Abstract

Contemporary societies are bound in a fiscal social contract between citizens and their elected governments who administer the states in the interest of all members. The fiscal social contract implies that citizens should pay tax which is utilized by government to execute programs for the collective good. While the advanced countries have done a better job of mobilizing tax as a resource for societal development, developing countries have performed poorly. A large number of high-income earners in developing countries avoid the tax system thus hampering development efforts. Previous studies have alluded to a culture of tax evasion among citizens of developing countries as a key factor influencing noncompliance. However, this study argues that these studies did not reach the best conclusion as their methodology excluded the taxpayers’ narratives. We interviewed self-employed taxpayers in Nigeria’s capital city, Abuja. Results of the analysis revealed taxpayers’ frustration with an opaque tax system, deplorable socioeconomic condition, and nonfunctioning of the tax audit system. We argue that the massive tax noncompliance in developing countries may be better understood as “tax boycott” arising from taxpayers’ frustration with the fiscal social contract of governance. Policy implications of the findings were discussed in the concluding section.

Keywords

Introduction

Government–citizen relationship has evolved since the beginning of civilization. According to Locke (1689), prior to civilization, the human race lived in disorderly societies where might was right and survival was for the fittest. People’s response to this chaos, which Locke termed “state of nature,” was to organize societies under governments who administer the affairs of people living within their jurisdictions. The social contract is the implied legal relationship between citizens and those elected to govern in the overall interest of the community. The fiscal social contract is an offshoot of the social contract and it is beginning to generate scholarly interest. The fiscal social contract implies that members of the society pay tax in return for sharing in the benefit of governance. A former United States’s Supreme Court Justice, Oliver Wendell Holmes, was quoted to have said, “taxes are what we pay for a civilized society.” Contemporary scholars have established a link between states’ ability to generate tax and their levels of development (Besley & Persson, 2014; Burgess & Stern, 1993; Ivanyna & Haldenwang, 2013).

The fiscal social contract between citizens and governments is recognized even in ancient civilization. For instance, Sihag (2009, p. 56) quoted Kautilya, an ancient Indian philosopher and a contemporary of Aristotle, who stated as follows:

When there was no order in the society and only the law of the jungle prevailed, People (were unhappy and desirous of order) made Manu, the son of Vivasvat, their king and they assigned to the king one-sixth part of the grains grown by them, one-tenth of other commodities and money. The king then uses these to safeguard the welfare of his subjects. Those who do not pay fines and taxes take on themselves the sins of the kings, while kings who do not look after the welfare of the people, take on themselves the sins of their subjects.

The above quotation aptly describes the fiscal social contract even in ancient civilization. While the advanced countries have performed fairly well in tax revenue generation, developing countries are not able to do so. The dichotomy in tax revenue generation between advanced and developing countries has been a long-standing one. It was brought to scholarly attention as far back as 1963 by Nicholas Kaldor. He stated that advanced countries were generating about 25% to 35% of their gross domestic products (GDPs) as tax revenue while developing countries were generating 8% to 15%. Kaldor (1963) contended that developing countries will remain trapped in underdevelopment unless they are able to mobilize 15% and above of their GDPs as tax revenue. Over 50 years after Kaldor’s seminal exposition, the problem largely remains and contemporary scholars have continued to draw attention to it (Besley & Persson, 2014; Burgess & Stern, 1993; Ivanyna & Haldenwang, 2013). Though high level of poverty exists in developing countries, there also exist a large number of middle- and upper-class citizens (Kaldor, 1963). One of the duties of government is to generate tax revenue from the high-income segment of the population for transfer to the poor thus ensuring redistribution (Anderson, 2012). Poverty and wealth also coexist in advanced countries but a sense of community ensures that the poor are, at least, provided with basic needs.

In developing countries, inability of governments to generate adequate tax revenue has been linked to noncompliance especially by the wealthy segments of the society (Kangave, Nakato, Waiswa, & Zzimbe, 2016; McCluskey, 2016). Previous studies have investigated the phenomenon of tax noncompliance in developing countries (Besley & Persson, 2014; Burgess & Stern, 1993).). Despite these numerous efforts, tax noncompliance in developing countries remains a misunderstood phenomenon. Leading researchers have attributed part of the blame to a culture of noncompliance among citizens in developing countries (Bahl & Bird, 2008; Besley & Persson, 2014; Burgess & Stern, 1993). Bahl and Bird (2008) referred to extreme instances where tax evasion in developing countries is seen as a badge of honor rather than a crime. For Burgess and Stern (1993), “taxation is a strange, unwelcome and sometimes incomprehensible concept to many people in developing countries” (p. 799).

Despite good insights from the above studies, we disagree with the authors for reaching conclusions about taxpayers in developing countries without hearing their own sides of the story. We argue that the methods employed by these studies leave a huge gap in the effort to understand the phenomenon of tax noncompliance in developing countries. These studies were mostly quantitative analyses and theoretical discourse. In all these studies, the voices of the taxpayers are rarely heard. Even quantitative survey, which is a common tax compliance research method, is limited as well because it only permits taxpayers to tick predetermined options such as “agree,” or “disagree”. Details of why and how they agree or disagree are not known. As Bird (2015) noted, the most important players in the tax game are the taxpayers. Hence, studies that seek to deeply understand tax compliance issues must engage taxpayers in discussion.

Tax researchers in advanced countries have advocated for the qualitative method in understanding tax compliance issues (e.g., Oats, 2012), and many studies have been conducted in advanced countries using this method (Ashby & Webley, 2008; Björklund Larsen, 2013; Boll, 2014; Morse, Karlinsky, & Bankman, 2009; Onu & Oats, 2016; Rawlings, 2003; Rawlings & Braithwaite, 2003). Perhaps, due to numerous qualitative insights on tax compliance behavior in advanced countries, understanding of the subject appears deeper than what is known in developing countries. Researchers in advanced countries are becoming more innovative in the use of qualitative methods to understand the complexities of tax compliance behavior. For instance, Onu and Oats (2016) explored online discussions among taxpayers to come up with a highly informative insight on their mind frames. Studies that utilize this method are rare in developing countries thus limiting understanding of tax compliance issues in these countries. Using the qualitative method, this study brings new insight on tax noncompliance in developing countries. From the analysis of intensive interviews with taxpayers, this study argues that the phenomenon of tax noncompliance in developing countries could be better understood as “tax boycott”—a deliberate abandonment of tax obligations due to dissatisfaction with governance.

The objective of this study is to gain a deeper understanding of the problem through engaging the taxpayers in intensive interviews. This study is significant for the fact that a deeper understanding of the problem could inform more effective policies. Improving tax compliance in developing countries is important to international stakeholders. The failure of taxation as a communal obligation in developing countries has constituted a problem for advanced countries because they are under pressure to provide financial aids from their own communal resources. Tackling the issue of tax noncompliance in developing countries will thus be in the interest of advanced countries since they will be relieved of financial commitments in the form of development assistance if developing countries can generate their own tax revenues.

Research Design and Method

The Research Design

Due to the objective of the study which emphasizes gaining in-depth understanding of tax noncompliance and the motivations behind it among taxpayers in developing countries, we adopted the qualitative design and utilized the grounded theory approach based on insights from Creswell (2013). Creswell advises that the qualitative approach is a better option when we need a complex, detailed understanding of a problem and this can be accomplished by talking to those involved directly. Another reason that makes the qualitative design the better option in this study is the need to “empower individuals to share their stories” (Creswell, 2013, p. 48). As we stated earlier, taxpayers in developing countries are often accused of evasion by government functionaries and researchers. However, studies hardly give them the chance to narrate their own sides of the story. By utilizing the qualitative design, we attempt to fill this gap. The grounded theory approach, according to Charmaz (2006), allows theories to emerge grounded in the data. This is in line with our objective which seeks to understand tax noncompliance issues based on the perspectives of the taxpayers. We utilized intensive interviewing which, according to Charmaz, (2006), allows participants to do most of the talking.

In addition, qualitative design was adopted for this study because of the limitations of alternative methods such as quantitative surveys (e.g., Kirchler, Hoelzl, Leder, & Manneti, 2008), experimental methods (e.g., Alm et al., 1992, 1995), and studies based on secondary data (e.g., Slemrod, Blumenthal, & Christian, 2001). Quantitative surveys are limited in the sense that they present predetermined choice of responses to the participants. For instance, in a quantitative survey, a participant could indicate dissatisfaction with public services by ticking “dissatisfied,” “agree” or “disagree” depending on the available options and framing of the question. However, beyond ticking these options, quantitative surveys cannot unravel deeply held feelings behind them. For instance, why and how exactly is the respondent dissatisfied may not be known and the respondent’s input in tackling the problem may not be known from mere ticking of “dissatisfied.” Proponents of experimental design, for instance, James Alm, argues that it gives reliable information (Alm, 2012). However, Devos (2007) argued that the actions of student samples usually utilized for experimental studies may not be applicable in real-life tax compliance settings. Though the qualitative design has its own limitations in terms of coverage and smaller sample size, the depth of information it can provide could be very useful in dealing with a complex problem such as tax noncompliance in developing countries, hence it was chosen for this study.

Research context, population, and participants

Due to the constraint of qualitative research design in terms of coverage, this study was limited to self-employed business owners in Nigeria’s capital city, Abuja. The choice of Nigeria is informed by the fact that the country presents a good case for studying tax revenue generation problems in developing countries. The country is one of the most populated (185 million; United Nations Economic Commission for Africa [UNECA], 2015) among developing countries. Based on this population, the country represents close to a quarter of sub-Saharan Africa’s population of 800 million (International Monetary Fund [IMF], 2015). The country also presents a striking paradox of a developing country with one of the fastest growing economies in the world up to 2014 (Organisation for Economic Co-operation and Development [OECD], 2014). In 2014, the country’s GDP of $568.5 billion made it the 22nd largest economy in the world, yet, it has one of the lowest tax to GDP ratios globally (Cobham, 2014). This presents a striking paradox of low tax collection in the midst of wealth. The self-employed taxpayers were the focus of this study because, of all taxpayer segments, they pose the greatest challenge (Joshi, Prichard, & Heady, 2014; Kirchler, 2007). The participants were 32 self-employed business owners in Nigeria’s capital city of Abuja between the ages of 33 to 62 years. They operate businesses as diverse as transportation, auto dealership, general merchandise, hotel ownership, and professional service providers (doctors, lawyers, engineers). The selected participants have annual income in the range of N5,000,000.00 (US$16,556.00) to N20,000,000.00 (US$66,225.00) at the current exchange rate.

Procedure

Semistructured interviews were used to elicit responses from the participants following the procedure of Ashby and Webley (2008). Semistructured in the sense that a standard question was put across to all participants thus: Government has complained of tax noncompliance among business owners. We would like to know your experience about the tax system generally and reasons, in your opinion, people do not pay tax.

However, the entire interviews could be described as open-ended because, apart from the single standard question, responses were not structured and follow-up questions depended on the responses from participants. In most cases, the interviewers sought clarifications on some responses and in some cases, responses led to follow-up questions. To elicit frank responses, the interviews were conducted in an informal atmosphere, in a conversational tone. The interviewers were instructed to avoid questions that could be directly vindictive in order not to jeopardize the truthfulness of responses. Interviewers were also instructed to avoid being judgmental, to be good listeners and to inquire when they needed clarifications. This is because tax compliance is a sensitive topic and taxpayers may not be willing to cooperate unless their confidence is gained (Kaplan, Newberry, & Reckers, 1997).

Recruitment

Participants were randomly recruited within the capital city of Nigeria—Abuja. The process began with 100 introductory letters, consent forms and brief demographic questionnaire distributed to business owners across the city. The letters introduced the researchers and explained the rationale of the research. Participants were assured that the research is an academic exercise with the objective of contributing to improving the tax system and not a government-initiated investigation. They were also informed that participation was entirely at their discretion and they could opt out at any stage of the exercise. Hence, consent forms were attached to the introductory letters for participants to communicate their consent or otherwise. The introductory letters also clearly stated that views and opinion of participants would be treated anonymously. A demographic questionnaire was attached to each letter and the essence was to screen out those that did not meet the criteria for the interview. Participants were also requested to choose their preferred dates for the interviews within a period of 3 weeks and also their preferred venues. This served as a guide in scheduling the interview appointments. A total of 38 processed forms, out of the 100 sent, were retrieved translating to 38% response rate.

The interviews

The interviews took place over 17 days according to dates chosen by participants though there were slight adjustments in some cases. Most of the participants chose their offices as preferred venues. The interview crew consisted of two interviewers. A tape recorder was used but a note-taker also wrote proceedings directly on paper as the participants spoke. This was to safeguard against possible loss of data from the tape recorder. The lead researcher was also part of the team as the leader and director of proceedings. He also took notes and asked questions as the need arose. Interview times ranged from 40 min to 2 hr depending on the participant’s willingness to engage in wider conversations. At times, conversations veered into non-tax issues to keep participants engaged, enliven the discussion, and gain their confidence. Though 38 interviews were scheduled, only 32 participants were interviewed because saturation point was reached at about the 30th interview. Saturation point, according to Creswell (2013), is the point at which adequate information has been gathered and interviews are no longer yielding additional information. Table 1 presents demographic information on the 32 participants interviewed for the study.

Particulars of Participants.

Source. Field data.

Qualitative data analysis

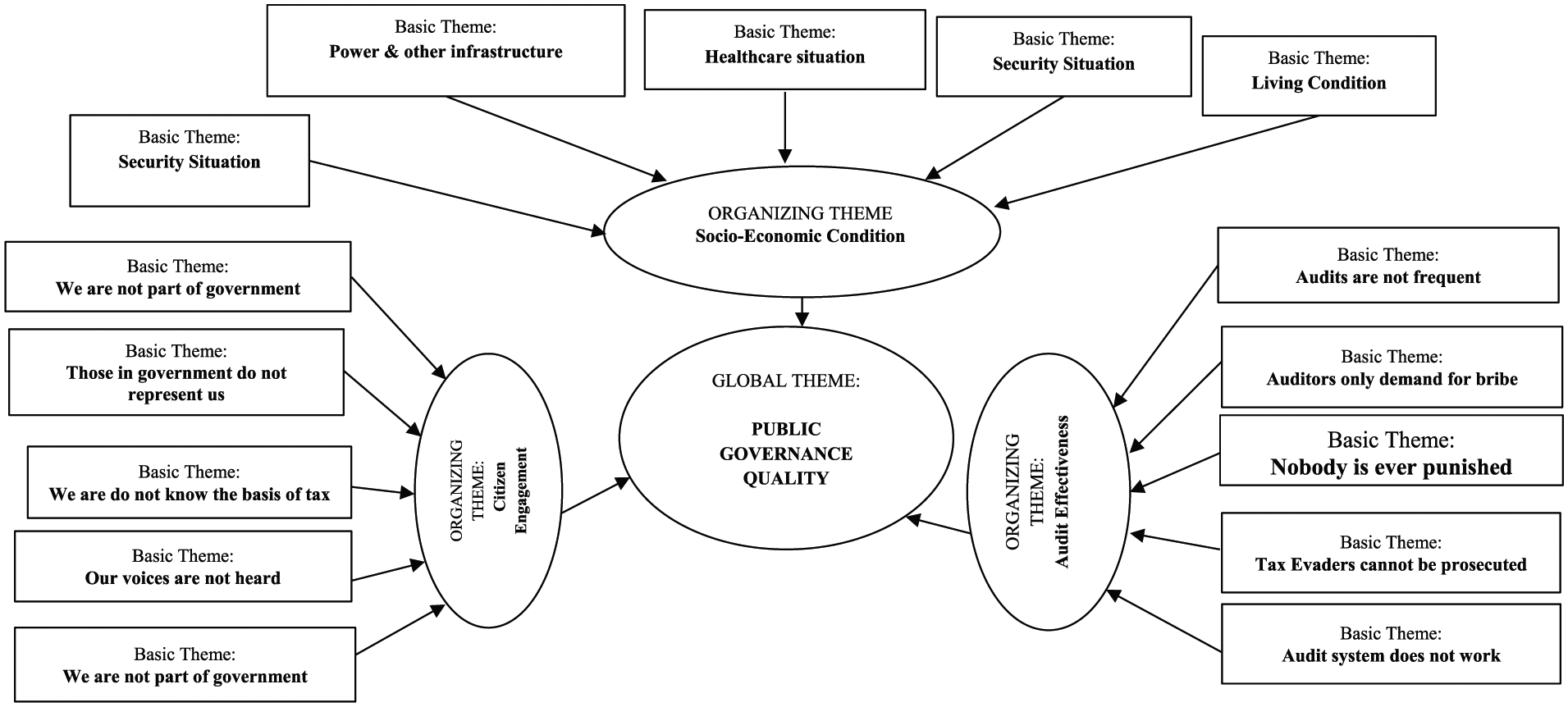

We ensured validity and reliability of the data by member-checking on participants’ statements. However, unlike the norm where researchers go back to participants, after transcribing, to confirm the accuracy of the transcribed statements, we were confirming participant’s statements on the spot. This was due to extensive nature of the interviews, difficulty of obtaining repeat appointments, and the logistical problems another round of visits would entail. The interview tapes were transcribed and checked against manual notes for likely discrepancies. The transcripts were then analyzed using thematic networks in line with Attride-Stirling (2001). The first step was a thorough line-by-line reading of the transcripts to identify basic themes; these basic themes were then arranged into organizing themes which then coalesced into a global theme.

Results

Our analysis produced numerous basic themes which cluster around three organizing themes—citizen engagement, socioeconomic condition, and audit effectiveness. These three organizing themes also coalesced into a global theme of governance quality. Summary of findings under each organizing theme are presented as follows.

Citizen Engagement

Responses from many participants indicated their disengagement from the tax system and affairs of governance generally. For instance, “I do not know the basis of these monies they are collecting” (Participant 3). When probed further on the choice of the word “they” as he used in referring to those in government, he stated that “they” is justified because those in government are there for their own selfish interest hence do not “carry citizens along” in affairs of governance. In his words (Participant 3), “we are not part of them.” Participant 10 decried the lack of information on how government affairs are conducted and accused those in government of running an exclusive “cult.”

They are like cult, when you find yourself in government, you take your share but when you are an ordinary citizen like me, you are on your own—how do you pay tax to people who are so rich from government money?

Participant 30, a 37-year-old female bakery owner, asked why government needed tax monies in the first instance. “They are government and they have the central bank, can’t they print all the money they want? They are only disturbing us.” She was asked why she kept referring to those in government as “they,” and whether she is not aware that those in government are there to represent her. The word “represent” appears funny to her as she chuckled. “Represent me! How do they represent me? They only represent their pockets and those of their families and friends.” She was reminded that government organizes town hall meetings periodically and whether she never attended any. “Meeting?” she asked in unbelief. “I was never invited for any meeting.” She contended that even if they organized such meetings, it would only be for formality, to fulfill all righteousness, as the citizens have no say. To worsen matters, she said town hall meetings, if they are ever organized, could just be another conduit pipe for siphoning funds from the treasury as public officers in charge of organizing such events would submit invoices 100 times the real cost.

Participant 17 made similar statements as Participant 30. When asked whether he, or in conjunction with other citizens, have tried to discuss their grievances with those in government, the participant expressed shock at the “naivety” of the interview crew. He remarked,

Where will you see them (government officials)? Those people are in a different world. You can only see them during election campaigns, after that, they disappeared and you only see them on television when they want to tell lies. Ordinary citizens do not have access to them as they are guarded by tens of policemen and protocol officers.

Nineteen other participants made statements similar to those of Participants 3, 10, 17, and 30. We coded statements such as, “they are in government,” “we are on our own,” “I do not know the basis of these monies they are collecting,” “we are not part of them,” “we are not carried along,” “we do not have any say,” and others, as basic themes indicating non-engagement of citizens in the process of governance and taxation and it falls under the organizing theme of citizen engagement.

Socioeconomic Condition

Numerous responses from participants indicated their dissatisfaction with socioeconomic condition of living and doing business generally. In the words of a visibly angry Participant 18,

What do you mean by tax? I am sponsoring two children’s education abroad because of incessant strikes in our universities, there is no public water in my house so I operate a personal bore hole, I power my business with a private generating set. Do you know how much I spend on all these? What tax do you want me to pay?

Participant 23 was calm but bitterness could be discerned in his voice as he explained why he believed the tax system would not work:

My brother’s wife just returned from India for treatment of kidney ailment. Two people accompanied her on the trip and that translates to air tickets for three. Add that to the cost of treatment and feeding for three in a foreign land—what is wrong with our health system? My brothers (referring to the interview crew), is it not better for government to fix our health care so we can get treated locally? We can then save money to pay tax. Believe me, as it stands currently, tax cannot work in this country.

Participant 5 lamented the avoidable difficulties faced by citizens in their day-to-day living and wondered why any government would expect citizens living under such conditions to pay tax. The interview crew reminded him of his income status which is N10,000,000.00 to N15,000,000.00 (US$32,680.00-US$49,019.00), according to the demographic information available to us (refer to Table 1), and asked why he complained of difficulty in living with such a huge income. “You will not understand,” he challenged the interview crew. “Those of us with some visible incomes are the most affected by the economic condition.” He explained that the extended family system in the country poses a big problem to middle-class citizens. They have to cater to the needs of immediate and extended family members in the absence of any lifeline from government. He admitted that business owners in his position do not like paying taxes because “government has not sowed the seeds needed to reap taxes.”

Participant 1, who operates a fleet of transport vehicles, narrated a lengthy tale of the obstacles he battles with in running his business.

Due to bad condition of our roads, my vehicles become unserviceable within five years. A truck requires a major service after just 1,000 kilometers journey. Fuel scarcity is a major bane of the business and this result from policy failures. Serious accidents occur frequently due to bad roads and in some cases, vehicles are written off.

Participant 20, who is in the same line of business, stated that in some portions of the highways, it could take haulage trucks an hour to navigate potholes in a stretch of only 20 kilometers and this also goes with higher fuel consumption. Serious wear and tear depreciate vehicles within a short period. According to the participant, while he struggles to keep his business afloat, the last thing on his mind is tax. When asked how he expects government to fix the roads if he does not pay tax, he responded,

The government had so much money from oil, if they did not fix infrastructure with that, I am not sure they will fix it with tax money. But I am ready to pay tax if I am sure they are serious.

Participant 27, who own a restaurant chain with daily stream of customers, lamented the obstacles she tackles in running her business:

I run two power generating sets in each business location because there is virtually no public power supply. One power generator operates for 8 hours, it is switched off and allowed to cool off while the second set takes over. Most of the profit goes into providing power. My children are all in private schools and this takes millions of naira annually, I do not have money to pay as tax—even if I have, why should I pay?

Participant 29, an estate developer, narrated the difficulty he encounters in doing his business:

There is housing crises in the country which provides opportunity for estate developers but it is not easy in this business. There is no supporting infrastructure for the business hence an estate developer needs to provide all the facilities—water, power, roads, and even basic things as waste disposal services. When the cost of these privately provided facilities are transferred to the buyers, the cost becomes prohibitive so we do not get good patronage.

He added that due to inadequate public security, no estate is complete without private security provided at a huge cost. He wondered what would be left to pay tax after all these troubles.

Participant 11 is a 60-year-old lawyer who runs a law firm. Perhaps because of his legal background, he was very choosy with words. He lectured the crew on the law of contract. He stated that in a contract, there must be offer and acceptance, and it could be frustrated by a breach from either party. When asked to explain how this relates to the issue of paying tax to government, he stated that signs of breached fiscal social contract by government are everywhere. When told that the non-taxpaying citizens are themselves culpable for breaching the contract, he responded by saying “anybody can opt out of a failed contract,” suggesting that the business owners opted out of the tax contract because of government’s failure to fulfill its own part. The interview crew suggested that government deserves some tax, at least for providing national security through the army and police force. He found this statement funny as he laughed loudly. “National security? Which security when 30,000 citizens have been massacred in the past four years by insurgents, many of them while sleeping innocently in their bedrooms.” The interview crew asked whether the citizens can resort to the instrument of the law to enforce their fundamental human rights as enshrined in the constitution. He stated that there are copious provisions in the constitution to protect ordinary citizens but the law and the judiciary have been hijacked by the ruling elites to serve their selfish interest. “As it is currently, the law doesn’t protect the ordinary people.” Most of the participants throughout the interviews spoke of harsh conditions in terms of health care, security, education, and others. We identified those basic themes and analyzed them under the organizing theme of socioeconomic condition.

Audit Effectiveness

Many of the participants who have some sympathy for the tax system alluded to a nonfunctional audit system as a discouraging factor even when they intended to pay tax. For instance, Participant 2 stated that “even if you want to pay, you would be discouraged. Have you ever heard of anybody punished for not paying tax?” The interview team leader intervened by mentioning some current cases of the revenue authorities sealing off businesses that breached the tax laws. “These are mere jamborees,” he remarked. “Please mention names of people you know were convicted of tax crimes in this country,” he further challenged the interview crew. There was a momentary silence as if everyone was busy thinking up some names of convicted tax evaders, but no one could come up with any name. The team leader broke the silence and directed that proceedings should continue.

Participant 24, a poultry farmer, introduced a comic dimension to the discussion: “I do not receive any audit visit in my office except towards year end festivities and when the auditors come, they request for chickens for Christmas and New Year celebrations.” Participant 13 did not blame the auditors for negotiating bribes during audit visits because it is the general trend in the society: “How do you expect tax auditors to be different with the level of decadence in the society,” he asked. Participant 21 saw beyond the nonfunctioning audit system and traced the problem to government elites who misappropriate public revenue. “The auditors are aware the funds will be diverted to private use so they tend to help themselves. Tax audits can only work when the entire government machinery is transparent and will never work in isolation.”

Participant 25 admitted knowing people arrested for tax offenses but the police did not cooperate with the revenue agency. Police officers are always lamenting their ill luck in not having access to public treasury like some other agencies and when tax offenders are brought to them, “the cooperate with the offenders to fill up their own pockets.” Participant 25 stated that the courts are even worse than the police and tax evaders “jump for joy” when they are threatened with court action. When asked to explain why criminals would be joyous in the face of prosecution, he grinned. “A simple case of tax evasion could last for years without actually commencing and when it commences, it may never be concluded. The money spent by the government in prosecuting the evader may triple the evaded amount.” He said the judiciary prosecutes such cases nonchalantly as judicial officers are aware that those in authorities are the bigger evaders. Themes from this subsection points to a dysfunctional audit system, from the likelihood of audit, detection probability, and sanctions. We analyzed these basic themes under the organizing theme of audit effectiveness. Figure 1 depicts the thematic networks analysis of the entire interview data.

Thematic network analysis of data.

General Discussion

Analysis of data from the participants (see Figure 1) revealed three key organizing themes which taxpayers mentioned as reasons they are not being satisfied with the tax system: disengagement from governance and by extension, the tax system (citizens engagement); difficult living condition (socioeconomic condition); and dysfunctional audit system (audit effectiveness). These findings are not entirely new in tax compliance research as similar findings have come up repeatedly in about 50 years of tax compliance research. However, our objective in this study is to gain an in-depth understanding of taxpayers’ behavior in developing countries, and our findings appear to be deeper than what previous studies found.

On citizen engagement, a recent Afrobarometer survey (Aiko & Logan, 2014) found that taxpayers in Africa are willing to pay tax but expressed their frustration about the opacity of the system. Kirchler et al. (2008) found that engaging taxpayers with information on tax and its benefits and the manner such information is framed leads to enhanced compliance. Findings of this study show that the issues are deeper than mere information campaigns. Taxpayers want to be generally engaged in the political process, especially fiscal matters. Currently, they feel alienated and do not feel a sense of belonging in the entire governance process. They perceive the entire political process to be hijacked by the governing elites and as such, they operate independently of the system. Worse still, they perceive the ruling class as adversaries in the race for survival. Disengagement from the political system also goes along with dodging tax. In the field of public administration and political science, researchers (Bowler, Donovan, & Karp, 2007; Holmes, 2011; Krawczyk & Sweet-Cushman, 2017) have found the imperative of citizen engagement in eliciting support for government programs. Moreover, Prichard (2010) emphasized the imperative of citizen engagement for tax reforms to succeed in developing countries. The findings of this study reveal an extremely high level of citizen disengagement from the system.

The difficult socioeconomic condition of living is also a key organizing theme found in this study. Participants narrated their struggles with a harsh socioeconomic system that does not support citizens in their efforts to survive, hence they justified evasion. Numerous previous studies have made similar findings but in different ways. For instance, Alm, Jackson, and McKee (1992) found that supply of public goods positively influences tax compliance. Doerrenberg (2014) found tax compliance to be influenced by tax revenue usage and Kirchler (2007) also affirmed the relationship between availability of public goods and tax compliance. An Afrobarometer study (Asunka, 2013) found that Africa’s citizens rate their governments poorly on the supply of basic amenities like water and electricity which is similar to our findings. However, previous studies did not provide avenues for taxpayers to explain how the lack of or dysfunctional public facilities affect their ability and willingness to pay tax. The narratives in this study have revealed the depth of the problem beyond what we know from previous studies.

Audit effectiveness is the third organizing theme revealed by our data analysis. Findings on the role of audit in tax compliance are as old as tax compliance research. It was the key issue when Allingham and Sandmo (1972) pioneered empirical tax compliance research. Many studies after Allingham and Sandmo found audit to be a determinant of compliance behavior. Kirchler (2007) drew attention to a possible backlash if audits are not effective. If audits do not apprehend and prosecute offenders, then even taxpayers who wish to comply may feel cheated and resort to evasion. With time, evasion will permeate the entire system. Statements from participants in this study confirm Kirchler’s (2007) position. The tax gap in developing countries is huge and a breakdown of the audit system as found in this study could be a key factor. This study also revealed that taxpayers do not take cognizance of audit probability alone as indicated by many studies but they assess the entire system, from audit probability to detection probability and even the effectiveness of prosecution, in deciding whether to comply or not.

More importantly, previous studies treat the determinants of tax compliance as independent variables. Tax awareness, public goods supply, fairness perceptions and audit probability were all treated as independent variables which influence tax compliance. While this is true, findings from this study revealed that taxpayers do not perceive these elements in isolation. They perceive them in relation to public governance quality generally. Hence our thematic networks analysis revealed public governance quality as the global theme that drives the themes of citizen engagement, socioeconomic condition, and audit effectiveness. The participants could be right because the more advanced countries, where these themes work better, do have a better governance quality. Richard Bird, who has a long-term and wide-ranging working experience on tax administration in developing countries, stated this much:

What any country does with its tax system is inevitably determined, in the first instance, by political and not economic calculations. Some countries are close to failed states in which institutions are so ineffective that whatever they attempt to do does not work. (Bird, 2008, p. 21)

Insights from our data are in line with this expert opinion of Bird. The difficult socioeconomic condition, citizen disengagement, and dysfunctional audit system are all symptoms of a larger problem of government failure.

Most importantly, findings from our study revealed an overwhelming “boycott” of the tax system. Middle-class citizens, who earn some measure of income, pay income taxes in advanced countries but the reverse appears to be the case in developing countries. There is pervasive unwillingness to comply with tax provisions. Noncompliance is so widespread that the usual “evasion” and “noncompliance” terminologies may not be adequate in explaining it. We suggest that what is currently obtainable in developing countries is a “tax boycott.” We propose a preliminary definition of tax boycott as a situation where noncompliance is so pervasive that more than 50% of eligible taxpayers do not comply due to dissatisfaction with governance. Our data revealed that more than 80% of our participants do not want to have anything to do with the tax system. Moreover, similar data are found across developing countries (Kangave et al., 2016; McCluskey, 2016). Based on revelations from our participants and similar data from other studies (Kangave et al., 2016; McCluskey, 2016), which found that more than 50% of taxpayers across several developing countries avoid their tax obligations, our position that the tax noncompliance in developing countries could be better understood as a tax boycott also represents a significant finding of this study.

Limitations and Implications of the Study for Further Research

We conducted this study fully aware of the peculiar limitations of a qualitative study—inadequate and non-representative sample size, possible bias, and less rigor in data analysis. However, we tried to minimize these pitfalls in all the steps and at every stage of the study. In our sampling, we made effort to contact about 100 participants knowing that there would be a high rate of refusals. Out of the 38 participants who indicated their willingness to participate, we picked 32. This number is acceptable as adequate sample size even in quantitative studies where larger sample sizes are required (Sekaran & Bourgie, 2013). Hence, for a qualitative study, the sample size is a large one. To ensure that our participants were representative of self-employed business owners, we picked them randomly from different business groups, gender, and different levels of income. During the interview process, the interviewers were not allowed to introduce their personal opinion. Rather, at intervals, we reminded participants about government’s position on certain issues to ensure balanced discussion. Data analysis was carried out based on a prepared template—thematic networks (Attride-Stirling, 2001). This ensured that the analysis followed a standard format and minimized possible interference with the data. Despite all efforts to ensure a valid study, we observe that our attempt to explain tax compliance challenges in developing countries with the sample from Nigeria may require further research due to the diverse nature of these countries. However, we are confident that the conditions alluded to by participants in this study also exist in many other countries, hence the tax compliance issues are bound to be similar. However, where doubts exist, there may be need to replicate the study in other countries to confirm or modify our findings; hence, we provided a lucid explanation of our methodology.

Conclusion

Previous studies lacked in-depth understanding of the motivations behind the pervasive noncompliance in developing countries. We sought to understand these motivations through intensive interviews with self-employed business owners and our findings point to the existence of an extensive tax boycott by eligible taxpayers who justify their position by citing the harsh socioeconomic living condition, disengagement from governance, and a dysfunctional audit system. These findings have significant policy implications and call for the re-examination of the fiscal social contract of taxation between governments of developing countries and their taxpayers. First, citizen non-engagement in tax matters points to a breach of the fiscal social contract. It is implied in the fiscal contract that citizens should be involved and carried along in an open two-way communication (no taxation without representation). Second, while it is not expected that governments in developing countries should provide public goods at the same level as the advanced countries, at least taxpayers expect value for money. The advanced countries did not get to their current status at once but made steady progress in a virtuous cycle of taxation and public goods supply with the involvement of citizens. This is what is essentially missing in developing countries. Commensurate with the resources available to developing countries, infrastructure is grossly inadequate leading to loss of confidence in governance. This is contrary to the spirit of the fiscal social contract. Third, weak rule of law ensures that some people can break the law with impunity. For instance, some participants in this study stated that nobody that they are aware of has ever been convicted of tax evasion. This is contrary to the fiscal social contract which is supposed to bind all members of the society on equal terms. When the law, especially tax law, is weak, as Kirchler (2007) noted, the ranks of compliant taxpayers get gradually depleted until an overwhelming majority boycott the tax system. This is the problem with taxation in developing countries.

Currently, the popular policy framework for solving tax revenue problems in developing countries is tax reform largely supported by the World Bank and IMF. But as Bahl and Bird (2008) noted, about 30 years of these tax reforms have left so much gaps uncovered. Perhaps, the inadequacy of these reforms stems from the fact that they focused too much on tax administration tools (computers, IT, human resources, salaries, tax administration autonomy) and focus less on the people who will eventually pay the taxes (Di John, 2006). While tax administration reforms in developing countries have done a lot of good, it may not accomplish the goal of significantly improving taxes in these countries unless the taxpayers themselves are fully integrated into the reforms and the fiscal social contract is upheld. The findings of this study reveal a deep-rooted disenchantment with government and the tax system, so much that tax administration reforms may not be able to make much impact. The policy implication requires that a three-pronged strategy be adopted to pacify taxpayers—embark on intensive citizen engagement with governance, noticeably improve their socioeconomic condition, and make tax audit effective as a deterrent to evasion. While these solutions may not be practicable simultaneously, perhaps, due to funding and political constraints, there are easy solutions that could be exploited. For instance, intensive citizen engagement and setting public goods targets with the involvement of the taxpayers could be some good starting points.

There are roles for the World Bank, IMF, and donor countries who keep granting aids to developing countries while advocating for tax reforms. They could concentrate more on influencing improvement in public governance first before aid and tax reforms because, in the absence of improved governance, aid monies and tax reforms often fail as noted by Richard Bird (2015). Tax administration reforms should be preceded by or take place simultaneously with “taxpayer reforms”; otherwise, “tax boycott” may persist in developing countries.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.