Abstract

Sexual violence can trigger adverse economic events for survivors, including increased expenses and decreased earnings. Using interview data, this exploratory study examines how access to assets (liquid assets, familial financial assistance, and homeownership) affects survivors’ economic well-being during recovery. In keeping with asset theory, liquid assets and familial assistance can help offset post-assault expenses and facilitate access to services. Homeownership, meanwhile, appears to have mixed effects on survivors’ economic well-being. These findings suggest that the economic costs of sexual violence can burden survivors with fewer financial resources more heavily than those who own significant assets. As such, these findings shift the focus toward a dimension of inequality in recovery from sexual violence that is often overlooked in research and that may have implications for public policy and victim services.

At age 27, Lil’ Miss had recently embarked on a career in law enforcement, and she was thriving. After enduring a violent rape, her performance at work suffered, and she lost her job. Unable to work due to trauma, Lil’ Miss used her “three to four thousand dollars” in savings to support herself for a year and a half until she was able to work again. She also relied on her brother and a close friend for financial assistance when money grew short during her long recovery. As Lil’ Miss’ story suggests, sexual assault often triggers increased expenses (Miller, Cohen, & Weirsema, 1996), barriers to work (Loya, 2014a), and decreased earnings for survivors (Macmillan, 2000). Lil’ Miss’ experience also illustrates how assets, such as savings and financial assistance from family and friends, can help survivors to weather economic difficulties in the wake of sexual assault. Research in the field of asset development suggests that modest financial assets can stabilize households facing adverse financial events of this kind (Sherraden, 1991). However, few studies have empirically examined whether financial assets play a role in recovery from sexual violence, and qualitative research on this issue is particularly scarce.

To address this gap in the literature, this study uses asset theory and analysis of 27 in-depth interviews with sexual assault survivors and rape crisis service providers to examine how access to assets can impact survivors’ economic and overall well-being. Three types of asset are considered: liquid assets, financial assistance from family or friends, and homeownership. This exploratory research makes two contributions to the field’s understanding of sexual assault and recovery. First, this study suggests that financial and familial assets can help to buffer the financial costs of sexual violence and facilitate access to services. Second, by highlighting the potential value of assets for survivors, the findings suggest that the negative economic consequences of sexual violence may burden survivors with fewer financial resources more heavily than those who own significant assets. As such, these findings shift the focus toward a dimension of inequality in recovery from sexual violence that is often overlooked in research and that may have important implications for public policy and victim services.

Sexual violence can take many forms, including rape, attempted rape, and unwanted sexual contact or threats. In this article, the terms sexual violence and sexual assault are used interchangeably to refer to this inclusive definition of rape and other sexually violent experiences. The present study focuses on isolated sexual violence, which is defined as sexual violence that is not part of a pattern of abuse by an intimate partner. (For more information on this definition, see Loya, 2014a).

Economic Impact of Sexual Violence

Researchers have documented a range of economic impacts of sexual violence, including increased expenses and effects on employment and earnings. First, Miller and colleagues (1996) estimated that each rape or sexual assault (excluding child abuse) costs US$87,000: US$5,100 in tangible losses (e.g., lost productivity, medical care, police services) and US$81,400 in lost quality of life in 1993 dollars. This translates to US$142,533 in 2014 dollars (U.S. Bureau of Labor Statistics, 2015; for state-level estimates, see also Post, Mezey, Maxwell, & Wibert, 2002). Notably, survivors are often personally responsible for a share of these expenses, including the costs of medical and mental health care and lost wages (Chrisler & Ferguson, 2006). In addition, there is evidence that some sexual assault survivors need to move residences (Elklit & Shevlin, 2009), which may trigger housing-related costs such as the security deposit and first and last months’ rent.

Second, sexual violence can affect survivors’ employment and reduce their lifetime earnings. Survivors of sexual violence often require time off from work (Tjaden & Thoennes, 2006) and suffer from higher rates of unemployment compared with non-victims (Byrne, Resnick, Kilpatrick, Best, & Saunders, 1999). Indeed, Loya (2014a) uncovered numerous negative employment consequences of isolated sexual assault—including unpaid time off, diminished performance, job loss, and inability to work—all of which can lead to lower earnings. Similarly, MacMillan (2000) found that sexual victimization during adolescence can diminish survivors’ educational and occupational attainment, leading to lower earnings in adulthood.

These economic consequences of sexual assault are similar to the negative financial effects of intimate partner violence (IPV), which can include physical or sexual violence, control tactics, and economic abuse (Adams, Tolman, Bybee, Sullivan, & Kennedy, 2012; Browne, Salomon, & Bassuk, 1999; Lloyd & Taluc, 1999; Raphael & Tolman, 1997; Romero, Chavkin, Wise, & Smith, 2003). In the IPV field, there is also evidence that financial stability and homeownership are associated with lower rates of violence (Benson, Fox, DeMaris, & Van Wyk, 2003; Brownridge, 2005; Christy-McMullin, 2006; Fox, Benson, DeMaris, & Van Wyk, 2002; Page-Adams, 1995; Rennison & Welchans, 2000), suggesting that asset ownership may be a protective factor against IPV. In recent years, policymakers and service providers have developed asset building and financial education programs for IPV survivors, with the goals of increasing their financial independence, self-esteem, and safety (Sanders & Schnabel, 2006, 2011; Sanders, Weaver, & Schnabel, 2007). This research and practice may have implications for survivors of sexual violence outside the context of IPV; yet few researchers have considered the relationship between assets and non-IPV sexual violence. Thus, it is worth considering whether access to financial assets can buffer the economic impacts of isolated sexual violence, including non-IPV sexual assault.

Asset Theory and Related Literature

Asset theory contends that asset ownership can play a crucial role in cushioning economic shocks such as job loss, divorce, or unanticipated medical bills (Sherraden, 1991). This cushioning can mean the difference between long-term economic stability and the cyclical revisiting of poverty. Asset theory also suggests that asset ownership is associated with psychological and physical benefits and that it can have a transformative effect on a family’s class status. Although prior asset research has not addressed sexual assault as a cause of economic shocks, the research outlined above demonstrates that such violence may indeed trigger unanticipated expenses and lost wages. Thus, the principles of asset theory suggest that assets may play an important role in survivors’ recovery from sexual violence.

Assets may be tangible possessions (e.g., savings, real estate) or intangible resources (e.g., social and human capital; Sherraden, 1991). As Chang (2006) summarizes, assets offer many benefits that income does not: Wealth can be transferred to others, can generate income (through interest, capital gains, and rent, for example), can be used as collateral for loans and provides the ability to weather common financial crises, such as spells of unemployment or illness, in which income is temporarily disrupted. (p. 112)

The children and other kin of asset owners benefit from their relatives’ wealth via financial support, gifts, and inheritance (Chiteji & Hamilton, 2005; Oliver & Shapiro, 1995; Shapiro, 2004). Similarly, social capital—one’s social network—can also be an asset. For example, in times of need, rather than relying on public benefits and charities, those with strong social networks can turn to friends and relatives for emergency housing or help paying bills (Edin & Lein, 1997).

While it is intuitive that those with greater resources are better positioned to recover from economic challenges, research suggests that even in relatively small amounts, assets can significantly improve a household’s financial stability in the face of adverse events. For instance, researchers define asset-poverty as having inadequate liquid assets to support one’s household for 3 months at the federal poverty level. To be above the asset–poverty threshold (“asset-owners”), a family of four would own at least US$4,000 in 1997 dollars, or US$5,900 in 2014 (Haveman & Wolff, 2004; U.S. BLS, 2015). McKernan, Ratcliffe, and Vinopal (2009) found that asset owners are less likely to experience material hardship following an economic shock than are asset-poor households. For example, asset owners who experience involuntary job loss are much less likely to face food insecurity as a result, in part because they can spend their assets to maintain their former level of consumption (see also Keating, 2012). Importantly, McKernan and colleagues also found that assets have the largest protective effects for families in the two lower thirds of the income distribution, even though they own significantly smaller dollar amounts than the top third. To the extent that sexual violence creates economic shocks, assets may help cushion such adverse financial effects even for low-income survivors.

In addition to providing a cushion in the case of financial emergencies, asset ownership is associated with improved health and well-being for individuals, families, and neighborhoods. The beneficial byproducts of asset ownership, known as asset effects, include improved life satisfaction, a greater sense of control over one’s life, increased future orientation, children’s improved educational performance, and better health (Moore et al., 2001; Page-Adams, Scanlon, Beverly, & McDonald, 2001; Rohe & Stegman, 1994; Yadama & Sherraden, 1996; Zhan & Sherraden, 2003). Homeownership is also associated with lower rates of IPV (Brownridge, 2005; Christy-McMullin, 2006; Page-Adams, 1995; Rennison & Welchans, 2000).

The literature on assets and isolated sexual violence is limited. Loya (2014b) makes a theoretical argument that asset ownership may be both a protective factor for sexual violence and help survivors to recover because women can leverage their assets to increase safety and to access supportive services. Similarly, Myhill and Allen (2002) found that the prevalence of rape among British women living in owner-occupied housing is half that of women in the private rental sector and one quarter that of public housing residents. This may suggest that homeownership has a protective effect against rape, as with IPV. However, these differences may also be explained by other housing or neighborhood characteristics, such as crime rates, social norms, or police attention. In addition, Ullman (1996, 1999) documented an association between social support and improved recovery from rape, but researchers have not considered financial assistance from family and friends as a type of social support. At present, no empirical research has examined whether asset effects extend to the well-being or recovery of sexual assault survivors. The present exploratory study begins to address a gap in the literature by considering whether and how asset ownership affects sexual assault survivors’ well-being during recovery.

Method

Participants

The data for this study are drawn from in-depth, semi-structured interviews with 18 rape crisis service providers and 9 sexual assault survivors. These two groups of participants offer distinct and valuable perspectives on the research question. Through their experience helping survivors overcome various post-assault barriers, rape crisis service providers have access to a wealth of knowledge about the needs of sexual assault survivors during recovery. Importantly, rape crisis service providers can offer information about patterns they have observed among the many survivors with whom they have worked over time. As a key feature of assets is their ability to prevent financial strain, service providers are well situated to detect such effects by comparing among their clients. Sexual assault survivors can speak to the economic impact of sexual violence in their own lives and whether assets played a role in their recovery. This sampling strategy allows for triangulation among different types of providers as well as between providers’ and survivors’ perspectives (Krefting, 1991; Lincoln & Guba, 1985).

I used a purposive sampling technique to recruit service provider participants in two metropolitan areas in a northeastern state. The sampling objective was to interview providers from a range of locations in the rape crisis service network so that respondents could speak to the experiences of survivors who enter the service system at various points, seeking a variety of services. I identified rape crisis agencies through referrals from the Department of Public Health and the state’s largest rape crisis center. I recruited providers who had worked directly with survivors of isolated sexual assault and who reported having knowledge of the economic dimension of sexual violence for their clients. While some providers worked with survivors of multiple kinds of violence (IPV, child sexual abuse, and isolated sexual assault), the interviews focused on the impact of sexual violence that was not part of a pattern of abuse.

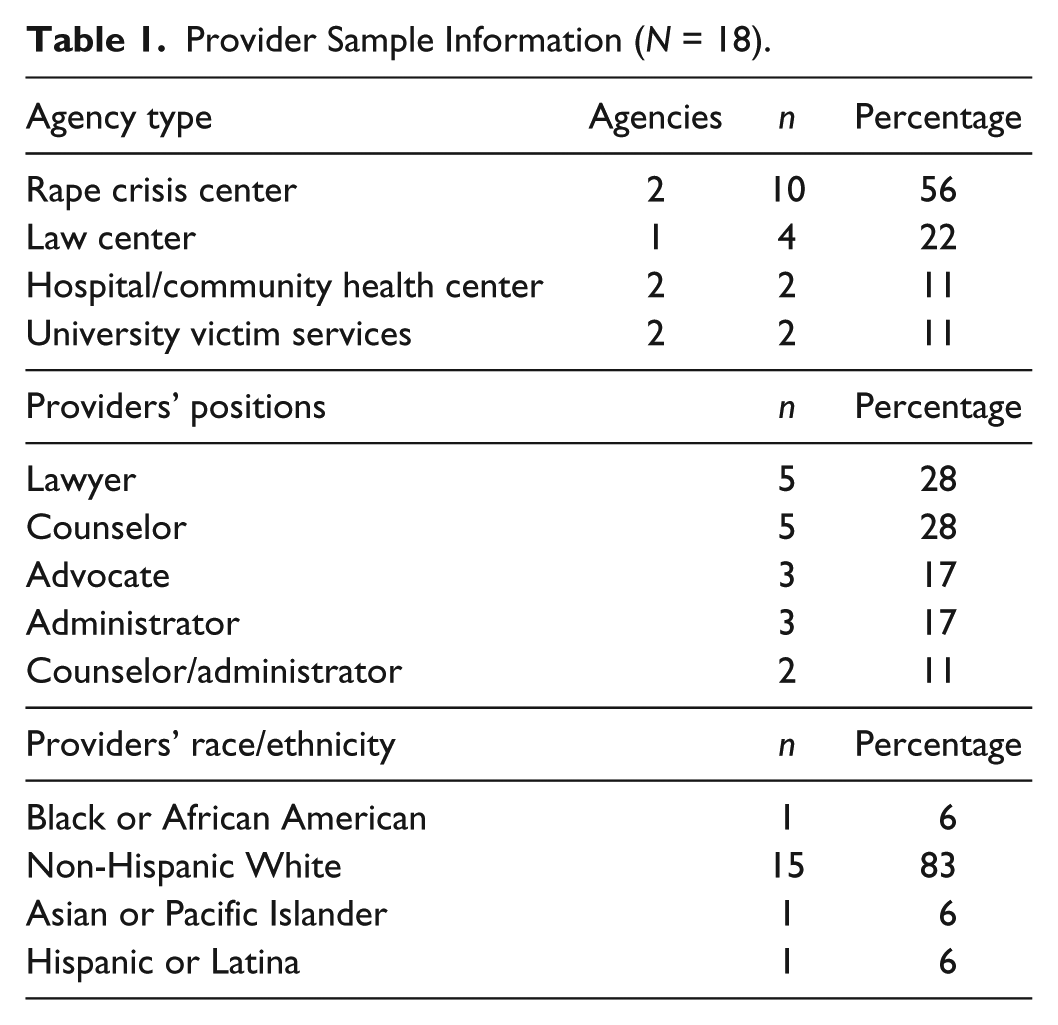

I interviewed 18 service providers from seven agencies, as noted in Table 1. Within each of these agencies, I interviewed a director plus one to three staff members from each department or specialty area, depending on the size of their staff and scope of their services. Agencies offering more services are more heavily represented in the sample. Providers included lawyers, counselors, advocates, administrators, and those holding dual roles. Providers had an average of 10.5 years of experience in the rape crisis field, with a range of 16 months to 20 years. The majority of provider participants (15) were White, which generally reflected the demographics of their agencies. The providers served survivors at all stages of recovery, from immediately post-assault to decades later, so participants offered various perspectives on the recovery trajectory.

Provider Sample Information (N = 18).

I used a convenience sampling technique to recruit survivor participants. I posted flyers at local service provider agencies, college campuses, and a women’s community center. The Department of Public Health sent an e-mail announcement to its statewide listserv, and rape crisis agency volunteers and staff disseminated the announcement to their networks as well. I recruited survivors who were age 18 or older and self-identified as victims or survivors of isolated sexual assault, using the study’s definition: rape, attempted rape, or other unwanted sexual contact or threats since the age of 12, which is not part of a pattern of abuse. Note that this definition includes both assaults committed by non-intimates (e.g., strangers or acquaintances) and violence committed by intimate partners that was not part of a pattern of abuse (e.g., a single rape by an otherwise non-violent husband). In addition, while members of the sample may have also experienced a pattern of IPV or child abuse, the interviews focused on the isolated sexual assault(s) each survivor had experienced since the age of 12. This age threshold was based on the criteria used by the state’s largest rape crisis center, which offers services to survivors age 12 or over and refers younger victims to a child-specific service provider. At least 1 year must have lapsed since the survivor’s most recent sexual assault, with no upper time limit. This way, different survivors could speak about both their long- and short-term experiences of recovery.

I conducted interviews with 10 female survivors, 1 of whom was excluded from the final sample because she viewed her rape as part of a pattern of abuse by an intimate partner. The survivors’ basic demographic information is noted in Table 2. At the time of the interview, survivors’ income levels ranged from less than US$15,000 to more than US$105,000 annually, while their households ranged in size from 1 to 4 persons, with a mean of 2.4. Eight of the 9 survivors had been raped, while the 9th experienced a non-rape sexual assault. The mean number of lifetime sexual assaults was four. Most of the assault incidents were committed by people known to the survivors (acquaintances, intimates, or family members), but about half of the participants (5) had been assaulted by strangers. Survivors were between 18 and 32 years old (with a mean of 24) at the time of their most recent assault. The mean number of years since the most recent assault was 17, with a range of 2 to 31. To ensure confidentiality, pseudonyms are used for survivors, and identifying details have been changed or omitted.

Survivor Sample Information (N = 9).

These numbers exceed the survivor sample size (9) because some survivors were assaulted by more than one perpetrator.

Data Collection and Analysis

All interviews were conducted by the author and followed an interview schedule that was developed as part of a larger project examining the impact of sexual assault on survivors’ financial well-being. In the interviews, participants answered questions about what expenses arose in the wake of sexual violence and how survivors paid for these costs. Drawing on Shapiro’s (2004) qualitative approach to the study of asset ownership, I also asked participants whether they (or their clients) had access to three major types of assets: (a) liquid assets, (b) financial assistance from family or friends, and (c) homeownership. Those who reported that they (or their clients) had access to assets were also asked whether and how each type of asset affected the survivor’s experience post-assault. Survivors who had experienced multiple isolated sexual assaults were asked about the role of assets in recovery from each assault. Providers and survivors were asked questions on the same topics, with the exception of information related to personal experiences with sexual violence and certain demographic items. Interviews were conducted in person at a location of the participant’s choosing or by phone between January and July of 2011. The interviews lasted from 40 min to 2 hr, with most lasting 60 to 90 min.

To analyze the interview data, I used open and focused coding, which is a form of thematic analysis that combines inductive and deductive inquiry (Emerson, Fretz, & Shaw, 1995). Using Atlas.ti software, I coded the data on both a priori expectations (derived from the literature) and ideas that emerged from participants’ stories. A priori codes include asset type, asset amount, and asset effect (an asset’s reported impact on the survivor’s ability to cover new expenses, afford services, or endure an economic shock). Examples of inductive codes include assets improving survivors’ flexibility with work and homeownership as a double-edged sword. Next, I analyzed the data by asset type and identified different themes for liquid assets, familial assistance, and homeownership. Finally, I examined the coded data for triangulation or divergence among various types of providers and between providers and survivors. In general, there was a high degree of consistency between the groups’ responses. The analysis was verified at each stage using peer examination and debriefing (Krefting, 1991; Lincoln & Guba, 1985). Although the small sample size limits the generalizability of these findings, the rich data offer insight into the roles of financial and familial assets in recovery from sexual violence.

Findings: The Role of Assets in Recovery From Sexual Violence

The majority of providers (15 of 18) and survivors (8 of 9) reported that assets—liquid assets, familial financial assistance, or homeownership—have a positive impact on some aspect of survivors’ post-assault well-being. However, the three asset types seem to affect survivors’ well-being differently. The data suggest that liquid assets and familial financial assistance can help survivors to weather economic shocks and boost their sense of control and security, while homeownership can have mixed effects on survivors’ economic and overall well-being.

Liquid Assets

Respondents consistently reported that survivors benefit from access to liquid assets, which include savings, stocks, and bonds. Most providers (11 of 18) reported that their clients had drawn upon liquid assets during recovery, and about half of the survivors (4 of 9) had access to liquid assets immediately following one of their assaults. Survivors reported that they owned from “a little” to US$50,000 at the time of the assault. Although limited in number, there was strong agreement among the asset owners that savings positively impacted their recovery in ways that were consistent with providers’ responses. I identified three major themes related to liquid assets: These assets can (a) cushion economic shocks related to the assault, (b) increase survivors’ flexibility and their access to services, and (c) help survivors to feel more secure.

First, these data suggest that survivors can use liquid assets to cover their immediate expenses and cushion economic shocks, such as job loss and emergency expenses. For instance, a lawyer (P102) described how her clients have used savings when their employment was disrupted: If you get unemployed and if you have some savings, at least you’re not going to be destitute right away. It’s just like that with any client. I mean, especially if they need time off work, they can fall back on savings. Or if they get fired, if they get laid off [or] something, or if they quit, they have some sort of savings that they can fall back on for a little while. If they don’t have it, then they can’t necessarily focus on their emotional well-being. That they have to think about how are they going to survive and support themselves and their kids?

Similarly, survivors who owned assets reported using their savings to get through post-assault earnings disruptions. For instance, Lil’ Miss, a 51-year-old survivor who was introduced above, was fired from her job as a result of posttraumatic stress disorder (PTSD)-related performance issues. She lived off her “three to four thousand dollars” in savings for 18 months until she could secure a new job.

In addition to job loss, unanticipated expenses, such as medical bills, counseling fees, and moving costs, often arise in the wake of sexual violence. Participants consistently reported that survivors who own liquid assets use them to cover such unanticipated expenses. For instance, a lawyer (P110) described how savings facilitate access to services and allow survivors to benefit from victim compensation programs, which reimburse survivors for crime-related expenses: If they have access to savings, it makes it much easier for them because a lot of these costs, too, you pay it up front, and then you’re reimbursed. So, I think the long-term effects are lessened, because they can pay it. They have the money, it’s in reserve, they can pay it, and then they’ll get refunded or reimbursed. It goes back into the savings, so over the course of a year, let’s just say, they’re back at base level.

In contrast, those without savings would need to either incur debt to pay the up-front costs or forego services altogether. Indeed, providers reported that many of their poor, uninsured clients go without HIV prophylaxis because they cannot afford the US$600 to US$1,000 expense, while others experience financial crises when ambulance bills (as high as US$800) eat up income that was intended for rent and other necessities. Survivors who were uninsured and had no savings post-assault also explained that they could not afford medical and mental health care.

Second, in addition to buffering economic shocks, liquid assets can give survivors more options to access the services they need without raising significant financial concerns. Savings also allow some survivors the flexibility to take time to recover, to focus on their emotional well-being, even to change jobs or go back to school. For example, one counselor (P106) described how savings proved useful to a client who had been assaulted in her home: [She] was able to move [to a new home] because she did have assets. It was a no-brainer. It was going to happen, and it happened really quickly, and she didn’t have to think twice about it. And it was a huge relief. So knowing you can afford co-payments for mental health care. Knowing you could throw away every, you know, the sheet, the comforter, and the pillows and go out and drop a few hundred dollars for new bedding or even a new mattress. Knowing you could take two weeks off and do nothing or go away, if you want.

This counselor described an array of benefits and comforts her client was able to access due to her savings, including the ability to move to a new home quickly. This stands in stark contrast to the challenges faced by poor and asset-poor survivors. For instance, many providers described their less advantaged clients spending months on the waiting list for subsidized housing.

Another provider, an administrator (P107), similarly compared the flexibility conferred by liquid assets with the stark choices faced by some asset-poor survivors: It makes all the difference if they have it [savings] or if they don’t have it. If they have it, then they are still going to be dealing with all of those same issues, but they have that cushion there. So if they need to leave their job and take a few months, then maybe they can do that and get back up on their feet enough so that they can start a new job and feel comfortable doing that. If they don’t have that cushion, then they need to force themselves to go to work when they’re not feeling capable of doing that. Or if they do lose their job or have to quit their job, then they’re definitely in danger of becoming homeless and incurring a lot of debt because they don’t have anywhere to turn and any way to protect themselves and give themselves the time that they need to get back on their feet.

Survivors’ stories echoed these sentiments about how liquid assets increased their flexibility and options for recovery. For instance, Lisa, a 48-year-old survivor, quit the job where her perpetrator worked and was subsequently unable to work due to rape-related trauma. To support herself, she liquidated her US$50,000 in stock and sold the home she owned with her then-husband. These assets allowed Lisa to take a year off from work, then go back to college, and ultimately change professions entirely. Referring to the proceeds from her stocks, she explained, Thankfully, it gave me an opportunity to go back to school . . . That’s in my 30s, you know, so at that point, [I was] just feeling as though, “This: It’s now or never. I mean, if I want a career, then I’ve got to go back to school.” And if I didn’t have the savings that I had . . . I mean really, I ended up being able to live off of the savings I had and live off of it for probably two and a half or three years.

These assets played a life-altering role in Lisa’s recovery by opening up options for her to finish her college education and access a professional career. (Lisa’s homeownership is discussed in detail later.) Other survivors in the sample used their assets to take time off from work, pay for counseling co-pays, and access healing services such as yoga or massage.

Third, participants reported that owning liquid assets can boost survivors’ sense of control over their lives, increase feelings of safety, and dispel panic about what would happen if they lost their employment. For instance, a counselor (P112) described this benefit, saying asset ownership “affects their [survivors’] sense of safety and well-being. Okay, so, if you have savings, then there’s this sense like, ‘You’re going to be okay,’ or you have some control over the fact that you’re going to be okay.’” Importantly, this counselor suggested that the value of assets goes beyond the knowledge that a survivor will “be okay,” extending to her sense of control over that outcome. Similarly, another counselor (P111) described the comfort one of her clients took in knowing that her savings kept her from being completely reliant on the income from her job: It wouldn’t be the end of the world that she lost her job. She doesn’t have the stress about the fact that she might be too depressed to go to work one day . . . There’s this extra layer of stress that a lot of my clients get, that they start to panic around “what if.” So one of the things we work on [in counseling] is being in the present. They start to panic around, “What if I can’t go to work? What if I can’t do the work, what if I lose my job? What if, what if, what if?” She doesn’t have the panic about the “what if.”

This counselor suggested that much of the benefit of asset ownership lies in the absence of worry about economic concerns, compared with non-owners. For this reason, service providers are a useful source of data, as they may be able to detect such effects through comparison among clients. For survivors, it may be more difficult to perceive such effects firsthand. Indeed, a survivor’s description of the effect of her inherited savings bears this out.

Juana, a 28-year-old survivor, was first assaulted 5 years ago and suffered a second assault at age 25. She first mentioned her inherited savings in the context of her current assault-related medical bills, which exceed US$800. When I asked how she managed these expenses, Juana explained, “I was lucky enough that I was left some money by my grandfather, so I have a little bit of a cushion that I can use. But another part is I make sacrifices.” She later explained that she used this inheritance to support herself through college, to pay for all expenses not covered by her scholarship. Later in the interview, I asked Juana if these assets played any role in her experience following the assault. She responded, Not really, because they [inherited savings] weren’t something that I really consciously thought about, unless I was in kind of dire straits for money. I mean I knew it was there. I knew that’s what I would use to pay my rent each month, but I didn’t think of it as something I could use as any sort of luxury.

From her response, it appears Juana did not readily recognize any additional security her savings conveyed post-assault. Yet, by noting that she “knew the savings were there” and that they allowed her to pay her medical bills, she implied that her inheritance alleviated a potential source of stress. When viewed within the context of providers’ reports and asset theory, Juana’s story is consistent with the contention that asset ownership is associated with an increased sense of security. However, this example also demonstrates the difficulty of detecting or measuring this type of effect among survivors and suggests the need for further research in this area.

Financial Assistance From Family or Friends

The second type of asset examined in this study is financial assistance from family or friends, such as providing money for rent or offering a place to stay. The majority of providers (11 of 18) and survivors (7 of 9) affirmed the value of this type of assistance. For instance, a lawyer (P100) explained the manifold benefits of kin assistance for her clients: Any time a survivor feels like they have someone who is supporting them, that’s another person who can help them brainstorm, another person who can sort of tap into their network of trying to figure out financially what to do, or it may be even more tangible: Maybe it’s someone they can stay with or someone who can help them this month, or whatever it is, [with] very tangible things. A lot of survivors will move in with someone who believes them to [get] help.

Many survivor participants echoed this lawyer’s statement, explaining that they relied heavily on family and friends for shelter, food, and other financial assistance in the aftermath of sexual violence. For instance, Brooke, a 35-year-old survivor, explained that she relied on the goodwill of friends when she was unable to work for several years after being raped, and her family turned its back on her: I had friends who took me into their home and paid for—paid my rent, paid for my food, took me places, basically treated me like family for about 3 years. I probably would’ve thrown myself off a building if it wasn’t for them.

Brooke’s statement speaks for itself as far as the impact this assistance had on her life. Financial assistance also takes less substantial forms, including the comfort of knowing one could rely on family or friends for help if funds ran short. For instance, Jane, a survivor who was raped at age 22, explained, My parents would have [helped me] if I needed it. They would have supplemented my—what I was earning, if I needed—if I didn’t have enough for rent. But I was really sort of determined to try to—It was at a stage where I was trying to become independent from them, and I was reluctant to want to ask for help. So, I tried to avoid that to the extent I could. But my—I mean my parents were willing and able to supplement if I needed it . . . You know, my dad came down to help me, and he helped me move.

By emphasizing that she knew her parents were “willing and able” to help her as needed, Jane suggests that this knowledge offered her comfort, even as she strove for independence.

Beyond the material benefits of such support, several providers talked about how assistance from family and friends is important because it communicates others’ belief in and support for the survivor at this crucial moment in her or his life. For example, a provider who held dual roles as a counselor and administrator (P109) spelled out the multifaceted value of familial financial assistance for survivors: It provides them with money, but I also think there is this way of people giving back to them. Somebody took stuff away and there is this real [effect] . . . but it’s [also] symbolic—seeing those people are there for you when you’re at your lowest point. So, I think it’s money, and it’s really helpful. And I think it’s also—it probably is [as] good as any intervention. It’s just like, “Okay, people care enough to provide me with support.”

As this provider emphasizes, economic support can represent much more than money. Survivors benefit from both the direct financial effects of such support, as well as its symbolic value.

While familial financial assistance can be very important to survivors, many do not have access to such assistance. Respondents reported numerous barriers to financial support, including relatives’ inability to help, survivors’ hesitation to seek assistance, and people not believing the survivor. First, a family’s ability to offer financial assistance often hinges on their income level and asset ownership, and poorer families simply have less to offer in this area. For example, a lawyer (P101) explained that unlike her middle-class clients, her low-income clients “don’t have family who have money, and they don’t have friends who have money.” Another provider, a counselor (P106), said simply, “If you come from poverty, you’re not going to be able to turn to your family for money . . . And people who have families with less income are probably much more reticent to ask for any help.” Lil’ Miss, a survivor whose story is told above, may offer a helpful example of this. Lil’ Miss grew up in a low-income community, and although she reported that her brother and best friend would write her checks whenever she asked, she struggled with homelessness and poverty for years after depleting her own savings. This suggests that there were limits to the amount of help she was willing to seek or that her kin were able to give.

A second barrier to seeking financial help is that survivors may feel inclined to spare their families from the pain of their assault for a variety of reasons. For example, a counselor (P112) explained that her clients often fear that their family members “will have a heart attack or suffer some sort of mental breakdown if they found out.” Similarly, Sally, a survivor who lost her job after being raped at age 23, explained that she did not want to burden her recently divorced mother by asking for help: My father died when I was a child, and my mother had gone through a divorce a couple of years before the assault, and so I didn’t really want to ask her [for financial assistance], and plus . . . it was really important for me to just feel like I was on my own.

Instead of asking for financial assistance, she worked in temporary jobs, earning a subsistence living for 4 years until she was ready to return to full-time work.

A third barrier is that stigma associated with sexual violence can keep people from seeking or receiving assistance. A lawyer (P100) explained, It would be one thing if they had crashed their car and needed help buying a new car. But of course when you layer on that it’s a sexual assault, there’s all this stigma and shame and blame, and nobody wants to talk about it . . . So that many survivors will feel like they can’t reach out to their normal support system because of the issue.

As the stigma associated with rape victimization is widespread and deeply entrenched (Herman, 1992; Ullman, 1996, 1999), it may serve as a significant barrier preventing survivors from seeking financial assistance from family and friends. Survivors’ willingness to ask for help may also depend on the quality of their relationships with kin.

A fourth and related barrier to familial assistance is when survivors’ social networks do not believe or support them. For instance, a lawyer (P100) described how this has affected her clients: “So many of my clients do not have that option [familial financial assistance], either because they’re ostracized by their family, the family knows the assailant and they believe him or her, or they just don’t want to tell.” Several survivors in the study reported that their families and friends responded in this way, either not believing them or blaming them for the violence. For instance, Brooke was kidnapped and raped at age 16 by a man she had met online. She explained that her family, friends, and community blamed her for the attack: Well, my mother decided that I was a pathologically lying slut. So that relationship, crap as it was, was pretty much turned on its ear. My local friends, many of them didn’t really want anything to do with me the following year, since “pathologically lying slut” went around my church youth group as well. I did pick up new friends that year, but I lost contact with them almost immediately.

Brooke later dropped out of college out of fear when her perpetrator contacted her on campus. She was fortunate to make new friends who provided her significant help until she was able to support herself financially. Still, for survivors like Brooke, having family and friends who do not believe and support them shuts the door on a potential source of financial and emotional support.

Homeownership

The third type of asset considered in this study is homeownership. Ten providers offered information about the effects of homeownership on survivors’ economic well-being, and one survivor owned a home at the time of her assault. This low rate of homeownership at the time of the assault may be due in part to the relatively young age at which most of the survivors were assaulted. Survivors in this sample were between 18 and 32 years old at the time of their most recent sexual assault, with a mean age of 24, while the median age of first home purchase in the United States is 31 (Taylor, 2013). Despite this smaller subsample, these exploratory findings may shed light on the role of homeownership in recovery and help to identify areas for further research. The interview data suggest that homeownership can have mixed effects on survivors’ economic well-being. Some respondents reported that homeowners can experience a greater sense of stability, but many noted that homeownership can be a “double-edged sword.”

Six provider respondents and one survivor reported that homeownership can be beneficial for survivors. However, the extent to which survivors can make use of this benefit depends on whether the survivor wishes to move as a result of the assault. First, providers noted that homeowners have the freedom to make changes to their homes to feel safer in the wake of violence. For example, a lawyer (P110) explained, “If they own their home, we don’t have to worry about working with landlords to get locks changed or anything like that. I guess they incur that expense, but at least we’re not negotiating.” A second benefit of homeownership in these data is the potential to leverage one’s equity to purchase services that enhance safety or aid with recovery. For instance, a lawyer (P100) explained, I think the pro if it [the rape] didn’t happen in the house would be that you do have this asset, so that if you took out a second—I don’t really know that much about finances—but if you took out a second mortgage, or if you were able to get a loan, you might be able to leverage it to get some money to be able to take time off work or whatever it was.

Through home equity lines of credit, homes can function like liquid assets, increasing survivors’ flexibility and potentially cushioning economic shocks. However, this provider went on to note that any benefits of homeownership are lessened if the assault occurred in the house: But if happened in the house, I think it’s a con because now you’re stuck living in your [house], and it’s tainted. Maybe it’s been your house for 20 years, like where you raised your family, and ugh, that’s a mess.

In a similar vein, Lisa, who was introduced above, was the only survivor who owned a home at the time of her assault. She explained that she felt compelled to move to a new home after her husband raped her in the house they owned together: There was no way I was going to stay in that house, because it did happen in the house, and it happened where my stepdaughter heard everything. So, so, I wanted—I definitely wanted to move to a new [home]. This was in [a different state], and it would have been very easy for the wife to keep the house. It’s a super, super easy thing in the [state’s] divorce court. But yeah, there was no question, no question.

At the same time, Lisa also noted that the proceeds from the sale of her home were important to her recovery. She explained that she and her husband “divided the investments and we sold the house. And I was able to use all of that to support myself and go to school.” As she noted, Lisa lived on the money from that home sale, along with her stocks, when she quit her job and went back to college. Her college degree allowed her to pursue a new career as a teacher. Lisa rented a home for many years, until she and her second husband purchased a home together. Lisa’s experience illustrates the potential for homeownership to offer flexibility and security during recovery, at least for a survivor who is willing and able to sell her home.

However, seven provider participants reported that homeownership creates barriers for survivors in the wake of assault because owning a home is expensive and makes moving difficult. Many survivors wish to move for safety reasons, while others find they are no longer able to afford their homes due to assault-related income disruptions. A lawyer (P110) explained, “Often if they own their own home too, they can’t move as easily. That’s their home, so if they don’t want to continue living there, they have to sell that home . . . yeah, now we’re opening a big bag of worms.” As this lawyer implies, selling a home is more time-consuming and complex than moving from one rental to another. The alternative process of finding a tenant and managing a rental property similarly requires time and attention, which would add to a survivor’s burden in the immediate aftermath of trauma. Plus there is a chance that the house would not sell or rent, and the survivor would find herself forced to continue living in a home in which she does not feel safe or which she can no longer afford.

Another potentially negative impact of homeownership that emerged from these data is the drive to keep a home that has become unaffordable. For instance, a lawyer (P103) explained, “When they do [own property], it’s huge. I think that they don’t want to lose it . . . It becomes this ‘die by the sword’ type of a moment for them, even to the point of their own safety being jeopardized.” This lawyer shared the case of an asset-poor survivor who had purchased a condominium using a subsidized mortgage program. After being raped, she could no longer work full time. The resulting reduction in her income caused her to fall nearly US$4,000 in arrears. The lawyer explained that her client would likely never recover financially from this setback because she simply could not afford her home payments on her new part-time salary. Yet, the client was doing everything in her power to keep the home.

Relatedly, an administrator (P107) noted that homeowners are not immune from the challenges faced by renters, such as difficulty making payments when income is disrupted: If the person owns their place but they still have a huge mortgage, I think that they fall in the same trap of “How do I pay this mortgage?” I mean, they may be able to hold onto where they’re living longer and not have to deal with, you know, “What do I tell my landlord or don’t tell my landlord?” It’s more about personally how they are going to figure it out. So yeah I think it does help a little bit, but in the end if they don’t have a lot of savings to help them out, it might not.

Other providers similarly talked about clients losing their homes to foreclosure because their earnings decreased dramatically in the aftermath of sexual assault. These stories illustrate the precarious position that homeowners who are otherwise asset-poor face when their income is disrupted. Having a mortgage on a home is not enough; savings or other liquid assets are needed to cover housing costs in the case of serious income disruption.

Discussion

These findings suggest that financial assets, particularly savings and familial financial assistance, can serve as a crucial bridge to recovery from sexual violence by standing in for lost wages, covering unexpected expenses, and increasing flexibility. While asset theory has not previously been applied to isolated sexual violence, these findings are consistent with the theory’s central contention that assets can buffer economic shocks. Because sexual violence can create a wide range of adverse economic events for survivors, these data suggest that those with financial resources may be better situated to recover from this trauma.

The idea that wealth inequalities inform rape survivors’ experiences contrasts with the common belief that “sexual violence does not discriminate” (as an administrator stated in an interview). Advocates in the field of violence against women have long used this as an organizing idea to combat stigma and raise awareness that sexual and domestic violence happen in rich and poor communities alike (Richie, 2000). While the idea that “rape does not discriminate” often refers to its prevalence across socioeconomic strata, this message ignores the potential for disparate effects for poor survivors. This study’s findings suggest that the economic effects of sexual violence may weigh more heavily on asset-poor victims than wealthy ones. Hence, these findings point to inequalities in recovery from sexual violence, which are often not considered in research and that can inform public policy and victim services. Due to the small sample size and exploratory nature of this study, further research is warranted to gain a generalizable understanding of the roles of asset ownership—and asset-poverty—in recovery.

This study also builds upon and extends our understanding of asset theory and the role of assets in recovery from trauma in several ways. First, the findings suggest that liquid assets can buffer the economic shocks associated with sexual violence and facilitate some aspects of survivors’ subjective well-being. Shobe and Page-Adams (2001) argue that assets “provide people with otherwise unattainable opportunities to hope, plan, and dream about the future,” which improves their social and economic well-being (p. 119). In contrast, they argue, asset-poor people must work to make ends meet on a “day-to-day basis.” Asset-poor survivors must similarly cope with the aftermath of assault on a day-to-day basis, which makes them more vulnerable to the financial shocks that can follow rape. Those who own assets, meanwhile, have the opportunities to plan for the future, to be flexible in their response to unexpected occurrences, and to take comfort in the knowledge of those plans and options. By allowing them to make decisions and plans, assets can increase survivors’ sense of control over their lives. This sense of control may be particularly valuable to survivors of sexual violence, in which the perpetrator takes away the victim’s control over her or his body (Herman, 1992). This is not to minimize the numerous negative effects of sexual assault for all survivors, asset owners or no, but rather to suggest that such ownership may facilitate recovery in important ways.

Second, this study’s findings on the value of familial financial assistance and unequal access to such support extend asset theory’s approach to the intra-familial transmission of wealth. Shapiro (2004) defines transformative assets as inherited wealth that lifts a family beyond their own earnings level, such as a single mother whose familial assistance allows her to live a middle-class lifestyle despite her own low wages. Familial financial assistance for survivors may be similarly transformative by opening options that they could not otherwise afford, such as taking time off from work or accessing costly medical services. In addition, just as Shapiro (2004) notes that White families are more likely to benefit from transformative assets than Black families, inequalities may also emerge in familial assistance for survivors. In the U.S., families’ income and asset levels are highly unequal by race (Campbell & Kaufman, 2006; Kochhar, Fry, & Taylor, 2011), suggesting White families are in aggregate better situated to provide financial assistance to survivors than are Black, Latino, or Native American families. This study was unable to assess the degree to which racial differences exist in familial financial assistance for sexual assault survivors, but it documented many barriers to familial financial assistance, including poor families’ limited financial capacity. Future research should examine the impact of racial wealth inequalities on survivor outcomes.

Third, these findings add complexity to current discussions of homeownership within the asset field. Adherents of asset theory report that homeownership is associated with a wide range of benefits to health, well-being, and safety. Yet in the context of sexual violence, owning one’s home appears to be a mixed blessing. Homeowners may have the option to leverage their investment to increase stability, but this benefit is tempered by the possibility that a survivor may wish to move from the home where the assault occurred. In addition, homeowners can face the same concerns about housing affordability that arise for renters, but with higher stakes. These findings suggest a need to turn a more nuanced lens to the study of homeownership, particularly as it relates to trauma and recovery.

Policy Recommendations

By noting that asset ownership can help with recovery, this research identifies a need as well as a potential solution. The need I identify is that survivors of sexual violence require economic resources to facilitate recovery. Existing wealth inequalities mean less privileged survivors may face negative economic effects of sexual violence disproportionately, which suggests that policy intervention may be appropriate to create equitable outcomes. Importantly, many existing policies address the economic needs of IPV survivors but exclude survivors of non-IPV sexual violence. If a woman who is raped by her landlord or her boss deserves the same financial assistance as one who is raped by her husband, then existing policies for IPV survivors need to be expanded to include all sexual assault survivors. The solutions lie not only in supporting private asset ownership but also in policies and services that can offer some of the benefits of asset ownership to asset-poor individuals.

First, IPV services often include economic components, such as financial assistance, transitional housing, and financial literacy education (Lyon, Bradshaw, & Menard, 2012). Yet, financial assistance services for non-IPV sexual assault survivors are not widely available, as most rape crisis centers lack the funding and staff to offer such services. State and federal dollars should be made available to rape crisis service providers to create economic stabilization funds for sexual assault survivors. The Office on Violence Against Women could begin by funding pilot programs to identify best practices and create a model for nationwide implementation. Importantly, service providers in the present study reported that survivors often need relatively small amounts of assistance (approximately US$1,000) to maintain their financial stability and prevent homelessness. If investing this modest sum in survivors in the immediate aftermath of trauma could help prevent a downward spiral, this could ultimately create savings for the state on homeless services, subsidized housing, and other welfare programs.

Second, small business development, or microenterprise, can boost survivors’ financial stability and empowerment. Tailored microenterprise programs have been developed for IPV survivors (e.g., Pathways to Independence, The Enterprise Center, 2013; Project Phoenix, Vera House, 2014), and such programs can provide helpful models for addressing the needs of isolated sexual assault survivors. Microenterprise programs for sexual assault survivors should include trauma-informed and culturally sensitive training, mentorship, and seed money. Self-employment may be particularly appealing for survivors who have been assaulted in the workplace or who have difficulty continuing their pre-assault careers for other reasons.

Third, this study’s findings suggest that assets can play an important role in recovery for sexual assault survivors. One policy strategy for encouraging asset ownership among low- and moderate-income people is the Individual Development Account (IDA). IDAs are savings accounts that offer matched funds for asset-building purposes, such as homeownership, post-secondary education, or small business. Tailored IDA programs should be developed for sexual assault survivors, similar to the ones that exist for IPV survivors (Sanders & Schnabel, 2006, 2011; Sanders et al., 2007). IDA programs often include financial education and a peer support structure. These elements can be designed to address common concerns of sexual assault survivors, such as fostering peer-to-peer recovery strategies and sharing information on financial assistance for crime victims. Beyond asset building, the goals of these IDAs would be to help survivors both recover from past violence and feel safer in the future.

Conclusion

This exploratory study has applied the asset framework to recovery from isolated sexual violence, a problem that is not often recognized as a source of economic concern for survivors. This study’s qualitative approach allows us to learn from survivors and the people who help them about how financial resources can help to lighten the economic burden caused by sexual assault. These findings suggest that liquid assets and familial financial assistance can help offset post-assault expenses and can facilitate access to resources that are helpful for recovery. Specifically, these types of assets can stand in for lost wages and help cover new expenses that arise as a result of the violence, such as medical fees, counseling bills, and moving costs. Both owned assets and familial financial assistance can also convey a sense of security and control over one’s life. Homeownership, however, seems to have mixed effects. For some survivors, a mortgage can be leveraged to enhance economic stability, but for others, homeownership is costly and makes moving difficult.

Survivors do not have equal access to financial and familial resources. Instead, unequal wealth ownership, as well as the numerous barriers to familial assistance described in the findings, place asset-based remedies out of reach for many survivors. These data suggest that the negative economic consequences of sexual violence likely burden survivors with fewer financial resources more heavily than those who own significant assets. Although private asset ownership cannot be equalized, public policies for IPV survivors can be expanded to better meet the economic needs of all sexual assault survivors.

Footnotes

Acknowledgements

The author would like to thank Thomas Shapiro, Janet Boguslaw, and Ilene Seidman for their guidance and input. The author also thanks Laura Sullivan and Ken Sun for their insightful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author was supported by a Ford Foundation Predoctoral Fellowship during the data collection and analysis phases of this project.