Abstract

Mobile banking (m banking) is the breakthrough technology in banking sector which has significantly improved efficiency of banks and people’s quality of life. Banks seem particularly interested in such systems that provide their customers with better services. However, acceptance of and loyalty to m banking depends on how effectively banks motivate their customers to adopt the technology and retain their continued use. The adoption rate in China is very low and quite a few studies have focused on issues related to m banking. The purpose of this study is to examine factors that affect m banking adoption and usage intentions of Chinese bank customers. The proposed model has extended the technology acceptance model (TAM). Data were collected through a field survey questionnaire and analyzed through partial least square structural equation modeling (PLS-SEM). The results showed that acceptance of and loyalty to m banking among Chinese bank customers was significantly and positively affected by resistance to change, perceived risk and low awareness of services, and perceived benefits. The results will be useful to retain existing users and attract new ones. This study is unlike past studies that merely studied short messaging service (SMS) banking and initial adoption or technological aspects of m banking. This study also provides Chinese banks with applicable strategies to effectively design and implement m banking; thus, it is expected to potentially contribute to prevailing literature, especially in the context of China, where few studies that address m banking acceptance and loyalty exist currently.

Introduction

Technological developments have equipped the banking industry with various electronic channels that have drastically lowered significance of traditional banking. Among these developments, mobile banking (m banking) is a breakthrough technology, and thus, it remains of highest interest. This technology frees customers from temporal and spatial limitations and enables them to perform banking transactions at any time and any place (Cheng, Lam, & Yeung, 2006; Chin, Marcolin, & Newsted, 2003; Salimon, Yusoff, & Mohd Mokhtar, 2017; Siyal, Ding, & Siyal, 2019) with a constant control over their financial assets (Koksal, 2016). This freedom of preferred time, place, and constant control has also supplemented customers’ banking affairs with lower cost (Lawler, 1990; Muhammed, Jabbar, Mujahid, & Lakhan, 2013). Users regard mobility and round-the-clock service availability as the most important elements of m banking (Raza, Umer, & Shah, 2017). These elements have been proven effective in promoting existing commerce (Afshan & Sharif, 2016; K. K. Kim & Prabhakar, 2004) and capturing new markets at a global level (Püschel, Afonso Mazzon, Mauro, & Hernandez, 2010). This preliminary growth led banks and service providers toward huge investments in the technology (Luarn & Lin, 2005). According to Alalwan, Dwivedi, and Rana (2017), globally, a total of US$115 billion had been invested at the end of 2013 to implement m banking technology. The huge investments in the technology infrastructure also attracted scholars to foresee future worth of the innovation by predicting its mass utilization. Scholars have predicted, for example, that mobile devices will replace PCs as the main device to access Internet (Coursaris, Hassanein, & Head, 2003); m banking will surpass all other banking channels (Teo, Tan, Cheah, Ooi, & Yew, 2012); and m banking is expected to reach 5.07 billion users by 2019 (Sharma, Govindaluri, Al-Muharrami, & Tarhini, 2017), which is in sheer contradiction with Bill Gates’s prediction that mobile banking apps will have more than 2 billion users by 2030 (Ramayah & Lo, 2007).

All these predictions seemingly lack fortified results because despite portability and doorstep services of m banking, the far-fetched gains fail to realize estimated levels of its mass utilization (Dineshwar & Steven, 2013; Koksal, 2016; Raza et al., 2017; Selye, 1946), and even in the established markets, the adoption level is low (Aboelmaged & Gebba, 2013; Siyal et al., 2019). This is ascertained by statistics reported by researchers that only 4% of approximately 25 million users of American banking services actively use m banking (Hanafizadeh, Behboudi, Koshksaray, & Tabar, 2014), whereas 12% of German consumers use their mobiles for banking or shopping (Tanner, 2008). This delay in adopting technology further warrants negative impacts on per capita income and development (Nysveen, Pedersen, & Thorbjørnsen, 2005; Podsakoff, Mackenzie, & Podsakoff, 2012). The delay in adoption of technologies also contradicts all the future use predictions of latest innovations, thereby calling for further investigation of adoption and continuity issues.

Extant research has merely focused on initial adoption of m banking (Cheng et al., 2006; Chin et al., 2003; Laforet & Li, 2005; Laukkanen, 2007) without heeding to post-adoption issues, which contradicts the conclusions of Corradi, Montanari, and Stefanelli (2001) that long-term viability and ultimate success of information systems depend on continued rather than one-time usage. Little research has been conducted to identify factors that prevent adoption of new technologies (Makanyeza, 2017). This scarcity of research has eventually resulted in the meager number of youngsters who have adopted m banking in both developed and developing countries (Moser, 2015; Tanner, 2008; Teo et al., 2012). According to Laukkanen (2016), resistance toward latent technologies is natural and increases as consumers delayed or prevented adoption. The innovation literature noticeably exhibits a prochange bias, arguing that innovations are always good and improved products or services are welcomed by consumers as they always want to switch to novel products and services. On the other hand, Ram (1987) and Dai and Palvi (2009) contradict this notion and describe it as a limitation of literature on innovations that fail to investigate adoption and diffusion of new technological advancements. This confinement has resulted in astonishingly scarce studies focusing on resistance to innovations (Kleijnen, Lee, & Wetzels, 2009), thereby necessitating further elaboration regarding the barriers inhibiting acceptance and loyalty of users toward newest technologies (Ferreira, Da Rocha, & Da Silva, 2014).

To address this gap, it is mandatory to understand inhibitors driving innovation toward failure (Laukkanen, 2016) and develop appropriate measures to enhance adoption rates (Elizabeth George, 2015), because success can only be achieved by retaining users and facilitating their continued utilization of the innovations (Cheng et al., 2006). This study has attempted to highlight strategies required to boost up low levels of customer demand and profitability against heavy investment of banks (Selye, 1946). It also provides measures to overcome threats posed, which led some American Banks to terminate their m banking services (Ajzen, 1985; Teo et al., 2012).

The study highlights fundamental barriers which refrain customers from accepting m banking in China and simultaneously provides remedial measures for customer loyalty. To date, little research focuses adoption or rejection mechanism (Laukkanen, 2016) because most past studies merely concentrated on short messaging service (SMS) banking without heeding to m banking (Mehrad & Mohammadi, 2016; Mohammadi, 2015b; Shaikh & Karjaluoto, 2015b). Some of the recent studies have opted to focus on the initial adoption of m banking (Cheng et al., 2006; Mullan, Bradley, & Loane, 2017) and the motivations toward m banking without focusing on the post-adoption or retention perspective (Lawler, 1990; Siyal et al., 2019). Recent studies of Mohammadi (2015a) and Sharma et al. (2017a) have neglected untapped market potential of nonusers and have opted to study the users alone, whereas others have explored the technological aspects of m banking rather than user behaviors (Fishbein & Ajzen, 1975; Hsu, Wang, & Lin, 2011; Kazi & Mannan, 2013), and surprisingly, most of these studies focus on developed countries that have relatively mature markets for technologies.

Banks in emerging economies continue facing environmental challenges for acceptance of m banking and may require more time and efforts in comparison with developed economies where the issues related to technology adoption have already been addressed to a greater level (Sharma et al., 2017). According to Teo et al. (2012), developing countries have largely remained neglected. In sum, least preference has been given to consumer perspectives (Glavee-Geo, Shaikh, & Karjaluoto, 2017), which corroborates the perspective that barriers to adoption of m banking is the least focused aspect (Mehrad & Mohammadi, 2016), leaving a developing country like China untapped and, henceforth, necessitating a dire need to study, identify, and examine such antecedents (Aboelmaged & Gebba, 2013). The prevailing situation calls for a probe into adoption and usage issues, which is the area explored in this study. The results of this study provide banks with applicable strategies to effectively design and implement m banking and exploit untapped market potential and attract new users. Moreover, it also serves the expectations of existing customers to enhance business performance, save precious time, money, effort, and above all improve their quality of life. To the best of our knowledge, this is the first study in the context of China that has addressed m banking barriers, and accordingly, our study answers to the recent calls to look into acceptance and loyalty issues.

The remainder of the article is ordered as follows: We address literature review in the next section, followed by the presentation of the research hypotheses, results and discussion of findings, theoretical and practical implications, conclusion, and finally limitations and further study recommendations.

Literature Review

Overview

M Banking is a self-service delivery channel (Püschel et al., 2010), which offers products and services with ubiquitous access for conducting financial or nonfinancial transactions using a mobile device such as a Smartphone or tablet (Spector, 2006). This has become an inseparable part of business today (Afshan & Sharif, 2016) but is still facing strong resistance for its widespread acceptance. This hinders banks and service providers from deriving its competitive advantage (Makanyeza, 2017). M banking is supposed to improve banks’ efficiency and people’s quality of life (Malaquias & Hwang, 2016) and provide them with multiple value-added banking services such as fund transfers, utilities, stocks, and other miscellaneous services (Mehrad & Mohammadi, 2016; Talke & Heidenreich, 2014). The use of m banking services empowers users to input and authorize their own financial and nonfinancial transactions (C. Kim, Mirusmonov, & Lee, 2010) and the same is also acknowledged by banks to their consumers, confirming the status of their authorized transactions (Tam & Oliveira, 2017). But besides all these facilities, mass institutionalization of m banking still remains an unfulfilled dream (Raza et al., 2017), which is being periodically predicted by various concerns. Therefore, the prevailing conditions necessitate identification of barriers blocking users’ attitude and intentions, which can help banks and service providers better understand key factors affecting the use and adoption of m banking (Mohammadi, 2015b; Siyal et al., 2019).

M Banking in China

China ranks first in global mobile subscription with around 90% of its population owning cell phones (Richards, 2015), and Smartphones were expected to surpass 700 million by 2018 (China Internet Watch [CIW], 2015). According to China Internet Network Information Center (CNNIC; 2017), mobile Internet users in China reached 695 million, representing 95.1% of the netizen (Internet users) population, a growth of 5.1% from the year 2015. This rapid expansion in usage of Smartphones and the exceptionally significant increase in Internet users indicate a remarkably potential cushion for m banking. Despite such a giant cellular base and Internet usage, inclination toward m banking has remained quite low, which is ascertained by the undersized adoption rate of 7.1% (Flavián, Guinaliu, & Torres, 2005). Although the total clientage is around 180 million in the top three banks of China (Agricultural Bank of China, Bank of China, and China Construction Bank; Yuan, Liu, Yao, & Liu, 2016), the growth in m banking transactions has only been 5.1% in 2017 (CIW, 2017). This fading facet fortifies the fact that despite a huge Smartphone and Internet usage base, the netizens are still using precursors of m banking for meeting their financial and nonfinancial needs (Mehrad & Mohammadi, 2016; Mohammadi, 2015b).

This resistance from consumers ascertains that technological advances and service availability do not automatically lead to ubiquitous adoption and utilization of latent technologies (Hanafizadeh et al., 2014). It also points out lack of service awareness (Selye, 1946) and perceived benefits that influence adoption and continuity intent of users (Tran & Corner, 2016) by creating multiple usage risks (Luo, Li, Zhang, & Shim, 2010) and enhancing security-related anxiety (Podsakoff, Mackenzie, Lee, & Podsakoff, 2003), which is corroborated by the limited research conducted in this segment (Gillenson & Sherrell, 2002; Mehrad & Mohammadi, 2016; Püschel et al., 2010). These factors call for further investigation to identify core barriers to wider adoption and continued usage of m banking.

The main contribution of our study is in extending the technology acceptance model (TAM) with core barriers such as resistance to change, perceived risk, awareness of services, and perceived benefits, which prevent acceptance of and loyalty to m banking in China, highlighting both users and nonusers and identifying and suggesting fixes to the obstacles. This study sheds light on factors that resist customers from accepting latent technologies such as m banking and keep them bound with traditional banking. Past research has neglected m banking as most of them attended to SMS banking except a few studies that have recently looked at some aspects of m banking such as initial adoption and technological grounds rather than consumer behavior, which are contributed in this study by defining acceptance and loyalty barriers. For generalizing the results, the research sample comprised participants of various age, income, and education levels and were working in different fields. Our study investigated the mediating role of perceived usefulness (PU) and perceived ease of use (PEOU), influencing user behavior indirectly, which is contrary to the studies of Hanafizadeh and Khedmatgozar (2012), Koksal (2016), Makanyeza (2017), and Püschel et al. (2010) who studied the direct impact of these variables on behavioral intention. Therefore, the present study is anticipated to take available literature a step forward to better comprehend various consumer behaviors.

TAM

Prior researches on information systems have reported that users’ attitude plays a crucial role to accept novel technologies (Al-Somali, Gholami, & Clegg, 2009; Davis, 1989). Scholars have been continuously striving to explore factors that deteriorate adoption of latent technologies and enhance acceptance of and loyalty to their usage. Several models have been developed to predict individuals’ inclination to use information systems but TAM has been widely applied in studying information system acceptance (Davis, 1989; Venkatesh & Davis, 1996). This study opted to choose a simple model that could address the prevailing core barriers and lead Chinese netizens to accept m banking. Recently, Poong, Yamaguchi, and Takada (2017) argued that developing countries cannot directly adopt information system strategies of developed countries as they need different researches to fill up knowledge gap. Therefore, considering the lower acceptance rate of m banking in China, we decided to extend the original TAM. The basic TAM was deemed more relevant and suitable for a theoretical foundation to propose conceptual model rather than TAM2 or TAM3 (Salimon et al., 2017). M banking is a relatively new technology and the original TAM is a more appropriate model because it cuts across various settings in both developed and developing countries (Salimon et al., 2017). Because China is a developing country and m banking in China is also at an early stage, the current study considers the original TAM.

TAM proposed by Davis (1989) has been used extensively to measure adoption of various technologies. This model is adapted from the theory of reasoned action (TRA) and postulates that two specific beliefs PU and PEOU primarily determine consumers’ attitude toward using a novel technology. PU concerns the degree to which individuals believe that the use of a specific technology would enhance their job performance, whereas PEOU concerns the degree to which individuals believe that the use of a particular technology would be free of efforts (Davis, 1989). TAM has witnessed individuals’ usage behavior and the factors impacting their acceptance of latent technologies (Venkatesh & Davis, 2000). Intention in TRA is the direct determinant of behavior impacted by attitude. TRA and its extension theory of planned behavior (TPB; Ajzen, 1991) have been vastly utilized and tested in the field of information systems. Later, Venkatesh, Morris, Davis, and Davis (2003) supplemented the information systems theory with a more complete model called unified theory of acceptance and use of technology (UTAUT), which integrated eight established models on technology acceptance. These models were summarized to state that four elements, namely, performance expectancy, effort expectancy, social influence, and facilitating conditions, significantly and directly influence technology acceptance and use behavior.

The chronological relationship between attitude and usage behavior helps to predict acceptance rate of innovations, wherein the prime factors of TAM, PU and PEOU, perform the mediating role of validating consumer attitude and usage behavior toward novel technologies (Akturan & Tezcan, 2012). Besides mediating potential, PU and PEOU can also impact behavioral intention as independent variables (Bankole, Bankole, & Brown, 2011; Davis, 1989). TAM assumes that PU and attitude jointly predict individuals’ intention to adopt a new technology (Davis, 1989) and has been widely recognized due to its capability to better explain users’ inclination to use information systems in comparison with TRA and TPB (Al-Somali et al., 2009; Mathieson, 1991). Yousafzai, Foxall, and Pallister (2010) compared the ability of the three models (i.e., TRA, TPB, and TAM) to determine users’ online banking behavior and concluded that TAM is superior to the other models in terms of predicting consumers’ online banking behavior. Rammile and Nel (2012) concluded that PEOU had a significant positive effect on PU, whereas Makanyeza (2017) in his study of mobile banking determinants in Zimbabwe found that PU had a significant positive impact on consumers’ behavior in accepting m banking services. Alalwan, Dwivedi, Rana, and Williams (2016) used TAM to identify acceptance of mobile banking in Jordan with a convenience sample of 500 bank customers and found that PU and PEOU significantly influenced behavioral intention to adopt m banking. Püschel et al. (2010) conducted a cross-cultural study in Australia and Thailand to investigate factors influencing adoption of m banking and found that PU and PEOU were the primary factors of adoption in both the countries.

Viability and Robustness of TAM

Viability and robustness of TAM have been validated and established in different information system domains decades ago since Davis (1989) introduced TAM based on TRA. TRA elicits salient beliefs of attitude to be more relevant and specific toward the use of latent technologies such as m banking (Benbasat & Barki, 2007). The available literature significantly demonstrates viability and robustness of TAM in technology adoption (Poong et al., 2017). Individuals and organizations in both developed and developing economies around the globe have used TAM to predict adoption and use of latent technologies (Glavee-Geo et al., 2017). Moreover, findings of Shaikh and Karjaluoto (2015) reveal that existing literature on adoption of m banking generally relies on TAM and its modifications. These studies have modified and extended TAM to enhance its power of prediction and explanation in the arena of technology acceptance (Jayasingh & Eze, 2009; Thompson, Compeau, & Higgins, 2006). However, despite a well-established, powerful, and robust model, TAM is still considered incomplete (Brown & Venkatesh, 2005) because it excludes economic, demographic, and external factors (Mehrad & Mohammadi, 2016). Therefore, extant studies have also suggested supplementing TAM with additional variables to better understand and predict technology use behavior (Liébana-Cabanillas, Marinković, & Kalinić, 2017).

Earlier studies of Amin, Supinah, Aris, and Baba (2012), Anderson and Gerbing (1988), Bankole et al. (2011), Chang (2008), Ramayah and Suki (2006), and Venkatesh and Morris (2000) have ascertained that the prime factors of TAM (i.e., PU and PEOU) have proven to be the most constructive elements in predicting acceptance of information systems in different settings such as online ticket reservations (Gurit & Siringoringo, 2013), tele-banking (Sundarraj & Wu, 2005), SMS banking (Amin, 2007; Amin & Ramayah, 2010), mobile phone credit cards (Amin, 2008), mobile website (Zhou, 2011), mobile payments (Hampshire, 2017), e-banking (Salimon et al., 2017), e-payment (Teoh, Choy Chong, Lin, & Wei Chua, 2013), online shopping (Gefen, Karahanna, & Straub, 2003), and mobile shopping (Chen, Hsu, & Lu, 2018). These factors have remained useful and valid to comprehend individual’s behavioral intention to accept various information systems with different user sample sizes of users and software choices (Al-Somali et al., 2009; Wang, Wang, Lin, & Tang, 2003).

According to Davis (1989), TAM can be supplemented with external variables, which may be the reason that TAM is one of the most widely used model. Various studies have extended TAM on different technological aspects, which have been found to be supportive of service industries and acceptance of m banking (Moser, 2015) such as studies on compatibility with lifestyle (Hanafizadeh et al., 2014), word of mouth (Mehrad & Mohammadi, 2016), relative advantage and personal innovativeness (Chitungo & Munongo, 2013), and perceived security (Hsu et al., 2011). King and He (2006) conducted a meta-analysis of TAM including 88 studies that utilized TAM in different settings and termed the model as the most powerful, versatile, and robust with highly reliable predictive capabilities in various contexts. Basic TAM can accurately elaborate acceptance rate of a novel technology such as m banking if the proposed subject and focus are accurate (Al-Somali et al., 2009; Hernandez, Jimenez, & Martín, 2008). In fact, nearly 40% of information systems research has utilized TAM (Hanafizadeh et al., 2014; Siyal et al., 2019).

Conceptual Model and Hypotheses

In this section, we will present core barriers.

Core Barriers

Resistance to change

Innovations demand consumers to switch their existing traditional banking patterns to the latent technologies; this leads to resistance in consumers’ attitude and intention to change their existing banking practices. Agarwal, Rastogi, and Mehrotra (2009) in their study of customer perspectives about e-banking found that traditional ways of banking resist acceptance of novel technologies and bind customers with their long-established banking modes. Consumer resistance to innovations is a normal human response (Laukkanen, 2016) and often appears due to learning requirements for new channels (Kuisma, Laukkanen, & Hiltunen, 2007), but this response prevents acceptance of new technologies along with a risk barrier that results in meager investment returns for banks (Mohammadi, 2015a). Laukkanen and Kiviniemi (2010) argued that consumers only accept latent technologies after they have overcome initial resistance which necessitates identification of barriers and expansion of policies to decrease resistance. Furthermore, Laukkanen and Kiviniemi (2010) explained that communicability with consumers is very essential because it demonstrates that how innovation services and benefits are presented to consumers. Kuisma et al. (2007) claimed that nonadopters suffer from low awareness about novel technologies. According to Elizabeth George (2015), resistance to innovations is globally assumed to emerge from a product’s negative evaluation, which may be due to lack of information about the service or its benefits. Consequently, a higher level of resistance will lead to greater extent of negative attitude toward innovation (Raza et al., 2017). Therefore, to overcome customers’ resistance, awareness of services and benefits is a must, which promises to satisfy their banking needs (Al-Somali et al., 2009) at a risk-free level (Makanyeza, 2017). Hence, we hypothesize that resistance to change negatively impacts attitude and intention through PU and PEOU:

Perceived risk

Bauer (1960) proposed theory of PR to describe customer behavior and ambiguous consequences of their activities. Online transactions carry probability of financial, psychological, and social loss (Hanafizadeh et al., 2014; Im, Kim, & Han, 2008). Mobility enhances risk factor in m banking and poses security threats such as financial loss, personal data exploitation, cell phone theft, or device loss. This is congruent with the findings of Koenig-Lewis, Palmer, and Moll (2010) that PR is concerned with the likelihood of undesirable consequences of an action. Hampshire (2017), in his study of mobile payments, concluded that PR negatively influences PU, which ultimately deteriorates users’ attitude to accept the technology. Gupta and Arora (2017) also found that security concerns have considerably hampered growth of mobile shopping by negatively influencing customers’ attitude to accept it. Makanyeza (2017) argued that intangibility of m banking services is the main reason that hinders consumers in evaluating services prior to actual use and enhances their concern over security issues. Being a remote link, m banking is perceived at a greater risk level in comparison with fixed devices, which is ascertained with the recent research of Püschel et al. (2010) who suggested that despite being customized and context-based, m banking inherently carries higher degree of risk that results in greater negative attitude toward the technology (Wessels & Drennan, 2010). PR is one of the core barriers that affects PU and PEOU through attitude (Akturan & Tezcan, 2012). Henceforth, we hypothesize that

Awareness of services

Acceptance of novel technology depends on how service providers pass on necessary information to their customers about technology services and benefits (Sathye, 1999). Since m banking is a new experience to most customers, a low awareness of technology features is a strong barrier to its acceptance (Mohammadi, 2015a), which causes low customer demand and meager returns on investment. This is congruent with the findings of Laforet and Li (2005) that lack of innovation knowledge and advantages are major barriers in acceptance of online and mobile banking in China. Daud, Mohd Kassim, Said, and Noor (2011) concluded that low awareness of services and advantages resisted customers from using Internet banking. The recent study by Safeena, Date, Kammani, and Hundewale (2012) has argued that nonadopters of online banking are not aware about the service and its benefits. According to Raza et al. (2017), service awareness and advantages lead customers to accept the technology by significantly and positively affecting PU and PEOU. Moreover, service awareness and advantages also minimize different aspects of perceived risk. Henceforth, it is necessary to make individuals aware about novel technologies to motivate them to accept latent technologies such as m banking. Consequently, we posit the following hypotheses:

Perceived benefits

Perceived benefit (PB) comprises efficiency and convenience, which are overlapping concepts in electronic service consumption that consumers cognitively receive as sacrifice or costs (Laukkanen, 2007). Earlier, customers used to buy products with multiple benefits, which corroborates PB as analogous to PU (G. Kim, Shin, & Lee, 2009). Forsythe, Liu, Shannon, and Gardner (2006) argued that PB strongly determines individuals’ adoption behavior of online shopping. They further explained that PB is the positive predictor of customers’ future online shopping intentions. Lee (2009), in their study of Internet banking adoption, concluded that perceived benefits of low cost and speedy transactions at home around the clock inclined individuals to adopt Internet banking. Moreover, Zheng et al. (2006) also found that e-business is significantly and positively influenced by perceived benefits. While in the case of m banking, efficiency and convenience are evaluated as product’s utilitarian and hedonic benefits (Akturan & Tezcan, 2012). This ascertains PB as a significant factor effecting technology’s usefulness and consumers’ attitude and intention for adoption and continued use, thereby necessitating further elaboration to better understand the technology. According to Laforet and Li (2005), lack of awareness of PB proved to be a very strong barrier in adoption and continuity intent of m banking, which needs to be comprehensively passed on to the consumers to smoothen uptake of the technology. Hence, we hypothesize that

PU

PU is a primary factor in original TAM that significantly enhances acceptance of a new technology. It is usually defined as a degree under which individuals believe that use of a novel technology would enhance their job performance (Al-Gahtani, 2001; Davis, 1989, 1993; Mathwick, Malhotra, & Rigdon, 2001). PU plays a vital role to determine customers’ positive attitude toward the technology advantages which ultimately leads them to accept the technology (Mohammadi, 2015a; Tan and Teo, 2000). Ko, Kim, and Lee (2009) found that PU is a strong predictor of mobile shopping intentions in Korea. Raza et al. (2017) concluded that PU is an utmost influential driver of behavioral intention to accept m banking. Liébana-Cabanillas et al. (2017) in their study of mobile commerce concluded that customers accept novel technologies subject to their improved usefulness in comparison with the available alternatives. PU significantly and positively impacts individuals’ attitude toward use of m banking (Al-Somali et al., 2009; Mehrad & Mohammadi, 2016). In fact, usefulness of m banking is one of the main factors that inclines individuals to accept the technology; hence, we posit the following hypothesis:

PEOU

PEOU is also a prime factor of TAM which refers to the extent to which individuals can use a new technology free of efforts (Davis, 1989; Venkatesh & Davis, 2000). PEOU actually defines individuals’ assessment of required efforts to use a novel technology such as m banking (Raza et al., 2017). Extant studies of Hanafizadeh et al. (2014), Luarn and Lin (2005), and Wang and Liao (2007) have found significant positive impact of PEOU on customers’ attitude toward acceptance of and loyalty to m banking. Mazhar et al. (2014) concluded that PEOU is a major attribute in electronic channels of banking and commerce. Recent studies have ascertained that PEOU is a highly influential factor in adoption of mobile commerce (Liébana-Cabanillas et al., 2017), online banking (Al-Somali et al., 2009), mobile payments (C. Kim et al., 2010), and mobile shopping (Ko et al., 2009). Significant positive relation between PU and PEOU (Anderson & Gerbing, 1988; Koksal, 2016; Raza et al., 2017; Safeena et al., 2012) suggests that if the technology is useful and easy to use, then such technology will meet users’ expected benefits and performance and will ensure greater level of acceptance (Shaikh and Karjaluoto, 2015). Makanyeza (2017) argued that when users find that the system is more easy to use, they are more inclined to use it. Customers’ preference to usage ease also invites attention of banks to develop more user-friendly interfaces to motivate their customers to accept latent technologies such as m banking. Henceforth, we posit the following hypothesis:

Attitude and intention

Attitude in TAM is the core antecedent and mediator of variables that affect individuals’ intention to use a new technology (Schierz, Schilke, & Wirtz, 2010). Davis (1989) argued that attitude plays a decisive role in shaping individuals’ intention to use a novel technology such as m banking. Gopi and Ramayah (2007) in their study of online trading system in Malaysia found that attitude and intentional use are significantly interlinked, leading customers toward system loyalty. Gupta and Arora (2017) further explained attitude as individuals’ psychological tendency, which results in positive or negative evaluation about a certain technology or entity. Recently, in the technology acceptance domain, Raza et al. (2017) found that attitude dwells in an individual’s mind, which leads to a behavior showing variations in e-intentions. Therefore, attitude can be used to predict acceptance of a new technology like m banking (Mehrad & Mohammadi, 2016; Mohammadi, 2015a). The findings are congruent with the studies carried out by Merchant, Van Der Stede, and Zheng (2003), Raza et al. (2017), Riquelme and Rios (2010), and Shaikh and Karjaluoto (2015) that individuals’ attitude significantly and positively affects their acceptance of and loyalty to m banking, and hence, we hypothesize that

Conceptual Model

Drawing upon the hypotheses presented in the theoretical framework of the study, the conceptual model is developed in Figure 1. The factors of resistance to change, perceived risk, awareness of services, perceived benefits, PU, PEOU, attitude, and intention are used to test in this model. Table 1 presents the definitions of the entire studied variables.

The hypothesized model.

Definitions of Studied Constructs.

Research Design

Sampling and Data Collection

It is imperative to determine appropriate sample size in survey research (Hair, Black, Babin, & Anderson, 2010), as it is needed for minimizing sampling error. Hence, for this purpose, we opted for power of statistical test (Cohen, 1988; Urbach & Ahlemann, 2010). Researchers generally suggest larger sample size for having better statistical power (Hair, Risher, Sarstedt, & Ringle, 2019; Muskat, Hörtnagl, Prayag, & Wagner, 2019; Umrani, Kura, & Ahmed, 2018). Power analysis is a statistical procedure to find a correct sample size for a given research project (Sabiu, Kura, Mei, Raihan Joarder, & Umrani, 2018). Therefore, to find a minimum sample for the present study, we used a priori power analysis method through G*Power 3.1 software (Faul, Erdfelder, Buchner, & Lang, 2009; Urbach & Ahlemann, 2010). Using parameters such as Power (1 − β err prob; 0.95), an alpha significance level (α err prob; 0.05), medium effect size f² (0.15), and the number of predictors such as of our model, a minimum sample of 129 was found to be required (Cohen, 1992; Faul et al., 2009; Urbach & Ahlemann, 2010). Although our priori power analysis suggested that 129 responses should be acquired, to avoid low response issue, it became necessary to look into other means to determine sample size.

The purpose of this study is to trace out barriers jeopardizing intention of prevailing m banking users and diminishing inclination of nonusers toward the innovation, thereby leaving the far-fetched gains, industry efforts, heavy investments, and expert predictions in vain, creating a very crucial and concerning state to ponder upon the factors deteriorating acceptance of m banking. Henceforth, naturally, our study targeted individuals having both a mobile phone and a bank account. The students and staff of three reputed universities in Hefei were the target population of this study, including both m banking users and nonusers. We attempted to acquire a major portion of the data from students as they are the largest and early adopters of the technologies (Davis, 1989; Hanafizadeh et al., 2014), which eventually filter through older age groups (Afshan & Sharif, 2016). We approached the students and staff of these universities and explained the purpose of our study. They were already maintaining their accounts in different banks. We randomly selected participants from those universities and sent them the questionnaire via emails and WeChat. In the span of 8 weeks from February to March 2018, we succeeded to obtain 200 valid samples from the different universities. The sample strength guarantees robust structural equation modeling (Merchant et al., 2003). We utilized the stratified sampling method, which is considerably consistent with the approach due to its diversity and Cochran’s formula (Stringer, Didham, & Theivananthampillai, 2011) to determine the sample’s representation of a larger society. Our sample proved to be a satisfactory representative as a whole, with a reliability of 90 and denotes appropriate consistency among questions regarding all the constructs:

The collected sample shows justified distribution among gender: males 52.5% and females 47.5%; gender distribution of the sample shows deemed consistency with China’s latest Internet users’ report of 2017 (CNNIC, 2017), which distributes males and females as 52.4% and 47.6%, respectively, proving to be a better countrywide representative. Furthermore, it encompasses different age groups as 45% from age group of 18-30; 25% from age group of 31-40; 17.5% from age group of 41-50, and 12.5% from age group of above 50, respectively. This ascertains that the studied sample is bias free. Table 2 provides the complete picture of the overall demographic uniqueness of the studied sample.

The Demographic Characteristics of the Sample.

Measures and Legitimacy

We measured resistance to change using the scale adopted from Al-Somali et al. (2009); this scale consists of three items. The perceived risk was measured using the scale adopted from Ahmed and Amir (2011); this scale also consisted of three items. The three-item-based scale for awareness of services was adopted from Al-Somali et al. (2009). The Akturan and Tezcan (2012) scale for perceived benefits was adopted with three items. The scales for PU and PEOU were adopted from C. Kim et al. (2010); each consisted of four items. We measured attitude using the scale adopted from Schierz et al. (2010), which consists of three items. Finally, we measured intention by adopting scales from Chen and Lien (2008) and Schierz et al. (2010).

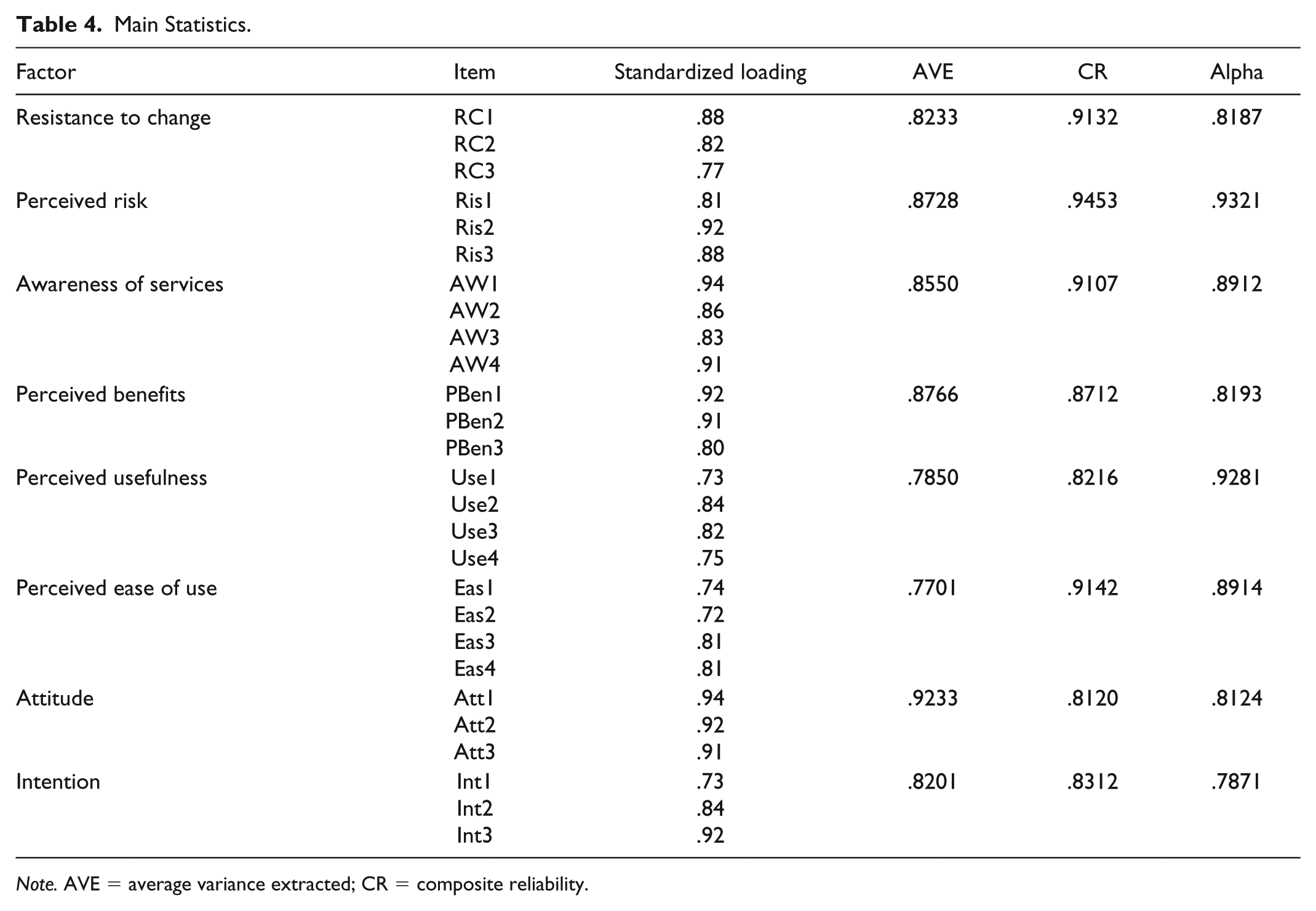

In an attempt to highlight core barriers, we filtered utilized measures from prevailing literature and discussed their validity and reliability with five banking information system experts, and with their invaluable guidance and feedback, changes were carried out. Moreover, to assess the responses, we utilized a 7-point Likert-type scale ranging from 1 (strongly disagree) to 7 (strongly agree), and before launching a formal survey, a pilot test of the adopted measures was conducted on a representative sample of 25 people selected at random. This produced fortified outcomes, and based on the obtained results, we further proceeded to launch the formal survey. Table 4 represents a thorough overview of the measures and factor loadings.

Results

We used SPSS software for the preliminary analysis and data cleaning. The missing values analysis was performed using mean replacement since the missing value pattern was random and the extent of missing values was below 5% (Hair et al., 2010; Schafer, 1999; Tabachnick & Fidell, 2007). Next, the assessment of outliers was performed by following Tabachnick and Fidell (2007). We examined univariate outliers with a cut-off of ±3.29 (p < .001) and we did not find any potential univariate outliers. Second, we examined multivariate outliers using the Mahalanobis distance (D2) test (Hair et al., 2010; Tabachnick & Fidell, 2007b) and found only one multivariate outlier (case number 200), which was deleted from the data set (Hair et al., 2010; Tabachnick & Fidell, 2007). Hence, the final data set for the further analysis consisted of 199 cases. We next examined normality of the data (Reinartz, Haenlein, & Henseler, 2009) using histograms (Field, 2009; Tabachnick & Fidell, 2007) and found that the data of the present study follow a normal distribution pattern (Figure 2).

Normality.

We performed assessment of multicollinearity by examining the variance inflated factor (VIF); our assessment found that VIF values (Table 3) for each latent variable were below the suggested threshold (Hair, Ringle, & Sarstedt, 2011). Thus, multicollinearity was not a problem.

VIF Scores.

Note. VIF = variance inflation factor.

Common method variance (CMV)

The present study attempted to minimize the influence of CMV using various procedural remedies such as informing participants about the fact that there are no right and wrong answers, ensuring confidentiality, improving survey scale items by pretesting with truly representative respondents, and by choosing more simple language (Mackenzie & Podsakoff, 2012; Podsakoff et al., 2003, 2012). Second, we used Harman’s single factor test for examining CMV (Podsakoff & Organ, 1986). Our assessment indicated a cumulative of 15.19% variance, with the first (largest) factor explaining only 3.95% of the total variance, which is less than 50% (Kumar, 2012). Moreover, the results depict that not even a single factor accounted for the majority of covariance in the predictor and criterion constructs (Podsakoff et al., 2012). It therefore suggests that the common method bias is not a major problem in this study.

Choice of statistical analysis

The structural models were examined either by employing a covariance-based approach (Bock & Bargmann, 1966; Byrne & Van De Vijver, 2010), variance-based approach, or partial least square structural equation modeling (PLS-SEM; Chin, 1998; Henseler, Ringle, & Sinkovics, 2009; Wold, 1974). We selected PLS-SEM due to the reasons that (a) it is preferred over other multivariate approaches that are traditional (Haenlein & Kaplan, 2004); (b) we chose PLS-SEM due to its ability for the simultaneous estimations of the hypothesized relationship, as reflected in the structural model and relationships between indicators and their corresponding latent constructs as reflected in the measurement model (Hair, Hult, Ringle, & Sarstedt, 2016; Hair, Ringle, & Sarstedt, 2013; Henseler et al., 2009); (c) PLS-SEM was selected due to the fact that it delivers estimates that are statistically reliable based upon a bootstrapping method, which produces standard errors for path coefficients (Hair et al., 2013, 2016; Kock, 2014); (d) the focus of the present study is prediction (refer Figure 1—conceptual framework of the study) and hence, PLS-SEM was deemed appropriate (Hair et al., 2016). In addition to the user-friendly interface of SmartPLS (Henseler, Ringle, & Sarstedt, 2015), ability to handle small samples, and non-normal data, we choose this technique due to the complexity of our research model (Urbach & Ahlemann, 2010). Finally, PLS-SEM is experiencing widespread application as a popular method for data analysis (refer, for example, Hair et al., 2019; Muskat et al., 2019; Sabiu et al., 2018; Sarstedt et al., 2019; Umrani et al., 2018). Therefore, it was opted for analysis purpose.

Looking at the guidelines from the popular literature on PLS-SEM, the following two-step approach was adopted; we first examined the measurement model and then tested the structural model for hypotheses testing and predictive capability assessment (Hassan, Hassan, Khan, & Iqbal, 2013; Henseler et al., 2009). First, we ascertained inter-item reliability through evaluating factor loadings and maintained a threshold of .70 (Hair et al., 2016); we next examined convergent validity by looking at average variance extracted (AVE) and all the AVE values for latent variables were greater than .50 (Bagozzi, Yi, & Phillips, 1991; Chin, 1998; Fornell & Larcker, 1981; Gefen, Straub, & Boudreau, 2000); similarly, we then evaluated internal consistency reliability through examining composite reliability (CR) scores with a minimum threshold of .70 or above and Cronbach’s alpha with a threshold of .70 or above (Bagozzi et al., 1991; Chin, 1998; Fornell & Larcker, 1981; Gefen et al., 2000; Hair et al., 2016). Our results presented in Table 4 indicate that the entire above threshold was successfully achieved.

Main Statistics.

Note. AVE = average variance extracted; CR = composite reliability.

Discriminant validity—HTMT

Due to recent criticism on the criterion by Fornell and Larcker (1981), we used the heterotrait–monotrait ratio of correlations (HTMT) method, which is based on the multitrait–multimethod matrix (Henseler et al., 2015), to determine discriminant validity. Accordingly, if the HTMT value is greater than HTMT0.85 value of 0.85 (Kline, 2011), or HTMT0.90 value of 0.90 (Gold, Malhotra, & Segars, 2001), then there is a problem of discriminant validity. As all the values passed the HTMT0.90 (Gold et al., 2001) and also the HTMT0.85 (Kline, 2011), it indicates that discriminant validity has been ascertained (Table 5).

Discriminant Validity (HTMT Ratio).

Note. PEOU = perceived ease of use; PU = perceived usefulness; HTMT = heterotrait–monotrait ratio of correlations.

HTMT is the advanced method to Fornell and Larcher criterion.

Hypotheses Test

As per guidelines of Hassan et al. (2013) and Henseler et al. (2009), the second step was to assess significance of the path coefficients. We used bootstrapping procedure with 5,000 subsamples method (Hair et al., 2011) through SmartPLS 3.2.7 software (Ringle, Wende, & Becker, 2015). Our results indicate empirical support for all the hypothetical relationships (Figure 3 and Table 6).

Structural model results.

Path Coefficients and Significances.

Note. CI = confidence interval; PEOU = perceived ease of use; PU = perceived usefulness.

Predictive power of the model

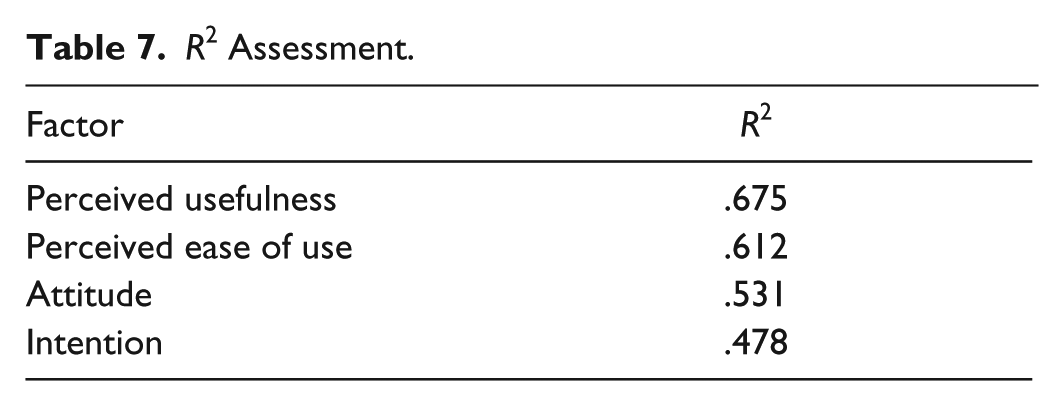

We examined R2 for determining predictive power of the model. Using PLS algorithm in SmartPLS, to compute R2, we found R2 value of .67 for PU, .61 for PEOU, .53 for attitude, and .47 for intention. According to Falk and Miller (1992), these R2 values are acceptable as they are above the .10 threshold in social science research. These scores are further presented in Table 7.

R2 Assessment.

We next examined effect size; this assessment is necessary for determining the relative effect of exogenous variables over dependent variables (Chin, 2010). As per guidelines drawn by Cohen (1988), the f2 value of 0.02 is considered small, 0.15 is considered as medium, and 0.35 is considered as large effect size. The results of our analysis related to f2, for further consideration, are presented in Table 6.

Finally, we conducted an assessment of relevance of the dependent variables of our model by evaluating Q2 (Fornell, 1994). The assessment of Q2 was performed through a blindfolding procedure by looking at cross-validated redundancy (Fornell, 1994). According to Chin (1998), if the obtained Q2 value for the dependent variable is greater than zero, it suggests that the model demonstrates predictive relevance. Our results are provided in Table 8 indicating that our model successfully demonstrates predictive relevance.

Predictive Relevance Assessment.

Note. PEOU = perceived ease of use; PU = perceived usefulness; SSE = sum of squares of prediction errors; SSO = sum of squares of observations.

Discussion

Drawing upon the results, which show banks’ concern over relative benefits of m banking such as lower costs and higher returns. This latent technology has prompted the banking industry to launch several value-added services that are aimed to retain their own consumers and attract others. In doing so, banks are opting to maximize their competitive advantage by enhancing their service domains and thereby curtailing their overheads. So far, growth rate has not yet fortified their anticipations. Therefore, besides these endeavors, banks need to fix traced out barriers that jeopardize consumers’ usage and continuity intentions. The current study elaborates several barriers deteriorating customer attitudes toward m banking usage and intention stability. The factors incorporate resistance to change, perceived risk, awareness of services, and perceived benefits. The analytical results show that the research model examined in this study is acceptable and contributes to the existing literature. We have tested our hypotheses using bootstrapping procedure. All the hypotheses have been supported except Hypothesis 5.

Empirical analysis revealed several important findings, interpretations, and implications founded upon the analysis as discussed in the following: findings reveal that m banking awareness of services left a substantially positive effect on attitude and led into further inquiry of the technology and its perceived benefits. This creates an instinct toward technology adoption, when the customers perceive that m banking saves time, offers a wide range of services, and can save the transaction handling charges. They develop a positive attitude and intend to use m banking applications. Lack of awareness stood out as a barrier to adoption of m banking, which agrees with Elizabeth George’s (2015) study that awareness of technology leads customers toward further inquiry of the innovation, which ultimately results in their intention to use new technology. Although impact of awareness of PU was rejected, it is accepted that it has a significant effect on PEOU, and influence of PB on both PU and intention was also found significant. Therefore, customer awareness of services and their PB should be emphasized by banks because impact of awareness about services mediates through PEOU on intention to use m banking, whereas effect of PB, besides affecting PU, directly influences customer intention to use m banking. Thus, besides traditional advertisement tools, such as leaflets, brochures, and text messages, banks should also focus on social networking sites as their advertisement tools and place visual-based m banking advertising material on social networks to educate both users and nonusers.

Consequently, it would prove beneficial for users to continue using m banking, and it would also be helpful for nonusers by arousing inclination toward using m banking, as most of the Chinese netizens remain regular visitors of various social networking sites. Banks should also arrange potential customer training sessions in their bank branches/field offices or customer/user target locations such as industries, associations, companies, universities, colleges, libraries, and so on to pass on necessary information of the services and their benefits to customers and resolve their usage barriers by helping them out with hands-on practice.

Resistance to change was found to have a significant negative effect on m banking adoption in the studies carried out by Al-Somali et al. (2009) and Mohammadi (2015a). In this study, resistance is also identified to have a significant effect on users’ attitudes toward m banking usage because low awareness of services and their benefits creates multiple risks in users’ minds, which ultimately causes customers not to adopt or use it. Perceived risk also positively affected attitude, resulting in users’ unwillingness to adopt m banking, which agrees with the findings of D’Souza (2002) that new products inherently contain risks that result in avoidance. Online and mobile banking comparatively encompass greater risk than traditional banking (Selvaraj, 2009) as it causes fear in users regarding their personal data and bank balance being virtually exploited. This keeps them reluctant toward the usage of technology. Therefore, banks need to enhance customer confidence regarding safeguarding of their passwords, personal data, financial transactions, and security of their system as a whole. Equipments of the existing systems with latent prototypes such as biometrics and voice patterns are highly commendable to minimize risk.

Role of PU and PEOU remained significant in determining customer attitudes toward m banking adoption and continued use, which is in line with the studies conducted by Koenig-Lewis et al. (2010), Mehrad and Mohammadi (2016), and Thakur (2014). Therefore, it necessitates banks to upgrade systems to the preferential levels of users, so users find it easier to manage their m banking accounts that offer a wider variety of banking services with a better uninterrupted network. Thus, seeing the positive impact of PEOU on PU and the mediating role among attitude and usage intention, it is compulsory to improve the prevailing system to be more user-friendly, with greater focus on retaining the existing users and to arouse inclination of the nonusers to adopt m banking. Nevertheless, usage ease and usefulness denoted noteworthy mediated potential on attitude in terms of diverting users to switch from their traditional banking practices to the latent innovation. Our study revealed that low awareness of services and their PB came out as a major hindrance for leaving the stone unturned, and this situation is then dominated by resistance to change and perceived risk. Hence, it is recommended to spread utmost awareness of services and their PB to minimize users’ resistance and perception of risks. Customer perspectives should remain fundamentally focused while developing systems: as execution of enhanced m banking communication strategies would definitely prove more productive than mere upgradation of product strategies (Laukkanen, 2007; Siyal et al., 2019).

Theoretical and Practical Implications

The study significantly extends the existing information system literature in China in terms of latent technologies such as m banking, which needs to be further evaluated. This study attempts to fill the gap by highlighting the basic inhibitors to m banking acceptance and loyalty and ensuring its adoption and continued use. The statistical perspectives of the empirical results duly support TAM and the external variables of resistance to change, perceived risk, awareness of services, and their PB to predict the customers’ adoption and continuity intention. The results are significant and anticipated to help develop both theory and practice of acceptance and usage of new technologies.

Our research findings ascertained significant positive impact of awareness regarding services and their relative benefits on the attitude of netizens in China because most of them are unaware of the latent technology services and benefits, which is ascertained with an undersized adoption rate of 7.1% (Flavián et al., 2005). Although the total clientage is around 180 million in the top three banks of China (Yuan et al., 2016) the growth in m banking transactions has only been 5.1% in 2017 (CIW, 2017). The relatively small number of users to m banking ascertains lack of research in the Chinese context. To overcome customers’ resistance and risk perceived in the novel technologies, banks should formulate prioritized marketing strategies aimed at educating consumers regarding newest technology services and benefits. The design of marketing campaigns should involve customers to systematically experience m banking through dummy applications prior to their actual transactions. Such experience could straight away minimize their resistance and the negative impact of low awareness regarding services and benefits on PU and PEOU and encourage them to use m banking. Comparative awareness campaigns differentiating m banking services and benefits from traditional banking would be commendable as such campaigns could explain to customers that using m banking, they could make all types of financial and nonfinancial transactions without any spatial and temporal limitations besides saving their valuable time, efforts, and money, whereas traditional banking requires visiting bank branches in person to make any transaction, thereby consuming plenty of time, effort, and money within a restricted timeframe. Awareness can be created that transactions including fund transfers, balance inquiry, checkbook issuance, account statement, and so on can be easily performed using m banking.

Banks can use social media for customer awareness by ensuring availability of visual-based material such as customer training videos, product information, and other value-added services on YouKu and QQ.com, which are the most popular among Chinese. We recommend banks to create their channels at YouKu and QQ.com and place videos that focus on customers and guide them to attract new users. Availability of tutorial videos on YouTube, Facebook, and Twitter could also advance technology adoption rate (Alalwan et al., 2017). Awareness minimizes customers’ resistance and perceived risk of the technology and proves helpful to attract new customers. Infact, PU and PEOU mediate indirect effect of awareness on behavioral intention to utilize m banking. Therefore, banks need to arrange training sessions with trial versions of latent technologies like m banking, wherein customers become aware of the technology functionalities by executing dummy transactions. Such sessions would boost up customer confidence to accept the technology and recommend them to their near and dear ones. According to Liébana-Cabanillas et al. (2017), users who have benefited from such awareness trainings and educational campaigns will spread positive word of mouth to attract new users.

Consumers who are conversant with system functionalities will be able to overcome resistance and the risk prevailing in their minds. This is a direct result of the fact that when consumers are unfamiliar with the technology services and benefits, they perceive multiple safety risks such as privacy and financial loss. Therefore, it necessitates banks to equip latent systems with novel prototypes such as voice pattern or biometric and to launch campaigns that highlight banks’ policies that aim to protect and safeguard customers’ financial and personal information. Such campaigns could be more beneficial to mitigate consumers’ perception of risk. In addition, banks should also initiate consumer-centric campaigns emphasizing banks’ role in the cases where m banking transactions have failed or have been misreported. Such campaigns should also include the reversal or remedial timelines of these unsuccessful transactions as it could fix consumers’ resistance and lead them to accept m banking. Banks should offer toll-free numbers to their customers as the lengthy process to queue up to connect with a call-center agent and go through the verification protocols becomes costly, and in case of call drop instances, customers have to repeat the whole procedure again. Due to the limited number of agents in call centers and outsourced customer-care facilities, customers have to line up for inquiring any services or products, and their complaints and grievances also take a longer time to be resolved. This long and expensive mechanism resists consumers from accepting m banking and binds them to traditional banking. Provision of toll-free calls to the customer service center could be more beneficial to promote m banking in potential users and persuade customers to inquire new products and services.

The positive effect of the basic TAM factors (PU and PEOU) on customer attitudes toward m banking acceptance and loyalty has been ascertained in this study. Customers prefer advantageous and effortless technologies that are congruent with other systems. For instance, experience of smooth and effortless transactions at point of sales would enhance customers’ confidence that their m banking account is compatible with other systems and such satisfied consumers would remain loyal to the technology and would rather spread positive word of mouth that could attract new users. Hence, it is necessary for banks to provide most compatible and user-friendly interfaces with a wide range of services and an uninterrupted network. This will in turn be helpful for banks to retain existing users and attract new users. However, the mediated role of PU and PEOU proved to have a strong effect on users’ attitudes to exit traditional banking and accept m banking.

Conclusion

M banking is a breakthrough technology in the banking sector. Its novelty, ease, and usefulness have attracted a huge interest in researchers to investigate the factors that hinder acceptance of this technology. The lower acceptance rate of m banking in China, despite the large number of Internet users and Smartphone holders generated the necessity to conduct this study and highlight factors that are preventing the Chinese bank customers from adopting this latent technology. The delayed acceptance of latest innovations is also due to the reason that few studies have been conducted to address the relative issues of technology adoption and use. In the context of China, little is known about the factors that affect acceptance of and loyalty to m banking. Therefore, to fill this gap, our study had an objective to investigate the main factors which prevent Chinese netizens from using m banking. While considering lower acceptance rate and lack of studies addressing issues of technology acceptance in China, there was a need to come up with a theoretical foundation which could deal with the important aspects of intention and adoption. Keeping in mind the different knowledge gaps of developing countries such as China, we selected basic TAM and extended it with four latent variables of resistance to change, perceived risk, awareness of services, and perceived benefits. The study aimed to explore the effect of these latent variables on acceptance of and loyalty to m banking in China.

Our study extends the empirically grounded theory that attitude predominantly influences future m banking usage behaviors. Therefore, we selected to study the basic inhibitors preventing consumers from accepting m banking, and to better comprehend consumer behaviors, the mediating role of TAM’s prime factors (i.e., PU and PEOU) was adopted. The results brought invaluable insights and applicable strategies and designs for bank managers and marketing departments in the industry.

Our study is unique in the following aspects. First, we analyzed the basic inhibitors to consumer behaviors that bind them to traditional banking practices and prevent consumers’ acceptance of and loyalty to the latent technologies, rather than the technological aspects of m banking that have remained the focus in past researches in this area. Second, past studies mostly focused on SMS banking (Mehrad & Mohammadi, 2016), except a small number of recent studies that have looked at the technological aspects of m banking (Sharma et al., 2017) neglecting user behaviors, whereas others considered motivational factors toward m banking (Lawler, 1990) without considering loyalty perspectives. Recent studies of Mohammadi (2015a) and Sharma et al. (2017a) have neglected nonusers, the giant and untapped market and prospect customer base for latent technologies like m banking. A review of the past literature ascertains that barriers to overcome consumer resistance have not yet been well evaluated (Mehrad & Mohammadi, 2016), thereby creating a dire need to identify and fix such inhibiting factors (Aboelmaged & Gebba, 2013). Consequently, our study contributes to explain inhibitors to m banking, which hinder customers’ acceptance of and loyalty to latent innovations, focusing on both users and nonusers. Third, the studied sample consists of a mixed population with different age, income, and education levels, including a major proportion of students as they are the largest and early adopters of new technologies (Afshan & Sharif, 2016; Mohammadi, 2015a) and older age individuals (Luo et al., 2010), which ensured generalizability of results. Fourth, our study contributed to identify the significance of the mediating role of TAM’s prime factors, which is contrary to the results of Koksal (2016) and Püschel et al. (2010) who explored the direct effect of PU and PEOU on user behavior; hence, this study is a step forward in understanding fundamental inhibitors to consumer acceptance of and loyalty to m banking.

Limitations and Directions

While investigating acceptance of and loyalty to m banking in China, the authors of this study faced several limitations. First, the study looks at the existing bank account holders ignoring the nonaccount holders. Second, the majority of participants possessed a graduate degree, which could be problematic to represent as a whole. Third, the study did not include demographical factors, which could have affected the findings. Finally, the study has been conducted through the cross-sectional model, which identifies user behaviors for a specified time frame. Therefore, we recommend future studies to conduct a longitudinal survey to find out consumer variations over time and also incorporate demographical factors to explore the effect of gender, age, income, and education.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.