 1.4 million wageworkers in the northeastern region (Annual Labor Statistics | Ministry of Labor, n.d.), we decided to employ the quota sampling approach to collect data from 300 wageworker respondents from the six most populated provinces in this region. Quota sampling is a nonprobabilistic sampling technique using which researchers can form a sample involving individuals that represent a population and are chosen according to traits (Hair et al., 2008), in this case selected provinces in the northeastern region. Trained surveyors were employed to collect the data based on a structured questionnaire through a face-to-face interview of 300 respondents from the six most populated provinces in the northeastern region (National Statistical Office of Thailand, n.d.), namely, Nakornratchasima, Ubonratchathani, Khon Kaen, Udonthani, Buriram, and Srisaket, with 50 respondents for each province. As compared with other 15 provinces in the region, these six selected provinces were the most urbanized. Typically, wageworkers in Thailand are mostly laborers working at factories or offices in the city areas. Choosing those six most urbanized provinces rather than other remote provinces would increase the possibility for the surveyors to approach targeted respondents more correctly and conveniently. Trained surveyors were assigned to collect data at the provincial landmarks, for instance, provincial parks, office building avenues, industrial estates, and shopping malls. All respondents were informed of the confidentiality agreement and the purpose of this research prior to data collection. Of the 300 wageworkers successfully interviewed, regardless of missing values and outliers, only the valid returned data from 279 participants were utilized. Table 2 describes demographic profiles of all the respondents. Note that, as for 9.68% in the age group below 21 years, most of these respondents decided not to continue studying but work to financially support themselves and families at a young age. From the interview, this was because their parents, grandparents, or relatives were unable to support them on education financially. Due to families’ financial burdens, these young wageworkers were required to work. In addition, as for the income group of the respondents, the classification of income groups was based on the existing salary scales of urban wageworkers in the northeastern region which range approximately from 10,000 to 150,000 Baht (researchers’ own observation in 2018). With regard to the observed salary scales, we decided to use a 1- to 5-point rating scale with an increment of 40,000 Baht starting from 0–10,000 Baht to above 120,000 Baht (see Table 2). Although statistics revealed that the Thailand’s 2018 average income per capita was around 27,000 Baht (Thailand Average Monthly Wages | 2019 | Data | Chart | Calendar | Forecast, n.d.), we decided to maintain the proposed income scales to demonstrate the fact that our quota sample was wageworkers from urban areas. Excluding rural workers with a lower income, the descriptive results of the income groups yielded the mode around 40,000 to 80,000 Baht.

Demographic Profiles of Respondents (n = 279).

Source. Data adapted from authors (2019).

Data Analysis

The study’s data analysis utilized the SEM approach. SEM encompasses such diverse statistical techniques as path analysis, confirmatory factor analysis (CFA), causal modeling with latent variables, and even analysis of variance and multiple linear regression. We performed SEM using Amos (Byrne, 2016). The SEM approach was applied to examine the model’s estimation in two steps (Anderson & Gerbing, 1988). Step 1 is to validate the outer CFA model to measure the relationship between each indicator and its variable, whether it is valid and reliable. This step involves the examination of goodness of fit (GOF), convergent validity, and discriminant validity. Step 2 is to examine the inner structural model to measure whether the full structure is reliable, consisting of the examination of GOF. Next, to analyze the moderating effect of age on the structural relationship suggested by the life-cycle hypothesis theory, we employed multigroup moderation analysis which would be Step 3 in this approach. This step performs a measurement invariance (MI) analysis using age as a moderator dividing the sample into two groups (below and above 30 years old) and then conducts z test for the difference between factor loadings of those two groups. Note that we decided to use the age of 30 as a cut-off for multigroup analysis because most Thai citizens start to save and accumulate long-term assets (e.g., properties and cars) around this age. The results of the statistical analysis are discussed in detail below.

Results and Discussion

There are two primary steps in performing a statistical test on SEM: measurement model (CFA) and structural model (Anderson & Gerbing, 1988).

Step 1: Measurement Model (CFA)

The measurement model was tested using CFA. In this respect, the model was assessed for internal consistency, reliability, convergent validity, and discriminant validity. CFA was performed by connecting all constructs with covariances (Hair et al., 1998). All constructs must involve their manifest variables before testing. Covariances among errors within the same construct were allowed to improve the GOF of the whole relationship.

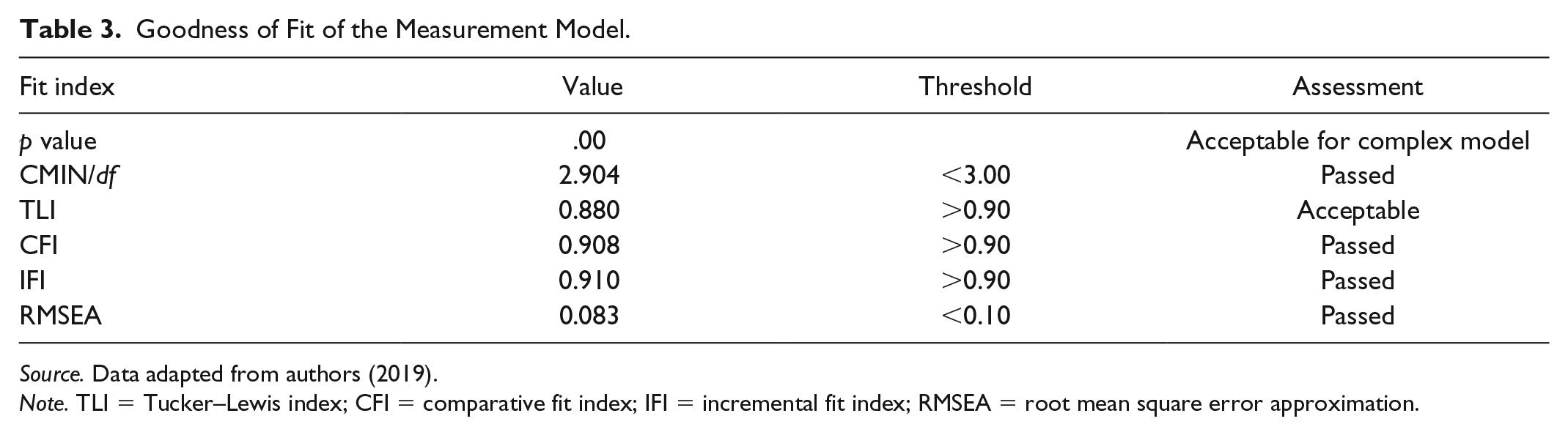

GOF

Table 3 illustrates the GOF measures and their thresholds. The results were quite acceptable in that the majority of the measures passed the suggested thresholds. CMIN/df (2.904), comparative fit index (CFI; 0.908), incremental fit index (IFI; 0.910), and root mean square error of approximation (RMSEA; 0.083) passed the designated thresholds, whereas Tucker–Lewis index (TLI; 0.880) was close to the threshold enough to be accepted in this respect.

Goodness of Fit of the Measurement Model.

Source. Data adapted from authors (2019).

Note. TLI = Tucker–Lewis index; CFI = comparative fit index; IFI = incremental fit index; RMSEA = root mean square error approximation.

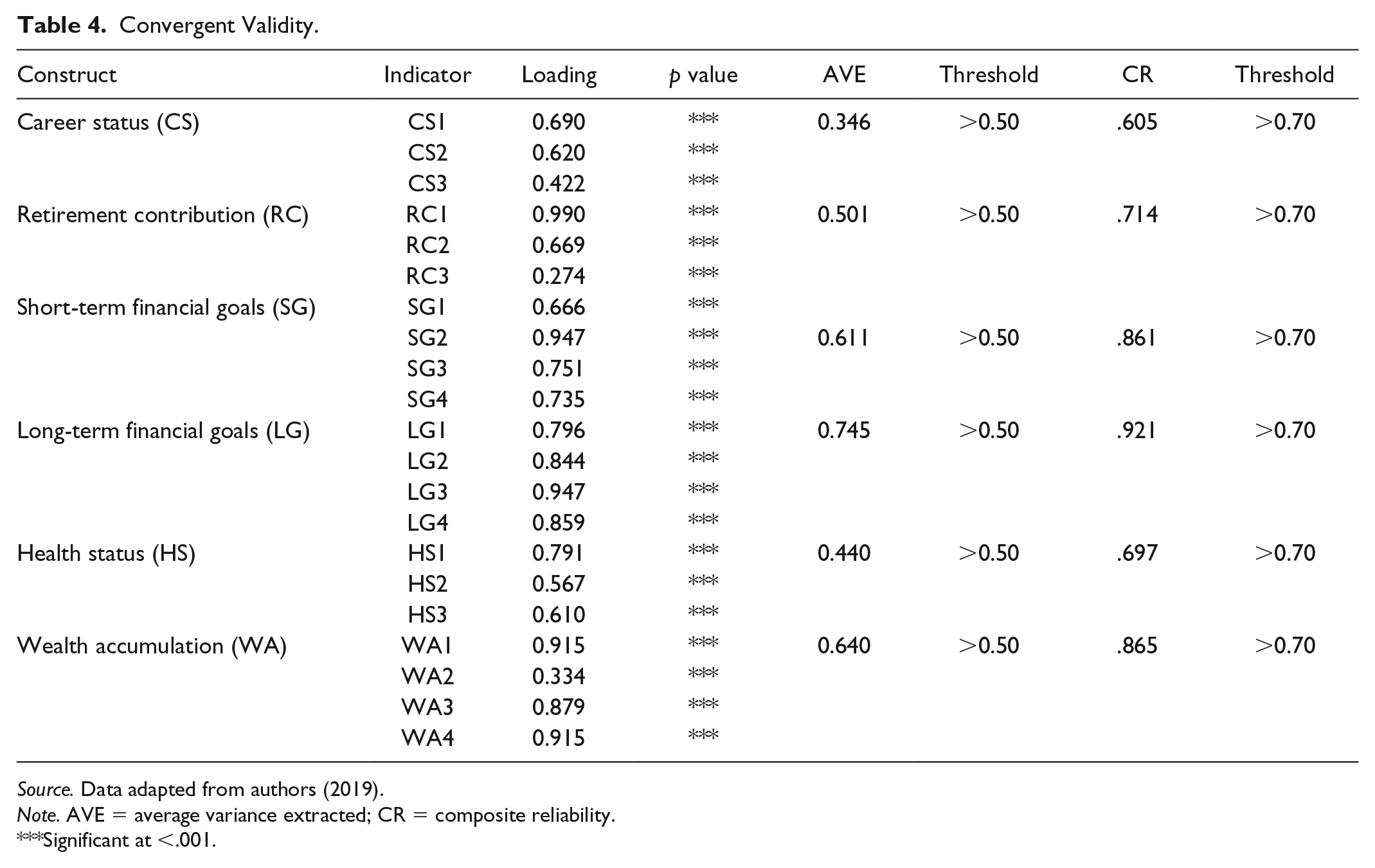

Convergent validity

This is examined by comparing the model results with the fit index thresholds. AVE stands for average variance extracted (Fornell & Larcker, 1981) and CR stands for composite reliability (Hair et al., 1998). According to Table 4, the suggested thresholds of the convergent validity measures and the calculated indicators are as follows.

Convergent Validity.

Source. Data adapted from authors (2019).

Note. AVE = average variance extracted; CR = composite reliability.

Significant at <.001.

Referring to Table 4, the RC (retirement contribution), SG (short-term financial goals), LG (long-term financial goals), and WA (wealth accumulation) constructs very well passed the convergent validity criteria when comparing the calculated measures with their thresholds. As for the HS (health status) construct, all the indicators were statistically significant at the <.001 level, but the AVE of 0.440 and the CR of .697 were slightly below the thresholds (AVE > 0.50 and CR > .700) but were still acceptable. As for the CS (career status) construct, although all the indicators were statistically significant at the <.001 level, both the AVE (0.346) and the CR (.605) performed poorly against the designated thresholds. However, this study decided to retain the CS construct in this analysis due to the relationship suggested by the literature review and proposed hypotheses. The p values less than .001 of all indicators (CS1, CS2, CS3; RC1, RC2, RC3; SG1, SG2, SG3, SG4; LG1, LG2, LG3, LG4; HS1, HS2, HS3; WA1, WA2, WA3, WA4) suggested that all the manifest variables belonged to their latent constructs (CS; RC; SG; LG; HS; WA) as claimed by the literature review.

Discriminant validity

Discriminant validity is the degree to which two or more conceptually similar constructs are different. This is examined by comparing the square root AVEs (on diagonal) with the correlations in the associated matrices (Fornell & Larcker, 1981). According to Table 5, all constructs passed this validity check.

Discriminant Validity.

Source. Data adapted from authors (2019).

Note. WA = wealth accumulation; HS = health status; LG = long-term financial goals; SG = short-term financial goals; CS = career status.

Step 2: Structural Model

Preliminary test results

After validating the measurement model, the structural model was developed by connecting all the constructs according to the proposed model in Figure 4. After all the variables were run according to the proposed model, the results revealed supports by the majority of GOF criteria as suggested by Hu and Bentler (1999). CMIN/df (2.567) was less than 3.00. TLI (0.901) was slightly greater than 0.90. CFI (0.923) and IFI (0.924) were both more than 0.90. RMSEA (0.075) was less than 0.10. The GOF indices were satisfied in this respect (Table 6).

Goodness of Fit of the Structural Model.

Source. Data adapted from authors (2019).

Note. TLI = Tucker–Lewis index; CFI = comparative fit index; IFI = incremental fit index; RMSEA = root mean square error approximation.

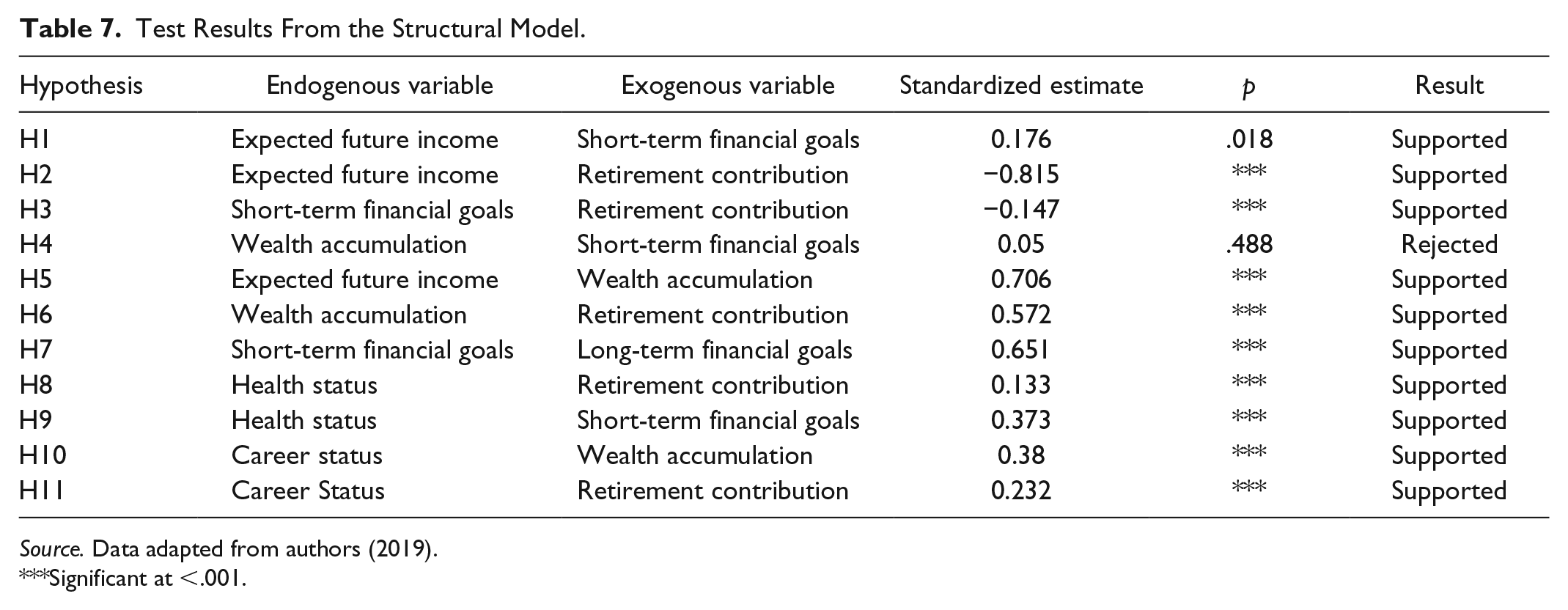

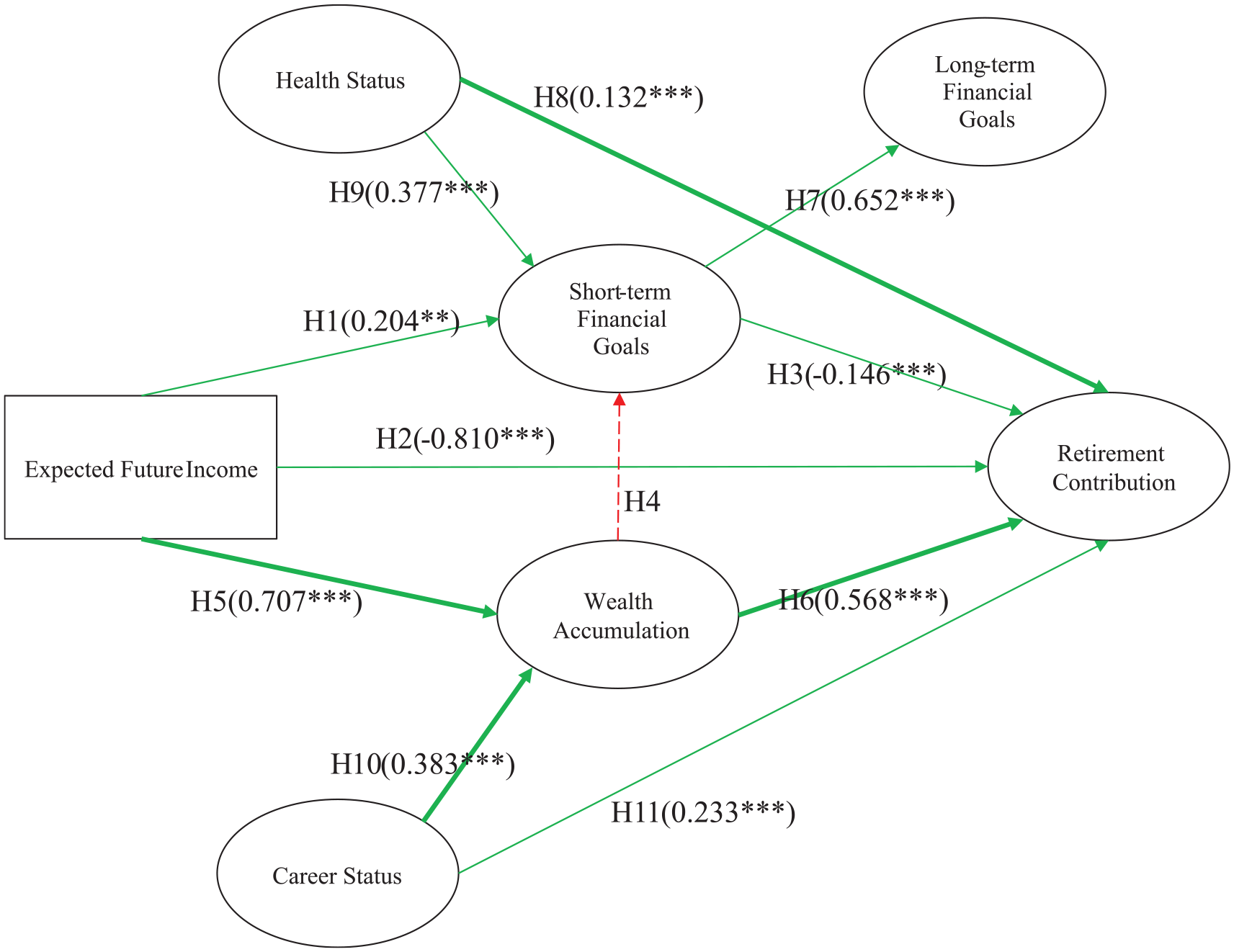

However, the test results from Table 7 demonstrated that the results were contradictory to the established hypotheses. The hypothesis test results supported H1 to H3 and H5 to H11 at the significance level of .05. Nonetheless, the test results only rejected H4, which stated that wealth accumulation influenced a wageworker’s short-term financial goals. This result were contradictory to the theory of life-cycle hypothesis proposed by Modigliani and Ando (1957), which implied that an individual’s short-term consumption was not dependent on his or her wealth. On the contrary, an individual’s short-term consumption solely depended on his or her expected future income, which was confirmed by the H1 test result. This implied that Thai wageworkers separated wealth from neither their short-term nor their long-term consumption. Instead, wealth accumulation positively related to a wageworker’s retirement contribution, which supported life-cycle hypothesis (Modigliani & Ando, 1957).

Test Results From the Structural Model.

Source. Data adapted from authors (2019).

Significant at <.001.

At this stage, the decision was to modify the model due to a highly insignificant statistical relationship between the WA construct and the SG construct (rejected H4). Therefore, H4 was omitted in the modified model. The modified structural model is shown in Figure 5.

The modified structural model.

Main test results and mediating analysis

The final structural model that resulted from omitting H4 is presented in this section. According to Table 8, the modified model demonstrated improved GOF indices in that CMIN/df decreased from 2.567 to 2.555 and TLI just slightly increased from 0.901 to 0.902. The improvement in GOF indices indicated that the new structural model could better represent the new relationship among the existing variables.

Goodness of Fit of the Modified Structural Model.

Source. Data adapted from authors (2019).

Note. TLI = Tucker–Lewis index; CFI = comparative fit index; IFI = incremental fit index; RMSEA = root mean square error approximation.

According to Table 9, the test results from the modified structural model supported H1 to H3 and H5 to H11 at the significance level of .001 or less, which indicated that the relationships among the constructs were highly significant in statistics. Let us begin our analysis by considering the following constructs: expected future income, short-term financial goals, wealth accumulation, and retirement contribution. Expected future income related positively to an individual’s short-term financial goals and wealth accumulation, which was consistent with the life-cycle hypothesis theory (Modigliani & Ando, 1957) and permanent income hypothesis theory (Friedman, 2018). The theories suggested that when an individual expected to earn some future income, he or she might choose to either spend or save based on expected future circumstances this individual might experience. Of course, saving was the amount left from an individual’s consumption. Short-term consumption negatively related to retirement contribution because pursuing short-term consumption might discourage an individual’s retirement contribution. For instance, spending money on a dinner at a luxurious restaurant would automatically reduce an individual’s ability to save for retirement because the money was already spent on expensive food rather than saving for a later life. On the contrary, expected future income positively influenced wealth accumulation with a very strong standardized loading of 0.707. In addition, wealth accumulation such as investment in financial assets, for example, stocks, bonds, mutual funds, and properties, extra income from a second job, and cash deposit would greatly enhance retirement contribution with a standardized factor loading of 0.568. Explicitly, mediated through wealth accumulation, this study found that retirement contribution could be greatly boosted when a wageworker spared a part of his or her income on wealth accumulation. The more devoted to wealth accumulation, the more retirement contribution could be enhanced. Moreover, this study also found that expected future income negatively influenced one’s ability to contribute to retirement with a negative factor loading of −0.810. This negative relationship explains a phenomenon that a worker’s time before retirement could be shorter every day when he becomes older, hence lowering his or her ability to contribute to retirement.

Test Results From the Modified Structural Model.

Source. Data adapted from authors (2019).

Significant at <.001.

This study also suggested that accomplishing short-term financial goals took place before and positively affected achieving long-term financial goals (Barsky et al., 1997; McGarry & Schoeni, 1995), with the standardized estimate of 0.652. Efficiently managing short-term finance such as meeting daily/weekly budget plan would allow an individual to plan for his or her long-term financial achievements such as owning a house, taking care of family, and other paying off long-term debts.

In addition, health status was found to influence both a wageworker’s retirement contribution (standardized estimate = 0.132) and short-term financial goals (standardized estimate = 0.377). As an employee was physically and mentally well (Asch et al., 2005), he or she might work and contribute to fulfill both retirement contribution and short-term financial goals. Empirical results from this study revealed that physical health performed more dominant roles than mental well-being in enhancing a worker’s retirement contributions.

Considering the last three constructs—career status, wealth accumulation, and retirement contribution—a mediating effect among these variables was also critical. This study demonstrated that career status positively influenced an individual’s ability to contribute to retirement with a standardized loading of 0.233. The result implied that the better the career, the more motivated a worker would save for retirement (Lusardi & Mitchell, 2007b). On the contrary, mediated through wealth accumulation such as investing in financial assets, earning extra income from a second job, and having cash deposit, better career status would greatly enhance an individual’s ability to contribute to his or her retirement, CS → WA standardized loading = 0.383 and WA → RC standardized loading = 0.568. For example, a medical doctor (good career) who invested in financial assets such as long-term equity funds (wealth accumulation) before contributing to his or her retirement would likely be more successful than another doctor who directly contributes to his or her retirement fund without investing in any financial assets.

In conclusion, wealth accumulation is the most crucial approach to enhance a wageworker’s retirement contribution. The source of money for a wageworker to accumulate wealth is mainly from his or her expected future income. Moreover, having good health status would allow a wageworker to work effectively and would enhance his or her ability to contribute to retirement.

Step 3: Multigroup Moderation Analysis

MI analysis

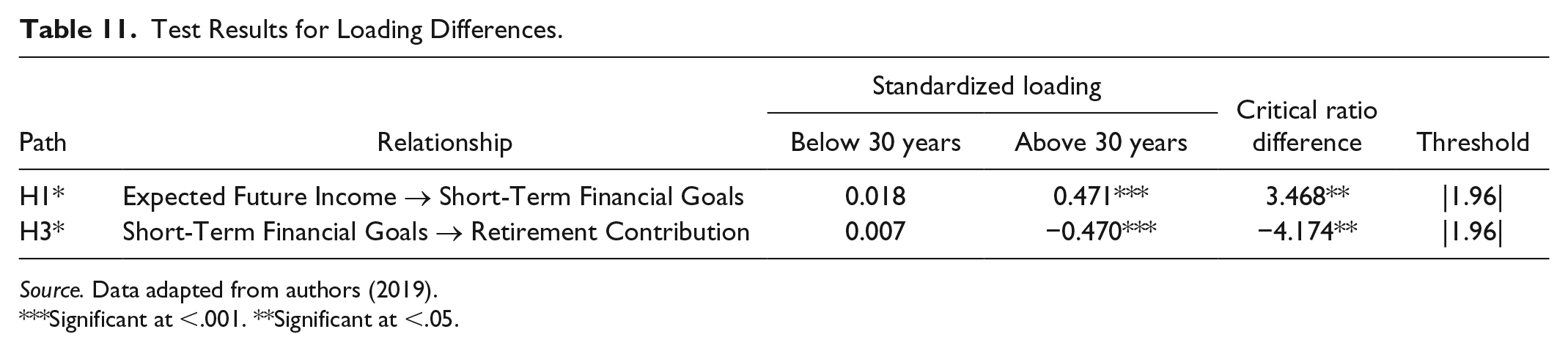

MI is the approach to examine whether the measurement model is not statistically different between two groups (Steenkamp & Baumgartner, 1998). In other words, MI helps us to assess whether respondents between the two groups (below and above 30 years old) understand the questions underlying the latent constructs from the questionnaire in the same way. Based on the CFA model, the MI method further performs the following: (a) establishing configural invariance (unconstrained model); (b) establishing metric invariance (equal factor loadings); and (c) establishing scalar invariance (equal intercepts). If only configural invariance and metric invariance are satisfied, partial MI is supported, allowing one to compare factor loadings between two groups. However, if partial MI holds and scalar invariance is accepted, full MI is established, which permits to compare factor loadings between the groups. Table 10 demonstrates the examination of MI successively conducted after the CFA model.

Measurement Invariance.

Source. Data adapted from authors (2019).

Note. CFI = comparative fit index; RMSEA = root mean square error approximation.

According to Table 10, although CFIs of the configural invariance and metric invariance models were slightly below the threshold of 0.90, their values (0.872 and 0.857) were high enough to be regarded as an acceptable fit (Browne & Cudeck, 1993). Considering the other fit indices that passed the stated thresholds, configural invariance and metric invariance were acceptable. However, scalar invariance was not supported when the value of CFI was too low (0.821). Therefore, partial MI was established, allowing us to perform further analysis in the next section.

z test for loading differences

In this section, we conducted a z test comparing the factor loadings between structural models (below and above 30 years) using the critical ratio difference (Byrne, 2016). This approach yields a list of critical ratios for the pairwise differences among the parameters estimated in the multigroup analysis. If the critical ratio value is greater than the absolute value of 1.96, then the factor loadings are significantly different between the two considered groups. According to Table 11, the pairs’ standardized loadings from both paths (H1 and H2) were significantly different (p value < .05). The results (H1 and H2) supported the life-cycle hypothesis theory suggested by Modigliani and Ando (1957). For Thai citizens with a young age (below 30), expected future income has no effect (loading = 0.018 and insignificant) in determining their current consumption (short-term financial goals). It is true that most young citizens in urban areas cannot satisfy their current consumption fully themselves due to the high cost of living but low income. These days, many early-career citizens in Thailand need to rely on their parents financially. Some may need to borrow from others. With the age above 30, an individual’s expected future income can positively influence his or her current consumption significantly (loading = 0.471, p value < .001). When career is increasingly more secure, an individual is able to satisfy his or her current consumption better. This is the time when people start accumulating long-term assets such as properties and plan for their families. Concerning retirement contribution, current consumption demonstrated no effect (loading = 0.007 and insignificant) on retirement contribution for the young-age citizens because they do not incur enough net income to save for retirement in the long term. However, for citizens with the age above 30, pursuing short-term financial goals would negatively affect their retirement contribution (loading = −0.470, p value < .001). This represents a trade-off between two activities. For instance, if an individual decides to spend on a vacation abroad, his or her ability to contribute to retirement saving will decline. The opposite is also true. On the contrary, if one chooses to save for retirement, he or she will have to trade an opportunity for a vacation abroad.

Test Results for Loading Differences.

Source. Data adapted from authors (2019).

Significant at <.001. **Significant at <.05.

The following section would elaborate further on these results where research implications of this study would be deliberated.

Research Implications

Derived from the research findings, the following recommendations were proposed to three main stakeholders including individual wageworkers, employers, and policymakers at the national level in Thailand.

As the findings from this research article clearly demonstrated that retirement contribution of a Thai wageworker was highly generated from wealth accumulation which resulted from expected future income and career status, wageworkers were recommended to continue improving their professional skills to improve their career status which would in turn help raise the expected future income in the long run. The more expected future income, the better capability an individual would accumulate wealth. It was recommended that wageworkers should accumulate wealth through different means, for instance, investment in financial assets, for example, stocks, bonds, mutual funds, and properties, extra income from a second job, or simply cash deposit. To accumulate wealth more efficiently, an individual worker was required to have financial knowledge regarding portfolio diversification and capital market. However, according to the statistics (Bank of America Private Bank, n.d.; The Stock Exchange of Thailand, n.d.), Thai people invest around 30% of their portfolios in capital markets, whereas in a developed country like United States people invest 76% (21% in bonds and 55% in stocks). The lack of diversity in investment portfolio allocation in Thailand is due to limited saving instrument alternatives available and insufficient financial knowledge about riskier financial instruments that potentially give better returns. Hence, the government and authorized bodies such as the Bank of Thailand (BOT) and the Stock Exchange of Thailand (SET) should create more investment alternatives and provide investment knowledge to the citizens.

Moreover, to enhance a worker’s career status, the government is expected to enforce minimum educational attainment at least at the vocational level to ensure that each individual is attached to professional skills ready to utilize at a workplace. Moreover, low-cost quality health service should be provided by the government. This is to ensure that workers do not fall into extreme financial burdens when experiencing severe health problems, which may obstruct their retirement contribution. Good health will allow workers to perform their work tasks efficiently until they retire. Following the three retirement pillars established by the World Bank, it is strongly recommended that Thai government should legislatively implement the second pillar—public mandated, privately managed, defined contribution system. This forced retirement contribution is expected to generate more sufficient retirement money for Thai wage employees as a whole.

Employers can contribute greatly to wageworkers’ successful retirement contribution. Employers can play their roles in creating sustainable retirement for their employees via creating retirement contribution schemes proper for different ages and the amount of money required by employees after retirement. As retirement contribution takes a strong effect starting at the age of 30, employers should provide retirement contribution schemes consisting of financial assets allowing wageworkers’ retirement portfolio to grow in the long term, for instance, stocks or property funds. In addition, career preparation and training should be conducted periodically to improve employees’ skills necessary to accomplish their work task (Phonthanukitithaworn et al., 2017). Furthermore, employers may support their workers’ health by different schemes. Mental well-being can be enhanced by creating a pleasant work environment, for instance, unpolluted and relaxed workplace, whereas physical well-being is through health benefit schemes such as fair health insurance and annual health checkup.

Research Limitations

This research has several limitations which also provide possible avenues for future research. First, although a comprehensive conceptual model was tested in this study, this research emphasizes on only wage employees. Hence, the results may be interpreted more meaningfully when using the multigroup model, for instance, government and nongovernment workers or even young and older workers. Second, sampling and data collection were limited to the northeastern region of Thailand, and hence this study provides a limited empirical application. Even though this study reports interesting results, caution must be exercised when trying to generalize them.

Conclusion

To summarize, this research was grounded on the life-cycle hypothesis theory pertaining that spending and saving behavior of an individual over lifetime depends on his or her expected future income. Incorporated with other latent variables such as health and career status, the aim of this article is to describe the act of how wageworkers in Thailand contribute to their retirement funds. It was found that an individual with positive expected future income and developing career status could greatly enhance his or her retirement contribution if mediated through adequate wealth accumulation schemes involving investing in financial assets and acquiring extra income from bonuses, an extra job, or owning a business, for instance. We found that the purpose of a wageworker to accumulate wealth was not to fulfill his or her short-term financial goals. Rather, an individual aimed to accumulation of wealth to enhance his or her financial contribution in the longer term. In addition, a wageworker with positive well-being both mentally and physically could demonstrate better capacity to contribute to retirement fund. Nonetheless, this study revealed a trade-off between current consumption and retirement contribution. It is true that pursuing current consumption would diminish an individual’s ability to contribute to his or her retirement fund, and vice versa. It was also found that age played a moderating role in the relationship between current consumption and retirement contribution. This study demonstrated that current consumption has a stronger trade-off effect on retirement contribution for older wageworkers than the younger ones. Thus, it is essential for authorities to promote wealth accumulation in several means because it is a way to promote a wageworker’s sustainable retirement in the long run.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The researchers would like to thank Khon Kaen University International College (KKUIC), Khon Kaen University (KKU), and the National Research Council of Thailand (NRCT) for financially supporting this research project.