Abstract

As an effective means in fighting poverty, microfinance experienced an unprecedented growth in many emerging economies followed by stagnation and deep crisis, due to an inherent paradox in the fundamental missions of microfinance industry: serving the poor and making profits to maintain institutional sustainability. This article explored sustainable mechanisms in balancing the paradoxical missions of microfinance institutions in the post-crisis era through an in-depth case study on RSL, a microfinance institution in China. The managerial principles and framework of RSL revealed in this article could guide indigenous microfinance companies to deal with the paradoxical nature of their missions and build a sustainable path in poverty alleviation.

Keywords

Introduction

Lacking access to credit is one of the main reasons why the poor in developing countries remains poor (Coleman, 1999; Fletschner, 2009; Karnani, 2007). Microfinance, lending small amounts of working-capital to the poor who have traditionally lacked access to credit, is one of the most sound and effective anti-poverty strategies (Bakhtiari, 2011; Copestake, 2007). In some developing countries in Asia and Latin America, microfinance programs were put into practice as a major means for poverty alleviation, and the success of the microfinance has been broadly discussed in the literature (Khandker, 2005; Montgomery & Weiss, 2011; Patten & Johnston, 2001).

However, in recent years, it has been criticized that many microfinance institutions (MFIs) have abandoned their original social mission of poverty alleviation, while increasingly focused on earning profit or even became purely commercial institutions (Hishigsuren, 2007; McIntosh & Wydick, 2005). Microfinance was shifting from poverty-alleviation to profit-maximization due to excessive commercialization (Woller, 2002), which was identified as a mission drift by Yunus (2011). Gradually, a microfinance crisis was triggered in many developing countries in recent years as borrowers no longer believe that the MFIs are alleviating them out of poverty, but instead, exploiting them and often making them much poorer. Therefore, more and more bankrupted and quasi-bankrupted borrowers stopped making repayments since they did not worry to lose more from their already poorest conditions (Dowla, 2012; Polgreen & Bajaj, 2010; Saxena, 2014). The most recent crisis was erupted in an Indian state of Andhra Pradesh in 2010 when excessive interest rates of “50% -100%” charged by MFIs generated widespread over-indebtedness of the poor borrowers and caused about 30 to 60 cases (or even more) of suicides which badly tarnished the microfinance industry in India as well as globally (Ashta, Khan, & Otto, 2015; Haldar & Stiglitz, 2014).

Despite an emerging body of researches addressing microfinance crisis from many different perspectives, there is still a considerable theoretical gap in the microfinance literature regarding the fundamental reason of the crisis—the paradoxical nature of the dual missions of MFIs (Caserta, Monteleone, & Reito, 2018; Okoye, Okoye, Siwale, & Siwale, 2017). Researchers agree that MFIs have dual missions and many MFIs had abandoned their original social mission of poverty alleviation and excessively focused on financial performance (Mia & Lee, 2017; Xu, Copestake, & Peng, 2016). In general, the prominent symptoms of mission drift are high interest rates and profitability-orientation (Lopatta, Tchikov, Jaeschke, & Lodhia, 2017; Taylor, 2011), adverse selection of solidarity lending (Bhole & Ogden, 2010; Jackson, 2016), and failed social mission (Freedman & Click, 2006; Ullah & Routray, 2007). However, very little effort has been made in the existing literature to answer whether the paradoxical nature of the dual missions of MFIs could be handled or balanced and how to balance the two conflicting missions of MFIs. Therefore, whether microfinance is really an effective tool for fighting poverty is increasingly being questioned. It is this gap that shapes the main focus and contributions of this article. Our research aims to fill this theoretical gap by exploring mechanisms in balancing the paradoxical missions of MFIs in the post-crisis era through an in-depth case study on RSL, an MFI in China. We argue that microfinance is still one of the most important tools for lifting people out of poverty. It is possible that MFIs could find a right balance between the dual missions and rebuild a sustainable path in the post-crisis era. The findings from this study not only contribute to the emerging literature on microfinance but are also helpful to managers of MFIs who are constantly searching for ways to improve the institutional sustainability.

This article is structured as follows: we will critically examine three prototypical models of microfinance by analyzing the symptoms and root cause of the mission drift in MFIs. We then propose an in-depth case study of Rishenglong Ltd. (RSL), an MFI in Pingyao, China, by analyzing RSL’s operation characteristics and discuss some insights on how it balances the social mission and financial mission in its development and how it finds a sustainable path in the post-crisis era. We conclude our article by discussing how our findings could guide indigenous microfinance companies to deal with the paradoxical nature of their missions and build a sustainable path in poverty alleviation.

Paradoxical Missions of MFIs—A Critical Review on Bangladesh, Bolivia, and Indonesia Models

It is generally believed Bangladesh, Bolivia, and Indonesia models are three prototypical models of microfinance industry (Dowla, 2012; Maclean, 2010; Revindo & Gan, 2017). Many emerging economies largely adopted the operational and managerial principles from these three models when they build and structure their microfinance industry (Khandker, 2005; Montgomery & Weiss, 2011; Patten & Johnston, 2001). In this section, we will critically review these three models by focusing on the paradoxical missions and the resulting mission drift rooted in these models.

A Brief Introduction of the Three Models

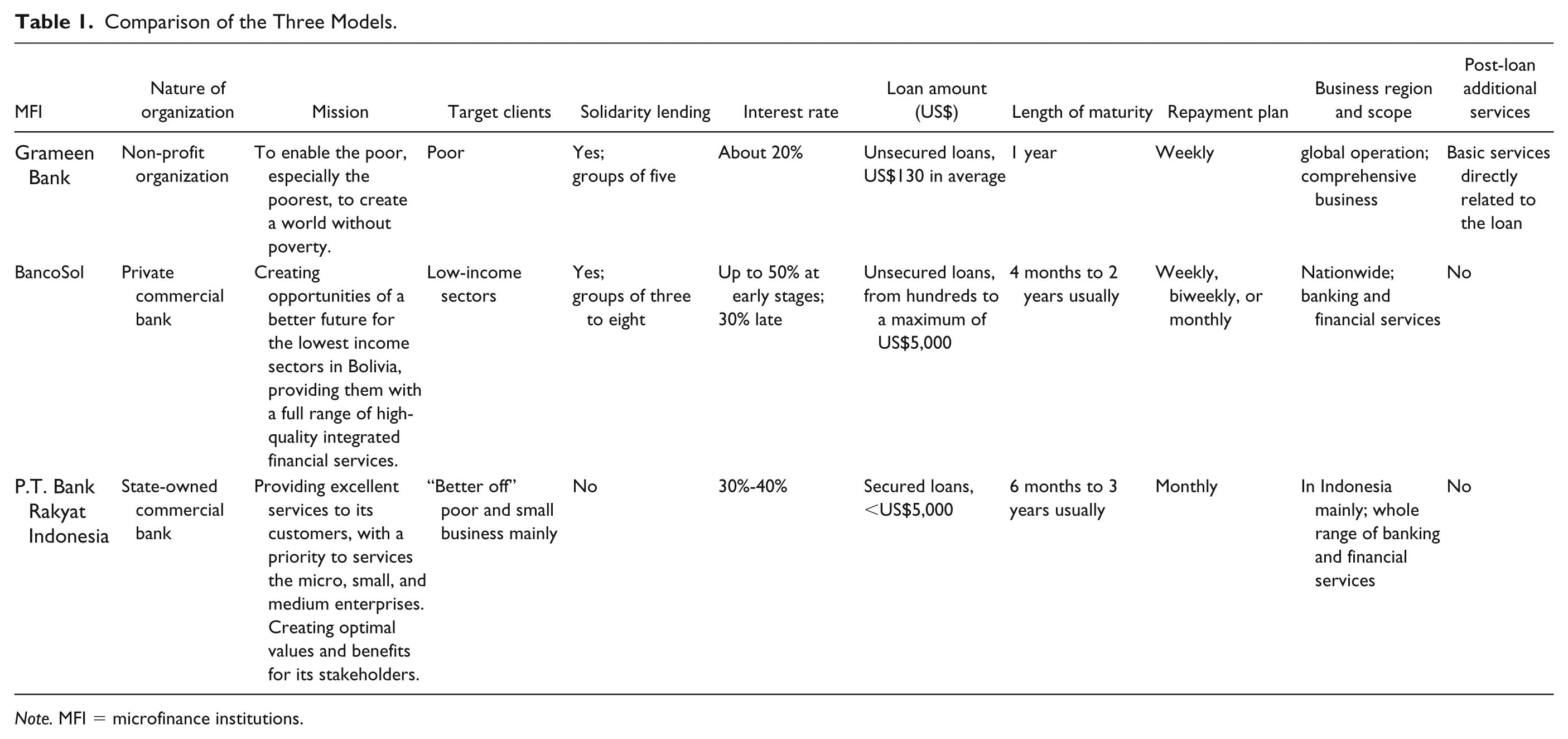

Grameen Bank (GB) was founded in Bangladesh as a microfinance corporation and community development bank in 1983 with the original mission of alleviating poverty. Based on mutual trust, GB offered small loans to poor people at about 20% nominal interest rate. GB designed solidarity lending to reduce defaults whereby loans are issued to individuals in groups of five who collectively guarantee the repayment of each other’s loans. Although GB had claimed a big success in its mission of alleviating poverty, researchers are getting more and more skeptical. For example, Yunus claimed their repayment rate has always been at a very high level of “over 98%,” some researchers pointed out that in fact GB has been in serious trouble in 1999 because of massive defaults (Dowla, 2012; Tesfatsion, 2010). To overcome these problems, GB gradually commercialized itself that makes it more concerned about profits. It was accused of using exploitative lending techniques that made the poor much poorer eventually (Hudon & Sandberg, 2013). After three decades’ development, GB has developed nowadays into a large international comprehensive business group covering microfinance, telecom, trust and insurance, agriculture, fisheries and animal farming, renewable energy technologies, education, health care, and so on. Clearly, today’s GB is no longer an MFI.

BancoSol in Bolivia started its operations as a nonprofit MFI (PRODEM) in 1986 and transformed into a licensed for-profit commercial bank dedicated exclusively in microfinance since 1992, whose aim was to provide high-quality financial services for the low-income sectors. Similar to GB’s solidarity lending, BancoSol issues unsecured loans, usually hundreds dollar, to members in a group, and all group members remain jointly liable for the repayment of the loans as a whole. Due to Bolivia’s underdeveloped financial markets with inherently high default risk (Maclean, 2010), BancoSol charged a high interest rate up to about 50% to ensure its ability to cover the high costs (Barboza & Trejos, 2009; Schicks, 2007). It has been argued that BancoSol put poverty alleviation secondary compared with maintaining financial health; and as a result, loans do not penetrate the lowest levels of poverty (Barboza & Trejos, 2009; Sengupta & Aubuchon, 2008). Today’s BancoSol has developed into one of the two largest MFIs in Bolivia and has grown to be a leading microfinance bank in Latin America.

P.T. Bank Rakyat Indonesia (BRI) is one of the leading and state-owned commercial banks and the second largest lender in Indonesia whose microfinance business started in 1984. As a full-service commercial bank with more than 10,000 outlets throughout Indonesia, BRI provides a whole range of banking products and services, particularly the microfinance services to “better off” poor and small businesses. More specifically, BRI provides secured loans with repayment periods ranging between 6 and 36 months with a monthly repayment term (Revindo & Gan, 2017). Unlike BancoSol and GB, however, BRI does not adopt solidarity lending but requires the individual borrowers to offer collateral as a guarantee (Munandar, 2015) which largely prohibits the poorest people who cannot provide any collateral from borrowing. In general, the borrowers are started off with small loans, which may increase in size depending on the borrower’s repayment performance. The interest rates on these loans are usually 30% to 40%, while the real interest rates may be 22.5% to 30% after a refund of 25% of the amount of interest as a reward for repayment without delay (Ahmed & Masyita, 2013).

The basic characteristics of these three prototypical models of MFIs are compared in Table 1.

Comparison of the Three Models.

Note. MFI = microfinance institutions.

A Critical Analysis of the Three Models

In principle, microfinance industry provides a viable and actionable path toward poverty alleviation by offering access to credit for those who are at the bottom of the economic pyramid (Lopatta et al., 2017). While doing so, MFIs usually fulfill dual missions: to provide services to poor customers and at the same time earn a profit to be financially viable. However, these dual missions are paradoxical in nature since earning a profit for MFIs will inherently impact negatively the degree of the help provided to the poor by MFIs. Therefore, not just the three models above, almost all MFIs are experiencing the struggle between the two inherently paradoxical missions of maintaining financial viability and providing sustainable social services (Caserta et al., 2018; Fouillet & Augsburg, 2010).

Unfortunately, the issues on whether the paradoxical nature of the dual missions of MFIs could be balanced and how to balance these two conflicting missions are not fully understood yet. We could only look for some insights in some studies relates to social enterprises. To the best of our knowledge, two significant researches undertaken by Agafonow (2015) and Agafonow and Donaldson (2015) contribute to our investigation in which they focused on the topic of how social enterprises and social businesses prevent mission drift and make a trade-off between non-profit and for-profit. More specifically, the practice of MFIs seems suggesting that most of MFIs are increasingly focusing on financial performance at the expense of poverty reduction (Mia & Lee, 2017; Xu et al., 2016), referred as the mission drift of the microfinance industry. Mission drift can substantially weaken the impact of microfinance services and possibly triggered the global microfinance crisis (Lopatta et al., 2017). Although the literature in microfinance does not reach unanimous agreements about the emergence of mission drift, there is a growing body of evidence suggesting that microfinance is not having the desired effect of lifting poor people out of poverty (Caserta et al., 2018). Beisland, D’Espallier, and Mersland (2017) argue mission drift should be attributed to a change in the focus and strategy of MFIs or excessive external competition. And it is also a consequence of the commercialization process within the microfinance industry which is believed to have a fairly negative effect on MFIs’ outreach and performance in the long term (Assefa, Hermes, & Meesters, 2013). Okoye et al. (2017) note that one of the main reasons for mission drift is the absence of official regulation and supervision, for example, India’s microfinance industry was considered as a typical example which operated in a regulatory vacuum (Nair, 2011; Polgreen & Bajaj, 2010). Furthermore, Cull, Demirgüç-Kunt, and Morduch (2009) suggest that the low industry access standards are also contributing to mission drift which leads to a large influx of profit-seeking capital. Thus, opponents of microfinance argue that microfinance should not be hailed as poverty alleviation any more but the cause of more poverty (Aslanbeigui, Oakes, & Uddin, 2010; Saad-Filho, 2010). Therefore, whether microfinance is really an effective tool for fighting poverty is increasingly being questioned yet unanswered by the current literature.

All three prototypical models of MFIs described above clearly demonstrate the mission drift when they deal with their dual missions. Some prominent symptoms of mission drift could be derived from their practices, for example, high interest rates and profitability-orientation, adverse selection of solidarity lending, mis-targeting and social failure.

The first symptom of the mission drift is the high interest rates and profit-orientation of MFIs. It is believed that MFIs suffer from higher operational expenses since they handle customers of low credit worthiness and high-risk collateral-free lending. When handling this challenge and trying to remain operationally viable, most MFIs shifted the high operating costs to their clients and charged high interest rates to offset the costs. Objectively, it is reasonable to charge a moderately high interest rate due to MFIs’ high transaction costs which is approved by Rosenberg (2007). Nevertheless, on the pretext of high transaction costs, many MFIs charged higher-than-necessary interest rates driven by profit maximization motive. In addition, when issuing microloans, most MFIs require compulsory savings that are not allowed to withdraw partially or fully until the loans are paid off, and ask excessively frequent installment repayments plan. However, in doing so, there is every possibility for MFIs to charge more for high yield, which might positively associate to mission drift (Sun & Im, 2015). Such abusive financial practices have put the borrowers in over-indebtedness and created serious debt traps for the poor (Taylor, 2011). Ironically, although the poor are considered more trustworthy with very high repayment rates (Kropp, Turvey, Just, Kong., & Guo, 2009; Yunus, 1999), they are still charged high interest rate with excessively frequent repayments, leading the borrowers who cannot manage to earn a rate of return above the interest rate at a speed quicker than repayment rate may actually end up much poorer (Conning & Morduch, 2011; Karlan & Zinman, 2008), defying the claimed social missions of MFIs.

The second symptom of the mission drift is adverse selection of solidarity lending. Most MFIs adopted solidarity lending where small groups collectively borrow and mutually guarantee the repayment of each individual’s loan (Khavul, 2010). It uses social relationship as credit collateral to substitute traditional assets collateral. In principle, solidarity lending can be instrumental in improving repayment rates, allowing for lower interest rates, and raising social welfare (Montgomery, 1996; Morduch, 1999); however, it could also serve as a double-edged sword to microfinance (Lopatta et al., 2017). Jackson (2016) reports that MFIs sometimes recover loans by harshly exploiting group pressures and applying aggressive collection practices. Furthermore, when some MFIs aim to achieve a better outreach, they might imprudently simplify the screening procedures and put the clients in jeopardy of over-indebtedness. More seriously, if one member of the group failed to repay their loan as scheduled, all other group members are usually treated jointly as being in default (Hermes & Lensink, 2007). Bhole and Ogden (2010) found that group lending can worsen repayment rates, especially in the presence of strategic default. What usually happened is the adverse selection in practice (Laffont & N’Guessan, 2000)—when one member defaulted and all other members are also marked by MFIs as default, other members will cease to repay their loans or temporarily cease to repay. More seriously, the borrowers in a solidarity group may even collude against the MFI (Armendáriz de Aghion & Morduch, 2000). A growing evidence shows that solidarity lending has failed to help MFIs in its original mission, and it is frequently happened that solidarity lending aiming to control default risks actually magnifies the risk (Xu et al., 2016).

The third symptom of the mission drift is the failure of their social mission. Many MFIs failed to achieve their social missions of delivering truly meaningful services to the poor. Although lacking access to credit is considered as a main reason for poverty, there is a consensus that the non-financial services, such as training and technical assistance, education, capacity development, marketing, and institutional support, also significantly contribute poverty alleviation, (Biosca, Lenton, & Mosley, 2014; Brau & Woller, 2004; Copestake, 2007). Fighting poverty is far more than providing a certain amount of capital to the poor, but rather a systematic project. Regrettably, most MFIs do not provide sustained post-loan management and non-financial support services. It is believed that after the loan is issued, post-loan management should be kept going before repayment to ensure the security of the loan principal (Makina & Malobola, 2004; Pollinger, Outhwaite, & Cordero-Guzmán, 2007). However, due to expensive maintenance cost, most MFIs prefer to charge high interest rates to mitigate their risks (Morduch, 2000), rather than providing sustained post-loan management and services, defying their intended social missions (Freedman & Click, 2006; Ullah & Routray, 2007).

The current literature has made some meaningful attempt in studying factors that might influence or even mitigate these symptoms of mission drift, such as prudential regulation and supervision on some specific issues (Abdulai & Tewari, 2017), government regulations on the corporate governance in the microfinance sector (Okoye et al., 2017), risk preference of loan officer (Jia, Cull, Guo, & Ma, 2016), loan portfolio design (Lopatta et al., 2017), and the influence of CEOs’ gender (Hartarska, Nadolnyak, & Mersland, 2014) as well as the staff training and adequate incentive of loan officer (Aubert, Janvry, & Sadoulet, 2009) in MFIs on the trade-off between financial sustainability and social goals. Although these meaningful attempts have been made, the extant studies on microfinance still do not answer fundamentally whether it is possible to balance the paradoxical nature of the dual missions of MFIs and if it is possible, how to balance the two conflicting missions of MFIs. Built upon the insightful discussions by Agafonow (2015) and Agafonow and Donaldson (2015) within the framework of economics which is applied to account for social enterprises and social businesses such as microfinance, our research aims to fill this theoretical gap by exploring sustainable mechanisms in balancing the paradoxical missions of MFIs in the post-crisis era through an in-depth case study on RSL, an MFI in China.

Method

Setting

Despite the unparalleled economic growth, there is no doubt that China is still a developing country and poverty is still a salient problem in China. About 200 million Chinese, or 15% of China’s population, are considered poor by international poverty line, set at US$1.25 a day, in which, more than 82 million Chinese live on less than US$1 a day (Wong, 2014). The absolute majority of poor people in China live in rural areas, and lack of access to credit is considered as one of the main reasons why the poor remains poor. The regional imbalance in financial services makes China’s poverty a serious problem. For instance, in 2014, there are still 1,570 rural towns in China without any financial services while the number was 1,696 in 2011 and 2,945 in 2009 (People’s Bank of China [PBC], 2015). Shanxi Province is a typical underdeveloped province with about 10% rural poor people, and 58 of its 118 counties identified as poverty stricken before 2019 (Xinhua, 2019). Pingyao is a regular county in Shanxi Province which has more than 80% rural population whose average annual income about US$1,600 (Pingyao Website, 2018).

Our research is based on a case study of RSL Microfinance Co. Ltd. in Pingyao, Shanxi. In 2005, China Central Bank (PBC) and China Banking Regulatory Commission (CBRC) initiated a pilot program, establishing seven commercialized MFIs in five impoverished provinces for poverty alleviation. RSL is one of the seven. On December 27, 2005, RSL was founded officially by three individual shareholders with ¥17 million initial registered capital. According to the regulatory policy of targeted poverty alleviation, RSL’s geographical scope is limited to Pingyao. In the early stage, significant market development, variable products design and painstaking care of its founders for poverty alleviation earned RSL an excellent reputation, as proudly announced in the company’s motto—“Providing financial service to agriculture, rural areas and farmers; boosting the development of SMEs.” In 2008, German Technical Cooperation (GTZ) noted the social impacts of RSL and reached an all-round cooperation agreement with RSL which involved GTZ providing no-interest loan of €150,000 from July 2008 to December 2009 for improving RSL’s IT infrastructure and services. In the following years from 2008, attention to corporate governance, products innovations, cost control, service quality, and post-loan services put RSL in a sustainable path of development, and RSL twice won the award of “Top 100 Microfinance Company of China” in 2011 and 2013. As a small company with only 15 staff in total, RSL’s total amount of loans have risen significantly to ¥2.96 billion issued to about 15,000 poor clients in the last 10 years.

Our study on RSL started in 2011, the sixth year after the initiation of the pilot program of commercialized microfinance in China and establishment of RSL. Over these 6 years, RSL gained more and more attention for its social responsibility, business model, and influence on peer MFIs. In 2011, the first author had a chance to be introduced to RSL and made the first visit. Since then, the first author began to keep a direct contact with RSL’s CEO. After a full year of preparation, in 2012, we started our 5 years’ investigation and observation on RSL.

Data Collection

Semi-structured interviews were used as our primary method for this study (Yin, 1981). The semi-structured interview enjoys its popularity because of high degree of flexibility, accessibility, and intelligibility. Particularly, it is capable of discovering some important and often hidden facets of organizational behavior. It is usually considered the most effective and convenient means of gathering information with meaningful insights and rich details (Wengraf, 2001).

We conducted 39 semi-structured interviews with 36 interviewees between 2012 and 2016. Our sampling follows a logic from purposeful to theoretical. To understand RSL thoroughly, we started interviewing internal members of RSL. The eight members we interviewed (one shareholder, one CEO, all the three department executives, and three staff members) represent different divisions of the company and different levels of experience that occupy about 50% of RSL’s total staff, most of whom began their career in RSL from its establishment, so they proved to be a good sample for us to understand RSL’s development and operations. Among them, CEO of RSL was interviewed four times (May 2012, August 2014, March 2015, and October 2016). We expanded our interviews to 14 clients of RSL selected on the suggestion of Credit department to represent different situations of clients. We then interviewed five executives from local peer MFIs to investigate in more detail and cross-validate information on RSL’s products and services quality, poverty alleviation effects, market feedback, and peer evaluation. Finally, to help us understand RSL in the context of China’s microfinance industry, we interviewed three specialists from China Microfinance Project Team of World Bank Institute (WBI), three microfinance researchers from different research institutes, and three policymakers from regulatory authority who could provide rich and insightful information on microfinance and MFI-related information in a broader scope.

The interview protocols were designed after a systemic literature review. Different sets of semi-structured interview questions were developed for different types of interviewees to get data as consistent and comparable as possible. For example, to eight internal members of RSL, the questions were centered on RSL’s social responsibility, fulfillment of missions, balancing the conflicting dual missions, its sustainable development, credit model, effective operations, and so on, while to three policymakers from regulatory authority, the questions were centered on evaluation of current microfinance models, crucial factors that impact a MFI’s sustainable development, the role of government regulations in influencing MFIs, and the commercialization of MFIs.

Procedurally, prospective interviewees were contacted by telephone in advance. The first author explained the project and sent them the interview protocol to help them familiarize with the topic. The site and time of interviews were chosen by the interviewees and almost all interviews were conducted at interviewees’ own workplace. The interviews were conducted ranging from 1 to 3 hr in length and were tape recorded with their permission. After the interview, the tapes were carefully labeled with an identification code and a data preparation chart containing the information of date, time, place, data code, and so on was created to track individual interviews and the progress of transcription process. All interviews were conducted and transcribed verbatim in Chinese to ensure accuracy and reliability, and later, the transcriptions were translated into English and cross-checked for accuracy by the second author.

To help us understand RSL better, we also studied information posted on RSL’s website which includes detailed descriptions of corporate strategies, the vision, business philosophy, and the organizational changes. Furthermore, with the permission from RSL’s CEO, we had access to its internal documentation including its annual reports, periodical statistics, market research, and cost analysis, though parts of these documents are not allowed to be copied or disclosed publicly.

Data Analysis

By 2016, we accomplished the planned interviews and moved into the data analysis phase. The interview data are composed of 39 interview documents, a total of 452 pages with 218,650 words. Similar to the methodology of grounded theory (Glaser & Strauss, 1967), the data analysis in this article relied on an iterative coding and categorization of the dataset, involving identification of common themes or ideas from interview data. In general, the authors respectively read the transcript and made notes about the key themes, especially the different opinions between interviewees. Then, the authors exchanged periodically and discussed emerging principles until agreement was reached about the overriding themes.

Specifically, we conducted a preliminary filtering, screening, and integration of the data by deleting and removing some invalid and meaningless expressions, for example, Chinese greetings and expressions of courtesy, some repetitive introductory information. Therefore, the interview data were reduced to 337 pages with 150,375 words. Based on a comprehensive study about the database, we identified a number of RSL’s program-related views, ideas, and practices that seemed to underpin RSL’s organizational responses to market and environmental challenges. In total, the dataset was classified into 72 categories in the initial stage. We then counted the occurrence frequency of the encoded text (a phrase, a sentence, or a paragraph). For example, a segment of the Interviewee #7’s comments: [. . .] RSL maintains a meager profit strategy: our Return on Equity (ROE) has been limited less than 5% in these years. The meager profit just aims to cover the costs. The initial goal which inspired us engaged in microfinance is not to make big profit, but poverty alleviation. In fact, from a profit-making perspective, it is not a good investment decision because there are a lot of business opportunities to make big money [. . . ]

was coded into four categories of “meager profit,” “financial strategy,” “cost,” and “profit-pursuing” and each category was counted once.

Another segment from Interviewee #33: [. . .] In essence, microfinance is a risky business in most countries. How to hedge the default risk is always a troublesome issue. However, we cannot imitate the traditional commercial bank’s credit review model which requires the applicants to provide standardized financial statements and collateral. So, we had to create some new measures to handle the challenge. For example, firstly, the defense line of MFI related to credit risk management is its loan officer which highlights the crucial importance of human resource management (HRM). Secondly, we argue that a trust-base customer relationship management (CRM) [. . .]

was coded into “default risk,” “credit risk management,” “collateral,” “HRM,” “CRM,” and “credit assessment” and each category was counted once.

Next, the subsequent readings and coding of our data revealed some emergent categories, and some existing categories were either merged into more general categories to gradually move to a more general explanation or further split into finer categories to capture the details in RSL’s practices. For example, we further divided the initial “action” category into practice-oriented (primarily aimed at exploring and processing the data of “what” and “how”) and theory-oriented (primarily aimed at reflecting on the issues of “why”), and then we recombined “practice-oriented actions” with the major category “product and post-loan services” and combined “theory-oriented actions” with the major category “mission.” This iterative coding, categorizing, and re-categorizing facilitated comparison of each author’s interpretations of categories, and discrepancies about same issue were usually cross-validated to deepen our understanding.

In the next stage of the analysis, we focused on how the various categories we had identified could be linked into a deep theoretical thinking on how RSL balances the paradoxical missions to find a sustainable path in the post-crisis era. We iteratively examined the specific practice of RSL and compared similarities and differences with other MFIs. Eventually, most RSL program-related data were categorized according to both their orientation and role and grouped into five major processes with 46 categories that appeared to help RSL to find a sustainable path (Table 2). As Table 2 reported, the frequency of the 46 categories is counted to be 3,006 in total. This analysis helped us link the actions and elements and converged into a tentative framework. Positive feedback on our tentative framework from different informants reinforced our confidence in the reliability of our constructs and paradigm.

Key Categories and Their Frequency Identified From Interviews.

Note. RSL = Rishenglong Ltd.; MFIs = microfinance institutions; WBI = World Bank Institute; HRM = human resource management.

In addition, to corroborate our interpretations and increase the robustness and generalizability of our categorization scheme, our findings were submitted to interviewees, and their comments sometimes proposed alternative explanations to be examined and helped us reinforce the validity of our framework. Eventually, we believe that our analysis and findings on the case of RSL present a satisfactory answer to the research questions we have and provide a refreshingly new perspective of microfinance in the post-crisis era.

Findings

In this section, we develop a detailed overview of how RSL finds a sustainable path in balancing its dual missions and generate effective impacts on poverty alleviation.

The Balance of RSL’s Dual Missions

The most frequently appeared categories in our dataset are the keywords of “mission,” “targeted poverty alleviation,” “commercialization,” and “financial sustainability,” suggesting a self-awareness of the paradoxical nature of RSL’s mission. Although all interviewees support the view that the purpose of a commercialized MFI should be to achieve a social mission through the use of market mechanisms and their commercial activities are a means toward social ends, they all recognized that MFIs are at risk of focusing too heavily on business goals. As observed by Interviewees #1, 28, 30, 32, and 35, RSL has been painstakingly put in efforts to balance its dual missions so as to generate necessary profits but without losing sight of their social goals.

RSL’s business practices provide us some valuable insights on this balancing. According to Interviewee #1, “providing financial service to agriculture, rural areas, and farmers; and boosting the development of SMEs are our social mission, although it needs a requisite financial foundation to sustain it.” In RSL, “the financial mission is just a bottom line to sustainable development while we are not pursuing big profit” (Interviewee #2). Interviewee #7 explained, “RSL maintains a meager profit strategy: our Return on Equity (ROE) has been limited less than 5% in these years. The meager profit just aims to cover the costs.” We found adequate evidence in RSL’s annual reports that its profit margin has maintained at very low level over the years. As a practitioner of inclusive finance, in its 10 years development, RSL has always given its social mission the top priority.

The key question here is why RSL has no desire to make big profit? Our data revealed two major reasons as follows.

First, pursuing big profit is not RSL shareholders’ primary goal. All the shareholders of RSL are Pingyao native and have been successful entrepreneurs before starting this project. Therefore, they do not have much pressure in making profit through RSL. Interviewee #1 explained “the original motivation driving us to engage in microfinance is just providing financial services to our neighborhoods, especially local low-income groups, to help them improve their lives.” This small step, if successful, may lead to a fundamental change in Pingyao’s economy and credit market, and improved credit access would contribute to a boom of Pingyao’s rural economy. We hope to achieve this ideal through our persistent efforts.

For the founders of RSL, pursuing big profit has never been their primary goal. Instead, helping more neighbors overcome poverty and improving their economic conditions are their ultimate goal for RSL. In essence, MFIs are also social enterprises or social businesses, that is, neither pure non-profit organizations nor sheer for-profits. Therefore, RSL’s meager profit strategy is consistent with the studies of Agafonow (2015) and Agafonow and Donaldson (2015) in which they focused on how social enterprises and social businesses prevent mission drift.

At the same time, our interviews revealed that although RSL only gets meager profit as a microfinance business, it gained significant intangible benefits such as a good reputation and strong social impacts in Pingyao locals as reflected by the numerous awards RSL received, such as Good Faith Effort Award in 2007, Top 100 Microfinance Company of China in 2011 and 2013, and lots of media reports for its poverty alleviation efforts. As a result of these intangible benefits, RSL’s shareholders have enjoyed a positive image and reputation in Pingyao, which was ultimately translated into tangible benefits for shareholders’ other businesses. Interviewees #10, 11, 15, 17, 18, 21, 24, and 35 all touched on RSL’s shareholders’ other business activities. Interviewee #35 provided us a 2010 news report about the main shareholder of RSL who is the chairman of a local coal trading company. While the entire coal industry fell into recession in 2009 and his coal trading company also suffered from capital trouble, in 2010, the local government provided him necessary assistance and financial support in reward for his good social responsibility as one of the founders of RSL. As a result of this assistance, his coal trading company turned losses into profit in the following years.

Second, we found that proper social value orientation in RSL is an important factor to balance its dual missions. RSL meticulously emphasizes the importance of the social values in their daily operations. They proposed and adhered to some classical business philosophies that are deeply rooted in Chinese traditional culture. Interviewee #2 presented us a detailed introduction on their business values. For example, “Even though a gentleman loves money, he gains it in a proper way and use it to a right degree”; “The gentleman knows the value of righteousness while the petty man only knows interest or benefit”; and the idea of benevolence from Confucianism, all of which serve as their guiding principles when doing business. In RSL’s business operations, righteousness, credibility, and faith are the foremost principles while profit is secondary. These philosophies have been highly endorsed by Interviewees #31, 32, and 33, who all argued that these business philosophies are the pivotal factors in accomplishing a balance of dual missions. Therefore, for MFIs, proper social value orientation will contribute to capitalize on the economies of scale to harness the process of value creation for the sake of value capture (Agafonow, 2015).

As a result of these two factors, RSL did not implement aggressive expansion strategy as many other MFIs did. Its prudent strategy not only harvested a good social effect, but also achieved financial sustainability. As explained by Interviewees #2 and 5, RSL’s annual interest revenues from microloans have been able to cover the full costs of its activities since 2007 which was confirmed by RSL’s financial reports. Furthermore, RSL gained competitive advantage gradually. Especially in recent years of economic depression in China, when many MFIs are stuck in customer drain and increasing overdue loans, RSL received more and more positive market responses.

To successfully maintain the balance between potentially conflicting dual missions, RSL implemented some practical measures (a localized model, a reputation-based credit model, and a targeted product design and sustained post-loan service) that strengthened the effectiveness of this balance.

The Localized Model Used by RSL

Our data revealed that, distinguished from most of other MFIs, RSL has an interesting operational model: an MFI of the local, by the local, for the local. We found RSL actively maintained this localized operational model, which could be characterized as a financial institution suitable for the local culture and history that only hires local people to serve the local people through locally targeted products and services. This is in sharp contrast to a generalized model of most MFIs where an aggressive expansion strategy is often used to build many branches in different regions whose operations, products and services are standardized across.

This localized model helps RSL in balancing its dual missions. Both Interviewees #1 and 2 explained that the root cause of poverty is usually characterized by strong regional differences. Poverty alleviation thus needs to address these regional differences and targets specific situations in different regions. A generalized model of providing microloans to the poor people without differentiated products and services and without an operational strategy suitable for the local culture and history will not be effective in fighting poverty. “RSL only operate in Pingyao. We don’t expand since we are only concerned to serve Pingyao locals for their poverty alleviation efforts” (Interviewee #2).

Our data revealed four major characteristics of this localized model.

First, Pingyao is still a typical acquaintance society with low migrant population. In such an acquaintance society, the traditional culture and social conventions of Pingyao are conserved, and a shared norm of moral constraints plays a significant role in regulating people’s behavior. Local people attach great importance to their personal reputation. Interviewees #32 and 33 argued that this acquaintance society will contribute to a credit society where default in loans will harm the personal reputation of locals. More specially, in our interviews with Interviewees #9 to 22, RSL’s clients, we explored how their social networks are impacting their loan repayments. What we found is that the majority of Pingyao natives live in a small social circle, and the traditional regional culture and values still have strong constraints on people’s behavior. In this social environment, if a person defaults, the news will spread in his social circle quickly which will generate a lot of negative impacts on his or her daily life. So, as an inherent characteristic of acquaintance society, moral constraint is effective in regulating local people’s behavior such as timely repayments, upon which RSL’s local business model could be successful.

Second, a localized employment system is also an important component to this model. As Interviewees #2 and 3 explained, the recruitment and selection of employees in RSL focus on candidates who must be Pingyao native, brought up in such a traditional culture environment, and behaved ethically in the past, on top of having strong responsibility and necessary experience in finance industry. Interviewees #2 to 8 confirmed these measures using their personal experience and how they joined RSL. In addition to necessary background review and occupational assessment on the candidates, we found an interesting selection mechanism in RSL—it uses an integrity investigation through the acquaintance circle of job candidates. Job candidates must be recommended by a credible acquaintance whose reputation is well recognized in Pingyao. This way, the performance of the employees is tied to the credibility of the acquaintance who recommended him or her, which will impose strong moral constrains to employees’ behaviors and motivate them to work better.

RSL also adopts a competitive compensation system. Based on Interviewee #3, RSL’s salary is higher than other local MFIs in Pingyao, and significantly higher than the local average income. RSL successfully balanced the cost of human resources and the meager profit strategy of the company. Interviewee #2 explained that although the human resource cost is higher in RSL than others, its total operational cost is relatively lower thanks to its lean management and almost zero-default in loans. Therefore, RSL has forged a highly efficient running team with only 15 staff in total who serve RSL effectively for its competitiveness.

Third, Pingyao’s distinguished regional culture fundamentally influences RSL’s localized operational model. Pingyao is famous for its glorious finance history and business culture in Ming and Qing Dynasties (1370s-1910s) which still have a profound impact on today’s Pingyao. Almost all interviews touched on the worship of Guan Yu (161-220 AD, Shanxi native, one of the best known Chinese historical figures), for his loyalty, honesty, and integrity, which, in their view, are the crucial virtues for doing business. Throughout the interviews, we found that the worship of Guan Yu is deeply rooted in the cultural identity of Pingyao locals. Therefore, according to Interviewee #32, the shared regional history and culture strengthened their business ethics and strongly influenced their business operations in balancing its dual missions.

Fourth, besides contributing to the decreased operating cost, the improved microloan performance, and better customer services, RSL’s localized model helped the formation of a self-discipline mechanism. To the staff of RSL, the self-discipline guides them to work effectively not just for their high salary, but for their reputation (and for maintaining their recommenders’ credibility). To the clients, because they care about their own reputation, self-discipline guides them to abide by the loan contract as much as possible. According to the data provided by the Interviewee #2, although there are few clients delinquent temporarily, they have accomplished a 100% recovery of maturing loan principal. And they also have a high recovery rate for loan interest except a few waivers granted to clients based on the occurrences of unexpected life events.

The Credit Model of RSL Based on Reputation Mechanism

Besides the four characteristics discussed above, RSL’s localized model also implies an effective and efficient credit model suitable for Pingyao local situation. We found that the credit model of RSL is different from other MFIs in two distinctive aspects: credit worthiness assessment based on reputation and improved solidarity lending.

First, as Interviewee #2 introduced, RSL has created a distinctive credit model based on reputation mechanism that dictates daily practices from pre-loan investigation to loan recovery. Interviewee #5 explained: to better understand a potential new client’s credit worthiness, RSL has used a comprehensive credit assessment. Since the vast majority of small loan clients are unable to provide effective household financial information or collateral, RSL has focused its pre-loan investigation and credit assessment on client’s honesty and integrity through their acquaintances circle. RSL called it “moral evaluation” (Interviewees #2 and 3). In essence, it is a subjective assessment without a concrete collateral. Interviewees #2 told us “we maintain that the clients should be of sound moral character which is more important than financial collateral in Pingyao, an acquaintance society.” The staff will first investigate the potential clients’ reputation through their social cycles, family members’ reputation, and interpersonal relationships before they examine regular credit collaterals in loan approval. Interviewee #2 admits that moral evaluation is subjective but they observed that repayment willingness is more important than repayment ability, i.e., the higher moral level of a client, the lower likelihood of default.

Second, RSL improved the traditional solidarity lending model. Interviewee #5 described that RSL extends the regular “Credit group lending” to “Credit village lending” which was designed to issue loans to the whole village if the majority of households in the village is engaged in similar undertakings (such as crop farming, livestock breeding, transport service, and handicrafts). Thus, each household can easily obtain the loans if the village is granted an overall credit. “By Credit village lending, we boosted the economy of scale in villages and significantly reduced our average operational cost” explained by Interviewee #2. For example, Interviewee #12 told us, I’m a pig farmer and there are a lot of pig farmers in our village. Our village has a credit and I had applied for loans from RSL twice. It is very simple, quick and convenient. RSL often gives us (the whole village) some information on market trend and breeding technology. Our business risk is reduced greatly.

Furthermore, RSL made another improvement on the solidarity lending: if a group member defaults, the others in the group are not liable for the repayment of the defaults but they will be denied for future loans. This improvement effectively avoids the adverse selection problem, and when one member defaulted, other members are very likely to continue their repayment since they are not marked by RSL as default. In that case, the other members will either put strong pressure or even provide some help on the default member so that the default member could re-start repayment.

The Products and Post-Loan Services of RSL

RSL also strengthens the effectiveness of the balance between potentially conflicting dual missions through products and post-loan services designed to target local people. That is, to improve the effectiveness of poverty alleviation, RSL designed a variety of loan products and services for the local market.

First, the product portfolio designed by RSL reflects its anti-poverty mission as an MFI. RSL focuses its business on agriculture-related short-term microloans distributed to as many clients as possible. According to the data provided by Interviewee #5, the percentage of RSL’s agriculture-related loans is always kept above 70%, and even reaches 100% in some years (2007, 2008, and 2011). The loan terms correspond to farming seasons ranged from 1 to 12 months, among which, about 20% are 1 to 3 months loans, 60% are 4 to 6 months loans, and 20% are 7 to 12 months loans. The loan amounts ranged from ¥1000 to ¥100,000 and above 75% of the loans are below ¥50,000. It should be noted that, according to Interviewee #2, RSL maintains a lower loan interest rates than other local MFIs, and provides a flexible repayment plan (bullet repayment or monthly repayment). As Interviewee #2 indicated: RSL upholds our mission as an anti-poverty financial institution in these years. We are able to help as many local Pingyao farmers as possible by providing them small loans for a short term with very low interest rate. We are able to achieve this due to our low operating costs and at the same time, this actually lowered our business risks.

RSL also issues charity loans for impoverished family or economic vulnerable groups at very low interest rates, to assist them to cope with financial difficulties. Interviewee #14 told us his experience of applying for charity loans from RSL: There are six members in my family living in a very poor condition and we don’t have any savings. In 2012, unexpectedly, my wife needed a surgery costing us ¥30,000 which we need to pay before the surgery. However, the new rural cooperative medical system can only kick in long after the surgery. So, I applied for a six-months’ charity loan from RSL and got it in the same day. The surgery was performed without delay.

We learned many similar cases like this in our interviews. And based on the data provided by Interviewee #5, by 2016, RSL has issued urgent charity loans for medical emergency for over 100 applicants in total to aid their families coping with difficulties.

Second, different from most MFIs whose operational focus is on the loan issuing and recovery, RSL puts significant efforts to provide additional services after the loan is issued to clients (post-loan services) to improve the loan performance in poverty alleviation. Interviewee #2 explained: microfinance should be an integrated package of services, rather than just a loan deal, and what the clients lacked is not just funds. After the clients received the loans, RSL will support the user of the loan throughout its life cycle. During this process, we found more than 50% clients need training in farming techniques and they also need market information for their corps and livestocks. Based on their needs, RSL regularly offers training on farming and breeding and provides market prediction to the clients at appropriate time.

All of the clients we interviewed are the beneficiaries of such post-loan services. Highlighted by Interviewees #28, 30, 32, and 33, although providing sustained post-loan services incurs additional costs, it will build a better relationship with clients, improve clients’ income, reduce the default risk, and enhance both RSL and clients’ financial sustainability. Most importantly, in the process of post-loan services, RSL can continuously monitor the loan usage, which further contributes to their risk management.

The Role of Policy Regulation and Industry Association in RSL’s Development

The last prominent category in our data points to the importance of institutional environments for RSL’s sustainable development. Two major institutional forces are frequently mentioned by interviewees and reflected in the archival documents: the coercive forces from regulatory policies in different levels of governments and the normative forces from the regional industry association initiated by RSL and two other MFIs.

From different perspectives, Interviewees #2, 23, 25, 27, 32, and 33 discussed the positive role the regulatory authority has played. Between 2005 and 2016, the regulatory authorities at different levels of governments gradually strengthened the supervision on microfinance industry and improved the policy guidance and policy support for MFIs in China. We found in our data the regulatory authorities have implemented three categories of policy guidance and supports: risk control, mission enhancement, and tax credit. For example, to mitigate and control credit risk, MFIs are not permitted to conduct deposit taking business in China, and in Shanxi Province, the minimum registered capital requirement for MFIs was increased from ¥10 million in 2005 to ¥50 million in 2009. These two policies reduced the possibility of radical expansion and contributed to the enhancement of MFIs’ anti-risk capability. To enhance the intended missions of MFIs, the upper limit on loan interest rates of MFIs has been restricted as four times of the benchmark interest rate in China which restricts potential usury. In Shanxi Province, the lower limit on the percentage of agriculture-related loans for MFIs is set at 50% which significantly contributed to the poverty alleviation mission of MFIs. Moreover, a certain amount of tax credit is given to MFIs who maintain high percentage of agriculture-related loans. As Interviewee #35 explained, “Policies are an important institutional guarantee for the sustainable development of microfinance industry. These coercive supervision and regulation ensure the basic function of MFIs in poverty alleviation and avert MFIs’ mission drift.”

In addition, we found that the normative forces of the industry association are effective and efficient to sustain the development of MFIs. In 2008, RSL and other two microfinance companies initiated the establishment of China’s first regional Microfinance Industry Association in ally with 29 local microfinance companies. Interviewee #2 introduced the five basic functions of the Association: enforcing self-discipline, formalizing industry standards, enhancing industry services, strengthening industry supervision and regulation, and keeping competition in orderly fashion. According to Interviewee #2, members of the Association meet monthly to evaluate public policy and economic situation, discuss new product development and staff training, negotiate and assess venture deposit adequacy ratio, share best practices, and exchange information on a list of default customers. The Association also conducts on-site inspections on members and provides incentives or disincentives to regulate its members’ operations. As the Association members, Interviewees #23 to 27 have a high opinion of the establishment of the Association. According to Interviewee #31, “MFI is a newly emerged financial institution under a pilot program in China which needs a multi-level regulatory system. As the first regional Association in China, this Association is constructive on the sustainable development of local MFIs.”

Discussion and Conclusion

Poverty is not created by poor people but created by the system (Yunus, 2007). Lacking necessary formal financial services, especially credit service, is a major cause of chronic poverty. Taking China, for example, the 2005 closure of tens of thousands branches of “Big four banks” in rural areas due to their poor financial performance made the financial service shortage worse and exacerbated poverty situation in rural China.

Microfinance fills in this gap as an innovative financial tool to allow poor people lifting themselves out of poverty by giving them the access to credit and the necessary financial services. Nevertheless, microfinance crisis erupted in 2010 rang an alarming bell to the rapid development of microfinance industry. For example, many MFIs in China have failed to realize their original objective of poverty alleviation in the impoverished areas of China (Jia et al., 2016; Tang, 2012; Xiong & Wang, 2013). Globally, researchers have argued that profit pressures can easily produce mission drift (Epstein & Yuthas, 2010; Jones, 2007), and there are many cases in the world that verified the trends of mission drift (Copestake, 2007; Dees & Anderson, 2003). To address this fundamental problem in microfinance industry, it is important to find a sustainable path for MFIs with balanced dual missions to develop and flourish in the post-crisis era, as exemplified by the case study of RSL in this article.

The fundamental reason for mission drift in MFIs is the logics behind all MFIs. MFIs simultaneously emphasize social logics and business logics (Austin, Stevenson, & Wei-Skillern, 2006; Defourny, 2001). Though an MFI creates social value to address social needs of poverty alleviation, the organization’s efforts are short lived if the necessary business logics are absent. Survivability, not organizational mission, is the foremost concern for any organization. Thus, a socially driven organization must also focus on its fiduciary responsibilities, which can lead to mission drift as an MFI spends more and more resources to survive (and thrive) and conversely fewer and fewer resources to fulfill its social mission (Bielefeld, 2009; Connolly & Kelly, 2011). A paradox emerges whereby the business logics driving survivability and thriveability interfere with the social logics used to aid the needy, and vice versa. MFIs need to seek financial sustainability while fulfilling their social value, leading them to constantly struggle between seeking to maximize their profitability at the expense of social service delivery and providing valuable social services despite the risks to their profitability.

What we found in this article suggests that this paradox faced by all MFIs could be effectively eased by putting priority to the social mission of MFIs through a set of mechanisms. In RSL’s business practices, its social mission is always given top priority, and its financial mission is defined in a way to sustain the organization (survivability), rather than pursuing big profit (thriveability).

The major strategic choice of RSL to handle the paradox is its adoption of a localized model. This is in sharp contrast to the strategic choices of the most of MFIs globally, who have been adopting aggressive expansion strategy to provide standardized products and services across all branches. RSL’s localized model is not just referring to the geographical area where RSL operates, but referring to the historical-cultural traditions of the local within the local value systems. A small group of local employees selected based on the reputation of their local references operates RSL and designs and targets its products and services (especially post-loan services) for the specific needs of locals. The business scope of RSL is deliberatively controlled within a limited range and RSL upholds a philosophy of anti-diversification, which, combined with the characteristics of local acquaintance society, contributes to the low risk and high yield of the business. The local scope implies an acquaintances society, where people attach great importance to their personal reputations leading to the reduced risks in defaults, especially after a moral evaluation of loan applicants. Compared with the globally recognized three prototypical models of MFIs that we reviewed, RSL’s localized model touched on the essence behind the missions of MFIs-targeted poverty alleviation and addressed this mission from its root: poverty alleviation at the grassroots level of a local region.

Our findings in this article highlight a viable alternative for MFIs: instead of adopting a generalized model where an aggressive expansion strategy is used to build many branches in different regions whose operations, products, and services are standardized across, a localized operational model could be more sustainable in addressing mission drift and the paradox of business and social logics facing all MFIs. An MFI of the local, by the local, for the local, suitable for the local culture and history, hiring only local people to serve the local people through locally targeted products and services, is a sustainable path for MFIs.

This article contributes to the emerging literature on microfinance industry by suggesting a sustainable path of development of MFIs in the post-crisis era. The managerial framework of RSL revealed in this article could guide indigenous microfinance companies to deal with the increasing complex and changing business environment and build a sustainable path in poverty alleviation. We call for more empirical researches on the positive examples such as RSL in the microfinance industry to enlighten both researchers and practitioners on how a hybrid organization with paradoxical logics and missions could survive and thrive.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.