Abstract

Previous studies of mobile payment (m-payment) services have primarily focused on a single group of adopters. This study identifies the factors that influence an individual’s intention to use m-payment services and compares groups of current users (adopters) with potential users (non-adopters). A research model that reflects the behavioral intention to use m-payment services is developed and empirically tested using structural equation modeling on a data set consisting of 529 potential users and 256 current users of m-payment services in Thailand. The results show that the factors that influence current users’ intentions to use m-payment services are compatibility, subjective norms, perceived trust, and perceived cost. Subjective norms, compatibility, ease of use, and perceived risk influenced potential users’ intentions to use m-payment. Subjective norms and perceived risk had a stronger influence on potential users, while perceived cost had a stronger influence on current users, in terms of their intentions to use m-payment services. Discussions, limitations, and recommendations for future research are addressed.

Keywords

Introduction

Rapid innovations associated with handheld devices have significantly changed and improved the functionality of mobile phones, allowing people to use them for more than just the purpose of instantaneous communication. Of these innovations, mobile commerce (m-commerce) has emerged as a significant area for mobile phone use in the age of wireless technology. In particular, the use of mobile payments (m-payments) is becoming a key driver of m-commerce, as any purchase of goods or services using m-commerce channels requires a payment system. In other words, the prosperity of mobile commerce heavily relies on consumers’ acceptance of m-payments conducted via terminals such as mobile phones or tablets (Y. Yang, Liu, Li, & Yu, 2015). In addition, consumers would not be the only beneficiaries of the wider use of m-payment services. The success of m-payments is important because it can generate returns for individual companies that invest in its development and can improve a country’s overall financial services standards, as this mode of payment allows greater cost efficiency compared with a paper-based payment system (Bank of Thailand, 2015).

Despite these varied attempts by mobile operators, including the Bank of Thailand, to launch the latest m-payment services in Thailand, m-payment is still the least preferred payment method among Thai consumers when compared with card-based and Internet-based payments (Bank of Thailand, 2015; Tavilla, 2015). Although the Thai market includes a large consumer base with mobile phones, the adoption rate of m-payment services is still lower than expected. Notably, in 2015, the number of mobile phone subscriptions in Thailand was approximately 83 million, but only 8.5% of Thai mobile users were using m-payment services (Bank of Thailand, 2015; The Office of The National Broadcasting and Telecommunications Commission, 2015). Likewise, a survey conducted by the National Statistical Office Ministry of Information and Communication Technology (2015) revealed that approximately 5% of Thai mobile phone users had used their mobile phones to conduct a financial transaction. It is unclear why m-payment services have lagged behind the relatively high degree of mobile phone use in Thailand, given the significant advantages associated with m-payment services in terms of convenience and flexibility (Phonthanukitithaworn, Sellitto, & Fong, 2016).

Previous studies have drawn on the technology acceptance model (TAM) to examine individual intentions to adopt m-payment services (Arvidsson, 2014; Bamasak, 2011; Chandra, Srivastava, & Theng, 2010; L. Chen, 2008; Garrett, Rodermund, Anderson, Berkowitz, & Robb, 2014; Keramati, Taeb, Larijani, & Mojir, 2012; Lu, Yang, Chau, & Cao, 2011; Nguyen, Cao, Dang, & Nguyen, 2016; Phonthanukitithaworn, Sellitto, & Fong, 2015, 2016; Schierz, Schilke, & Wirtz, 2010; Shin, 2010; G. E. Tan, Ooi, Chong, & Hew, 2014; Yan et al., 2009; Y. Yang et al., 2015; Zhou, 2011, 2014). However, the findings of these studies tend to be reported from the perspective of a single group, such as potential m-payment users (Garrett et al., 2014; Keramati et al., 2012; Schierz et al., 2010; Shin, 2010), people who make online payments (Lu et al., 2011), Internet users (Liébana-Cabanillas, Sánchez-Fernández, & Muñoz-Leiva, 2014a, 2014b), mobile phone owners (Bamasak, 2011; L. Chen, 2008; Nguyen et at., 2016; Phonthanukitithaworn et al., 2016; G. E. Tan et al., 2014; Zhou, 2011, 2013), and specific m-payment users (Arvidsson, 2014; C. Kim, Mirusmonov, & Lee, 2010; Phonthanukitithaworn et al., 2015). Notably, such user groups have seldom been compared with one another. Moreover, studies that investigate both adopters (current users) and non-adopters (potential users) tend to be underreported in the literature (Dahlberg, Guo, & Ondrus, 2015; G. E. Tan et al., 2014). Hence, findings that focus on particular sets of adopters may not offer holistic insights into understanding the potential use of m-payment among non-adopters. Moreover, to understand patterns of m-payment adoption, the perceptions of both current and potential user groups must be considered. Clearly, these groups may perceive the usefulness of m-payment differently and adopt new payment technologies accordingly. In other words, the factors that influence the adoption of m-payment are expected to affect potential users and existing users differently. Previous studies that have compared current users with non-users of a newly introduced idea or innovation have revealed that the strength of the determinants’ influence can vary across groups (Vandenberg & Lance, 2000; Vandenberg & Scarpello, 1990).

Given the importance of establishing a holistic understanding of m-payment and its adoption patterns to determine how to stimulate the adoption of m-payment, this study poses two main questions. First, what factors influence an individual’s intention to adopt m-payment services? Second, which factors have significantly different effects on m-payment users compared with potential users? The first question focuses on comprehensively identifying factors that influence individuals’ intentions to adopt m-payment by considering a wide range of people. The second question is formulated to discover the difference in the factors that influence its adoption by comparing m-payment users and potential users. To answer these questions, we extended the TAM to the context of m-payment by incorporating the influencing constructs (compatibility, subjective norms [SNs], perceived risk [PR], perceived trust [PT], and perceived cost [PC]). The developed model was validated in Thailand, and the study sample contained both current users and potential users of m-payment services.

The remainder of this article proceeds as follows. The next section presents a relevant discussion of the theoretical framework concerning technology adoption and the hypotheses guiding the research. The article then describes the methods used to conduct the study. The data analysis results are described and followed by an extended discussion. The article concludes by discussing the theoretical and practical implications of the findings, the limitations of the study, and recommendations for further research.

Theoretical Background

Several models can be used to examine differences in the adoption of m-payment services. To date, information system acceptance research has been predominantly influenced by intention-based models that are rooted in cognitive psychology, including Ajzen and Fishbein’s (1980) theory of reasoned action (TRA), Ajzen’s (1991) theory of planned behavior (TPB), Davis’s (1989) TAM and its extensions, and the diffusion of innovations (DOI; Rogers, 2003).

Specifically, the TRA model suggests that a person’s actual behavior is determined by his or her behavioral intentions to perform a particular activity. Behavioral intentions are shaped and influenced by individuals’ attitudes and SNs, which are in turn shaped by their beliefs in relation to both their motivations and the evaluation of their beliefs. Because the TRA lacks constructs to emphasize specific aspects of a particular type of behavior, it was deemed unsatisfactory and was developed further into the TPB. The TPB adds an additional variable to the model, perceived behavioral control (PBC), to reflect the parameter of control beliefs that relate to one’s abilities, situation, and resources (Ajzen, 1991). Despite the important role of PBC in the TPB, it has become a problematic concept as researchers have reported inconsistent results regarding the measurement of PBC (Taylor & Todd, 1995b) and the use of PBC in predicting behavioral intentions and actual behavior (Bagozzi & Kimmel, 1995; Terry & O’Leary, 1995).

Drawing on the TRA and the TPB, Davis (1989) proposed the TAM, which aims to examine the mediating role of perceived usefulness (PU) and perceived ease of use (PEOU) and the relationships between external variables and the probability of information systems adoption. For a long time, the TAM proved to be a useful theoretical model that helped understand and explain usage behavior in information systems implementation (Legris, Ingham, & Collerette, 2003). However, some researchers found the TAM to be a parsimonious model because it includes only two individual beliefs. In response to this criticism, researchers recommend adapting the TAM by adding components that better predict an individual’s technology acceptance. For instance, Venkatesh and Davis (2000) introduced TAM2 by incorporating social and organizational variables, such as SNs, image, job relevance, output quality, and result demonstrability, into the original TAM model.

On the contrary, the DOI explains how innovations are adopted over time by examining the innovation-decision processes that influence innovation adoption among members of a social system (Rogers, 2003). The innovation-decision process consists of five stages—knowledge, persuasion, decision, implementation, and confirmation. Rogers (2003) claimed that potential adopters evaluate an innovation based on their perceptions and that they will decide to accept an innovation if they perceive that it has the attributes of relative advantage, complexity, compatibility, trialability, and observability. Many researchers have found that the DOI theory offers a powerful paradigm for conceptualizing an innovation’s development and acceptance. However, the DOI theory has been criticized because it lacks explanations for adoption behavior (Thong, Yap, & Raman, 1996) and the effects of adopters’ demographic characteristics on innovation adoption (Hartwick & Barki, 1994; Mathieson & Keil, 1998).

Each of the models discussed above has strengths and weaknesses. However, comparisons between innovation adoption theories show that the TAM appears to have advantages over the TPB and the DOI because it is a simpler model that is easier to apply and more efficient in predicting and explaining an individual’s adoption intentions and actual behavior. Many studies that investigate m-payment service adoption have selected the TAM over other theories because it allows a causal validation of variables (M. Chen & Teng, 2013; J. B. Kim, 2012; Phonthanukitithaworn et al., 2015, 2016), an exploration of the adoption of m-payment services (Goeke & Pousttchi, 2010; Keramati et al., 2012; C. Kim et al., 2010; Koenig-Lewis, Palmer, & Moll, 2010; Nguyen et al., 2016; Schierz et al., 2010; Shin, 2010; Yan et al., 2009; Zhou, 2011), and a comparison through multi-group analysis (C. Kim et al., 2010; Liébana-Cabanillas et al., 2014a, 2014b; Lu et al., 2011; G. E. Tan et al., 2014). Therefore, based on the recommendations of past studies and the inherent superiority of the TAM, this study modified the TAM by maintaining the major constructs of PU, PEOU, and behavioral intentions while extending the model with other relevant constructs.

According to a review of previous studies on m-payment service adoption, a number of possible constructs can be used in the conceptualization of the research framework. However, in most cases, the constructs are not aligned with the cultural characteristics of the country in which the studies are conducted, which can potentially affect the outcomes. According to Chau, Cole, Massey, Montoya-Weiss, and O’Keefe (2002), and Mallat and Tuunainen (2008), cultural differences and market conditions influence people’s beliefs and play an important role in the way that people adopt new technologies. For instance, people from Japan and Korea, who are often recognized as global leaders and users of digital technology and electronic payment services, may find technology to be more useful and easier to use than people from countries where technology is relatively underdeveloped (Zhang & Dodgson, 2007). As a result, this study employed the constructs of compatibility (COM), SNs, PR, PT, and PC as extended constructs, as they have been empirically tested in the Thai setting and have been suggested as reliable tools for measuring perceptions regarding the adoption of m-payment services in Thailand (Jaruwachirathanakul & Fink, 2005; Phonthanukitithaworn et al., 2015; Prompattanapakdee, 2009).

Research Model and Hypotheses

Drawing from the literature, we propose a conceptual research model (Figure 1) with an appropriate set of hypotheses that are aligned with individuals’ intentions to use m-payment services. The model consists of independent variables (PU, PEOU, SN, COM, PR, PT, and PC) and dependent variables (behavioral intentions to adopt m-payment services).

Conceptual research model used to investigate m-payment services.

PU

PU was originally proposed to indicate the degree to which an individual believed that using a particular idea, technology, or innovation would improve his or her job task and performance (Davis, 1989). In the context of m-payment service adoption, PU reflects the use of a service that is perceived to be useful when conducting payment transactions. For instance, a consumer may feel that m-payment services will allow him or her to pay via his or her mobile phone, negating the inconvenience of carrying cash for payments. Recent empirical work by Liébana-Cabanillas et al. (2014a) identified PU as a strong predictor of the behavioral intention to use m-payment services. Moreover, Taylor and Todd (1995a) suggested that PU was a strong predictor in delineating the differences between adopters and non-adopters. Notably, PU was an important factor for non-adopters, whereas people who had already adopted the technology were less concerned about PU. Hence, the PU construct is explored in this study through the following hypotheses:

PEOU

PEOU is the extent to which using a new idea, technology, or innovation is expected to be relatively free of physical, emotional, or psychological efforts for prospective adopters—thus enabling them to improve their job-task outcomes. PEOU is a major concern for most consumers when considering m-payment services because of the numerous stages associated with the payment process, which may be challenging for prospective adopters. PEOU has been identified as having a direct effect on the behavioral intention to adopt m-payment services or as having an indirect impact by mediating the PU of m-payment services (Peng, Xiong, & Yang, 2012; G. E. Tan et al., 2014; Zarmpou, Saprikis, Markos, & Vlachopoulou, 2012). Moreover, the influence of PEOU may vary depending on an individual’s experience. Inexperienced users may initially focus on ease of use, while experienced users have presumably overcome concerns regarding ease of use and may instead focus their attention on PU (Taylor & Todd, 1995a). Hence, in this study, the PEOU construct is investigated using the following hypotheses:

Compatibility

In the context of m-payment services, COM is aligned with a user’s intrinsic characteristics—such characteristics generally reflect an individual’s social image and requirements, personal values, lifestyle, beliefs, and experiences (Rogers, 2003). COM has been identified as an important factor with regard to the adoption of m-payment services (L. Chen, 2008; Mallat & Tuunainen, 2008; Phonthanukitithaworn et al., 2015, 2016; Schierz et al., 2010; Wu & Wang, 2005). For instance, L. Chen (2008) proposed that m-payment services are likely to be highly desirable when people find that using such services is compatible with their lifestyle and social image. Furthermore, the COM construct influences both potential and existing m-payment users’ intentions to adopt m-payment services (S. Yang, Lu, Gupta, Cao, & Zhang, 2012). Hence, in this study, the COM construct is explored as follows:

SN

An SN can be viewed as the degree to which an individual is influenced by the opinions of others who may be important to him or her when considering a particular activity (Fishbein & Ajzen, 1975). An SN is an important factor early in the uptake of m-payment services, particularly when people may not be knowledgeable about the practicalities of the service (S. Yang et al., 2012). Users may experience feelings of uncertainty regarding the consequences of using m-payment services and may, in turn, opt to consult other users regarding their opinions and experiences through social networks (Liébana-Cabanillas et al., 2014b). Furthermore, the effect of SN on behavioral intentions is anticipated to be stronger for users who have no experience, as they are more likely to rely on others’ reactions to inform their intentions. SN can be viewed as a measure of the influence of important peers and/or other social groups, including friends, parents, and colleagues, on a person’s intention to adopt m-payment services. Hence, this study proposes the following hypotheses pertaining to the SN construct:

Perceived Risk

PR is defined as the degree of uncertainty among consumers regarding the possible negative consequences of using new technology, which may dissuade its adoption (Bauer, 1967). Featherman and Pavlou (2003) referred to risk as an expectation of loss, and PR will be higher when the expectation of loss is higher. This implies that an increasing level of uncertainty will elevate the level of PR toward m-payment services. Prior studies have shown that PR can directly influence a person’s intention to adopt m-payment services, as it is a relatively new form of payment transaction. As Schierz et al. (2010) observed, people tend to be less motivated to adopt new payment methods when the new methods are perceived to present higher risks than existing payment methods. A recent empirical study by Tan and Lau (2016) confirmed the negative impact of PR on behavioral intentions to adopt mobile banking services among generation Y consumers in Malaysia. Indeed, PR is argued to be a critical determinant when considering new forms of innovation. This pre-adoption stage reflects a time when people have limited experience with the innovation and are wary of the risks and consequences of its use. Hence, the PR construct is explored in the following hypotheses:

PT

The DOI theory’s view of the innovation-decision process posits that encouraging a trusting consumer attitude toward a new innovation can be a vital promotional activity in the pre-adoption stage (Rogers, 2003). Mayer, Davis, and Schoorman (1995) defined trust as the willingness to be placed in a vulnerable position based on the positive expectation of another party’s reciprocated future behavior. Gu, Lee, and Suh (2009) suggested that trusting a bank allows consumers to see the value of mobile banking and encourages them to use it. Therefore, for the purposes of this study, PT reflects the degree to which the consumer believes he or she can trust the parties involved in the m-payment process (such as banks, mobile operators, merchants, and third parties) to perform the expected activities without taking advantage of consumers (Zhou, 2011). According to Chandra et al. (2010), PT in a service provider has a direct impact on consumer intentions to use m-payment services, whereas a lack of consumer trust may be an impediment to the uptake of this type of payment service. Similarly, the recent study of Nguyen et al. (2016) found that PT has the strongest impact on behavioral intentions to adopt m-payment services among potential users in Vietnam. Hence, this study explores the PT construct in the following hypothesis:

PC

Additional costs may be associated with the use of m-payment services, such as the cost of acquiring a mobile phone, transactional fees to use the service, and ongoing access and maintenance costs. Thus, PC reflects whether and how an individual considers m-payment service use to impose additional financial costs beyond his or her current situation (Luarn & Lin, 2005). Indeed, Zhou (2011) suggested that PC is an important determinant that can negatively influence consumer intentions regarding m-payment services. The high usage costs associated with using m-payment services, including communication and transaction fees, can slow the expansion of services and thus potentially result in the underutilization of such services (G. E. Tan et al., 2014). Given its importance, researchers have suggested that PC should be included in the model when investigating m-payments (Ho Cheong & Park, 2005). Hence, this study proposes the following hypotheses related to the PC construct:

Method

This study aimed to collect data across the two groups of interest (current and prospective users of m-payment services) to test the proposed research model and its corresponding hypotheses. The survey items used to measure the constructs were adapted from the extant literature, allowing the researchers to align the final questionnaire with the m-payment context (see the appendix). Each questionnaire item used a 7-point Likert-type scale that ranged from 1 (strongly disagree) to 7 (strongly agree).

The questionnaire was developed in English, translated into Thai, and then back translated (into English) to confirm that no loss of meaning occurred in the Thai version during the translation process (Douglas & Craig, 2007). The measures were pre-tested with 10 native Thai mobile phone users who were invited to join a group discussion and asked to give feedback on the questionnaire. Based on their feedback, the wording and additional information for some items were modified and expanded to ensure clarity and comprehension.

For the purpose of this study, the target population includes any individual who currently owns a mobile phone, as mobile phone users have a higher potential of adopting m-payment services than individuals who do not have mobile phones (L. Chen, 2008). The data collection technique used in this study was the intercept survey in which potential respondents were intercepted at a location and asked to participate in the research study (Churchill, Brown, & Suter, 2008). Potential respondents were randomly approached at various mobile phone shops in Bangkok, the capital of Thailand. Bangkok was chosen as the sampling location because the largest pool of mobile phone users is located in Bangkok (National Statistical Office Ministry of Information and Communication Technology, 2015). The researcher checked to determine whether the potential respondents were appropriate for this study. They were asked whether they had participated in this survey before and whether they were adopters or non-adopters of m-payment services. After fulfilling these criteria, the respondent was given a questionnaire for completion.

At the end of the survey, a total of 825 completed questionnaires had been received. Of these, 29 cases were dropped due to many missing values. Another 10 cases were identified as outliers and were removed because they proved to be aberrant and non-representative of the general data set—resulting in data non-normality (Kline, 2005) and seriously affecting the statistical tests (Hair, Black, Babin, & Anderson, 2010; Tabachnick & Fidell, 2006). The exclusion of the outliers yielded the final sample data of this study, with 785 respondents for the analysis. Table 1 summarizes the demographic profile of the 785 respondents in terms of their gender, age, and occupation.

Demographic Profile of Respondents.

A two-step approach involving structural equation modeling (SEM) was adopted for measurement scale validation and structural analysis (Byrne, 2000; Hair et al., 2010). The maximum likelihood estimation procedure was employed using AMOS Version 22. This study’s proposed research model was analyzed following three main steps. First, a covariance matrix of all measured variables was constructed and subjected to a series of validity and reliability checks. Upon establishing the model fit, we estimated the significance and size of each structural parameter for the specified model. Finally, a multi-group analysis was employed to test the difference between the groups of current and potential users in their adoption of m-payment services. The detailed results of the analysis are discussed below.

Results

Reliability and Validity of Measurement Items

A confirmatory factor analysis (CFA) of all items was simultaneously conducted to evaluate the validity of the items and the eight underlying constructs in the measurement model. Table 2 summarizes the results of the measurement model across the model-fit indices. All model-fit indices indicate that the measurement model exhibits a good fit with the data collected. Hence, we proceeded to examine the measurement model’s psychometric properties to evaluate its reliability and construct validity.

Results of the Measurement Model Across Model-Fit Indices.

Note. GFI = goodness-of-fit index; AGFI = adjusted goodness-of-fit index; CFI = comparative fit index; NFI = normed fit index; SRMR = standardized root mean square residual; RMSEA = root mean square error of approximation.

Construct validity was examined using the test for convergent and discriminant validity. Convergent validity was evaluated using the attributes of factor loading, average variance extracted (AVE), and construct reliability (CR). Table 3 shows the factor loading, AVE, and CR values that were used to assess convergent validity for the seven-factor CFA model. The item loadings for the seven-factor CFA model show that all scale items are highly loaded on their respective constructs, as all factor loadings are above the threshold value of 0.70. Each indicator’s item reliability, including CR, was above .70, suggesting good reliability and convergent validity. Notably, all CR values for the eight constructs in the model were above .90, which provides strong evidence that these measures consistently represent the same latent construct.

Factor Loadings, AVE, Item Reliability, and Construct Reliability of the Eight-Factor CFA Model.

Note. AVE = average variance extracted; CFA = confirmatory factor analysis; CR = construct reliability; PU = perceived usefulness; PEOU = perceived ease of use; COM = constructs of compatibility; SN = subjective norms; PT = perceived trust; PR = perceived risk; PC = perceived cost; BI = behavioral intention.

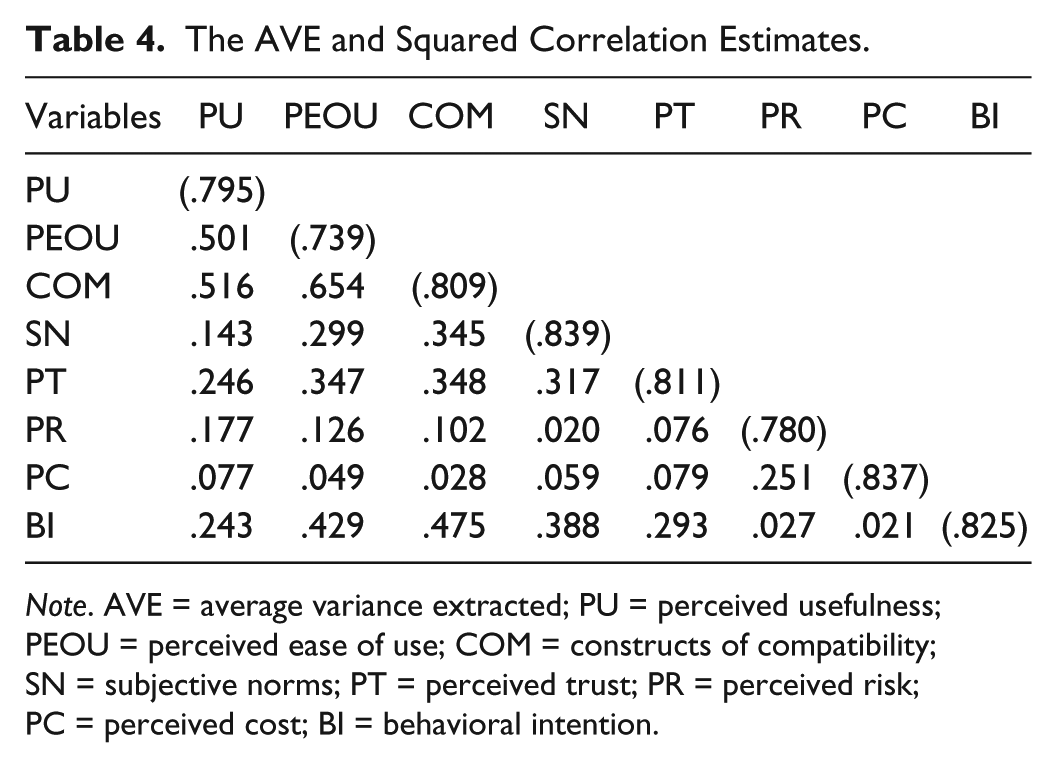

The AVE values were compared with the squared estimate of the correlation estimates to assess discriminant validity. The correlation matrix in Table 4 shows that all AVE values are greater than the squared correlation estimates; this result confirms that a satisfactory level of discriminant validity has been achieved and indicates that the measured variables have more in common with the construct with which they are associated than with other constructs in the model. Furthermore, this finding indicates that all constructs in the measurement model are significantly different from one another.

The AVE and Squared Correlation Estimates.

Note. AVE = average variance extracted; PU = perceived usefulness; PEOU = perceived ease of use; COM = constructs of compatibility; SN = subjective norms; PT = perceived trust; PR = perceived risk; PC = perceived cost; BI = behavioral intention.

Structural Model and Hypothesis Testing

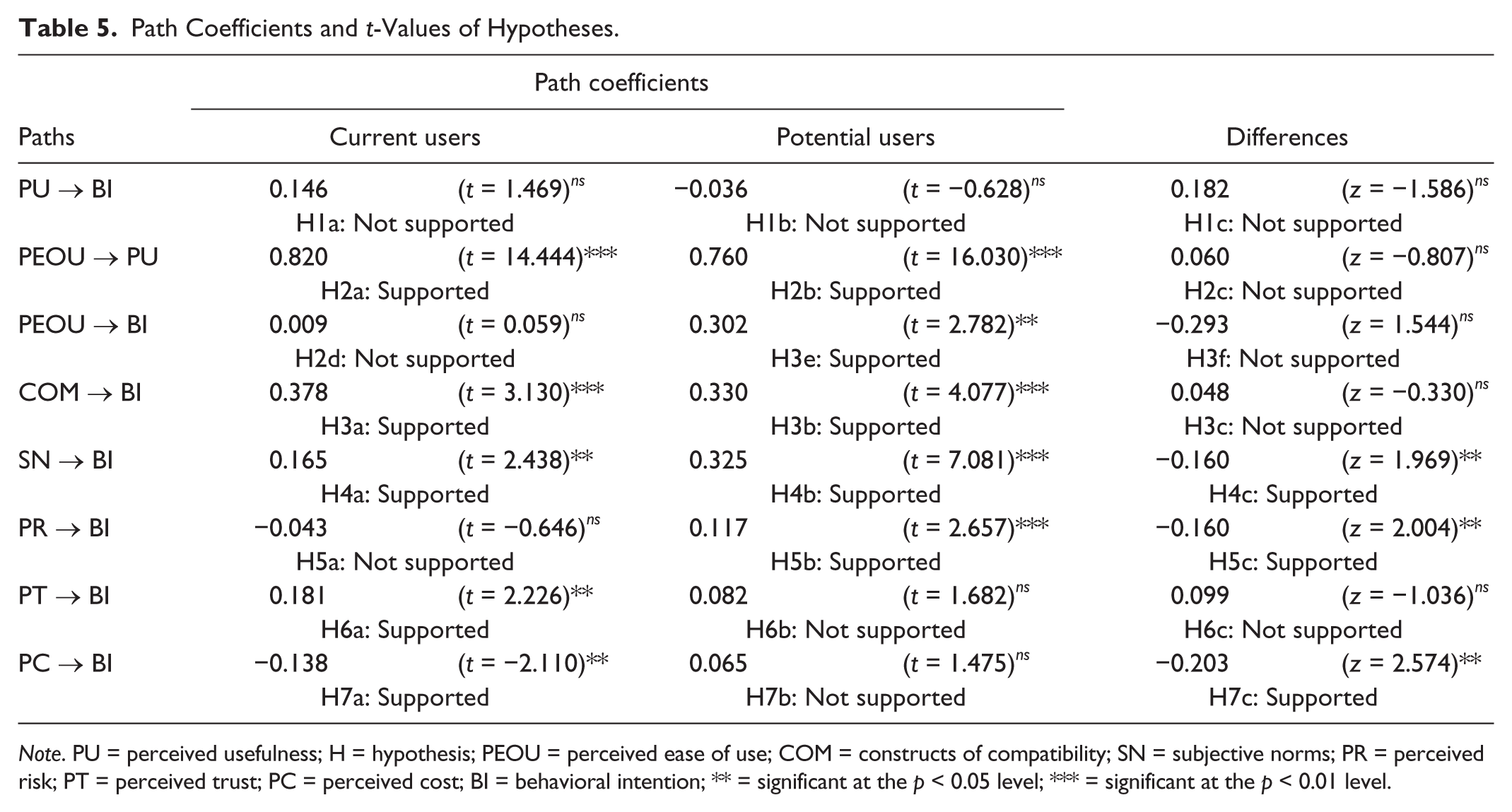

The results of the full structural model showed a good fit of the data to the model: χ2/df = 1.941, goodness-of-fit index (GFI) = 0.910, adjusted goodness-of-fit index (AGFI) = 0.884, comparative fit index (CFI) = 0.974, normed fit index (NFI) = 0.949, standardized root mean square residual (SRMR) = 0.028, and root mean square error of approximation (RMSEA) = 0.035. This study tested each hypothesis by examining the path significance. Figure 2 illustrates the path diagram with the resulting fully standardized structural parameter estimates included on the paths. The paths from COM, SN, PT, and PC to adoption intentions are statistically significant in the current user group (t-values range from −2.110 to 3.130). These factors explained 64% of the variance in current users’ intentions to adopt m-payment services. By contrast, in the potential user group, the paths from PEOU, COM, SN, and PR to adoption intentions are found to be statistically significant (t-values range from 2.657 to 7.081). These factors explained 55% of the variance in potential users’ intentions to adopt m-payment services. In addition, the path from PEOU to PU was revealed to be statistically significant in both the current and potential user groups (t-value of 14.45 for current users and 16.03 for potential users). The PEOU factor accounted for 68% of the variance in current users’ perceptions and 49% of the variance in potential users’ perceptions of the usefulness of adopting m-payment services. Interestingly, the results showed that, for both groups, PU was not a mediating variable in the relationship between PEOU and behavioral intentions.

Structural path analysis results for the research model.

The next data analysis was performed to investigate the differences in the factors that influence the adoption of m-payment services between current and potential users. We followed a systematic approach by testing a series of hierarchical hypotheses, as recommended by Bollen (1989). We first determined whether the covariance structure was invariant across current users and potential users. The result of this comparison was positive (Δχ2 = 49.57, df = 506, p value = .002); therefore, we proceeded to test for invariance in the factor patterns and regression weights. We applied a test comparing the regression coefficients between structural models, which were considered in pairs using the critical ratio difference (CRDIFF; Byrne, 2000). This approach yields a list of critical ratios for the pair-wise differences among all parameters estimated in both single- and multi-group analyses. If the CRDIFF value is greater than 1.96, then the relationship posited by that path is significantly different between the groups. We found statistically significant differences between current users and potential users in their SN, PR, and PC. The respective z scores of 1.969, 2.004, and 2.574 were greater than the CRDIFF value of 1.96 (Figure 2). The influence of SN and PR on adoption intentions was stronger among potential users than among current users. However, the influence of PC on adoption intentions was stronger among current users than among potential users. Table 5 summarizes the SEM analysis results and hypothesis testing results.

Path Coefficients and t-Values of Hypotheses.

Note. PU = perceived usefulness; H = hypothesis; PEOU = perceived ease of use; COM = constructs of compatibility; SN = subjective norms; PR = perceived risk; PT = perceived trust; PC = perceived cost; BI = behavioral intention; ** = significant at the p < 0.05 level; *** = significant at the p < 0.01 level.

Discussion

Previous studies examining the adoption of m-payment services have typically investigated a single group—either users or non-users. Our study provided a holistic overview of m-payment service adoption by first identifying the factors that influence m-payment service adoption among current and potential m-payment users and then comparing these two groups to identify any differences in these factors. We found that COM was the factor that most strongly affected current users’ intentions to adopt m-payment services, followed by SN, PT, and PC. By contrast, the SN factor was found to have the greatest influence on potential users’ intentions to adopt m-payment services, followed by COM, PEOU, and PR. Regarding the differences between current and potential users in adopting m-payment services, SN and PR had a stronger influence on potential users than on current users. However, PC had a stronger effect on current users’ intentions to use m-payment services. Consistent with S. Yang et al. (2012), the outcomes demonstrate that potential adopters tend to form their intentions to adopt m-payment services by considering both the positive and negative factors.

This study reveals that COM influences both current and potential users’ intentions to adopt m-payment services. The effect of COM on behavioral intentions implies that people tend to be more concerned about whether using m-payment services aligns with their needs, social image, and lifestyle. This finding is in accordance with the study of S. Yang et al. (2012), which indicates a significant relationship between COM and potential and existing users’ behavioral intentions to adopt m-payment services. This finding highlights the importance of COM in determining behavioral intentions, which is often not considered by adoption studies because COM is not considered in the original TAM model.

SN is another important factor that influenced the uptake of m-payment services among current and potential users. Previous work has indicated that SN reflects the influence of work colleagues, friends, and family as a critical determinant in an individual’s decision-making process regarding the use of m-payment services (Keramati et al., 2012; Nguyen et al., 2016; Phonthanukitithaworn et al., 2016; Schierz et al., 2010; Shin, 2010; Yan et al., 2009; S. Yang et al., 2012). Moreover, we found the effect of SN to be stronger among potential users than among current users. This finding is consistent with previous studies by Fishbein and Ajzen (1975) and Taylor and Todd (1995a), who noted that the effect of SN on behavioral intentions is likely to be stronger for individuals who have no experience because they rely heavily on other people’s suggestions to help them make decisions.

PR was found to negatively influence the uptake of m-payment services only among potential users. This finding supports the notion explained in E. Tan and Lau’s (2016) study and in the DOI innovation-decision process that PR plays a critical role in the technology or innovation pre-adoption stage when people have no understanding of the innovation and are wary of the risks and consequences associated with its use (Rogers, 2003). Arguably, PR can lower individuals’ intentions to use m-payment services, particularly among people who have no understanding of m-payment services. Given that consumers likely have certain expectations about the risks associated with m-payment services, providers of these types of services would benefit from clearly articulating their ability to protect critical information during the transaction process. This assurance might be provided through satisfaction guarantee policies that protect users from the harmful consequences of service failure or through offers of potential user training and trial use activities.

Furthermore, PT was found to have a direct effect on current users’ behavioral intentions to use m-payment services, but it was not found to have a direct effect on those of potential users. This result implies that current users are highly concerned about the issue of trust with entities involved in the m-payment process and activities as they are acutely aware of giving m-payment providers their personal information (e.g., telephone number, date of birth, address, credit card number) when conducting such payment transactions. Thus, trust in m-payment entities is important from their perspective. As a result, service providers should pay attention to building trust among current m-payment users because, if this group senses a lack of trust in m-payment entities, they may have negative feelings about m-payment services and thus discontinue their use. Interestingly, PT was not found to affect potential users’ behavioral intentions to use m-payment services. Given that this group has yet to experience the specific process and activity of using an m-payment service, they may be unaware of the negative consequences that might be derived from unreliable m-payment systems and service providers. Hence, PT may not have emerged as a significant factor for them.

PC has been identified as a major barrier to the subsequent uptake of m-payment services. Specific m-payment costs, such as transaction fees, new headset costs, subscription fees, and communication access, all contribute to incremental cost increases associated with the use of these services (Ho Cheong & Park, 2005; Keramati et al., 2012; Lu et al., 2011; Luarn & Lin, 2005; Tsu Wei, Marthandan, Chong, Ooi, & Arumugam, 2009; Wu & Wang, 2005). This study found a significant effect of PC on current users’ behavioral intentions to use m-payment services. This result was likely observed because current users are acutely aware of all the incremental expenses experienced through their use of m-payment services. PC was not found to affect potential users’ behavioral intentions to use m-payment services. Given that this group has yet to experience the specific costs of using an m-payment service, they may be unaware of the additional costs that might be incurred.

Finally, the findings of this study also reveal a lack of significance of the PU and PEOU constructs among current users of m-payment services. The non-significance of PU and PEOU could indicate that these determinants are irrelevant for current users. Current users who have experience using m-payment services are already aware of these services’ usefulness and ease of use. By contrast, PU is irrelevant for potential users, whereas PEOU is an important factor that influences their intentions to adopt m-payment services. This finding implies that the effect of PEOU will play a critical role for potential users who are not familiar with m-payment services. Arguably, the influence of PEOU may vary depending on an individual’s experience and awareness of new services. Potential users may first focus on ease of use, while current users will have presumably overcome concerns about ease of use and may instead focus their attention on the usefulness of the service.

Implications

Theoretical Implications

From a theoretical standpoint, the findings of this study hold several implications for scholars in the field of technology adoption. First, the current study provides a better theoretical understanding of the factors that influence the adoption of m-payment services by identifying relevant factors and comparing their effects on people who use this payment service and on non-users. Existing studies tend to focus on either adopters or non-adopters of a new idea, innovation, or technology, whereas this study’s focus on both groups distinguishes it from other investigations and facilitates comparisons to gain further insight. Furthermore, the study has successfully extended the TAM by including COM, SN, PR, PT, and PC. The integrated model provides a clearer explanation of adoption intentions than the TAM alone. It advances the understanding of key m-payment adoption attributes in the context of mobile-based financial service consumption. Finally, the model and its constructs can be replicated or extended to different economies to determine whether the findings are similar or otherwise.

Practical Implications

From a practical perspective, the findings of this study hold important implications for the practical context of the m-payment industry in Thailand in terms of strategies that it can adopt to pursue greater acceptance and diffusion of m-payments in the mobile phone user market in Thailand. First, service providers should carefully consider issues regarding the service’s compatibility with Thai consumers as this study found that the perceived compatibility construct influenced both current and potential users’ intentions to adopt m-payment services. Hence, organizations that seek to promote m-payment activities should ensure that the services offered to customers meet their personal needs and reflect lifestyle considerations.

Second, the strong impact of SN on intentions, particularly among potential users, demonstrates that adopting m-payment services can serve as a means to reinforce individuals’ social connections and social status through group affiliation. The practical implication of this finding is that service providers must consider people’s social connections, networks, and status to potentially increase the use of m-payment services. Accordingly, promoting m-payment services through a social or community network may be a useful approach for m-payment service providers (Phonthanukitithaworn et al., 2016).

Third, risk avoidance and risk reduction is another important issue that service providers prioritize, especially among potential users. This finding implies that service providers should ensure a strong security system when offering m-payment services to customers. For instance, the application of a mobile digital signature and highly secure passwords when conducting transactions can ensure the confidentiality and authenticity of an m-payment system (E. Tan & Lau, 2016). In addition, offering potential users training and trial activities before using an m-payment service may be a helpful approach to reduce their level of risk.

Fourth, the positive relationship between PT and current users’ behavioral intentions to adopt m-payment services indicates that these users are highly concerned about the issue of trust surrounding the entities involved in m-payment processes and activities. This finding implies that building trust among current users should also be made a strategic priority, as they may discontinue their use of m-payment services if they sense a lack of trust in m-payment entities. According to Zhou (2014), consumer trust can be built by providing a positive user experience. Therefore, to provide current users with a positive experience, the entities involved in m-payments should ensure that the m-payment system is reliable, free of technical errors, and highly responsive to their inquires or to any problems that might arise.

Finally, this study indicates that a cost increase has a negative effect on current users’ intentions to use m-payment services as they are aware of all the incremental expenses that they experience in their use of m-payment services. Thus, service providers must highlight the value of m-payment services vis-à-vis traditional payment services and emphasize the functional advantage of using m-payment services to demonstrate that the benefits gained justify the cost. In addition, creative promotional and pricing strategies, including cost reductions, should be implemented to attract price-conscious customers.

Limitations and Recommendations for Future Research

All studies inevitably have limitations. First, this study focused only on the extended TAM to identify the factors that influence m-payment adoption. Given the existence and use of various models, including TPB and DOI, testing which of the models provides the optimal explanation of technology adoption for m-payment purposes may be advisable. Second, given the innovative nature of m-payment services and the early stage of m-payment implementation, this study focused solely on behavioral intentions as the dependent variable to interpret theory-driven actual behavior in the early adoption stage. Therefore, further studies may improve measurement reliability by employing additional methods, such as a field study and/or a longitudinal study, to more closely observe and investigate the later stages of m-payment adoption. Finally, the study sourced its data from Thailand, an Asian country in which Eastern cultural factors may have influenced the responses. Thus, future research might seek to include such cultural factors in further exploring m-payment service adoption.

Conclusion

This article reports the results of a study examining m-payment services and identifies the factors that influence an individual’s intention to adopt m-payment services. The set of factors were applied to two groups: people who were already using m-payment services (current users) and those who had not yet adopted these services (potential users). The study’s results suggest that individuals’ perceptions of compatibility and SNs are important elements in their consideration of m-payment services; consequently, both factors should be considered in the strategies designed to promote service adoption. Hence, the m-payment services industry should ensure that their offerings are aligned with consumers’ current values, needs, and lifestyles. Moreover, promoting m-payment services through business, employer, and social networks may be useful in increasing potential uptake. An important finding concerns how certain factors such as trust and cost become significant issues after people begin using m-payment services—a differentiating issue between the two groups. The practical implications of these findings can assist managers in the mobile and electronic payment industries who seek to implement appropriate service strategies and business models for current and future markets.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.