Abstract

The public health spending in India has been hovering around 1% of gross domestic product (GDP), and it contributes only 28% of total health expenditure. Hence, out-of-pocket (OOP) payments continue to be the dominant source of health care financing in India. However, for providing protection from the economic effects of health shocks, last few years have seen a plethora of central and state government–sponsored private health insurance schemes for the deprived groups, particularly those working in the unorganized sector. The latest is the Rajiv Gandhi Jeevandayee Arogya Yojana (RGJAY), launched by the Government of Maharashtra in 2012. This study is an attempt to assess the extent to which RGJAY protects the families from making OOP expenditure while availing the tertiary care from the RGJAY accredited facilities. Both primary and secondary data were utilized for this study. Despite being enrolled in RGJAY, more than three fifths (63%) of the beneficiaries still incurred OOP payments for services when admitted in the hospital, and more worryingly, it was found that a significantly higher proportion of persons from Below Poverty Line (BPL) families (88.23%) reported paying for diagnostics, medications, or consumables. Furthermore, our study found that about a third of the beneficiaries experienced financial catastrophe if indirect expenditure is taken into consideration. This also implies that for the poor, ill-health has further deepened the existing poverty.

Background

In India, over the last three decades, the government has been spending approximately 1% of the gross domestic product (GDP) on health. This accounts for less than a third of the total health expenditure of the country. The contribution of the public sector toward health care in India is thus lower than the average public health spending for Sub-Saharan Africa and for the “least developed countries” in the world. This chronic neglect has severely limited the ability to establish and run public health care facilities and provide quality health care resulting in people relying on private health care services (Dreze & Sen, 2014). The absence of other health care financing options like insurance eventually leads to high out-of-pocket (OOP) health payments for purchasing health care from private providers. According to the latest national health accounts, OOP expenditure accounts for about 70% of India’s spending on health care (Murthy, Rout, Nandraj, Arya, & Kumar, 2008).

This overreliance on OOP health spending causes significant financial burden on households who may resort to distress financing options such as sale of assets or borrowing at exorbitant rate of interest to cope with the cost of health care (Bhandari, Berman, & Ahuja, 2010). The rest do not undergo treatment at all due to lack of purchasing capacity Thus, about 40 to 60 million people in India become impoverished every year and more than 13% of households experience catastrophic payments (Bhandari et al., 2010; Garg & Karan, 2009; Ghosh, 2011) while a fourth of the population goes untreated on account of financial constraints (Ghosh, 2014a).

Ironically, though majority of the populace of India still lies outside the ambit of prepayment and risk pooling mechanisms, India is one of the first developing countries to establish a system of social protection in health, namely, the Employees’ State Insurance Scheme (ESIS) as early as in 1952 for the people engaged in private enterprises in the organized sector. This was followed by a social health insurance program for the central government employees called “Central Government Health Scheme” (CGHS in 1954). However, the history of private health insurance (PHI) in India has been very short. In fact, the first PHI product, namely, Mediclaim, a hospital indemnity scheme, was introduced in 1986 by the nonlife public insurance companies. The public insurance companies had complete monopoly over private health insurance market until 1999 when it was opened for private participation and foreign direct investment. Since then, the insurance sector has shown a rapid growth, but till 2004 to 2005, merely 1% of the population had any type of health insurance (National Sample Survey Organization [NSSO], 2006). But in the last few years, with the central and state governments subsidizing private health insurance under Rashtriya Swasthya Bima Yojana (RSBY—national health insurance) and other publicly funded health insurance (PFHI) schemes, the PHI industry received a major boost with the current health insurance coverage expected to be anywhere between 15% and 25%. The latest PFHI scheme is the Rajiv Gandhi Jeevandayee Arogya Yojana (RGJAY), launched by the Government of Maharashtra in 2012.

The PFHI schemes have brought in fundamental changes in the public financing and provisioning of services in the health sector in India. Traditionally, the tax-based financing system relied on a network of public health facilities for service provision. Instead of relying on supply side interventions, government introduced demand side health financing measure by paying premiums to insurance companies to extend health insurance with a package of inpatient care to Below Poverty Line (BPL) populations. This health insurance based health system actually led to a provider–purchaser split where the government’s role has been reduced to only a payer as the health care packages are now procured by a financial intermediary also known as mostly, health insurance companies. Although the financial intermediaries’ purchases care from both public and private providers, private sector ends up getting higher revenues as it invariably dominates the network of empaneled providers across schemes.

Another attractive feature of PFHI is that these schemes promise that the enrolled persons can receive cashless benefits, implying that no payment is required at the point of service. In cashless method of claim settlement, the whole hospitalization-related expenditure is borne by the insurance companies, and therefore, there will not be any financial burden on the insured persons. In fact, one of the reasons for adopting cashless method over reimbursement of claim is that the insured will be able to avail services without incurring any OOP payments.

The current literature on PFHI is not very extensive, and the opinion regarding extent of financial risk protection is mixed. One interpretation is that PFHI programs will improve access and provide financial protection to the poor against health shocks (Forgia & Nagpal, 2013). It would also ameliorate the efficiency problem of health care at the secondary and tertiary levels because of the provider–purchaser split (Fan, Mahal, & Karan, 2012; Fischbacher & Francis, 1998). Despite its popularity in the policy circles, many believe that these new financing approaches have created inefficiency, increased costs, and led to an expansion of a largely unregulated market for insurance and health care (Dreze & Sen, 2014; Gaitonde & Shukla, 2012; Sen, 2012; Varshney et al., 2012). It is, however, difficult to determine whether all the criticisms are fair. For example, while Ghosh (2014b) and Karan and Selvaraj (2012) showed that RSBY has failed to reduce the vulnerability of poor households to financial catastrophe from health shocks, other studies found that PFHI schemes significantly reduced OOP spending on health care (Aggarwal, 2010; Fan et al., 2012; Rao et al., 2012; Sabharwal, Mishra, Naik, Holmes, & Hagen-Zanker, 2014).

Nevertheless, the cashless treatment at the point of use that PFHI theoretically offers to beneficiaries does not appear to be infallible. Rao et al. (2012) found that nearly 60% of the beneficiaries in Andhra Pradesh reported a median expenditure of  3,600 (US$59) as OOP payments. Similarly, Devadasan, Seshadri, Trivedi, and Criel (2013) observed that 97% of the eligible population who utilized RSBY had paid cash for services. Forty-four percent of those in possession of the RSBY health card incurred OOP expenditure at the time of admission to the hospital even though they were entitled to receive the services free of cost.

3,600 (US$59) as OOP payments. Similarly, Devadasan, Seshadri, Trivedi, and Criel (2013) observed that 97% of the eligible population who utilized RSBY had paid cash for services. Forty-four percent of those in possession of the RSBY health card incurred OOP expenditure at the time of admission to the hospital even though they were entitled to receive the services free of cost.

The review of literature suggests that only a few studies have attempted to analyze the expenditure incurred by beneficiaries utilizing the services covered under PFHI schemes. This study is therefore an attempt to fill the gap in literature by assessing the extent to which RGJAY protects the families from making OOP expenditure and prevents catastrophic expenditure for utilizing tertiary care. In addition, we also studied the disease profile of the beneficiaries, assessed disease-specific OOP payments made by the RGJAY beneficiaries, and investigated the reasons for incurring OOP expenditure.

The Key Features of RGJAY

Under RGJAY, both BPL

1

and Marginally Above Poverty Line (MAPL) families with annual income up to 100,000 (US$1,639) are entitled to receive tertiary care from accredited institutions.

The Rajiv Gandhi Jeevandayee Arogya Yojana Society (RGJAYS) is the principal body that overlooks the governance and implementation of the scheme in the state. It pays a premium per eligible family to a commercial insurance company depending on the number of orange ration card holders, 2 yellow ration card holders, Antyodaya card holders, and Annapurna card holders in the state based on the data provided by the Food and Civil Supplies Department.

For the year 2014-2015, according to the RGJAYS, premium was paid for 21.9 million households. In other words, 85% of the population is currently covered by the scheme. Against the premiums, the insurance company provides a hospital indemnity to the beneficiary families for medical expenses up to 150,000 (US$2,459) that covers 971 surgeries, therapies, and procedures under 30 specialties with 121 follow-up packages. The insurance company hires private firms known as third-party administrators (TPAs) to carry out all the administrative work of the scheme such as hospital empanelment, hospital grading, preauthorization, checking claim documents, and so on (Figure 1).

Stakeholders in RGJAY.

The packages that are to be reimbursed to the hospitals are based on Diagnostic Related Groups (DRGs). On the basis of various parameters such as human resources, infection control, facilities management, and so on, hospitals are classified into four grades, namely, Grades A, B, C, and D with Grade A1 hospitals receiving full 100% packages, A2 receiving 90%, B1 receiving 85%, B2 receiving 80%, C1 receiving 75%, C2 receiving 70%, and D1 receiving 60%. D2-grade hospitals are considered to be “not eligible” for the scheme.

As per the guidelines, when a beneficiary goes to an empaneled network hospital, the patient should be assessed and categorized as an inpatient or outpatient. If a patient is identified as eligible for RGJAY, he or she receives free consultation and diagnostics. The person needs to be registered with RGJAY before the treatment is provided. The RGJAYS has started providing health cards to the eligible households, which could be used at the network hospitals. However, it is not mandatory to have the health card for accessing services. Those who do not possess the card can still avail services by showing their ration cards and valid photo ID proof at the hospitals’ RGJAY counter. The Arogyamitra then registers the person on the online portal after which the person is eligible to get the benefits under RGJAY.

For the inpatient procedure, the empaneled hospital raises a preauthorization that has to be approved by the TPA within 24 hr. The hospital then performs the procedure and discharges the patient. Ten days after discharge, the hospital submits the claim to insurance company. After verifying the documents uploaded by the hospital, the insurance company is supposed to pay the claim amount to the hospital within 15 working days (Figure 2). RGJAYS runs a customer care helpline where patients can complain regarding problems like refusal of hospital to treat patients or cases of money collection.

Workflow of RGJAY in the empaneled hospital.

Implementation of RGJAY in the State

In the first phase, the scheme was launched in eight districts of Maharashtra, namely, Gadchiroli, Amravati, Nanded, Sholapur, Dhule, Raigad, Mumbai city, and Mumbai Suburban. The second phase of the scheme was inaugurated on November 21, 2013, thus extending it to the whole state. In its first phase, RGJAYS had empaneled 142 hospitals in eight districts. Majority of them are private hospitals (98; 69%) and rest are public hospitals (44; 31%).

Method

Both primary and secondary data were utilized for this study. The secondary data consist of data related to utilization of RGJAY packages as well as data from the grievance department of RGJAYS that records complaints logged on the customer service helpline. The latter refers to the 1,489 resolved cases during the period from November 16, 2012, to June 27, 2013. The secondary data were analyzed to assess the most commonly reported problems faced by the beneficiaries in using services from the RGJAY accredited hospitals.

Mumbai and Mumbai Suburban district was purposively selected for the study as this district experienced highest utilization of RGJAY services. According to the program data, 32,566 surgeries and therapies had been performed in Mumbai under the scheme in its first phase, that is, from July 2, 2012, to July 1, 2013. Using this as the base population and keeping confidence level at 95% and confidence interval at ±8, we arrived at a sample size of 152 patients for the survey. The study region had a total of 47 empaneled hospitals; 19 (40%) of which were government and 28 (60%) were private. The sample size of eight hospitals was pragmatically selected based on the time and resources available to the researchers. Out of these eight hospitals, we selected three (38%) and five (62%) hospitals from public and private sectors, respectively, keeping the proportion of public–private hospitals similar to the study area ratio. The hospitals were randomly chosen by paper chit method. Primary data were collected by conducting exit interviews of beneficiaries who had utilized the scheme in these eight empaneled tertiary care hospitals. Data collection was done using a structured interview schedule from August to September 2013. Statistical analysis of the data was performed with the help of SPSS Version 20.

To assess the extent of financial risk protection provided by RGJAY to its beneficiaries, we calculated the incidence of catastrophic expenditure in the study population, that is, the percentage of households whose OOP health payments exceed a certain percentage of household’s total consumption expenditure, used as the proxy for household’s capacity to pay (Wagstaff & van Doorslaer, 2003; Xu et al., 2003). In this study, a threshold of 10% was used (Ghosh, 2011). The underlying assumption in setting the threshold for defining catastrophic expenditure is that if a household’s expenditure on health care is more than the threshold, the household will have to reduce its expenditure on other subsistence needs because of the need to pay for health care. Hence, if household’s expenses on health care exceed 10% of the household’s prepayment income, then it is considered to be catastrophic in nature.

Results

Socioeconomic Profile of Study Population

Table 1 provides a profile of the socioeconomic and demographic characteristics of the RGJAY beneficiaries in our sample. There was higher representation of males in the study sample with 59% of the respondents being male. While 70% of the population was currently married, 16% and 14% were widowed and unmarried, respectively. Age distribution of the sample population reveals that more than half of them (51%) were aged between 41 and 60 years, and only 7% were below 14 years of age. While almost half of respondents (45%) had secondary education, a quarter of them (24%) did not have any formal education. The distribution of households by religion reveals that a majority of two thirds of them are Hindus.

Characteristics of Respondents that Utilized RGJAY Benefits, Mumbai and Mumbai Suburban Region, 2013.

Note. RGJAY = Rajiv Gandhi Jeevandayee Arogya Yojana.

Other includes Christians, Sikhs, and Jains.

In total, 51.3% of the families reported family income up to 100,000 per annum. Most importantly, results indicate that almost half of the households (48.7%) reported having a family income higher than 100,000 per annum but received benefits as they had a yellow or orange ration card.

According to the data provided by the Food and Civil Supplies Department, of the total eligible families in Mumbai, 99.22% are orange ration card holders, 0.28% are yellow ration card holders, 0.27% are Annapurna card holders, and 0.23% are Antyodaya card holders (Table 2). In our study population, though, 89% had orange ration cards and the rest (11%) had yellow ration cards.

Distribution of Eligible Beneficiaries in Mumbai and Mumbai Suburban, 2013.

Source. Data provided by Food and Civil Supplies Department, September 2013.

The analysis of primary data provides insights into the utilization pattern. In our sample, 61% of the beneficiaries accessed services from private hospitals and 39% from public hospitals. This is clearly in line with the public–private distribution of empaneled hospitals in the scheme and in the study sample. In private hospitals, of those who availed services, 63% of them were orange ration card holders and only 37% were yellow ration card holders. However, we observed a reverse trend in public hospitals wherein 53% of the beneficiaries were yellow ration card holders and 47% were orange ration card holders.

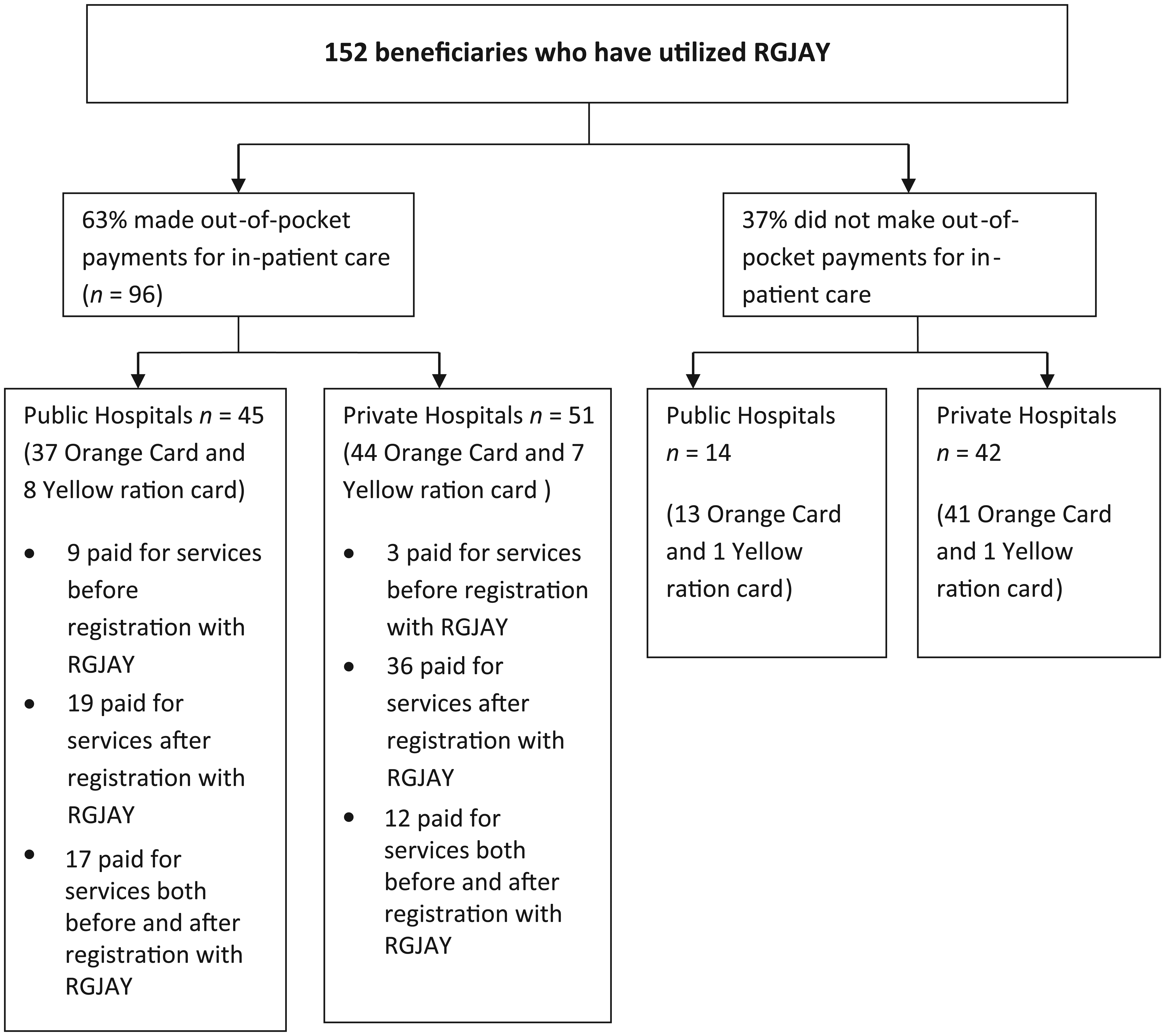

The rest of the analysis focuses on the financial protection aspect of the scheme. The secondary data revealed that of the total complaints received on the customer care helpline, 43% were cases of money collection by the hospitals from the patients. Analysis of our sample data shows that despite being enrolled in RGJAY, more than three fifths (63%) of the beneficiaries still incurred OOP payments for services when admitted in the hospital, and more worryingly, it was found that a significantly higher proportion of BPL families (88%) reported paying for diagnostics, medications, or consumables compared with their MAPL counterparts (58%). Among those who paid for services during inpatient care, 12.5% paid for services before registration with RGJAY, 57% paid for services after registration with RGJAY, and 31% paid for services both before and after registration with RGJAY (see Figure 3).

Incidence of out-of-pocket payment among the beneficiaries of RGJAY, Mumbai and Mumbai Suburban, 2013.

OOP Expenditure by Beneficiaries Availing Treatment Under RGJAY According to Treatment Group

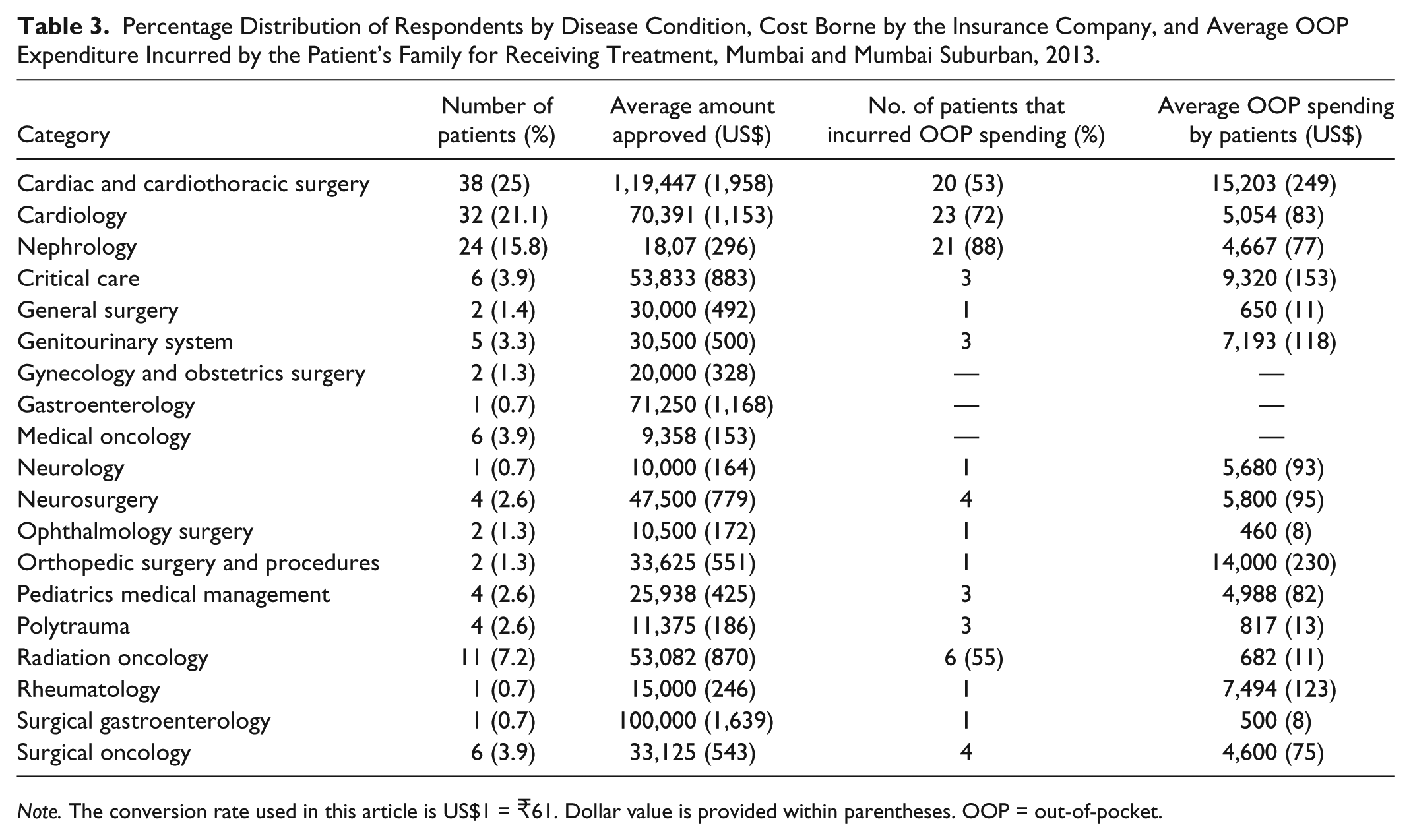

The data on the nature of illnesses reported by the hospitalized patients enable us to group the diseases and study the disease profile of the RGJAY beneficiaries, the cost borne by the insurance company, and the OOP expenditure incurred by the patients for treating a specific disease condition. The proportion of patients treated for various categories of diseases is given in Table 3. The diseases reported for hospitalizations are grouped into categories based on the disease classification used by RGJAYS. Among the hospitalized cases, cardiac and cardiothoracic surgery and cardiology together accounted for 46% of the disease burden. Nephrology, medical oncology, and critical care accounted for 15.8% and 3.9%, respectively. Although there was relatively a higher incidence of OOP payment for beneficiaries from certain specialties such as cardiology and nephrology, the results indicate that people had to incur OOP payments for treatment of majority of conditions.

Percentage Distribution of Respondents by Disease Condition, Cost Borne by the Insurance Company, and Average OOP Expenditure Incurred by the Patient’s Family for Receiving Treatment, Mumbai and Mumbai Suburban, 2013.

Note. The conversion rate used in this article is US$1 = 61. Dollar value is provided within parentheses. OOP = out-of-pocket.

The OOP payments for treatment of cardiac and cardiothoracic surgery, cardiology, and nephrology averaged at 15,203 (US$249), 5,054 (US$83), and 4,667 (US$77) per capita, respectively. Interestingly, we found that people undergoing treatment for medical oncology, obstetrics, and gynecology did not report any OOP expenditure.

Composition of OOP Expenditure Incurred by RGJAY Beneficiaries

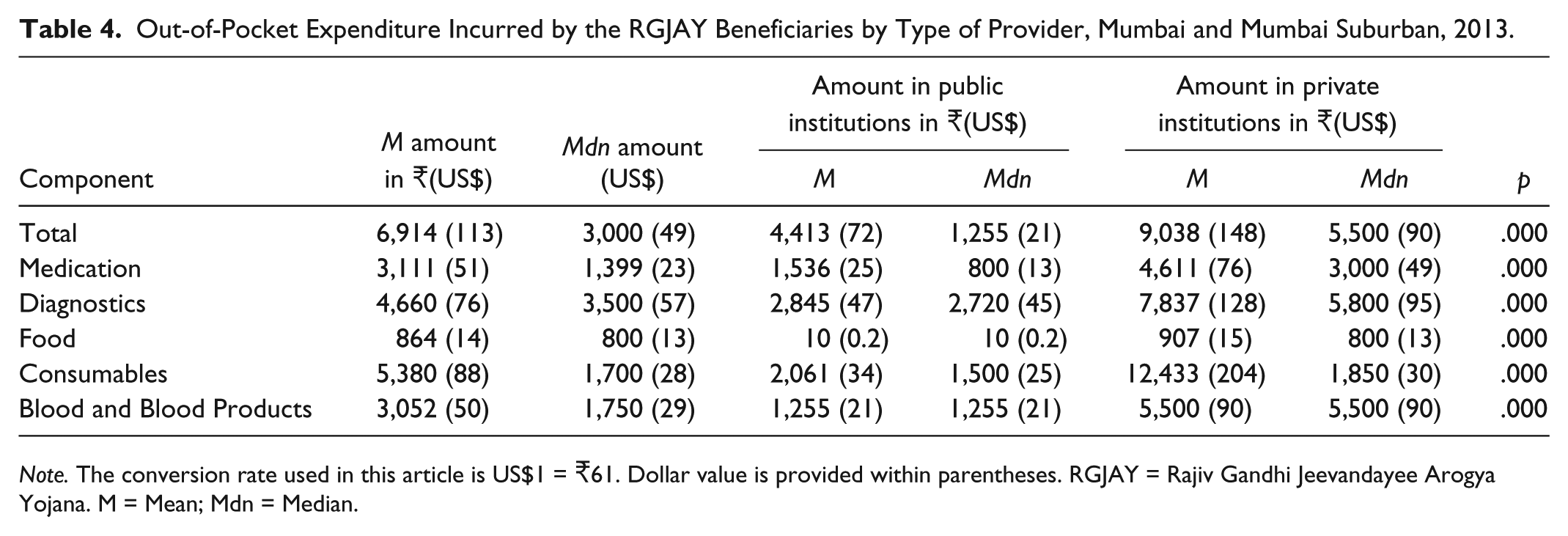

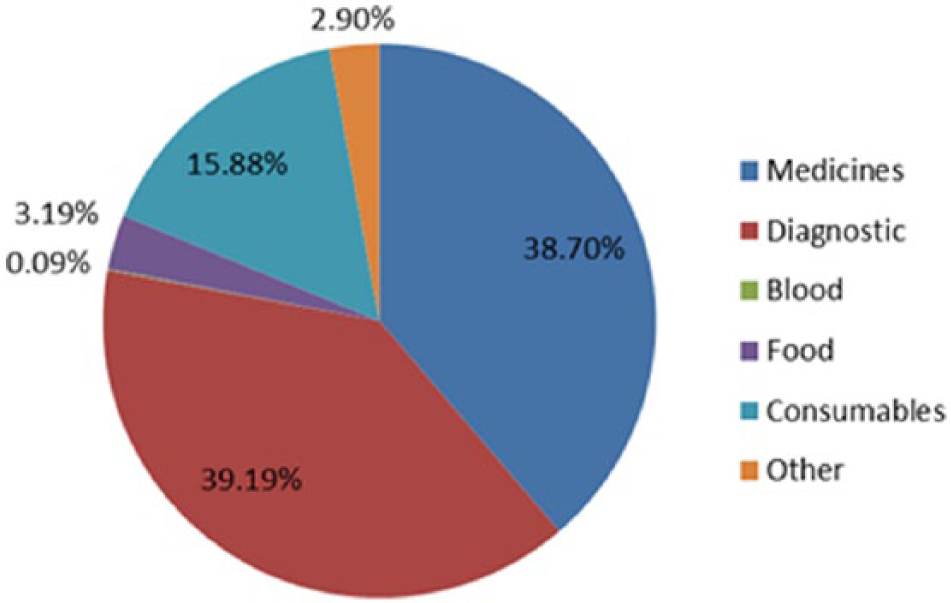

Table 4 gives us the mean OOP expenditure borne by beneficiaries on different components while availing treatment under the scheme. Besides, Figure 4 presents percentage shares of direct OOP payments on medicines, diagnostics, food, consumables, and blood and blood products. The OOP expenditure on diagnostics and medicines was quite substantial in absolute terms as well as a proportion of total OOP payments (39.2% and 38.7%, respectively). Notably, the overall mean OOP spending as well as OOP expenditure on various components of health care services were found to be significantly higher in private hospitals (p < .001) than in public hospitals.

Out-of-Pocket Expenditure Incurred by the RGJAY Beneficiaries by Type of Provider, Mumbai and Mumbai Suburban, 2013.

Note. The conversion rate used in this article is US$1 = 61. Dollar value is provided within parentheses. RGJAY = Rajiv Gandhi Jeevandayee Arogya Yojana. M = Mean; Mdn = Median.

Break-up of the total out-of-pocket expenditure incurred by the RGJAY beneficiaries, Mumbai and Mumbai Suburban, 2013.

Reasons for Paying for Services in Public Hospitals

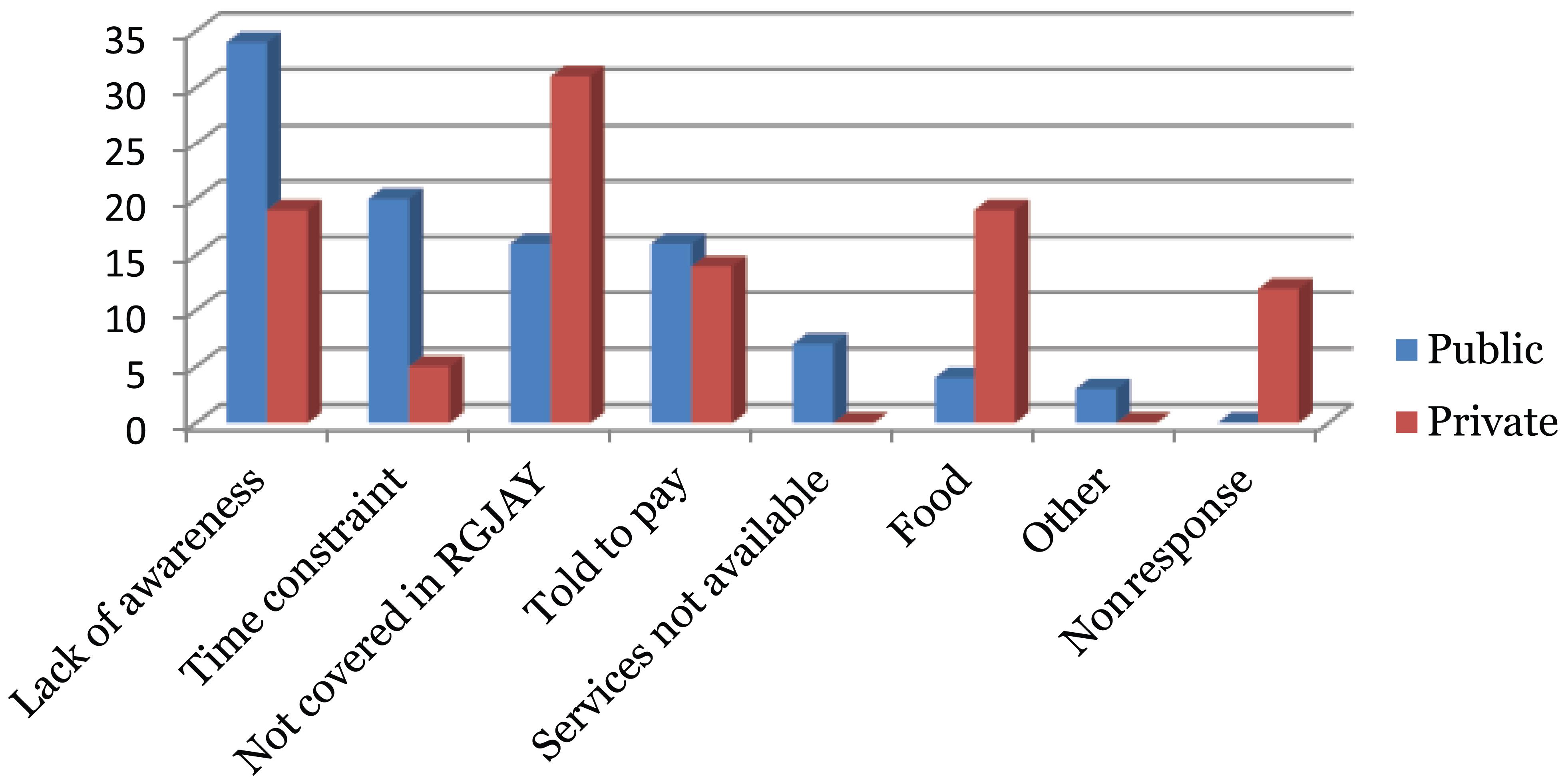

An analysis was carried out among the public and private hospitals on the reasons for incurring OOP expenditure to understand why beneficiaries had to pay for services when admitted in RGJAY empaneled hospitals. It can be seen from Figure 5 that the proportion of those who cited “lack of information” as the reason for paying for services in public hospitals was highest (33%), followed by “unavailability of time to complete all the necessary paperwork” to avail of the services (19%). In these circumstances, patients hardly have any option other than availing diagnostic facilities and medications from outside (private facilities and chemists’ shops) or paying for the services instead of waiting for completing the necessary formalities. The next common reason was that the procedure or comorbidity was not covered under RGJAY and that they had been asked to pay for the services (15% each). Unavailability of the diagnostic tests or medicines in the empaneled hospital was cited as another reason for paying for availing services from nonempaneled diagnostic facilities and medical shops.

Reasons for paying for RGJAY covered health care services in empaneled hospitals, Mumbai and Mumbai Suburban, 2013.

Reasons for Paying for Services in Private Hospitals

The most predominant reasons cited for paying for services in private hospitals (30%) were “procedure was not covered under RGJAY,” followed by “lack of knowledge” (18%). The other reasons were paying for food, “noncooperation from hospital staff,” and “lack of time to complete the necessary paperwork.”

RGJAY reimburses the return travel fare of the beneficiary. Hence, in this study, we only considered the cost of the patient when coming to the service outlet for treatment. Companion cost includes expenditure on travel, food, accommodation, and wage loss of any person who accompanied the beneficiary during his or her hospital stay. While the mean indirect expenditure was 5,711 (US$93.6; Table 5), the mean OOP expenditure including the indirect expenditure incurred by the beneficiaries for treatment under RGJAY turns out to be 12,625 (US$207).

Composition of Indirect Expenditure on Health Care Incurred by the RGJAY Beneficiaries, Mumbai and Mumbai Suburban, 2013.

Note. The conversion rate used in this article is US$1 = 61. Dollar value is provided within parentheses. RGJAY = Rajiv Gandhi Jeevandayee Arogya Yojana. M = Mean; Mdn = Median.

Catastrophic Impact of OOP Expenditure Incurred by RGJAY Beneficiaries

If we take only direct expenditure into consideration, 15% of the sample households experienced catastrophic health expenditure (CHE) because of their OOP spending while receiving treatment at RGJAY empaneled hospitals. However, the incidence of CHE rises to 30% if indirect expenditure is accounted for in the calculation of CHE.

Conclusion

Maharashtra is subsidizing the health insurance premiums under RGJAY to overcome financial barriers to utilization of tertiary care and provide financial risk protection to deprived households against health expenditure. The findings of our study indicate that the scheme has several design and implementational issues.

The analysis revealed that almost half of the RGJAY beneficiaries are actually from the noneligible category with family income higher than 100,000 per annum. This clearly suggests that targeting is a major concern for RGJAY despite the fact that it uses much wider criteria than RSBY and other schemes for providing access to tertiary care to the eligible households. Such unusual high level of leakages was also observed in another study conducted in Maharashtra on RSBY (Ghosh, 2014b). Considering the fact that a large number of vulnerable households are actually not in possession of any of the cards that could prove their vulnerability status (Dreze & Khera, 2010; Swaminathan, 2008), they will not be reached by the health insurance based health system unless the targeting approach is abandoned by the government, and a universal approach is adopted, which also augurs well for the government’s much publicly expressed commitment toward universal health coverage.

Although the cashless feature of RGJAY sounds attractive, evidence indicates that it has not been successful in preventing the prevalence of OOP expenditure. Our estimates suggest that more than three fifths of the beneficiaries incurred a median expenditure of 3,000 (US$49) and a mean expenditure of 6,914 (US$113). These observations are similar to findings from other studies wherein Rao et al. (2012) found that nearly 60% of the “Aarogyashri” beneficiaries in Andhra Pradesh reported a median expenditure of 3,600 (US$59) as OOP payments and Devadasan et al. (2013) observed the median expenditure incurred by the RSBY beneficiaries was 6,000 (US$100). Furthermore, if indirect cost is considered, the average total cost borne by the RGJAY beneficiaries would stand at 12,625 (US$207). The other related finding is that, in contrary to one view that OOP spending is usually concentrated on certain treatment (or surgical) procedures, we observed that there is no such pattern. Importantly, results indicate that BPL families experienced significantly greater financial burden due to OOP health payments than the APL families. This could possibly be attributed to the low level of awareness and empowerment among the people from BPL category.

A notable finding was that the mean OOP spending in private hospitals was more than twice compared with public hospitals. Our analysis also shows that diagnostics and medications together accounted for almost 80% of the total OOP expenditure. The same was observed by Palacious, Das, and Sun (2011), revealing that under RSBY, patients were asked to buy medicines from private medical stores. This suggests that private hospitals may be charging patients for services already covered under RGJAY. Although the patients in public hospitals also had to incur OOP expenditure, the reasons for this were mostly related to administrative lacunae. Another important finding related to the cash payment to the hospitals was the lack of knowledge regarding the complete cashless feature of the scheme among the beneficiaries.

Our study found a low level of awareness about the scheme and its components among the beneficiaries who were hospitalized and utilized the scheme. The level of awareness about RGJAY in the community was assessed by another study conducted in the slums of Mumbai by Shetty (2014) which revealed that less than 12% of the RGJAY-insured households had sufficient knowledge about the various aspects of the scheme (Shetty, 2014). A low level of awareness among the RGJAY-eligible households could either mean that beneficiaries would incur OOP expenditure as they do not know about the facilities they are eligible for and may pay for services which they are entitled to receive for free or some may forego treatment all together because of fear of high OOP expenditure.

The above evidences suggest that awareness campaigns targeting the eligible households need to be carried out not just by media but by including local nongovernmental organizations (NGOs) and self-help groups to make people aware about the scheme’s features and benefits. On admission, hospitalized beneficiaries should be explained by the Arogyamitra about the amount approved, inclusions they are entitled to, and protocols regarding registering complaints. As public hospitals have shown better compliance, it would be prudent on the part of RGJAY to involve more public hospitals under its ambit.

The other major reason for paying for services was unavailability of services in the hospital. Although RGJAY does an audit of the hospital before empaneling it under the scheme, there is no provision if a diagnostic facility breaks down or medicine stock is unavailable in the hospital after empanelment. This issue could be easily resolved if the hospitals are provided some funds in advance by RGJAY so that they can meet the exigencies by tying up with other diagnostic centers or pharmacies to provide cashless services to the beneficiaries.

An unusually high percentage of patients reported paying for diagnostics, medications, and procedures as they were told those services were not covered under RGJAY. It should be noted that this is the reason that was reported by the beneficiaries and has not been cross-verified if this was truly the case. Although it is true that RGJAY has a limited purview of 971 procedures and certain diagnostic procedures, medicines, and comorbidities are not covered under RGJAY, it is highly unlikely that this proportion could be as high as found in our study sample. RGJAY does not seem to have any mechanism in place to check whether the hospital is charging the patient despite already receiving funds courtesy insurance leading to double billing. On admission, the Arogyamitra should explain to the patients if there are any exclusions related to the condition he or she is being treated for. In case of any requirement arising later that is not included in the scheme, it would be advisable if the Arogyamitra informs the patients instead of the hospital staff ensuring that any type of malpractice is avoided.

Finally, we found that the households continue to incur OOP payments even while availing services under RGJAY because of the reasons discussed above. About a third of the beneficiaries experienced financial catastrophe if indirect expenditure is taken into consideration. However, one interpretation is that had there been no insurance scheme for the poor, the proportion of households facing financial catastrophe would be much greater and many of them would have forgone treatment altogether. Thus, it can be said that RGJAY provides some relief to the poor.

Given the fact that precious financial resources are spent for implementing RGJAY, it would be desirable that policy makers take note of the above evidence and do a critical analysis to fully understand the implications of this new financing intervention.

Limitations

The study is based on a relatively small sample of patients, and hence, the generalizability of the findings may be limited. Besides, the method for primary data collection was exit interviews, with the respondents still in close proximity to the health care provider, which may have caused a certain amount of bias in the study.

Footnotes

Acknowledgements

We would like to thank RGJAY society for granting permission to carry out the study. We are also grateful to Dr. Raju Jotkar and Dr. Jitendra Shirname for their valuable inputs and help in conducting the study.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.