Abstract

According to the European Commission's Sustainable Finance Strategy, the financial system has a key role to play in promoting sustainable development toward a greener and more sustainable economy. Small and Medium-sized Enterprises (SMEs) represent over 99% of all European businesses and are responsible for around 60% of all business greenhouse gas emissions. Small and Medium-sized Enterprises are therefore crucial to the success of the European Union's sustainability transition. The share of sustainable finance for SMEs will grow both as a result of increasing sustainability legislation and the expectations of customers and stakeholders. However, integrating sustainability can be challenging for SMEs due to limited resources and expertise. The article highlights the importance of clear, transparent, and implementable contract documents as tools to enhance sustainability in financing. Proactive contracting and legal design approaches are discussed as means to transform contracts into management and communication tools, to promote sustainable business practices.

Introduction

Within the framework of the European Green Deal, the European Commission announced the renewed Sustainable Finance Strategy in 2021. 1 A part of the strategy is the European Commission's Action Plan “Financing Sustainable Growth” 2 (hereinafter Action Plan), which is one of the key actions to implement the Paris Agreement 3 and the United Nations’ UN 2030 Agenda for Sustainable Development. 4 According to the Action Plan, the financial system has a key role to play in promoting sustainable development toward a greener and more sustainable economy. 5 The Action Plan aims to redirect capital flows toward sustainable investment to achieve sustainable and inclusive growth; to manage financial risks arising from climate change, resource depletion, environmental pollution, and social issues; and to promote transparency and sustainability in financial and economic activities. According to the European Commission, Small and Medium-sized Enterprises 6 (SMEs) represent more than 99% of all European businesses and are responsible for around 60% of all business greenhouse gas emissions. Small and Medium-sized Enterprises are therefore crucial to the transformation to sustainability. 7 However, SMEs often face human resource constraints, including limited expertise and skills which may challenge the effective integration of sustainability into their business operations and the execution of a sustainability transition as compared to large companies. 8

One important way to promote a greener and more sustainable economy and to redirect capital flows toward sustainable investments is corporate finance. Influencing businesses through finance is effective, as companies often need equity or debt finance when they invest or expand their business. The increasing legislation on sustainability alongside banking legislation has led, relatively quickly, to a situation where banks have a strong interest in promoting sustainable finance and ensuring that the companies they finance are aware of their ESG risks (pertaining to environmental, social, and governance factors) and taking steps to manage them. Borrowers (client companies) also have many incentives to promote sustainable investments and to utilize sustainable finance. In addition to sustainable legislation, ESG-linked investments are signals to stakeholders, such as lenders, investors, and customers, indicating a company's commitment to ESG objectives and practices. It is therefore also a question of the company's reputation. Another important incentive is that ESG factors may affect the cost and availability of business finance. 9

Sustainable finance generally refers to ESG considerations when making investment decisions in the financial sector, leading to more long-term investments in sustainable economic activities and projects. Sustainable corporate finance solutions can be divided into two categories (ESG loans 10 ): Sustainability-Linked Loans and Green Loans. Sustainability-linked loans can be used for general corporate purposes. They are linked to the sustainability performance of the borrower, measured against ESG criteria. Green loans, on the other hand, proceed directly to finance projects with explicit environmentally friendly purposes. Currently, ESG loans are typically issued to larger companies. However, the new European Union (EU) directive on corporate sustainability reporting 11 and proposal on corporate sustainability due diligence directive (CSDDD) 12 set new requirements concerning ESG obligations affecting a wider range of companies including their value chains and subsidiaries of EU companies and EU subsidiaries of non-EU companies. Moreover, the expectations of stakeholders and customers, as well as other sustainability legislation, commitments, and guidelines, already affect SMEs indirectly through contractual cascading in the value chains of large companies. To sum up, sustainability is becoming a more tangible part of SMEs’ business operations, and the share of SMEs in sustainable finance is increasing.

Loan agreements play a crucial role in committing borrowers to sustainability and advancing ESG goals in their business practices. 13 It is therefore important that contract documents avoid complex clauses and jargon, and sustainability factors are expressed in an understandably and unambiguously way. Clear and measurable ESG clauses in contracts also ensure that the lender receives adequate and accurate data over the life of the loan to monitor their clients’ sustainability performance and reduce the risk of greenwashing.

This article discusses how to promote responsible and sustainable contracting in SMEs’ sustainable finance loan agreements through proactive contracting and legal design approaches. The aim is to study how multiprofessional collaboration and user-centered contract design can simplify ESG-related clauses in contract documents, how to make them visible through information design methods, how to enhance a common understanding between contracting parties, and how to contribute to the achievement of ESG objectives in day-to-day business practices. Although the EU sustainability legislation extends its impact beyond Europe through corporate value chains, this article focuses on SMEs’ loan agreements at the European level.

The structure of the article is as follows. First, it provides a brief overview of the regulatory framework for sustainable finance that is relevant to the content of the article. Second, it presents ESG loans as a form of sustainable finance. Third, it outlines ways to improve contractual effectiveness and achievement of objectives through proactive contracting and legal design approaches. Fourth, it introduces different types of information design tools and provides examples to illustrate them. Finally, concluding remarks are presented.

Impacts of sustainability requirements on the finance of SMEs now and in the future

Sustainability is a central focus both in the EU and globally, as evidenced by numerous laws, commitments, and guidelines. Examples include Article 3 of the Treaty EU 2012/C326/01 addresses sustainable development. 14 The adoption of international agreements such as the Paris Agreement and the United Nations 2030 Agenda for Sustainable Development have further highlighted the importance of sustainability. The Green Deal, approved in 2020, is a comprehensive set of measures and policy initiatives that aims to make the entire EU economy sustainable for the benefit of both citizens and businesses (European Commission 2019). The ultimate goal is to achieve climate neutrality by 2050. The European Climate Law (EU 2021/1119) also makes the Green Deal targets legally binding and requires EU institutions and Member States to take the necessary measures at the EU and national levels to achieve the climate neutrality target.

The Sustainable Finance Strategy sets out a number of initiatives to address climate change and other environmental challenges. It also aims to increase the involvement of SMEs as the EU moves toward a sustainable economy. 15 Legislation on sustainability at the EU level has increased significantly over the past decade and this trend is continuing. This increase can be compared to the increase in banking legislation, and one can even speak of a tsunami of sustainability legislation. As mentioned in the introduction, currently the legislation, with mandatory reporting requirements, mainly affects large companies, but sustainability is also becoming increasingly tangible in the business of SMEs. Alongside new legislation proposals, the growing expectations of stakeholders, such as partners, suppliers, financiers, customers, and shareholders, are driving this change and shifting social attitudes toward sustainable business practices.

In the context of this article, the key EU sustainability legislation projects that have or will have a direct or indirect impact on SMEs and their finance are the Taxonomy Regulation (EU 2020), the Corporate Sustainable Reporting Directive (CSRD), 16 and the Directive on CSDDD proposal. 17

As part of the Action Plan and legislation of financial markets, the European Commission adopted the Taxonomy Regulation 18 (hereinafter Sustainable Finance Taxonomy). 19 The Sustainable Finance Taxonomy is the first EU-wide classification system to define what types of investments and financial projects are considered environmentally sustainable 20 (Article 4). The aim is to direct capital toward sustainable business and sustainable development investments and to support the green transition and the goals of the Green Deal. 21 The European Commission has established the Platform of Sustainable Finance based on the mandate set out under the Sustainable Finance Taxonomy 22 (Article 20). The platform serves as an advisory body to support the development of sustainable finance and the EU Taxonomy Regulation. Moreover, in 2022, the new ISO Standard of Sustainable Finance has been introduced to offer guidance on integrating crucial sustainability principles into organizations’ operations and business strategies. This ISO standard can help companies demonstrate their adherence to sustainability practices and principles. 23

To speed up and enhance sustainability-related information processes, the CSRD will be phased in from the beginning of 2024. The directive will extend the current Non-Financial Reporting Directive 24 and introduce new, much broader mandatory sustainability reporting standards. Furthermore, the scope of the CSRD is much broader than that of the NFRD and it will also apply to listed SMEs from the beginning of 2026. 25 Other SMEs and listed microenterprises are excluded. However, despite the limits, reporting requirements will extend to SMEs from the outset, because reported sustainability information should contain information on the entire value chain of the reporting company, including its business relationships and value chain within and outside the EU 26 (Recital 33). Thus, reporting requirements for large companies extend to SMEs through the value chains of large companies. This implies that large companies should consider the requirements when contracting with SMEs in their value chains. Moreover, SMEs are strongly encouraged to follow the simplified reporting system on a voluntary basis. The European Commission argues that ESG disclosure will become common practice in the near future and will form a basis for many other transactions, such as financial transactions. It can also provide a basis for better dialogue and communication between companies and their stakeholders and help companies improve their reputation 27 (Recital 12).

Complementing the CSRD, the European Commission adopted a proposal for a CSDDD in February 2022. The goal of the CSDDD is to promote sustainable and responsible corporate behavior and to integrate human rights and environmental considerations into companies’ operations and governance, including their global value chains. The proposal sets out new legislation that will require all large companies and some SMEs (more than 250 employees and annual turnover exceeding €40 million) in specific industries (e.g., textiles, agriculture, forestry, and mining) and non-EU companies meeting certain criteria to assess and identify the negative environmental and human rights impact of their activities, including in their value chains 28 (Article 2). 29 Furthermore, according to the CSDDD proposal companies should enforce their sustainable due diligence measures in situations where they have factual control, i.e., either through direct contracts or where control could be exercised by the company through contractual cascading or other leverage in indirect business relationships. 30 This indirectly affects SMEs and also obliges them to implement sustainable due diligence measures further in their value chains.

Thus, regardless of how the legislation proceeds, it is clear that the legislation of sustainability already impacts SMEs indirectly through value chains. Large companies, including those in the financial sector, have a need and desire to manage their value chains carefully. Although sustainability reporting is voluntary for SMEs, they may need to comply with reporting requirements to meet the reporting needs of financiers and stakeholders in their value chain. Moreover, banking legislation indirectly requires banks to consider ESG risks 31 in their customer finance. Banks’ credit risks, including the ESG risks of borrowers, affect their capital and risk requirements. The higher the perceived risk of the borrower, the higher the credit risk to the bank and the higher the capital requirement for the bank associated with the loan. 32 According to the Action Plan, the European Commission will consider whether further capital requirements could be adopted to better reflect the bank's ESG risks. 33 The European Banking Authority (EBA) has also issued guidelines on how sustainability issues should be considered as part of banks’ lending processes (EBA). The guidelines clarify how banks should assess and manage ESG risks and recommend how ESG risks should be monitored during the maturity period. The EBA guidelines apply to all borrowers, including those who do not report on sustainable issues. Therefore, the challenge in complying with these guidelines is to obtain information from those borrowers, such as SMEs, who do not report on sustainability. 34

In summary, the current sustainability legislation does not directly affect SMEs. However, the legislation has an indirect impact on them through contractual cascading, where large companies pass on sustainability requirements and obligations in their value chains. Future legislation will also have a direct impact on some SMEs. Moreover, SMEs have other incentives to promote their sustainability. One such incentive is the positive impact of sustainable business practices on the cost of and access to finance. Sustainability practice and reporting are also ways for both financiers (lenders) and borrowers (client companies) to credibly signal to stakeholders, such as investors and customers, how committed they are to ESG practices and objectives. The assumption is therefore that sustainable finance solutions (ESG loans) will be increasingly extended to SMEs. The next section provides a more detailed analysis of ESG loans and highlights the challenges that SMEs may face in relation to ESG loans.

ESG loans in a nutshell

“Sustainable finance” in general refers to environmental, social, and governance considerations in making investments and loan decisions in the financial sector. The aim of sustainable finance is to enhance the role of finance in promoting sustainable growth by funding society's long-term needs and integrating environmental, social, and governance factors into investment decision-making. 35

In corporate finance, there are two main categories of ESG-related loans (also called ESG lending 36 ): Sustainability-Linked Loans (also called ESG-Linked Loans) and Green Loans. A sustainability-linked loan is a general-purpose loan, that is, not a specific sustainable asset or investment. The loan clauses are linked to the borrower's predefined sustainability performance targets measured by predefined key performance indicators such as reduction of greenhouse gas emissions, increased use of renewable energy, or by using external ratings and/or equivalent indicators. The aim of sustainability-linked loans is to enhance the borrower's ESG profile by aligning the loan agreement clauses with borrowers’ sustainability performance targets. The clauses of the loan are adjusted based on the borrower's performance in meeting these targets, and the loan's pricing is typically pegged to this performance. Failure or achievement of the targets will only have an economic impact and will not constitute an event of default that would allow the lender to demand repayment of the loan. If the targets are met, it means a lower interest rate (margin rate) and, if not, the rate may be higher. It may also be easier to access the loan with sustainability impacts. 37 So far, the sustainability elements have typically been related to environmental issues, but they are gradually being expanded to encompass social and governance factors as well. Green loans, in turn, proceed directly to finance projects and assets with explicit sustainable environmentally friendly features, such as renewable energy, energy efficiency, clean transportation, sustainable water, and wastewater management. To ensure that all market participants have a clear understanding of what constitutes a green loan, the Green Loan Principles outline categories for eligible green projects based on the following four components: (1) the use of proceeds, (2) the process of project evaluation and selection, (3) management of proceeds, and (4) reporting. These components ensure that projects deliver clear environmental benefits that are assessed, measured, and reported by the borrower. 38

To simplify, these two ESG loan categories differ in terms of their intended purpose. A common feature, however, is that the borrower reports to the lender on a regular basis, usually annually, on the achievement (or nonachievement) of the objectives set out in the loan agreement clauses. Through this reporting, the lender monitors that the assets or investments financed by the loan and the sustainability objectives of the loan are contributing to the objective or purpose as expected. In practice, the reporting requirement means increased data collection by the borrower. While banks have analysts and experts on sustainability issues, the knowledge and expertise of borrowers are crucial, as they are the primary experts on their own operations. 39

There is already some research on how loan agreements indirectly shape and influence companies’ ESG policies and commitment to sustainability. 40 As stated earlier in this article, borrowers have in addition to legislation several incentives to comply with the clauses agreed in loan contracts, such as loan pricing, stakeholder requirements, and reputation. However, SMEs may face challenges in producing the necessary and reliable data, as they may not have the same level of knowledge and resources as large companies. It has been stated that reporting requirements for SMEs need to be adapted to their capacity and simplified. 41 Another problem may be implementing the requirements and sustainability issues as part of the overall operations of SMEs.

This section focused on two main categories of ESG loans: Sustainability-Linked Loans and Green Loans. The key difference between these loan categories lies in their focus. Sustainability-linked loans are linked to the overall sustainability performance of the company, while green loans specifically finance sustainable projects and assets. However, both types of loans share a common goal: to encourage companies to transition their operations toward greater sustainability by imposing certain criteria and requirements on their operations. In addition, the section explored the challenges that SMEs may face in relation to ESG loans compared to large companies due to their limited resources to generate all the necessary information and implement the requirements and sustainability issues in their operations.

I argue that the way in which sustainability-related clauses are framed in contracts is crucial to the promotion, implementation, and reporting of sustainability, particularly in SMEs. The clauses have to be clear, understandable, unambiguous, and tangible to be implemented in business. They must support a common understanding between the parties and those implementing the contract. This requires a shift from a legal perspective in contract drafting to a more comprehensive contract design process that is based on a proactive approach to contracts and collaboration between multiple professions and disciplines. This is discussed next.

The role of proactive approach and design in making sustainability visible and monitorable in loan agreements

Proactive contracting

The concept of proactive contracting was introduced by legal scholar and practitioner Helena Haapio in 1998. In her conference paper, she defined proactive contracting as an approach “recognizing and making use of contracts and contracting processes as planning tools to guide and support the success of your business. It provides the support needed to identify opportunities in time to take advantage of them—and potential problems in time to take preventive action”. 42 As her statement points out proactive contracting approach has two dimensions: preventive and promotive. The preventive dimension emphasizes identifying potential problems, preventing them, and minimizing the impact of unavoidable risks. The promotive dimension on the other hand emphasizes the positive, proactive dimensions of contracts by seeing them as tools for promoting business success, enhancing opportunities, and fostering collaboration and relationships. The aim is that contracts must not only be legally binding and in line with legal principles and established business practices, but they must also be operationally effective and functional. 43 Proactive contracting embraces also the relational aspects 44 of contracts and emphasizes the relationship between a formal contract and relational governance. It aligns with the ideas of relational contract theory but is more practice-oriented, providing practical tools for implementing the ideas of relationalists in the context of contract design. 45 Haapio's conference paper initiated academic work on a proactive approach to business contracts. Soon after, other scholars and practitioners became interested in the approach and continued to develop it. Since then, the proactive approach has developed worldwide, with numerous conferences, books, and articles on proactive contracting and proactive law. 46 The proactive approach has also been adopted by the European Economic and Social Committee in 2009 47 as a part of the EU's Better Regulation strategy (European Commission).

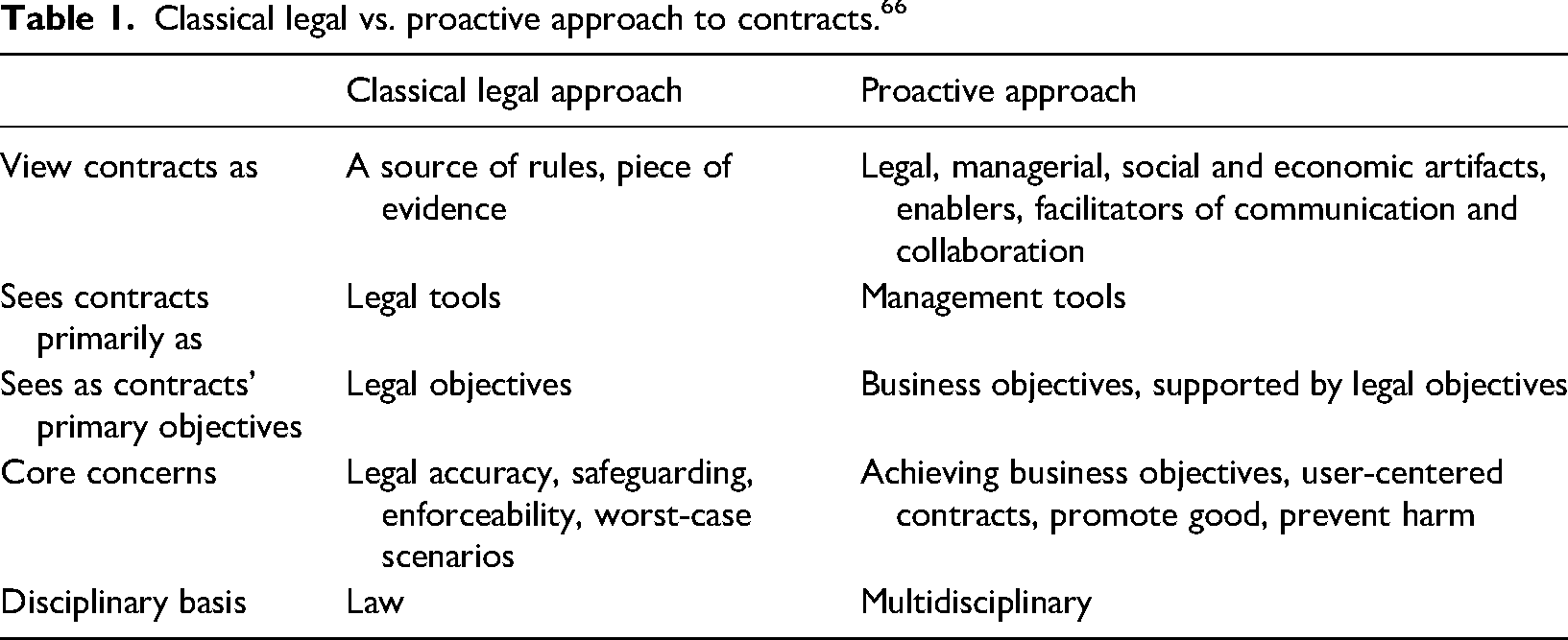

From Haapio's statement above, one can identify three main perspectives that distinguish the proactive approach from the classical legal approach to contracts. These perspectives can also be applied to the analysis of ESG loan contracts. First, the proactive approach shifts the focus of the goals of contracts. According to the classical view, contracts are perceived as legal tools that prioritize legal goals and interests. Contracts are detailed agreements defining the obligations and rights of the parties involved, including safeguarding clauses to secure a company's own interests and position in the event of disputes. 48 The proactive approach, on the other hand, regards contracts not only as legal tools but also as management tools. Therefore, contracts are considered legal, economic, managerial, and social artifacts. 49 This reflects the fact that contracts have multiple functions. However, according to contract research, safeguarding still seems to be the most common function of business contracts. 50 Moreover, it is common for many businesspeople to perceive contracts as a necessary time-consuming evil, as an administrative burden, or as an obstacle to decision-making. 51 Contracts are not considered valuable intangible assets, nor tools for producing tangible assets. It is important to manage risks through contracts. The function of contracts is, among other things, to anticipate and prevent problems, minimize the impact of unavoidable risks, and manage and resolve conflicts. However, the risk management and safeguarding function should not be prioritized at the expense of other contract functions. Functions such as promoting business and fostering collaboration between the contracting parties are equally significant. More precisely, contracts serve as tools for coordinating and managing business; achieving benefits; creating, allocating, and protecting value; communicating, sharing, minimizing, and managing risks; preventing problems; and safeguarding the parties’ rights. 52 ESG loan agreements have these functions and goals as well. They aim to manage risk, enhance business, and foster relationships between the contract parties. Moreover, ESG loan agreements must support the implementation of sustainability objectives. The clauses of a contract must be clear and specific enough to ensure that ESG reporting from the borrower to the lender is adequate, accurate, and correct. Otherwise, on environmental issues, incomplete information may give the impression of greenwashing.

The second perspective that distinguishes the proactive contracting approach from the classical one is that the latter views contracts from an ex-post perspective. The classical approach increases the tendency of lawyers to prepare for ex-post interpretation of contracts in court, resulting in an emphasis on worst-case scenarios. 53 The proactive approach, in turn, is about foresight instead of hindsight. It aims to ex ante detection and exploitation of opportunities that will enable business success. 54 In ESG loans, the proactive approach is crucial. The borrower is obligated to regularly report to the lender the progress of meeting the ESG goals tied to the loan. In order for the lender to receive the necessary and adequate information in time, the sustainability-related clauses have to be designed from the viewpoint that it is practically possible for the borrower to fulfill this obligation. It can be challenging, if not impossible, for the lender ex-post alone to find out all the factors affecting the borrower's sustainability. 55 Being proactive rather than reactive in the contract design process helps both the borrower and the lender to achieve their goals: reporting by the borrower and monitoring by the lender.

The third way in which the proactive contracting approach differs from the classical legal view is that instead of solely relying on contract documents, it views contracts as a continuous and evolving process throughout a business relationship. In line with Winston Churchill's statement, “War is too important to be left for generals,” Haapio also stated in the title of her conference paper that “contracts are too important to be left to lawyers”. 56 The classical approach to contracts puts lawyers at the center of the contract drafting process, rather than viewing contracts more from the business perspective. 57 However, the business perspective should not play a secondary role and the law should only be one of the tools in contract drafting. 58 Collaboration among multiple professionals is necessary for contracts to foster the core values of businesses and to enable business success, good customer relationships, and effective management. 59 Contracts consist of various aspects, notably the legal, business, financial, technical, and implementation aspects, and all these aspects should form a functional and compatible whole. 60

The integration of legal knowledge and various areas of expertise within an organization is crucial, as different professionals have varying individual contract skills. To produce better contracts, companies should enhance their contract capabilities, and the individual contract-related skills of members of the organization should be combined to form an organizational contracting capability. 61 This approach allows organizations to utilize the individual strengths within the company to design, maintain, and manage contracts and contract processes effectively. 62 Also, in terms of ESG loans, this means that a collaborative effort, involving not only legal and sustainability experts but also a wide range of business experts is crucial in the contract design process. When aiming for operationally effective and functional contracts, it is important to take the users’ perspective into account. 63 The goal is that contract clauses are appropriate and effectively applicable to the business at hand. This also requires considering the contractual processes at the customer interface, which means ensuring that the customer understands what it is committing to and what the contract requires from its business practices.

The following table (Table 1) summarizes the main differences between the classical legal approach and the proactive approach to contracts mentioned above.

Classical legal vs. proactive approach to contracts. 66

In this section, the proactive contracting approach was explored, identifying three main perspectives that distinguish it from the classical legal approach to contracts. These perspectives are not only relevant and applicable in general but also within the context of ESG loan agreements. First, proactive contracting recognizes that contracts have multiple functions beyond being legally binding. It emphasizes that contracts must not only be legally binding but also serve to coordinate and manage the business and be operationally effective and functional. The second point was the ex-ante perspective of contracts. The objectives of contracts are ex ante to identify potential problems, prevent them, minimize the impact of unavoidable risks, and emphasize the positive, proactive dimensions of contracts by seeing them as tools for promoting business success, enhancing opportunities, and fostering collaboration and relationships. Thirdly, it was pointed out that proactive contracting perceives contracts as a continuous and evolving process, focusing not only on the contract documents but also on the processes involved. This approach emphasizes multiprofessional collaboration.

The proactive contracting approach is influenced by various research fields, disciplines, and theories. 64 One of the key disciplines involved is design, with the primary aim of enhancing the user-centredness, accessibility, and usability of both contract documents and contract processes. The use of design in legal domain will be discussed in more detail in the next section.

The concept of legal design

Like proactive contracting, design, and design thinking have their roots in several disciplines. What design thinking means depends on where, by whom, and for what purpose it is used. As a theoretical framework, design thinking is a problem-solving technique in which the principles of design are applied to generate new, innovative, improved, and more efficient solutions. 65 Despite the various perspectives, design thinking is characterized by user-centeredness and a multidisciplinary approach. 67

Legal design merges legal and design thinking, but it even goes beyond design thinking. It is more like design doing, and applying design thinking in the real world by working in a design mode. 68 According to the Legal Design Alliance, an interdisciplinary network of academics and practitioners in law, design, and other disciplines, legal design “applies human-centered design to the world of law to enable desirable outcomes and prevent the causes of problems from arising and developing into conflict and disputes”. 69 It is a collaborative approach that combines the legal expertise of a lawyer with the creative mindset and methodologies of a designer, as well as the potential of technology. The goal of the legal design is to create legal outcomes that are not only useful and usable but also engaging and understandable to the users. The aim is to make legal information and services easier to understand and use, particularly for nonexperts. 70 However, it is important to note that legal design is not a synonym with contract document design. The same user-centered methodology can also be applied to solve problems in other legal domains, including also legal, services, processes, and systems. 71

This section examined the concept of legal design and presented a brief overview of design thinking and its application in the field of law. The aim of the legal design is to make legal information and services user-centered, understandable and, improve communication and knowledge sharing between the stakeholders involved. As mentioned above legal design is a methodology that can be applied to different areas of law, including contracts. The integration of legal thinking with design doing and the transition from contract drafting to contract design are discussed next.

The shift from contract drafting to contract design

There is no unambiguous definition of contract design. Various disciplines have presented different perspectives. Among legal scholars, the term has traditionally been used as a synonym for contract planning and drafting. 72 In organizational studies, contract design is related to transaction costs, governance, and the psychological impact of contracts. 73

The pioneers of proactive contracting and contract design have described contract design as an effort to integrate strategic business decisions, business objectives, and legal knowledge by collaborating with various professionals such as managers, lawyers, technical experts, salespeople, designers, contract implementers, and other professionals. The goal of this collaborative effort is to increase the likelihood of business success, minimize risks and disputes, and foster collaboration between contracting parties. By combining the expertise and perspectives of a diverse group of professionals, contract design seeks to align business objectives with legal requirements while creating contracts that are effective, efficient, and mutually beneficial. 74 Overall, contract design encompasses both the design of contract documents—content, structure, language, and layout—and the design of contract processes and their integration into business processes. 75 Emerging technologies provide new opportunities to contribute to the change from contract drafting to contract design. 76

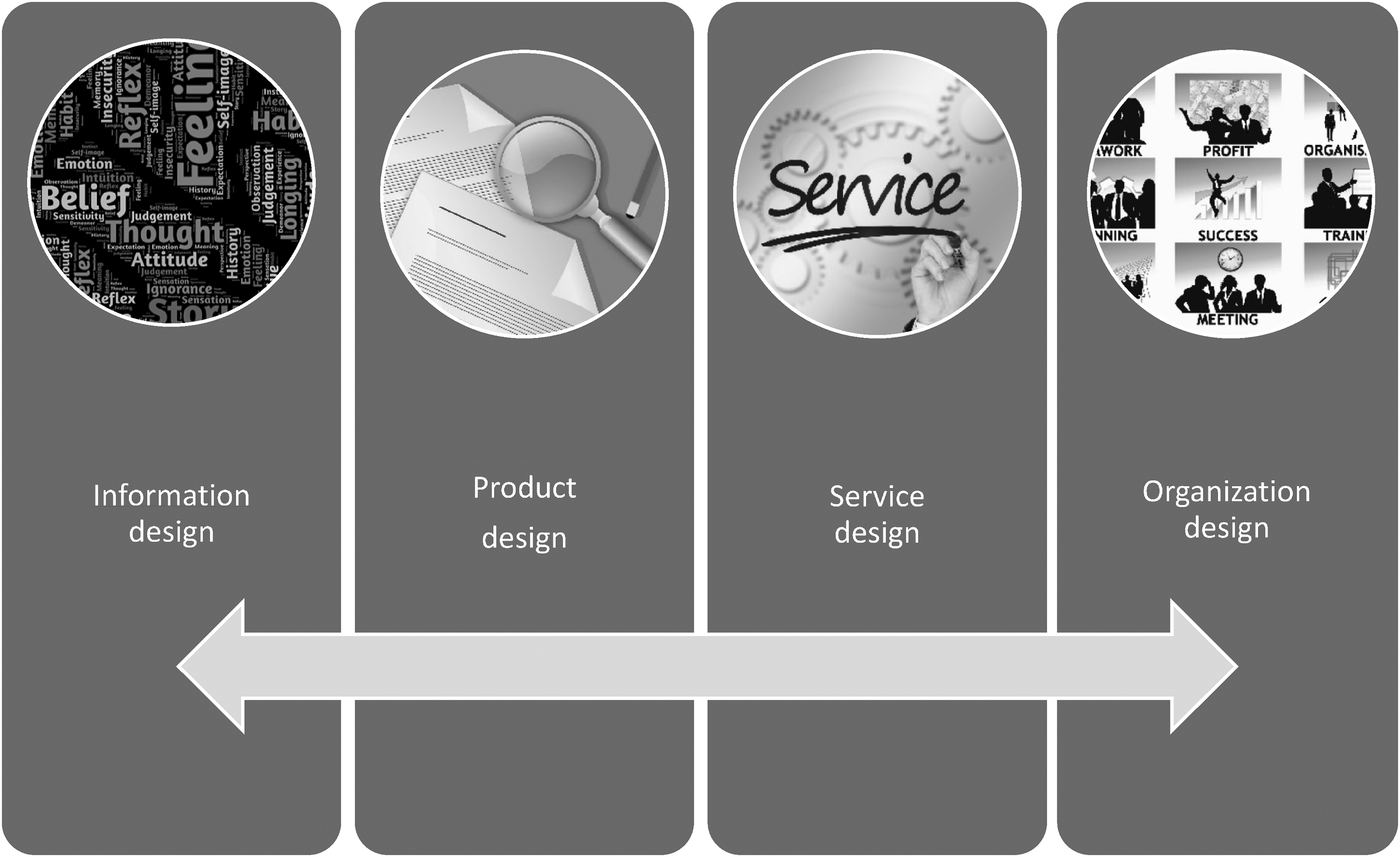

The application of various design domains in shifting from contract drafting to contract design is illustrated in the context of this article in Figure 1.

Design domains that can be utilized to shift from contract drafting to contract design.

In the context of contracts, information design involves the production, processing, communication, and utilization of information during the contract process. This includes also designing the language, content, structure, and layout of contract documents with an emphasis on using plain language, simple sentence structures, and visual elements such as icons, diagrams, charts, and other design patterns. 77 The objective of information design is to enhance the effectiveness and accessibility of contract documents by presenting the information in a manner that is understandable, accessible, and actionable. By leveraging visual and other design elements, information design helps to minimize ambiguity, reduce complexity, and increase the likelihood that parties will understand the contract clauses. 78 Product design considers contracts as legal, economic, managerial, and social artifacts that function as tools for management, communication, knowledge sharing, and collaboration. 79 Service design focuses on designing customer interface contract processes. The goal is to improve the customer experience and to ensure the efficient implementation of contracts. 80 Organization design provides tools for designing internal contract processes, improving organizational structure, fostering cooperation between organizational actors, and developing policies. The aim is to enhance an organization's contract capability. 81

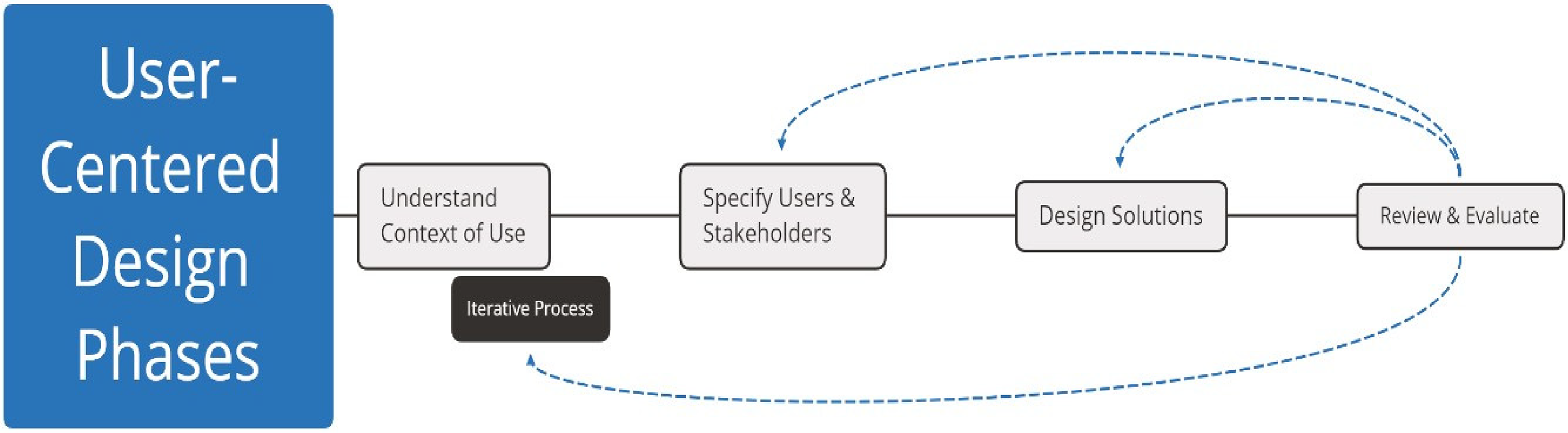

As with any design process, the contract design process is a cyclical and iterative process with multiple stages that can be repeated in any order (on the design process). 82 The starting point is to identify and define the users, understand the context of use, and establish the objectives of the project. The next step is to develop and test different solutions, review and evaluate the outcome, and make modifications as necessary. 83 The process is illustrated in Figure 2. 84

User-centered design phases. 88

This section focused on the concept of legal design in the context of contracting. Contract design is a cyclical and iterative process that involves the integration of strategic business decisions, legal knowledge, and collaboration with various professionals to align business objectives and create effective contracts. It encompasses the design of contract documents and processes, using methods from information design, product design, service design, and organizational design. Information design focuses on enhancing accessibility, understanding, and actionable information through paying attention to language, structure, and the use of visual elements in contracting processes and contract documents. Product design views contracts as versatile tools for management, communication, and collaboration. Service design improves the customer experience and ensures efficient contract implementation. Organizational design in turn enhances internal processes, collaboration, and policy development.

The following section delves deeper into the concept of information design and demonstrates its application through examples.

Making sustainability information visible and monitorable through information design

The pioneers of plain language have stated that ask ten people to define information design, and you are likely to get as many different answers. In the context of contracts, information design can be defined as the overall process of developing a successful document and presenting information in it. 85 More precisely, it can be defined as “the process of identifying, selecting, organizing, composing, and presenting information to an audience so that it can be used efficiently and effectively by that audience to achieve a specific purpose”. 86 The aim of information design is to ensure that people using information find what they need, understand what they find, and are able to use the information appropriately. 87 Moreover, in the context of contracts, the aim is to produce contracts that support shared understanding—both between the parties of the contract and between actors within the organization—and effective implementation of the contracts. Information design tools, such as visualization, plain language, layering, and design patterns, help to simplify complex information, make it easier to understand and accessible, and streamline the contract design process. 89

The following examples (Figures 4 and 5) illustrate the application of information design to contracts. The aim of the design is to create user-centered and easy-to-understand contract documents that encourage borrowers to read and engage with the contract.

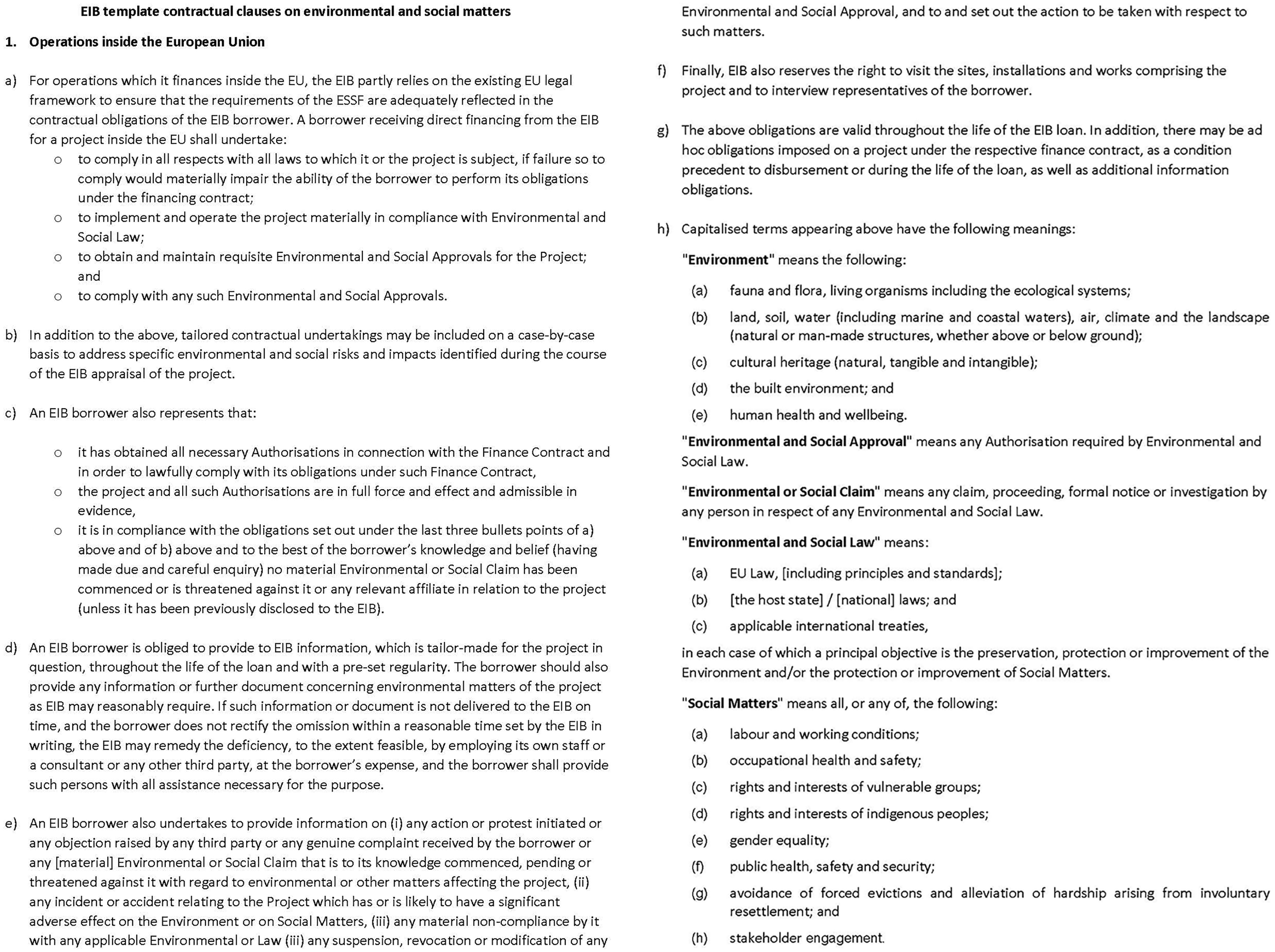

European Investment Bank. Template contractual clauses on environmental and social matters (January 2023). The template clauses referred to above are for reference purposes only and may not reflect the precise terms concluded under specific operations. Reflecting the risk-based approach which EIB adopts with regard to environmental and social risks and impacts, individual finance contract provisions may vary as a function of the nature and characteristics of the operation and the findings of the appraisal carried out by EIB staff for the purpose of the financing. In conducting its appraisal and determining which risks and impacts may be relevant to an operation, EIB will have regard to the EIB Group Environmental and Social Policy and to the EIB Environmental and Social Standards (together the Environmental and Social Sustainability Framework (ESSF)). Used with permission.

(Redesigned by Aino Kännö 2022. Used with permission).

The aim of the redesign of the template contractual clauses (Figure 3) was to overcome various communication barriers that may hinder effective communication and lead to interpretational issues. These barriers encompass elements such as small print, complex language, complex sentence structures, and vague terms (such as materially and reasonable). Moreover, the aim was to avoid the “wall of text effect” and lengthy text blocks.

(Redesigned by Aino Kännö 2023. Used with permission).

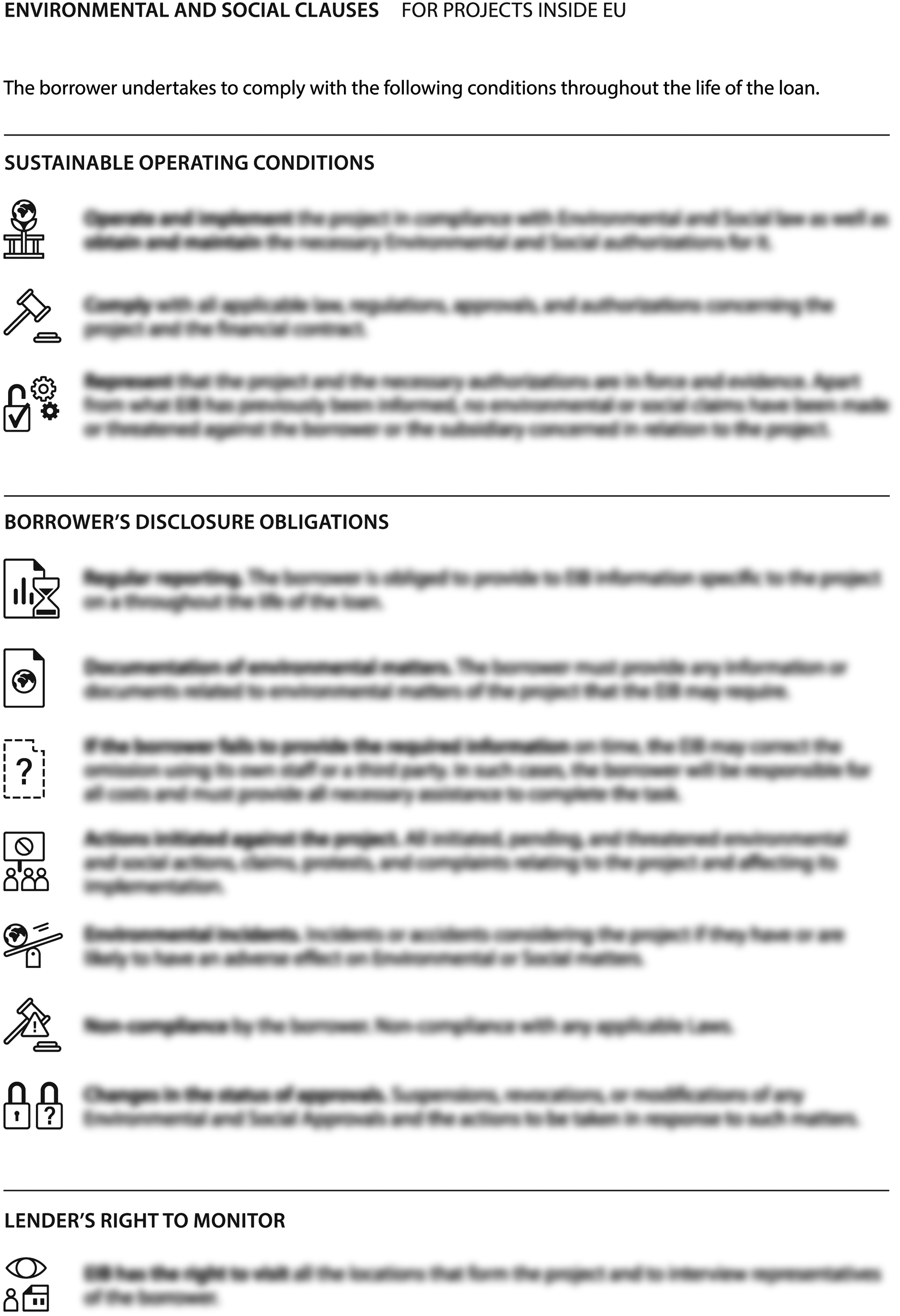

In the first redesigned version (Figure 4) the content of the document was restructured. The text was analyzed and organized into major themes. These themes were given clear headings and the text was made simpler and easier to understand for nonlawyers and nonexperts. 90 Visual elements (icons) were added to effectively convey the meaning of the clauses. The icons were carefully considered to ensure a cohesive and memorable impression. The objective was to create a set of icons that are simple, recognizable, visually appealing, and effectively convey the meaning of the clauses. For example, the use of a judge's gavel icon indicates compliance with laws, approvals, and authorizations; the lock icon represents the status of licenses and approvals; and the globe icon signifies environmental concerns. However, abstract icons, such as the one that symbolizes the pillars of green business and economic growth (the first one), may be open to interpretation and were therefore used sparingly.

The organization and interconnection of clauses significantly impact the user's ability to navigate the document and understand its content. Compact headings play a vital role in directing the reader's attention and providing an overall understanding of the contract. Simplifying complex legal language aligns with the goals of enhancing comprehension and reducing ambiguity. 91 However, it has been noted that “people learn better from words and pictures than from words alone”. 92 This suggests that plain language alone is insufficient to change the way how people perceive and engage with contracts. 93

In summary, the changes allow users to quickly grasp the essential information and gain a general understanding of the content quickly and without much effort. Furthermore, the changes improve understandability and promote common understanding, and foster collaborative relationships among the parties and stakeholders. In addition, the changes minimize the risk of information overload, which often results in misunderstandings and slower information processing. 94

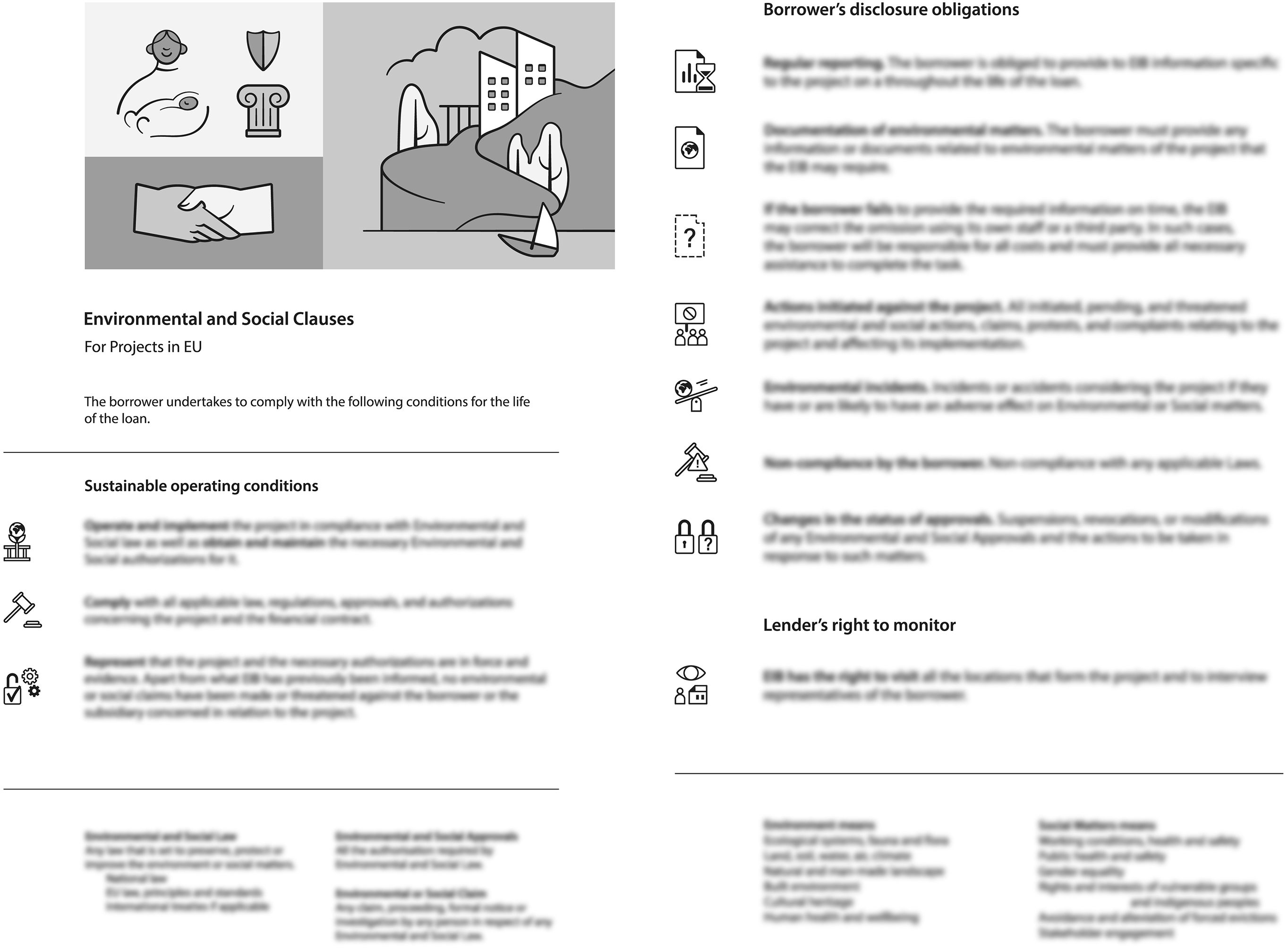

In the second version of the redesign (Figure 5), the text and icons remain unchanged in regard to the first version (Figure 4). The information was divided into two pages. This makes the layout more spacious. In addition, more detailed information on key concepts was added to the footnotes, and a few images were added at the beginning of the document to provide a visual representation of the different environmental and social aspects of sustainability (Figure 3, page 2), such as nature, cultural heritage, safety, health, and human rights. The images of different aspects of sustainability make the different elements of sustainability more tangible to the reader.

This section provided a case study of how contract design offers a number of benefits that improve the effectiveness of contracts. By using information design tools such as plain language and visualization, and considering the needs of users, contracts become more accessible, readable, understandable, and engaging, ultimately improving their effectiveness, supporting the objectives of contracts, and reducing the likelihood of disputes.

Conclusions

According to the European Commission's Sustainable Finance Strategy, the financial system has a key role to play in promoting sustainable development toward a greener and more sustainable economy. Increasing legislation on sustainability alongside banking legislation, and expectations of stakeholders have led to a situation where both banks and companies have a strong interest in promoting sustainable business. SMEs represent more than 99% of all businesses in the EU, and they are responsible for about 60% of all greenhouse gas emissions produced by businesses. SMEs are therefore crucial to the success of EU's sustainability transition.

The purpose of taxonomy regulation is to direct finance toward sustainable investments. To comply with the Sustainable Finance Taxonomy, banks are required to assess the sustainability of their corporate finance clients. Banks also have an interest in identifying sustainable companies within their client base in order to meet their own sustainability targets and to consider the impact of their client's ESG risks on the bank's capital requirements. The new reporting requirements under the CSRD and the proposal on CSDDD will also to some extent affect SMEs both directly and indirectly through the value chains. Considering these factors, as well as the expectations of SME stakeholders and customers, it is necessary for SMEs to integrate sustainability into their business development and risk management. This in turn will contribute to increasing the share of sustainable finance for SMEs.

However, SMEs may face challenges in effectively integrating sustainability into their business operations and in transitioning to sustainable practices, which differentiate them from larger companies. One of the key factors contributing to these challenges is the limited resources available to SMEs. Compared to their larger counterparts, SMEs often lack specialized skills and limited access to legal and sustainability experts. As a result, SMEs may not have a comprehensive knowledge of relevant legislation, have challenges implementing sustainability practices in their day-to-day operations, and may struggle to monitor, measure, and report on their sustainability targets and indicators. 95

Legislation is a tool to influence the transition to sustainability. It provides a framework to guide businesses and ensure compliance with sustainable practices. Contracts complement this framework. They serve as tools to guide and help businesses implement sustainability principles in their operations and ensure that sustainability is promoted in their day-to-day practices. However, the value of a contract is highly dependent on its content. It is therefore crucial to draw attention to the contract processes and to ensure that contract documents are understandable, unambiguous, transparent, and implementable in day-to-day business. Contract documents should avoid complex clauses and jargon, and sustainability factors should be expressed understandably and unambiguously.

This article discussed proactive contracting and legal design approaches as a means to enhance sustainability in financing. By adopting proactive contracting and legal design policies contracts can move beyond their traditional role as mere legal tools to become management and communication tools, as well as to promote good and sustainable business. Furthermore, this article stated that making sustainability visible and monitorable in loan agreements requires a shift from contract drafting to contract design. This requires multiprofessional collaboration and user-centered perspective. Design provides tools and methods for the development of contract processes and contract documents. This article presented information design as an example of the application of design principles in contract documents. Clear and understandable contracts make sustainability more visible, and measurable. This in turn facilitates the implementation, reporting, and monitoring of sustainability targets, contributing to a financial system that directs sustainability development toward a greener and more sustainable economy as outlined in the EU's Sustainable Finance Strategy.

Limitations and future research

Proactive contracting and design research are practice-oriented research streams, that involve a multidisciplinary and multi-methodological approach. When studying contracts and contracting in different business models, it is useful to complement the study of general contract law doctrines with empirical research. This article pointed out the role of SMEs in sustainable business, and more specifically in sustainable finance. To move forward, future research on this topic should take an empirical approach focusing on loan agreements and contract processes with the aim of improving sustainable finance through proactive contracting and legal design. This could be done both by examining the current state of loan agreements, and then using design thinking and action research to design, and evaluate changes in contract processes and contract documents. This approach provides a practical perspective that goes beyond theoretical principles and allows for a deeper analysis of the structures, characteristics and dynamics of contracting in different business models.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.