Abstract

This study contributes to sustainable entrepreneurship by examining the influence of entrepreneur personality on sustainability orientation in a digital finance market context. Extraverted entrepreneurs exhibit strong social connectivity. Consistent with the upper echelons theory, we show that extraversion has significant explanatory power for commitment to a sustainability agenda in initial coin offerings (ICOs). Drawing on institutional difference theory, we find that regulatory change and social pressure moderate the relationship between the extraversion of ICO entrepreneurs and sustainability orientation. Importantly, extraversion plays a significant role in an ICO’s success. Our study highlights the impact of entrepreneur personality traits on driving sustainability efforts and fundraising success.

Keywords

Introduction

With the growing worldwide awareness of sustainability issues, entrepreneurs are making more effort to consider socio-environmental factors in their core business activities and minimize potentially negative influences on society so as to enhance the success of their financing campaigns (Gast et al., 2017; Mansouri & Momtaz, 2022; Muñoz et al., 2018). This progressive transition toward sustainable entrepreneurship (SE hereafter) calls for a better understanding of precisely what drives ventures in this direction.

Startup entrepreneurs vary in talent and skill and have specific personality traits that are expected to significantly impact their ability to recognize and exploit sustainable entrepreneurial opportunities. Shane (2003) highlights the role of the “individual-opportunity nexus” in entrepreneurial finance, emphasizing the importance of individual differences in seizing entrepreneurial opportunities. 1 If there were no differences between individuals, everyone would recognize and pursue the same opportunities, eliminating the prospect of competitive advantage for profit through resource recombination. As well as the potential to generate positive financial returns, SE initiatives involve identifying, developing, and exploiting opportunities within the spheres of environmental, social, and governance (ESG) concerns (Mansouri & Momtaz, 2022). 2 However, there is substantial heterogeneity in entrepreneurs’ SE uptake, prompting the question of why some individuals excel in discovering and exploiting sustainable opportunities, and providing a primary focus for SE research (Anand et al., 2021).

Previous studies have highlighted a variety of core themes associated with individuals engaged in SE, including prior knowledge (Mupfasoni et al., 2018), intent (Castellano et al., 2017), and moral cognition (Kuckertz & Wagner, 2010). However, there is relatively little in the existing literature about how entrepreneurs’ personality traits affect their sustainability strategies. Such traits can be defined as the intrinsic characteristics that influence individuals’ decision-making and reflect the enduring patterns of thoughts, emotions, and behaviors that differentiate individuals (Brandstätter, 2011). We focus specifically on extraversion, recognized as the most influential personality trait (Cain, 2013; Green et al., 2019). Extraversion has been associated with an individual’s motivation and inclination to engage in social activities (Wilt & Revelle, 2019), as well as their governance effectiveness (Judge et al., 2002), and their potential pro-environmental behaviors (Markowitz et al., 2012), all of which align with the principles of SE. Because extraversion is thus reflective of a person’s embrace of a variety of ESG-related abilities, we leverage this personality trait to explore whether entrepreneurs’ extraversion levels are reflected in the ESG orientations of their ventures. Given that extraverted individuals are more sensitive to social concerns and responsive to changes in information and social issues (Morrone-Strupinsky & Depue, 2004; Swickert et al., 2002), we argue that entrepreneurs with similar levels of extraversion may make different strategic choices regarding their ventures’ ESG orientations, influenced by sustainability-related institutional differences.

In this article, we seek to fill some of the research gaps highlighted above by exploring the impact of entrepreneurs’ personalities on their sustainability orientations in a unique financing context, that of initial coin offerings (ICOs). The ICO market represents an emerging form of entrepreneurial financing in which technology startups sell digital assets to public investors. In contrast to traditional financial markets, the ICO market attracts entrepreneurs and investors with diverse objectives, not least in relation to considerations of sustainability (Fisch et al., 2021; Schückes & Gutmann, 2021). Moreover, the ICO market is characterized by its global participation (Bellavitis et al., 2022; Huang et al., 2020; Huang et al., 2024), which also allows us to explore the impact of institutional differences on the relationship between entrepreneur personality and SE adoption. Such distinctive characteristics make the ICO market an ideal context for examining the association between extraversion and SE, while taking into account the potential moderating effects of institutional differences.

To assess extraversion levels, we use information from the LinkedIn profiles of ICO founder CEOs. According to the psychological literature, the extraversion of LinkedIn users can be derived from the information on their profile (Fernandez et al., 2021; Roulin & Levashina, 2019; Van de Ven et al., 2017). Following Fernandez et al. (2021), we ask human raters to score 10 extraversion indicators of ICO founder CEOs on the basis of their LinkedIn profile information, such as their number of connections and whether they have taken a leadership position in previous jobs. Because LinkedIn is used by most ICO teams to convey human resource information to potential investors, this approach overcomes the common data-deficiency problem in personality evaluation. 3 To measure the ESG orientation of an ICO venture, we follow Mansouri and Momtaz (2022) in applying a text-based machine-learning method to calculate the extent to which ESG-related content is addressed by an ICO project in its white papers. 4

Our sample covers 1,011 ICOs issued between 2015 and 2021. After controlling for sample selectivity, a series of ICO-specific characteristics, country dummies, and time fixed effects, we find that the extraversion levels of ICO founder CEOs are significantly and positively associated with the ESG orientations of their ventures. We further leverage the EU’s Commission Action Plan for Financing Sustainable Growth and nation-level social pressures regarding sustainable behavior and practices to examine whether extraverted founder CEOs are more sensitive to sustainability-related social concerns than non-extraverted ones.

Finally, we explore the potential economic advantages to ESG-oriented startups when led by extraverted founder CEOs. Mansouri and Momtaz (2022) report that ESG orientation is effective in attracting funding in the ICO market, and we explore whether the greater sociability of extraverted founder CEOs enhances the external visibility of an ICO’s ESG orientation, which could magnify the influence of ESG on financial performance (Bissoondoyal-Bheenick et al., 2023): we find that the positive relationship between ESG orientation and ICO fundraising is amplified for extraverted entrepreneurs.

Our article makes several contributions. First, we contribute to the understanding of the factors that drive SE uptake (e.g., Castellano et al., 2017; Kuckertz & Wagner, 2010; Muñoz et al., 2018; Mupfasoni et al., 2018; Spence et al., 2011). In contrast to demographic factors or specific values, personality traits are intrinsic, fundamental, and stable aspects of an individual’s nature (Digman, 1990; John et al., 2008; Jung, 1921). Prior research has focused primarily on entrepreneurs’ acquired attributes; we shed light on the influence of their individual psychological differences on sustainable opportunity recognition and exploitation. Second, we add to the literature at the intersection of SE and institutional theory (e.g., Boettke & Coyne, 2009; Bradley et al., 2021; Chowdhury et al., 2019). Prior research on entrepreneur personality traits has tended to ignore the context in which the entrepreneur has evolved and is often conducted in a single country, which further exacerbates the disregard for potential variations in institutional contexts (e.g., Antoncic et al., 2015; Karimi et al., 2017; Zhao et al., 2010). By exploiting the international and decentralized context of ICOs, we show how institutional differences associated with increased awareness of sustainability issues, such as policy changes and social pressures, influence extraverted entrepreneurs’ propensities for stronger ESG commitments. Third, we contribute to the field of ICO research by offering additional insights into the emergence of innovative sources of entrepreneurial finance. We expand the understanding of the relationship between entrepreneur characteristics, SE, and funding outcomes. In recognizing the multifaceted nature of ICO ventures, our study emphasizes the importance of aligning entrepreneur personality traits with sustainability objectives to achieve favorable funding outcomes.

The article is organized as follows: in section “Theory and Hypothesis Development,” we summarize the theoretical background to our work and develop our hypotheses; in section “Data and Variables,” we describe our data and variable construction, before providing empirical results in section “Results.” Section “Discussion and Conclusion” presents our discussion of our study’s main results, its academic contributions and its implications for practice, together with its limitations and the avenues opened for future research.

Theory and Hypothesis Development

SE and Factors Affecting SE Uptake

SE is a burgeoning area of research within the entrepreneurship literature, focusing on the integration of broader sustainable objectives with traditional business activities (Anand et al., 2021). The concept of sustainability and entrepreneurship is introduced by Hart and Milstein (1999), building upon Schumpeter’s (1942) notion of “creative destruction.” Subsequently, the seminal work of Shane and Venkataraman (2000) plays a pivotal role in establishing the legitimacy of the entrepreneurship field, emphasizing the centrality of opportunity in entrepreneurial endeavors and providing a foundation for the identification and leverage of such opportunity within the broader sustainability context. Based upon this and in line with the wider ESG literature, Mansouri and Momtaz (2022) define SE as “entrepreneurial activity aimed at achieving positive nonfinancial outcomes concerning environmental, social, and governance aspects,” recognizing, developing, and exploiting opportunities therein.

SE-related literature can be categorized according to its focus: either on the factors influencing SE uptake, the SE process itself, or the specific outcomes of SE, with particular attention currently being given to the first of these (Anand et al., 2021). Understanding the factors that affect SE uptake is crucial to the development of effective strategies and policies to promote and support SE initiatives. It provides valuable insights into encouraging the diffusion of sustainable technologies and assisting entrepreneurs in formulating innovative strategies that balance profitability with environmental and social impacts. In addition, it helps to identify policies that facilitate the integration of sustainability into entrepreneurship and to address the challenges faced by entrepreneurs when embracing sustainable practices (Ghisetti et al., 2015; Hockerts & Wüstenhagen, 2010).

Shane (2003) emphasizes the pivotal role of the individual-opportunity nexus in entrepreneurial activity, highlighting the significance of individuals’ differences when it comes to exploiting entrepreneurial opportunities. If everyone exhibited the same perceptions and behaviors, competitive advantage would be greatly diminished. Similarly, the individual entrepreneur is a central component in understanding factors affecting SE uptake, where the focus is on encouraging individuals to engage in sustainability-oriented activities (Vuorio et al., 2018). In addition, the research in this area examines the interactions between individual entrepreneurs and their external environment, recognizing that individual decision-making is influenced by a variety of contextual factors (Anand et al., 2021; Shane, 2003).

In terms of differences between individuals, studies have highlighted various key themes in relation to SE engagement, including motivation(s), intent, moral cognition, self-efficacy, and sustainability orientation (Castellano et al., 2017; Kuckertz & Wagner, 2010; Muñoz et al., 2018; Mupfasoni et al., 2018; Spence et al., 2011). Vuorio et al. (2018) find entrepreneurs’ attitudes toward sustainability and perceived entrepreneurial desirability to be positively associated with their sustainability orientation. Mupfasoni et al. (2018) document the contribution of prior knowledge to the sustainability aspect of business plans, while Ploum et al. (2018) focus on the moral antecedents of sustainable entrepreneurs and how these influenced the recognition of sustainable development opportunities.

With regard to contextual factors, the institutional environment, including the economic, political, and cultural context, significantly influences opportunity exploitation in entrepreneurship (Shane, 2003). Ceptureanu et al. (2017) investigate the relationship between local embeddedness and sustainable opportunity recognition. Moreover, studies focusing on sustainable development and sustainability transformation have emphasized the role of stakeholder management, strategic partnerships, alliances, and collaborations with local communities (Bischoff & Volkmann, 2018; Juma et al., 2017; Muhammad Auwal et al., 2020; Schaltegger et al., 2018). These research efforts underscore the significance of the institutional and local context in the exploration of opportunities and implementation of SE initiatives, but personality traits are an underexplored aspect of individual differences among sustainability-oriented entrepreneurs.

Entrepreneur Personality and Entrepreneurship

The management literature argues that organizational outcomes offer a reflection of the senior management teams involved (a.k.a. the upper echelons theory) (Cannella, 2001; Carpenter et al., 2004; Hambrick, 2007; Hambrick & Mason, 1984). Personality traits are intrinsic characteristics that significantly impact individuals’ actions, representing enduring patterns of thoughts, emotions, and behaviors that distinguish individuals from one another (Brandstätter, 2011). Unlike prior knowledge or specific values, personality traits are inherent, underlying aspects of an individual’s makeup (Digman, 1990; John et al., 2008; Jung, 1921), and they exert a critical influence on individuals’ decisions and behaviors when exploiting entrepreneurial opportunities, regardless of whether those individuals otherwise possess the same information and skills (Brandstätter, 2011; Shane, 2003). Moreover, personality traits tend to be stable and enduring throughout an individual’s life, exhibiting consistency and continuity across different stages and experiences (Roberts et al., 2006). While certain life events and experiences may affect personality, its core aspects remain relatively stable over time. Importantly, personality traits manifest differently in different situations according to the surrounding context, and their impact on entrepreneurial outcomes can vary depending on factors such as industry, culture, and specific business contexts (Rauch & Frese, 2007).

Prior studies have investigated the effect of entrepreneurial hubris or confidence on a firm’s corporate ESG practice (e.g., Cronqvist & Yu, 2017; Davidson et al., 2019; Hegde & Mishra, 2019; McCarthy et al., 2017). For startups, some studies find that entrepreneurs with extraversion tend to show higher levels of opportunity recognition and are more likely to engage in opportunity exploitation (Brandstätter, 2011; Zhao et al., 2010). Furthermore, the proactive personality, personified by individuals who are proactive, persistent, and take the initiative, has been found to positively influence the recognition and exploitation of opportunities (Crant, 1996; Parker et al., 2010). Two other important personality traits that affect how entrepreneurs perceive and evaluate opportunities are risk propensity and tolerance of ambiguity (Liñán & Chen, 2009). While certain personality traits have consistently shown associations with higher levels of entrepreneurial activity, contextual factors can influence their expression and effectiveness in this regard. For instance, the significance of traits such as networking and assertiveness, often linked to extraversion, may vary across different industries and cultural contexts (Zhao et al., 2010).

While conventional entrepreneurship focuses primarily on economic utility, SE extends its objectives to encompass broader ESG concerns (Mansouri & Momtaz, 2022). Thus, it is important to explore how specific personality traits may influence opportunity recognition and exploitation in the SE context. In addition, the role of contextual factors in this relationship is especially worthy of exploration, given the more unique prospectus of noneconomic utility also involved.

The ICO Market

The ICO market (i.e., the token offering market) is an emerging entrepreneurial financing market that enables technology startups to sell blockchain-based digital assets to public investors (Momtaz, 2020). It provides an ideal research setting in which to investigate the role of entrepreneurial personality in SE for several reasons.

First, in ICO ventures, the CEO typically emerges as one of the founders (Colombo et al., 2022), which reduces agency concerns and magnifies the influence of the founder-CEO’s personality in shaping a venture’s culture and values (Mousa & Wales, 2012; Nelson, 2003). Moreover, the entrepreneurial context provides valuable insights into how entrepreneurs navigate resource constraints, uncertainty, and intense competition while integrating sustainability practices (Cohen & Winn, 2007; Eisenhardt & Schoonhoven, 1990). Furthermore, studying SE at this early stage enables researchers to understand how entrepreneur personality traits drive the incorporation of such considerations into decision-making and strategic planning, highlighting, for example, the role of innovation and risk-taking in the fostering of SE (Hockerts & Moir, 2004; Zahra, 1993).

Second, the institutional features unique to token offerings provide opportunities for quantitative analysis of SE and financial performance, differentiating them from other forms of entrepreneurial finance. Token offerings require extensive disclosure of critical information, including how sustainability challenges will be addressed, typically presented in publicly available white papers (Mansouri & Momtaz, 2022; Momtaz, 2021a). In addition, the transparency of the ICO mechanism allows for the public observation of the funding amounts raised by ICOs.

Third, the ICO market attracts entrepreneurs and investors with both financial and nonfinancial objectives, highlighting the multifaceted nature of participants in this space (Fisch et al., 2021; Schückes & Gutmann, 2021). Much like crowdfunding, token offerings emerged as a result of concerns about the fairness of traditional financial markets (Fisch et al., 2021; Howell et al., 2020). As a consequence, the entrepreneurs and investors involved in ICOs may exhibit a heightened awareness of and appetite for sustainability-oriented business opportunities (Mansouri & Momtaz, 2022).

Last, the ICO market stands out as a result of its global nature, enabling entrepreneurial entry without significant barriers (Bellavitis et al., 2022). This global aspect offers a unique opportunity to examine the impact of extraversion on a consistent basis across different institutional contexts, as well as facilitate the exploration of potential moderating effects from institutional and cultural factors on the relationship between extraversion and SE.

Existing studies of ICOs have focused mainly on their financial performance. For example, Thewissen et al. (2022) apply a topic-modeling approach and find that, in white papers, it is technological rather than management or governance-related topics that significantly and positively affect ICO success and post-ICO performance. Further, Colombo et al. (2022) find that attractive ICO founder CEOs are preferred by potential investors and are hence associated with higher valuations and more sustained post-ICO performance than non-attractive CEOs. Huang et al. (2022) have shown that team confidence levels, as perceived by investors, are positively related to ICO funding amounts. Research on sustainability orientation and entrepreneurial characteristics in such digital financing markets has been limited, with more exploration required. One recent exception is that of Mansouri and Momtaz (2022), who identify the degree of ESG orientation within ICO white papers and holistically examine the economic attractiveness of SE in the ICO context; their focus, however, is not on the factors driving such ESG orientation.

Founder-CEO Extraversion and Venture’s Sustainability Orientation (Hypothesis 1)

Extensive research supports extraversion as the “single most important” aspect of an individual’s personality (Cain, 2013), showcasing its association with the seizing of entrepreneurial opportunities (Wooten et al., 1999), influencing career outcomes (Green et al., 2019), and driving corporate financial outcomes (Adebambo et al., 2019). Extraverts are considered to be warm, sociable, assertive, talkative (John & Srivastava, 1999), and desirous of social interaction (Wilt & Revelle, 2019). Extraversion is the personality trait that exhibits the closest association with social connection and leadership (Malhotra et al., 2018), highlighting its potential to strongly influence the recognition and exploitation of SE opportunities. In the following paragraphs, we explore the potential connections between extraversion and the separate aspects of ESG in the context of SE.

Because of their innate sociability and preference for social interactions, extraverts tend to exhibit a heightened interest in social issues. Eaton and Funder (2003) report that extraverts possess exceptional social skills and are adept at creating friendly environments, which fosters their proclivity for the promotion of positive social interactions. Block et al. (2019) find that extraverted business angels are more likely to engage in syndication, an investment strategy that necessitates effective coordination and collaboration among investors, while Ormiston and Wong (2012) demonstrate that extraverted CEOs are less likely to engage in socially irresponsible behaviors. Collectively, these findings suggest that extraverted individuals, driven by their sociability and preference for social interactions, tend to prioritize social issues and contribute actively to fostering a socially responsible environment. This inclination positions them to better recognize SE opportunities with a social aspect and motivates their effective exploitation of such opportunities.

Extraversion has been consistently associated with leadership and management effectiveness (Bentz, 1985; Grant et al., 2011; Judge et al., 2002). Extraverted individuals tend to be more assertive and decisive (Wilt & Revelle, 2019), which has been linked to their ability to excel in governance roles. Specifically, research has shown that extraverted CEOs enhance corporate efficiency and achieve higher returns on acquisitions (Green et al., 2019; Malhotra et al., 2018), while Gupta et al. (2019) show that extraversion strengthens the impact of CEO ideology on corporate strategies. Accordingly, we expect extraverted founder CEOs to actively promote strong governance within their ventures by implementing efficient management structures and formulating clear and feasible business roadmaps.

The relationship between extraversion and the environmental aspect of ESG is more complex and inconclusive. A number of studies have failed to find a significant connection between extraversion and environmental concerns, suggesting that such issues may not be a primary focus for extraverted individuals (Hirsh, 2010; Hirsh & Dolderman, 2007; Milfont & Sibley, 2012). However, other research shows a positive correlation between extraversion and pro-environmental behaviors (Brick & Lewis, 2016; Markowitz et al., 2012), with entrepreneurs who exhibit extraverted traits showing more inclination toward sustainable outcomes. For example, Chapman and Hottenrott (2022) find that, owing to their active and sociable nature, extraverted founders are more effective in promoting environmentally friendly products, helping them identify and leverage diverse knowledge related to green products. Similarly, Hrazdil et al. (2021) discovered a positive relationship between extraversion in US CEOs and their firms’ environmental engagement, suggesting that extraverted CEOs are more responsive to stakeholders’ environmental concerns. However, whether extraversion contributes to the recognition and exploitation of environmental opportunities in the context of SE remains an empirical question.

Overall, extraverts tend to seek social stimulation and opportunities to engage with others, thereby creating more incentives to promote social benefits within their surrounding environment. Moreover, because extraverted founder CEOs are expected to have better governance-related abilities, they can formulate better internal governance mechanisms for their ventures. If we assume that extraverted founder CEOs may also pursue environmental goals more strongly, we formulate our first hypothesis:

Hypothesis 1: The extraversion level of ICO founder CEOs is positively related to the ESG orientation of the ICO ventures they manage.

Institutional Difference, Extraversion, and Sustainability Orientation (Hypothesis 2)

Previous research has established a consensus that personality traits are generally shared and consistent across countries (Katigbak et al., 2002). However, entrepreneurs do not operate in a vacuum when pursuing opportunities (Shane, 2003), and institutional context is pivotal in shaping their decision-making processes, most particularly in relation to sustainable practices. On the basis of the institutional difference hypothesis of Julian and Ofori-dankwa (2013) and the context-bound nature of ESG (Amaeshi et al., 2006; Matten & Moon, 2008; Robertson, 2009), we contend that entrepreneurs with similar levels of extraversion may exhibit variation in their decisions regarding SE owing to the specific contextual factors of the countries in which they operate.

Institutional differences encompass the rules of the game that economists believe generate incentives for certain types of action (e.g., changes in regulation) as well as the country-specific settings that determine entrepreneurs’ legitimate and acceptable behavior in relation to sustainability (Halme et al., 2009; Matten & Moon, 2008; Robertson & Crittenden, 2003). Thus, the country-specific context is likely to moderate the relationship between SE and extraversion. Drawing on the global engagement of ICOs (Huang et al., 2020; Shrestha et al., 2021), our second hypothesis investigates how broader country-specific factors moderate the impact of extraversion on an ICO’s SE stance.

Regulatory Environment

We first examine the impact of a change in regulation that alters stakeholders’ awareness of sustainability, testing whether extraverted founder CEOs show more response to the indirect regulation change than introverted ones. The psychological literature suggests that extraverts, with their greater sociability, exhibit a heightened sensitivity to social concerns and are more responsive to changes in information and social issues (Morrone-Strupinsky & Depue, 2004; Swickert et al., 2002). Bellavitis et al. (2022) document a phenomenon of “regulation spillover,” in which a regulatory change in one set of countries could influence entrepreneurial markets in other countries owing to anticipation of similar change. Because of extraverts’ heightened sensitivity to information and executive force, when an external event increases the social concerns of ESG, we hypothesize that extraverted CEOs are more likely to act and thus display such spillover behaviors. By contrast, their introverted counterparts may pay less attention to any such change.

To this end, we exploit the European Commission (EC) Action Plan on Financing Sustainable Growth, adopted on March 8, 2018, as a policy shock that increased social concerns in relation to sustainability. The plan aims to reorient capital flows toward investments in more sustainable and inclusive growth. It requires both public and nonpublic firms to “disclose how they consider sustainability factors in their strategy and investment decision-making process.” Because of this disclosure requirement, institutional investors who make sustainable investments benefit from reduced exposure to future regulatory risks. Because EU institutional investors play a significant role in the global ICO market (Capolaghi & Swertvaeger, 2022), ICO ventures with a stronger ESG focus are likely to attract those EU institutional investors who prioritize sustainability. In addition, ICO entrepreneurs may anticipate spillover of sustainability-focused regulations into other countries with a substantial ICO investor base, thereby promoting the adoption of ESG-oriented business goals in ICO projects. If extraverted founder CEOs are aware of growing social concerns about sustainability in their extensive social networks, they may strategically enhance the sustainability content in their white papers to attract institutional investors accordingly.

Hypothesis 2a (regulatory environment): Following the 2018 EC Action Plan on Financing Sustainable Growth, extraverted entrepreneurs are more likely to exhibit elevated ESG orientation in the ICO ventures they manage.

Social Pressure

Social pressure can drive sustainability, creating a ripple effect that motivates individuals and communities to take sustainable actions and bridge the gap between attitudes and behaviors (Kollmuss & Agyeman, 2002; Schultz et al., 2007). Sustainable practices become widespread when sustainable lifestyles become the dominant norm (Kollmuss & Agyeman, 2002).

Social pressure promotes sustainability through social norms, public opinion, consumer demand, and public debate (Schultz et al., 2007; Thøgersen & Crompton, 2009). Social norms influence behavior by making specific actions socially desirable (Cialdini & Trost, 1998). Prior studies have documented that public opinion shapes attitudes and behaviors toward pro-environmental activities (Cialdini, 2003; Steg & Vlek, 2009), while consumer demand influences companies to adopt sustainable practices (Delmas & Burbano, 2011). By establishing sustainable practices as desirable and necessary, social pressure can effectively promote sustainability within a country.

Given extraverts’ tendency to conform to social norms (Ashton & Lee, 2009), value social feedback (Srivastava et al., 2003), and be more attuned to social cues (Baumeister & Leary, 1995), it is reasonable to assume that social pressure can impact the sustainable orientation of extraverted entrepreneurs, who are more sensitive to social context and more likely to conform to societal expectations regarding sustainability. We therefore hypothesize that extraverted entrepreneurs are more likely to demonstrate elevated ESG orientation in countries where sustainable behavior and practices are widely embraced.

Hypothesis 2b (social pressure): Extraverted entrepreneurs are more likely to exhibit elevated ESG orientation in the ICO ventures they manage in countries that mostly embrace sustainable behavior and practices.

Extraversion, Sustainability Orientation, and ICO Success (Hypothesis 3)

In addition to exploring the impact of an entrepreneur’s extraversion on their ICO’s ESG orientation, we are ultimately interested in investigating the potential economic advantages of ESG orientation during the ICO stage. Mansouri and Momtaz (2022) find ESG orientation to be positively associated with increased funding during the ICO stage, indicating that investors place a premium on ventures with strong ESG commitments. However, the entrepreneur’s personality traits, such as extraversion, are likely to influence this relationship because extraverts tend to attract social attention (Ashton, 2022), which may lead to greater external visibility of their ICO’s ESG orientation. In fact, recent evidence suggests that increased visibility through media coverage can amplify the influence of ESG on financial performance (Bissoondoyal-Bheenick et al., 2023). Green et al. (2019) find a positive association between CEO extraversion and investor recognition owing to the visibility generated by the extraverts’ tendency to attract social attention. Given that startups with high ESG visibility are seen as more accountable and trustworthy, and are more likely to attract investors and customers who prioritize sustainability and ethical business practices (Mansouri & Momtaz, 2022), ICOs with more visible ESG-oriented practices can be expected to be more successful. As such, we hypothesize that the positive impact of ESG orientation on corporate performance will be more significant for extraverted entrepreneurs than non-extraverted ones.

Hypothesis 3 (economic impact): The positive relationship between ESG orientation and venture funding is amplified when the ICO venture is managed by extraverted entrepreneurs.

Data and Variables

Data Source

Our final sample consists of 1,011 ICOs between 2015 and 2021. We collect ICO-specific variables from the Token Offering Research Database (TORD) 5 and obtain founder-CEO characteristics from their LinkedIn profiles. 6 Further, we supplement missing variables by manually searching via ICO aggregators and search engines. Specifically, we first retrieve ICO white papers from TORD, which collects information from major ICO research data sources (Momtaz, 2021c). 7 We then identify the LinkedIn profiles of ICO founder CEOs from major ICO aggregators, 8 where such profiles are prominently displayed to convey the team background to potential investors (Howell et al., 2020; Momtaz, 2021b). We manually check founder CEOs’ identities via their title and compared their tenure times with the founding times of the ventures, shown on LinkedIn, to ensure that no CEO turnover occurs during our sample period. In total, we identify 1,174 founder CEOs for our 1,011 ICO ventures between 2015 and 2021. Where an ICO has multiple founder CEOs, we take the average extraversion score. Compared to the latest literature on ICO CEOs, our sample size is reasonable; for example, Momtaz (2021b) employs a sample of 232 ICO CEOs, Huang et al. (2022) test 515 ICOs, while Colombo et al. (2022) collect information on 740 ICO founder CEOs. We measure the degree of social pressure on sustainability-related issues at the country-level using the Global Sustainable Competitiveness Index (GSCI) published by SolAbility (Zurich/Seoul). The GSCI evaluates a country’s emphasis on sustainable competitiveness on the basis of various economic, social, and environmental factors in a given year, and has been widely used in prior studies, including those of Herciu and Ogrean (2014), Januškaitė and Užienė (2018), and Salimova et al. (2018).

Extraversion Measurement

Psychologists infer extraversion according to survey questionnaires (Rammstedt & John, 2007). However, with a survey-based experimental method, obtaining a sample sufficient for an empirical study on CEOs’ personality traits is difficult. In recent years, with the development of data mining techniques, researchers have measured personalities, especially extraversion, from speech transcripts of the Q&A portion of conference calls (Adebambo et al., 2019; Green et al., 2019; Lartey et al., 2020). Extraversion is reflected in speech patterns, such as word variety, tone, and verbal output, and can thus be captured by text-based algorithms (Mairesse et al., 2007).

However, such speech transcripts are not available for nonpublic firms, such as private companies or ICO ventures. In this case, researchers must turn their attention to social media data, which becomes more valuable in entrepreneurial markets because, compared to public firms, entrepreneurial ventures typically have little information to disclose, which limits the data available for the investigation of their management practice. In this study, we use the novel approach of evaluating entrepreneurs’ extraversion via LinkedIn—the world’s largest professional network and career development platform. LinkedIn profiles are structural and straightforward and, hence, serve as a good data source when it comes to revealing individuals’ differences. As a social network for professionals to connect, share, and learn, LinkedIn profiles generally display users’ detailed work experience, educational background, social network connections, and self-reported working skills and associated endorsements, all of which have been shown in psychological studies to be important predictors of an individual’s extraversion level (Roulin & Levashina, 2019; Van de Ven et al., 2017).

Psychological experiments have shown that the information disclosure in LinkedIn profiles can provide an accurate assessment of true personality, especially in relation to extraversion (Fernandez et al., 2021; Roulin & Levashina, 2019; Van de Ven et al., 2017). For example, the number of connections and followers is a strong evidence of social activity, and thus of extraversion. Figure A1, Appendix A of the Online Appendix shows examples of a LinkedIn user profile.

LinkedIn users generally have little incentive to provide inaccurate information because of the high costs of false information in relation to LinkedIn’s purposes of recruitment and self-promotion (Fernandez et al., 2021). Indeed, Guillory and Hancock (2012) find that LinkedIn profiles are more honest than paper résumés. LinkedIn profiles may not be updated frequently, but it is worth recalling that extraversion is a highly stable personality trait (Cain, 2013). Roulin and Levashina (2019) find that human raters can predict the extraversion, skills, and cognitive ability of individuals from their LinkedIn profiles. In a similar vein, Van de Ven et al. (2017) find that information from LinkedIn allows for better inferences of extraversion. Thus, using the LinkedIn profile information of founder CEOs should generate a reasonable and accurate extraversion measure. Fernandez et al. (2021) conducted regression analyses and classification statistics to compare the personality assessments from LinkedIn indicators with psychological questionnaires for a group of participants who varied in gender, age, and nationality. Their results show that LinkedIn can provide accurate signals of extraversion.

Operationalization

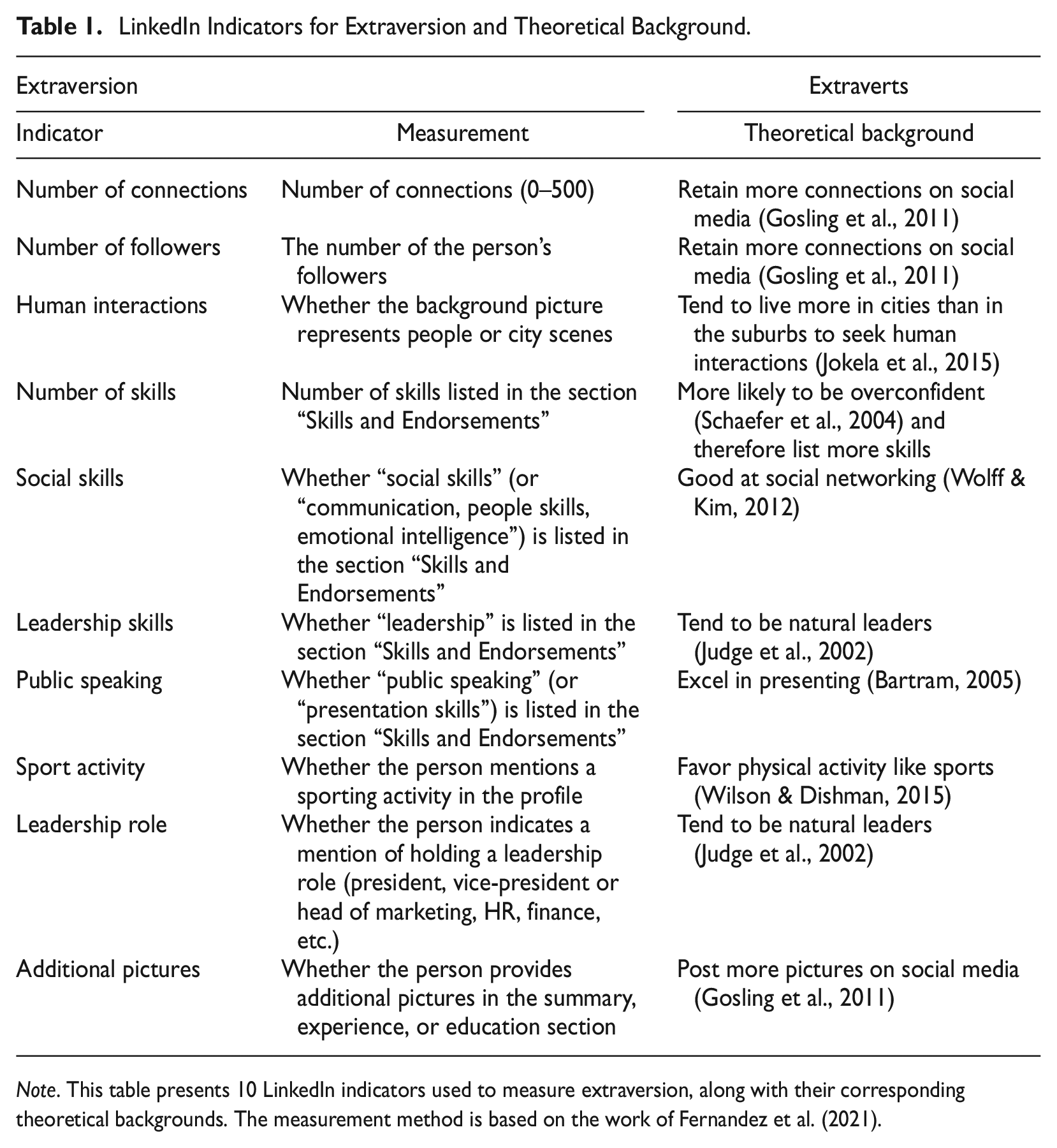

We follow Fernandez et al. (2021) in using signals available in LinkedIn profiles to infer founder CEOs’ extraversion. 9 Specifically, we propose 10 LinkedIn indicators, summarized in Table 1. Extraverts are more likely to engage in networking and exhibit more extensive social networks, more frequent interactions, and greater picture-sharing on social media than introverts (Gosling et al., 2011; Wolff & Kim, 2012). We thus assume that founder CEOs exhibiting extraverted personality traits will be associated with more LinkedIn connections and followers. For extraverted founder CEOs, the quantity of LinkedIn followers reflects their popularity and the level of interest they generate, while the number of connections signifies their number of acquaintances on the platform. Given that extraverts are drawn to bustling urban environments and are more likely to reside in city centers (Jokela et al., 2015), we also expect that extraverted founder CEOs will opt for background pictures that depict cities or people, rather than, for example, serene landscapes.

LinkedIn Indicators for Extraversion and Theoretical Background.

Note. This table presents 10 LinkedIn indicators used to measure extraversion, along with their corresponding theoretical backgrounds. The measurement method is based on the work of Fernandez et al. (2021).

Furthermore, we anticipate that extraverted founder CEOs will list proportionately more skills because research suggests that extraverts tend to display overconfidence (Schaefer et al., 2004). Extraverts are known to excel in social interactions, possess natural leadership qualities (Judge et al., 2002), exude charm (Bono & Judge, 2004), and excel at presenting information to audiences (Bartram, 2005). Therefore, extraverted founder CEOs are more likely to list leadership, social skills, and public speaking abilities on their LinkedIn profiles. We also anticipate that extraverted founder CEOs will have prior experience in leadership roles. It is essential to distinguish between “leadership skills” (which pertain to self-recognition) and “leadership roles” (which are practical outcomes). Research suggests that extraverts are more likely than introverts to engage in physical activities (Wilson & Dishman, 2015) and to report such experiences (Cole, 2009). While sports-related information may seem irrelevant on a LinkedIn profile, extraverted individuals would probably include this information to differentiate themselves from other candidates (Roulin & Levashina, 2019). Lastly, we anticipate that extraverts would be more inclined to include pictures to illustrate their past experiences. This may serve as another way for them to demonstrate their level of engagement on the platform (Gosling et al., 2011).

Thus, we first rate 10 extraversion-related indicators according to users’ LinkedIn profiles based on the criteria presented in Table 1. 10 Each indicator is then winsorized at the 99th percentile to eliminate outliers and rescaled to an indicator value of between 0 and 1. We then prepare an overall score of the extraversion by summing all 10 indicators before standardizing this composite index. Summary statistics of the 10 LinkedIn indicators are reported in Table A1 of the Online Appendix.

Measurement Validation

To establish the external validity of our measurement of extraversion, we center our attention on a primary outcome of extraversion: sociability. Given that extraverted individuals are inclined to seek out social engagements, we propose three sociability variables in the context of ICO to gage the social outcomes of founder CEOs, namely, the number of ICO advisors in the team (Number of advisors), the number of endorsements the ICO received (Number of endorsements), and the number of social media followings the founder CEO has (Number of followings). Variable definitions are provided in Table A2 of the Online Appendix.

ICO advisors are external consultants who provide technical, marketing, and economic expertise (Phua et al., 2022). Because advisors often serve multiple ICO teams, they have access to extensive networks of information and can act as central nodes in the ICO network (Giudici et al., 2020). The decision to hire advisors is at the discretion of the CEO, and the number of advisors hired varies according to their preferences. Our sample shows that about 50% of ICOs engage at least one advisor, consistent with Phua et al. (2022), and the number of advisors hired ranges from 1 to 32. We contend that hiring more advisors may indicate that the CEO places a high value on social connections and networking, which is an important outcome of extraversion. Endorsements play a crucial role in helping investors to evaluate project quality. The primary endorsement on which ICOs rely is expert ratings, which are published by ICO aggregator websites (Florysiak & Schandlbauer, 2022). ICOs led by sociable CEOs are more likely to receive more endorsements, because this involves increased visibility of the project to experts through measures such as publishing in multiple ICO aggregators and inviting experts to rate it. In terms of social media use, extraverted individuals are more likely to be active (Bowden-Green et al., 2020) and thus we can expect them to follow more users on platforms such as Twitter: a higher number of Twitter followings could indicate a more substantial interest in content shared by others and more frequent use of the platform, reflecting their social inclination.

In Table A3 of the Online Appendix, we present the pairwise Pearson correlations in Panel A and the results in Panel B. All three sociability variables exhibit the expected positive and significant correlations with the variable Extraversion. We implement univariate linear regression models in which we regress Extraversion on each sociability variable in turn. We then introduce founder-CEO demographic variables, market conditions, country, and quarter-year fixed effects as controls. Our findings suggest that our extraversion measurement captures the sociability of the founder CEOs, establishing the external validity of our measurement approach.

ESG Orientation Measurement

Previous studies have evaluated the ESG data of public firms by using the ESG rating information provided by rating agencies. For nonpublic firms, for which these agencies do not provide rating information, prior studies have instead applied text-based methods to capture ESG orientation from the firms’ major public disclosure documents. For example, Hörisch (2015) uses the self-reported classification of “environmentally oriented” to rate crowdfunding projects. Vismara (2019) defines a crowdfunding project as sustainability-oriented if its description contains at least one term from a specified sustainability-related dictionary. Similarly, Mansouri and Momtaz (2022) propose an integrated text-based machine-learning approach to quantify the ESG properties of ICO startups, and we follow their method to measure each ICO’s ESG orientation from ICO white papers. These are essential documents that contain all the information about an ICO venture, including the product introduction, business vision, technical documentation, team, and roadmap, and are important information channels for potential investors (Florysiak & Schandlbauer, 2022; Howell et al., 2020; Lyandres et al., 2022). Intuitively, the more ESG-related topics that are mentioned in the white paper, the more ESG oriented is the venture. To capture the ESG-related wording in an ICO context, an ESG dictionary is generated from a seed-word list, constructed using the most frequent words in Financial Times articles on the topics of “ESG investing” and “moral money” and a word-embedding model. 11

We quantify the ESG score by counting the occurrences of ESG dictionary words in the white paper and scaling the score according to the size of the corresponding word list and the length of the paper. For ICO white paper

where

We manually check the ESG measurements in terms of word lists and the highest-rated ventures and find the results to be reliable. The calculated ESG orientation score is standardized.

Other Variables

Following previous ICO studies (Fisch & Momtaz, 2020; Florysiak & Schandlbauer, 2022; Lyandres et al., 2022; Mansouri & Momtaz, 2022; Thewissen et al., 2022), we control for ICO, venture, and founder-CEO characteristics and collect the control variables from TORD, LinkedIn, and ICO data aggregators. 12 Variable definitions are provided in Table A2 of the Online Appendix.

We first include a number of ICO-specific variables that are frequently used in previous studies and have potential effects on the ESG orientation of ICO projects. Specifically, we include dummy variables that indicate whether an ICO offers utility tokens (ICO) 13 , whether the ICO has a pre-ICO (PreICO), whether the ICO involves a whitelist or know-your-customer (KYC) process (WhiteKYC) 14 , whether the ICO accepts fiat currency as payment (Fiat), whether the ICO has a minimum investment requirement (Mininvest), and whether the ICO restricts the participation of United States investors (US Restrict). We also control for the number of social media pages that the ICO uses for ICO promotion (Social media). We include (the natural logarithm of) the Bitcoin price (Bitcoin price) to control for the popularity of virtual currencies. We control for ICO types because these can fall under different regulation frameworks, which could affect the content of the white paper (Momtaz, 2020). Variables related to the ICO registration and promotion process take account of potential interaction between ICO teams and investors, which can induce founder CEOs to modify white paper content to meet investor preference in relation to ESG topics.

Further, we control for demographic attributes of the founder CEOs to account for the influence of personal characteristics on ESG orientation. For example, gender and age greatly influence the tendency toward ESG (Cronqvist & Yu, 2017; McGuinness et al., 2017). We use dummy variables that indicate founder-CEO gender (Gender), their experience in the technology industry (Technology experience), and their experience in the finance industry (Finance experience); we also construct categorical variables to account for their educational level (Degree) and age (Age), which may shape entrepreneurs’ attitudes toward sustainability issues (Borghesi et al., 2014; Hegde & Mishra, 2019).

In addition, we include variables of venture characteristics; specifically, the logarithm of the number of team members in the ICO project (Team size), the average rating of the ICO project on ICO aggregators (Rating), the number of industries involved in the ICO (No. of industries), and a dummy variable that indicates whether the ICO project concerns an ESG-related industry (ESG-related industry). In this context, we use team size to control for venture size, while rating reflects the project quality in experts’ eyes (Florysiak & Schandlbauer, 2022; Lee et al., 2022), and ESG-oriented projects may attract a more favorable rating; the number of industries represents the business diversity of a venture (Fisch & Momtaz, 2020), and the more diverse it is, the more likely it is to involve ESG-related business goals, which contributes to ESG orientation. Mansouri and Momtaz (2022) find that ICOs in particular industries tend to involve more ESG-related content in their white papers, and so we also control for five specific industries (health, energy, manufacturing, banking, and legal). Consistent with existing studies (e.g., Fisch & Momtaz, 2020; Huang et al., 2020; Momtaz, 2022), we control for time-related differences, such as ESG trends and white paper writing style. Finally, we include country-fixed effects to control for the potential impact of regional regulation (e.g., Fisch & Momtaz, 2020; Howell et al., 2020; Mansouri & Momtaz, 2022).

To test the moderating effects, we introduce Post-action as a time-based dummy variable to capture whether the ICO was issued after the adoption of the EC Action Plan in Q1 2018. This allows us to examine the moderating effect of changes in the political environment. To clearly delineate the time period, observations for ICOs issued in Q1 2018 are omitted when constructing the time dummy. In addition, we define hiGSCI as a dummy variable that indicates whether the ICO-issuing country exhibits a high sustainability orientation compared to the sample median, as measured by the GSCI. 15 This helps us capture the social pressure surrounding sustainability issues in the ICO-issuing country. Finally, the variable Amount raised represents the funding amount raised during the ICO, expressed in natural logarithm form, which we use in the regression analysis.

Method

Econometric Approach

Our analysis is based on ordinary least squares (OLS) models that incorporate fixed effects at both country and quarter-year levels, enabling us to control for unobserved variations at these levels. Because not all ICO projects provide a LinkedIn profile for their founder CEOs, the possibility of nonrandomness in the decision to include this information raises concerns of sample selection bias. To address this issue, we employ the Heckman (1979) procedure in each of our models and calculate the inverse Mills ratio (IMR) to account for self-selection in the sample, an approach commonly used in previous studies (see, for instance, Momtaz, 2021b; Mansouri & Momtaz, 2022). To obtain the IMR, we first collect data from an additional 654 ICO projects that did not include LinkedIn links for their founder CEOs. We use a probit model to predict the likelihood of this information being present based on ICO and venture characteristics. 16 The calculation of IMR follows Mansouri and Momtaz (2022), and is then included in all models to control for sample selection bias.

We employ two methods to address potential endogeneity issues: restricted control function (rCF) and instrumental variable (IV). These methods allow us to account for potential omitted-variable biases. Again, we follow the approach of Mansouri and Momtaz (2022) by conducting a two-step rCF regression, which reduces the risk of spurious correlations generating endogeneity (Heckman & Navarro-Lozano, 2004). In the first step, we use a probit model to estimate the probability of having a highly extraverted founder CEO, defined as a dummy variable for founder CEOs whose extraversion is above the sample’s median. We next to add the generalized residual (GenRes) from the first stage as an additional control variable of unobserved heterogeneity (Gourieroux et al., 1987).

Further, we use the IV approach to verify that our result is not driven by unobserved variables that could simultaneously explain the dependent and independent variables. Based on psychological literature that finds physical attractiveness to be one of the origins of extraversion (Lukaszewski & Roney, 2011), we use founder-CEO physical attractiveness as the IV. Adopting an extraverted social strategy, which involves actively approaching others and striving for attention, benefits individuals in initiating and maintaining social relationships. The variation in extraversion is believed to result from trade-offs between these benefits and the underlying costs, such as time loss, energy consumption, and the potential for rejection or neglect (Ashton & Lee, 2007; Nettle, 2005). Attractive individuals, in particular, experience lower costs in social interactions, including a lower chance of rejection and better memorability (Kurzban & Leary, 2001; Smith et al., 2009). Consequently, attractive individuals are more likely to adopt extraverted social strategies, leading to higher levels of extraversion. Specifically, we measure the attractiveness of founder-CEO LinkedIn portraits using the Face++ API (Megvii Technology Co. Ltd (Beijing)). Physical attractiveness shows a positive correlation with extraversion, but no link to an individual’s ESG orientation, making it a suitable IV. 17

Robustness Tests for the Measurement of Extraversion

Because data collection takes place after the ICO events, there may be a measurement time bias. For example, the founder CEO of an early ICO could have potentially gained more connections and developed more skills following their ICO event, inflating the subsequent extraversion measurement. To address this concern, we conduct four robustness tests, namely: (i) controlling for the trend effect associated with ICO events; (ii) re-performing the main regression using a subset composed of recent ICOs; (iii) using an alternative text-based measurement for extraversion; and (iv) deriving historical extraversion scores from earlier versions of founder-CEO LinkedIn profiles.

Thus, first, to account for the time-varying effect of ICO occurrence, we follow Huang et al. (2022) and include a time-trend-effect control variable, which is set to 1 for the earliest ICO in our sample set, 2 for the next earliest, and so on to a maximum of 1,011 for the last ICO to occur in our sample period. The second robustness test involves a subsample analysis restricted to ICOs from the three most recent years of our sample (specifically, from 2019Q2 to 2021Q2), where the time gap is relatively minimal, thereby alleviating the concern regarding post-ICO LinkedIn profile changes. For the third test, we follow Block et al. (2019) and employ an alternative measurement of extraversion based on text data from Twitter. Because ICO teams typically do not disclose their personal accounts, we first manually identify the founder CEOs’ Twitter accounts by conducting searches using the names of founder CEOs in our sample and verifying their identity through a comparison of demographic information (e.g., name and work experience) and profile pictures on LinkedIn and Twitter. Once we have identified the appropriate Twitter accounts, we extract the tweets posted by the account owners. To ensure data cleanliness, we remove emojis, hashtags, and non-English tweets. To predict extraversion from the Twitter text data, we implement the deep-learning-based model of Mehta et al. (2020) 18 to predict founder-CEO extraversion by (i) extracting language features from the training dataset, (ii) training the model with extracted language features, and (iii) inputting Twitter text to generate an alternative measurement variable, Extraversion (text). Implementation details are provided in Appendix C of the Online Appendix. Finally, we retrieve historical preICO versions of founder CEOs’ LinkedIn profiles (prior to 2016) from two data sources—a LinkedIn public profile database collected in 2015 and the Wayback Machine 19 and re-rate the LinkedIn indicators, as per section “Operationalization,” to construct Extraversion (historical). In total, we collect 111 historical LinkedIn profiles of founder CEOs from 108 ICOs; data collection details are provided in Appendix D of the Online Appendix.

Results

Summary Statistics

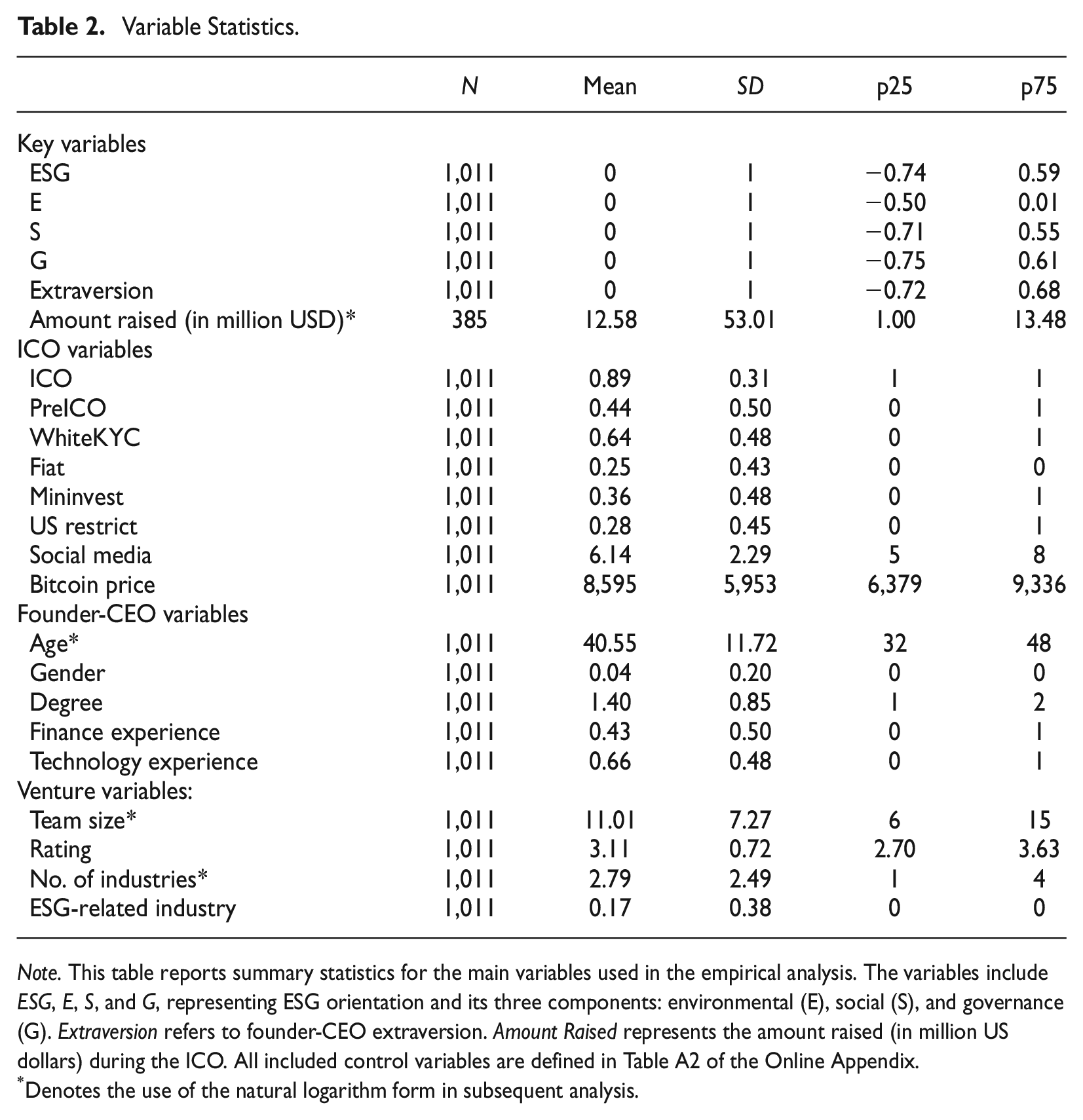

Table 2 shows the summary statistics of the variables. 20 On average, ICOs in our sample have 6.14 social media pages, and an ICO rating of 3.11 (out of 5). Nearly half of the ICOs have a preICO. Founder CEOs are, on average, middle-aged and have an educational level above that of a bachelor’s degree. There are more founder CEOs with technology experience than with finance experience. Female founder CEOs of ICO ventures are a very small population. Figure A2 in the Online Appendix shows the trend of ESG orientation over time: the quarterly mean increases significantly during the sample period, indicating that ESG-related topics are getting greater attention over time. In fact, we find ESG orientation increases by 42.8% between the third quarter of 2017 and the first quarter of 2020.

Variable Statistics.

Note. This table reports summary statistics for the main variables used in the empirical analysis. The variables include ESG, E, S, and G, representing ESG orientation and its three components: environmental (E), social (S), and governance (G). Extraversion refers to founder-CEO extraversion. Amount Raised represents the amount raised (in million US dollars) during the ICO. All included control variables are defined in Table A2 of the Online Appendix.

*Denotes the use of the natural logarithm form in subsequent analysis.

Founder-CEO Extraversion and Sustainability Orientation (Hypothesis 1)

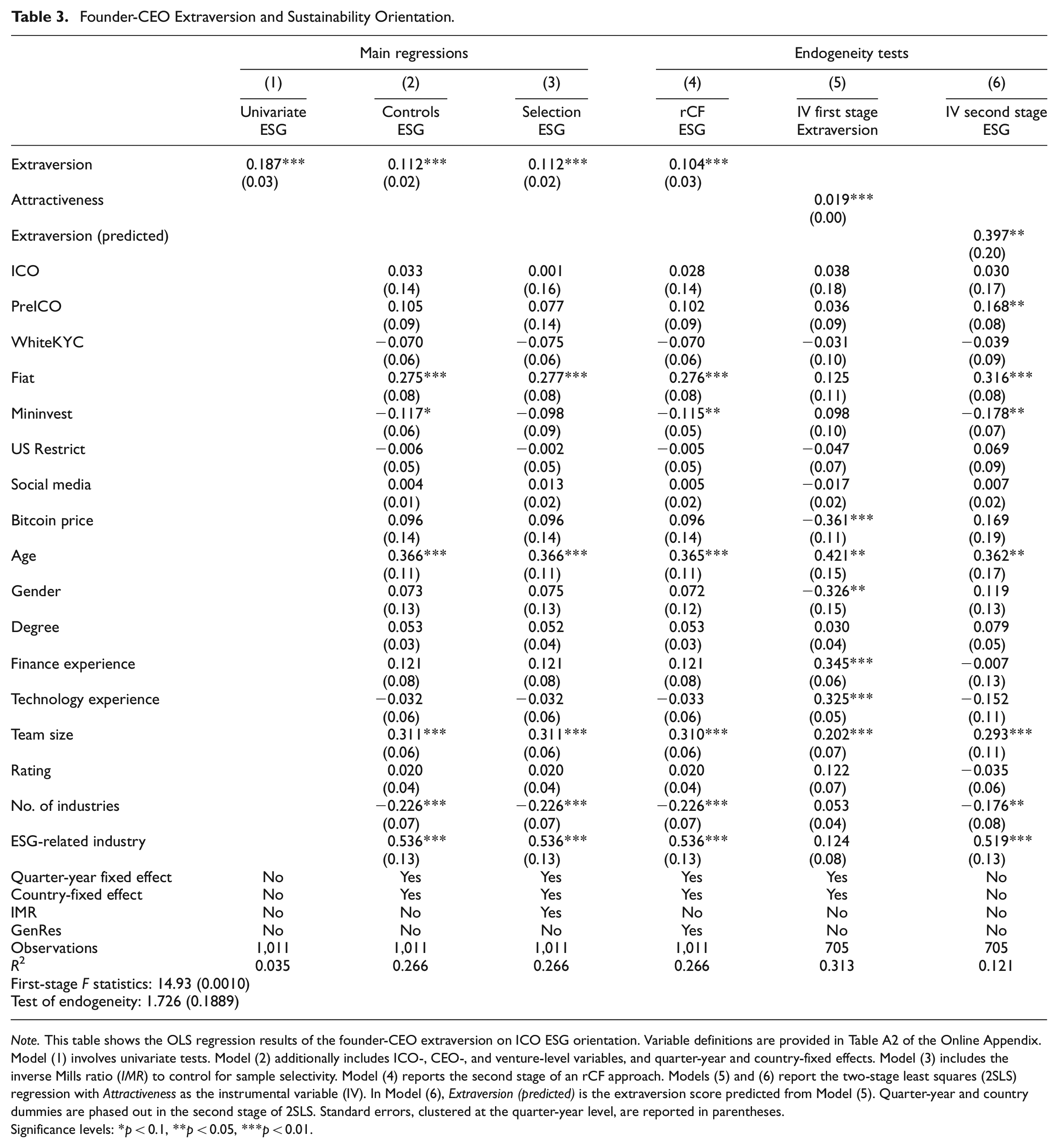

Table 3 shows the results of regressing ICO ESG orientation on the founder-CEO’s extraversion level. Column (3) shows our main estimation results, which control for ICO-specific characteristics, founder-CEO characteristics, quarter-year and country dummies, and sample selection bias by including IMR as an additional control. In line with Hypothesis 1, the coefficient of Extraversion is significantly positive at the 1% level, with a value of 0.112 (p-value < .01). This result is economically significant, with a one standard-deviation increase in founder-CEO extraversion level being associated with an 11.2% standard-deviation increase in ESG orientation. 21 If the IMR control is excluded (see Column [2]), the magnitude and significance of the Extraversion coefficient remain quantitatively similar, indicating that there is no serious sample selection bias in our results.

Founder-CEO Extraversion and Sustainability Orientation.

Note. This table shows the OLS regression results of the founder-CEO extraversion on ICO ESG orientation. Variable definitions are provided in Table A2 of the Online Appendix. Model (1) involves univariate tests. Model (2) additionally includes ICO-, CEO-, and venture-level variables, and quarter-year and country-fixed effects. Model (3) includes the inverse Mills ratio (IMR) to control for sample selectivity. Model (4) reports the second stage of an rCF approach. Models (5) and (6) report the two-stage least squares (2SLS) regression with Attractiveness as the instrumental variable (IV). In Model (6), Extraversion (predicted) is the extraversion score predicted from Model (5). Quarter-year and country dummies are phased out in the second stage of 2SLS. Standard errors, clustered at the quarter-year level, are reported in parentheses.

Significance levels: *p < 0.1, **p < 0.05, ***p < 0.01.

In terms of control variables, Fiat is positively correlated to ESG because accepting fiat currency is a signal of the legitimacy and quality of an ICO project, which is associated with better governance performance. With regard to founder-CEO demographics, Age is positively and significantly associated with ESG orientation, indicating that ventures with older founder CEOs tend to be more ESG oriented. Greater Team size is also positively and significantly associated with ESG orientation, and ICOs in ESG-related industries exhibit strong ESG orientation too, which is not surprising given that the business vision in these industries typically involves ESG-related elements.

The results from our rCF and IV approaches in response to endogeneity concerns are reported in Columns (4) to (6) of Table 3. The second stage of the rCF analysis (Column [4]) confirms a positive and significant association between Extraversion and our dependent variable. In the two-stage IV regression, Attractiveness is positively associated with Extraversion (Column [5]) and the predicted Extraversion remains significant in explaining ESG (Column [6]). 22 These results reinforce our main finding that founder-CEO extraversion is positively correlated with ESG orientation in ICO ventures.

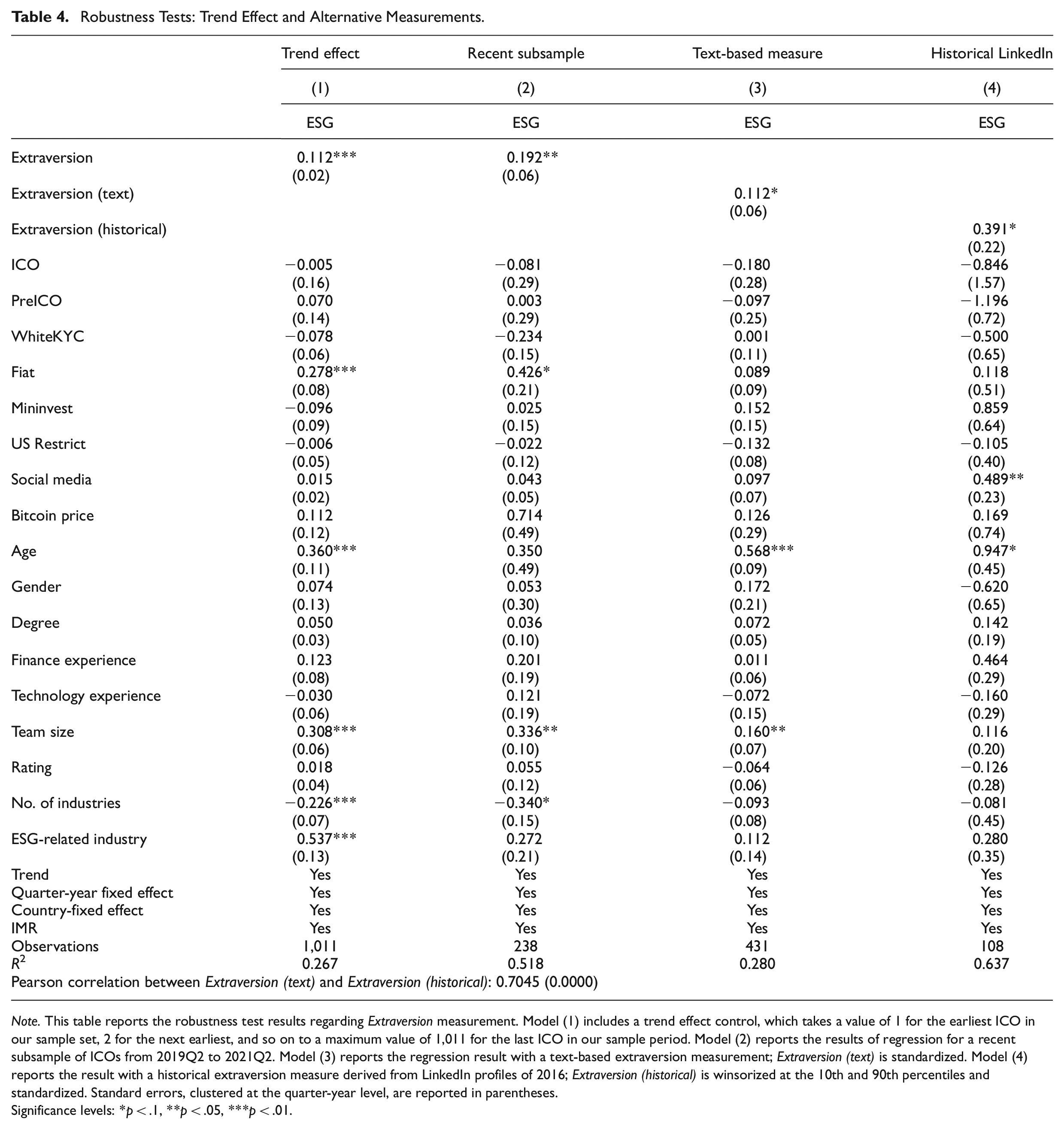

Table 4 shows the results of our robustness checks in relation to the measurement of extraversion, as discussed in section “Robustness Tests for the Measurement of Extraversion.” In Column (1), the coefficient of Extraversion remains positive and significant after controlling for the time-trend effect. In Column (2), we find that the result also remains quantitatively similar when only the most recent ICO subsample is used. Columns (3) and (4), respectively, show our results when we regress ESG on Extraversion (text) and Extraversion (historical). The coefficients of Extraversion (text) and Extraversion (historical) are 0.112 (p-value < 0.1) and 0.391 (p-value < 0.1), which are consistent with our main result. 23 Furthermore, the correlation between Extraversion (historical) and Extraversion is 0.70 (p-value < 0.01), indicating that our measurement is consistent over time. These results suggest that our measurement of extraversion is robust to the potential time bias described in section “Robustness Tests for the Measurement of Extraversion.”

Robustness Tests: Trend Effect and Alternative Measurements.

Note. This table reports the robustness test results regarding Extraversion measurement. Model (1) includes a trend effect control, which takes a value of 1 for the earliest ICO in our sample set, 2 for the next earliest, and so on to a maximum value of 1,011 for the last ICO in our sample period. Model (2) reports the results of regression for a recent subsample of ICOs from 2019Q2 to 2021Q2. Model (3) reports the regression result with a text-based extraversion measurement; Extraversion (text) is standardized. Model (4) reports the result with a historical extraversion measure derived from LinkedIn profiles of 2016; Extraversion (historical) is winsorized at the 10th and 90th percentiles and standardized. Standard errors, clustered at the quarter-year level, are reported in parentheses.

Significance levels: *p < .1, **p < .05, ***p < .01.

Institutional Difference, Extraversion, and Sustainability Orientation (Hypothesis 2)

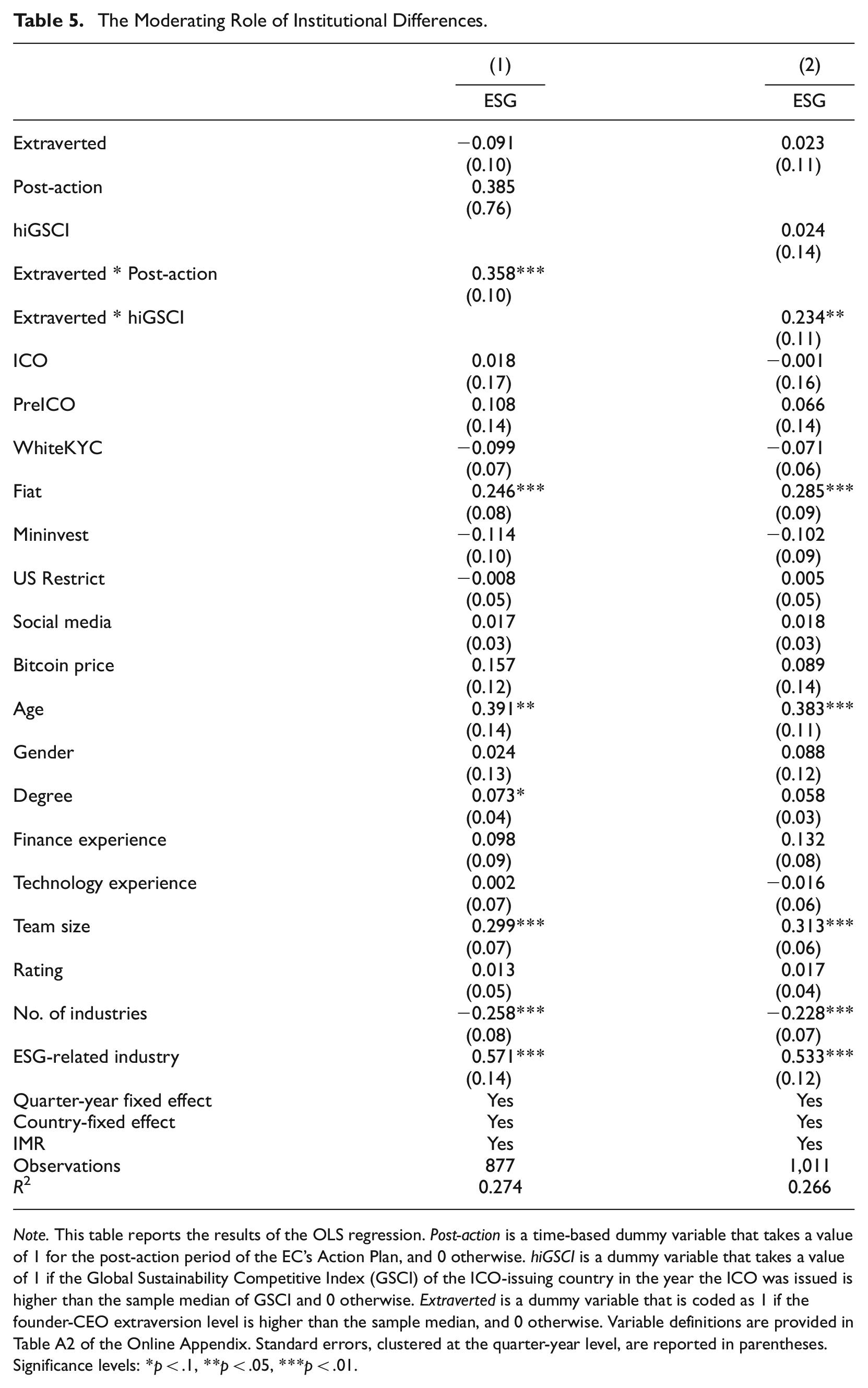

Table 5 shows the results of our analysis of the moderating effects of environmental factors on the relationship between founder-CEO extraversion and ICO ESG orientation. In Column (1), we include the interaction term between founder-CEO extraversion and post-action. The coefficient of the term is significantly positive, indicating that following the adoption of the EC Action Plan, extraverted founder- CEOs tend to emphasize ESG orientation more in their white papers than their peers. This finding supports Hypothesis 2a. 24 Our results show that ICO ventures led by extraverted founder CEOs and initiated after the Action Plan experience a substantial 35.8% standard-deviation increase in ESG orientation, which is economically significant and implies that exogenous shocks such as regulations, policies, and action plans can effectively stimulate the ESG orientation of ICO ventures led by extraverted founder CEOs. The coefficient of the interaction term between founder-CEO extraversion and hiGSCI is reported in Column (2) and indicates that ventures managed by extraverted founder CEOs and issued in a sustainability-oriented country have a 23.4% standard-deviation increase in ESG orientation compared to those managed by introverted founder CEOs and issued in countries with lower social pressure in relation to sustainability. This finding is consistent with Hypothesis 2b.

The Moderating Role of Institutional Differences.

Note. This table reports the results of the OLS regression. Post-action is a time-based dummy variable that takes a value of 1 for the post-action period of the EC’s Action Plan, and 0 otherwise. hiGSCI is a dummy variable that takes a value of 1 if the Global Sustainability Competitive Index (GSCI) of the ICO-issuing country in the year the ICO was issued is higher than the sample median of GSCI and 0 otherwise. Extraverted is a dummy variable that is coded as 1 if the founder-CEO extraversion level is higher than the sample median, and 0 otherwise. Variable definitions are provided in Table A2 of the Online Appendix. Standard errors, clustered at the quarter-year level, are reported in parentheses.

Significance levels: *p < .1, **p < .05, ***p < .01.

Extraversion, Sustainability Orientation and ICO Success (Hypothesis 3)

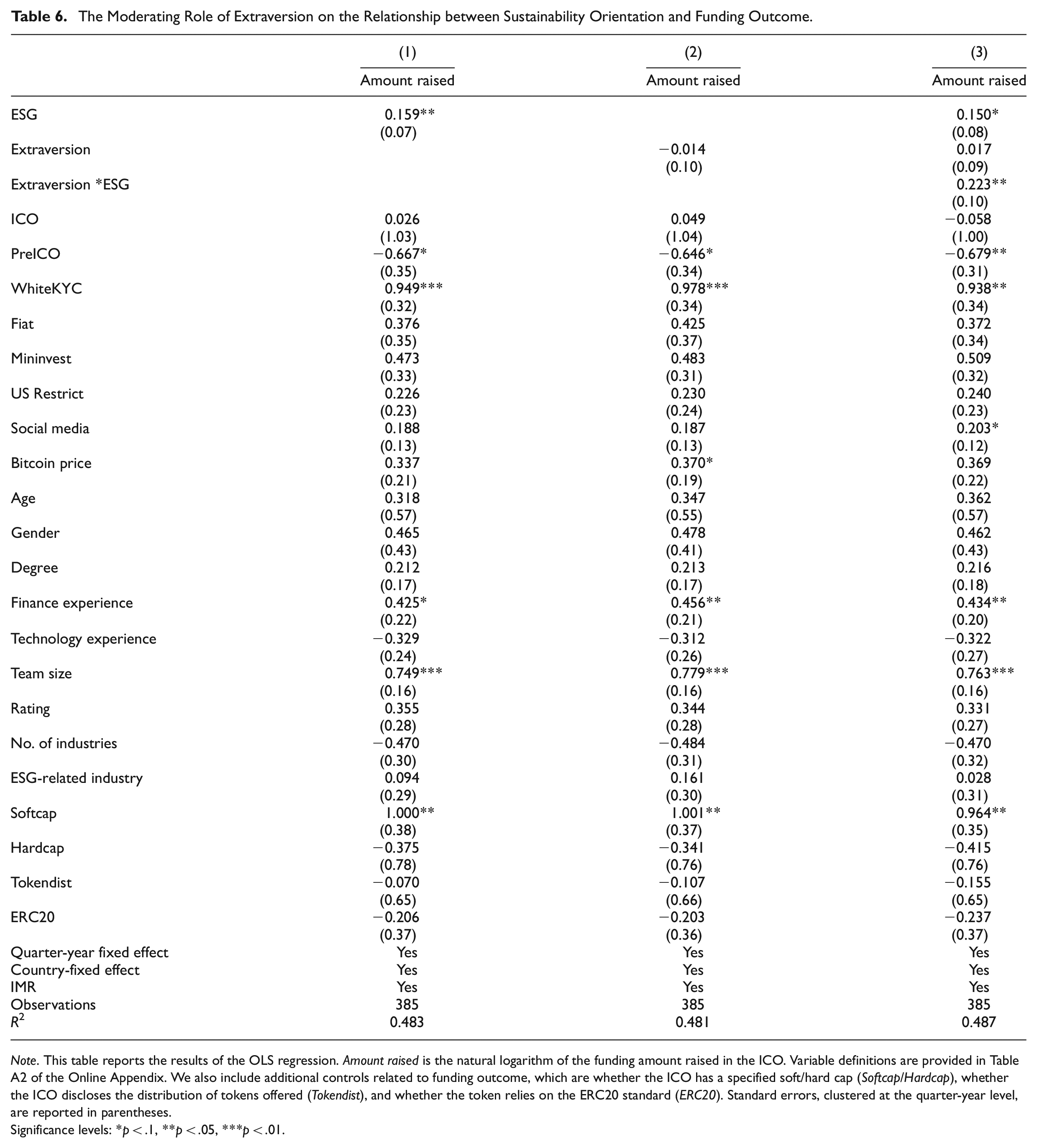

Table 6 presents the analysis results in relation to the potential moderating effects of founder-CEO extraversion on the relationship between ESG orientation and ICO success. In Column (1), the findings indicate a positive and significant correlation between ESG orientation, and the amount raised during the ICO, which is consistent with Mansouri and Momtaz (2022). When the interaction term between extraversion and ESG is included, in Column (3), the coefficient is 0.223 (p-value < .05), suggesting that when both ESG orientation and founder-CEO extraversion increase by one standard deviation, the amount raised during an ICO increases by approximately 25.0% (i.e., exp(0.223)−1). This finding supports Hypothesis 3, indicating that the impact of ESG orientation on ICO performance is magnified if the ICO is managed by an extraverted entrepreneur.

The Moderating Role of Extraversion on the Relationship between Sustainability Orientation and Funding Outcome.

Note. This table reports the results of the OLS regression. Amount raised is the natural logarithm of the funding amount raised in the ICO. Variable definitions are provided in Table A2 of the Online Appendix. We also include additional controls related to funding outcome, which are whether the ICO has a specified soft/hard cap (Softcap/Hardcap), whether the ICO discloses the distribution of tokens offered (Tokendist), and whether the token relies on the ERC20 standard (ERC20). Standard errors, clustered at the quarter-year level, are reported in parentheses.

Significance levels: *p < .1, **p < .05, ***p < .01.

Robustness Checks and Additional Analysis

To provide further insights into the specific relationships between founder-CEO extraversion and the individual pillars of ESG, we conducted separate regressions of E, S, and G on Extraversion. Our findings reveal that the S (social) and G (governance) pillars show significant associations with founder-CEO extraversion, but no significant relationship is observed for E (environmental). We provide detailed results and discussion of this in Appendix B of the Online Appendix.

To ensure the robustness of our findings, we conducted a series of additional tests. These included examining the models in balanced samples using propensity score matching and entropy balancing, controlling for other Big-Five personality traits, addressing LinkedIn-indicator collection-time bias by controlling for time-trend effects, using an alternative measure of extraversion based on text analysis, and incorporating alternative control variables. In all such tests, the results remained consistent with our main findings, indicating their robustness. For the detail of these tests, please refer to Appendix C of the Online Appendix.

Discussion and Conclusion

Summary of the Main Results

This study contributes to the existing literature on the determinants of SE by examining the influence of entrepreneur personality on the ESG orientation as expressed in ICO white papers, and its economic impact. Empirically, we find a positive association between founder CEOs’ extraversion, as measured by LinkedIn indicators, and the level of ESG orientation in their ventures. These results remain robust when controlling for a variety of factors and addressing potential sample biases. Furthermore, we examine the moderating role of the institutional environment and find that extraverted entrepreneurs are more likely to demonstrate higher ESG orientation following the adoption of the EC’s Action Plan and in countries that manifest more sustainable behaviors and practices, resulting in a positive economic impact. Finally, we find that the positive relationship between ESG orientation and venture performance is amplified by the extraversion of founder CEOs.

Academic Contributions

Our study provides contributions to several literature streams. The functional and dynamic dimensions of emerging innovative entrepreneurial finance markets, such as the ICO market, have received substantial attention in the field of entrepreneurial finance and the broader entrepreneurship literature (Bellavitis et al., 2022; Huang et al., 2020; Mansouri & Momtaz, 2022; Momtaz, 2021a, 2021b). Our research covers the intersection of the entrepreneurial and sustainable finance domains, enriching our comprehension of entrepreneurial orientation in relation to sustainability. Our work is most closely related to that of Mansouri and Momtaz (2022), which suggests that greater ESG orientation within an ICO white paper improves short-term funding performance but increases long-term financial constraints. Our research sheds new light on this by exploring the determinants of entrepreneurs’ ESG orientation. Thus, we investigate: (i) the potential of entrepreneurs’ personality traits, such as extraversion, to explain ICO orientations toward ESG; (ii) the interplay between entrepreneurs’ extraversion and institutional factors; (iii) the influence of an entrepreneur’s extraversion on the economic impact of ESG orientation in the success of the ICO.

Understanding the factors that affect the practice of SE has become a major focus (Anand et al., 2021). For example, Vuorio et al. (2018) highlight the positive association between entrepreneurs’ attitudes toward sustainability and their sustainability-oriented entrepreneurial intentions, while Mupfasoni et al. (2018) emphasize the contribution of prior knowledge to the sustainability aspect of business plans. We contribute further understanding of the vital role of underlying and enduring personality traits in shaping how individuals perceive and seize entrepreneurial opportunities, even when they possess ostensibly identical information and skills (Shane, 2003). Taking as a starting point Shane’s (2003) seminal work on the pivotal role of the individual-opportunity nexus in entrepreneurship, we argue that extraverted entrepreneurs are better able to recognize and exploit SE opportunities than their introverted counterparts. Our evidence suggests that founder CEOs with higher levels of extraversion are more likely to demonstrate a strong commitment to sustainability, which can be attributed to their greater social inclination and more effective management capabilities. By presenting the influence of individual psychological differences on entrepreneurs’ recognition and exploitation of opportunities, particularly within the context of ESG considerations, our results contribute significantly to the SE literature.

Our theory and its associated cross-country empirical evidence also provide important contributions to the literature at the intersection of SE and institutional theory (e.g., Boettke & Coyne, 2009; Bradley et al., 2021; Chowdhury et al., 2019). For the most part, prior research on entrepreneur personality has not been context specific, and has typically been conducted in single countries (e.g., Antoncic et al., 2015; Karimi et al., 2017; Zhao et al., 2010), effectively ignoring potential variations between countries of institutions. The implicit assumption in this regard has been that personality traits and their associated processes are universal, and where they are studied is therefore of no consequence. However, when pursuing entrepreneurial opportunities, entrepreneurs are not isolated actors. On the contrary, they are influenced by the institutional context in which they operate (Shane, 2003). Given the context-bound nature of ESG (Julian & Ofori-dankwa, 2013), we argue that entrepreneurs with similar levels of extraversion may have different views of, and take different strategic decisions about, ESG orientation as a result of institutional differences (Amaeshi et al., 2006; Matten & Moon, 2008; Robertson, 2009). We specifically demonstrate that extraverted founder CEOs, with their broader networks and heightened social inclination, show greater sensitivity to sustainability-related social concerns than non-extraverted ones. Importantly, we observe that ICO ventures led by extraverted founder CEOs display a higher ESG orientation in their ICO white papers following a regulatory change, such as the EC’s Action Plan on Financing Sustainable Growth. Likewise, in countries where sustainable behavior and practices are more widely adopted, extraverted entrepreneurs are again more inclined to exhibit greater ESG orientation. Overall, we provide empirical support to the institutional difference hypothesis, which suggests that ESG responses will be significantly context dependent and thus likely to depend on the institutional context in which the venture is operating. Our work fills a gap in the understanding of how individuals’ duality and context explain the complex, temporal interactions between sustainability-oriented entrepreneurs and their surroundings (Johnson & Schaltegger, 2020).

Finally, our study contributes significantly to the broad stream of ICO literature by extending the linkage between entrepreneurial characteristics, SE, and funding outcomes. 25 By exploring how the interaction between entrepreneur personality and SE impacts such outcomes for ICO ventures, our research adds to the foundations of the recognition of the multifaceted nature of new fundraising methods, and highlights the importance of aligning entrepreneurial personality traits with sustainability objectives to achieve favorable funding outcomes. As such, our work also contributes to the research focus on the economic impact of managerial personality traits (Green et al., 2019).

Practical Implications

Given the link established between extraversion and SE, policymakers can more strategically allocate resources and extend support to initiatives to prioritize ESG-related impacts within entrepreneurial ecosystems, incorporating a more specific emphasis on extraverted entrepreneurs. By directing attention toward such individuals, policymakers can leverage their natural inclination and proficiency in engaging others to maximize the efficiency and effectiveness of resource allocation. Furthermore, recognizing that entrepreneurs are influenced by their surrounding environment, policymakers can strategically create and cultivate a sustainability-oriented institutional framework that serves as a motivating force for adopting SE.

Gaining insights into how institutional factors moderate the relationship between extraversion and SE is crucial for entrepreneurs when it comes to developing effective adaptation strategies that align with their specific institutional context. By understanding the interplay between extraversion and institutional factors, entrepreneurs can tailor their approaches and behaviors to leverage the associated opportunities and navigate the challenges within their institutional environment. For instance, in a sustainability-oriented institutional context, extraverted entrepreneurs can capitalize on their social inclinations and governance skills to proactively engage with stakeholders, build networks, and promote sustainable practices. Moreover, to achieve improved financial outcomes, entrepreneurs can strategically enhance the visibility of their advocacy efforts in relation to sustainability.

Investors can greatly benefit from considering personality as a relevant factor when evaluating entrepreneurial ventures. By incorporating this dimension into their evaluation criteria, they can make more informed investment decisions and conduct more thorough risk assessments. In addition, the consideration of extraversion can help funding organizations to allocate support and resources to ventures that demonstrate higher likelihoods of achieving both sustainability and financial outcomes.

Limitations and Avenues for Future Research