Abstract

This research examines corporate governance disclosure in Nigerian and South African Banks using the unweighted disclosure index technique. This research provides a cross-sectional examination of corporate governance disclosure practices in the annual reports of listed banks in Nigeria and South Africa. The results suggest that Nigerian and South African banks have a high level of corporate governance disclosure. However, Nigeria and South African banks have low levels of voluntary corporate governance disclosure. Furthermore, in reporting of voluntary corporate governance disclosure, Nigerian banks appear to be collating information with no link to the overall business strategy of the organization while the South African banks have a more robust approach to voluntary corporate governance disclosure as they apply international guidelines such as the Global Reporting Initiative to their disclosure.

Background of the Study

In the last decade, corporate governance has become a lexicon in developing countries, particularly because of the increasing level of corporate governance scandals that have occurred in America, Europe, Asia, and Africa, as well as the global financial crisis that occurred in the last decade (Bhasin, 2010; Okpara, 2009). The recent global financial crisis has demonstrated that lack of transparency in business practices, responsible corporate executives and shareholders rights, could lead to possible business failures of even strong economies due to diminishing investors’ confidence (Solomon, 2010). Developing countries, in particular, have been warned of the consequences of adopting poor corporate governance practices that may cause the shares of businesses to be sold for billions of dollars less than they ought to if their firms had put in place good corporate governance practices and policies (Anon., 2001). Bernard Black conducted a study to determine whether corporate governance matters, in terms of share price. He found that it made a huge difference (Black, 2001). Equally, Russian firms that saw a significant rise in their share prices were firms that adopted and implemented corporate governance reforms (Miller, 2002). These are some of the genuine explanations that have deepened the interest in corporate governance among policy makers in developing countries across Asia and Africa.

The model of corporate governance in developing countries has embraced both market-based and insider approaches to corporate governance (Humayun & Adelepo, 2012). Privatization of government-owned business enterprises is one example of market-based corporate governance practices (Ahunwan, 2002). Of recent, the increasing trend of privatization mantra has followed decades of state ownership and control of business enterprises (Oyejide & Soyibo, 2001)—a common characteristic of most developing countries in Africa. After the period of independence, state ownership was done more as a sign of national pride and sovereignty rather than any practical economic considerations (Ayittey, 1989). With the unsustainability of most state-owned enterprises by developing countries in Africa, most African countries have carried out far-reaching economic reforms that have focused on privatizing most government-run state enterprises (Adekoya, 2011; Isukul & Chizea, 2015). The role of government in these countries has been redefined to focus on creating and providing the necessary infrastructure, enabling environment and regulatory framework for corporate governance firms and business enterprises to thrive (Adegbite, 2012).

Also, a common feature of corporate governance in developing countries is the inclination toward an insider approach, with a prevalence of family-owned, closely guarded business enterprises and the problems and issues that arise with family-oriented business structures (Adegbite & Nakajima, 2012). The board executives of most of these businesses are filled with family members and close friends; often times, none of them are qualified for sensitive positions they occupy (Samaha & Dahawy, 2010). In a business environment such as this, the executives are more inclined to further their own personal interests to the detriment of other critical stakeholders and shareholders (Yakasai, 2001). As a means of checking the excesses of board members, independent directors have been advocated as a panacea to curb the improper executive action (Solomon, 2010). However, in developing countries this is not the case, as the business community can be regarded as quite small and also there is an interlocking of personal and financial interests (Nenova, 2005). In such developing countries, independent directors are more likely to be rubber stamps and as such are unlikely to act as effective checks against executive excesses (Tsamenyi, Enninful-Adu, & Onumah, 2007). The weak nature of financial and capital market infrastructure and poor legal enforcement mechanisms implies that shareholder protection, especially minority shareholders and property rights of individuals and corporations, are not effectively protected (Humayun & Adelepo, 2012; La Porta, Lopez-de-Silanes, & Shleifer, 2002).

To address the myriads of issues affecting corporate governance in developing countries, Okike (2007) emphasize the importance of strengthening domestic institutions—They maintain that it is important for financial institutions to improve transparency, risk management, and self-regulation. Furthermore, they encourage the adoption of international standards and best practices in accounting, auditing, and corporate governance disclosure as a means of improving corporate governance standards and practices. Adegbite (2010) also proffers solutions to tackling corporate governance problems in developing countries; he maintains that solutions to corporate governance problems in developing countries must be tackled within the institutional context. He suggests that homegrown solutions should be applied to address the issues, rather than the easier option of applying solutions that have worked in developed countries without regard to whether they are applicable to developing countries.

Statement of the Research Problem

Corporate governance disclosure is crucial for the functioning of an effective and efficient financial market (Brennan & Solomon, 2008; R. Gray, Bebbington, & Walters, 1993). Business firms provide disclosure through several mediums: standardized annual reports that include the financial statement of the firm, management analysis and discussion, footnotes, and other regulatory requirements and fillings (Berndt & Leibfried, 2007). Also, business firms engage in voluntary disclosure through various communication channels such as managerial forecasts, press releases, financial analyst presentations, Internet sites, conference calls, and other corporate reports such as corporate social responsibility and sustainability reports ( Cheng & Courtenay, 2006). Finally, there are also disclosures about firms made by information intermediaries such as financial press, industry experts, and financial analysts (Healy & Palepu, 2001).

The timeliness, adequacy, and availability of appropriate information about financial and market securities are critical for both market confidence and pricing efficiency (Abdelkarim, Shahin, & Arqawi, 2009; Brennan & Solomon, 2008). For investors to make critical decisions and sound judgments on the value of market securities, they need to be well informed of the relevant facts (Haniffa & Cooke, 2002). Information disclosure is considered an important element that is needed for the effective operation of financial and security markets. Presently, regulators are increasingly disturbed about the quality of both financial and nonfinancial information disclosure of firms (Abdelkarim et al., 2009).

Of significant importance, to note, is how corporate governance disclosure practice has evolved. Initially, disclosure simply focused on a firm’s financial statement: At present, corporate disclosure is used as a strategic business tool in risk assessment and value creation (Belkaoui & Karpik, 1989). Recently, the emergence of detailed, extensive, and comprehensive corporate governance disclosure strategies that include every aspect and facet of a firm’s performance has largely resulted in expanding and broadening not just the scope but also the scale of information released by corporations (Eng & Mak, 2003). Disclosure strategies have significantly expanded to include economic, environmental, and social information, and are now considered as key ingredients of many firms’ investors’ requirements and criteria (Abdelkarim et al., 2009; Richardson & Welker, 2001).

In countries with developed capital market and effective legal/regulatory frameworks, a significant amount of research on corporate governance disclosure has been executed (Bushman, Chen, Engel, & Smith, 2004; Marston & Shrives, 1991). Unfortunately, this is not the case with countries with less developed markets. In less developed countries, there is a paucity of research on corporate governance disclosure; in all sincerity, this should not be so (Adelepo, 2011; Bhasin, 2010; Oluwagbemiga, 2014). Compared with corporate governance disclosure in developed countries, in developing countries there are generally lower disclosure standards, weaker regulatory and legal systems, as well as limited enforcement capacity (Nenova, 2005; Okike, 2007); there is significant state ownership or holding of many private business corporations in developing countries (Samaha, Dahawy, Hussainey, & Stapleton, 2012), and board effectiveness and independence tend to be weak and ineffective (Ahunwan, 2002).

From the onset, the intention of this research was to select some of the best banks in Africa to examine their corporate governance disclosure practices, as larger banks are known to have better disclosure practices than smaller banks, because corporate governance disclosure tends to generate considerable costs to firms (Maingot & Zeghal, 2008). More importantly, the research intends to examine the current state of corporate governance disclosure practices in Nigerian and South African banks so as to understand and inform on the nature, focus, and extent of corporate governance disclosure in the Nigerian and South African banking industries. This will inform to what extent corporate governance disclosure in Nigerian and South African banks is similar and different, and if there are differences, what the differences are exactly. The research questions this article intends to address are as follows:

This article intends to contribute to the burgeoning research on corporate governance disclosure in developing countries with particular emphasis on South African and Nigerian Banks. Thus far, there is a paucity of research on comparative corporate governance disclosure in developing countries as most research in developing countries tends to focus on disclosure practices of a single country. This research intends to focus on comparative corporate governance by investigating disclosure practices of South African and Nigerian Banks. In so doing, it extends the research on corporate governance disclosure in developing countries beyond the single case study. This research article begins by exploring the various theoretical frameworks on corporate governance—agency theory, institutional theory, and stakeholder theory. It goes on to examine the literature on corporate governance in Nigeria and South Africa, and research on corporate governance disclosure. It follows with the justification of the methodology adopted in the analysis of the result and discussion of the findings.

Agency Theory

In corporate governance research, agency theory has been used to investigate corporate governance disclosure (Brennan & Solomon, 2008; Cohen, Krishnamoorthy, & Wright, 2004; Healy & Palepu, 2001). The basic assumption about the agency theory is that managers’ (agents) and the owners’ (principals) interest are not aligned (Jensen & Meckling, 1976). The managers or directors are more interested in maximizing their own wealth, power, and prestige while safeguarding their reputations; on the contrary, shareholders are more inclined to maximize the value of their shares and asset holdings (Eisenhardt, 1989). This divergence in the alignment of interests has been the cause of severe tension between agents and principals. Donaldson and Davis (1991) posit that these divergences of interest could sometimes lead to what they call “agency loss.” Agency loss may occur when the returns to the residual claimants (the owners) fall short or below what they would be if the principals, the owners, exercise direct control of the corporation (Guilding, Warnken, Ardill, & Fredline, 2005).

According to the agency theory, in a bid to address these tensions and resolve the differences, the principals have developed a number of policy incentives that seek to align the interests of agents alongside theirs (Hill & Jones, 1992). Some of the policy prescriptions include incentive schemes for managers which recompense them monetarily for enhancing shareholders’ interest. These schemes constitute plans allowing senior executives to obtain shares of the company usually at a reduced price, consequently aligning financial interest of executives with those of shareholders (Jensen & Meckling, 1976). There are other policies designed in a similar manner; however, they are targeted at increasing the levels of transparency and corporate governance disclosure (Bushman & Smith, 2001). Business management and accounting researchers have applied themselves to investigating mechanisms of transparency (financial reporting and voluntary disclosure) which sought to align interests of shareholders and managers (e.g., Bushman & Smith, 2001; Healy, Hutton, & Palepu, 1999; Healy & Palepu, 2001; Hermanson, 2000). Apparently, transparency in the form of increased corporate governance disclosure is considered an important instrument for aligning management and shareholders’ interest (Brennan & Solomon, 2008). Also, it serves as a means of mitigating the information asymmetry that exists between management and shareholders.

Institutional Theory

In contrast, institutional theory maintains that the quality of institutions tends to influence corporate governance practices (Aguilera & Jackson, 2003; Fiss, 2008). This is more so in developing countries where the quality of institutions is poor; corporate governance practices tend to suffer as a result (Adegbite & Nakajima, 2012; Klapper & Love, 2002). Institutional deficiencies such as weak investor protection, poor enforcement of contracts, high levels of corruption in private and public sectors, lax regulatory environment, and unstable political institutions are important determinants in the quality of corporate governance (Adegbite, Amaeshi, & Nakajima, 2013; Claessens, 2006). While agency theory focuses on the relationship between the principal and the agent (Jensen & Meckling, 1976), institutional theory goes beyond the principal/agent relationship—It looks at the broader context and environmental influences that are capable of influencing corporate governance (Amenta & Ramsey, 2010; Meyer, 2007; Scott, 2004). Institutional theory acknowledges that for any business or firm to function effectively, it needs an enabling environment where the rule of law is sacrosanct, viable institutions that protect investors and business firms, and the removal of unnecessary bureaucratic bottlenecks that escalate the costs of doing business (Adegbite & Nakajima, 2012).

Previous definitions of institutions paid significant attention to the formal element of institutions (North, 1990). The term institutions were narrowly defined as enabling and constraining human behavior (Helmke & Levitsky, 2003). Institutions were regarded as formalized structures of written rules, regulations, and codes that have to be obeyed (Hodgson, 2006); failure to comply with the rules and laws resulted in punishments in the form of fines and fees or physical incarceration depending on the gravity of the offense (Nutt-Powell, 1978). A common thread which has been woven through these research studies is the focus on formal institutions to the detriment of the informal elements of institutions (Scott, 2007; Tsai, 2006). Informal institutions were not given much academic consideration. At the time, a common critique and frustration with venturing into research on informal institutions was the difficulty in measuring, appraising, assessing, and evaluating informal institutions (Peng & Jiang, 2010). Informal institutions can be described as manifestations of a society’s normative configuration; they symbolize society’s decisions about the desirability of actions and events.

Recently, a broader definition has been sought to include the formal and informal nature of institutions. Ménard and Shirley (2008) define institutions as “the written and unwritten rules, norms and constraints that humans devise to reduce uncertainty and control their environment” (p. 1). These include (a) written rules and agreements that govern contractual relations and corporate governance; (b) constitutions, laws, and rules that govern politics, government, finance, and society more broadly; and (c) unwritten codes of conduct, norms of behavior, and beliefs. Institutional theory maintains that institutions have the ability to form, build, and create institutional pressures that nudge business firms to seek for social conformity and legitimacy. Again, institutional theory posits that multilevel influences are more important than market pressures and market mechanisms in influencing behavior of business organizations. However, institutional theorists have been criticized for failure to take into consideration individual-level explanations and influences on organizations.

Stakeholder Theory

It does appear that stakeholder theory is similar to agency theory; both theories focus on a nexus of relationships between various stakeholders of the firm (Schwarzkopf, 2006; Solomon, 2010). Stakeholder theory broadens the stakeholders’ relationship beyond the principal/agent relationship to include other critical stakeholders whose activities can significantly influence or impact on the business activities of the firm (Donaldson & Preston, 1995; Hill & Jones, 1992). Another similarity between the stakeholder theory and agency theory is that both theories focus on the creation of value: Agency theory is intent on providing shareholder value while stakeholder theory aims at maximizing value for a diverse group of stakeholders (Reynolds, Schultz, & Hekman, 2006). Of particular importance in stakeholder theory is the expanding of the roles of businesses beyond the narrow profit-seeking motive to include social and ethical obligations of businesses to its various stakeholders (Bosse, Phillips, & Harrison, 2009; Parmar et al., 2010). In doing so, stakeholder theory is redefining the roles and responsibilities of business by suggesting that while making profit is important, businesses have other nonmonetary and nonpecuniary obligations that they need to fulfill (Solomon, 2010).

Stakeholder theory argues that business organizations have relationships with a diverse group of people and that it can foster, support, and maintain the interests of these groups by balancing and taking into consideration their needs and interests (Freeman, Wicks, & Parmar, 2004; Phillips, Freeman, & Wicks, 2003). Stakeholders can be classified into two distinct categories (Reynolds et al., 2006): primary stakeholders and the secondary stakeholders. The primary stakeholders include the following group of people: shareholders, investors, employees, suppliers, customers, local community, and government. The secondary stakeholders can be described as those groups of persons who are not directly involved in the firms’ business activity but can significantly influence the operations of the business.

To date, the influence of stakeholder theory in the field of finance, economics, and accounting is obvious (Strand & Freeman, 2015). It is standard practice for multinational corporations and big businesses to include elements of corporate social reporting in their financial reports. The inclusion of corporate social reporting in financial reports is an attempt by businesses to recognize the importance of other stakeholders who are not necessarily shareholders/managers. Furthermore, by inclusion of social and environmental reports in their financial statements, businesses are beginning to realize that they do have social and environmental obligations to critical stakeholders whose activities can influence their business operations.

In summary, stakeholder theory suggests that the roles of business should be redefined and businesses do have moral, ethical, and social obligations that they need to address. Doing this not only ensures that interests of the various interest groups will be met, but it also ensures that business organizations are allowed to focus on their business operations without any undue distractions that may arise as a result of conflicts between business and its stakeholders (Strand & Freeman, 2015). However, identification and balancing of the interests of the various stakeholders is not as simple as the stakeholder theory implies—It, in fact, can be a cumbersome and complex process (Schwarzkopf, 2006). And sometimes, it will be impossible for firms to identify and balance the needs of the various stakeholders for a variety of reasons, some of which may be that the resources to do so are not available, or the requests made by the various stakeholders are unrealistic and therefore impossible to satisfy (Solomon, 2010).

Corporate Governance in Nigeria and South Africa

In Nigeria, corporate governance practices and conduct have been characterized by endemic corruption, poor transparency, and disclosure practices, as well as significant political interferences in corporate governance activities, consequently distorting and undermining corporate governance development (Ahunwan, 2002; Okike, 2004, 2007; Oyejide & Soyibo, 2001; Yakasai, 2001). In recent times, ongoing corporate governance reforms have been initiated to improve corporate governance practices in Nigeria. Some of these reforms include the following: the 2003 Code of Conduct for Corporate Governance, the 2006 mandatory Code of Conduct for Nigerian Banks post consolidation, the 2007 Code of Conduct for Shareholders Association in Nigeria, consolidation of Nigerian banks, and the increase in the minimum of capital base. These measures were taken to prevent a repeat of the incident that occurred when several banks were bailed out by the Central Bank of Nigeria (CBN) for inability to perform their banking obligations as a result of financial failure, fraudulent activities by bank managers, and questionable business practices (Ogbeche & Koufopoulos, 2007; Isukul and Chizea, 2016).

The story in South Africa is not entirely different. Among emerging countries in the world, South Africa stands out as a very interesting case in which to examine how specific corporate governance reforms have emerged or unfolded (West, 2006). Armstrong, Segal, and Davis (2005) identify a number of government legislations that have been designed to influence and strengthen corporate governance in South Africa: the Companies Act (1973), the Insider Trading Act (1998), the Public Finance Management Act (1999), and the Securities Services Act (2004). In addition, South Africa initiated the publication of corporate governance guidelines and codes of practice with the King I Report (1994), King II Report (2002), King III Report (2009), and King IV Report (2016), instigating an unprecedented global interest in corporate governance in Africa. The King IV report makes particular emphasis on enhancing accountability through disclosure of executive remunerations in three sections of the financial report: the overview of the remuneration policy, background statement, and implementation report. In spite of several comprehensive legislation’s corporate governance reforms, South Africa has been affected by major corporate governance failures in recent years. The collapse of corporations such as Macmed, Regal Treasury Bank, and Leisurenet are particularly significant (Sara, 2004). In an effort to reform and address peculiar corporate governance problems in South Africa, Armstrong et al. (2005) recommend that the following issues need to be resolved: intentional regulatory and bureaucratic strangling of small- and medium-scale business enterprises, addressing the problem of a weak, incompetent, and ineffective board structure, and also the issue of independence of board.

Research on Corporate Governance Disclosure

Corporate governance disclosure practices do not and cannot develop in a vacuum. Adhikari and Tondkar (1992) maintain that the levels of corporate governance disclosure tend to reflect the underlying institutional and environmental influences that affect managers and business firms in different countries. There are a variety of environmental factors that influence disclosure practices by companies, they have been identified (Radebaugh & Gray, 1993), and these factors include regulatory framework, capital markets, economy, enforcement mechanisms, and culture (Cooke & Wallace, 1990; Haniffa & Cooke, 2002). Most research papers on corporate governance disclosure has focused on disclosure issues of developing countries and have been researched from an agency theory perspective (e.g., Bushman & Smith, 2001; Healy et al., 1999; Healy & Palepu, 2001; Hermanson, 2000). Again, agency theory perspective has used transparency as a tool and mechanism for aligning the interest shareholders and management. The influence of corporate governance on disclosure has been examined at the level of country (Bushman et al., 2004; Francis et al., 2003) and also at the level of the firm (Beekes & Brown, 2006; E. C. M. Cheng & Courtenay, 2006). The extant research predicts that the governance variables likely to influence corporate governance disclosure can be classified into two categories: external governance mechanism in the form of political institutions, legal system, and freedom of the press for the country-level studies (Aguilera, Filatotchev, Gospel, & Jackson, 2008; Claessens, 2006; La Porta et al., 2002); and internal governance mechanisms that involve regulatory oversight, ownership concentration, share ownership by directors and managers, organizational structure of the corporation, and costs of voluntary corporate governance disclosure (Bushman et al., 2004; E. C. M. Cheng & Courtenay, 2006).

In developing countries, research on corporate governance disclosure are few and have focused on some of the following issues: overall levels of disclosure using disclosure index extracted from corporate governance literature, levels of compliance with international standards and domestic regulation, and institutional factors that hinder, constrain, and hamper corporate governance disclosure (Mensah, 2002; Samaha & Dahawy, 2010; Tsamenyi et al., 2007). In general, the research on corporate governance disclosure for many developing countries reveals a low or minimal level of disclosure (Agyei-Mensah, 2012; Barako, 2007; Samaha et al., 2012; De Zoysa & Rudkin, 2010).

Samaha et al. (2012) assess corporate governance disclosure of Egyptian firms listed on the Egyptian Stock Exchange (ESA), and they find that the level of corporate governance disclosure by Egyptian firms to be minimal; however, they also find that levels of disclosure of corporate governance are high for items that are considered mandatory under the Egyptian Accounting Standard. They conclude that the levels of corporate governance disclosure are lower for companies with duality position, and levels of corporate governance disclosure increase with the number of independent directors on the board. Agyei-Mensah (2012) investigates the extent to which Ghanaian firms comply with International Accounting Standards and also with the levels of corporate governance disclosure. The findings of the research reveal that most of the firms listed in the Ghana Stock Exchange did not overwhelmingly comply with International Accounting Standards disclosure requirements.

The pioneering research on corporate governance disclosure in Nigeria was done by Wallace (1988). His findings reveal that most of the companies in the study had a high level of corporate governance disclosure with respect to balance sheet, valuation method, and historical items. However, the companies did not adequately comply with the disclosure requirements and also the levels of corporate governance disclosure were poor, an estimated 43.11%. A similar study on corporate governance disclosure in South Africa was done by Fire and Meth (1986), who did a comparative analysis of corporate governance disclosure in South Africa and the United Kingdom. For South Africa, the study revealed low levels of disclosure for listed South African firms, and this was found to be common with other studies done on corporate governance disclosure in developing countries. Although the findings are not encouraging, they are consistent with Street and Gray (2001), Barako (2007), and Dahawy (2009) who find similar results with companies in other developing countries.

Characteristics of the Banking Sector in Nigeria and South Africa

Prior to the banking consolidation reforms in 2004, there were a total of 89 banks in Nigeria with a total of 3,200 deposit money banks (DMBs), and total employment in the sector has gone up from about 55,000 before reforms to over 77,519 currently (Gunu, 2009). The banking consolidation exercise by the CBN demanded that all deposit banks increase their minimum capital base from US$15 million to US$200 million by December 2005. Banks that failed to meet these new requirements were expected to merge for failing to do so, and those who failed to meet the new minimum capital base requirements would have their licenses revoked. In actual fact, these banking reforms were constructed to prevent the emergence of a banking crisis that could result from inherently weak banks characterized by persistent undercapitalization, high levels of nonperforming loans, illiquidity, insolvency, and poor corporate governance practices (Uchendu, 2005).

As of December 2013, the Nigerian Banking Industry comprised of 20 domestic banks and four foreign banks. The six Tier 1 banks (Zenith Bank, United Bank for Africa, Access Bank, First Bank, Equatorial Trust Bank, and Guaranty Trust Bank) accounted for 70% of the industry’s total assets of $136 billion as at December 2012. The other banks (18 in number) held less than 35% of total assets. For that reason, it should not come as a surprise that research on the Nigerian banking industry focuses on the five leading banks. According to CBN, Nigerian banks operate through an extensive network that includes over 5,585 DMBs and close to 12,755 automated banking machines (ABMs) across the country. In total, these financial institutions have over 136 billion dollars in assets, which represent a 300.5% increase in assets within 7 years of the banking consolidation (Umar & Olatunde, 2007).

In comparison, South African banks appear to have a better developed and more robust banking infrastructure than Nigerian Banks. They have a large sophisticated financial structure and a highly competitive banking industry which is dominated by both local and foreign banks. The total financial sector asset is an estimated 298% of GDP and exceeds those of most developing economies. Commercial banks assets alone are an estimated 112% of GDP, while the insurance-sector gross assets are 67% of GDP. The South African Reserve Bank (SARB) maintains that total banking sector assets recorded, on average, an annual growth rate of 7.2% during a 3-year period (2011-2014), reaching US$362 billion by December of 2014. On the whole, Southern African banks are well capitalized and, more often than not, have lower nonperforming loan ratios in comparison with the other developing countries.

In South Africa, there are 31 registered banks which comprise of 17 South African Banks, 14 foreign banks, and three mutual banks. Also, 41 international banks have authorized representative offices in South Africa; however, these representative offices do not collect financial deposits. Five major commercial banks continue to dominate the South African banking industry: the Amalgamated Bank of South Africa (ABSA), Nedbank, FirstRand Bank, Investec, and Standard Bank group—These banks account for an estimated 85% of total assets and have significant international presence. According to the SARBs, South African banks function through sophisticated and intricate networks that consist of 5,144 DMBs and close to 27,953 ABMs throughout the country.

Method

In constructing a disclosure index, numerous studies and approaches have been developed; this is done with the purpose of ensuring that a scoring scheme can be designed that will serve as a useful guideline for assessing and determining the disclosure levels of annual reports (Ceft, 1961; Cooke, 1989; Marston & Shrives, 1991). In business and accounting research, there are two known methods of designing a disclosure index: weighted disclosure index (Botosan, 1997; Buzby, 1974; Eng, Hong, & Ho, 2001) and unweighted disclosure index (Akhtaruddin, 2005; Archambault & Archambault, 2003; Raffournier, 1995). Both have been used in various accounting and business research papers in measuring the degree of disclosure in annual reports. Both techniques used in measuring disclosure in annual reports are not without their flaws; the unweighted disclosure index, for example, has been criticized for making the basic assumption that all items in the annual reports are equally important to the information users. The use of a weighted disclosure index has also been criticized because of the possibility of introducing a bias toward specific information users. However, the use of the unweighted disclosure index technique addresses the issue of subjectivity that arises in assigning of different weights to different items when user preference of annual reports remain unknown (Adrem, 1999; S. J. Gray, Meek, & Roberts, 1995). As a result of the critique against the use of weighted scoring technique, unweighted disclosure technique has become the norm that is applied in conducting research for this type of studies (Arvidsson, 2003). In his considered opinion, Wallace (1988) maintains that all disclosed items should be given equal consideration and that they should be of equal importance to the average users (Ahmed & Courtis, 1999). In this research, therefore, voluntary corporate governance disclosure in annual reports for five Nigerian and five South African banks for the year 2013 was considered and scored on a dichotomous basis. A score of 1 is assigned to a company’s disclosure of an item and 0 for nondisclosure of an item. For all of the annual reports selected for this research, to calculate the disclosure score, the number of items that have been disclosed in the annual report was divided by the total number of items relevant to the particular bank, which the report covers.

The total disclosure score for each firm is

where di is 1 if an item is disclosed and 0 if not; m is the number of voluntary items disclosed in the annual reports (here m = 51).

The coding sheet on disclosure of corporate governance in Nigerian and South African banks, seen in its entirety in the appendix, has 51 elements. The first step that was taken was reviewing the extant literature on corporate governance disclosure research. A particular research paper was of immense significance (Maingot & Zeghal, 2008). A number of their suggested essential elements of disclosure have been adapted and integrated into the coding sheet. The second step was the use of supplementary points of interest that were revealed when examining the 2013 annual reports of the five largest banks in Nigeria (United Bank for Africa, Guaranty Trust Bank, Zenith Bank, First Bank of Nigeria [FBN], Access Bank) and five largest banks in South Africa (FirstRand, African Bank, Nedbank, Capitec Bank, and Standard Bank). The coding guideline and instruction is as follows: A positive score of 1 is given to any bank when it discloses the statement in question; if it fails to disclose, the bank is given a score of 0.

In collecting the data for this research, a methodological approach was used in selecting the Nigerian and South African banks under the study. To make the list, the Nigerian and South African banks had to rank among the top 50 banks in Africa. Second, the banks in consideration had to have their annual reports available on their Internet websites; banks in Nigeria and South Africa which had no Internet presence were not considered. Having done this, the following banks in Nigeria emerged for consideration: First Bank, United Bank for Africa, Guarantee Trust Bank, and Access Bank. For South Africa, the following banks made the list: African Bank, FirstRand, Standard Bank, Nedbank, and Capitec Bank. In analysis of the annual report, the corporate governance disclosure index was used as a guideline. The index served as a useful guide in deciding what issues in corporate governance disclosure had to be examined and what had to be ignored.

It is important to state that the Internet has significantly enhanced data collection in developing countries and has made it convenient for researchers to collect data from the confines of their own offices; they do not have to travel long distances and spend outrageous amounts of money and time in different cities. It is essential that the term corporate governance voluntary disclosure should be defined. In this research, corporate governance voluntary disclosure has been defined as the prudent and discretionary release of financial as well as nonfinancial information through annual reports, that is, information that is considered over and above the mandatory requirements with regard to Nigerian and South African company laws, regulatory requirements, and professional accounting standards.

Discussion of Findings

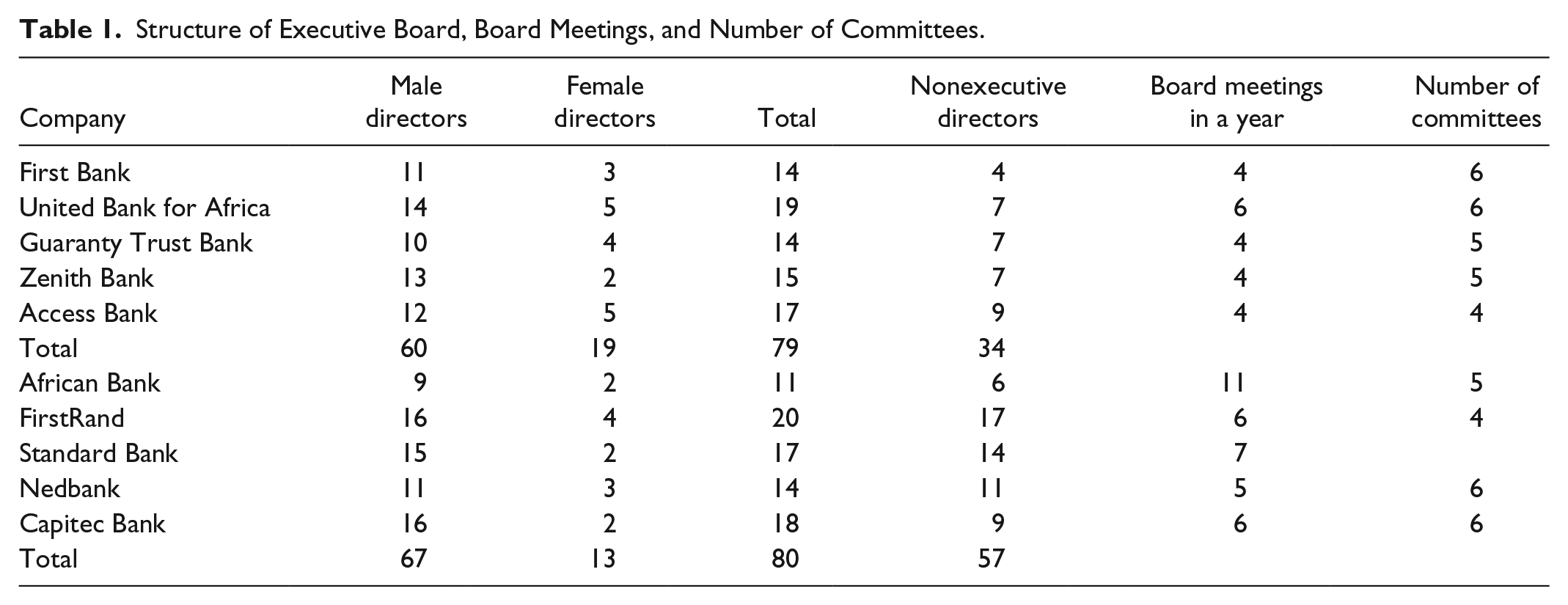

In Table 1, the descriptive statistics indicates that South African and Nigerian banks both have similar unitary board structure that consists of a mix of executive and nonexecutive directors. The United Nations (UN; 2006) guidance on good corporate governance disclosure recommends specifically that the composition of the board regarding the balance of executive and nonexecutive directors should be disclosed: The composition of the board should be disclosed, in particular the balance of executives and nonexecutive directors, and whether any of the nonexecutives have any affiliations (direct or indirect) with the company. Table 1 also shows that the mix of executive directors for South African and Nigerian banks are both male dominated with fewer women holding executive positions in both banks. In Nigerian Banks, women account for 24.05% of the total board of directors, while in South African banks women account for only 16.25% of the total board of directors, a much lower percentage when compared with that of Nigerian Banks. With regard to the number of committees, all banks in South Africa and Nigeria have at least three committees. The UN (2006) categorically states that the establishing of board committee is intended to “facilitate fulfillment of certain of the board’s functions and address some potential conflict of interests” (p. 15). The King II Report (2002) report and the Nigerian Code on Corporate Governance are both very clear on committee representation and state that for effective governance of the company’s affairs, all companies should have a minimum of two committees which should include remuneration committee and audit committee.

Structure of Executive Board, Board Meetings, and Number of Committees.

General Corporate Governance Disclosure of the Banks

A summary of corporate governance disclosure for Nigerian and South African banks can be seen in Tables 2 and 3. The coding sheet was divided into six different sections: (a) The board structure and directors profile are basically about information that relates to the board of directors, for example, the number of directors, qualifications of the directors, number of years on board, and biography of the directors; (b) financial information and corporate information deal with the following issues, for example, summary of financial data for at least a minimum of 2 years, share price information, corporate mission statement, and statement disclosure relating to competitive position in the industry; (c) board independence and board committee relate to, among other things, disclosure involving separating the roles of the chairman and chief executive officer (CEO), independence of the board committees, and duties of the various committees; (d) corporate social responsibility disclosure is specific to corporate governance disclosure on community involvement/participation, statement on corporate social responsibility, and environmental projects/activities taken; (e) information on website section deals with the disclosure of corporate governance information on the Internet, for example, availability of online annual reports, online proxy circulars and notices of annual meeting, and having a corporate governance webpage; and (f) remuneration of board section is about issues relating to remuneration of the executives, number of shares owned by directors, and loans to directors.

Summary of Corporate Governance Disclosure for Nigerian and South African Banks.

Note. UBA = United Bank for Africa; GTB = Guaranty Trust Bank; ZEN = Zenith Bank; FBN = First Bank of Nigeria; ACS = Access Bank; RAND = FirstRand; AFN = African Bank; NED = Nedbank; CAP = Capitec Bank; STD = Standard Bank.

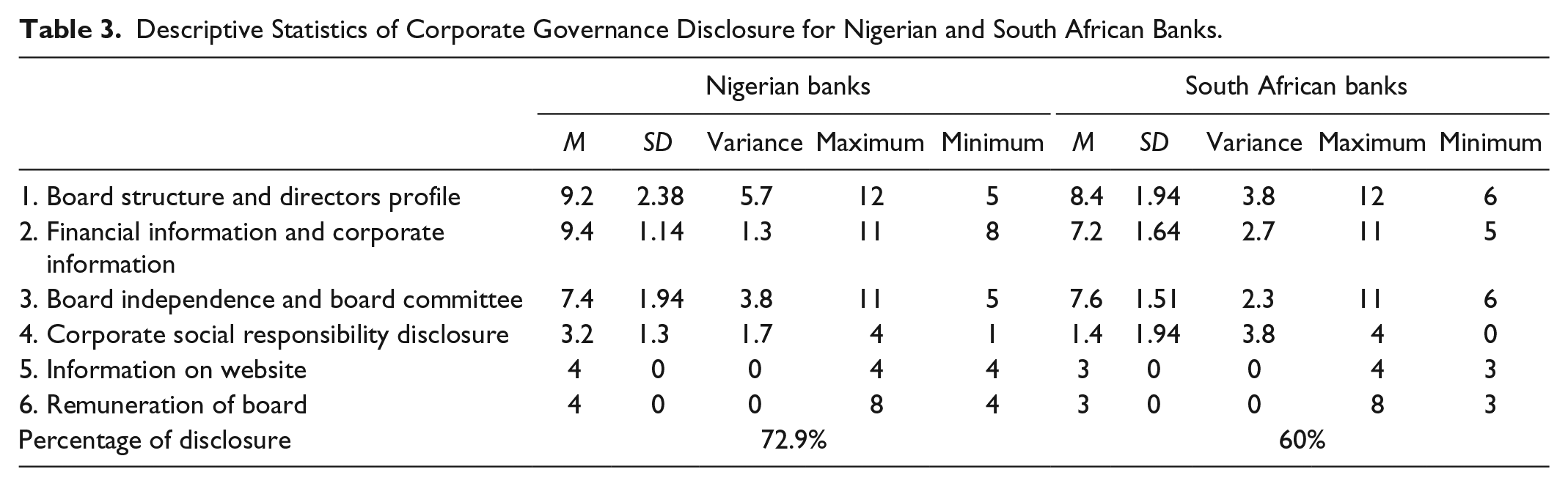

Descriptive Statistics of Corporate Governance Disclosure for Nigerian and South African Banks.

A cursory glance at the summary of corporate governance disclosure for Nigerian and South African banks reveals that Nigerian banks, on average, tend to disclose more corporate governance information than South African banks. In general, the Nigerian banks’ annual reports tend to be more voluminous than the annual reports from their South African counterparts. Some of the Nigerian banks’ annual reports were more than 300 pages, while those of South Africa were between 180 to 260 pages. Surprisingly, one would have expected that South African banks would have better corporate governance disclosure scores than that of Nigerian Banks; South African banks tend to be multinational banks with a global spread, are more sophisticated, and have vast branch networks across the globe when compared with the Nigerian banks which are all indigenous banks. South African banks tend to disclose less information in three core areas: board structure and director profile, financial and corporate information, and corporate social responsibility disclosure. A genuine reason for the difference in the levels of disclosure between Nigerian banks and South African banks is as a result of mandatory corporate governance disclosure requirements demanded of Nigerian banks by the regulatory authorities. In addition, we find in the overall level of disclosure, there is a 4% margin between FBN and Standard Bank, but the margin increases significantly between FBN and African Bank at 13%, and FBN and Capitec Bank at 17%. However, the average disclosure score for Nigerian banks and South African banks is quite high (72.9% and 60%) when compared with developing countries such as Brazil, 32.65% (Patel, Balic, & Bwakira, 2002); Bangladesh, 43.5% (Akhtaruddin, 2005); and Ghana, 52% (Tsamenyi et al., 2007). A plausible explanation could be that corporate governance practices in developing countries have had some marginal improvements over the years, as most of the studies in question are over a decade old.

Another explanation could be the small sample size of the study in question which examined Nigerian and South African banks that were regarded as the best ranking banks, and as such this may not reflect the disclosure practices of all banks in Nigeria and South Africa. If a larger sample size is considered to include more banks, the results may be different. One of the noticeable trends in corporate governance in developing countries is the development of regulations and codes of corporate governance targeted at improving corporate governance practices and policies (Bhasin, 2013; Samaha et al., 2012), which is in line with global best practice. Still, there is room for improvement: The overall disclosure score for Nigerian and South African banks is 72.9% and 62.7%, respectively.

It is possible for developing countries to improve their levels of corporate governance disclosure over time, and while the average percentage score for corporate governance disclosure for Nigerian and South African banks appears high, this is not the case when individual bank corporate governance disclosure scores are examined, for instance, a Nigerian bank, Zenith’s overall corporate governance disclosure scores 58.8%, while a South African bank, Rand’s overall corporate governance scores 47%. This simply implies that while, on average, corporate governance scores for Nigerian and South African banks appear high, individual bank scores may differ. In reality, that means some banks would have better corporate governance scores than others.

Board Structure and Directors Profile

The King and the CBN corporate governance code recommend the separation of the role of the chairman and the CEO. Both roles are considered too powerful to be given to a lone individual to execute. This is considered good corporate governance practice, as outlined in the CBN’s Corporate Governance Code and the King report, and all Nigerian and South African banks in the study have complied with this guideline requiring them to separate the roles of the chairman and the CEO. In addition to regulatory requirements, the Nigerian and South African banks have disclosed more information in terms of qualifications of directors, photographs of directors, and the number of years they have served on the board.

However, there is evidence to suggest that Nigerian banks tend to disclose a bit more information about the board structure and directors profile than their South African counterparts. With regard to disclosure on board structure and director profile, Nigerian banks score 92% while South African banks score 86%. The slight differences in scores were as a result of the following in Table 4: Only one South African bank disclosed information regarding duties of the directors of the board, and two of the banks had photographs of members of the board.

Board Structure and Directors Profile.

Financial and Corporate Information

The findings of the research reveal that Nigerian and South African banks follow international and domestic guidelines in disclosing their financial and corporate information as well as the operating results. The UN, the King III report, and the CBN Corporate Governance Code all request that corporate entities disclose their financial and corporate information so that shareholders and stakeholders can understand the nature and present state of affairs of the business.

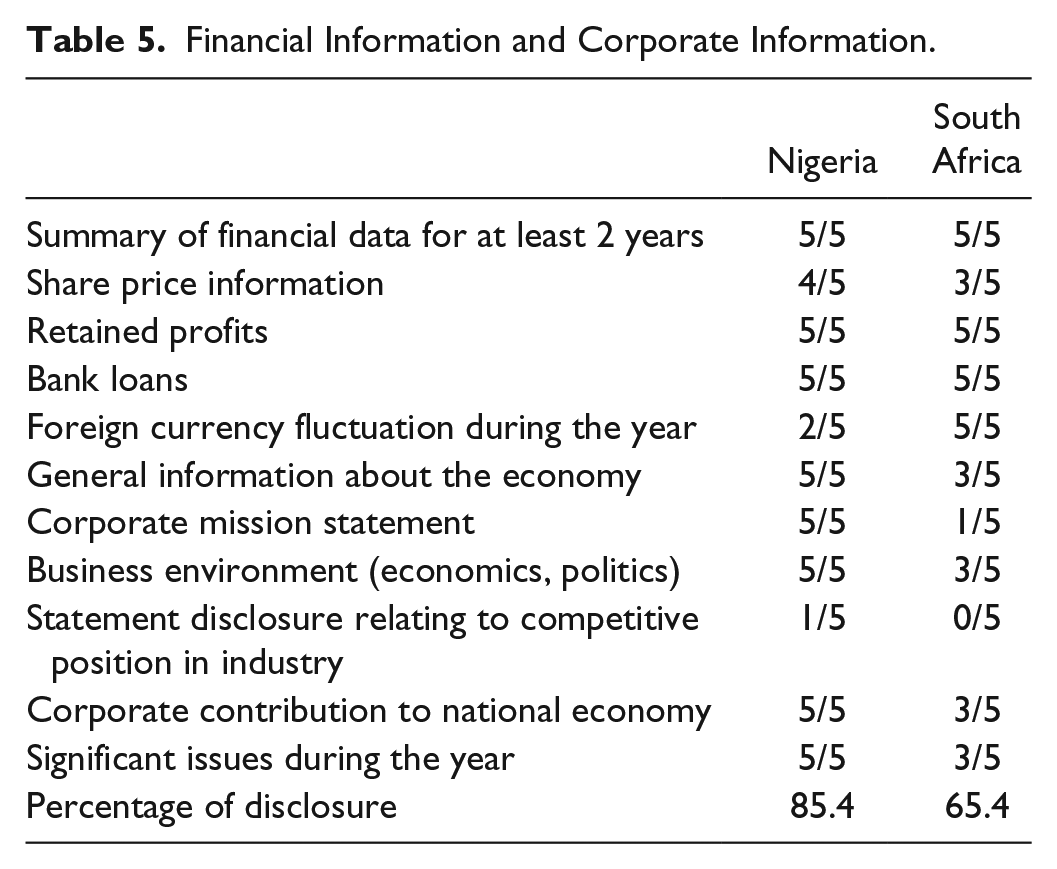

In Table 5, the financial and corporate information disclosure reveals that Nigerian banks scored 85.4% while South African banks scored 65.4%, a 20% point difference. In the areas of summary of financial data, disclosure of retained profits, and bank loans, Nigerian and South African banks tend to be at par, in terms of the levels of disclosure. However, Nigerian banks tend to disclose a bit more information in the areas of general information about the economy, corporate mission statement, business environment, and contribution to national economy.

Financial Information and Corporate Information.

Corporate Social Responsibility Disclosure

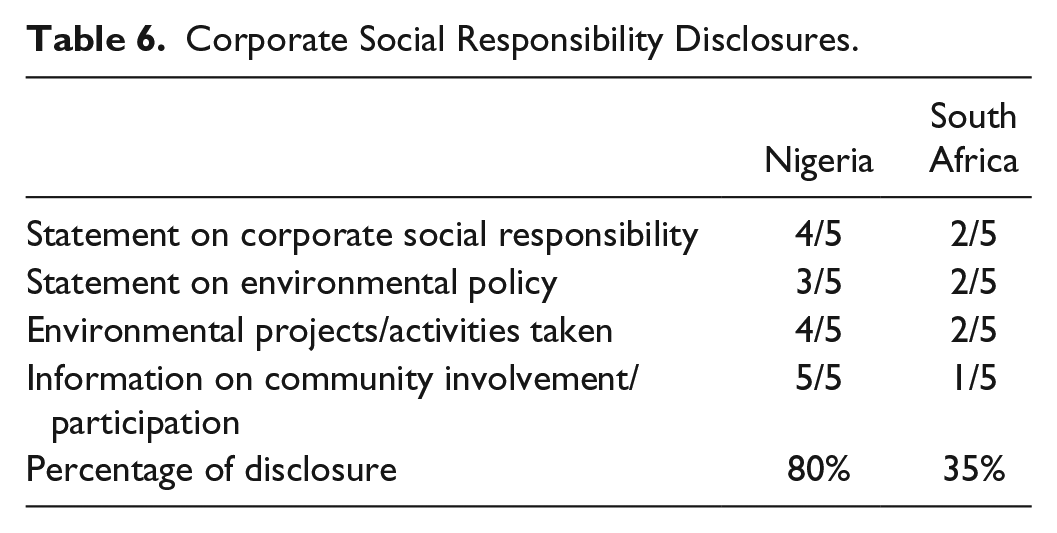

The King report encourages South African companies to report on corporate social responsibility, but this is not the case in Nigeria as none of the regulatory agencies require that companies should report on corporate social responsibility. However, there is an awareness of the importance of integrating corporate social responsibility disclosure as part of the banks’ environmental, social, and ethical risk strategies (Carroll & Shabana, 2010; Kotler & Lee, 2006; Porter & Kramer:, 2002; Tencati, Perrini, & Pogutz, 2004; Weber, 2008). Both Nigerian and South African banks seem to recognize that nonfinancial risks can pose significant threats to their business activities and so have decided to design effective strategies to tackle nonfinancial risks that may threaten the continuity of the business. South African banks tend to be more systematic in the reporting of corporate social responsibility; they abide by regulations of the King report and also apply international standards such as the global reporting initiative in their corporate governance voluntary disclosure. Sadly, with regard to corporate social responsibility disclosure for Nigerian banks, disclosure appears to be a compiling and collation of information at the end of the year. Certainly, this should not be so; nonfinancial disclosure should be linked to the overall business strategy of the organization. Furthermore, in corporate social responsibility disclosure, many of the Nigerian banks in the study have not taken the time to adopt any international guideline in their reporting. Consequently, there is no uniformity in the way the corporate governance voluntary disclosure is done (see Table 6).

Corporate Social Responsibility Disclosures.

Board Independence and Board Committee

Board independence is an integral element of corporate governance practices. Research maintains that an independent board enhances corporate governance practices as boards of directors who do not have pecuniary and material interests invested in the corporation tend to give more independent valuations and are less swayed to protect managerial interests to the detriment of shareholders. The UN, the King III report, and the CBN Corporate Governance Code all stress the importance of an independent board of directors. In disclosure relating to board independence and board committee, Nigerian banks and South African banks tend to have similar levels of disclosure as the Nigerian banks’ score of 74% is 2% lower than South African banks’ score of 76%.

Still, when a meticulous examination of board independence and board committee in Table 7 is undertaken, the findings reveal that in relation to sections dealing with outlining board independence and determining independence of board remuneration, Nigerian banks perform worse than their South African banks’ counterparts. In Table 8, corporate governance disclosure relating to remuneration of board of Nigerian and South African banks, the tables reveal low levels of disclosure for Nigerian and South African banks on both issues. In fact, corporate governance disclosure on remuneration of the board of directors appears to be the least disclosed for Nigerian and South African banks, with Nigerian banks scoring 30%, that is 20% lower than the South African banks’ score of 50%. For Nigerian and South African banks, none of the five banks disclosed any issues relating to loans to CEO, explanation of CEO stock requirements, and loans to directors. On the whole, South African banks disclose more information relating to remuneration of board than Nigerian Banks.

Board Independence and Board Committee.

Remuneration of Board.

Corporate Governance Voluntary Disclosure of Nigerian and South African Banks

A more informative sign or indicator of a bank’s corporate governance disclosure is the level of voluntary corporate governance disclosure (Mensah, 2002; Oluwagbemiga, 2014; Samaha & Dahawy, 2010; Tsamenyi et al., 2007). Voluntary corporate governance disclosure is simply explained as information that banks provide that they are not obligated to disclose or divulge under any form of regulation. In determining which items of the coding sheet were mandatory and which items were voluntary, a review of the disclosure requirements of the Nigerian Stock Exchange, Corporate Governance Code for Nigerian Banks, Corporate Matters Allied Act, King Report, South African Stock Exchange, United Nations Corporate Governance Code, and Organization for Economic Co-Operation and Development (OECD) Governance Code was taken.

Out of 51 items that were listed on the coding sheet, 20 of the items were found to be completely voluntary. The list of these voluntary corporate governance items with the frequency of their governance disclosure is displayed in Table 9. In comparing the levels of disclosure, a comparative analysis was done between Nigerian and South African banks. In general, the results show that Nigerian and South African banks have poor levels of voluntary corporate governance disclosure, with South African banks faring a bit better with a score of 38.9% while Nigerian banks scored 28.4%. More South African banks had disclosure of online information, online annual reports, number of years on board, and online links to corporate governance webpages than their Nigerian banks’ counterparts. However, there are some issues in voluntary corporate governance disclosure where Nigerian and South African banks record poor levels of voluntary disclosure and they include residence of directors, explanation of CEO stock requirements, past committee experience, and number of directors who can sit on and outside the board.

Governance Information Disclosed Voluntarily.

Summary and Conclusion

The findings of this research are inconsistent with previous corporate governance research on Nigeria and South Africa (Fire & Meth, 1986; Wallace, 1988). Previous research had found low levels of disclosure for South African and Nigerian companies listed on the stock exchange. One sensible explanation would be that the previous research papers are more than two decades old; a lot of significant changes have happened over the period that would have enhanced disclosure practices such as the introduction of corporate governance codes intended to improve the levels of transparency and disclosure. The emergence of information communication technology and availability of Internet technology are responsible for enhancing corporate governance disclosure as business organizations can place electronic copies of their annual reports online as well as other relevant corporate governance information not included in the annual report.

Furthermore, corporate governance disclosure in Nigerian and South African banks appears to be heading toward greater stakeholder inclusivity, again reflecting a deeper shift from the prevailing shareholder and agency theory framework and toward a stakeholder-oriented framework. Here, corporate governance disclosure is targeted at disclosing information to a wide variety of users of corporate annual reports as well as internal and external stakeholders. Nevertheless, with regard to disclosure of nonfinancial information, by which we mean disclosure relating to social, environmental, and ethical reporting or corporate social responsibility as the names imply, it appears there is significant room for improvement in disclosure practices. As it stands, social, environmental, and ethical reporting or corporate social responsibility appears to be a collation of information at the end of the year. Certainly, this should not be the case. Nonfinancial information disclosure should be linked to the overall business strategy of the organization. Many Nigerian banks in the study failed to link nonfinancial disclosure to their overall business strategy. Nonfinancial disclosure appeared to be done for the sake of disclosure, without any thought of how to align nonfinancial disclosure with their business strategy. As it stands, most of the banks in question have not taken the time to adopt any international standard or guidelines in the disclosure of nonfinancial information. Consequently, directors and managers who are saddled with the responsibility of corporate governance disclosure in developing countries need to think carefully about corporate governance disclosure. Corporate governance disclosure should not be taken for granted nor should it be done in a haphazard manner. A lot of thought and meticulous deliberation should go into deciding what should be disclosed and also aligning what is disclosed with the overall business strategy of the firm. Corporate governance disclosure matters, and better disclosure practices have immense benefits for the firm such as attracting investors and enhancing firms’ capacity to attract loans at lower interest rates.

While this research has examined corporate governance disclosure in Nigerian and South African banks, there is still the need to conduct further research on corporate governance in developing countries. It would be interesting to have a longitudinal research on corporate governance in developing countries like Nigeria and South Africa to examine how corporate governance disclosure has evolved. Another direction that necessitates further research would be the examination of corporate governance disclosure in other industries, as the banking sector represents just one among several. This would help ascertain whether the level of corporate governance disclosure in the banks is similar to that of other industries or if it is different, and if different, what those differences may be.

Footnotes

Appendix

Corporate Governance Disclosure Coding Sheet.

| Coding sheet | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bank name | UBA | GTB | ZEN | FBN | ACS | RAND | AFN | NED | CAP | STD |

| Information on website | ||||||||||

| 1. Online information | ||||||||||

| 2. Online proxy circular and notice of annual meeting | ||||||||||

| 3. Online annual report | ||||||||||

| 4. Online histogram of organization | ||||||||||

| 5. Online link to corporate governance webpage |

||||||||||

| Subtotal | ||||||||||

| Board | ||||||||||

| 7. Number of directors | ||||||||||

| 8. Duties of board of directors | ||||||||||

| 9. Number of meetings | ||||||||||

| 10. Chairman identified | ||||||||||

| 11. CEO identified | ||||||||||

| 12. Minimum qualifications of directors | ||||||||||

| Subtotal | ||||||||||

| Profile of director | ||||||||||

| 13. Name | ||||||||||

| 14. Residence | ||||||||||

| 15. Qualification and occupation | ||||||||||

| 16. Number of years on board | ||||||||||

| 17. Photos of members | ||||||||||

| 18. Biography of members | ||||||||||

| Subtotal | ||||||||||

| Remuneration of board | ||||||||||

| 19. CEO salary | ||||||||||

| 20. Number of shares owned by CEO | ||||||||||

| 21. Explanation of CEO stock requirement | ||||||||||

| 22. Loans to CEO | ||||||||||

| 23. Directors’ salary | ||||||||||

| 24. Number of shares owned by directors | ||||||||||

| 25. Explanation of directors’ stock requirements | ||||||||||

| 26. Loans to directors | ||||||||||

| Subtotal | ||||||||||

| Board independence | ||||||||||

| 27. Separate section outlining board independence | ||||||||||

| 28. Separation of the role of chairman and CEO | ||||||||||

| 29. Capable of determining independence of board remuneration review | ||||||||||

| 30. Capable of determining independence of audit committee | ||||||||||

| 31. Capable of determining independence of conduct review or risk committee | ||||||||||

| Subtotal | ||||||||||

| Financial information | ||||||||||

| 32. Summary of financial data for at least 2 years | ||||||||||

| 33. Share price information | ||||||||||

| 34. Retained profits | ||||||||||

| 35. Bank loans | ||||||||||

| 36. Foreign currency fluctuation during the year | ||||||||||

| Subtotal | ||||||||||

| Corporate information | ||||||||||

| 37. General information about the economy | ||||||||||

| 38. Corporate mission statement | ||||||||||

| 39. Business environment (economics, politics) | ||||||||||

| 40. Statement disclosure relating to competitive position in industry | ||||||||||

| 41. Corporate contribution to national economy | ||||||||||

| 42. Significant issues during the year | ||||||||||

| Subtotal | ||||||||||

| Committees | ||||||||||

| 43. Number of committees | ||||||||||

| 44. Duties of committees | ||||||||||

| 45. Number of meetings | ||||||||||

| 46. Number of members | ||||||||||

| 47. Identify chairmen | ||||||||||

| Subtotal | ||||||||||

| Corporate social responsibility disclosure | ||||||||||

| 48. Statement on corporate social responsibility | ||||||||||

| 49. Statement on environmental policy | ||||||||||

| 50. Environmental projects/activities taken | ||||||||||

| 51. Information on community involvement/participation | ||||||||||

| Subtotal | ||||||||||

| Total score | ||||||||||

| Percentage of disclosure |

Note. UBA = United Bank for Africa; GTB = Guaranty Trust Bank; ZEN = Zenith Bank; FBN = First Bank of Nigeria; ACS = Access Bank; RAND = FirstRand; AFN = African Bank; NED = Nedbank; CAP = Capitec Bank; STD = Standard Bank.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.