Abstract

This article appraises a new empirical perspective about organizations, which disputes the mainstream economic view expressed in standard economic and financial economic textbooks. The mainstream view claims that organizations exist to increase their owners/shareholders value (wealth), and organizations’ operating activities could be dissociated from financial and investing activities (separability assumption). To the intangible flow theory, (a) the major aim of organizations is to deliver flows of operating products to members of society. These operating product flows are vital for human survival and existence. Thus, (b) operating, investing, and financing decisions are not randomly associated. I have studied 21,108 firms listed in the stock exchanges of 10 countries (i.e., Australia, Canada, China, Germany, Japan, Malaysia, Singapore, South Korea, the United Kingdom, and the United States) at the beginning of the 21st century (2000-2011). These are stock exchanges with many listed firms, ranging from 679 firms in Singapore to 4,440 firms in Japan. Organizations’ operating, investing, and financial decisions seem to be actually connected, as suggested by the intangible flow theory.

Introduction

This study compares two perspectives about organizations, namely, the mainstream economic view of firms argued by the standard economic and financial economic textbook, and the intangible flow theory perspective. According to the mainstream economic view, organizations exist to increase the wealth (value) of their owners/shareholders. In the context of the intangible flow theory (Cardao-Pito, 2004, 2010, 2012a, 2012b, 2016), the major purpose of organizations might be to deliver operating product flows to members of society. Intangible flow theory is not restricted to capitalist/market forms of organizations (Cardao-Pito, 2004, 2012a, 2012b, 2016). However, even capitalist-form organizations may aim delivering flows of operating product flows to their customers. For example, the major drive of a coffee shop may not be to make money payable to owners/shareholders per se as would be suggested by mainstream economics or financial economics (Berk & DeMarzo, 2014; Brealey & Myers, 2003; Damodaran, 2011; Geddes, 2011; Koller, Dobbs, & Huyett, 2011), but to deliver flows of coffees, teas, cakes, and other related products to customers that, as a consequence, will generate cash flows. Likewise, a textile manufacturer may aim to deliver flows of clothes and related products to members of society while managing productivity. According to the intangible flow theory, monetary inflows to organizations occur because organizations address their main purpose of delivering operating products to members of society (Cardao-Pito, 2004, 2010, 2012a, 2012b, 2016).

These two perspectives can be empirically evaluated. If the major organizational aim is to deliver product flows to members of society, then operating activities cannot be entirely dissociated from financial and investing activities, as is the case in the separability assumption found in standard economic or financial economic textbooks (e.g., Brealey & Myers, 2003; Damodaran, 2011; Mankiw, 2014; Marney & Tarbert, 2012; Ross, Westerfield, & Jaffe, 2004; Samuelson & Nordhaus, 2009). As further described in the next section, this assumption presupposes that operating, financing, and investing decisions should be independent. It is based on the framework developed by Franco Modigliani, Merton Miller, and Irving Fisher, which assumes that the right-hand side of the balance sheet (assets) is independent from the left-hand side (equity and liabilities), and vice versa (Fisher, 1906; Harris & Raviv, 1991; Miller, 1988; Modigliani & Miller, 1958, 1963; S. Myers, 2001).

In this article, I empirically assess the verifiability of the separability assumption. To this end, I have used a database to track 21,108 firms listed in stock exchanges with many listed firms. I have studied firms listed at the stock exchanges of 10 different countries (Australia, Canada, China, Germany, Japan, Malaysia, Singapore, South Korea, the United Kingdom, and the United States) at the beginning of the 21st century (2000-2011). These firms’ cash-turnover (revenue) size was found to be strongly empirically linked to the tangibility (i.e., physical-good component) of their operating product flows, which may be explained by inherent needs associated to the tangibility of operating product flows. In previous research, firms’ revenue size was found to be empirically associated with more debt in firms’ capital structures. Furthermore, it is reasonable to suggest that the production process requires specific investments related to concrete operating product flows. Therefore, these findings support the intangible flow theory perspective in view of the fact that organizations’ operating, investing, and financial decisions appear to be nonrandomly linked. Furthermore, these findings may refute the separability assumption, hence mainstream economic’s structural argument.

Mainstream Economic View of Firms

The classical economist Adam Smith (1776/1977) has modified the concept of capital. This fact has great bearings for economics and sociology. Although the previous concept of capital as money investable or invested in business is still used in business circles, in economics and sociology since long ago, capital generally implies elements involved in a production process that can be used to increase/benefit the wealth/position of investors/owners. For Smith (1776/1977), capital is no longer a sum of money that is to be invested, or which has been invested in certain things. The things themselves become defined as capital, for instance, machines, land, or persons (Cannan, 1921; Cardao-Pito, 2015, 2016, pp. 206-210; Hodgson, 2014; Innes, 1914; Schumpeter, 1954). This alteration to the word’s meaning has eliminated the direct association between capital and money. Thus, the word capital has been applied to describe both physical goods and human contributions to the productive process, which is quite troublesome as to understand both their distinctions and connections (Cardao-Pito, 2012a, 2016).

Nevertheless, Smith did not solve the problem of measuring his concept of capital, a problem that would later be addressed by Irving Fisher (Fisher, 1892, 1906, 1907, 1930; Miller, 1988; Parker, 1968; Stigler, 1950). Fisher has made a practical application of the discounted cash flow model. This model consists in an ad hoc method, to evaluate investment projects (Parker, 1968). It utilizes estimates of future cash flows, which are discounted by a rate that should account for risk and temporal value of money. Apart from limited situations, one can never be completely sure of what future cash flows will be or what discount rate should be used. These inputs are intangible because they cannot be assessed with precision at the moment of analysis (Cardao-Pito, 2012a, 2012b, 2016). Nevertheless, Fisher has attributed great consequence to the discounted cash flow model. To Fisher, capital value is equal to discounted projections of future income (Fisher, 1892, 1906, 1907, 1930; Miller, 1988; Parker, 1968; Stigler, 1950). Nowadays, mainstream economists still theorize capital and income in this manner (Tobin, 2005). In the process of defining capital–income value, Fisher has come up with a theory of the organization. It defines that the purpose of organizations is to increase their capital value, and therefore to increase cash flows payables to their shareholders/owners (Cardao-Pito, 2012a, 2012b, 2016).

Fisher’s view is the currently dominant view of firms in mainstream economics. Consequently, the dominant explanations of a firm’s capital structure assume that financial decisions can be taken as independent of operating and investing decisions. This separability assumption was reintroduced in Modigliani and Miller (1958), the opening paper to the contemporary field of financial economics (Harris & Raviv, 1991; S. Myers, 2001). This assumption’s origin is not merely a matter of interpretation of the current article. It is clearly stated and described by Miller (1988, pp. 114-115) himself, when celebrating 30 years of his influential piece with Modigliani. The assumption is as follows: “the firm’s financial decisions can be taken as independent of its real operating and investment decisions” (Miller, 1988, pp. 114-115). By following Fisher, Modigliani and Miller have offered a convenient solution for researchers who preferably use mathematical/quantitative forms of research. The intangible flow dynamics of economic phenomena was put inside a box that Modigliani and Miller use to represent the firm, and ignored there. The contents of that box would be considered irrelevant and/or negligible. Subsequent theoretical developments about the capital structure such as trade-off theory (Baxter, 1967; Miller, 1977; Modigliani & Miller, 1963), pecking order theory (S. Myers, 1984, 2001; S. Myers & Majluf, 1984; Yang, Chueh, & Lee, 2014), and market timing theory (Baker & Wurgler, 2002) were built presupposing the separability assumption.

During most of his career, Fisher was deemed one of the greatest economists in the United States. However, his reputation was deeply disturbed by the Great Crash of 1929 and ensuing economic contraction. He had written that such a crisis would be highly unlikely (Fisher, 1929, see also Fox, 2010). Yet, by 1932, stock prices in the United States had devaluated by 89%, thousands of banks would become bankrupt, and the economies of many countries were in great unrest (Fox, 2010; Michie, 2006). Fisher lost a large amount of his own invested money when the stock market collapsed. Furthermore, he faced the prospect of personal bankruptcy, from which he would barely have escaped if not for emergency loans from his sister-in-law (Allen, 1993). At some point, he had to sell his house to the University of Yale, which consented him to stay as a tenant. Later, he would be unable to pay the rent and need to move to a smaller house (Allen, 1993). As would be expected, in the aftermath of the great economic depression, the reception to his ideas has entered also into crisis (Allen, 1993; Dimand, 2007; Fox, 2010; Galbraith, 1977).

However, Fisher’s ideas would recover their past prominence. It is not the purpose of the current article to study the popularity of his ideas. Nonetheless, I can observe that decades later Fisher would be praised by many Nobel Prize in Economics laureates (e.g., Fama, 2014, p. 1471; Friedman, 1994, p. 37; Miller, 1988, p. 103; Samuelson cited in Mirowski, 1991, p. 223; Stigler, 1950). Likewise, many areas and concepts related to mainstream economics hold the view that organizations exist to increase the wealth of their owners, and that financial, investing, and operating decisions would be independent, for instance, the resource based view of the firm (Barney, 2001; Barney, Ketchen, & Wright, 2011; Kraaijenbrink, Spender, & Groen, 2010; Wernerfelt, 1984) or the human capital concept (Becker, 1962, 1964, 2008; Schultz, 1961). Similarly, Thaler (1997) has suggested that Irving Fisher could be considered a modern behavioral economist.

The Challenge From Intangible Flow Theory

A more detailed description of intangible flow theory’s framework appears in Cardao-Pito (2012b, 2016). This new theory suggests that flows of economic material elements (such as physical goods; and cash) are consummated by human-related intangible flows (such as work flows; service flows; information flows; and communicational flows) that cannot be precisely appraised at an actual or approximate value, and have properties precluding them from being classified as commodities, assets, capital, or resources. The new theory’s intangibility concept is not linked to the sense of touch, but to precision. The paradox of endeavoring to measure intangibility is that, by definition, intangibility cannot be precisely measured. At best, intangible dimensions can be transformed into measurable tangible elements when humans find quantitative methods to assign an actual or approximate value to them. The unmeasurable elements continue intangible. Therefore, although mathematical/quantitative research methodologies are very relevant for science, they are insufficient to study economy and society (Cardao-Pito, 2004, 2012a, 2012b).

This new theory suggests we must pay greater attention to flows of economic material elements that display a relevant degree of empirical precision (e.g., cash and physical goods flows), however, without ignoring the paradox of trying to measure intangibility, as occurs in nowadays’ mainstream economics. Mostly based upon quantitative research tools (Beed & Kane, 1991; Hoopwood, 2008; Leontief, 1982; Sutter, 2009), mainstream economics is thus not technologically prepared to address the intangibility of economic and societal production. Quantitative research tools must be linked to some form of measurement. However, intangible flows can be demonstrated but are not measureable with precision (Cardao-Pito, 2004, 2012a, 2012b, 2016). Moreover, the post-Smith concept of capital is highly problematic. It considers everything that may cause a cash flow as a form of capital and thus akin to a commodity, which results in interrelated conjectures such as human capital, human assets, and human resources (Cardao-Pito, 2004, 2012a, 2012b, 2016). Therefore, vital differences among economic elements remain under researched. The mainstream view is obsessed with cash flows. Nevertheless, it has not many explanations to offer in regard to how those cash flows may be actually generated.

The intangible flow theory rejects the post-Smith concept of capital and suggests a law for the social sciences asserting that we human beings are not commodities, assets, capital, or resources (Cardao-Pito, 2016). For example, a human-related intangible flow such as pure human service may have been necessary to generate a certain cash flow at economic production. However, according to intangible flow theory, neither the human or intangible contribution can be considered as commodities. Under the new theory’s framework, commodities are restricted to physical goods (Cardao-Pito, 2004, 2012a, 2012b, 2016). There are several reasons to restrict commodities to physical goods, and to distinguish several outputs of the production process from commodities. Rathmel (1966) and Shostack (1977) noted that there are very few products which are pure physical goods or pure services. Most products have tangible and intangible components. However, the degree of output intangibility can be classified according to a continuum. At one extreme are pure physical goods as for instance salt or fridges and at the other are products that are mostly intangible such as pure services (e.g., teaching, consulting). In the middle are products that are semi-intangible or mixed products themselves. For example, a restaurant meal includes the tangible food and drinks and intangible services such as cooking and attending. Hence, the type of products delivered by firms to their customers is by itself an important object of inquiry.

Furthermore, past research has identified that intangible products as pure services have concrete properties that distinguish them from tangible physical goods. Several of these properties are reviewed in Cardao-Pito (2012a, 2012b, pp. 337-344), which is not repeated in here. They include but are not restricted to (a) intangibility, (b) heterogeneity, (c) perishability, (d) nonseparation of production and consumption in many services, (e) nonownership of services, (f) active participation of the customer in the production of many services, contrary to what happens with physical goods, as well as other features of service production. Intangible flow theory suggests that the generation of cash flows cannot be simply explained by commodities, where everything that may originate a cash flow is a commodity. Human beings and intangible flows may have several characteristics preventing them from being considered as commodities, assets, capital, or resources.

Through the new theory framework, we may achieve tools to observe demonstrable human-related intangible flows in economic and societal production. The delivery of operating product flows to members of society may actually be an important phenomena to explain the existence of organizations. Mainstream economics is not technologically prepared to study this vital function organizations may have in human societies. Nonetheless, to inquire this possibility, the new theory requires methodologies to study and classify organizational operating product flows. One of those methodologies is proposed in the next section.

Research Design and Sample

Operating (In)Tangibility and the Classification of Organizations According to the Intangibility of Their Operating Product Flows

In the intangible flow theory, a product is an output that results from the productive process, and commodities are pure physical goods. Hence, a product can be, but is not necessarily, a commodity. A purely intangible product is a product that is not associated with any commodity (e.g., a pure service such as teaching). A hybrid product is an output of economic production that integrates one or more commodities with intangible flows such as service flows, communication flows, knowledge flows, and other intangible flows. As explained above, an example of a hybrid product might be a restaurant meal, which includes physical goods (food and drinks) and intangible services (cooking and attending).

Developed from the intangible flow theory, the concept of operating intangibility aims at inferring the tangibility of operating product flows produced by organizations (Cardao-Pito, 2010, 2012a, 2012b). The operating intangibility is the component of an organization’s operating cost structure that is not directly related to the costs of commodities (i.e., physical goods) or tangible fixed assets (e.g., equipment, property, or plant).

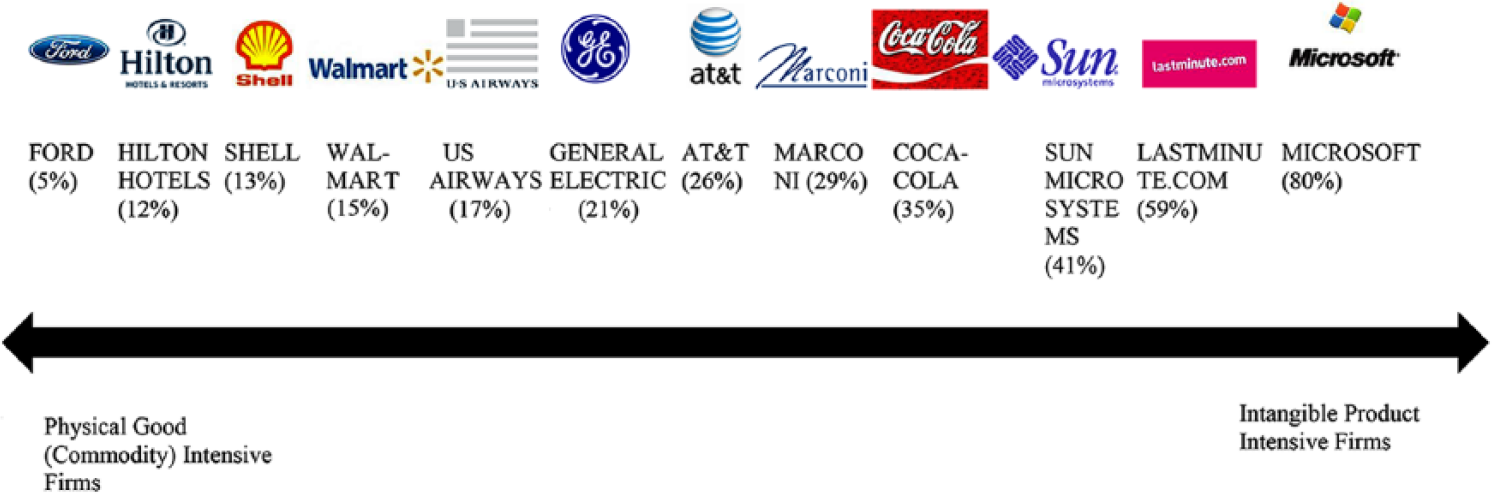

The level of operating intangibility (LOI) framework is intended to describe the degree to which an entire organization is reliant on intangible inputs and outputs (e.g., the LOI can determine whether the products of Microsoft and Coca-Cola are more intangible-intensive than the products of Ford and Shell). The LOI puts physical good-intensive firms (e.g., firms producing and selling automobiles, or relying heavily on physical infrastructures, such as hotel chains and airline companies) at one end of the scale, and intangible product-intensive firms (e.g., firms producing software and pure services) at the other end. Classified at the middle of the scale are firms that supply a mixture of physical goods and intangible products in their core business model, as well as firms that offer products that are themselves mixed. For example, whereas one may consider a soft-drink firm as a company focused mainly on the sales of physical goods, its mean LOI can be much higher than that of supermarkets. These relatively high values are consistent with a business model that is based on both tangible flows and important intangible flow-related expenses such as marketing and brand awareness (Cardao-Pito, 2010). Likewise, a hotel network, an airline company, or a supermarket chain would traditionally be considered as pure service firms. However, they rely intensively on physical commodities to generate their cash flows through product sales. To exemplify how the operating intangibility classification system works, Figure 1 orders several well-known firms operating in the United States according to the materiality of their product flows (outputs), identified by their mean level of operating (in)tangibility (adapted from Cardao-Pito, 2010, 2012a, 2012b, who has used the Compustat database over 41 years: 1966-2006).

Example of well-known corporations classified by the average tangibility of their product flows (operating intangibility; Years 1966-2006).

Linking Operating Intangibility to Other Economic Characteristics of Firms

The LOI methodology was used to classify organizations according to the tangibility of operating product flows they deliver to member of society. If this LOI is linked to other economic characteristics that are related to financing and investing decisions, then, it may also be possible to identify an anomaly to the dominant separability assumption found in mainstream economics. The other economic characteristics investigated in the article are the size of revenues, the capital structure, and the capital expenditures in tangible property, equipment, and plant. While trying to empirically identify connection among different firms’ characteristics, one needs to be aware that firms’ decision are not only dependent upon the firms themselves. These decision are impacted by a myriad of other factors. Furthermore, firms’ characteristics change along different historical periods, stages of the country development or firm life (DeAngelo & Roll, 2015; Graham, Leary, & Roberts, 2015).

Still, it may be possible to suggest an empirically connection between operating intangibility and the size of firms. The variable commonly identified in economics as size, or firm size, describes the magnitude of the monetary turnover (revenue) generated through the sales of products to customers. The material cash flows generated can be considered tangible flows because they can be precisely quantified to an exact value (Cardao-Pito, 2004, 2012a, 2012b). Regardless of the form that a cash flow may assume, the exact amount of money that has been moved is knowable. In the same manner, through the cash flow statement, a corporation presents a precise report of its complete cash movements during each fiscal period. Even if linked to distinct symbolic referents and social systems, the material practice of money is one of its defining properties (Gilbert, 2005). That is, even though money can have several social roles and meanings, which are debated by social scientists, it also has a pragmatic nature in the modalities of exchange and circulation (Maurer, 2006).

As noted previously, no product sale is completely tangible. While some firms may trade utterly intangible products (e.g., pure services), firms dealing in physical goods may trade both tangible and intangible flows of products with their customers (e.g., selling services, marketing), and thus they may require costly organizational infrastructures to deal with the physical goods. This reasoning is congruent with the enduring economic concept of break-even (e.g., Charnes, Cooper, & Ijiri, 1963; Dean, 1948). As is well known, a firm accomplishes the break-even point when its revenue function equals its cost function. A firm is unable to survive if it remains below the break-even point for many years, due to insolvency. Without loss of generality, one may observe that, in recent years, the sales values of two of the largest intangible product-intensive firms (i.e., Linkedln and Facebook) have been rather small compared with those of large physical good-intensive firms (i.e., Ford and Shell). Physical good-intensive firms may thus require larger economies of scale to function well and be sustainable in the long run. Although higher operating intangibility will not always imply a smaller firm size, this empirical association may be observable in samples with many firms.

If an empirical connection between operating intangibility and firm size does exist, it might also connect operating and financial decision. Past research has identified that in most countries, firms with larger revenue size tend to have more debt in their capital structures (Booth, Aivazian, Demirguc-Kunt, & Maksimovic, 2001; Fama & French, 2002; Frank & Goyal, 2009; Kurshev & Strebulaev, 2007; Öztekin, 2015; Rajan & Zingales, 1995). Hence, an association between operating intangibility and the capital structure would at least be mediated by firm size. Although country specific differences might exist, to some extent, there are two channels through which the materiality of a firm’s flows of products (outputs) might directly affect its capital structure via firms’ revenue size: (a) The collateral value associated with physical-good tangibility and related investments offers protection against default to lenders when negotiating debt contracts (see Jimenez, Salas, & Taurina, 2006). For instance, in the extreme case of default, a creditor may eventually take possession of fixed assets, physical goods, and raw materials. However, inherent characteristics of services and other intangible products prevent them from being considered as assets (see also Cardao-Pito, 2004, 2012a, 2012b, 2016). Therefore, creditors cannot take possession of services and other products in the same manner in which they would hold material economic elements such as physical goods and cash. Furthermore, the size of sales may assure creditors as a form of quasi-collateral. (b) The need for external financial sources for highly tangible investments that could be felt less as product-intangibility rises, and size decreases. Self-financing is generally considered to be the preferred source of a firm’s financing (Fama & French, 2005; Graham & Harvey, 2001), and product sales are the principal mechanisms for generating the operating material cash inflows. If, contrary to the more physical good-intensive firms, higher intangible product-intensive firms with smaller revenue size could more often manage to finance their investments without obtaining external capital (e.g., debt, equity, or hybrid securities), then this ability might have an impact on their capital structures.

I also tests whether higher product intangibility is associated with less capital expenditure for material physical infrastructure being required for producing and/or handling flows of physical goods, such as investments in tangible long-term (fixed) assets, namely, property, equipment, and plant. The materiality of the flows of products may create the need for a firm to invest in material devices necessary for its prosecution such as property, equipment, and facilities. Economic calculation is not an anthropological fiction, precisely because it is not a purely human mechanical and mental competence; it is distributed among humans and material devices (Callon & Muniesa, 2005). As noted by Volkoff, Strong, and Elmes (2007), when embedded in technology, social aspects, such as routines and roles, acquire a material aspect. Firms of differing sizes may have different levels of capital expenditure (Kerstein & Kim, 1995). However, even if I cannot find a quantitative empirical association between operating intangibility, or size, and investments in tangible devices as a proportion of revenues, it might be fair to assume that a large proportion of firms’ investments is directed to the production of operating product flows to be delivered to members of society. Thus, one may still be able to hypothesize that there is a qualitative intangible association between operating product flows and concrete investments made by firms.

One must be aware that firms decision are not only dependent upon themselves; they are impacted by many different factors arising from their environment and context.

Variable Definitions

The four key variables studied in this article are the (a) LOI; (b) size of the cash flow generated through sales; (c) proportion of debt in the capital structure; and (d) capital expenditures in property, equipment, and facilities. To test the separability assumption, I intend to identify interesting and useful correlations, not the direction of causation between these variables.

Under this theoretical framework, the LOI can be measured as follows:

where LOI (

A method is needed to infer the expenses that are directly related to commodities and tangible fixed assets (

Therefore, one must choose among information available in the database, even if such information is known to be imperfect. I define a proxy to identify a firm’s operating intangibility in the following manner:

where the LOI proxy (

The other variables are defined as follows:

In addition, two other two other control variables were used in regression models:

The testing variables and control variables to report mediating effects make reference to standard research in capital structure studies (e.g., Baker & Wurgler, 2002; Dempsey, 2013, 2014; Fama & French, 2002; Khalid, 2011; Lemmon, Roberts, & Zender, 2008; Mateev & Ivanov, 2011; Rajan & Zingales, 1995). For replication purposes, the appendix describes the specific data mnemonics necessary to compute the variables at the database.

Sample

The sample for this study was obtained from the Thomson Reuters’ Datastream Worldscope database, which provides information about firms listed in stock markets around the World. I have studied 10 countries samples, which are those with the highest number of usable firm/year observations in the database. These countries are Australia, Canada, China, Germany, Japan, Malaysia, Singapore, South Korea, the United Kingdom, and the United States. In total, 21,108 firms listed at the beginning of the 21st century (2000-2011) are used in the sample, providing 151,509 firm/year observations for analysis. Each firm in this study can be clearly identified by name, location, economic characteristics, and observation dates.

The selection of the 10 countries from the Thomson Reuters’ Datastream Worldscope database has followed a pragmatic criterion, namely, statistical and econometric robustness. The choice over countries with larger samples of usable observations was made taking in careful consideration the problem of the robustness of findings, giving that smaller samples could render results that were less conclusive (Balestra & Krishnakumar, 2008; Baltagi, 2008; Green, 2003; Matyas & Sevestre, 2008). Furthermore, smaller country samples might be organized around fewer geographical business clusters, where a business cluster is understood as a geographic concentration of interconnected businesses, suppliers, and associated institutions in a particular field (Eisingerich & Boehm, 2007; Porter, 1998, 2000) The eventual interconnectedness of firms will be interesting to study in future research. However, at this stage I am looking for heterogeneous country samples to study associations of the LOI to other economic characteristics of firms.

Therefore, given a myriad countries in the database, the 10 countries selected can be described as the set of countries with larger firm constituent list in Worldscope database. For example, countries such as Italy, Spain, and Brazil were excluded from the study on the simple grounds of having less listed firms (and reported in the database) in the studied period. The only exception to this simple rule is India that unfortunately does not have information necessary to compute LOI for most firms. The analysis starts on year 2000 because for most countries the number of usable observations before that year is relatively low. The time period of 2000-2011 corresponds to the first 12 years of the 21st century.

These 10 countries subsample can be seen as quite heterogeneous. They contain four countries located either in Europe or North America (Canada, Germany, the United Kingdom, and the United States), and six countries outside that geographical area (Australia, China, Japan, Malaysia, Singapore, and South, Korea). The majority of the population is not Christian/Catholic in five of the sample’s countries (China, Japan, Malaysia, Singapore, and South Korea). Furthermore, the sample contains eight countries that are part of G-20 group, which includes the most industrialized countries in the World (Australia, Canada, China, Germany, Japan, South Korea, the United Kingdom, and the United States), and two countries that are not included in the G-20 group, although having relatively sophisticated capital markets (Malaysia and Singapore).

The Financial Accounting Standards Board (FASB) accounting norms are applicable specifically in the United States’s economy and not followed in the other nine countries. Nevertheless, there has been a significant effort of harmonizing accounting norms over the world in the past years. Finally, four countries in the sample have English as the first speaking language (Australia, Canada, the United Kingdom, and the United States), and 10 countries have other first speaking language (China, France, Germany, Israel, Japan, Malaysia, Singapore, South Korea, Sweden, and Taiwan).

Moreover, I do not mix the 10 country samples to make inferences because we know that location is relevant for firms’ characteristics (Baschieri, Carosi, & Mengoli, 2015, 2016; Carosi, 2016). Thus, inferences are conducted by country sample. These 10 countries can be rather distinct in terms of political landscape, economic framework, society characteristics, economic development, cultural background, accounting norms and practices, and so on. Therefore, the sample used should not be seen as an aggregated sample but as a set of subsamples representing 10 quite different country subsamples. Therefore, I will avoid making conclusions from the full sample results and instead will report my findings from each country’s sample.

Descriptive Statistics for the Variables Under Study at Each Country Sample

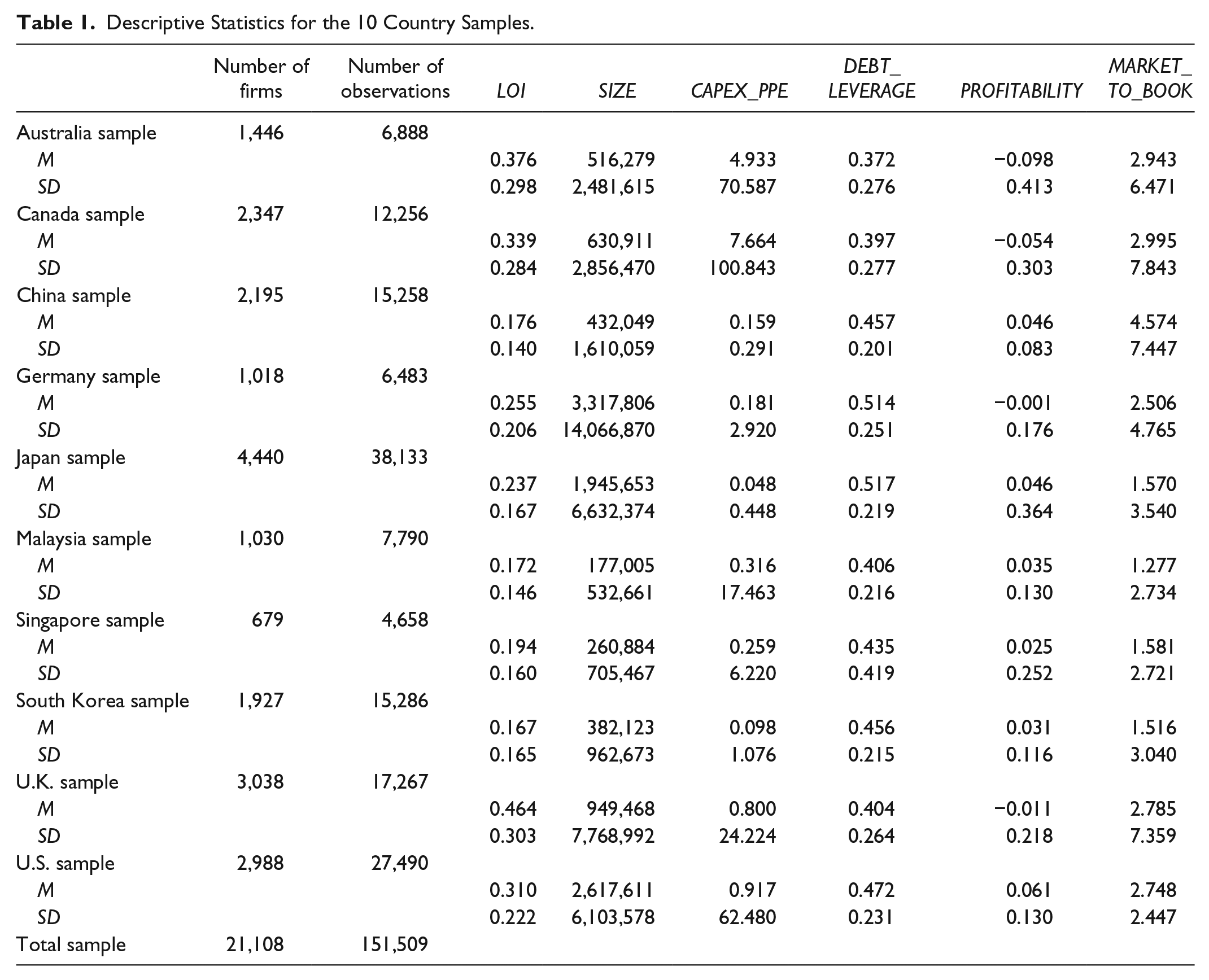

Table 1 reports the number of firms and observations at each country sample, and descriptive statistics for the four variables tracked in the article, namely, LOI, SIZE, CAPEX_PPE, and DEBT_LEVERAGE. Furthermore, Table 1 reports also two additional variables used in the robustness procedures involving regression models, namely, operating income divided by total assets, and the market to book value of equity. The observations described in Table 1 are those final observations used in this study. Beforehand, I have eliminated all observations where there was not enough information to compute the variable tracked in this study. Furthermore, to avoid possible errors in the database, I have eliminated a very small number of observations where LOI or DEBT_LEVERAGE were not included in the expected interval [0%; 100%].

Descriptive Statistics for the 10 Country Samples.

The variables are identified for each of the 10 country sample as to their mean, standard deviation, and t values. Table 1 presents detailed descriptive statistical data (mean value, standard deviation, and t value) for each economic variable under analysis. Statistical values are presented by country sample and by LOI decile within each country sample. As explained in the article, I intentionally avoid making any inferences from the total sample, because my sample includes a very heterogeneous set of countries. The analysis is only conducted within each country sample.

Statistical Procedures

Three key statistical procedures will be used to make inferences: (a) Pearson’s correlation coefficients, 1 (b) decile analysis, 2 and (c) panel data regressions. 3

Results

Mean LOI by Country Samples

Two phenomena are apparent from Figure 2, which describes the mean value of LOI for each sample year (2000-2011) and for each country sample. First, the yearly mean value of LOI is relatively stable within each country sample. Second, during this period, countries can be classified as having relatively low, intermediate, or relatively high mean LOI values. I use µ to denote sample mean. Samples with relatively low mean LOI values (<20%) include those of South Korea (µ = 0.17, yearly range of µ = [0.13; 0.18]), Malaysia (0.17, [0.16; 0.19]), China (0.18, [0.16; 0.20]), and Singapore (0.19, [0.18; 0.21]). Samples with intermediate mean LOI values (20%-30%) include those of Japan (0.24, [0.22; 0.25]) and Germany (0.25, [0.24; 0.27]). Samples with relatively high mean LOI values (>30%) are those of the United States (0.31, [0.30; 0.32]), Canada (0.34, [0.31; 0.36]), Australia (0.38, [0.33; 0.42]), and the United Kingdom (0.46, [0.42; 0.50]).

Spearman’s correlations at each country sample between indicative variables for LOI decile and SIZE, CAPEX, DEBT_LEVERAGE, and LOI.

Spearman’s Correlations

As described before, Spearman’s correlation coefficient (ρ) was used to identify whether the operating decisions captured by LOI can be statistically associated with the firm’s other economic characteristics that describe investment and financial decisions (i.e., SIZE, CAPEX_PPE, and DEBT_LEVERAGE). These correlation coefficients are reported in Table 1 and discussed below. The p value indicates the probability of obtaining a test statistic result at least as extreme as the one that would be actually observed, assuming that the null hypothesis is true. Thus, the lower the p value, the lower evidence we have to accept the null hypothesis.

Every country sample exhibits a nonrandom statistical relationship between LOI and SIZE (Table 2). For all country samples, this relationship is negative and has an absolute value of ρ greater than 23%. This phenomenon is observed in the relatively low mean LOI samples of South Korea (ρ = −0.261, p < .001), Malaysia (ρ = –.398, p < .001), China (ρ = −0.514, p < .001), and Singapore (ρ = −0.452, p < .001); in the intermediate mean LOI samples of Japan (ρ = −0.255, p < 0.001) and Germany (ρ = −0.231; p < .001); and in the relatively high mean LOI samples of the United States (ρ = −0.371, p < 0.001), Canada (ρ = −0.589, p < .001), Australia (ρ = –.437, p < .001), and the United Kingdom (ρ = –.617, p < .001). The sample for Germany has the lowest absolute value of ρ (which is still relatively high), whereas the United Kingdom sample has the highest absolute value of ρ.

Spearman’s correlations among the size of cash flow turnover (SIZE) and the level of operating intangibility (LOI), capital expenditures in tangible long term assets as proportions of revenues (CAPEX_PPE), and proportion of debt in the capital structure (DEBT_LEVERAGE).

Note. ρ = Spearman’s correlation of the variable with the LOI variable within the subsample. p value = Prob > |r| under H0: Rho = 0.

p value of at least 10%. **p value of at least 5%. ***p value of 1% or better.

As noted before in the literature review, previous research has found a strong statistical association between the proportion of debt in the capital structure (DEBT_LEVERAGE) and the size of revenues (SIZE). I have also found the same empirical association in the 10 country samples. The minimal ρ is Japan sample’s, which still holds the significant (ρ = .245, p < .001). Two countries have correlation above 50%, namely, Australia (ρ = .509, p < .001), and the United Kingdom (ρ = .598, p < .001). All the other countries display robust associations above 25%: Canada (ρ = .430, p < .001); China (ρ = .322, p < .001); Germany (ρ = .495, p < .001); Malaysia (ρ = .296, p < .001); Singapore (ρ = .274, p < .001); South Korea (ρ = .327, p < .001); and the United States (ρ = .443, p < .001). Hence, we may have found an association between operating decisions and financial decisions to be mediated by the size of firms’ revenues.

However, the relationship between LOI or SIZE to CAPEX_PPE appears to be less conclusive. Table 2 reports the association between SIZE and CAPEX_PPE, which otherwise of the previous relationships, display different behavior among the country samples (as the relation between LOI and CAPEX_PPE not reported in here for space motives). The correlation coefficient is not significant at least by the 10% level in two countries, namely Singapore and South Korea. It is positive and below 25% in four countries, namely, Germany (ρ = .162, p < .001), Japan (ρ = .125, p < .001), Malaysia (ρ = .039, p < .001), and the United Kingdom (ρ = .233, p < .001). On the contrary, ρ is negative and below 25% in the other four countries: Australia (ρ = –.149, p < .001), Canada (ρ = –.207, p < .001), China (ρ = –.172, p < .001), and the United States (ρ = –.032, p < .001).

LOI Deciles

As explained before, I divided the firms of each country sample into 10 deciles, according to their mean LOI. Firms with similar mean levels of operating intangibility were grouped together. Each decile has approximately the same number of firms (i.e., 10% of all firms in the respective country sample). When a firm is classified into a decile, all of its observations are also classified into that decile. The objects of analysis are the organizations. Organizations that share one similar characteristic—a similar mean LOI —are classified together by decile without assuming any status of homogeneity. Within every country sample, I created 10 dummy variables to identify the 10 deciles. These dummy variables are equal to one if the firm/observation is classified into the respective decile, and zero otherwise.

Figure 3 reports ρ between these dummy variables and LOI, SIZE, CAPEX, and DEBT_LEVERAGE at the 10 country samples. The green bar denotes the correlation with LOI at each dummy by decile. It is obviously the strongest, as firms were classified by decile according to their mean LOI in sample. Hence, the difference of correlations between decile 1 and decile 10 dummy ranges from 79% in Australia sample, and 97% in Japan.

Mean LOI for each year for the 10 country samples (2000-2011).

The correlations between the dummy variables and other variables are not as strong as those with LOI. Nonetheless, as is patent on Figure 3, the relation to the variables SIZE (blue bar), and DEBT_LEVERAGE (gray bar). In case of SIZE and DEBT_LEVERAGE at the 10 country samples, the dummy variables for lower LOI deciles (those where firms are most physical-good-intensive) have positive ρ with SIZE and, DEBT_LEVERAGE. On the contrary, the dummy variables of higher LOI deciles (those where firms are most focused on intangible product flows) have a negative ρ with SIZE and DEBT_LEVERAGE. As found before, the behavior of CAPEX_PPE among the LOI deciles is less conclusive as to find a similar pattern in all country samples in terms of money invested in tangible assets as a proportion of revenues.

Panel Data Regressions

Although the Spearman’s correlations seem to be quite interesting, they can only be used to identify eventual monotonic relations among the variables. Moreover, Spearman’s correlations are used only for two variables at a time. My sample can be described as a panel data sample. The same firm is likely to have several yearly observations over the studied period. Hence, the intradependence of those observations may affect results.

As explained before, to address these issues, I have implemented regression models prepared for panel data analysis, hence controlling for firm and year effects. In these models, I have regressed the variable SIZE on the variables LOI, CAPEX_PPE, and DEBT_LEVERAGE, and control variables PROFITABILITY and MARKET_TO_BOOK. The regression is conducted on SIZE because: (a) intangible flow theory suggests that inherent needs associated to the materiality of operating product flows may reflect on the size of revenues; and (b) previous research has found a strong empirical correlation between the size of revenues and the proportion of debt on capital structures; hence, it is interesting to observe whether this association persists when the LOI variable is included in the model along with the other variables. I have computed a model for each country sample. The results are displayed in Table 3.

Regression Analysis With Panel Data Models Controlling for Firm and Year Fixed Effects.

Note. The variables are defined in the article. These regression models are control the fixed effects of firms and years. β = regression coefficient. p value = Prob > |r| under H0: Rho = 0.

p value of at least 10%. **p value of at least 5%. ***p value of 1% or better.

The beta (β) identifies the regression coefficient that cannot be directly compared with ρ because β is not necessarily limited to the interval [–100%; 100%]. Furthermore, the β captures differences in means and distributions at each subsample. Nevertheless, the t value of β is an important indicator of empirical association among variables. The t value is related to the p value mentioned above, which indicates the probability of obtaining a test statistic result at least as extreme as the one that would be actually observed, assuming that the null hypothesis is true. Giving the sample size in every country sample, a p value of 10% requires an absolute t value of at least 1.645. A p value of 5% requires an absolute t value of 1.960. For a p value of 1% or better, an absolute t value of 2.576 or higher is demanded. The null hypotheses are that no statistically significant relation occurs among SIZE and the variables LOI, CAPEX_PPE, and DEBT_LEVERAGE. Figure 4 exhibits the t values at each country sample regression for the βs of SIZE, CAPEX_PPE, and DEBT_LEVERAGE.

At the country sample regressions on SIZE described in Table 3, the t values for the regression coefficient of LOI, CAPEX_PPE, and DEBT_LEVERAGE.

The first point to observe is that the r-squared is very high in all models, ranging from 0.891 in the Singapore sample and 0.976 in the Japan sample, which may denote strong robustness of the models used. Furthermore, in all samples, the β of LOI has a t value much higher in absolute terms than what is required to achieve a p value of 1%. The t value ranges from −12.32 in the Germany sample to −60.94 in the China sample. Hence, these findings seem to confirm that there appears to be a nonrandom empirical relation between LOI and SIZE in all country samples, as exhibited on Figure 4.

Although the absolute t values for the β of DEBT_LEVERAGE are not as high as those of LOI, they are still much higher than what would be required to attain the 1% level of significance. Thus, these t values are also not compatible with the null hypotheses in regard to DEBT_LEVERAGE. The t value ranges from 12.09 in the Germany sample (several times of what would be required for a p value of 1%) to 32.25 in the China sample. Therefore, these findings also seem to indicate a relevant empirical relation between SIZE and DEBT_LEVERAGE in all country samples, as found in previous literature. Therefore, an association between operating decisions and financial decisions is at least mediated by firms’ revenue size.

With regard to coefficient of CAPEX in the 10 country samples, a negative and significant coefficient at the 1% level was found in nine country samples (exception being South Korea sample). However, as this finding is not consistent with the previous Spearman correlation and decile analysis, I will avoid stating that these results can be considered as conclusive. I do not find totally demonstrable in these 10 country samples that firms with different SIZE or LOI may tend to have systematically different CAPEX. However, as I will explain later, this analysis takes into consideration merely the amount of money invested as a proportion of revenues. Thus, it cannot exclude considerations related to qualitative intangible dimensions of the investments implemented by firms.

Other Robustness Procedures

Similar results to the above were obtained when using Pearson’s correlation coefficients. Furthermore, all test have been repeated after outlier observations have been excluded from the 10 country samples. The removal of outliers did not produce substantially different findings.

Limitations

Despite the use of spearman correlations, decile analysis, and regressions for panel data controlling for fixed effects, there were still some imperfections in this study, both conceptually and empirically. As explained by the intangible flow theory, intangible flows cannot be measured with precision. By definition, a proxy cannot measure intangible flows exactly because this would imply that the measurement referred to tangible flows. Intangibility is endogenous. Therefore, we need to use tangible flows for quantitatively inferring intangible flows. The proxies used are merely estimates. For the large sample used, the proxies seem to be statistically significant and congruent. However, they are approximations, not precise measurements, of intangible flows. Furthermore, the item “selling, general, and administrative expenses” incorporates a diverse set of agglomerated expenses. Most of these expenses seem to be related to intangible flows, such as work and service production, marketing, R&D, legal expenses, and so on. However, some firms may incorporate items that are not intangible flow-related into their selling, general, and administrative expenses. Moreover, the use of different accounting policies between firms, years, and countries may influence the results, although the econometric robustness procedures address samples with panel data characteristics. In addition, some issues with the proxy can only be solved by accounting authorities, as only accounting norms have the power to mandate that companies discriminate expenses with more detail in their financial statements.

The fact that a very large sample was used and several econometric tests were implemented may contribute to the robustness of the findings. If fewer observations had been used, there would be a greater risk that the result would be due to the effects of a small sample size. All of the proxies that were used are related to operating expenses and, therefore, operating decisions, which is one of the major issues under study in this article. Nevertheless, this report represents the first time that operating intangibility proxies have been used in the context of identifying the tangibility of a firm’s product flows. As such, the behavior of operating tangibility is still not fully understood. A proxy for operating intangibility that is computed with publicly available information must always rely on a sensible balance between inferring immeasurable intangible flows with reasonably quantifiable tangible elements.

Discussion and Conclusion

The empirical results seem to indicate that firms partially organize themselves according to operating needs that are associated with the tangibility of the flows of operating products (outputs) sold to customers. Firms that produce and deliver physical goods/commodities (e.g., cars or planes) may inherently have different economic characteristics compared with firms that deliver intangible products (e.g., consulting or advertising). Thus, firms may indeed exist and organize to deliver operating product flows to members of society, as suggested by the intangible flow theory. This study reports a possible anomaly to the dominant separability assumption found in mainstream economics, which, as explained before, presupposes that (a) financial decisions are isolated from operating and investing activities and what firms actually do to generate cash flows; and (b) firms exist to increase the wealth of their owners/shareholders.

For the examined 10-country sample, and as predicted, strong empirically connections were found between higher operating intangibility and lower firm revenue size. Although not necessarily applicable to every firm, this statistical association may exhibit that intrinsic needs related to the tangibility of operating product flows are reflected on the size of firms’ revenues. Furthermore, and as in previous research, I have found a robust positive association between firm size and more debt in the capital structure. Therefore, an association between the operating intangibility and financial decisions is at least mediated by firm size.

If we were restricted to quantitative research tools as in mainstream economics, an association between operating intangibility and capital expenditures in tangible property, equipment and plant would be less conclusive in the studied 10 country samples. Nevertheless, the quantitative analysis mostly inquires whether firms invest more or less money in this investment rubric. If we do not exclude intangible dimension of firms’ investments, we can still hypothesize that concrete investments in the productive process might be related to specific flows of operating products. For example, an airline company that invests in new planes, a software company that invests in new cloud hardware facilities, and a car factory that invests in robots may have the same proportion of investments as a proportion of revenues. Yet, qualitatively, these investments are rather different. As explained by intangible flow theory, although mathematical/quantitative research methodologies are very relevant for science, they are insufficient to study economy and society. A possible association between operating product flows and capital expenditures cannot only be considered in terms of the invested money amount. Mainstream economics is not prepared to study intangible dimensions of investments because of its all-encompassing concept of capital, and lack of research tools to capture the intangibility of economic and societal production.

These findings may be useful and interesting. However, this is a descriptive analysis, and I make no claim as to the direction of causation between the studied economic characteristics. These findings merely reflect the samples and period under study. Furthermore, I do not advise that organizational managers or stakeholders make automatic and nonreflected decisions related to operating intangibility, size, capital expenditures, or debt leverage. Any major organizational decision must be carefully considered and chosen according to the specific characteristics, resources, and environment of the organization. Within the circumstance of the limitations and cautions mentioned above, the intangible flow theory may contribute to form a new perspective from which to observe real-life organizations.

Footnotes

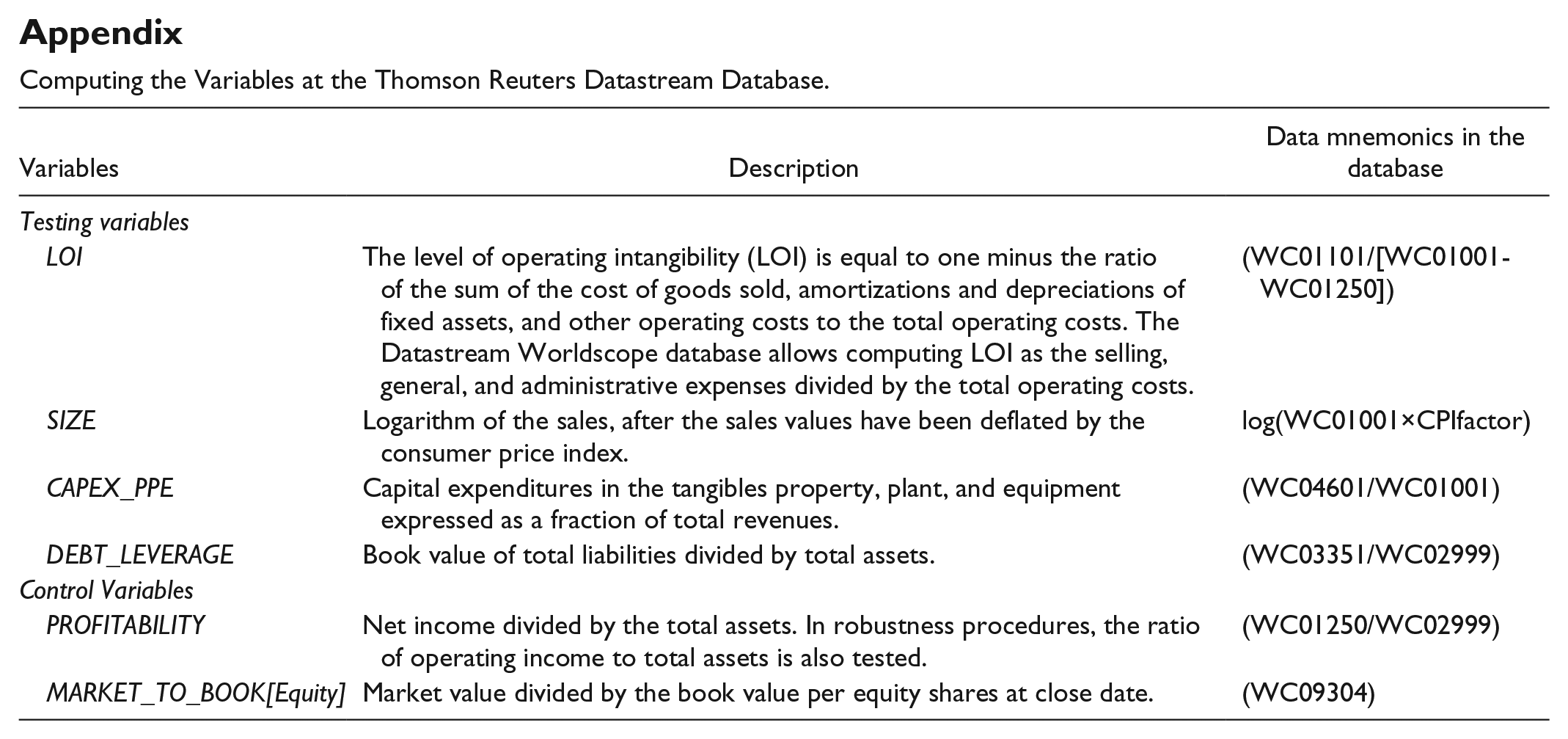

Appendix

Computing the Variables at the Thomson Reuters Datastream Database.

| Variables | Description | Data mnemonics in the database |

|---|---|---|

| Testing variables | ||

| LOI | The level of operating intangibility (LOI) is equal to one minus the ratio of the sum of the cost of goods sold, amortizations and depreciations of fixed assets, and other operating costs to the total operating costs. The Datastream Worldscope database allows computing LOI as the selling, general, and administrative expenses divided by the total operating costs. | (WC01101/[WC01001-WC01250]) |

| SIZE | Logarithm of the sales, after the sales values have been deflated by the consumer price index. | log(WC01001×CPIfactor) |

| CAPEX_PPE | Capital expenditures in the tangibles property, plant, and equipment expressed as a fraction of total revenues. | (WC04601/WC01001) |

| DEBT_LEVERAGE | Book value of total liabilities divided by total assets. | (WC03351/WC02999) |

| Control Variables | ||

| PROFITABILITY | Net income divided by the total assets. In robustness procedures, the ratio of operating income to total assets is also tested. | (WC01250/WC02999) |

| MARKET_TO_BOOK[Equity] | Market value divided by the book value per equity shares at close date. | (WC09304) |

Acknowledgements

The author thanks Joao Silva Ferreira (University of Lisbon), Julia Smith (University of Strathclyde), Patrick McColgan (University of Strathclyde), Tae-Hee Jo (State University of New York), Tony Lawson (University of Cambridge), Cynthia E. Devers (Michigan State University), Maria Nazaré Barroso (University of Lisbon), Steven Michael (College of Business at Illinois), Paul Adler (University of Southern California), Frederick Lee (University of Missouri-Kansas City), Andrew Marshal (University of Strathclyde), Christine Cooper (University of Strathclyde), Meghan A. Thornton (Purdue University), John Ferguson (University of Strathclyde), and the participants in conferences and seminars for reading and commenting articles related to intangible flow theory.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author acknowledges the financial support from the ADVANCE Research Center at ISEG, University of Lisbon and FCT—Fundação para a Ciencia e Tecnologia (Portugal), national funding through research grant (UID/SOC/04521/2013).