Abstract

Remittance inflows in the economy of Bangladesh are getting larger every passing year, matching with the increasing external demand for its manpower. The ensuing development impacts of remittances, as a means of transfer of wealth, on socioeconomic factors are increasingly viewed with importance. Remittances have helped improve the social and economic indicators like nutrition, living condition and housing, education, health care, poverty reduction, social security, and investment activities of the recipient households. The relative weight of remittances has also increased against most of the macroeconomic variables alongside the contribution to GDP. Moreover, Bangladesh has been able to avoid any serious imbalances in BOP’s current account, although it has persistent merchandize trade deficits. Not only that, the export tradable sector has thus far remained unaffected from the Dutch Disease effects of remittances.

Keywords

Introduction

Increased economic activities due to economic globalization in the 1980s and 1990s led to a rapid international rise in demand for skilled and unskilled manpower. That paved the way for many people, including those of the developing countries, to move to the outside destinations (Castles & Davidson, 2000). For a large number of Bangladeshi workers, mostly semiskilled and unskilled, this external demand opened up opportunities for earning their livelihood abroad. Many others have also left the country for different pull and push factors. 1 This migration was, however, a welcome relief for Bangladesh as its development strategies since independence could not cope with and accommodate the growing demand for employment from a fast growing population. The consequence of the multidirectional relocation of people, both temporary and permanent, was the quick rise in remittances in the economy of Bangladesh.

With the passage of time, however, a compositional shift seems to have taken place in migration from Bangladesh, particularly between pre- and postindependence phases, as temporary migration of workers now forms the overwhelming part of its total migration. This short-term migration has, again, remained mostly Asia-centric due to the fast expansion of demand for manpower in many economies within the region. As we know, massive investments in infrastructures in the Middle Eastern countries induced by petro-dollars 2 necessitated some of the Arab countries to look for external workforce since the mid-1970s. However, a rapid economic development of the newly industrialized economies (NIEs) 3 in the 1980s and 1990s coupled with the Japanese need created a high demand for cheap foreign labor in the East and South East Asian region (Cruz, 2005). Both these economic events created scope for short-term employment opportunities for workers of many labor-surplus countries including Bangladesh. Presently, as estimated by the Migration and Remittances Factbook (MRF) 2011 of the World Bank, Bangladesh has a total stock of 5.38 million migrants, equivalent to 3.3% of the its total population (World Bank, 2010). Of them, a significant portion is now based in Asia, particularly in the Middle East and the East and South East Asia. However, the direction of permanent migration from Bangladesh remains mostly to the West and other developed countries in the world, although a gradual shift is taking place as more migrants are heading toward developing economies for their long-term relocation.

As a parallel development to this growth in outward movements of workforce, the volume of inward remittances has accelerated to become a regular and substantial source of resource transfer in the Bangladesh economy, although this was not the case until 2000 when remittances were seen as trivial in size and had little developmental relevance. In fact, remittances now stand many folds to its foreign direct investment (FDI) and official development assistance (ODA) combined. According to the MRF 2011, official remittances to Bangladesh exceeded US$11 billion in 2010, making it the eighth largest remittances recipient country in the world (World Bank, 2010, p. 58). Certainly, this was a significant flow of fund for Bangladesh. Indeed, a regular growth in the flow of remittances has upended the developmental significance of remittances, both in social and economic sectors, in the eyes of the policy strategists.

However, linking development impacts of remittances with the socioeconomic variables in the recipient economy is largely dependent on the pattern of uses by the beneficiaries. In other words, the development linkages of remittances may be examined by their uses for consumption, savings, education, health care, businesses, assets holding, debt redemption, and so on of the recipient households. Although establishing such an association is acknowledged to be complex, researchers have been giving more attention to this aspect in recent times. For a developing country like Bangladesh, the developmental importance of remittances on economic and social sectors seems to have a strong basis when we find the argument that in less financially developed countries remittances promote growth and present an alternative mode of investment financing (Giuliano & Ruiz-Arranz, 2009).

In most cases, first-round effects of remittances on economic development are felt at the households of the migrants (Taylor & Wyatt, 1996) when we find remittances move as person-to-person flows, targeted to the needs of the recipients most of the time (Ratha & Mohapatra, 2007). In reality, remittances bring additional money to the recipient households to spend on higher consumption, better access to education and health services, improved housing and living conditions, and employment of resources in productive activities (Thao, 2009). At the end, workers’ remittances complement national saving to form a bigger pool of resources available for investment (Carling, 2004; B. Ghosh, 2005; Solimano, 2003). Hugo (2003) argues that remittances represent a substantially greater redistribution of wealth than FDI and ODA, mainly because of absence of any conditionalities (attached to ODA) and repatriation possibilities (of FDI). At macro level, these culminate in a chain of increase in aggregate demand-output-income, affecting growth of the economy at the end. The sustainability of the process could be debated though, as the development effects cannot be a permanent feature unless the commitment of migrants to remittances is institutionalized. This is still a problem in Bangladesh as use of unofficial channels 4 for sending remittances is popular, making the institutionalization process a bit difficult.

Many empirical and analytical works have examined the impact of remittances on the incidence of poverty, inequality, and economic growth position particularly in the developing countries. Adams (1991), for example, finds that although remittances reduced poverty in Egypt in a small amount, their overall impact on income distribution was negative. In his analysis for Pakistan in 1992, Guatemala in 2004, and Ghana in 2006, Adams concludes that remittances slightly reduced poverty but their overall impact on income distribution was negative (cited in Pfau & Long, 2007). But Taylor and Wyatt (1996) find that remittances reduce inequalities in rural Mexico. Adams and Page (2005), Lopez-Cordova (2006), Maimbo and Ratha (2005), Acosta, Calderon, Fajnzylber, and Lopez (2006), Yang and Martinez (2006), Ozden and Schiff (2006), Brown (2008), and so on have important studies in this context. However, the findings of the studies that investigated the impact of remittances on poverty and inequality form no single uniform standpoint and suggest a mixed picture. Except the real ground situations, the disuniformity could happen because of the underlying methodology to which poverty and inequality are highly sensitive (Acosta et al., 2006). Acosta et al. show that in Latin American countries, the proportion of the poor is reduced by 0.4% for a 1 percentage point increase in remittance to GDP ratio.

On the link between remittances and growth, studies suggest mixed evidence. Jongwanich (2007), for example, finds that remittances raise income and have a significant impact on poverty reduction in developing Asia and Pacific countries, although their impact on growth is marginal. Whereas Barajas, Chami, Fullenkamp, Gapen, and Montiel (2009) find no growth effects of remittances, a study by Catrinescu, Leon-Ledesma, Piracha, and Quillin (2006) shows a weak positive effect of remittances on long-term macroeconomic growth. But Vargas-Silva, Jha, and Sugiyarto (2009) summarize that fixed-effects and random-effects estimations indicate that remittances affect the real annual GDP per capita growth of home country positively. Their findings signify that a 10% increase in remittances as a portion of GDP should lead to about a 0.9% to 1.2% increase in growth of output in an economy. From the viewpoint of Bangladesh, the Philippines, Tajikistan, and so on, this is a significant figure as remittances account for more than 10% of their GDP. A number of studies like Barua, Majumder, and Akhtaruzzaman (2007), De Bruyn and Kuddus (2005), Deb (1986), Das (1981), the World Bank (2006), and so on have tried to find the relationship of remittances with socioeconomic development in Bangladesh. Their findings support a positive association between them.

But a number of studies like Akkoyunlu and Vickerman (2000), Solimano (2003), Rapoport and Docquier (2003), and so on have raised the possible “Dutch Disease” 5 effect of remittances, whereby an appreciation of the real exchange rate of the domestic currency due to inflow of a large sum of remittances could lead to a rise of price of exportable commodities. This may erode the competitiveness of the domestic products in the international markets, and thus jeopardizes the development of tradable goods sector. Empirical studies of Amuedo-Dorantes and Pozo (2004), Rajan and Subramanian (2005), and Lopez and Molina (2006) use cross-country data to document the real exchange appreciation following flows of remittance (cited in Acosta & Mandelma, 2007). Also, negative impacts of remittances on the labor supply of El Salvador and Mexico have been documented by Acosta (2006) and Hanson (2007). This happens as remittances may create a dependency syndrome among the recipients and may particularly affect rural development and change (Thao, 2009). Acosta and Mandelma (2007) examine whether an increase in remittances causes Dutch disease effects in Salvador, a small open Latin American economy with a large flow of remittances. The findings of their study generally suggest that the inability of the Salvadorian economy to absorb remittances leads to the realization of the Dutch disease phenomenon under three of the cases considered: “one where remittances are exogenously determined, another where remittances are countercyclical, and finally the case where remittances act like capital inflows” (Acosta & Mandelma, 2007, p. 22). For Bangladesh, the effects of such a “disease,” if any, need to be examined further.

The remainder of the article has been divided into five parts. The second part outlines the “Method” followed in the study. Bangladesh has seen a shift in the direction and composition of migration and remittances over time. The third part provides these directional and compositional changes. The development dynamics of remittances, contextualized in terms of socioeconomic impacts in Bangladesh, has been discussed in the fourth part. The fifth part concludes the article.

Method

By remittance, this study refers to the international transfer of funds by the migrants or emigrant diasporas to home country, through official channels, from the country where they work or live. So inward transfers by both temporary and permanent migrants are taken into account. In our study, temporary migration is characterized by employment with specific short-term job contacts and returning home of the workers after completion of the contract period. In case of Bangladesh, most short-term migrants abroad are from rural areas and poor (Hasan, 2006). Permanent migration, however, takes place when one migrates with a permanent change in usual residence so that the relocation becomes a lasting one. Another important aspect of this move is that the migrant holds no intention to return to live in future to the land he or she is leaving.

It is assumed that remittances sent by the Bangladeshi migrants go first to households, as remittances are fundamentally person-to-person flows. However, the remitted amounts ultimately join the mainstream economy by way of consumption and investment expenditures. Even if the migrants invest remittances in different government savings schemes like nonresident foreign currency deposit, U.S. Dollar premium bond, wage earners’ development bond, and so on, where they have the right to take the invested amount out of the economy again, these investments are, in the end, liquidated in the Bangladesh economy. There is little evidence to show that migrants channel their invested amounts significantly out of the economy again.

The study has been primarily based on the secondary sources of information. Here, the socioeconomic impacts analysis is broad in nature as the effects of remittances may become apparent from immediate to medium to long term. Although the study recognizes the economic and social impacts of unofficial transfer of remittances, it does not deploy any effort to present the effects of unofficial transfer in the economy because of the practical difficulties in quantifying the amount.

Remittance spending by the recipients has been divided into two broad categories: consumption and investment. The broad-head consumption includes the recipients’ expenses on items like food, clothes and furniture, medical treatment, repayment of loans, home construction/repair, social ceremonies, gift or donation, and others. Treating expense for home construction/repair as consumption expenditure may be debated because of the perceived indirect backward and forward linkage effects. But our discussion on the home construction/repair expense out of remittances takes the view that this expense does not generate any direct income as a return. Moreover, in most cases the recipient households are typically dependent on the remittances income for their living, so any expenses on home construction/repair turn out to be merely consumption expenditure. The rest of the uses of remittances is treated as saving or investment. The major items included in this category are business investment, savings/fixed deposit, purchase of agricultural and homestead land, release of mortgaged land or taking mortgage of land, education cost, community development investment, and sending family members abroad. The second grouping is based on the consideration that all these uses have potential short- and long-term returns to the users themselves and/or to the society. Again, the total weighted value to the two categories of expenditures, namely, consumption and investment, is assigned as one. 6

Out of the two, the portion of consumption expenses has been used to obtain the marginal propensity to consume value of remittances (MPCR). This is the decimal equivalent of the percentage of money used for consumption. Similarly, we calculate the value of marginal propensity to save of remittances (MPSR). The MPCR is expected to be different from the national marginal propensity to consume (MPC) value in Bangladesh for a number of reasons including higher average income of the remittance recipient households.

Finally, we calculate the value of remittance multiplier (rm) to find the GDP contribution of remittances, measured in terms of the aggregate amount of GDP added/created by remittances. 7 This is the GDP effect of the investment made out of remittances. In this study, the MPCR and MPSR have been calculated from the study of Siddiuqi and Abrar (2003). We use these MPCR and MPSR figures as well as a constant rm to calculate the approximate GDP contribution of remittances over the period of 1976 to 2009. These figures are accepted only as rough estimates of the actual coefficients over time.

Migration and Remittances

In this article, we primarily focus on the issues pertinent to development effects of remittances. But before dealing with that, we briefly touch on the direction of gross migration from Bangladesh and growth in remittances in its economy over the last three and a half decades starting from 1976. For that purpose, we have constructed Figure 1 to include the flows of migration from and remittances in Bangladesh since 1976-1977 to 2010-2011 and expect that this will help understand the developmental importance of remittances in the economy.

Migrations From and Remittances in Bangladesh, 1976-2011

From Figure 1, it could be seen that the migration figure has grown to 981 thousands in 2007-2008 from a tiny base of 14 thousands in 1976-1977. But in 2008-2009 the out-migration declined to 650 thousands. However, an analysis of the growth of migration during this period shows three distinctive phases: (a) a relatively slow growth from 1976 to 1990, (b) doubling of the figure in 1991-1992 from where the annual migration nearly stagnated to that level till 2005-2006, and (c) a fluctuation in growth in the subsequent 5 years up to 2011. Evidently, Bangladesh experienced a huge rise in the international migration during 2006 to 2008. But then the worldwide economic recession in 2008-2009 and recent turmoil in the Middle Eastern countries seemed to have affected the outflows, as reflected by the decline in 2009 and 2010, although a marginal improvement in the flows has taken place in 2011.

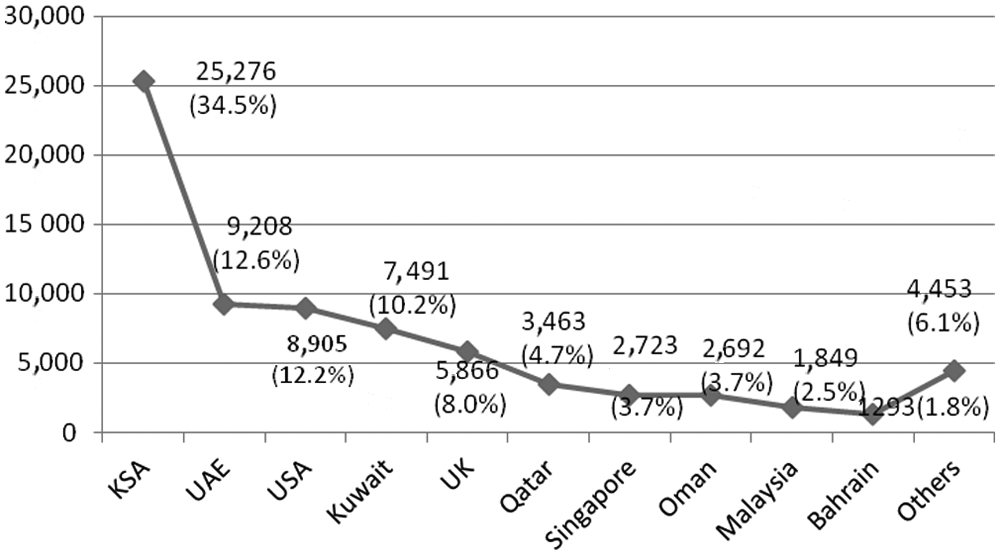

The cumulative figure also corroborates the growth of migration from Bangladesh. The Bangladesh Bureau of Statistics (BBS, 2010) estimates that since 1976 to 2009, a total of 5.5 million people left Bangladesh for employment abroad. Based on the BBS estimate, we have prepared Appendix Figure A2 to show the destination-wise cumulative distribution of migrants. The directional distribution for the period shows that the Middle East countries like the Kingdom of Saudi Arabia (KSA), the United Arab Emirate (UAE), Kuwait, Oman, Bahrain, Qatar, and Libya in Africa are principal destinations for Bangladeshi workers. These countries together absorbed about 70% of the cumulative total; the KSA alone accounted for 45%. Besides, Malaysia has emerged as the third largest importer of Bangladeshi workers, pulling about 10% of the cumulative total. Singapore, the United States, the United Kingdom, and Canada are also significant destinations. India, however, is a notable omission in the list, although unofficially it houses the highest number of economic migrants from Bangladesh (World Bank, 2010).

While dealing with remittances, we find that Bangladesh does not maintain any segregated records for remittances inflows from permanent migrants and temporary workers abroad. The segregated figures could have provided a better picture of contributions of the temporary and permanent migrants in the transferred amounts. Nonetheless, Figure 1 indicates that growth in remittances took place in tandem with the number of outgoing migrants during the period. Beginning with an amount of US$49 million in 1976-1977, the figure reached to US$9,689 million in 2008-2009, registering about 198 times increase during the period. However, the worldwide recession in 2008-2009 seems to have affected the number of migrants from Bangladesh, as indicated by a sudden decline in 2009, although remittance inflows during that time actually increased. The MRF 2011 shows that Bangladesh received US$11,050 million of remittances in 2010, marking an increase in aggregate amount but a decline in the growth rate of remittances (World Bank, 2010). Interestingly, remittances growth in Bangladesh followed a similar global pattern for the developing countries during 1970 to 2010, as is shown in Appendix Figure A2. This underscores a cherished area of wealth transfer where the developing countries have an absolute advantage and have tremendously outpaced the developed countries.

Constructed Figure 2 shows us the cumulative inflows of remittances from various countries to Bangladesh during 1980-1981 to 2009-2010. The importance of KSA in particular and other Middle Eastern counties in general could be understood for remittance inflows in Bangladesh. During the period, the KSA alone was responsible for 34.5% of the total remittances. Although the United States and the United Kingdom do not host many Bangladeshi short-term workers, in cumulative counting they hold the third and fifth position, respectively, highlighting the role of permanent migrants in remittance transfers. However, the cumulative figure of remittances from Malaysia, constituting only 2.5% of the total, may surprise many. The possible explanations for this smallness could be, first, that migration to Malaysia from Bangladesh is relatively a recent phenomenon; second, the jobs of the Bangladeshi workers are mostly manual in nature requiring lower skill and hence are financially less rewarding; and third, the migrants might be using unofficial channels more for sending remittances from Malaysia for a number of reasons including the presence of a higher number of illegal workers, their low level of education, convenience of using those channels, and so on. Increase in the amount of remittance inflows from other countries in the recent time indicates a diversification of destinations of the Bangladeshi migrants. The newer locations include South Korea, Iraq, Canada, Rumania, Australia, South Africa, Russia, and so on.

Bangladesh—Origins of remittance inflows (1980-1981 to 2009-2010 [cumulative, in million U.S. dollars])

A pertinent question arises—“What are the tentative motives of the migrants for sending remittances to Bangladesh?” Knowing the answer is indeed important as the underlying motives for sending remittances also influence the pattern of uses by the recipient households. The uses pattern of remittances in turn affects socioeconomic development variables at the macro level. Keeping this linkage in mind, we find that there are primarily four groups of motives for sending remittances by the migrants. These are altruistic motive, portfolio motive, loan repayment motive, and coinsurance motive. Most important of all is the altruistic motive where migrants are guided by the concerns for the well-being of the family members for sending remittances back home. Likewise, migrants may be motivated by self-interest and income differential for transferring funds. Barua et al. (2007) identify altruistic motive as the major determinant of remittances in Bangladesh. But we argue that remittances by temporary workers are broadly altruistic and portfolio in nature, whereas for permanent migrants they could mostly be guided by altruistic motives. This is because of the fact that remittances sent by the permanent migrants are basically for the welfare concerns of the recipients as the migrants do not intend to establish a future for themselves in their country of origin. On the contrary, most of the temporary workers work in a different country for their livelihood but see their future in the country where they have come from. So they send their earnings back to the country still they tend to belong for a future with both altruistic and portfolio motives.

The discussions above, however, do not highlight some important aspects of external migrations and remittances of Bangladesh. First, the United States and the United Kingdom as sources of transfer of remittances indicate that the Bangladeshi diasporas or permanent migrants play a significant role in the flow of remittances. This may be realized when we see that during 1980-1981 to 2009-2010, more that 20% of the cumulative total of remittances came from these two countries. An inclusion of remittances from the same type of migrants from Canada, Australia, Japan, and other countries will simply push their relative share further up. Second, the gender-wise statistics of external migration indicate that migration has remained mostly a male affair. The MRF 2011 of the World Bank shows that of the total migrants from Bangladesh in 2010, only 13.9% was female. Also, the migration rate of tertiary-educated population is considered to be low; it was only 4.3% in 2000. Similar statistics for Vietnam, a country with which Bangladesh may be compared in many ways, show a different composition. In 2010, for example, females comprised 36.6% of the total migration from Vietnam and even in 2000 the migration rate of tertiary-educated population consisted of 27.1% of the total (World Bank, 2010). Third, Bangladesh is still facing a problem with the mode of transfer of money earned by the migrants abroad. This is mainly because of preference of the workers to send remittances through informal channels, popularly known as hondi. According to Siddiqui (2004),

Hundi refers to illegal transfer of resource outside the international or national legal foreign currency transfer framework. Organised groups based in diverse cities such as London, New York, Dubai, Kuala Lumpur and Singapore conducts hundi operation through their partners in Bangladesh or in the region. (pp. 9-10)

The Global Economic Prospect (GEP) 2006 of the World Bank estimated that as much as 56% of remittances were directed through informal channels in Bangladesh. In their study, Siddiqui and Abrar (2003), however, find that 40% of the total volume of remittances had been channeled through hundi. Nonetheless, we believe that this problem has subsided a bit since then as there has been an improvement in the remittances receiving infrastructure up to rural level. This seemed to have helped increase the use of formal channels for transferring remittances in Bangladesh, but the problem persists. Finally, migration to India is never recognized in Bangladesh because of the political sensitivity of the issue and illegal routes used by the people for crossing the border. Remittances from these people most likely follow the unofficial routes. In our view, this is not only increasing the hondi transfer but also perhaps abetting the cross-border smuggling by supplying finance for such trade.

Utilization and Development Dynamics of Remittances

The development impacts of remittances may be assessed by the effects remittances have on various short- and long-term micro and macro socioeconomic variables. Again, these impacts are considered to be more in the developing countries with higher poverty incidence and lower financial development density (Giuliano & Ruiz-Arranz, 2009; Jongwanich, 2007). The remitters, who were mostly unemployed in their home countries, have now jobs in overseas places. This may create limited employment opportunities for the others in the home country. Likewise, the remittances they are sending back may help employment generation domestically as well. The latter happens through the reinforcement of remittances-induced national savings, capital accumulation, and investment (Barua et al., 2007). So the direct, trickle down, and indirect benefits of remittances could be significant in aggregate for many of the developing countries.

We argue that the development impacts of remittances on the economy and society are affected by the manner remittances are put to use. We may, however, examine the linkage between remittances and development following the flow paths in Figure 3. The figure lines up the present uses of remittances and links the consequential social and economic effects in the medium to long term. Once received, remittances are put to use in the forms of consumption, saving, and investment by the recipients individually and collectively. Yet, the savings out of remittances can promote them to initiate some entrepreneurial activities for further accumulation of capital. In the process, remittances also help develop soft power 8 of the individual beneficiaries. So what essentially begins as short-term micro-level benefits to individuals and households ultimately becomes a macro-level influencer of economic forces in the medium to long term to benefit the whole economy.

Socioeconomic development linkages of remittances

Uses of Remittances and Impacts on Socioeconomic Factors in Bangladesh

In analyzing the transfer and utilization dynamics of remittances, De Bruyn and Kuddus (2005) find that remittances inflows in Bangladesh happen mostly in the forms of (a) transfer to family and friends and (b) transfer to save or invest, and not much in the forms of (c) transfer to charity or community development and (d) collective transfer to charity or community development. So the impact assessment mainly centers on the first two types of transfers. Sensibly, in those two types of transfers, the recipients are often the father, mother, spouse, other family members or even relatives of near and far.

But how do recipient households in Bangladesh use the remittances they receive? Most of the studies that explored the dynamics of remittances utilization have divided various uses of remittances into two categories, for example, productive and nonproductive expenditures. The terminologies used are instructive of their meaning. Those uses of remittances are considered productive that have been used on assets that increase productive capacity and bring income to the households. The other uses, on the contrary, are nonproductive as they do not help accumulate capital or generate further income for them. In this study, we have, instead, grouped the uses of remittances under two separate categories, for example, consumption and investment to mean nonproductive and productive expenditures, respectively. This has been done to use their aggregate values to calculate the rm for Bangladesh.

To have a better picture of the uses of remittances in Bangladesh, we have summarized the findings Siddiqui and Abrar (2003) in Table 1. We have also included the results of De Bruyn and Kuddus (2005) in the same table to offer a comparative position on some of the uses. It has to be noted that the study of De Bruyn and Kuddus compiles remittance uses data from 21 studies including that of Siddiqui and Abrar. Column 3 in Table 1 has averaged out the range of minimum and maximum percentages of uses for respective heads from the study of De Bruyn and Kuddus. Technically, the figures in Column 3 give a view on the central tendency of the uses of remittances in those studies and amplify the fact that, as a whole, their findings on consumption and investment uses remittances draw nearly a similar picture as has been found by Siddiqui and Abrar (2003).

Bangladesh—Patterns of Utilization of Remittances

Note: Study I: Consumption Total = 66%; Investment Total = 34%.

Sources: Constructed. Study I, Siddiqui and Abrar (2003); Study II, De Bruyn and Kuddus (2005).

In this study, we tend to focus more on the findings of Siddiqui and Abrar (2003) because we have accepted their results as the base for grouping the uses of remittances into consumption and investment and further analysis. They surveyed a total of 100 remittance receiving households in two administrative blocks in two districts of Bangladesh. The survey also included another 20 remittance sending labor respondents in Ajman and Dubai in the UAE. But for our analysis, these also have formed the basis for calculations of the values of MPCR, MPSR, and rm.

To get the consumption estimate of remittances, we now add the recipients’ expenses on items like food and clothes, medical treatment, home construction/repair, repayment of loans, insurance, social ceremonies, gift or donation, sending relative for pilgrimage, furniture, and others. Broadly, these uses in Table 1 together constitute the percentage of remittances used for consumption by the surveyed households. However, all uses in business investment, savings/fixed deposit, purchase of agricultural and homestead land, release of mortgaged land or taking mortgage of land, education cost, community development investment, and sending family members abroad have been added together to calculate the percentage of remittances used for investment. Differences in opinions may exist on the reasoning for grouping the various uses with either one of the two, but we have explained our own kind of reasons for clubbing the uses into the groups of consumption and investment. Differences in opinions may exist on the reasoning for grouping the various uses with either one of the two, but we have explained our own kind of reasons for clubbing the uses into the groups of consumption and investment. However, by adding all the values into two groups, we find about 66%t of the remittances in Bangladesh are used for consumption and the rest 34% are for investment from the study of Siddiqui and Abrar (2003).

As mentioned, various consumption and investment uses of remittances have short- and long-term socioeconomic benefits at the household level in particular. They ultimately go beyond to affect the community and national economy as a whole. In this regard, Table 2 lists some major social and economic indicators and impacts of remittances on them at household and community levels in Bangladesh. It can be seen that indicators like nutrition, living condition and housing, education, health care, social security, and investment of the recipient households have been positively affected by remittances. The correlation between these benefits and remittances needs a bit explanation. As we may understand, the poverty profile of the migrants is important for the social benefits appraisal of remittances because the impact of remittance income on poverty reduction is expected to be more on the poorer households. In Bangladesh, most of the short-term migrant workers are from the poor families of rural areas. So, in most of the cases, remittances form an important part of the household earnings of the recipients and could constitute 51% to 70% of the households’ earnings on an average (Mahmood, 1991; Siddiqui & Abrar, 2003). Afsar, Yunus, and Islam (2002) in their survey find that household income of the migrants increases by 55% once they start sending remittances.

Impacts of Remittances at Household and Community Levels

Source: Hasan (2006), modified from De Bruyn and Kuddus (2005).

So this enhanced income helps loosen the financial constraints of the recipient families, allowing them to spend more on consumer durables, nondurables, health care, physical living condition, and so on. Investment in education, income generating assets, and social security measures also gets increased. So remittance income in the short and long term not only protects the recipients from negative income shock but also contributes to poverty reduction and economic growth (Hasan, 2006). This is corroborated by the GEPs 2006, which suggests that remittances in Bangladesh have helped the poverty headcount ratio decline by 6 percentage points during 1990 to 2006 (Word Bank, 2006).

Remittances and the Macroeconomy of Bangladesh

Remittances now represent an important external source of finance for Bangladesh, and the tentative impacts on macroeconomic development cannot be ignored. Figure 4 gives us a clear view on the growing importance of remittances while compared with GDP, external debt, imports, exports, and FDI flows in the economy, all figures presented at the current price. Evidently, the importance is growing rapidly since 2000.

Bangladesh—Remittances and Major Macroeconomic Indicators, 1980–2009

Let us take some comparative figures in perspective. In 2000, workers’ remittances amounted to 4.2 percent of GDP, 29.7 percent of exports, 12.4 percent of external debt, 699.3 percent of FDI, 23.4 percent of gross domestic savings and 21.6 percent of imports. The critical factor is the relative rise of remittances against external debt and imports. Bangladesh has remained a trade deficit country in most of the years since independence, but in the years onward from 2000, it has been continuously posting current account surplus (the gap between exports and imports of goods, services, and unrequited transfers), mainly because of remittance income. Notably, remittances have emerged to be the single largest source of net factor income from abroad, contributing to offset the pressure of deficit of merchandise trade and to service external debt. As a corollary of the surplus of current account, regular debt servicing, GDP growth, and so on, Bangladesh has bettered its international credit rating. In 2010, the Standard & Poor’s (S&P) assigned Bangladesh its first BB- for long term international credit and a B for short term credit (Wikipedia, 2011).

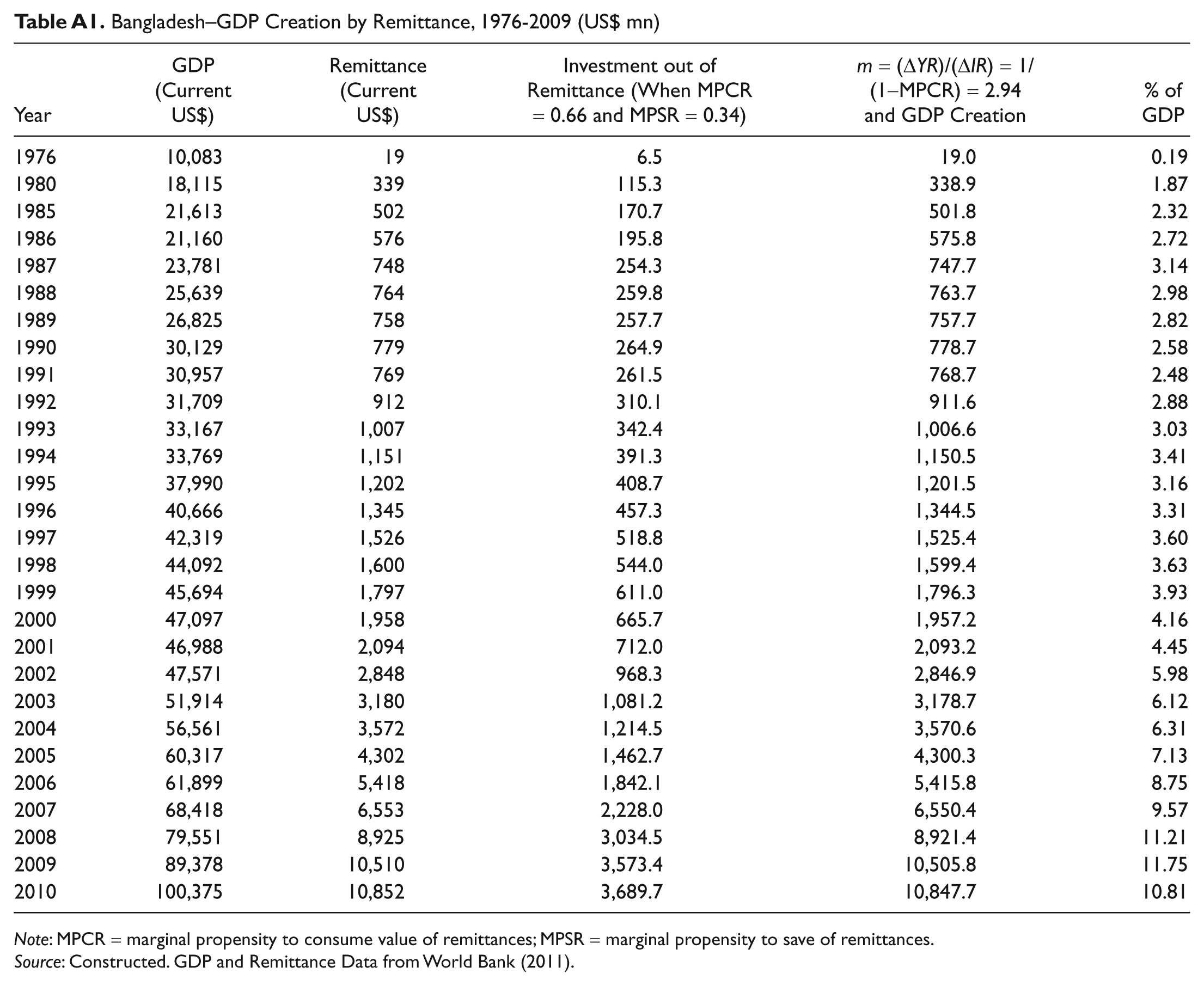

This brings us to the important task of assessing the contribution of remittances to GDP creation in Bangladesh. In doing so, we need to know the MPC for Bangladesh. B. K. Ghosh (2010) identifies that MPC on an average is higher in rural areas than in urban areas, and their average figures were 0.74 and 0.65, respectively, in 2005. We have already estimated from Siddiqui and Abrar (2003) that 66% of remittances received have been used for consumption, whereas the rest 34% are invested. So we consider the “marginal propensity to consume” of remittance and “marginal propensity to save” of remittance values of remittances as 0.66 and 0.34, respectively. Thus, our estimated MPCR looks to be close to the national average of MPC for Bangladesh. Moreover, the MPC of the remittance recipient households may be a bit lower even in the rural areas, given the kind of “elitism” they attain because of higher average income and exposure to cross-border culture.

Appendix Table A1 has been prepared to estimate the GDP creation of remittances income by using rm value as 2.94, calculated on the MPCR value of 0.66. The MPCR value of 0.66, which has been derived from the consumption uses of remittances from Siddiqui and Abrar (2003). The standard multiplier equation, m = (ΔY)/(ΔI) = 1/(1−MPC), has been applied with modification in MPC to make it MPCR and MPS to MPSR. By any measure, this was a substantial contribution. Had all transfers to Bangladesh been done through official channels, the GDP impact would have been calculated at a much higher value. The table shows that remittances created merely US$19 million (or 0.19%) of GDP in 1976. But with a rapid increase of remittances, the figures went up to US$ 6.5 billion (7.13%) in 2005 and then further up to US$10.5 billion (or 11.75%) to GDP in 2009. A marginal decline in the GDP creation by remittances (US$10.9 billion or 10.81%) has been followed in 2010 when growth in inward transfer slowed down considerably.

Have remittances adversely affected the external competitiveness of export trade by putting appreciating pressure on Bangladeshi taka (BDT), the local currency? It has indeed not, as the economy has so far been able to avoid the “Dutch Disease” effects of remittances at macro level due to a continuous depreciation of BDT against the major international currencies over time. For example, whereas US$1 could buy BDT 34.57 in 1990, it could trade against BDT 75.00 in 2011. Interestingly, the depreciation has accelerated since 2003 when Bangladesh adopted fully floated exchange rate. In other words, BDT has lost substantial exchange power during this time. Moreover, the export basket of Bangladesh is still small and is absolutely dominated by the ready-made-garment (RMG) products. To substantiate, the contribution of the RMG sector alone hovers around 77% to 80% of total exports in every year. Importantly, the sector employs a workforce that has huge local pool of labor supply, and a very few of them are remotely linked to the direct benefits of remittances. Furthermore, the domestic value addition in the sector is also increasing through backward and forward linkages of internal resources, and the utilization of import components is declining. All these together have an insulating effect on the most important export sector to remain internationally competitive even during the recession in 2008-2009.

But there are “quasi” Dutch Disease effects present in the remittance-related segments of the economy. It is apprehended that remittances may have contributed to the creation of dependency syndrome among a section of the recipients (De Bruyn & Kuddus, 2005). Such a syndrome usually inspires intentional unemployment, which could affect the allocation of human resources necessary to the development of domestic industries. This may be one of the important reasons that some of the zones that have the most remittance inflows within Bangladesh have less industrial activities. Moreover, superficial signs of inflation are visible in those “pockets of remittances” as prices of housing, land and properties, some food items, and so on are relatively higher than the national average. This robs part of the transferred resources that could have otherwise been used for productive purposes.

Conclusion

This study reveals the magnitude and direction of migration and remittances and the ways remittances are affecting the development of the society and economy as a whole. Plausibly, Bangladesh will remain a labor export franchise in the foreseeable future because of its low level of economic development and a huge surplus labor force that is always ready to fly. So remittances should continue to rise in the economy if the out-migration continues.

As we have seen, migration from Bangladesh is more diverse in terms of destinations. However, an improvement in the composition of female workers abroad could enhance economic empowerment of their families and the returnee female migrants at the end. Moreover, Bangladesh still needs to improve remittance delivery infrastructure so that migrants can avoid informal channels for sending remittances back home. That could help diminish the growth of the unofficial economy by reducing the unrecorded inflows of remittances. It may also minimize the problem of superficial inflation visible in the zones that have most migrants outside the country.

The recipients of remittances use their remittance income for a wide range of purposes, of course a substantial portion for consumption. Because of the higher density of poverty, MPC of remittances is expected to remain high in the future too. That will keep the investment multiplier value of remittance higher. For a better picture of the remittance-beneficiaries, the future Household Income and Expenditure Surveys in Bangladesh should identify the population that are benefitted by remittances in every quintile.

Remittances now weigh more importantly against many other macroeconomic variables. By offsetting the pressure of the deficits of merchandise trade balance, remittances have helped Bangladesh improve international credit rating. Moreover, a significant contribution of remittances in GDP creation makes it more important to the socioeconomic development of Bangladesh. Although the quasi Dutch Disease effects of remittances may have affected some small segments of the economy, Bangladesh has so far been able to avoid the “Dutch Disease” effects on real exchange rate. It seems that remittances have not added appreciating pressure to make export trade costlier. Rather, the depreciation of BDT on a continuous basis over time has warded off possible impacts on export trade. However, it is plausible to argue that the depreciation could have been much higher with much lower remittance inflows.

Footnotes

Appendix

Bangladesh–GDP Creation by Remittance, 1976-2009 (US$ mn)

| Year | GDP (Current US$) | Remittance (Current US$) | Investment out of Remittance (When MPCR = 0.66 and MPSR = 0.34) | m = (ΔYR)/(ΔIR) = 1/(1−MPCR) = 2.94 and GDP Creation | % of GDP |

|---|---|---|---|---|---|

| 1976 | 10,083 | 19 | 6.5 | 19.0 | 0.19 |

| 1980 | 18,115 | 339 | 115.3 | 338.9 | 1.87 |

| 1985 | 21,613 | 502 | 170.7 | 501.8 | 2.32 |

| 1986 | 21,160 | 576 | 195.8 | 575.8 | 2.72 |

| 1987 | 23,781 | 748 | 254.3 | 747.7 | 3.14 |

| 1988 | 25,639 | 764 | 259.8 | 763.7 | 2.98 |

| 1989 | 26,825 | 758 | 257.7 | 757.7 | 2.82 |

| 1990 | 30,129 | 779 | 264.9 | 778.7 | 2.58 |

| 1991 | 30,957 | 769 | 261.5 | 768.7 | 2.48 |

| 1992 | 31,709 | 912 | 310.1 | 911.6 | 2.88 |

| 1993 | 33,167 | 1,007 | 342.4 | 1,006.6 | 3.03 |

| 1994 | 33,769 | 1,151 | 391.3 | 1,150.5 | 3.41 |

| 1995 | 37,990 | 1,202 | 408.7 | 1,201.5 | 3.16 |

| 1996 | 40,666 | 1,345 | 457.3 | 1,344.5 | 3.31 |

| 1997 | 42,319 | 1,526 | 518.8 | 1,525.4 | 3.60 |

| 1998 | 44,092 | 1,600 | 544.0 | 1,599.4 | 3.63 |

| 1999 | 45,694 | 1,797 | 611.0 | 1,796.3 | 3.93 |

| 2000 | 47,097 | 1,958 | 665.7 | 1,957.2 | 4.16 |

| 2001 | 46,988 | 2,094 | 712.0 | 2,093.2 | 4.45 |

| 2002 | 47,571 | 2,848 | 968.3 | 2,846.9 | 5.98 |

| 2003 | 51,914 | 3,180 | 1,081.2 | 3,178.7 | 6.12 |

| 2004 | 56,561 | 3,572 | 1,214.5 | 3,570.6 | 6.31 |

| 2005 | 60,317 | 4,302 | 1,462.7 | 4,300.3 | 7.13 |

| 2006 | 61,899 | 5,418 | 1,842.1 | 5,415.8 | 8.75 |

| 2007 | 68,418 | 6,553 | 2,228.0 | 6,550.4 | 9.57 |

| 2008 | 79,551 | 8,925 | 3,034.5 | 8,921.4 | 11.21 |

| 2009 | 89,378 | 10,510 | 3,573.4 | 10,505.8 | 11.75 |

| 2010 | 100,375 | 10,852 | 3,689.7 | 10,847.7 | 10.81 |

Note: MPCR = marginal propensity to consume value of remittances; MPSR = marginal propensity to save of remittances.

Source: Constructed. GDP and Remittance Data from World Bank (2011).

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

The author(s) received no financial support for the research and/or authorship of this article.