Abstract

The aim of this article is to do a scoping review of accountability in the context of social entrepreneurship. Social entrepreneurship is becoming an important business model, while the concept of accountability is prevalent in today’s environment. The scoping review is a type of literature search with certain important distinctions from a literature review. Systematically, the scoping review explores the literature from a relevance viewpoint rather than by evaluating the quality of the research. Then the data are mapped or charted to identify key themes and gaps in the literature. We observe that accountability in social entrepreneurship is viewed and studied in three different ways: as a relationship between parties, as an outcome, or as a predictor variable. We also observe that most of the research is done in the United States, Europe, and Australia. Finally we observe that research methodologies utilized are primarily based around qualitative methods or conceptual descriptions.

Introduction

Social entrepreneurship (SE) is a young but yet vibrant field undergoing conceptual definitions among practitioners and academics (Mair, 2010). As a dynamic business model incorporating elements of commercialism, social involvement, and innovation, tensions inevitably result from conflicting or unclear objectives and responsibilities (Dey & Steyaert, 2012; Teasdale, 2012). In this context, mapping and understanding accountability relationships is likely to be a challenging task (Eisenberg, 2005).

Describing Accountability

Accountability is ambiguous as a term, complex and context dependent (A. P. Williams & Taylor, 2013). From the descriptive sense, it is possible to view accountability in a social context as a holistic framework in the not-for-profit sector, the public sector, or private sector (A. P. Williams & Taylor, 2013). Accountability can also be viewed in a legal, administrative, professional, or social framework (Bovens, 2007).

The academic literature proposes various definitions based on the broader environment in which accountability functions. For example, there are different models of accountability depending on the political, bureaucratic, legal, and business perspectives and along dimensions of vertical, lateral, and diagonal orientations (Bovens, 2007). Accountability has also been defined for individuals as well as for organizations where often the proxy of an individual is used to define the accountability of the organization (Bovens, 2007).

Accountability has been defined as being responsible to an audience with reward or punishment power (Brandsma & Schillemans, 2013, p. 954), or as “the obligation to explain and justify conduct” (Bovens, 2007, p. 9). It often involves a relationship between parties, groups, or individuals and is a mechanism for guiding the behavior of people involved.

One of the ways that accountability is modeled in the literature is from the viewpoint of relationships (Laughlin, 1990; Romzek & Ingraham, 2000). Romzek and Ingraham (2000) have described a “web of accountability relationships” (p. 241) that may create inter-party conflicts and non-optimal solutions. The relationships can be cast in a matrix of four quadrants describing hierarchical, legal, professional, and political relationships classified according to levels of autonomy and positioning of control or expectations (p. 242). Similarly, Behn (2001) and Sorensen (2012) have characterized accountability as a relationship issue between an accountability holder and an accountability holdee.

Brandsma and Schillemans (2013) view the accountability process in terms of outcomes by quantifying the transfer of information, the concentration of bilateral discussions, and the use of power to enforce accountability. They attempt to map “the intensity of all three phases” (p. 960) and create a three dimensional model of accountability within a public institution.

However, Koppell (2005) views accountability as an independent variable that is a predictor of dysfunction in an organization. He defines a typology that includes “transparency, liability, controllability, responsibility, and responsiveness” (p. 94) as elements of accountability. The problem of meeting “conflicting expectations,” according to Koppell (2005), determines the efficiency and effectiveness of problem resolution at an organizational level.

Obtaining a general sense of how accountability is described in the literature is not straightforward. However, from the accountability literature discussed here, three themes seem to be predominant. Accountability can be framed from the viewpoint of relationships, in terms of outcomes, and as predictors of dysfunction.

Describing SE

SE is a recent business construct where the typical entrepreneurship drive for profit is also complemented by an active concern for the environment and social issues (Austin, Stevenson, & Wei-Skillern, 2006). The formation of SE has been described as achieving both financial gain and providing social benefits (Battilana, Lee, Walker, & Dorsey, 2012). Roper and Cheney (2005) have discussed that SE is a “hybrid between private, non-profit and public sectors” (Roper & Cheney, 2005, p. 101). As social constructs, these types of firms are shaped by the environment in which they are launched which is reflected in their definition and the ambiguous terminology that is used around this definition (Dhesi, 2010). In North American society, SE firms generate revenue but yet have a primary drive for social and environmental concerns (Kerlin, 2006). The distinctions between profit-oriented and non-profit SE firms in North America relates to legislative nomenclature that determine a firm’s taxation status (Kerlin, 2006). From the SE field, whether they are considered for profit-oriented or non-profit has been defined by the allocation of those profits or re-investing of those profits into the social venture (Lepoutre, Justo, Terjesen, & Bosma, 2013). In Europe, the business model has traditionally been oriented around community-oriented firms with less concern about the generation of revenue for profit purposes (Kerlin, 2006). In developing countries, SE firms are agents of change that “allows the impoverished . . . to enter the circle of economic and social development” (Mair & Marti, 2007, p. 493). Their institutional impact from the viewpoint of profit orientation has not been extensively studied (Mair & Marti, 2007). Globally across the academic literature, profit-oriented and non-profit firms are currently accepted as models of the spectrum of SE firms (Battilana et al., 2012).

The terminology describing SE is also multi-faceted. Light (2008) examines various components of SE and focuses on the entrepreneurial component of these ventures. Similar definitions are found in research articles by Dees (1998), Lepoutre et al. (2013), and Mair and Marti (2007). However, there are also researchers who equate social entrepreneurial firms with social ventures (Dees & Anderson, 2003), social enterprises (Defourny & Nyssens, 2008; Nicholls, 2009), and other similar terms linked to socially responsible businesses (Yunus, Moingeon, & Lehmann-Ortega, 2010). Consequently, a scoping review within the context of SE will also need to consider some of the possible variations of SE terminology such as social enterprise and social ventures for completeness in the review process.

The Research Problem

The problem of accountability in the SE model is both theoretical and practical. From the theoretical standpoint, the concept underlies the models for governance of a firm. From a practical standpoint, as concerns for environmental and social sustainability increases, improved accountability to the public gains practical relevance. The objective of this study and its research question is to provide an overview or scoping of the type, extent, and quantity of research available in the current accountability literature related to SE. This scoping review will examine the academic literature as it relates to accountability and SE and tease out themes and common ideas. As part of the scoping study methodology, there will not be an exclusive focus on entrepreneurship or entrepreneurs but instead the scoping survey will review articles exploring the SE concept. Exploration of this kind may help to surface gaps in the literature that would need addressing and where no gaps are clearly identified, common trends can be described (Arksey & O’Malley, 2005).

Methodology

The scoping review is a type of literature review but with certain important distinctions. Systematically, the scoping review looks at the literature from a relevance viewpoint rather than by evaluating the quality of the research. This addresses the exploratory nature of a scoping review. Then the data are mapped or charted to identify key themes, and potential gaps in the literature. Finally, a consultation process with subject matter or contextual experts can be optionally used to validate the findings (Arksey & O’Malley, 2005). Arksey and O’Malley (2005) specify five stages to the scoping review. These stages will be integrated throughout this article: “identifying the research question” (p. 23), “study selection” (p. 25), “charting the data” (p. 26), collating and reporting on the results (p. 27). There is a final and optional step of consulting a subject matter expert that may be used if the remaining themes and issues do not identify a gap in the literature (p. 28).

We started the scoping review with a literature search which was conducted to identify peer-reviewed, English language, academic literature that was relevant to this article’s question. Boolean search expressions, as shown in Figure 1, were used to narrow the search results.

Scoping review search methodology.

The initial search used terms that were used to represent SE with the “AND” Boolean operator to capture all of the available literature within the searched databases. Using the term “accountability” focused on articles that were more concerned on accountability rather than accounting-related papers. From the initial results, a different Boolean operator was used to ensure that both terms were within 10 words of each other. In the ABI-INFORM database search, we used “NEAR/10” and in the EBSCO database search we used “N10.” We stayed with the search results from the WEB OF SCIENCE search. Focusing on the full text for ABI-INFORM and the full text for EBSCO, and using the WEB OF SCIENCE search engines ensured that papers focused on both issues of accountability and SE could be selected.

Subsequently the papers were reviewed for duplication and for papers that considered accountability rather than simply mentioned it. The main research questions of the relevant articles were paraphrased or extracted. Their research methodology and the way that “accountability” was used within the paper were listed. Similarities and themes from the theoretical viewpoint were teased out and reviewed.

Accountability articles were grouped according to the three principal themes that were described in the introduction: accountability relationships in SE (Romzek & Ingraham, 2000), accountability as dependent variables or outcomes in SE (Brandsma & Schillemans, 2013), and accountability as independent variables or predictor elements in SE (Koppell, 2005). The themes as listed in Table 1 were determined from reading the articles. The research methodology defined by the content of the articles is listed in the second major column of Table 1 summarized from the detailed listings in the appendix.

Summary of Selection of 27 Research Articles on Accountability Within the Field of SE/Enterprises/Ventures.

Note. SE = social entrepreneurship.

Results

The results described in Table 1 show three main accountability groupings and the methodology used by the researchers. Research questions were listed and whether the articles referred to non-profit/not-for-profit or for-profit firms was reviewed and listed in the appendix. As suggested by scoping review methodology, the articles were not analyzed in depth aside from their initial categorizations (Arksey & O’Malley, 2005).

Our first observation is that there are almost an equal number of articles for each accountability theme, indicating a variety of opinions of how accountability is considered. This is in line with general accountability literature where accountability is modeled as predictors, outcomes, or as the relationship between parties.

Our second observation is that the research methodology utilized in this field is primarily based around qualitative methodology with one article using quantitative methodology and the remaining articles of a conceptual nature. Most of the articles used case study methodology to describe or explore issues related to accountability. This type of qualitative methodology is expected around emerging issues and theories (Yin, 1981) and where “descriptive inferences” with incomplete data need to be made (Gerring, 2004). Given that several of the reviewed papers have focused on accountability as dependent variables or independent variables (outcomes or predictors), one would expect more quantitative studies of accountability in SE.

Another observation is that most of the research is based in the United States, Europe, and Australia with one article’s research originating in Jamaica and another in India. The accountability context is primarily oriented around social and administrative categories rather than political or legal categories (Bovens, 2007). This makes logical sense as this literature deals with the scope of SE activities that tend to be related to small firms involved in social activities (Battilana et al., 2012).

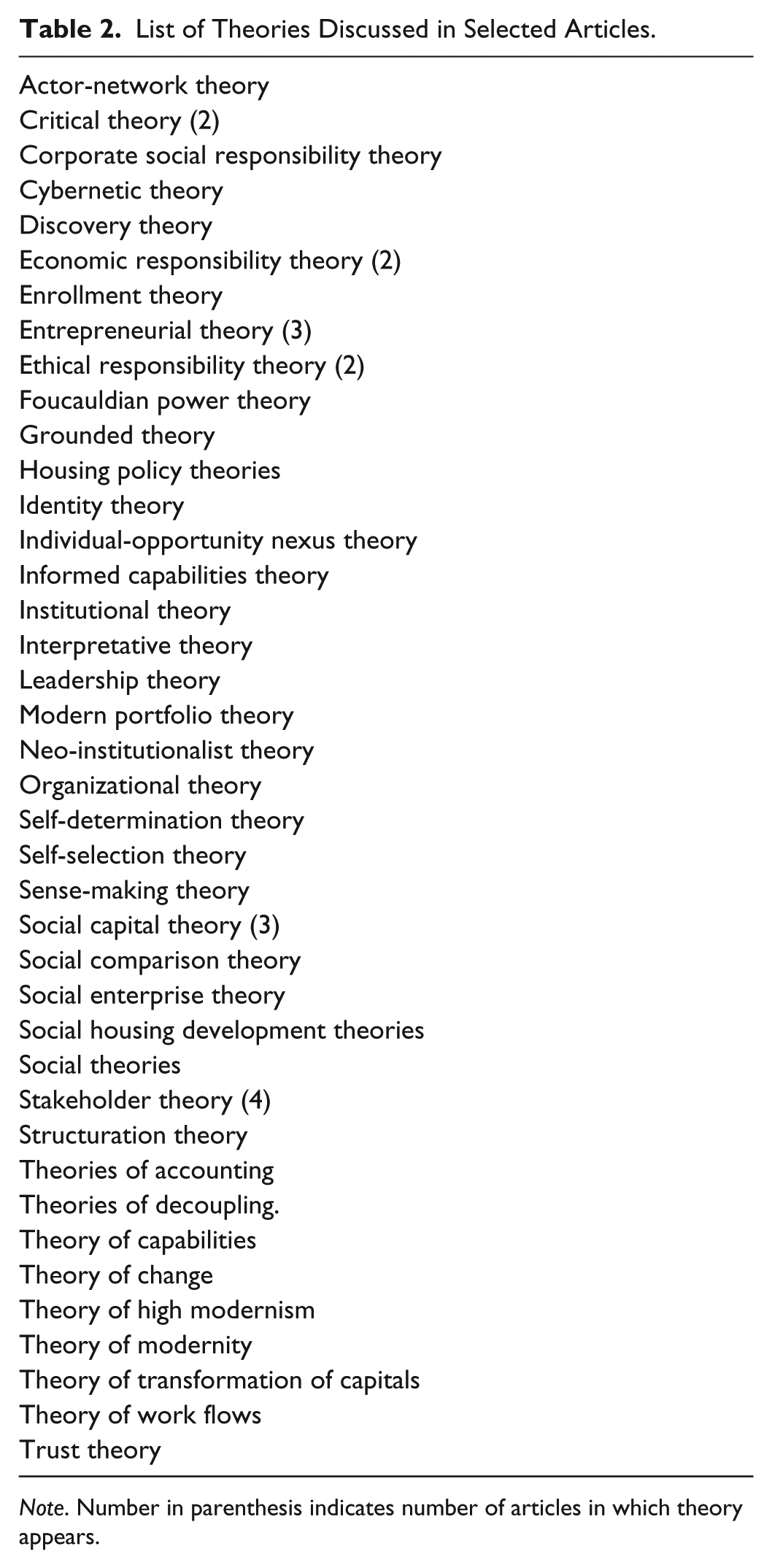

In the next stage, an iterative process as described in scoping review methodology (Arksey & O’Malley, 2005) was applied to the research results to view the results through the lens of different management theories. The results shown in Table 2 indicate the main management theories discussed in the articles as detailed in the appendix. The earliest published articles were from 2001 and 2002 which indicates a young research area. Based on Table 2, certain theoretical areas are represented more frequently: stakeholder theory, social capital theory, entrepreneurial theory, ethical responsibility theory, critical theory, and economic responsibility theory. Mainstream theories such as agency theory, stewardship theory, and institutional theory have previously been advanced as important theories to consider in the consideration of accountability (Mansouri & Rowney, 2014). Interestingly, neither stewardship theory nor agency theory were mentioned in any of the 27 articles. This could indicate the potential for additional research on accountability in SE using other theoretical perspectives.

List of Theories Discussed in Selected Articles.

Note. Number in parenthesis indicates number of articles in which theory appears.

Discussion

The objective of this study was to provide an overview of the type, extent, and quantity of research available on current accountability literature related to SE through a rapid gathering of literature and a mapping of the results. Arksey and O’Malley (2005) identify this technique as one that identifies research gaps without necessarily commenting on the quality of the extant research. Davis, Drey, and Gould (2009) suggest that the limits of the technique be clearly specified to improve the usefulness and applicability of the results. In the following discussion, the results will be analyzed and the limitations of the analysis will be presented.

This scoping review looked at accountability in social entrepreneurial settings and determined that this field of study has not been extensively researched. Of the 890 peer-reviewed articles dealing with accountability and some version of SE terminology, only 27 relevant articles were found from a search of the EBSCO, Proquest ABI-INFORM, and WEB OF SCIENCE databases that integrated both concepts. Our search methodology could have missed papers that did not describe accountability and SE within the number of words and with the terminology for SE that were defined in our search algorithm.

Our search methodology also included a manual revision of the 65 articles that were generated prior to narrowing the relevant articles to 27 (shown in Figure 1). During this revision, we were subjective in our interpretation of both the context of SE and how accountability was described within this context. As a limitation of this review, it is possible that we may have excluded some of the articles because of their marginal inclusion of accountability or marginal context of SE according to our interpretation of the concepts.

We found that there are gaps relating to the inclusion of theories that are described in the accountability literature resulting from our search. In particular, we could not find discussions of agency theory or stewardship theory. Agency theory has been described as driving accountability relationships (Bovens, 2007; Brandsma & Schillemans, 2013). Stewardship theory, institutional theory, and agency theory are also described within the context of accountability (Mansouri & Rowney, 2014). From the results of the scoping survey, accountability in a SE setting may derive more of its work from theories related to social dimensions such as stakeholder theory, social capital theory, and ethical responsibility theory among the others shown in Table 2.

This scoping review reveals that the literature on accountability of SE is still scarce. Dees (1998) in describing one of the five main roles of a SE firm discussed that they should be “exhibiting a heightened sense of accountability to the constituencies served and for the outcomes created” (Dees, 1998, p. 4). The different ways of defining accountability within the SE context shows that researchers are examining various facets of this variable using qualitative and conceptual articles. Accountability can be viewed as a predictor, as an outcome, or as the context or relationships in which SE operates.

We found that the articles selected did not specifically focus on defining accountability except for the article by Achleitner, Lutz, Mayer, and Spiess-Knafl (2013) who defined “voluntary accountability” (p. 105). We found that the other articles focused on the application of accountability practices in the SE context rather than focus on the conceptual definition of accountability.

Academic researchers continue to debate accountability in SE. There are ample opportunities to continue researching this area and contribute further to SE literature. We highlight some of the potential research areas.

Further research is needed to examine accountability in relation to the governance of the SE. Like any other corporations, social entrepreneurial firms need to be transparent in all aspects of their governance. They need to demonstrate accountability to their shareholders, as well as to stakeholders within and outside the firm. They need to deal with issues such as conflicting expectations and multiple accountabilities through proper governance structures. Good governance requires proper provision of information, proper debate of issues, and proper decision-making structures and processes. Even though governance of firms have been the subject of several studies, the specific characteristics of SE in relation to multiple expectation and accountabilities justify further studies of governance in the context of SE.

From the firm’s perspective, it is important to understand how accountability issues are raised, challenged, and resolved. When is accountability a predictor, an outcome, or a nexus of relationships? Further studies of how accountability is enacted in the context of SE are necessary to help practitioners design and implement proper governance structures.

From the social perspective, accountability in the context of SE implies multiple accountability scenarios. We expect that these relationships may be fluid in the context of a dynamic SE model and that they will impact the SE firm. What theory can be used to model multiple accountability scenarios and how can this be empirically described and measured?

From the critical perspective, accountability and SE can be researched from the viewpoint of whether SE should even be considered a business model as it is mostly assumed in the current literature search. Some critical perspectives discuss SE as extending beyond the business model (Hjorth, 2013) and as “a zero-sum game” (Teasdale, 2012, p. 515). Accountability in this critical context could be explored using institutional theory or stakeholder theory to account for their multiple accountability relationships.

The extant literature utilizes many organizational theories to explain that behavior results from control mechanisms, including accountability, whether formal or informal. Behavior takes place in a social context and is influenced by mutual exceptions, norms, and mutual patterns of behavior. More research is needed to understand the relationship between accountability and decision-making, how accountability guides behavior of a social entrepreneur, and what processes are implemented within a SE to enable accountability.

Conclusion

The purpose of this scoping review was to identify gaps without doing an exhaustive review of the literature. One of the gaps identified related to a lack of homogeneity in the theories used. The other main gap that was identified related to a lack of empirical and more specifically quantitative research on accountability in the social entrepreneurial sector.

Through this scoping review, we also identified multiple definitions of accountability in the context of SE. The lack of agreement in defining accountability as a theoretical construct and the lack of homogeneity in its operationalization in the research papers that were identified show both an opportunity and a challenge. The opportunity is to identify the specific SE context where accountability is most important. The challenge lies in that accountability as a construct may require anchoring to a particular theory to be able to define its relationship in the SE context.

SE continues to be a vibrant field and mapping accountability within this field is unexplored. This scoping study provides a launching pad for further conceptual and empirical research of accountability within SE.

Footnotes

Appendix

List of 27 Research Articles on Accountability Within the Field of Social Entrepreneurship/Enterprises/Ventures.

| Authors | Research question/objective | Type of research | Accountability as |

|---|---|---|---|

| El Abboubi and Nicolopoulou (2012) | “With our research question, we aim to understand the stakeholder-involvement process in certification projects. We are not testing a pre-conceived hypothesis but rather enabling enrichment of the theoretical framework from the data. A key part of our methodology is a qualitative analysis of organizational behaviour—that is, how managers, employees, and external stakeholders make sense of the involvement process.” (p. 402) | Qualitative case study | The context within which stakeholder involvement is investigated |

| Barkan (2013) | “The mega-foundations have the resources to shape public policy but they have no accountability to the public or to the people directly affected by their programs.” (p. 637) | Conceptual article | As part of the context in the operation of megafunds/big philanthropy |

| Birch and Whittam (2008) | “The present paper highlights the current government emphasis on public service delivery in Third Sector policy, especially in relation to regional development, and how this might prove detrimental to the promotion of social capital.” (p. 439) (For Peer Review) | Conceptual article | As part of the context of Third Sector definitions and conceptualizations including social enterprise, social entrepreneurship, and social economy |

| Gao and Zhang (2006) | “The key objective of this paper is to explore the applicability of social auditing as a practical approach to engage stakeholders in assessing and reporting on corporate sustainability, with a focus on the framework of AA1000 and the dialogue-based social auditing model.” (p. 724) | Conceptual article | As part of the context in defining AA1000 |

| Grimes (2010) | “The purpose of this article is to explore how organizations within the social sector are constructing the new organizational identity of these SEOs.” (p. 763) | Qualitative case studies | As contextual in the process of social entrepreneurial sense-making |

| Harman (2008) | “What are the factors associated with successful social entrepreneurship?” (p. 201) | Qualitative case study | As contextual in defining social entrepreneurship |

| Herranz, Council, and McKay (2011) | “The purpose of this article is to suggest that the concept of a tri-value social enterprise represents a distinctive type of social enterprise.” (p. 830) | Qualitative case study | As a contextual side issue to defining success of social entrepreneurial firms |

| Ottinger (2008) | Conceptual paper discussing philanthropy from the viewpoint of its impact on non-profit firms. | Conceptual article | As part of the context of a policy discussion |

| Shinde and Shinde (2011) | “The current study aims at exploring this spiritual form of entrepreneurship, a phenomenon that has largely escaped the notice of researchers in entrepreneurship studies as well as religion and spirituality.” (p.73) | Conceptual article | As part of the context (a control variable) in spiritual entrepreneurship |

| D. A. Williams and K’nife (2012) | “It raises the question as to whether or not all enterprises that deliver a social service can be duly classified as social enterprise and be linked to the wider field of social entrepreneurship.” (p. 63) | Qualitative case study | As part of the context of social entrepreneurship |

| Albareda, Lozano, and Ysa (2007) | “The objective of the research has been to develop an analytical framework that enables us to understand, through a more adequate methodology, the approaches and perspective of governments in designing and implementing public policies to promote CSR.” (p. 392) | Conceptual and qualitative content analysis of government policies | One of the outcomes of government CSR policies |

| Arvidson and Lyon (2014) | “The paper examines how social impact measurement can be used by resource holders to exert control over funded organizations.” (p. 871) | Qualitative case study | As an outcome of measurement processes |

| Blessing (2012) | “This exploratory contribution aims to expand the conceptual basis for research into the rise of not-for-profit social entrepreneurs in the housing market.” (p. 190) | Qualitative case study | As an outcome of frameworks of hybrid identities |

| Manetti (2014) | “The aim of this paper is to analyze the role of BVA in the evaluation of socio-economic impact of SEs with particular reference to the measurement model denominated ‘SROI analysis.’” (p. 446) | Conceptual article | As an outcome of the use of accounting tools |

| Sang (2004) | Conceptual discussion of health care organizations and accountability systems from the viewpoint of stakeholders. | Conceptual article | As an outcome of health care policies |

| Tracey, Phillips, and Haugh (2005) | “We describe the emergence of community enterprise as a distinctive organisational form in the UK. Finally, we discuss the implications of these partnerships for managing stakeholder relations and addressing the moral obligations that are increasingly placed on corporations by a range of social actors.” (p. 329) | Qualitative data using archival CIC data | As an outcome of CIC structure in the United Kingdom |

| van Overmeeren, Gruis, and Haffner (2010) | “In this article we aim to clarify the different functions of performance assessment, the different ways of designing the instrument, and the effects of performance assessment in relation to its functions, drawing on experiences in the Netherlands and England.” (p. 141) | Qualitative analysis using archival and case study sources | As an outcome of performance assessment systems |

| Smith (2010) | Policy paper discussing the relationship between government and social enterprises. | Conceptual article | As an outcome of public policy |

| Krauskopf and Chen (2010) | Policy paper discussing the principal–agent relationship between government and service/contract providers. | Conceptual article | As an outcome of public policy. |

| Darby and Jenkins (2006) | Developing sustainability tools and social accounting indicators for a social enterprise. | Qualitative case study | As an outcome of the application of measurement tools |

| Achleitner, Lutz, Mayer, and Spiess-Knafl (2013) | “What are important aspects that social venture capitalists focus on when judging the integrity of a social entrepreneur? Are internal factors, i.e., characteristics and efforts of the entrepreneur, or external factors such as judgments of third parties particularly relevant? How does experience influence the assessment of integrity?” (p. 96) | Quantitative experimental study | The predictor variable in an experiment determining the integrity of a social entrepreneur |

| Cornelius, Todres, Janjuha-Jivraj, Woods, and Wallace (2008) | “We pose the question: what frameworks might social enterprises employ to ensure that attention is paid to internal CSR, especially concerning employees’ organisation and career development and quality of life needs?” (p. 356) | Conceptual article | As a predictor of CSR |

| Larner and Mason (2014) | “There are increasing calls for more diverse (and qualitative) empirical studies of many aspects of social enterprise, and this naturally supports innovations in conceptual developments (Low, 2006; Spear et al., 2009). This paper works towards the second goal, presenting the findings from a small study of social enterprise governance in the UK.” (p. 181) | Qualitative thematic/content analysis of interviews | As a predictor of good corporate governance |

| Nicholls (2010) | “The research uses these approaches to examine the disclosure and reporting mechanisms designed for CICs in terms of the ‘regulatory space’ (Hancher & Moran, 1989) within which a range of key actors and discourses interacted to institutionalize the new legal form’s reporting and disclosure practices. Of particular significance here are the boundary factors that determine the regulatory context within which disclosure logics are negotiated and practices subsequently established” (p. 395) | Qualitative content analysis of archival case studies | As the predictor of reporting practices |

| Partzsch and Ziegler (2011) | “Here, we examine the role and potential of one such agent—the social entrepreneur—and we focus on one important sector for sustainable development—the water sector. In what sense are social entrepreneurs change agents in the water sector? What, if anything, gives these agents authority to pursue these social and environmental goals? . . . If social entrepreneurs are change agents, what might be the legitimating reasons that transform power into authority?” (p. 64) (For Peer Review) | Qualitative-field survey, case study, archival content analysis | As a predictor of social entrepreneurship involvement in water development |

| Purdue (2001) | “Local residents of the neighbourhood and collaborative social capital in the regeneration partnerships. This focus is intended to throw some light on the question of whether such community leaders can play an effective leadership role in their neighbourhoods and in the partnerships.” (pp. 2211-2212) | Qualitative case study | As a predictor in social capital accumulation. |

| Wagner (2002) | Conceptual discussion of philanthropy and the role of donor involvement | Conceptual article | As a predictor of donor/philanthropist involvement |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.