Abstract

In the decade since the global financial crisis, an increasing number of jurisdictions have added mandatory financial literacy education to school curricula. Governments recognize that this increases the burden on teachers, who may also lack the confidence to teach financial literacy. One response is to encourage the use of resources produced or sponsored by the financial services industry. The concern is that these resources may promote the industry’s interest in maximizing profits and minimizing regulation over students’ interest in becoming empowered financial consumers. As a first step in investigating this concern, we compared resources from the Canadian Financial Literacy Database produced or sponsored by the financial services industry with those produced by government, non-profit organizations and individuals. We focused on online resources intended for use by elementary teachers and students to determine whether the key themes and messages conveyed vary based on who made or paid for the resource. We found that key themes are consistent across resources, regardless of industry affiliation, but that resources produced or sponsored by the financial services industry are more likely to exhibit a moralistic tone.

Keywords

Introduction

The decade since the global financial crisis has seen an increase in the number of mandated financial literacy curricula (Batty et al., 2015). The addition of financial literacy education to mandatory school curricula increases the burden on teachers, who frequently lack the training, background, and confidence to teach in this area (Henning and Lucey, 2017). One often proposed response to alleviate this burden is to leverage the resources of financial services companies, including banks, credit unions, and payment networks (e.g., VISA) to provide financial literacy education resources (Batty et al., 2015; Organization for Economic Cooperation and Development [OECD], 2013; Task Force on Financial Literacy, 2010). The financial services industry is answering this call and producing or sponsoring financial literacy education materials intended for use by parents and teachers (McCormick, 2009).

The concern raised by using resources produced or sponsored by the financial services industry is that even when they are authored by experts or teachers, they will promote the industry’s interests in maximizing profits and minimizing regulation over students’ interests in becoming empowered financial consumers (Collins et al., 2017). Determining whether this conflict of interest should preclude educators from relying on such resources is difficult. One goal of financial literacy education is to encourage the use of asset-building financial products, such as savings accounts, which also helps to boost industry profits (Cole et al., 2013). Another goal is to help consumers choose from the increasingly wide array of complex financial products available (Financial Consumer Agency of Canada [FCAC], 2015; Ontario Ministry of Education Working Group on Financial Literacy, 2010), but focusing on educating consumers fails to hold the industry accountable for creating such a complex market in the first place.

As a first step in investigating this concern, our study examines whether the content of financial literacy education resources varies based on who makes or pays for them. We compared three categories of resources: resources produced by the financial services industry; resources sponsored by the financial services industry; and resources neither produced nor sponsored by the financial services industry. To our knowledge, this study is the first to compare the content of financial literacy education resources based on the producer or sponsor of the resource.

We focused on online resources aimed at elementary students and teachers. We selected online resources because of their predominance as a source of informal professional development for teachers (Beach, 2017). We focused on resources aimed at the elementary level due to the consensus in the literature that financial literacy education must start early if it is to affect individuals’ financial behavior in the long-term (Batty et al., 2015; FCAC, 2015; John, 1999; McCormick, 2009).

The scope for the study are resources aimed at elementary school aged children and elementary school teachers found in the Canadian Financial Literacy Database (“Database”). In their review of financial education programs aimed at children and adolescents, Amagir et al. (2018) found that the concepts covered in these programs does not vary by country, making our findings applicable and relevant outside of Canada. The online Database is curated and hosted by the Financial Consumer Agency of Canada, the federal agency tasked with financial consumer protection with respect to federally-regulated financial institutions. The Database was created on the recommendation of the federal Task Force on Financial Literacy to serve, among other purposes, as “a hub for Canadian teachers” providing “high-quality, unbiased information from a range of expert sources” (2010: 8, 62). Although the Database Terms of Use state that resources will not be included if they “promote the sale of a particular product or service or favor a particular product or service over others” (FCAC, 2017), this does not necessarily preclude materials that promote the interests of the financial services industry generally.

To compare resources currently included in the Database by producer or sponsor, we conducted a document analysis, combining elements of content analysis and thematic analysis (Bowen, 2009). We found that key themes (e.g., spending habits, money gives choice) were consistent across resources regardless of industry affiliation. One difference we found is that resources produced or sponsored by the financial services industry are more likely to exhibit a moralistic tone, by either explicitly or implicitly judging certain financial behaviors as right or wrong, and to place an even greater emphasis on individual responsibility for one’s own financial circumstances than resources produced by individuals, government, or non-profit organizations. This lends some support to the theory that these resources prioritize the industry’s interest in shifting the regulatory burden of ensuring the safety of financial products from the industry to the consumer (Williams, 2007).

The rest of the article is organized as follows. We first provide an overview of the relevant literature. We then describe our methodology, including the steps involved in the analysis. This is followed by a description and discussion of our findings. We conclude with study limitations and future directions.

Literature review

The definition of financial literacy used by the Canadian government is “having the knowledge, skills and confidence to make responsible financial decisions” (Task Force on Financial Literacy, 2010: 10). Other governments (Exec. Order No. 13646, 2013) and international organizations (OECD, 2012) use similar definitions. This definition combines the traditional understanding of financial literacy as knowledge of financial concepts with “financial capability” or “the skills to apply this knowledge” (Amagir et al., 2018: 57). The Ministry of Education of the Canadian province of Ontario also uses a similar definition, but adds that financial literacy education should also encourage students to develop “a compassionate awareness of the world around them” (Ontario Ministry of Education, 2016: 3).

Traditionally, the delivery of financial literacy education curricula was left to non-profit or charitable organizations. In the wake of the global financial crisis, however, governments identified financial literacy as a necessary life skill for individuals and decided that a financially literate population would improve financial stability (Amagir et al., 2018; OECD International Network on Financial Education [OECD/INFE], 2012). Governments’ current interest in financial literacy education is unlikely to wane, since increasing citizens’ financial literacy is a policy goal that appeals to parties across the political spectrum (Willis, 2008).

The evidentiary basis for this policy position is questionable. Evidence on the effectiveness of financial literacy education in not only improving students’ knowledge and understanding of financial concepts, but also improving their financial capability is limited and mixed at best (Amagir et al., 2018; Batty et al., 2015; Hamilton et al., 2012; Mandell and Klein, 2009; Miller et al., 2015; Willis, 2009). Blue and Pinto point to the problems and dangers of focusing on financial literacy training over improving employment opportunities in and for marginalized communities (Blue and Pinto, 2017). There appears to be a consensus in the literature, however, that if financial literacy education is to be effective, then it needs to start early, in the elementary school years (Amagir et al., 2018; Batty et al., 2015; FCAC, 2015; John, 1999; McCormick, 2009). The US President’s Advisory Council on Financial Capability suggested that “[p]arents can start teaching children as young as 2 about money” (President’s Advisory Council on Financial Capability [PACFC], 2013: 7). Evidence from other areas, such as nutrition, suggests that effects on attitudes of elementary students will carry through to adulthood (Batty et al., 2015). Furthermore, children are faced with having to make financial choices, even from a young age (McCormick, 2009). The challenge is that elementary school teachers often report feeling unqualified to teach financial literacy (Henning and Lucey, 2017; Ontario Ministry of Education Working Group on Financial Literacy, 2010; PACFC, 2013).

As governments’ attention to financial literacy education in schools has increased, so has their engagement with industry stakeholders in designing financial literacy curricula. At least one Canadian province explained its decision to create a new financial literacy curriculum as a response to “requests from the education sector and industry stakeholders” (Government of Saskatchewan, 2018: 1). Teachers are not necessarily opposed to engaging with industry on this issue: in one study of pre-service teachers and teacher educators, respondents supported collaborating with “members of the local financial services industry” to teach financial literacy in school (Henning and Lucey, 2017: 167–168).

Some scholars have expressed the concern that financial literacy education serves the interests of the financial services industry, rather than consumers. Financial literacy education driven by the industry may also “reinforce and reify conventional, neoliberal approaches, attitudes, and ideologies toward debt, credit, finance, and money” (Haiven, 2017: 349). It also shifts the focus away from the increasing complexity of the financial marketplace, caused by the industry, which creates the pressing need for financial literacy in the first place (FCAC, 2015; PACFC, 2013; Sawatzki, 2017; Willis, 2009). This gives the industry an incentive to support financial literacy education strategies to try to avoid other forms of financial products regulation. This creates the potential for conflict of interest when financial services companies produce or sponsor financial literacy education resources for use in the classroom, in contrast to, for example, resources found on company websites, where the self-interested motive is clear.

To some extent, this conflict is inherent in government financial literacy strategies because these strategies emphasize responsible money management by the individual or household over responsible lending and sales practices by the financial industry (see Waldron, 2011; Williams, 2007). Furthermore, one goal of financial literacy education is take-up of financial services, such as a savings account, which also may increase industry profits (Batty et al., 2015; Cole et al., 2013). So although these companies are in a conflict of interest when they produce or sponsor financial literacy education resources, the fact that industry-affiliated resources emphasize individual responsibility or promote the use of bank accounts does not necessarily mean that they are worse for students than resources with no industry affiliation. This is why a comparison between industry- and non-industry-affiliated resources is necessary.

Although, as noted above, this potential conflict of interest has been identified by other authors, we are not aware of any previous empirical studies that seek to examine whether financial literacy education resources provided by the financial services industry further the industry’s interests in maximizing profits and avoiding new regulation over students’ interest in becoming empowered financial consumers. As a first step in answering this question, we compared the key themes and messages of financial literacy education resources produced or sponsored by the financial services industry with those produced or sponsored by non-industry-affiliated individuals, governments and non-profit organizations to determine whether content varied based on industry affiliation. Our methodology is described in detail in the next section.

Methodology

Research design

This study employed qualitative methods and descriptive statistics to examine and compare the key themes and messages in three categories of financial literacy education resources: those produced by a financial services company, those sponsored by a financial services company, and those neither produced nor sponsored by a financial services company. Resources in this third category included those produced by individuals, governments, or non-profit organizations. We used a document analysis: “a systematic procedure for reviewing or evaluating documents”, including electronic documents (Bowen, 2009: 27). Through an iterative process of skimming, reading, and interpreting, we combined elements of content analysis and thematic analysis. The content analysis offered a process of organizing information from the Database into categories. This was followed by a thematic analysis, a process of careful reading and focused re-reading of the data (Bowen, 2009). As a result of the thematic analysis, key themes and key words were generated from the data (Thomas, 2006). We then coded resources for key themes and recorded the frequency of key themes and key words. Each step is further described below.

Context of the study

The financial literacy education resources reviewed for this study are those included in the Canadian Financial Literacy Database (https://www.canada.ca/en/financial-consumer-agency/services/financial-literacy-database.html). The Database was created on the recommendation of the federal Task Force on Financial Literacy and is maintained by the Financial Consumer Agency of Canada (“FCAC”) and housed on its website. Individuals or companies with an FCAC account may submit resources for inclusion in the Database. The FCAC in its sole discretion determines which submitted resources will be included based on the following criteria: the resource contributes to the financial literacy of Canadians, is available in one or both official languages, is free or for a “reasonable fee”, and “does not promote the sale of a particular product or service or favor a particular product or service over others”.

Data analysis

Identifying appropriate resources

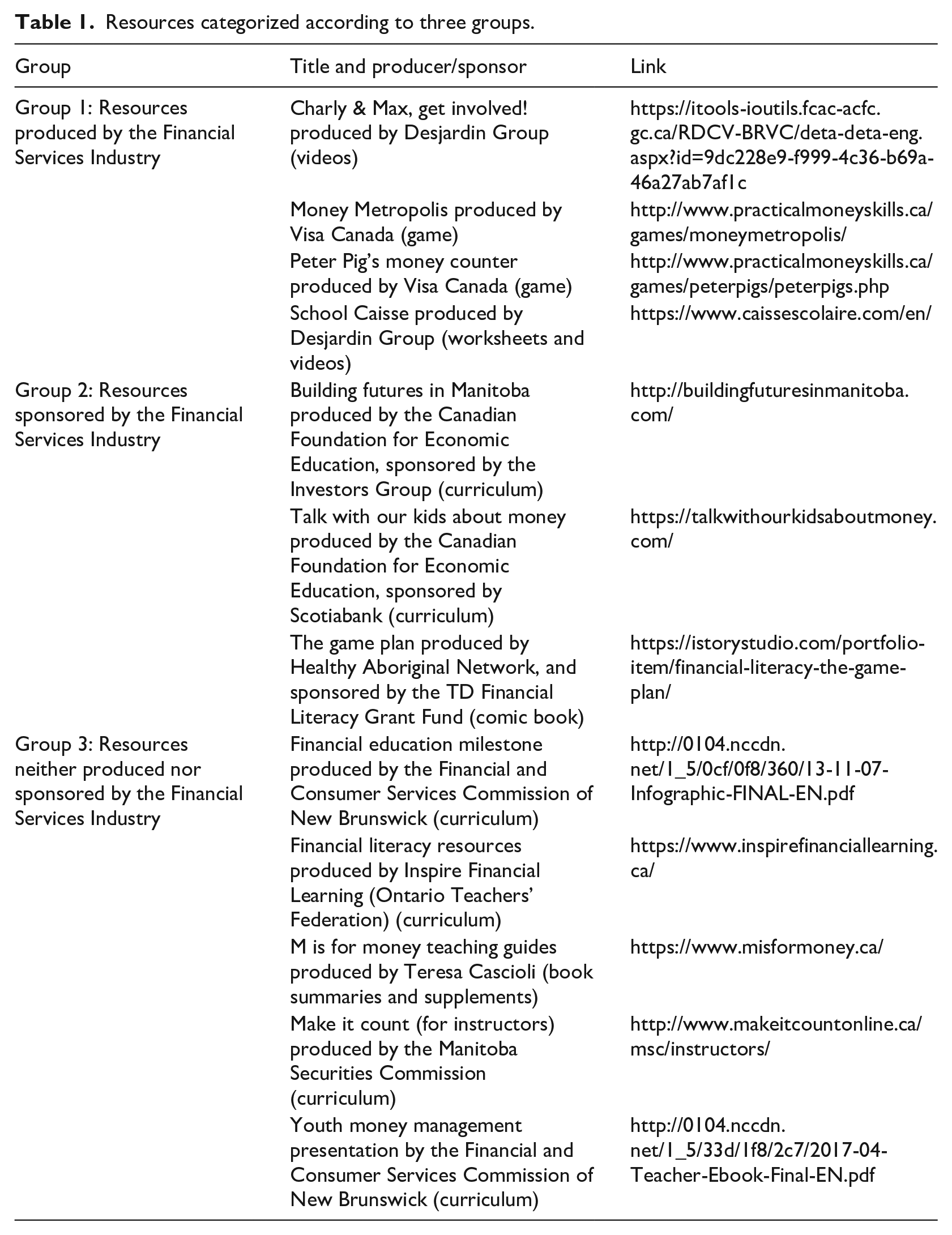

At the time of analysis, the Database included separate categories of resources for “Educators”, “Parents”, “Students”, and “Youth/youth at risk”. The scope for this study was narrowed to resources targeting elementary students and teachers. Resources in French or those that required payment to access were omitted. As a result, twelve resources, five targeted at elementary students and seven targeted at elementary school teachers, were included in our analysis (see Table 1). These twelve resources were divided into three categories: resources produced by the financial services industry, resources sponsored by the financial services industry, and resources which are neither produced nor sponsored by the financial services industry (i.e., no industry affiliation). This last category includes resources produced or sponsored by government agencies, professional teachers’ organizations, and individuals.

Resources categorized according to three groups.

Several of the twelve resources contained multiple “units”. Units included separate web pages, videos, games, lesson plans, and teacher guides and were identified in order to further examine and code as sub-components of each resource. We included the “Home Page” and “About Us” web pages from each of the twelve resources, as these would likely be initially viewed by site visitors when entering the websites. To maintain our focus on resources included in the Database, external links were excluded. All other units were included for 11 of the resources. For the twelfth resource (“Charly & Max, Get Involved!”), we selected a sample of 8 videos out of a total of 51. Quizzes following the videos were excluded from the dataset. The process of identifying units occurred through ongoing conversations between the research team and resulted in 141 total units. Most of the 141 units were PDF or text documents; the rest were videos and flash games. PDF or text documents were downloaded for coding. Videos were transcribed for coding. To code for key themes in flash games, a written description of the game was produced and then coded. To code for key words in flash games, one researcher played the games once and recorded each time a key word appeared in the game. All written documents were uploaded into NVivo (2012), a qualitative data analysis software program. NVivo was chosen for this study because it aids in the organization and management of large datasets.

Identifying and coding for key themes

An open coding process was used to identify recurring and relevant ideas expressed in the units included in the scope of the study. Twelve units from the Database were selected for this initial open coding. Two researchers separately reviewed these units and recorded “Plot or Activity”, “Key Messages”, “Terminology”, and “Notes” for each. A third researcher identified fifteen key themes from these notes. Two researchers then coded three units to identify examples of each key theme. Three researchers then revised this list down to twelve key themes and agreed on definitions and examples of each.

Two members of the research team coded the units for key themes. These researchers brought two different disciplinary perspectives to this process, law and education. Thirteen of the units (approximately 10%) were randomly selected from the total 141 units. These thirteen units were chosen across the different resources and included a variety of media (text, video, games). Each researcher separately coded these units for the twelve key themes. The researchers then met to compare results. Coding methods were revised so that each resource would be coded for a maximum of three key themes based on the most dominant messages in the unit.

The same two researchers then separately coded all 141 units. When the researchers met to compare results again, there was a 50% agreement rate. After discussion, the researchers removed two key themes: “Taking Personal Responsibility” and “Curiosity and Exploration”. The researchers decided that these two themes represented pedagogical descriptor-frameworks rather than tangible financial literacy topics. After these two key themes were removed, the two researchers compared disparity in codes and decided that if both identified common themes for a unit, the unit would be coded in the common theme and any theme coded for by only one researcher would be removed. The researchers also decided that if a unit was now empty-coded for one researcher (after removing the disparate theme), the unit would automatically be coded with the other researcher’s key themes. This process resulted in an 80% agreement rate between the two researchers.

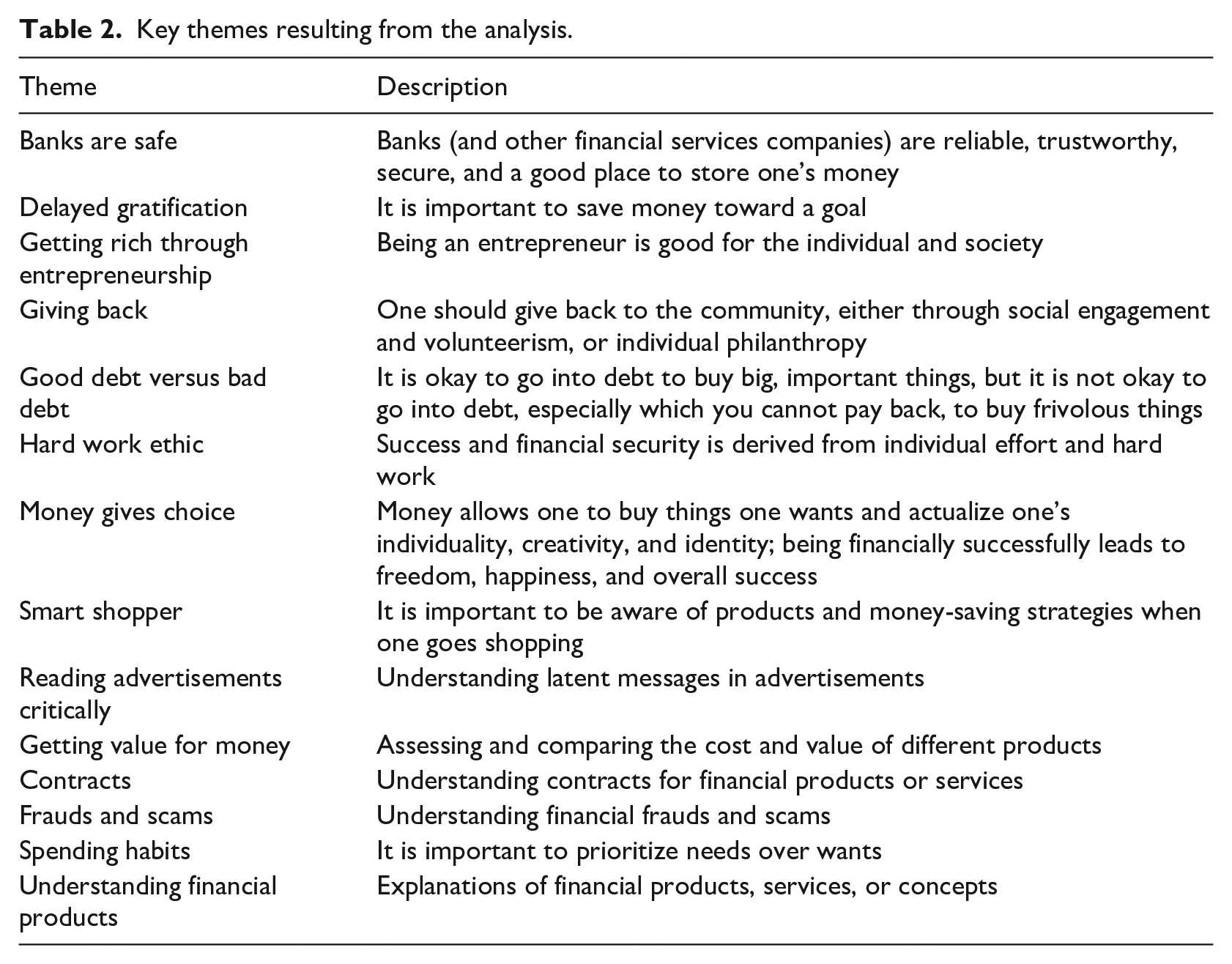

A final discussion among the research team led to the decision to separate the theme “Smart Shopper” into four sub-categories: “Reading Advertisements Critically”, “Getting Value for Money”, “Contracts”, and “Frauds and Scams”. This decision was made because each sub-category represented distinct and separate ideas. One researcher revisited the units coded for “Smart Shopper” and re-coded every unit as a sub-category. The final thirteen key themes and their definitions are listed in Table 2.

Key themes resulting from the analysis.

Identifying and coding for key words

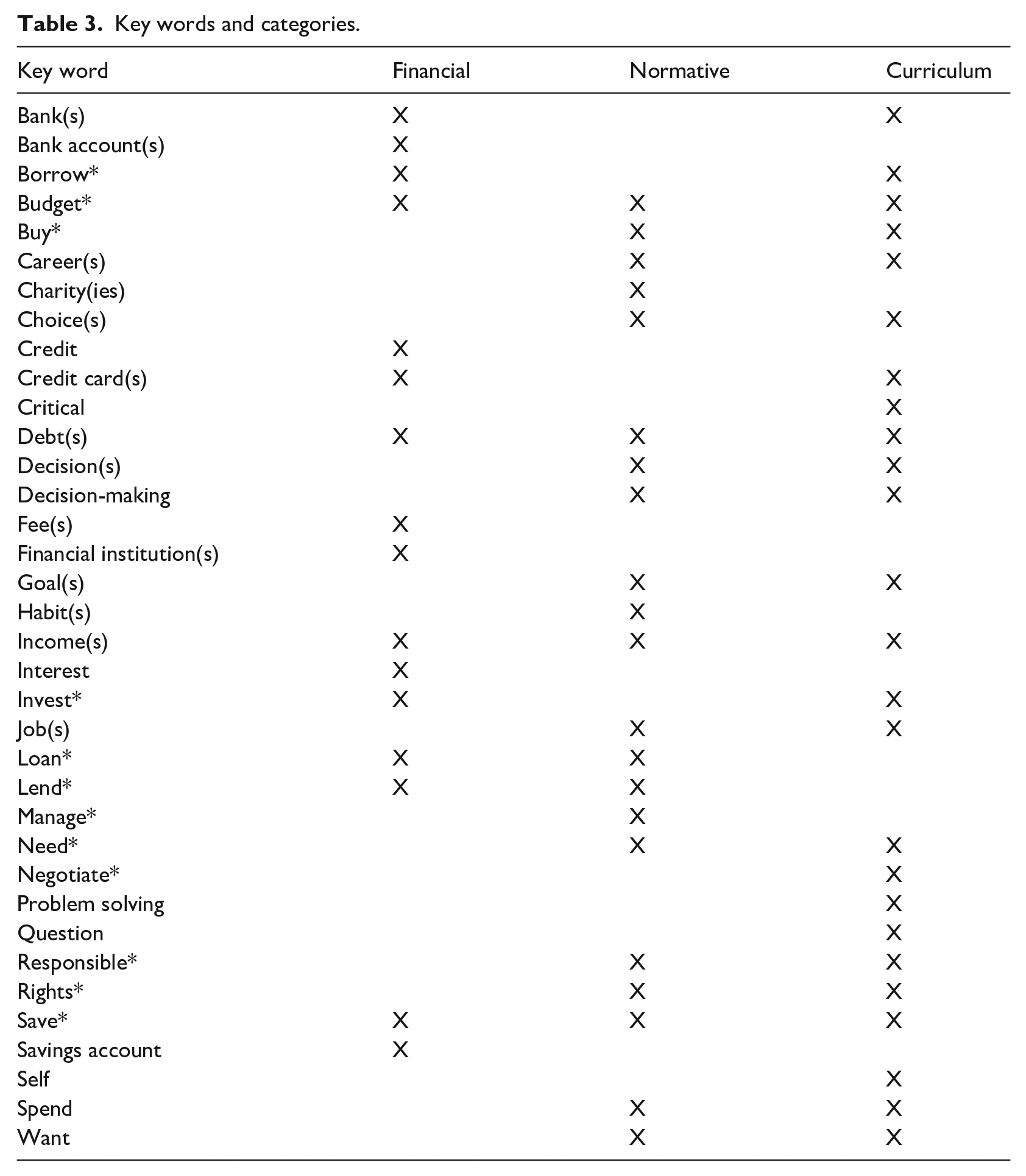

One member of the research team identified a list of 68 relevant key words targeting financial literacy terminology. These key words were developed based on the initial notes made on the same sample of twelve units discussed above. We also decided to use the Ontario Financial Literacy Scope and Sequence curriculum document for Grades 4-8 as a source for keywords (Ontario Ministry of Education, 2016). The decision to use this document was based on the familiarity of the document by one of the research team members, who had formerly taught in Ontario’s elementary education system. Additionally, Ontario is Canada’s most populous province and the province in which the research team’s institution is located. A future study could use additional curricular documents from a variety of provinces and states as sources for keywords. For the purposes of our exploratory methods, we deemed this scope and sequence document to be appropriate for offering keywords in addition to those identified based on our initial notes. Exact repetitions of key words were removed (e.g., combining “bank” and “banks”, but not “credit” and “credit cards”) and words with a common theme or prefix were expanded into a general word (e.g., using “self” to capture “self-awareness” and “self-monitoring”). In the end, the research team identified 36 key words to use to code the Database units.

Upon reviewing the key words in relation to the literature, the research team noted three major categories into which the key words could be sorted. These categories included: “financial” (16 key words), “normative” (21 key words), and/or “curriculum” (25 key words). “Financial” key words describe financial products or concepts, such as “credit”, “fee(s)”, and “interest”. “Normative” key words describe or relate to financial or other behaviors that are viewed as socially positive, for instance “charity(ies)”, “habit(s)”, and “manage*”. Key words that were categorized as normative represented opportunities for value judgments on different financial products or choices. Normative key words are especially pertinent to financial literacy education, given the focus on changing behavior. Finally, “curriculum” key words are drawn from the Financial Literacy Resource Guide for the Ontario Curriculum Grades 4-8, and included “negotiate*, “problem solving”, and “self*”. Words which were categorized as all three included “budget*”, “debt(s)”, “income(s)”, and “save*”. The complete list of keywords and how they were categorized can be found in Table 3.

Key words and categories.

One member of the research team coded all 141 units for the 36 key words. Units were coded using the “text search” function in NVivo. Most key word searches included stem variations of the key word (i.e., “borrow” included “borrows”, “borrowing” and “borrowed”). Some key words were limited to the exact or very similar form in cases when the research team agreed that adding stem variations would change the meaning of the key word (i.e., “bank” and “banking”). The researcher was careful to only record results for words that were used appropriately in a financial context (i.e., “interest” was only recorded when it referred to financial interest, “question” was only recorded when students were encouraged to question an idea or teaching).

Findings and discussion

Key themes

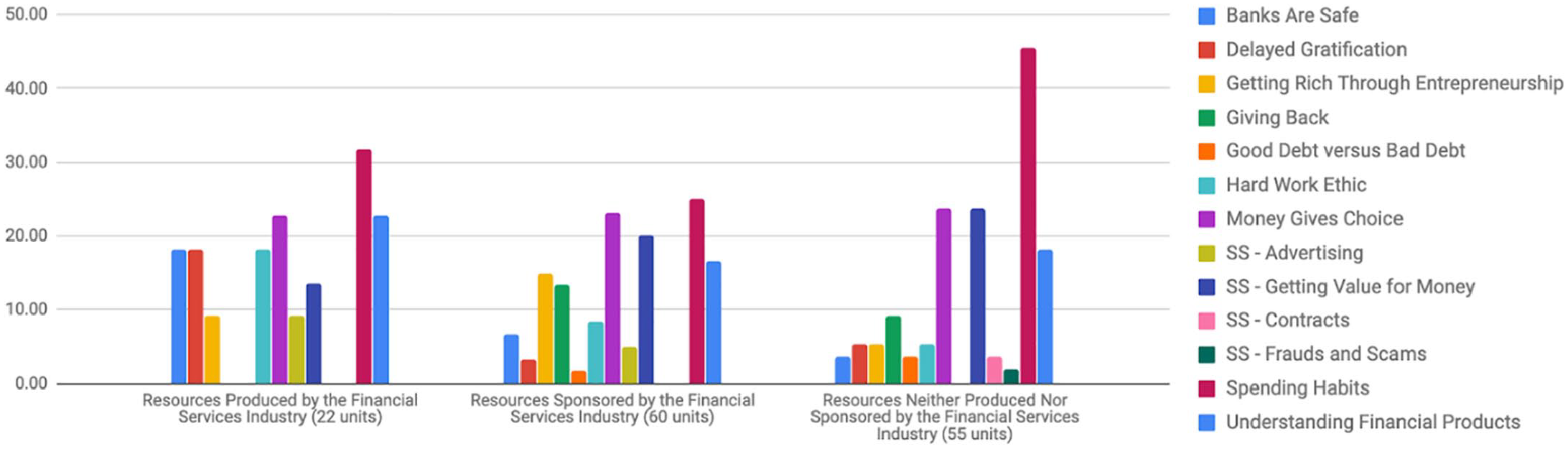

As illustrated in Figure 1, the key themes we identified appeared consistently across resources, regardless of industry affiliation, suggesting that content does not vary based on who made or paid for the resource. Both the key themes identified and the consistency are generally in keeping with the dominant, conventional approach to financial literacy, which focuses on individual choice, rather than systemic constraints on those choices (Blue and Pinto, 2017). Eight of the thirteen themes were coded for in all three categories of resources. The top two most frequently coded key themes, “Spending Habits” and “Money Gives Choice”, were the same in all three categories. “Getting Value for Money” was the third-most frequently coded theme in resources sponsored by the financial services industry and neither produced nor sponsored by the financial services industry. Although “Understanding Financial Products” was the third-most frequently coded theme in resources produced by the industry category, it is also the fourth most frequently coded theme in both other categories.

Percent of units coded with key theme in each resource category.

In terms of differences of theme concentration among the categories, resources produced by the financial services industry had the highest percentage of the themes “Banks Are Safe”, “Hard Work Ethic”, “Smart Shopper - Advertising”, “Understanding Financial Products”, and “Delayed Gratification”. The high percentage of “Banks Are Safe” is the result of one of the four resources in this category being an in-school deposit account program, which had three units coded for this theme. Resources sponsored by the financial services industry had the highest percentages of “Getting Rich Through Entrepreneurship” and “Giving Back”. Resources neither produced nor sponsored by the financial services industry had the highest percentages of the themes “Good Debt versus Bad Debt”, “Smart Shopper - Getting Value for Money” and “Spending Habits”, as well as the only instances of “Smart Shopper - Contracts” and “Smart Shopper - Frauds and Scams”.

A closer examination revealed some differences in how these key themes were reflected among the different categories. Although non-industry affiliated resources replicated the dominant, conventional themes of financial literacy education, the discussion of these themes makes a bit more space for students to develop “a compassionate awareness” of how circumstances beyond an individual’s control might affect their ability to save and budget. For instance, resources produced or sponsored by the financial services industry tended to be more prescriptive than resources neither produced nor sponsored by the industry, which took a more inquiry-based approach. In one unit of a resource produced by the financial services industry, the following statement was coded for the theme “Banks Are Safe”: “Maybe an account would be a good idea after all. . .my money would be safer!” (Charly & Max, Get Involved!, “High Security”). Similarly, in a unit of “School Caisse” students are encouraged to complete a fill-in-the-blank activity sheet which then reads “By choosing to deposit my money in the school caisse, I am learning about the world of savings”, implying that a deposit account with a financial institution is the only, or at least the best, way to save. By contrast, a unit neither produced nor sponsored by the financial services industry was less prescriptive, with a lesson plan prompting a discussion on the questions “How would you save money; where would you save it; what banks or credit unions are available in your community; why would you save your money in a bank/credit union and not a piggy bank?” (Inspire Financial Learning, “Bank It!”).

Units coded for the theme “Spending Habits”, which explored the distinction between needs and wants, also reflected this difference in approaches. A unit produced by the financial services industry involved the protagonist purchasing cakes and toys at a store instead of bread and milk, only to realize that she cannot eat a cake sandwich (Charly and Max, Get Involved!, “Priority Sandwich”). The distinction between needs and wants is clear and non-negotiable. This approach falsely presumes the same decision-making opportunities are available for all families and students (Blue and Pinto, 2017). In a unit in a resource neither produced nor sponsored by the financial services industry, students are encouraged to categorize needs and wants while creating a “piggy bank” covered in pictures and words that “represent their values and saving goals” (Youth Money Management Presentation, Teacher E-Book). Similarly, in another lesson plan neither produced nor sponsored by the industry, students are first asked to categorize recent family purchases as needs or wants, and then given different scenarios, such as being stranded on a boat or living in different climate environments, and an opportunity to reconsider how their needs and wants would change depending on the situation (Inspire Financial Learning, “Deserted (Needs vs Wants)”). Students are encouraged to consider that their perceptions of needs and wants might differ, and that these might shift depending on their situation. This approach better accounts for the barriers students of varying socio-economic backgrounds might face in trying to build savings or make a budget (Hamilton et al., 2012).

Resources produced by the financial services industry also had the highest percentage of “Hard Work Ethic”. The flash game Money Metropolis was coded with this theme. The game involves the player trying to “save” enough money for a goal they choose at the beginning of the game - usually fun activities, like going to the zoo, or big purchases, like a pet – by doing odd jobs or chores for which they are paid if they complete the task successfully. There is no other way to make money toward achieving the goal and winning the game other than by working through these jobs or chores. Even if the player chooses the least expensive goal, they will likely have to complete ten rounds of jobs or chores to afford their goal. Similarly, resources sponsored by the financial services industry coded with “Hard Work Ethic” also emphasize a direct and singular connection between success and individual work ethic. In “Getting & Earning Money, Grades 4-6” (Building Futures for Manitoba), students are encouraged to read “The Little Red Hen” and “The Three Little Pigs” in order to identify the characters who are “lazy” and “uncooperative”. Students are then directed to identify high-earning professions and discuss how a “strong work ethic” is the primary trait for high-income earners. Meanwhile, in resources neither produced nor sponsored by the financial services industry, units coded for this theme describe the hard work ethic of certain communities or collectives of people in hard times and characterize a hard work ethic as only one of many necessary factors for success. For instance, in M is for Money teaching guides, the author draws on her personal experience as a child of an Italian immigrant family. The author writes:

I learned the value of money at a very young age as I watched my parents work hard to make a new life in Canada [. . .] My parents talked to me about how difficult it was to earn a living, and when faced with competing priorities for their hard-earned money, hard decisions had to be made.

The author recognizes the hard work ethic of others in her community who contributed to her success, as well as the financial insecurity people can face even when they work hard.

Industry-affiliated resources were also more likely to exhibit a moralistic tone by either explicitly or implicitly judging certain financial behaviors as right or wrong. For example, “The Game Plan”, a single-unit resource produced by an Indigenous non-profit organization and sponsored by a financial services company, was one of three units coded for “Good Debt vs Bad Debt”. The comic book’s protagonist falls into “bad debt” through reckless credit card spending on personal items, such as lunches out and sports equipment, while another character thrives because she relies on “good debt”, such as a loan for expanding her small business. The moral of the story is that individuals who get caught in bad debt cycles do so because they indulge in spending on “wants”, rather than by reason of systemic discrimination and colonial structures facing Indigenous individuals and communities in Canada (Blue and Pinto, 2017). This is consistent with the “blame the victim” subtext in financial literacy education materials (Blue and Pinto, 2017; McCormick, 2009; Willis, 2008). The other two units coded for this key theme were neither produced nor sponsored by the financial services industry. One, produced by an individual, had students make a budget for a shopping list so they have enough money for the things they want to buy, and to make a simple loan agreement for a friend who wants to borrow money for lunch (M is for Money, “Teaching Guide for Books 4, 5, and 6”). The other, sponsored by the Ontario Teachers’ Federation, the professional association of Ontario’s public school teachers, helped students distinguish between building credit and going into debt, but avoided applying moralistic labels, with the stated intention to “equi[p] teachers, students, parents and guardians with unbiased, independent and effective tools and strategies to help them navigate the complex world of finances and also support[t] them in making responsible financial choices” (Inspire Financial Learning, home page).

While all three groups had relatively similar percentages of the theme “Money Gives Choice”, in three out of five units coded for this key theme in resources produced by the financial services industry, this theme is connected to choice over one’s apparel or appearance. In the flash game Peter Pig’s Money Counter, players use the money they win playing the game to buy clothing and accessories for Peter Pig. Similarly, in Money Metropolis, players could choose to spend their earnings on buying new clothing, rather than saving it all for their chosen savings goal. As noted above, there is a concern that financial literacy education resources produced by the industry will reinforce “neoliberal approaches, attitudes, and ideologies” about money and spending (Haiven, 2007: 349), specifically consumerism. In non-industry affiliated resources, “Money Gives Choice” was more commonly connected to different ways to treat money, such as saving, spending, donating, or investing it, and how to make that decision. For instance, in “The Money Dilemma” lesson plan, students are encouraged to discuss what to do with a ten-dollar bill they find - whether to spend it or save it, as well as how one earns ten dollars. Although this unit encourages more discussion regarding the uses of money, it does not necessarily challenge currently dominant ideas about money.

Perhaps surprisingly, resources produced by the financial services industry had the highest percentage of units dealing with “Advertising”, which focused on helping students to critically assess advertising techniques, and make choices based on their own best interests, rather than being influenced by advertising or peer pressure. This theme was differentiated from “Getting Value for Money”, in which the lessons focused more on the needs of the buyer, and ascertaining the value of different products to the buyer, rather than the intentions of the seller in trying to persuade consumers to buy their products through advertising. That said, resources neither produced nor sponsored by the industry are the only group with units coded with “Contracts” and “Frauds and Scams”, both of which teach students about consumer protection. In “Lessons for Life - First Mobile Phone”, a lesson plan from Make It Count, students are encouraged to discuss the basic terms of a phone contract as well as the concept of a contract. For instance, students are asked, “What are the different types of mobile phone plans?” and “What does it mean to sign a contract? What promises are you making by signing one? What happens if you don’t hold up your end of the bargain?” The lesson helps students to see how they can save more money by choosing a better phone plan, and to understand the basic legal obligations they undertake in signing a contract. In another lesson plan by Make It Count, “Lessons for Life - Frauds and Scams”, the only unit in the study coded for “Smart Shopper - Frauds and Scams”, students are taught to recognize and avoid different forms of frauds and scams. Students are prompted to research in groups different kinds of frauds and scams, such as online scams, ATM scams, identity theft and investment scams.

Key words

Similar to our findings with respect to the key themes, key words appeared consistently across the three categories of resources, indicating that the content of financial literacy education resources does not vary based on who made or paid for them. However, differences in the frequency of the three categories of key words – financial, normative and curriculum – supports the contextual analysis of key themes that resources produced or sponsored by the industry are more likely to take a prescriptive approach and/or exhibit a moralistic tone.

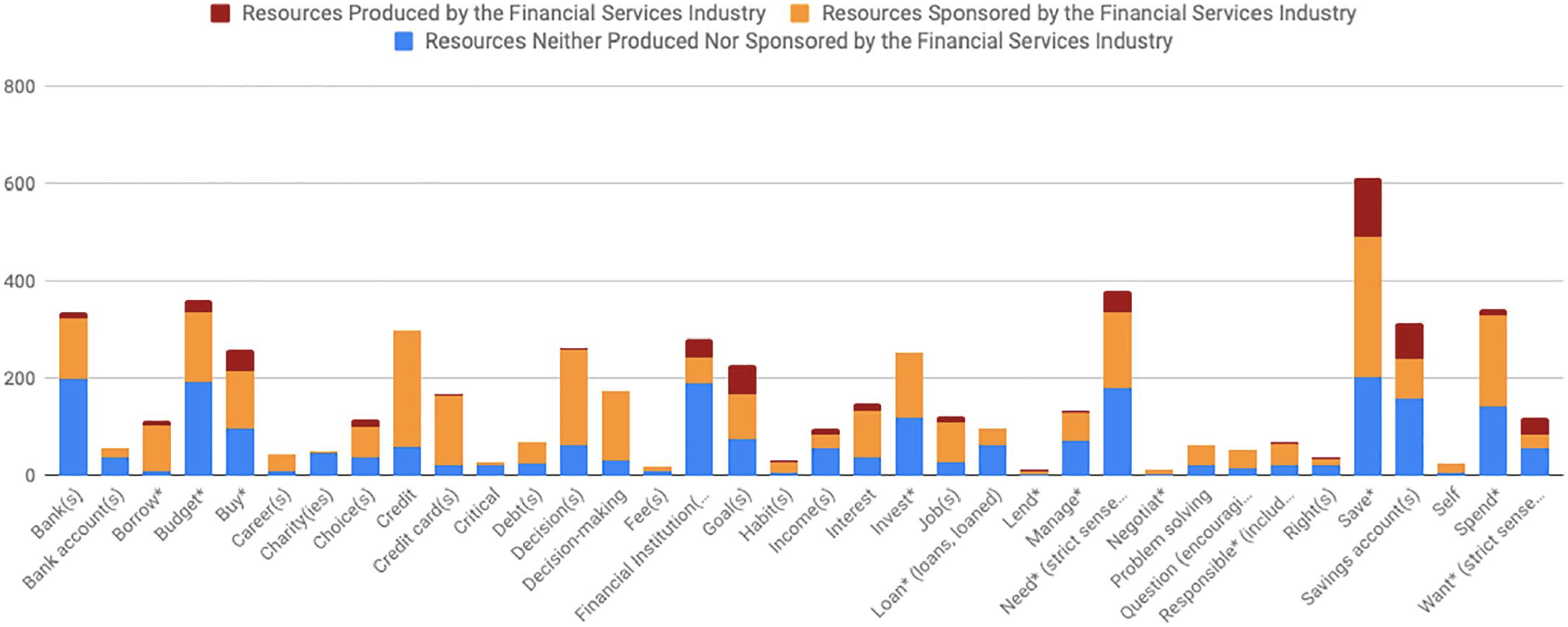

As shown in Figure 2, the most frequently coded key words across all three categories were “save*” (n = 613, 11% of all words identified), “need*” (limited to the context of needs versus wants; n = 380, 7%), and “budget*” (n = 361, 6%). The frequency of these terms reflects the prevalence of financial literacy topics common across resource categories, namely, how to save, how to distinguish needs from wants, and how to create reasonable budgets. “Save*” was the most frequent key word across all three categories of resources. After “save*”, the most frequent key words identified for resources produced by the industry were “savings account(s)” (n = 71, 13% of all words identified in this category) and “goal(s)” (n = 59, 11%), whereas for resources sponsored by the industry they were “credit” (n = 238, 8%) and decision(s) (n = 197, 7%), and for neither produced nor sponsored by the industry they were “bank(s)” (n = 200, 9%) and “budget*” (n = 192, 8%). Among the most frequent key words coded in all three categories, therefore, are words related to the use of financial products (i.e., “savings accounts”, “credit” and “banks”).

Word frequency (number) of each resource category.

In resources produced by the industry, nine key words were not identified at all: “bank account(s)”, “career(s)”, “charity(ies)”, “credit”, “critical”, “debt(s)”, “fee(s)”, “negotiate*”, and “self”. The omission of some of these key words, such as “critical”, “negotiate*” and “self” may suggest industry-affiliated resources focus less on helping students to develop a critical awareness of financial norms, services and products. The absence of “credit” and “debt(s)” is interesting, suggesting perhaps the industry resources reviewed chose not to discuss more complex money management relationships. The word “financial institution(s)” was identified more than “bank(s)”; this is likely due to the fact that financial institution is the legal term for the regulated entity and so likely reflective of how the industry describes itself in day-to-day corporate communications. The key words “financial institution(s)” and “bank(s)” appeared a combined total of 52 times, and thus together were the fourth-most frequently coded key word.

In resources sponsored by the industry, the words “self”, “negotiate*”, “interest”, “job”, and “career” appear most frequently as compared to the other resource groups. Furthermore, 80% of entries for the word “credit” were found in resources sponsored by the industry; 75% of entries for “decision(s)” were also found in this resource group. The marked difference in key word results between resources created by the industry and resources sponsored by the industry may reflect the influence from having a non-industry partner involved in the creation of the resources.

In resources neither produced nor sponsored by the industry, the words “bank” and “financial institution” appear most frequently compared to the other resource groups. As noted above, one of the difficulties in examining the question of conflicts of interest in financial literacy education resources is that one of the goals of financial literacy education generally is to increase the uptake of certain mainstream financial products, such as savings accounts.

In terms of categories of key words, “financial” words appear most frequently in resources neither produced nor sponsored by the financial services industry, whereas the highest concentration of “normative” key words was found in resources produced by the industry. This finding may reflect the differences in tone of messaging between non-industry resources as compared to industry resources noted above with respect to key themes, and suggests that even if the substantive topics are similar across resources, the terms and methods which are employed to discuss these topics is likely to vary based on who made or paid for the resource.

Study limitations

Our study focuses on the content, or the “what” of financial literacy education resources, and whether this content varies based on who made or paid for them. We do not address here more fundamental challenges to financial literacy education and its role in reinforcing pre-existing economic inequalities. We also do not examine the extent to which these resources have been made out of date by technological innovations and new financial products, such as cryptocurrencies and mobile phone payment and savings apps.

With respect to our findings regarding content, one limitation of the study is that only resources aimed at elementary school aged children and their teachers were analyzed. Key themes might differ at the secondary or adult education levels, revealing greater differences in content among categories of resources. A second limitation is that we analyzed only resources included in the Canadian Financial Literacy Database. While this provided a wide sample of the types of online resources available to teachers, it is not necessarily a representative sample of resources, and therefore our findings need to be interpreted with caution. Furthermore, online resources are not the only ways that financial services companies contribute to curricula. One area of future research would be to look beyond online resources to content being delivered in classrooms, for example, by guest speakers from the industry (Henderson, 2020).

Conclusion

Our results indicate that the content of financial literacy education resources does not vary based on who made or paid for them. Frequency and concentration of key themes and key words were consistent across the three categories of resources. “Spending habits” was the most frequent theme across all groups. While “Understanding Financial Products” was coded more frequently in units of resources produced by the industry, it was also frequently coded for in units from the other two groups. “Save” and its variants was the most frequently identified key word in all three groups.

While “savings account” was the second most frequently coded-for key word in resources produced by the industry, “banks” was the most frequently coded-for key word in resources neither produced nor sponsored by the industry. Since banks are only one type of financial institution available to financial consumers in most jurisdictions, it seems likely that teachers who want to inform their students of other institutional options when it comes to saving and investing will need to rely on their own financial knowledge. In Canada, while national or regional credit unions, such as Desjardins, have the resources to produce or sponsor financial literacy materials for inclusion in the CFLD, small, local credit unions, which are another savings option, likely do not. Hopefully, resources created or sponsored by government departments or agencies can step in to fill this gap. Financial literacy resources should also recognize and discuss community or collective savings practices, which take place independent of financial institutions, such as saving circles. Again, for now, teachers interested in diversifying their lessons in this way will have to search even further afield for materials.

One difference in frequency of key theme was Frauds and Scams. This key theme was coded for only in resources neither produced nor sponsored by the industry. This very low frequency even in this category may be a result of educators thinking this is too advanced for elementary school students, rather than as a result of who made or paid for the resource. Avoiding fraud is a central goal of Canada’s financial literacy strategy, however (FCAC, 2015). The omission of materials addressing this theme from industry-affiliated resources places the onus on teachers who rely on these resources to look elsewhere for credible information regarding frauds and scams to bring into their financial literacy lesson planning. In Canada, resources on frauds and scams are available from provincial securities commissions, which are regulatory agencies, but they are generally aimed at adults, rather than children. The Government of Ontario has called on the Ontario Securities Commission to collaborate with the Ontario Ministry of Education “to enhance the financial literacy curriculum” (Government of Ontario, 2019: 229). This collaboration may increase the materials available on avoiding frauds and scams in this jurisdiction.

Although key themes and words are consistent across categories, a closer analysis of the context in which the key themes were found indicates that resources produced or sponsored by the financial services industry are more likely to take a prescriptive approach and exhibit a moralistic tone than resources neither produced nor sponsored by the industry. This is evidenced in differences in how the key themes are reflected in the units reviewed, as explained in the examples above. Also, “financial” key words were more likely to appear in resources that are neither produced nor sponsored by the financial services industry than the other two categories, whereas “normative” key words were least likely to be coded for in this category. Discussions of financial literacy education in initial teacher education programs as well as teacher professional development should consider the industry affiliation of resources and be alive to the differences in tone.

National and sub-national financial literacy strategies in several jurisdictions encourage ministries of education, school boards and teachers to rely on financial literacy education resources produced or sponsored by the financial services industry (OECD, 2013). One concern with this approach is that these resources may be biased in favor of the industry’s interests over those of students. This study is a first step to attempt to measure empirically this potential conflict of interest by comparing key themes and key words in industry-affiliated and non-industry affiliated resources. Our results suggest that the content does not vary based on who made or paid for the resource, although industry-affiliated resources are more likely to exhibit a moralistic tone and to place greater emphasis on individual responsibility over systemic economic inequalities, which may not be appropriate, particularly for students whose families’ socio-economic circumstances may make it harder for them to engage in the financial behaviors promoted by these resources, such as accumulating savings and avoiding debt. More study of this question is desirable, given the ongoing government emphasis on incorporating financial literacy education into mandatory school curricula. Perhaps more importantly, both the key themes identified and consistency across resources, regardless of who made or paid for them, highlight the lack of diversity in existing financial literacy education materials and the dominance of the conventional approach, with its focus on individual responsibility. School boards that want to take an approach to financial literacy education that better accounts for the socioeconomic and cultural diversity of their students would be advised to develop their own financial literacy education materials.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Social Sciences and Humanities Research Council of Canada