Abstract

This study highlights the importance of political ties of top management on firm risk-taking preferences. This study divides the managerial powers into six categories and then tries to check the impact of those powers on firm risk-taking by considering internal and external input resources from 2011 to 2015. Interestingly, results show that firms with political ties are more risk-takers than nonpolitically connected firms. Managerial political ties empower them to control the internal and external resources of the firm and make them more authoritative to make investment decisions about risky projects. While expert power is the only source of authoritative decision-making power for managers regarding risk-taking in nonpolitically connected firms. These findings are of great importance for transitional economies, especially regarding Chinese unique business environment.

Introduction

The importance of having political ties and their impact on corporate decision making is a widely researched topic. Firms always enquire an easy access to financial resources to meet their needs for growth. The firm employs such managers who can facilitate firms to have easy access to external resources, that is, financial. However, having access to external financial resources is not easy especially in transition economies (Schweizer, Walker, & Zhang, 2017). It is well known in the literature that state-owned firms have more access to external resources than non-state-owned. Similarly, researchers have argued that firms with political ties have preferential access to external financial resources than firms with nonpolitical ties which increase their value and performance (Cull, Li, Sun, & Xu, 2015; Faccio, Masulis, & Mcconnell, 2006). Academicians have shown that firms are more interested in using bank loans rather than using other modes of finances as it mitigates agency problems (Hung, Wong, & Zhang, 2015; W. Liu & Atuahene-Gima, 2018).

However, it is needed to determine why do companies need to develop political ties and whether these connections are only utilizing to have easy access to financial resources? Establishing political ties provide not only external financial resources including bank loans and government subsidies but also an opportunity to such firms having access to implicit and explicit contracts (Dang, So, & Yan, 2018; Hung et al., 2015). Private entrepreneurs face lots of obstacles to run their businesses and become the victim of underdeveloped market conditions and legal systems, more government interventions and weaker investor protections (Faccio et al., 2006; Schweizer et al., 2017). So it is vital for privately owned firms in emerging economies like China to cultivate political ties to overcome such market failures and discrepancies. Therefore, managers in such private companies build up political ties with government officials (H. Li, Meng, Wang, & Zhou, 2008).

Managers play a very decisive role in corporate decision making. Private firms give preferences to hire such managers who have direct or indirect political ties (Wang & Chung, 2013). Managerial power theory argues that managers have more incentives if they have a controlling power in corporate decision makings. Their controlling power is mostly defined by various factors, like education, work experience, professional knowledge, number of shares, internal and external corporate links, and so on. However, excessive controlling power by managers can induce agency problems that can influence corporate decision-making behaviors. At the same time, resource dependence theory posits that firms may use managerial political ties as a strategic advantage and informal institutional arrangements to deal with environmental uncertainties that ultimately help these firms a considerable reduction in dependency on external environments in transition economies (Hillman, Withers, & Collins, 2009; Pfeffer, 1987). Jensen and Meckling (1976) propose a way to reduce opportunistic behavior and to solve agency problem through managerial equity incentives. Studies have shown that firms with founder managers (established of the firm) have different incentives than non-founder managers (F. Li & Srinivasan, 2011). So their political ties are expected differences in corporate decision making.

Studies have shown that firms with managerial political ties cannot only gain more investment opportunities but also increase their scales of investment and attain investment efficiency (Chen, Jin, & Dong, 2016; Faccio, Marchica, & Mura, 2016; Qian & Yeung, 2015; Xu & Xiao, 2014). Researchers have also shown that firms with more risk-taking behaviors gain more firm growth and sales revenue (John, Litov, & Yeung, 2008), and a significant increase in the market value of the firm (Xia, Ma, & Chen, 2015). However, researchers have argued that managerial willingness is the primary determinant of the firm’s risk-taking level (Khaw, Liao, Tripe, & Wongchoti, 2016). However, management has to consider internal governance mechanisms like ownership structure (Boubakri, Cosset, & Saffar, 2013b; W.-G. Li & Yu, 2012), managerial incentives (Choy, Lin, & Officer, 2014; Kempf, Ruenzi, & Thiele, 2009; X. Li & Zhang, 2014; J. Liu, Xiao Xi, Weng, & Wang, 2016), and governance characteristics (Cheng, Hsu, & Kung, 2015; Faccio, Marchica, & Mura, 2011) as managers have consider not only internal factors but also external market factors like environment uncertainties, corporate networks, religiosity, and creditor rights while considering a risky investment project (Caggese, 2012; Hilary & Hui, 2009; Jiang, Jiang, Kim, & Zhang, 2015; Jian-Li, 2009; Sun & Lu, 2017).

Studies have shown mixed results regarding firms with political ties and firm performance. Researchers have shown a significant increase in firm performance and overall market value with the attainment of political affiliations of top managers (Boubakri, Cosset, & Saffar, 2013a; Faccio et al., 2006; Hillman, 2005; Ling, Zhou, Liang, Song, & Zeng, 2016). Whereas some researchers have also shown that firms with politically affiliated firms have no link with firm performance (Wang & Chung, 2013). However, some researchers have suggested that firm performance is negatively associated with politically associated firms (Faccio, 2010; J. P. Fan, Wong, & Zhang, 2007; Fisman, 2001).

In this study, we have considered Chinese private firms on the following reasons. First, the Chinese economy provides unique market conditions where state intervention is quite massive. Chinese economy follows a bank-based financial system and dominates by state-owned banks where state-owned enterprises (SOEs) have preferential credit rights to deal with financial constraints (Bailey, Huang, & Yang, 2011; H. Li et al., 2008). However, private firms deal with substantial financial discrimination from the banking sector (Q. Liu, Tang, & Tian, 2013). Second, China is in a transition state to deploy privatization reforms, but the government still owns significant ownership rights in listed firms, which means the state can intervene in decision making of any privately listed firm at any time. So, private firms seek to build up links with government officials (H. Li et al., 2008). Therefore, such institutional settings can provide insightful evidence to contribute to the existing literature by examining the role of political ties on the association of managerial power with firm risk-taking.

This study has two significant contributions to the literature. First, this study examines private listed firms and comprehensively investigates how political ties and managerial power can influence risk-taking behavior. Most of the prior studies are limited to studying only one aspect of managerial power; however, this study considers a comprehensive set of managerial power. The findings add valuable information to the literature by showing that both political ties and managerial power are important factors influencing the risk-taking of Chinese firms. Second, this study considers one of the largest emerging markets, China, where political ties are one of the essential factors influencing corporate decisions. The results suggest that political ties are indeed one of the critical factors influencing the risk-taking behavior of Chinese firms. Most importantly, the findings illustrate that political connection can strengthen the effect of managerial power on risk-taking.

This study is unfolded as follows. The “Literature Review and Hypothesis Development” section provides a review of the literature and develops the hypotheses. The “Method” section clarifies data collection and describes the methodology. The “Empirical Analysis” section provides and discusses the empirical results, while in the “Conclusion” section, the conclusion is discussed and policy implications are highlighted. Finally, the references are provided.

Literature Review and Hypothesis Development

The resource-based theory postulates that a firm prevails in a competitive environment by acquiring tangible and intangible resources (Barney, 1991). The input of economic resources determines firm risk-taking while a lack of sufficient financial resources can induce investment failure. Researchers have acknowledged that in transitional economies, managerial ties with government officials is a relational asset to get support, bail out, and obtain key resources from the government (Boubakri, Cosset, & Saffar, 2012; Faccio et al., 2006). Most studies have provided a positive association of managerial, political linkage with firm performance (Boubakri et al., 2013a; Y. Luo & Chen, 1997; Peng & Luo, 2000). Based on social network theory and social capital theory, researchers have shown that political ties play a very crucial role in defining their competitive strategy in uncertain environments in China (Peng & Luo, 2000; W. Wu, Wu, Zhou, & Wu, 2012). Studies have also shown that politically connected firms are unable to add value under certain circumstances, even found a negative relationship with firm value in transition economies (H. Li et al., 2008; J. Wu, Li, & Li, 2013; You & Du, 2012). W. Li and Zhang (2010) argue that managers in foreign firms operating in China lack of creating political ties. Therefore, they have to rely on other external resources to improve firm performance.

Studies have pointed out several performance aspects regarding the firm’s political connectedness. It brings policy facilitations for politically connected firms to get preferential treatments like easy access to bank loans at lower interest rates, tax preferences, subsidies, and bailouts which let firms to pursue risky investment projects (Boubakri et al., 2012; Faccio et al., 2016). It also facilitates politically connected firms to diversifying their risk by having lower coordination costs regarding market entry which is usually controlled by the government (S. Luo, 2017). So, politically connected firms can control firm externalities by reducing uncertainties associated with investment projects that ultimately encourage such firms to engage in higher risk-taking (Z. Fan, Peng, & Liu, 2016). So it can be hypothesized as follows:

The importance of corporate governance mechanisms and managerial characteristics regarding firm performance are well documented. Studies have shown that the board of director’s characteristics determine the firm’s propensity level (Palmer & Wiseman, 1999). Academicians have argued about various influencing factors regarding firm risk-taking in theoretical perspective, mainly behavioral decision theory, resource dependence theory, and agency theory (Bromiley, 1991; Larraza-Kintana, Wiseman, Gomez-Mejia, & Welbourne, 2007; Wright, Kroll, Krug, & Pettus, 2007). These theories have provided essential support to researchers for examining the influence of top management on the firm’s propensity for taking risk.

Managerial power influences corporate decision makings in various ways. Shareholders try to control managerial powers through ownership concentrations, and they expect that the managers can align their goals with shareholders. However, researchers have shown that whether the managers with shareholdings will have more powers and pay more attention for a long-term and sustainable firm growth (Bebchuk, Fried, & Walker, 2004; Boubakri et al., 2013a). So managers are willing to make investments on risky projects by focusing on long-term development. As explained by Finkelstein (1992), management power is the ability of a management team to do its own will. Bebchuk et al.’s (2004) theory of managerial power posits that agency problem is the main issue as gaining more power can induce opportunistic behaviors in managers, but it can be controlled through the optimal contracting approach. Finkelstein (1992) explains that managerial power is a strategic choice to compete with other players in the market and to deal with market uncertainty as managing internal and external uncertainties give power to managers. He further argues about the role of management in firm performance by defining their roles and importance into four categories including structural power, expert power, prestige power, and ownership power. He explains that structural power comes from the organization structure and hierarchical authorities where the CEO has higher power than other management personnel so as the other managers to their subordinates. Behavioral decision theory posits that their personality characteristics such as reputation, education, gender, and “Hot Hands” as mentioned by Finkelstein (1992) determine the level of the firm’s risk-taking. At the same time, resource dependence theory explains that management with higher structural powers has more access and greater control to the resources than their subordinates, which encourages them to take more risks. So managers with political ties give them more access to external resources which not only give them a strategic competitive edge on their rivals but also support their risk-taking behaviors (Peng & Luo, 2000). Whereas ownership power controls the agency problem between managers and shareholders, to align their objectives. However, managers with significant shareholdings have more ownership power. Researchers have shown that if the manager/CEO is also the founder of the firm or related to the founder will empower them to influence decision making as such kind of power can reduce internal uncertainties (Schweizer et al., 2017). It is well documented that corporate risk-taking depends on the access to input resources, and political ties help firms to avail those resources more than their capacity. So, if such managers/CEOs have political ties then can also reduce external uncertainties (Schweizer et al., 2017).

Moreover, such managers with political ties are more entrusted by shareholders as there will be less risk of investment failure. Even, in case of any environmental or financial constraints, private firms with political ties will be subsidized/bailed out by the government to promote regional growth (Faccio et al., 2006; J. P. Fan et al., 2007; Hu & Shi, 2008). So managerial power with external and internal access to input resources can mitigate investment failures and can choose risky projects.

However, dealing with external environmental uncertainties regarding government, competitors, customers, and suppliers is one of the biggest challenges for the managers as it can hamper organizational growth (Porter, 1980; Thomas, Litschert, & Ramaswamy, 1991). So, managerial political ties play an essential role in dealing with such contingencies and empower them within the organization as management power is an internal governance mechanism while external connections (formal and informal) are the external capital for the firms. Researchers have shown that firms with more external capital especially policy resources through political ties are more prone to take risky projects (Srivastava, Moser, & Hartmann, 2018; You & Du, 2012).

Based on the above discussion, we can propose our hypothesis:

Method

Sample Selection

This study has taken data of Chinese private listed firms from the China Stock Market and Accounting Research (CSMAR) database, the Council of European Energy Regulators (CEER) database, and Compustat IQ. As we are determining the impact of political ties on firm risk-taking, we have excluded state-owned firms (SOEs) from our sample and only considered private listed firms.

Furthermore, we also have excluded firms marked as ST (special treatment) and PT (particular transfer) to avoid financial and risk-taking abnormalities as these firms show a continuous loss or change in their ownership status during the past 2 years. We have also excluded those firms that show more than two missing values for managerial power, political ties, and other control variables. Based on these screening criteria, we get 1,507 firm-year observations for the period of 2011–2015. For potential outliers, we have winsorized the data at 1% level. Year and industry effects are controlled.

Dependent Variable

Firm risk-taking is our dependent variable. Following Coles, Daniel, and Naveen (2006) and Low (2009), we have taken the daily stock return to calculate firm risk-taking.

Independent Variables

Managerial power

We have taken firm and manager’s characteristics while devising managerial power by following Finkelstein (1992); Finkelstein, Hambrick, and Cannella (2009); and Bebchuk et al. (2004). Furthermore, we have divided managerial power into six categories which include ownership power, prestige power and expert power, structure power, director supervision power, and shareholder supervision power. Their definitions are shown in Table 1.

Variables Definitions.

Political connection

Following Faccio et al. (2006) and Boubakri et al. (2013a), we have taken the affiliation of any member of top management with officials of central/local government or served as the official of central/local government in the past. Political connection data are taken from the personal profiles of top management (CEO, directors/managers) from CSMAR.

Control Variables

This study has taken various control variables based on literature. Following Cheng et al. (2015), Faccio et al. (2011), Faccio et al. (2016), and John et al. (2008), we have included board size, board independence, CEO compensation, managerial age, gender, firm growth, leverage, Tobin-Q, firm’s size, firm’s age, and turnover. Their definitions are explained in Table 1.

Model Design

The following regression models were employed to test the hypotheses.

Model 1 study the impact of political connection on the level of corporate risk-taking as follows:

where RTit represents the standard deviation of the daily stock returns. PCit is the dummy variable for the political association which is “1” if a firm has a political connection and “0” otherwise. Furthermore, CVit represents the control variable (board size, board independence, CEO compensation, managerial age, gender, firm growth, leverage, Tobin-Q, firm’s size, firm’s age, and turnover). We have controlled industry and year effects, and εit is the standard error.

Models 2 and 3 are formulated to investigate the impact of managerial power on the corporate risk-taking level and the importance of political connectedness, respectively.

where RTit represents the standard deviation of the daily stock returns. PCit is the dummy variable for the political association which is “1” if a firm has a political connection and “0” otherwise. Furthermore, MPit represents the different types of managerial power (ownership power, prestige power and expert power, structure power, director supervision power, and shareholder supervision power), PCit × MPit is the interaction term of political connectedness with different types of managerial powers, CVit represents the control variable (board size, board independence, CEO compensation, managerial age, gender, firm growth, leverage, Tobin-Q, firm’s size, firm’s age, and turnover). We have controlled industry and year effects, and εit is the standard error. We considered the fixed effects technique as appropriate after applying Hausman specification test (p = 0.000; Baltagi, 2005) by following similar studies (Bayrakdaroğlu, Ege, & Yazici, 2013; Iqbal, Ahsan, & Zhang, 2016; Sheikh & Qureshi, 2014).

Empirical Analysis

Descriptive Statistics

Descriptive statistics are shown in Table 2. It shows that the standard deviation of daily stock returns (Risk-Taking) has an average value of 0.029, with a minimum value of 0.013 and maximum of 0.076. It shows that firms vary in their risk-taking, significantly. Political ties show that more than 70% of private firms are politically connected.

Descriptive Statistics.

Note. See Table 1 for variable definitions.

Significance at 10%. **Significance at 5%. ***Significance at 1%.

For managerial power, ownership power shows that average shareholding ratio of a CEO in a firm is 3.3%, with a minimum of 0% and a maximum of up to 52%. Prestige power shows an average of 0.094. It shows that 9.4% of firms have CEOs who are also the founder of the firms. Expert power shows that the average working experience of a CEO is almost 5 years. While structure power shows an average value of 0.285, it indicates that 28.5% of the sample firms’ chairman and CEO are the same person. The director supervision power shows that average of 0.324. The shareholder supervision power shows that on average the largest shareholder has 3.14 times more ownership than the sum of second to the 10th largest shareholder in Chinese private firms.

For control variables, the mean value of director on board shows an average of nine members while independent directors on board show an average of three members on the board of directors of the firm. Managerial age is showing an average of 48 years. CEO compensation indicates an average of 13 times than other subordinates. Gender shows that there are more than 20% of the supervisors are males. Firm operating income is showing an average of 40% annual increase while 45.7% of the firms are on average shows that debt financing is still the primary mode of an external source. Tobin-Q shows an average of 2 times. The turnover ratio shows that Chinese private firms on average are 73 times the average total assets. Firm size is showing an increase of 22 times annually on average while the firm’s age shows an average of 18 years. The mean of the turnover ratio shows that on average, the operating income of Chinese companies is 72.580 times greater than their average total assets.

Regression Analysis

Political ties and risk-taking

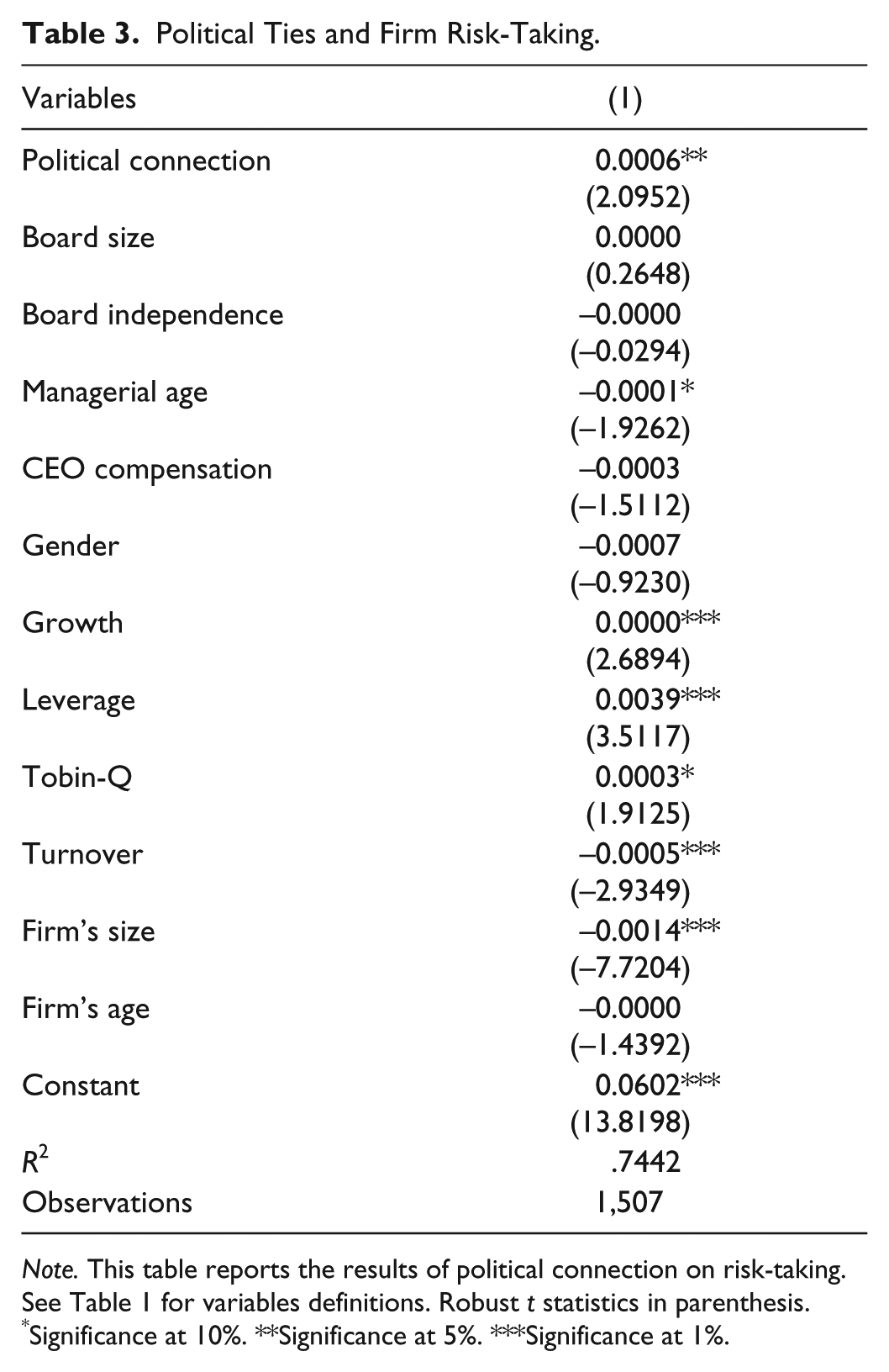

Regression results of political ties and control variables with risk-taking are shown in Table 3. After controlling management characteristics, firm characteristics, industry, and time effect to risk exposure, it shows that political ties are positively significantly correlated with risk-taking. It proves our Hypothesis 1 that politically connected firms are more inclined to take risks.

Political Ties and Firm Risk-Taking.

Note. This table reports the results of political connection on risk-taking. See Table 1 for variables definitions. Robust t statistics in parenthesis.

Significance at 10%. **Significance at 5%. ***Significance at 1%.

Furthermore, control variables show that firm growth, firm leverage ratio, and Tobin-Q are positively significantly associated with risk-taking, whereas managerial age, turnover, and firm’s size are negatively significantly correlated with firm risk-taking. It implies that firms with professional managers and lower operating income as well as bigger firms are not risk takers while firms with high growth, higher market value, and high leverage ratio are more risk takers. Board size, independent directors, CEO compensation, gender, and firm’s age are showing an insignificant relationship with firm risk-taking.

Managerial power and risk-taking

The relationship of managerial power with firm risk-taking is shown in Table 4. These results support our Hypothesis 2. Ownership power, prestige power, expert power, and structure power are positively significantly associated with firm risk-taking. It implies that CEO characteristics are determinantal of firm risk-taking such as firms with more CEO shareholding ratio, CEO considers both its own short-term and long-term interests while making investment decisions. CEO as the founder of the firm is more able to use professional knowledge to grasp the expected return on investment projects and risk accurately. CEO duality and CEO years of service also determine the firm’s risk-taking behavior. This study shows that the level of corporate risk exposure is significant and positively related to the experience of the CEO. It indicates that a CEO also designated as the chairman at the same time and with a longer tenure in Chinese private firms are considered more authoritative and experienced to deal with risky events and emergencies, and thus has a lower probability of investment failure. Therefore, they may be more inclined to undertake risky projects.

Managerial Power and Firm Risk-Taking.

Note. This table reports the results of managerial power on risk-taking. See Table 1 for variable definitions. Robust t statistics in parenthesis.

Significance at 10%. **Significance at 5%. ***Significance at 1%.

While board-related characteristics regarding supervision over managers also determine firm risk-taking behavior. This study shows that shareholder supervision power is negatively significantly correlated with firm risk-taking. It indicates that the largest shareholder with a lower ratio of ownership will have less controlling power and consequently, less management concern. Therefore, management will ultimately have greater management power and be more inclined to engage in highly risky investments. Possibly, high management power makes them risk-averse. Whereas director supervision power is showing a negative but insignificant relationship with firm risk-taking. It indicates that having fewer members on the board of directors provides more power to management, making it risk takers.

Political ties, managerial power, and risk-taking

Table 5 shows the results of the association of managerial power with firm risk-taking by dividing the sample into politically and nonpolitically connected firms. It shows that politically connected firms support the managers to take risks than nonpolitically connected firms, which supports our Hypothesis 3. Our results in Table 5 from column 1 to 6 show that the managerial ownership powers, prestige powers, and structure powers regarding firm risk-taking are strengthened by the managerial, political ties. Shareholder supervision power is showing a significant negative association with risk-taking in politically connected firms. At the same time, expert power and director supervision power are showing irrelevant results, but their coefficients are in accordance with prior literature. As mentioned by Dang et al. (2018), You and Du (2012), and Adams, Almeida, and Ferreira (2005), such CEO characteristics empower management to deal with external uncertainties and take risky projects.

Political Empowerment and Firm Risk-Taking.

Note. This table reports the results of political connection, managerial power, and risk-taking. See Table 1 for variable definitions. Robust t statistics in parenthesis.

Significance at 10%. **Significance at 5%. ***Significance at 1%.

While columns 7 to 12 show results of managerial power association with risk-taking for nonpolitically connected firms. It shows that only managers with expert powers are risk takers in nonpolitically Chinese private listed firms but other variables of managerial power. These results show that nonpolitically connected firms are fewer risk takers who are confirming prior studies (Boubakri et al., 2013a; Faccio et al., 2016).

Robustness test

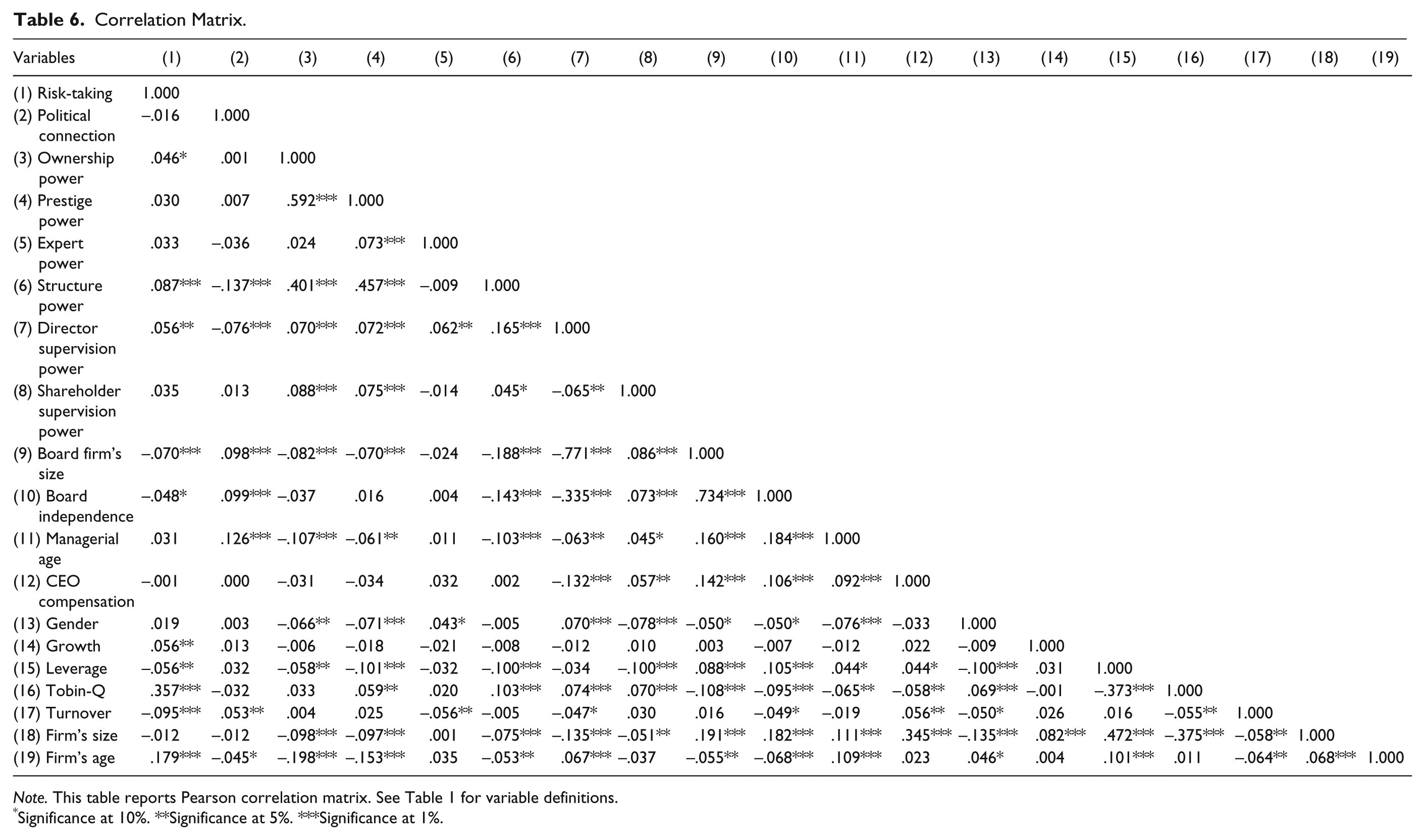

We have used six variables for managerial power, 11 control variables, and political association as a categorical variable. For this large number of variables, autocorrelation and multicollinearity may have been an issue. The results of the variation inflation factor (VIF) provide the highest VIF is less than 10. As such, multicollinearity is not an issue (Nachane, 2006; Ott & Longnecker, 2001).

Moreover, Pearson autocorrelation (Table 6) values are also in a reasonable range. Furthermore, to ensure the validity and robustness of the results, we performed post-estimation tests including the modified Wald test for group-wise heteroskedasticity in the fixed-effect regression model and the Wooldridge test for autocorrelation in the panel data. As a remedy for autocorrelation, we used robust standard errors adjusted for heteroskedasticity and clustered the robust standard errors adjusted for clusters in panels (firms).

Correlation Matrix.

Note. This table reports Pearson correlation matrix. See Table 1 for variable definitions.

Significance at 10%. **Significance at 5%. ***Significance at 1%.

Conclusion

This study examined that impact of managerial power and their political ties on firm risking-taking tendencies on Chinese private listed firms for the period of 2011-2015. The results of the study show that managerial powers and their political ties both impact firm risk-taking significantly, in China. Specific managerial characteristics highlight the importance of political ties regarding firm risk-taking.

Our results indicate that CEO ownership in the firm is one of the crucial determinants for firm risk-taking in politically connected firms. Politically connected CEOs with high shareholding ownership give them more power to control firm internal and external resources to make any investment decisions. Similarly, if the chairman of the board and the CEO are also the same person, then such firms are also aggressive in their risk-taking behaviors, especially in politically connected firms. Moreover, if the CEO has more working experience and is also the founder of the firm, such firms are more inclined to take risky projects in politically connected firms. Such CEOs can control their external resources through their political ties and not only are entrusted by shareholders (Boubakri et al., 2013a) but also considered more authoritative and experienced to deal with risky events and emergencies, and thus, has a lower probability of investment failure.

Furthermore, board characteristics regarding monitoring the performance of the managers also determine the firm risk-taking behaviors. Our results show that the number of directors on board and shareholding ratio of the largest shareholder in the firm also plays a significant role in investment decision making. Firms with more directors on board are risk averse as the management power is quite dispersed which let managers to control their investment decision making especially about risky projects. Similarly, it is found that higher shareholding ratio of the largest shareholder in the firm gives him more controlling rights which ultimately lower the firm risk-taking (Cheng et al., 2015). This shows that large shareholders in a company act as supervisors, restricting management from taking additional risk.

This study has used data of Chinese private listed firms with certain limitations regarding the collection of data and literature about the unique Chinese environment. The study period is quite limited. A more extended period can be helpful in the generalizability of the study in the field. Moreover, the addition of managerial power variables can deepen the understanding of the study.

The results of this article imply that experienced managers are more likely to recognize their potential during project decision-making and may be more proactive in capturing high-risk, high-return investment projects. At the same time, political affiliations enhance management’s willingness to invest in riskier projects, and an organization’s power structure affects corporate risk-taking. Therefore, enterprises should rationally allocate and actively supervise the management power structure and efficiently use the policy resources and investment opportunities provided through political ties.

Footnotes

Acknowledgements

We are very thankful to Khalil Jebran, PhD candidate, for his timely help to improve and deal with the issues regarding this study. We are also very thankful to the editorial team for their encouragement and the anonymous reviewers for their insightful valuable comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.