Abstract

This article differentiates the euro-economies in terms of the degree of synchronization with the cyclical position of Germany perceived herein as a hegemon economy. The purpose of this study is the identification of the euro-economies that can be identified as an effective monetary area in terms of similarity in economic structure with German economy. The cyclical position is expressed as an average of absolute values of differences of the output gaps between euro-countries and Germany. This procedure is supplemented by correlation and comparative analysis and with the assessment of empirical findings. Two groups are identified according to similarities in cyclical positions. Similar economic performance was ascertained in Austria, Belgium, France, Luxembourg, the Netherlands, and Finland, the economies of which are thus labeled as an effective currency region in the sense of optimum currency area. The assessment of the future development in Eurozone is made taking into account the current political and economic circumstances and the outputs of empirical analyses.

Introduction

“The art of economics consists in looking not merely at the immediate but at the longer effects of any act or policy; it consists in tracing the consequences of that policy not merely for one group but for all groups” (Hazlitt, 1946, p. 1). This thesis was, according to some economists (e.g., Krugman, 2013), ignored in the case of the single currency euro introduction.

The theoretical and empirical aspects of the single monetary policy were studied by many authors; among those studies, Mundell (1961) can be seen as one of the most significant contributors. Mundell in his early work provided an analytical framework outlining the conditions for the thriving functioning of the monetary union. The main prerequisite of successful monetary integration is linked to the characteristics of the geographic area that has a high degree of labor mobility factor inside and vice versa labor immobility factor outside (the optimum currency area). For that reason, such an area should have one currency inside and outside; it should have a flexible exchange rate; the labor mobility is seen as a substitute for the exchange rate variability. As regards the idea of monetary integration of Europe, Mundell literally says, “The question thus reduces to whether or not Western Europe can be considered a single region, and this is essentially an empirical problem.” In his later work, Mundell extended his analysis with a requirement for the stability of the purchasing power of the integrated currency region (Fleming, Johnson, & Swoboda, 1973, p. 1).

Krugman (2013) perceived Mundell’s theory of the optimum currency area as a theory about finding a balance between potential gains and losses in a qualitative sense. The success of monetary integration is conditioned by the existence of labor mobility, a similar economic structure, and fiscal integration (Kenen, 1969). The argument for the requirement of the compliance of a similar economic structure of the participating states is to minimize the occurrence of such asymmetric shocks that would otherwise require different monetary policy interventions (i.e., an effort to reduce cyclical heterogeneity in the monetary union conjugate countries). The argument for the fiscal integration policy leans on utilizing the opportunity of mutual insurance against the asymmetric development of united economies; in such a case, it is possible for the country affected by a negative shock to obtain a positive net transfer from a country not affected. Fidrmuc (2015) remarked that if the asymmetries are temporary, the effects of such an applied “suboptimal” fiscal policy are short term and may be offset by the benefits of risk sharing under the terms of mutual fiscal insurance. However, if the shocks are of a permanent nature, fiscal transfers will become largely deterministic and unidirectional with long-term costs burdening the donators.

The economic slump in Europe activated by the 2007 financial crisis renewed the debate about the relationship between the economic cyclicality of the participating countries and the efficiency of a monetary union in a situation of a nonexisting fiscal stabilization mechanism, limited mobility of labor factor, and economic heterogeneity of the member states (this issue was analyzed based on empirical data given in Montani, 2011, or Collignon, 2013).

In the context of the 2007 financial crisis, Fingleton, Garretsen, and Martin (2015) examined the vulnerability of heterogeneous economies bound by the euro. Their findings indicate that the larger the asymmetry of shocks across regions sharing single currency is, the more this area deviates from the optimum currency area in terms of the monetary policy implemented. Cancelo (2012) presented empiric evidence that the foundations, which explain the formation of the national cycles across the European Monetary Union aggregated through the crisis, were already latent in 2007.

Several authors have examined the influence of German interests on the formation of the European monetary policy. Kaltenthaler (2002) argued that the nature of the European monetary policy was influenced by German economic interests rather than the interests of European policy elites. From another perspective, the nature of the European monetary policy has been examined by Bulmer and Paterson (2013). It focused on the analysis of the evidence of the hegemonic role of Germany, which is considered to be a key player in the field of EU policy (Krampf, 2014); specifically, it deals with the interaction between Germany and the European Central Bank and the European Commission. Also, De Grauwe in 2013, saw the political objectives behind the decision to create the euro as a common currency with Germany and France being the main players in this field; as for France, its inferior position that it occupied in the European Monetary System initiated a proposal of monetary union (as justified in Jabko, 1999, in detail); as for Germany, the ultimate goal of unification was to perennially link the fates of France and Germany and thus to eliminate the danger of future wars on the European continent (Ash, 2012).

The purpose of this article is to differentiate the euro-economies in terms of the degree of synchronization with the cyclical position of Germany (hereinafter “reference region”). The cyclical position mirrors itself in the economic cycle in which euro-countries are found at a given time when compared with the reference region. Within the analysis, the assumption of the economic and political hegemony of Germany is accepted (based on the profound quantitative and qualitative analysis and rational arguments found in Paterson, 2011, and Bulmer, 2014). The synchronization/nonsynchronization of euro-economies with the reference region is assessed by means of a statistical and comparative analysis of the output gaps of gross domestic product for the period 2002-2016 (the data source was a publicly accessible database: OECD.stat, 2016). Artis, Krolzig, and Toro (2004) performed empirical analysis, which showed that larger differences in output gaps indicate a more serious fluctuation in the phase of the economic cycle.

Methodological Approach

The analysis of cyclical synchronization/nonsynchronization of the monitored euro-economies entering the Eurozone before and inclusive of 2002 compared with the German economy in the period 2002-2016 of the economic cycle is based on the quantification of the average difference of output gaps (Miles & Vijverberg, 2016, assessed cyclical synchronization of Eurozone by means of a method of switching Markov models examining the changes in output). The output gap of each economy in a given year is the difference of the real product (Y) and the potential product measured in percentage of Y. The average of absolute values of differences of the output gaps of the monitored economies (

The criterion defining the interface between the cyclical synchronized and unsynchronized euro-economies is the geometric mean of the average deviations

The imperfections of the criteria Y discussed by van den Bergh (2009) are disregarded. Furthermore, it is assumed that the potential output approximately expresses the highest sustainable performance of the economies under the condition of disposable amount and quality of factors of production (Durlauf & Blume, 2008).

Potential product is considered to be a relatively good criterion for depicting the state of the economy in the absence of demand and supply shocks in all markets (Gerlach & Smets, 1999). Although the identification of the disparity between the real and potential product is ambiguous (it is not clear to what extent it is, for example, a negative demand shock or a negative supply shock—both types of shocks within the metrics used reflect in the same direction, that is, in decline in the real output, though the monetary policy response may not be identical), it can be considered as an acceptable summarizing criterion (Apel & Jansson, 1999). We agree with Mandel and Tomšík (2015) who consider the synchronization appraisal of economies according to the growth rate as incorrect. The growth rate is a variable capturing the growth/decline of real product due to past performance expressed in percentage, which insufficiently indicates the phase of the economic cycle in which the economies are found. The product growth rates may be similar, although the phases of the economic cycle are fundamentally different and require different interventions of monetary policy (Grossman & Helpman, 1993).

Analysis of Cyclical Heterogeneity of Euro-Economies According to Output Gaps

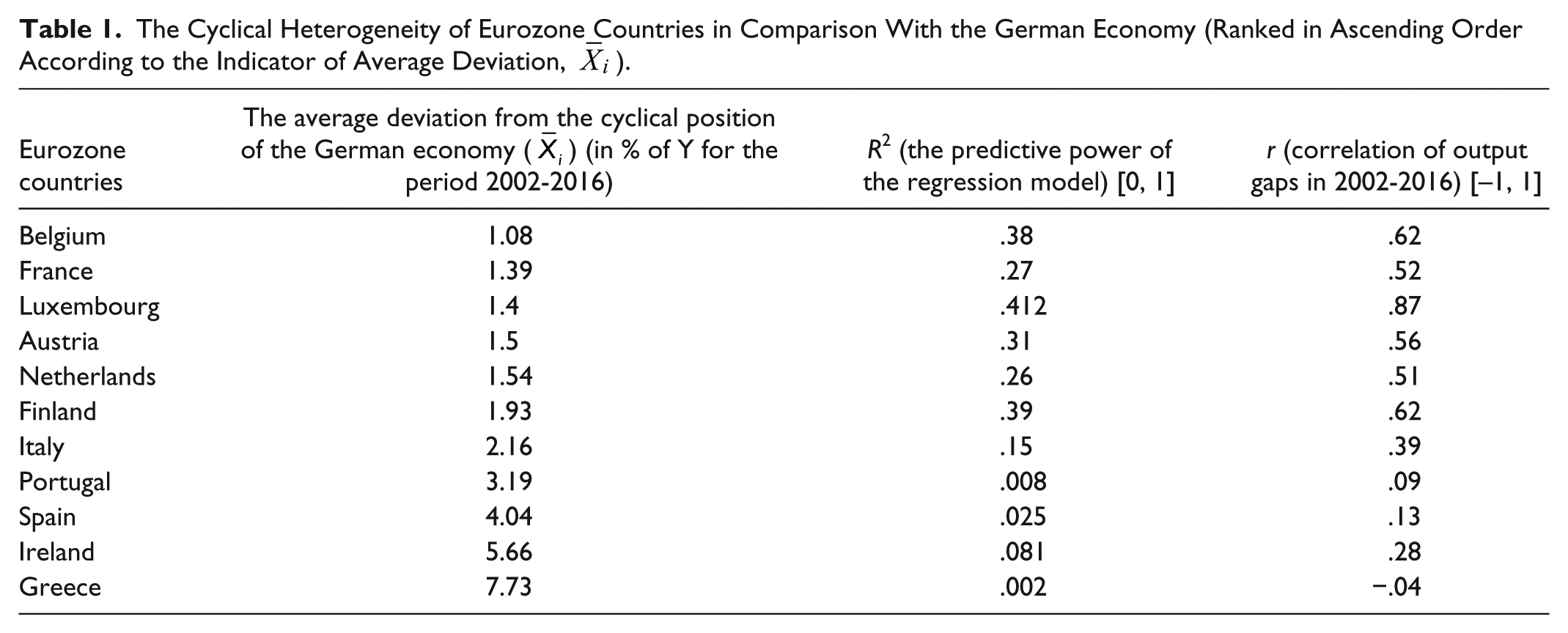

The impacts of demand and supply shocks on the Eurozone countries during the period 2002-2016 depict the respective positions of cyclical deviations of the monitored economies from the cyclical position of the reference economy. The cyclical deviations calculated according to Equation 1 are summed up in Table 1. The higher the value, the greater the divergence of the cyclical position of the countries surveyed compared with the reference region.

The Cyclical Heterogeneity of Eurozone Countries in Comparison With the German Economy (Ranked in Ascending Order According to the Indicator of Average Deviation,

According to the criterion of “synchronization,” it is possible to identify the degree of similarity of the economic cycle in Austria, Belgium, France, Luxembourg, the Netherlands, Finland, and Italy (further referred to as Group I) with the German economy. Similar development is identified in the countries whose average deviation from the cyclical position of Germany is located in the range [0, 2.3] percentage of Y in the selected period (see Table 1). The upper border value 2.3 is given by the geometric mean of the average deviations (see Equation 2). Conversely nonsynchronization is identified in the case of Ireland, Greece, and Spain, and to a lesser extent in Portugal (the property of asynchronous development of the cyclical position is related to economies whose average deviation from the potential product is higher than 2.3% of Y compared with the reference region—further referred to as Group II).

The correlation coefficients r as well as the coefficients of determination R2 (see Table 1) can be considered as the implementation of statistical relations between the values of the output gaps of the reference region and the surveyed euro-economies. These statistical measures are widely used to explain macroeconomic relations, for example, in Bianchi and Civelli (2015), Kiley (2013), or Havránek (2010). However, as Den Haan (2000, p. 3) pointed out, “unconditional correlation coefficients lose significant information about the dynamic aspects of the co-movement across variables.” In case of nonstationary variables, the unconditional correlation produces spurious estimates—as they do not imply causation. Therefore, it is necessary to consider their substantive contribution to the analysis according to other standards. The degree of similarity in terms of r and R2 is, therefore, assessed by means of the comparative approach whose results are captured in Figure 1. The regression lines there define a relationship between the reference region and the surveyed euro-economies. This relation leans on the assessment of the cyclical positions of the euro-economies of Ireland, Greece, Luxembourg, and Austria, and the reference region by means of the analysis of annual deviations from the potential product for the period 2002-2016.

The output gaps in percentage of Y of the reference region versus output gaps in euro-countries Ireland, Greece, Luxembourg, and Austria.

The relationship between the components of the cyclic position of Ireland and the cyclic position of the reference region (see the upper left graph of Figure 1) exhibits a low value of the coefficient of determination (R2 = .08) as well as a low value of correlation (r = .28). From Figure 1, it can be specifically learnt, for example, that when the output gap in the reference economy was above the potential by 0.71%, 2.57%, 0.59% and 0.03% of Y, the corresponding values of output gaps in Ireland amounted to 8.46%, 9.42%, –6.31%, and −4.51% of Y. In the case of the under potential values of −1.58%, −1.75%, and −1.9% of Y of the reference region, the Irish output gap was 7%, 7.02%, and −7.15% of Y. From this, the disproportion in the cyclical positions can be clearly seen. The right upper graph compares the output gaps of the reference region with the output gaps of Greece also revealing a strong disparity in the economic cycle (R2 = .002, r = –.04). The relationship between the output gaps of Germany and Luxembourg (see the bottom left graph of Figure 1, with R2 = .412, r = .87) shows substantial synchronization compared with previous cases. This also applies for Austria (R2 = .31, r = .56), whose position of the output gaps of Y compared with Germany is shown in the bottom right graph of Figure 1. The same can be concluded in the cases of Belgium (R2 = .38, r = .62), France (R2 = .27, r = .52), Netherlands (R2 = .26, r = .51), and Finland (R2 = .39, r = .62).

Discussion

The monetary transmission mechanism being changed by the euro introduction has in general resulted in different responses in the two groups of euro-economies (see analytical part above). On the basis of a distribution of the euro-countries to Group I and Group II, let us consider that the Group I has not been significantly weakened by the single monetary policy effects. Euro-economies with the severe cyclical deviations of Group II can, however, be deemed as more or less disadvantaged by the single monetary policy. De Grauwe and Foresti (2016) gave reasons for such a distribution pointing to the loss of ability of these economies to improve the strong asymmetric division by an appropriate manipulation of exchange rates to correct the real flow of goods and services within international trade and to appropriately influence national interest rates (Coudert, Couharde, & Mignon, 2013).

The empirical development of euro-economies studied in Barigozzi, Conti, and Luciani (2014) and Duwicquet, Mazier, Petit, and Saadaoui (2015) pointed to the strong cyclical heterogeneity of Italy owing to the idiosyncratic nature that can barely be coordinated by the single monetary policy (

The Heterogeneity in Outputs Gaps (percentage of Y) of Ireland, Portugal, Greece, Spain, and Italy Compared with the Output Gaps of Germany in 2015 and 2016.

Updating the statistical outcomes of the analytical section with these empirical findings and scientific analyses, Ireland, due to its productive recovery, can be perceived as a part of Group I; on the contrary, Italian after crises development resembles the euro-economies of Group II rather than the economic development in Group I. The question of whether or not Europe can be regarded a single region in terms of a similar level of economic performance can be positively answered in the case of Austria, Luxembourg, Belgium, France, Finland, and the Netherlands. This result corresponds with Regan (2017), who claims that uniting together two dissimilar macroeconomic regimes (domestic demand-led models, which prevail in southern Europe, and export-led models, which predominate the area of northern Europe) is the real origin of the euro crisis. From the short-term analysis point of view, Ireland can be included as well. Since the financial crisis in 2007, persistent heterogeneity is identified in Greece, Spain, Portugal, and Italy. This result is supported by Miles and Vijverberg (2016), already referred to in the methodological part, whose empirical analysis led them to conclusion that adoption of a single currency increased synchronization trend for nations ready for a single currency (namely the states of Group I), but it increased desynchronization of nations that were far from being synchronized before monetary unification (namely the states of Group II).

The results imply that single monetary policy and a single exchange rate cannot work in the conditions of structurally different economies (Fabbrini, 2013). This is probably an irreparable structural defect, which can be hardly healed by means of stabilization funds (Griffith-Jones & Ocampo, 2009). Under the current political and economic circumstances, we are inclined to the opinion of Sinn (2014), who, based on empirical data and the past and current political and economic development in the European Union, submitted rational arguments of the future development in Eurozone:

The currency union will not fall apart; the countries extremely affected by the adoption of the euro will remain the part of it.

Much of the debt of the highly indebted states will be forgiven so that they could revitalize.

The view of survival of monetary union in the present state is also shared by Eichengreen and Wyplosz (2016) under the condition that the minimal requirements will be fulfilled. These cover the decentralized fiscal policy, centralization of financial supervision, and monetary policy and debt restructuring. Furthermore, the results of a number of statistical and fundamental analyses (e.g., those performed by Baum, Checherita-Westphal, & Rother, 2013, and Égert, 2015), confirm that to mitigate the effects of the unsuitable single currency in the long term, it is necessary to keep the public debt and taxes within reasonable limits; these limits should vary for different economies.

Conclusive Summary

The optimum currency area theory provides an analytical framework for the functioning of a monetary union. One premise of a successful monetary integration is linked to the characteristics of the geographic area that has a high degree of mobility of factors inside and immobility of factors outside, besides which, a similar economic structure and fiscal integration are required. The purpose of this article was to retrospectively identify euro-economies that met the assumption of similarity in the economic cycle for the period 2002-2016 with the German economic cycle, which is conceived as hegemonic euro-economy.

For this purpose, the economies were analyzed wherein the euro was the denominated currency before and inclusive of 2002 (Germany, Belgium, Austria, France, Luxembourg, the Netherlands, Finland, Ireland, Greece, Spain, Italy, and Portugal) from the perspective of the degree of synchronization with the cyclical position of Germany. The cyclical position, expressed as an average of absolute values of differences of the output gaps of euro-countries and Germany, reflects the economic cycle in which each member country is found on average in relation to Germany. The greater the difference in yearly gaps of the product, the more severe the occurrence of dissimilarity in the economic cycle (the strongest dissimilarities were manifested in Greece, Ireland, Spain, and Portugal). This procedure was supplemented by correlation and comparative analysis together with the assessment of empirical findings, which led to the conclusion that the western European countries can be perceived as a single region in terms of a similar economic structure (Austria, Belgium, France, Luxembourg, the Netherlands, and Finland) and as such can form an effectively functioning monetary union. The assessment of the development in Eurozone for future decade was made taking into account the current political and economic circumstances and the outputs of empirical analyses.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.